chapter 6 - week 10

TRANSCRIPT

Chapter 6-1

Quiz 3 – 5 % - Chapter 5 & 6Quiz 3 – 5 % - Chapter 5 & 6

Class Assignment – 5% - Chapter 6Class Assignment – 5% - Chapter 6

Week 11 – 6/12/2010

Chapter 6-2

Reporting and Analyzing Inventory

Accounting, Third Edition

Chapter 6-3

1. Describe the steps in determining inventory quantities.

2. Explain the basis of accounting for inventories and apply the inventory cost flow methods under a periodic inventory system.

3. Explain the financial statement and tax effects of each of the inventory cost flow assumptions.

4. Explain the lower-of-cost-or-market basis of accounting for inventories.

5. Compute and interpret the inventory turnover ratio.

6. Describe the LIFO reserve and explain its importance for comparing results of different companies.

7. Apply the inventory cost flow methods to perpetual inventory records.

8. Indicate the effects of inventory errors on the financial statements.

Study ObjectivesStudy ObjectivesStudy ObjectivesStudy Objectives

Chapter 6-4

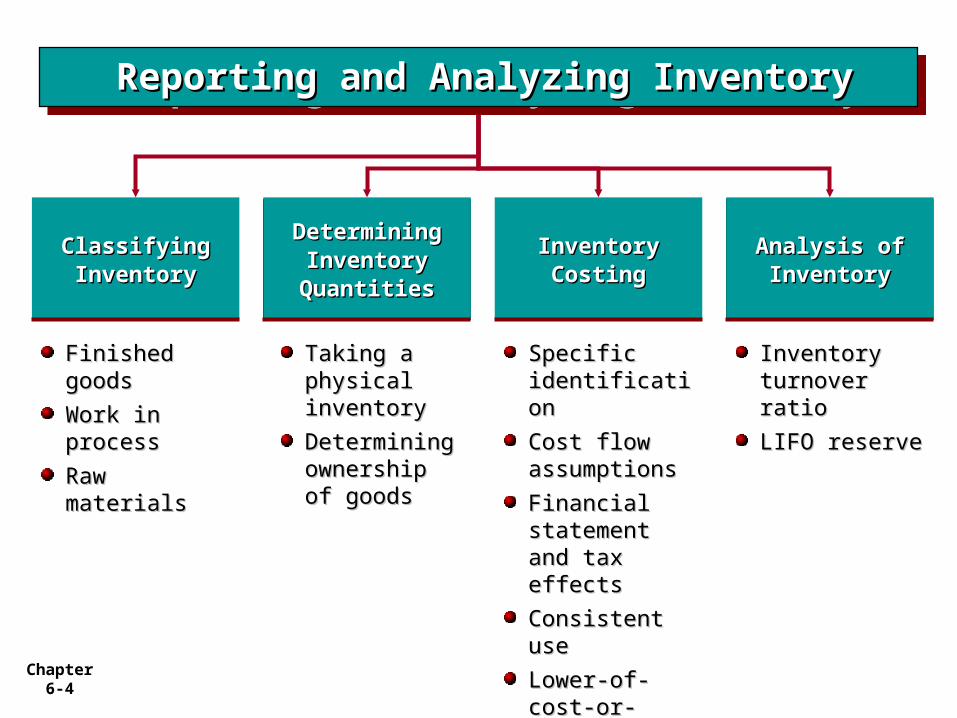

Classifying Classifying InventoryInventory

Classifying Classifying InventoryInventory

Finished goodsFinished goods

Work in processWork in process

Raw materialsRaw materials

Inventory Inventory turnover ratioturnover ratio

LIFO reserveLIFO reserve

Specific Specific identificationidentification

Cost flow Cost flow assumptionsassumptions

Financial Financial statement and statement and tax effectstax effects

Consistent useConsistent use

Lower-of-cost-Lower-of-cost-or-marketor-market

Taking a Taking a physical physical inventoryinventory

Determining Determining ownership of ownership of goodsgoods

Determining Determining Inventory Inventory QuantitiesQuantities

Determining Determining Inventory Inventory QuantitiesQuantities

Inventory Inventory CostingCosting

Inventory Inventory CostingCosting

Analysis of Analysis of InventoryInventory

Analysis of Analysis of InventoryInventory

Reporting and Analyzing InventoryReporting and Analyzing InventoryReporting and Analyzing InventoryReporting and Analyzing Inventory

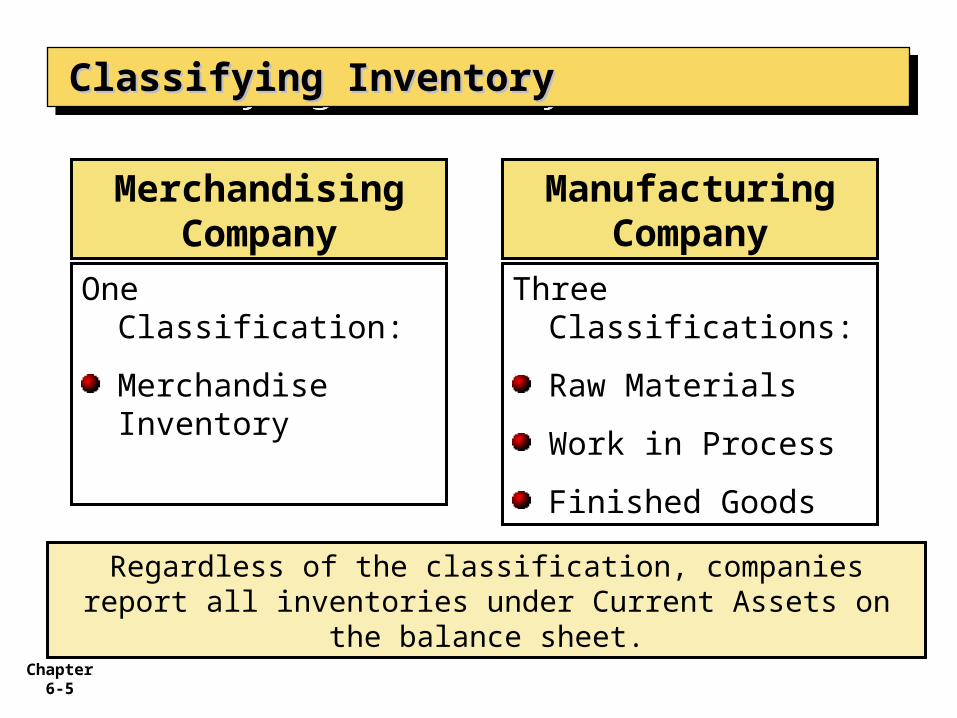

Chapter 6-5

Classifying InventoryClassifying InventoryClassifying InventoryClassifying Inventory

One Classification:

Merchandise Inventory

Three Classifications:

Raw Materials

Work in Process

Finished Goods

Merchandising Company

Manufacturing Company

Regardless of the classification, companies report all inventories under Current Assets on the balance sheet.

Chapter 6-6

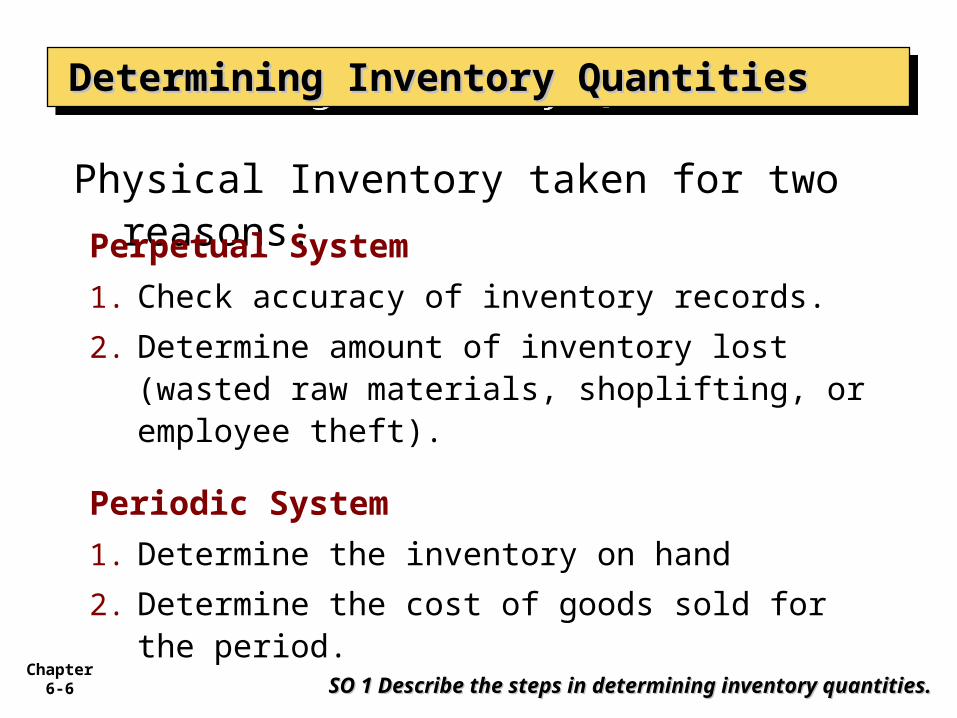

Physical Inventory taken for two reasons:Perpetual System

1. Check accuracy of inventory records.

2. Determine amount of inventory lost (wasted raw materials, shoplifting, or employee theft).

Periodic System

1. Determine the inventory on hand

2. Determine the cost of goods sold for the period.

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Chapter 6-7

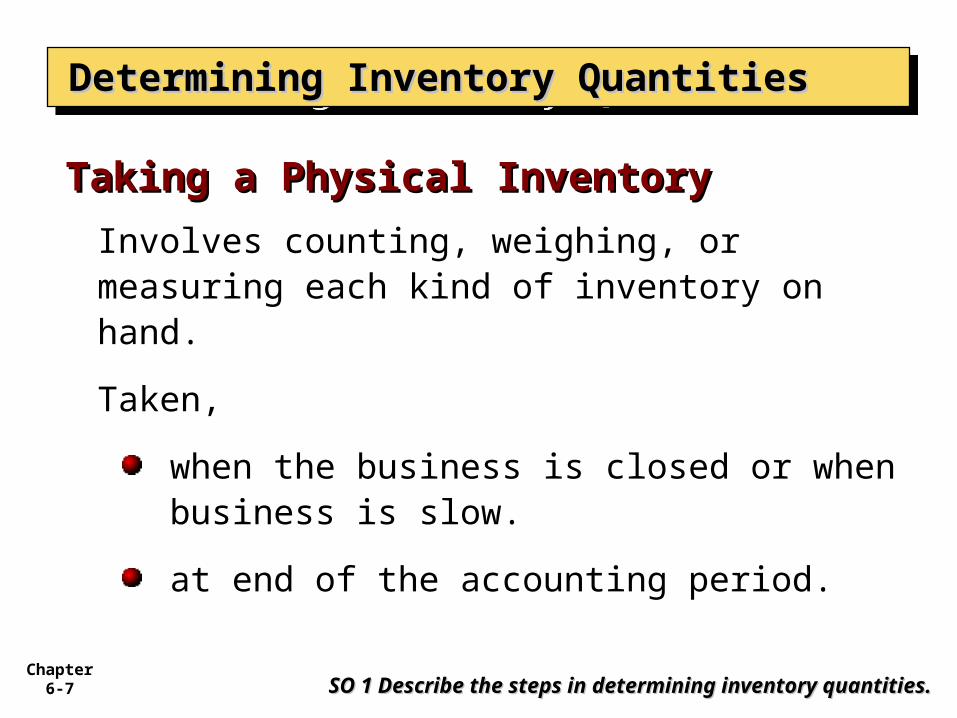

Involves counting, weighing, or measuring each kind of inventory on hand.

Taken,

when the business is closed or when business is slow.

at end of the accounting period.

Taking a Physical InventoryTaking a Physical Inventory

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Chapter 6-8

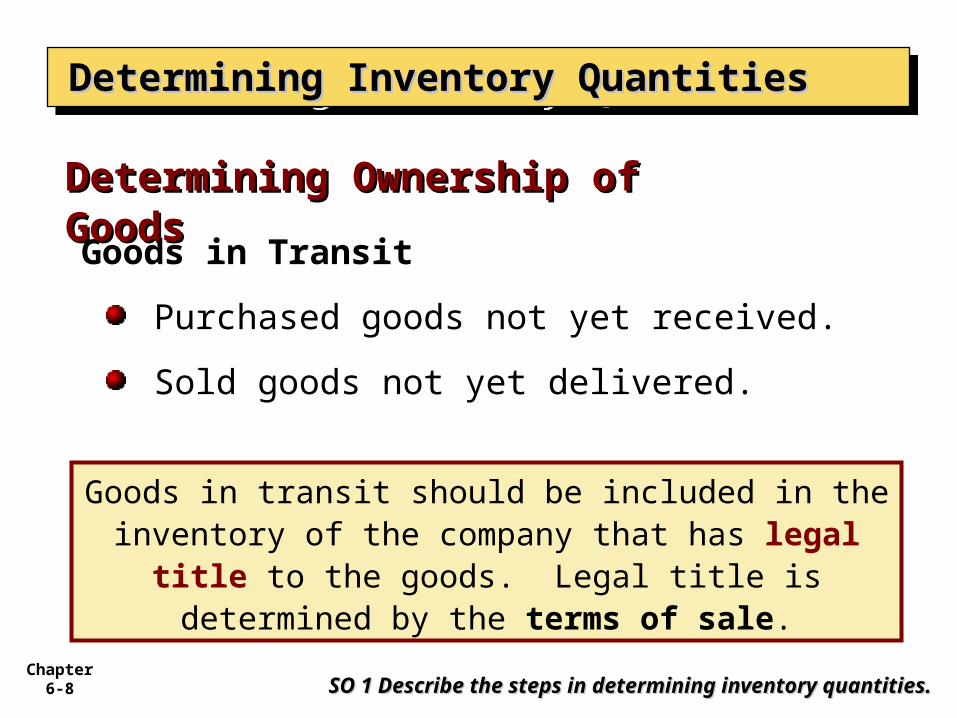

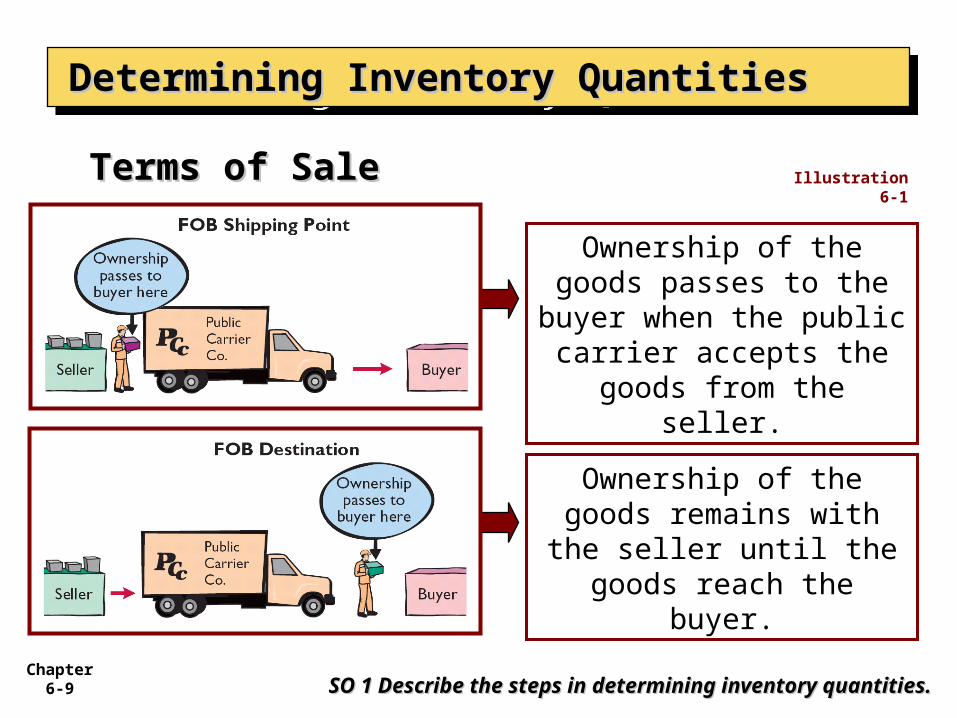

Goods in Transit

Purchased goods not yet received.

Sold goods not yet delivered.

Determining Ownership of Determining Ownership of GoodsGoods

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Goods in transit should be included in the inventory of the company that has legal title to

the goods. Legal title is determined by the terms of sale.

Chapter 6-9

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Illustration 6-1

Ownership of the goods passes to the buyer

when the public carrier accepts the goods from

the seller.

Ownership of the goods remains with the seller

until the goods reach the buyer.

Terms of SaleTerms of Sale

Chapter 6-10

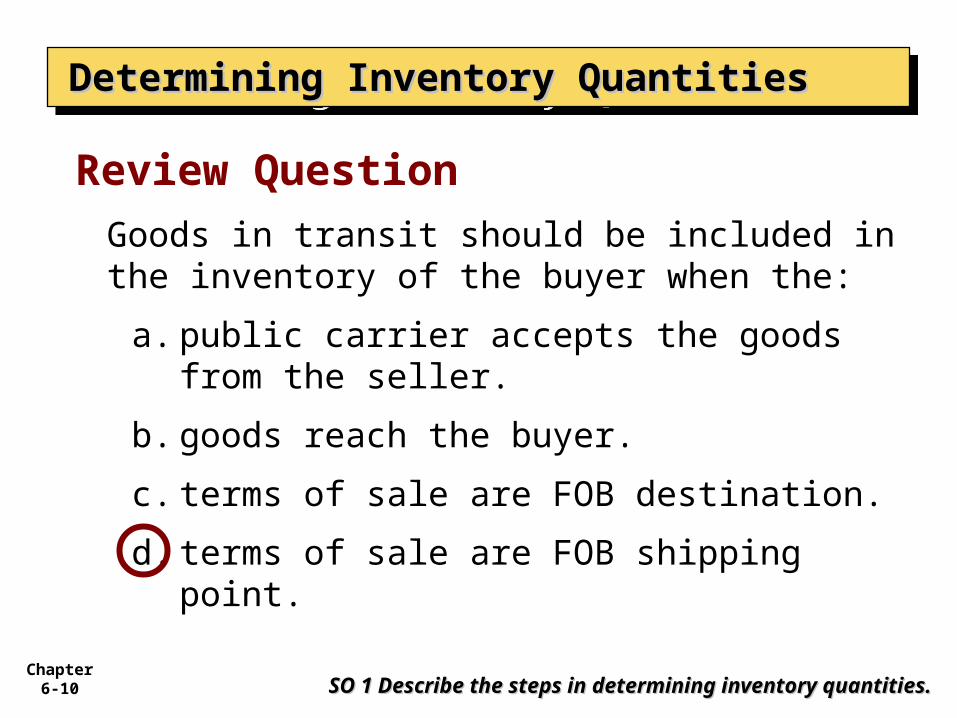

Goods in transit should be included in the inventory of the buyer when the:

a. public carrier accepts the goods from the seller.

b. goods reach the buyer.

c. terms of sale are FOB destination.

d. terms of sale are FOB shipping point.

Review Question

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Chapter 6-11

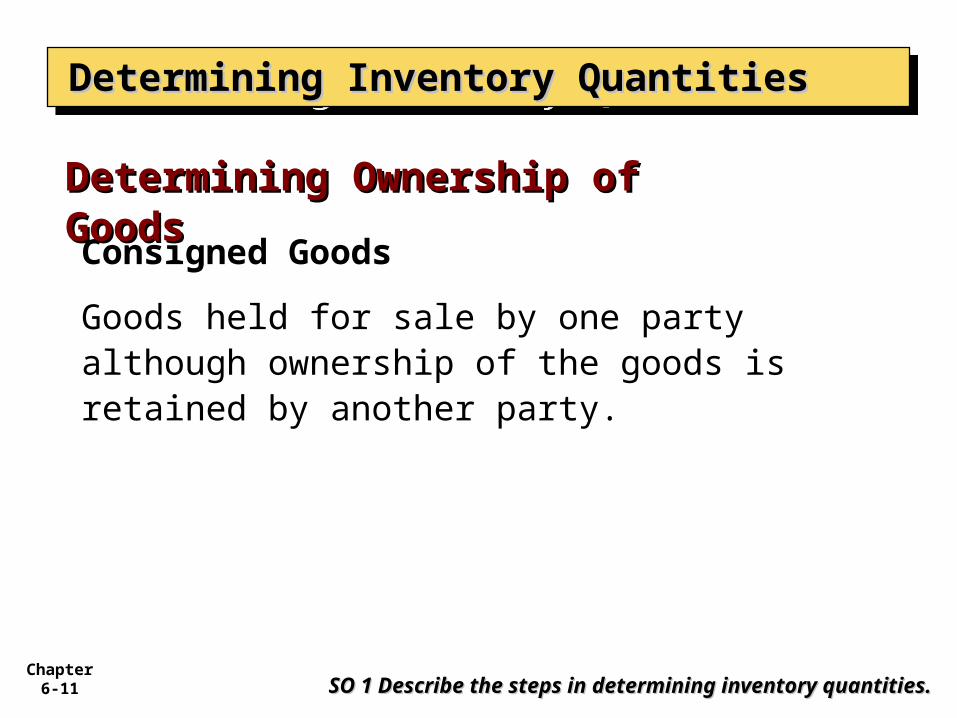

Consigned Goods

Goods held for sale by one party although ownership of the goods is retained by another party.

Determining Ownership of Determining Ownership of GoodsGoods

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

SO 1 Describe the steps in determining inventory quantities.SO 1 Describe the steps in determining inventory quantities.

Chapter 6-12

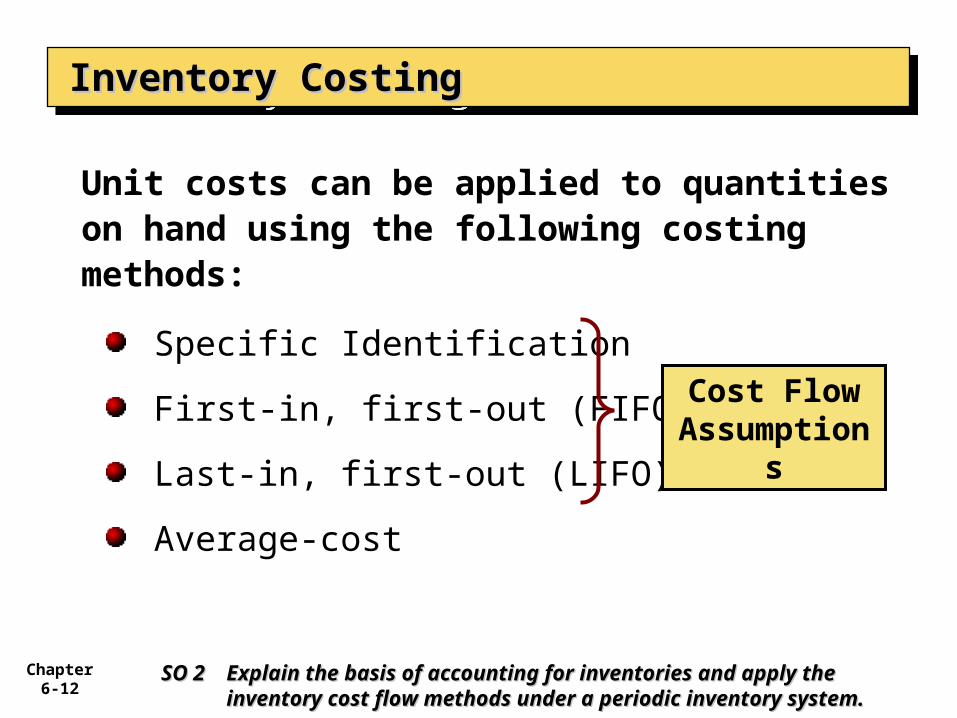

Unit costs can be applied to quantities on hand using the following costing methods:

Specific Identification

First-in, first-out (FIFO)

Last-in, first-out (LIFO)

Average-cost

Inventory CostingInventory CostingInventory CostingInventory Costing

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Cost Flow Assumptio

ns

Chapter 6-13

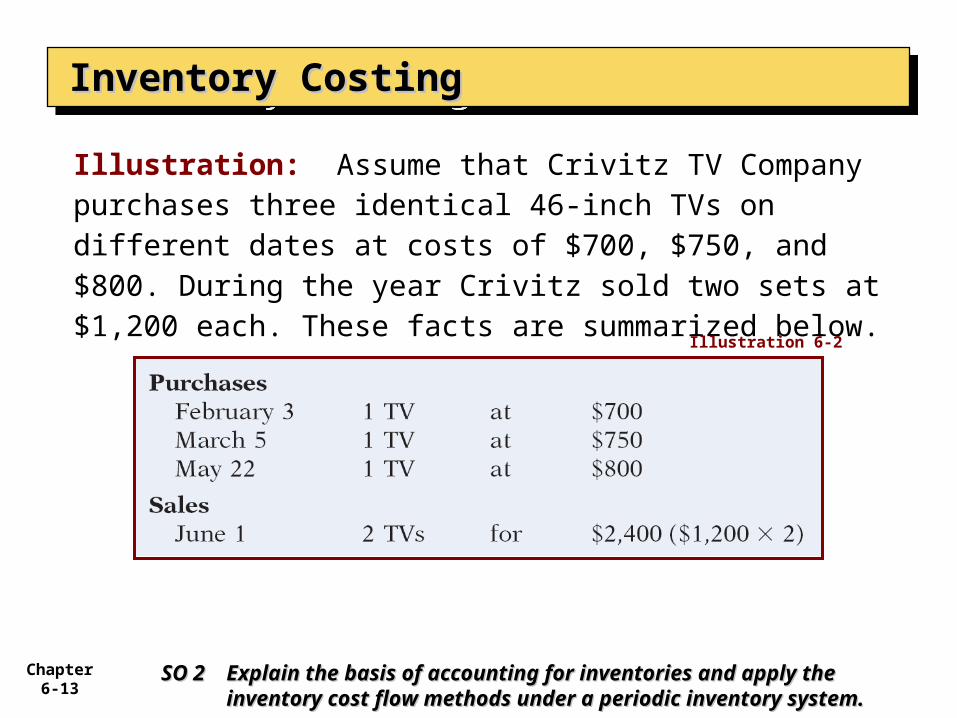

Illustration: Assume that Crivitz TV Company purchases three identical 46-inch TVs on different dates at costs of $700, $750, and $800. During the year Crivitz sold two sets at $1,200 each. These facts are summarized below.

Inventory CostingInventory CostingInventory CostingInventory Costing

Illustration 6-2

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-14

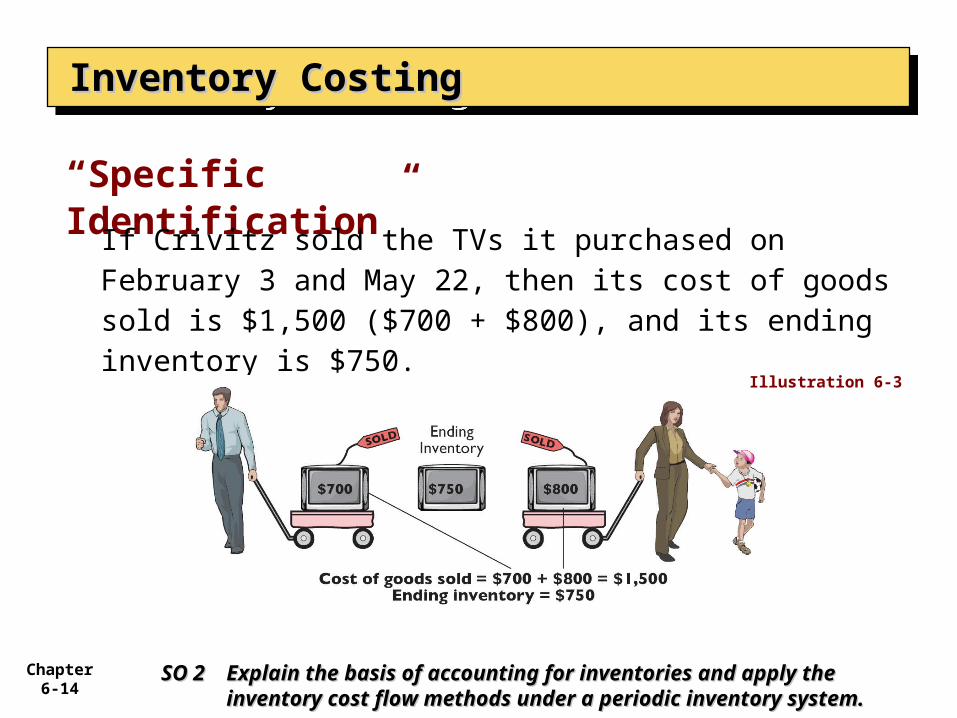

“Specific Identification”

Inventory CostingInventory CostingInventory CostingInventory Costing

If Crivitz sold the TVs it purchased on February 3 and May 22, then its cost of goods sold is $1,500 ($700 + $800), and its ending inventory is $750.

Illustration 6-3

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-15

An actual physical flow costing method in which items still in inventory are specifically costed to arrive at the total cost of the ending inventory.

Practice is relatively rare.

Most companies make assumptions (Cost Flow Assumptions) about which units were sold.

Specific Identification MethodSpecific Identification Method

Inventory CostingInventory CostingInventory CostingInventory Costing

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-16

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

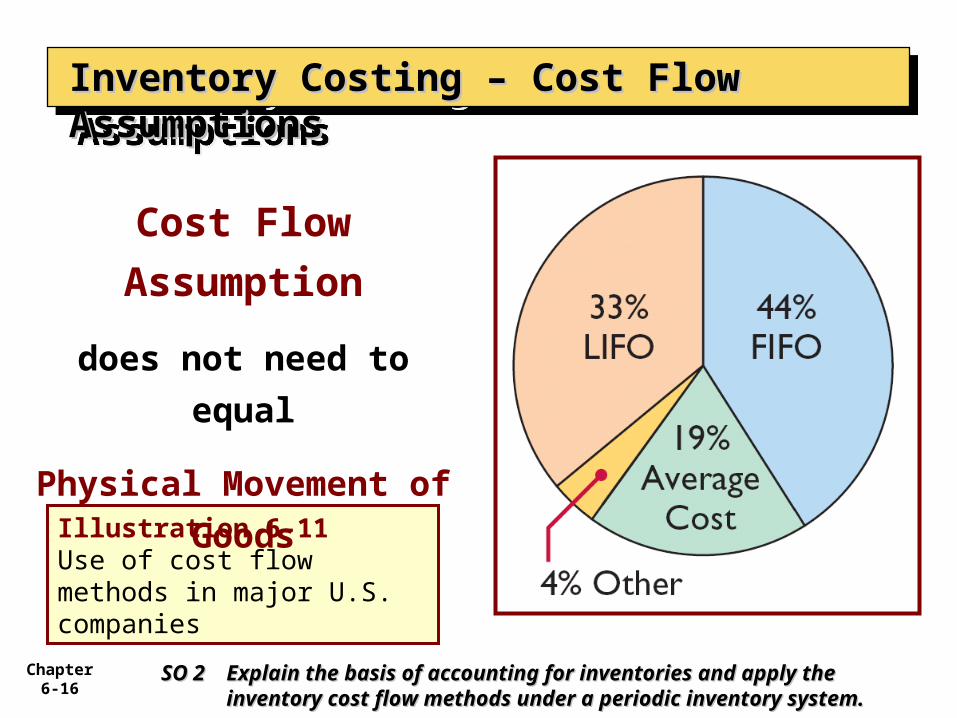

Illustration 6-11Use of cost flow methods in major U.S. companies

Cost Flow

Assumption

does not need to

equal

Physical Movement

of Goods

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-17

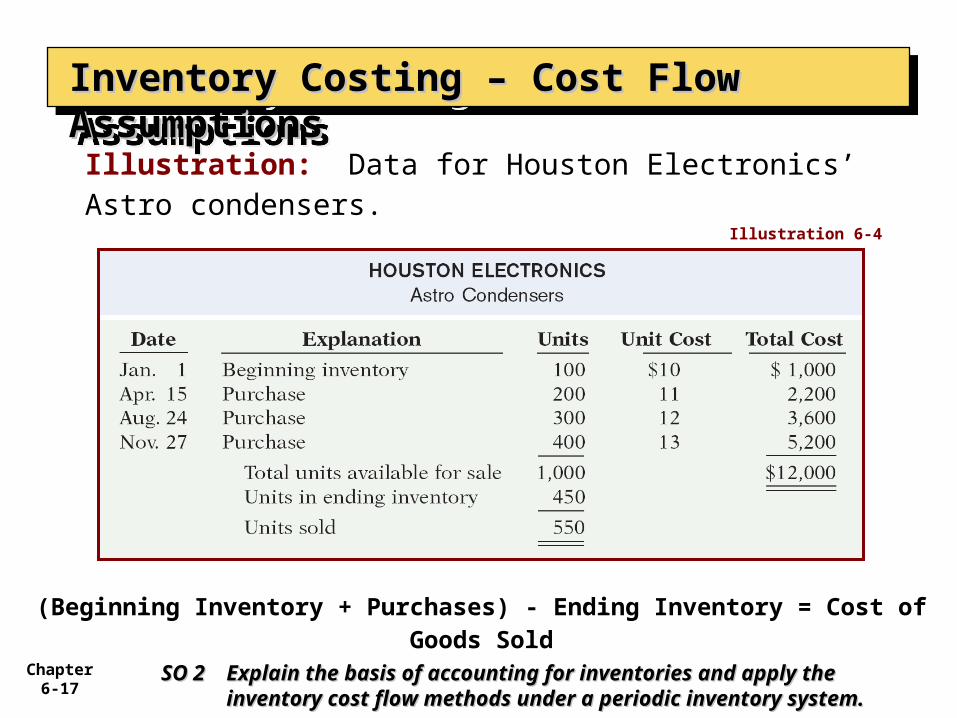

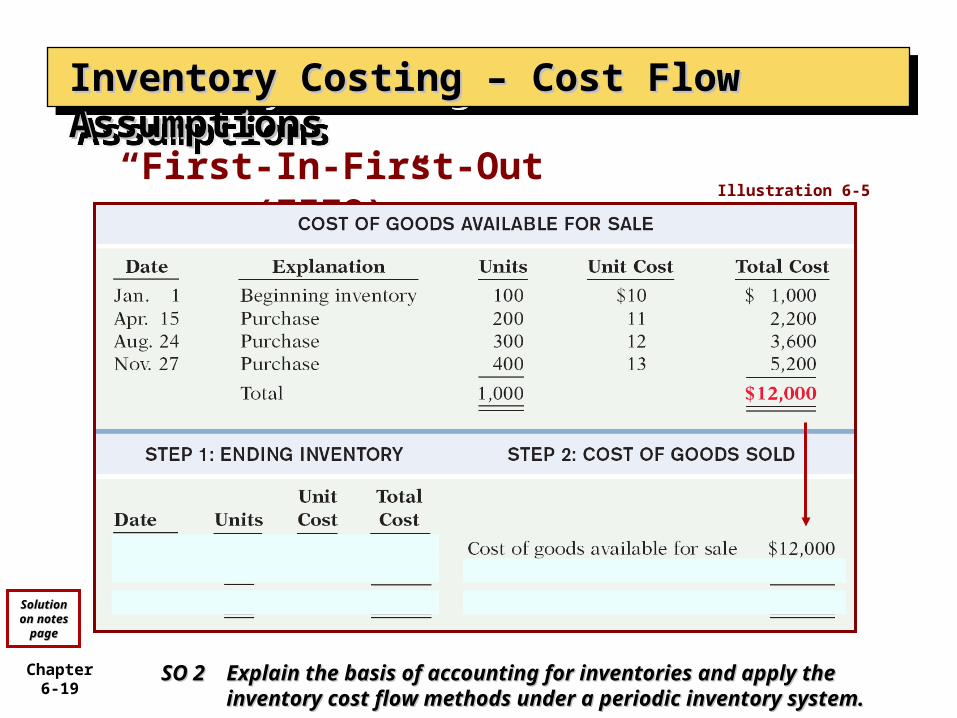

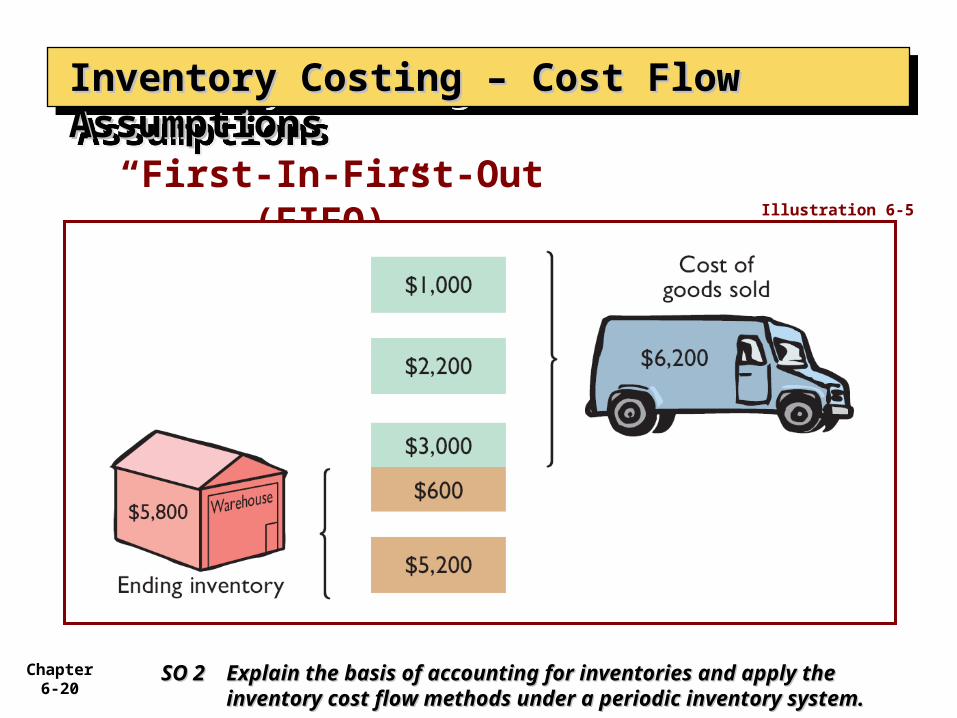

Illustration: Data for Houston Electronics’ Astro condensers.

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-4

(Beginning Inventory + Purchases) - Ending Inventory = Cost of Goods Sold

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-18

Earliest goods purchased are first to be sold.

Often parallels actual physical flow of merchandise.

Generally good business practice to sell oldest units first.

““First-In-First-Out (FIFO)”First-In-First-Out (FIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-19

“First-In-First-Out (FIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-5

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

SolutioSolution on n on

notes notes pagepage

Chapter 6-20

“First-In-First-Out (FIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-5

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-21

Latest goods purchased are first to be sold.

Seldom coincides with actual physical flow of merchandise.

Exceptions include goods stored in piles, such as coal or hay.

““Last-In-First-Out (LIFO)”Last-In-First-Out (LIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-22

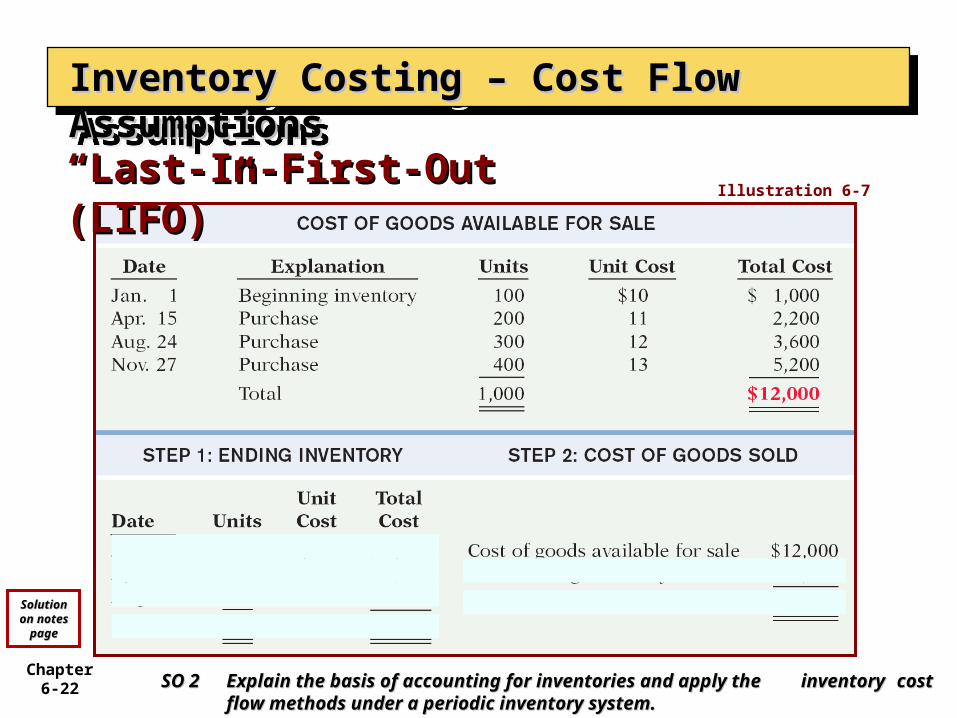

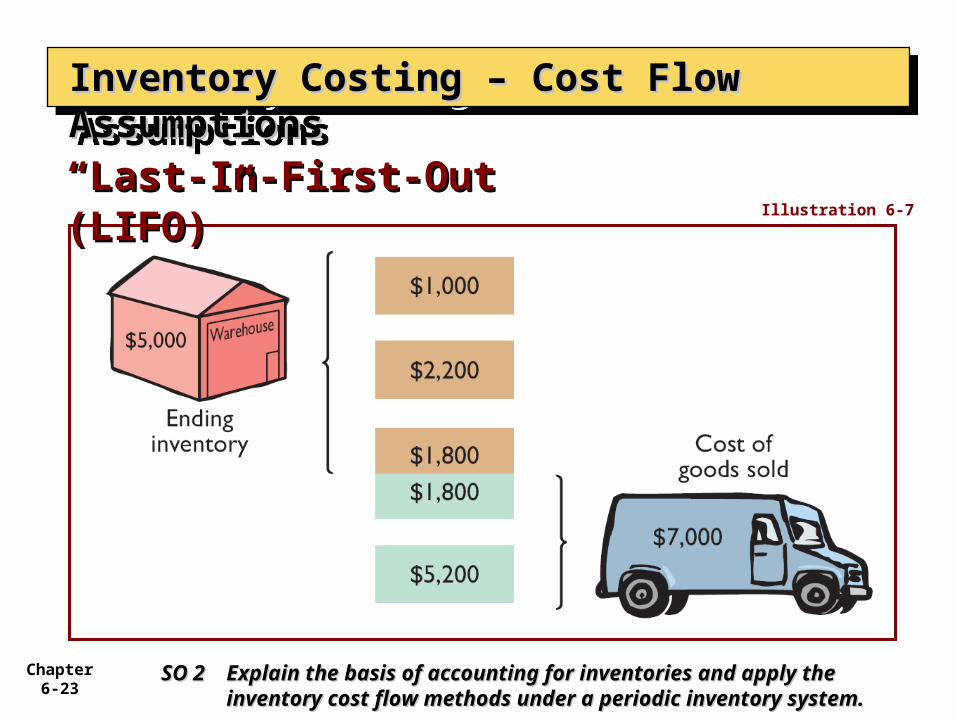

““Last-In-First-Out Last-In-First-Out (LIFO)”(LIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-7

SO 2 SO 2 Explain the basis of accounting for inventories and apply the Explain the basis of accounting for inventories and apply the inventory inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.system.

SolutioSolution on n on

notes notes pagepage

Chapter 6-23

““Last-In-First-Out (LIFO)”Last-In-First-Out (LIFO)”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-7

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-24

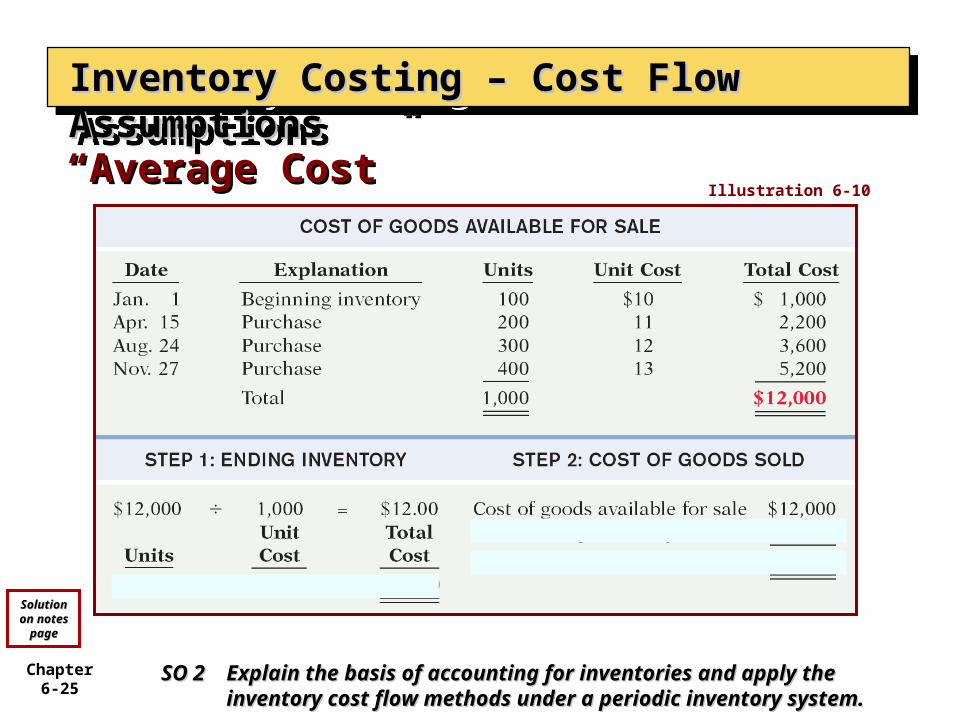

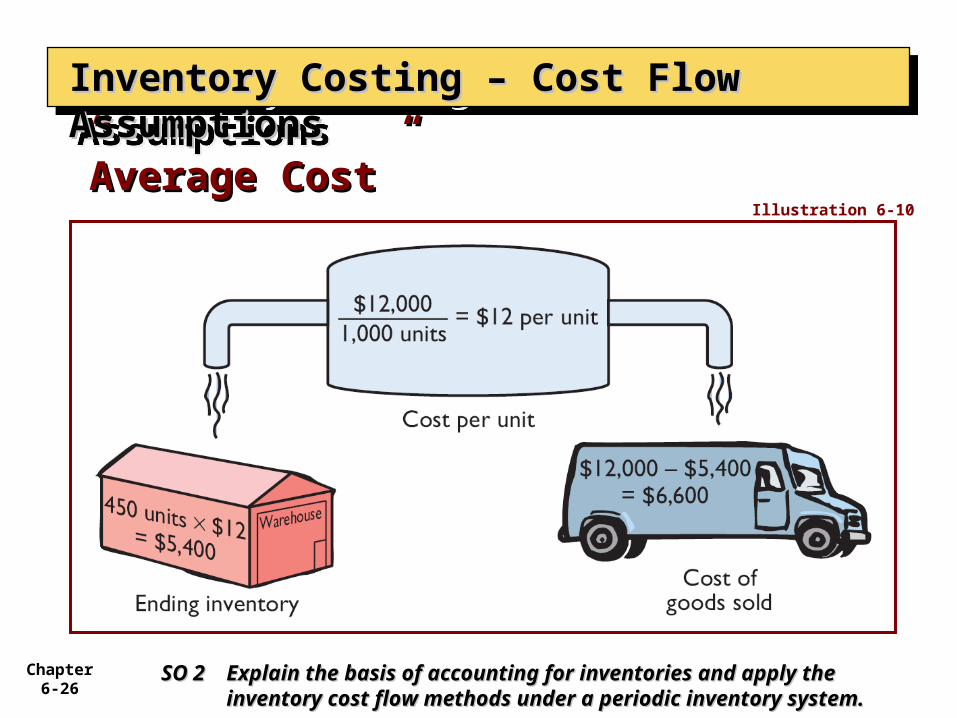

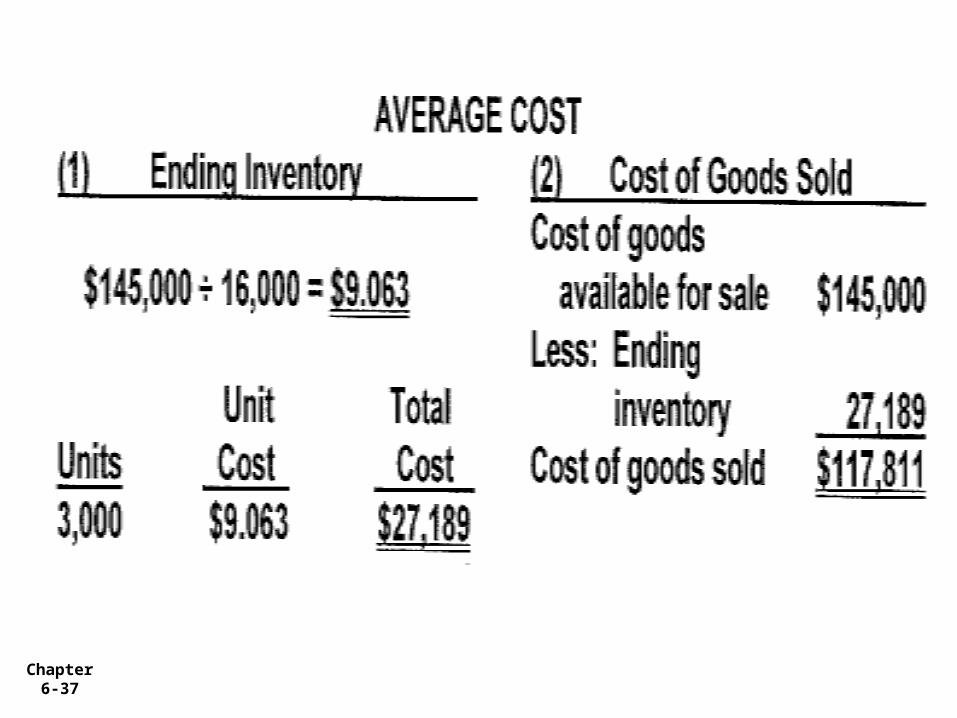

Allocates cost of goods available for sale on the basis of weighted average unit cost incurred.

Assumes goods are similar in nature.

Applies weighted average unit cost to the units on hand to determine cost of the ending inventory.

““Average Cost”Average Cost”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-25

““Average Cost”Average Cost”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-10

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

SolutioSolution on n on

notes notes pagepage

Chapter 6-26

””Average Cost”Average Cost”

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Illustration 6-10

SO 2 SO 2 Explain the basis of accounting for inventories and apply Explain the basis of accounting for inventories and apply the the inventory cost flow methods under a periodic inventory cost flow methods under a periodic inventory system.inventory system.

Chapter 6-27

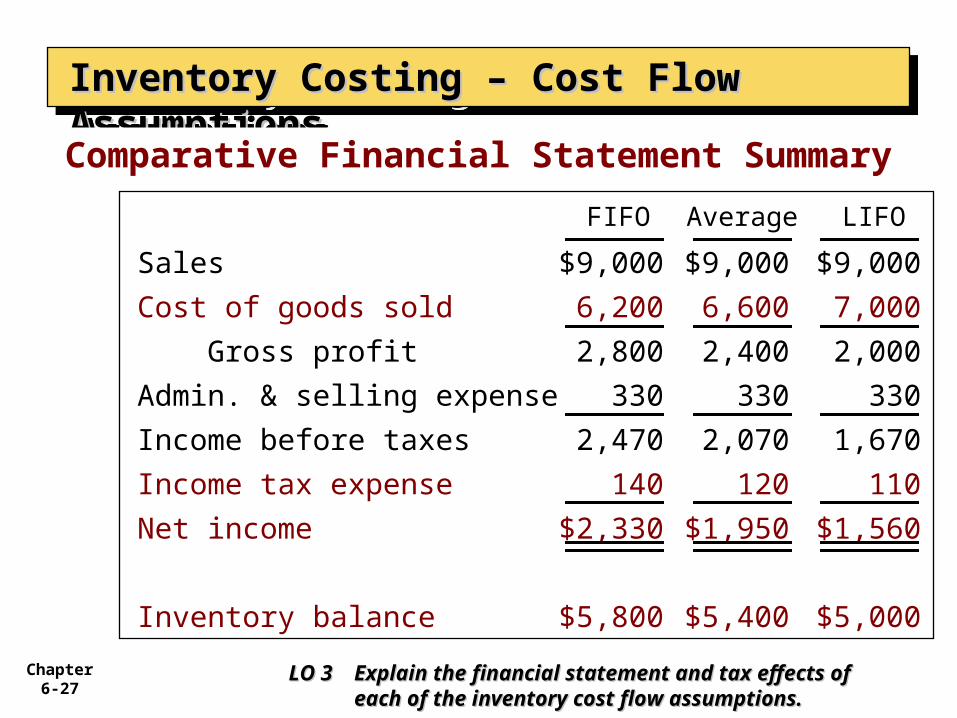

FIFO

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Sales $9,000 $9,000 $9,000

Cost of goods sold 6,200 6,600 7,000

Gross profit 2,800 2,400 2,000

Admin. & selling expense 330 330 330

Income before taxes 2,470 2,070 1,670

Income tax expense 140 120 110

Net income $2,330 $1,950 $1,560

Inventory balance $5,800 $5,400 $5,000

LIFOAverage

Comparative Financial Statement Summary

Chapter 6-28

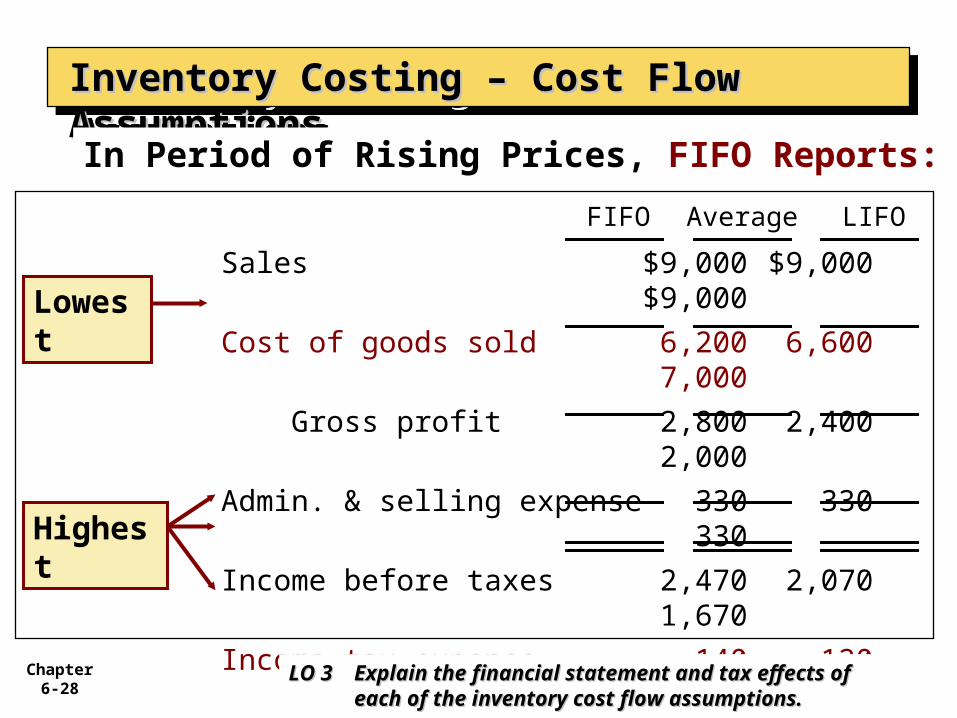

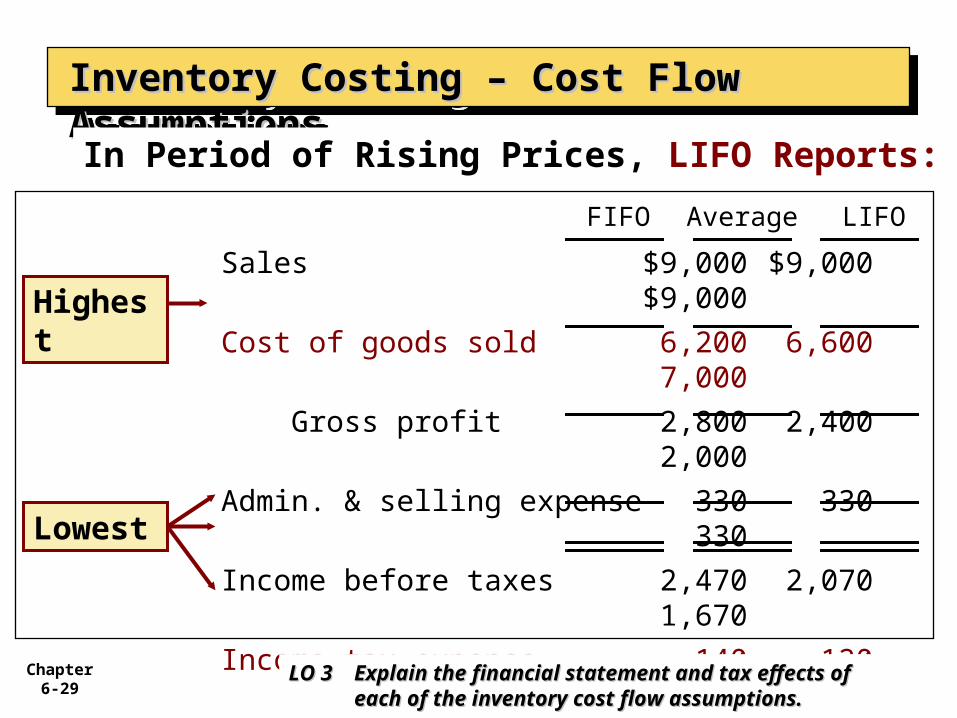

FIFO

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Sales $9,000 $9,000$9,000

Cost of goods sold 6,200 6,6007,000

Gross profit 2,800 2,4002,000

Admin. & selling expense 330 330330

Income before taxes 2,470 2,0701,670

Income tax expense 140 120110

Net income $2,330 $1,950$1,560

Inventory balance $5,800 $5,400$5,000

LIFOAverage

In Period of Rising Prices, FIFO Reports:

Highest

Lowest

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Chapter 6-29

FIFO

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

Sales $9,000 $9,000$9,000

Cost of goods sold 6,200 6,6007,000

Gross profit 2,800 2,4002,000

Admin. & selling expense 330 330330

Income before taxes 2,470 2,0701,670

Income tax expense 140 120110

Net income $2,330 $1,950$1,560

Inventory balance $5,800 $5,400$5,000

LIFOAverage

In Period of Rising Prices, LIFO Reports:

Lowest

Highest

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Chapter 6-30

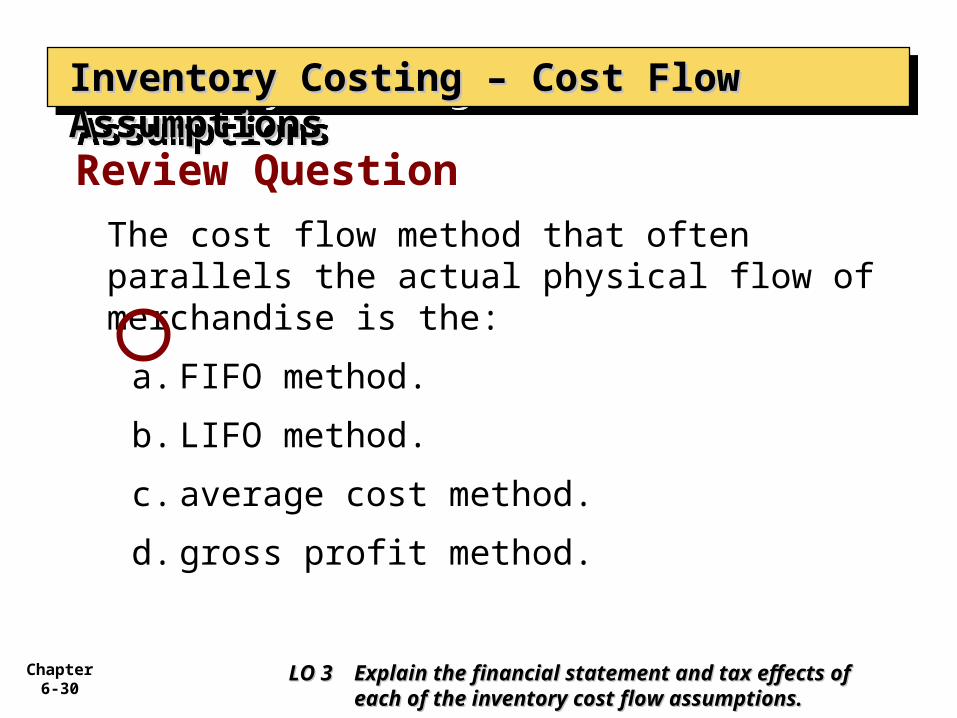

The cost flow method that often parallels the actual physical flow of merchandise is the:

a. FIFO method.

b. LIFO method.

c. average cost method.

d. gross profit method.

Review Question

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Chapter 6-31

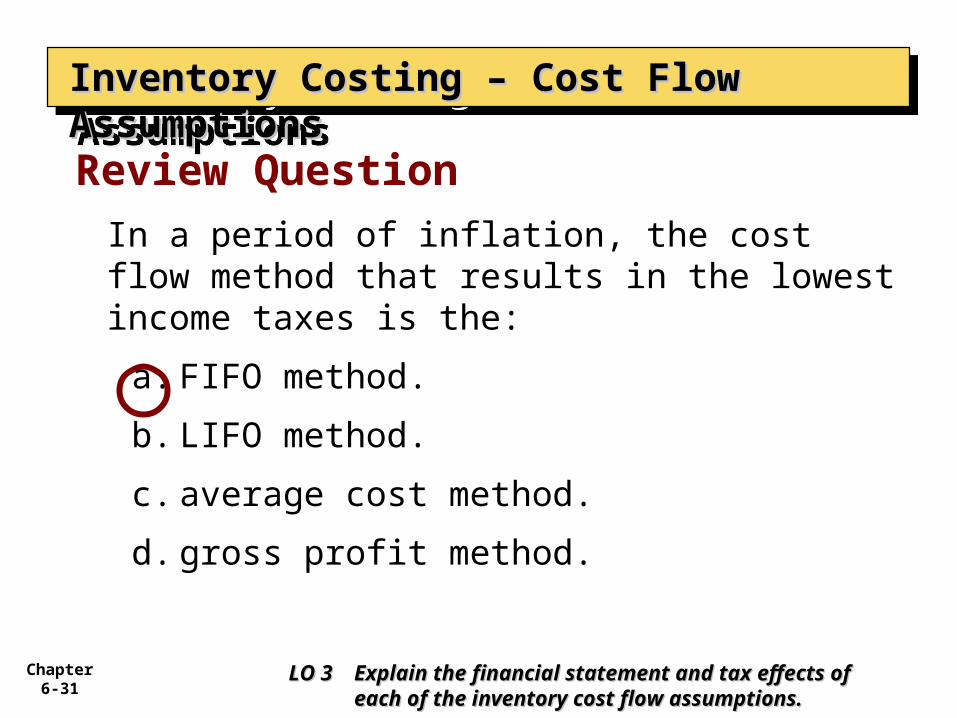

In a period of inflation, the cost flow method that results in the lowest income taxes is the:

a. FIFO method.

b. LIFO method.

c. average cost method.

d. gross profit method.

Review Question

Inventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow AssumptionsInventory Costing – Cost Flow Assumptions

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Chapter 6-32

Using Cost Flow Methods Using Cost Flow Methods ConsistentlyConsistently

Inventory CostingInventory CostingInventory CostingInventory Costing

Method should be used consistently, enhances comparability.

Although consistency is preferred, a company may change its inventory costing method.

LO 3 LO 3 Explain the financial statement and tax effects Explain the financial statement and tax effects of of each of the inventory cost flow each of the inventory cost flow assumptions.assumptions.

Chapter 6-33

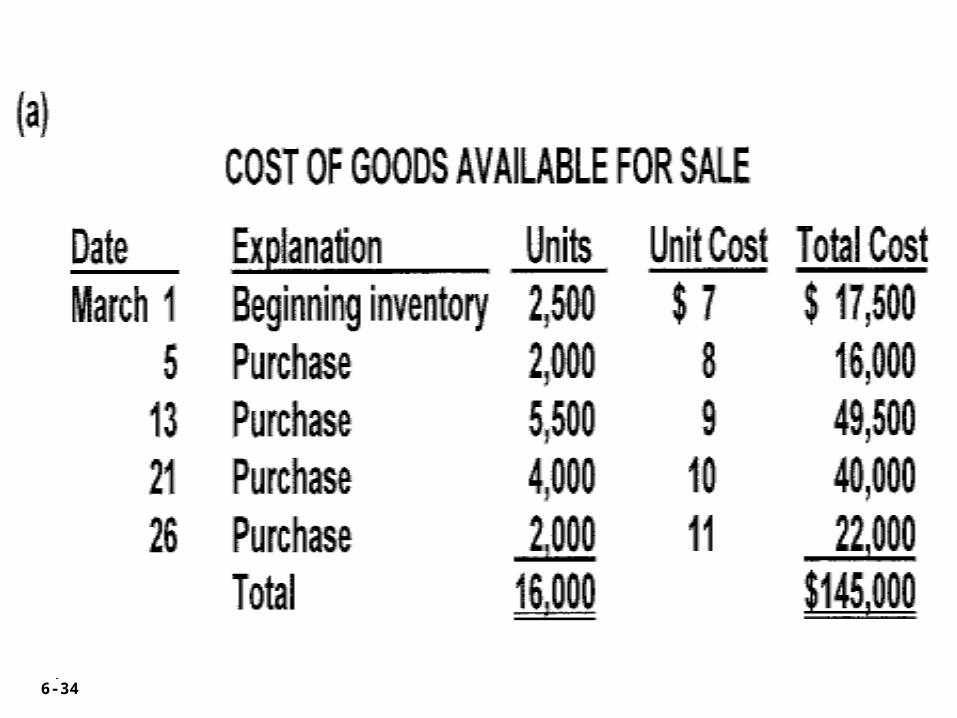

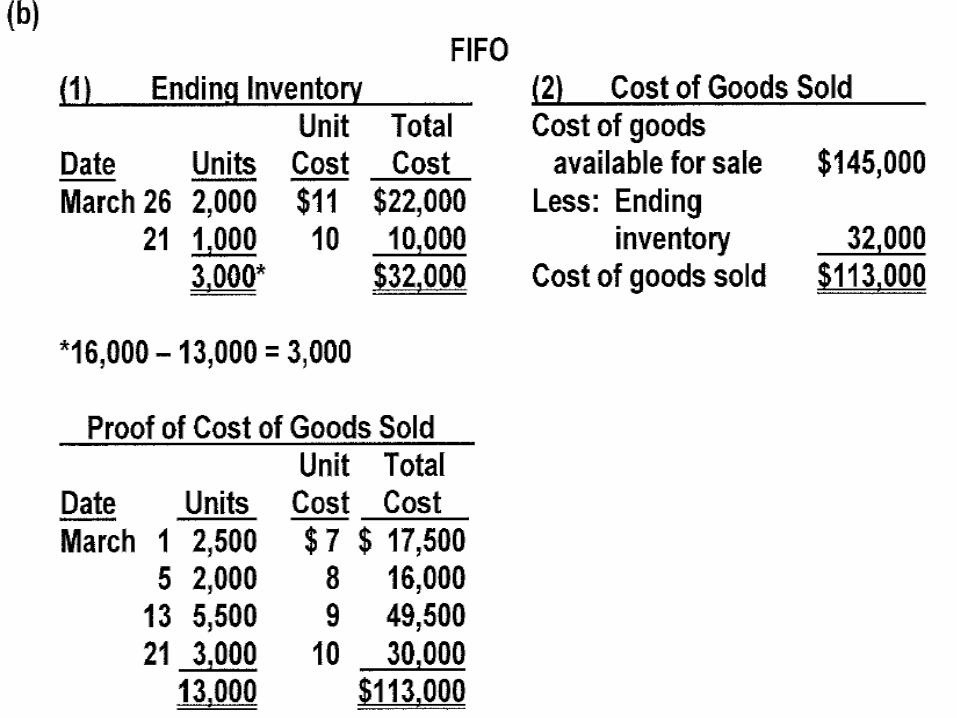

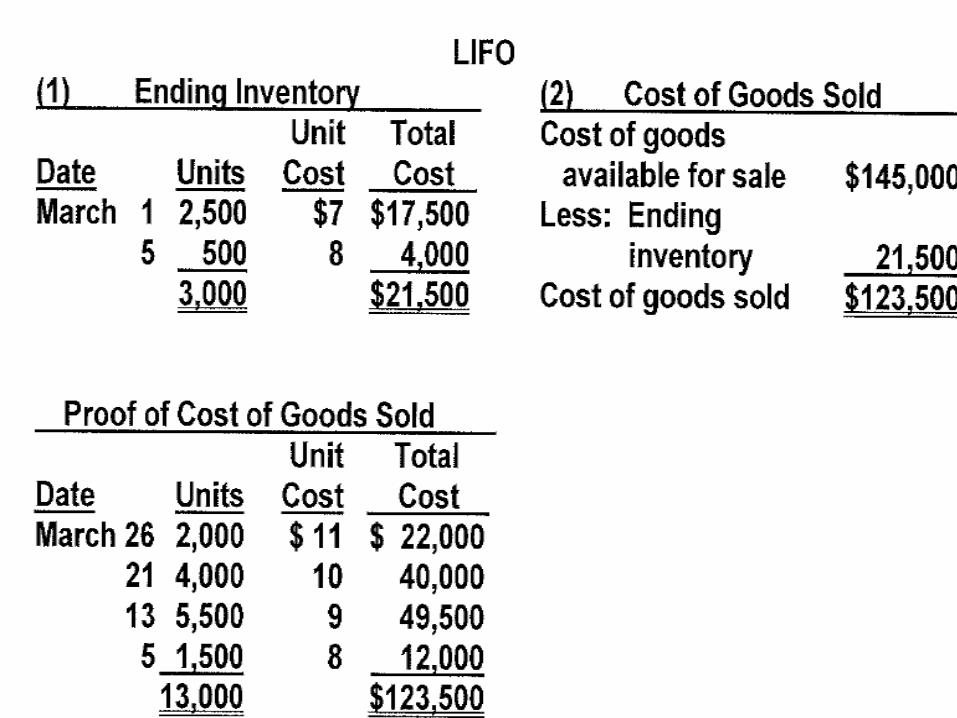

Question P6-2A on page 312Question P6-2A on page 312

Chapter 6-34

Chapter 6-35

Chapter 6-36

Chapter 6-37

Chapter 6-38

Chapter 6-39

Lower-of-Cost-or-MarketLower-of-Cost-or-Market

Inventory CostingInventory CostingInventory CostingInventory Costing

SO 4 Explain the lower-of-cost-or-SO 4 Explain the lower-of-cost-or-market basis of accounting for market basis of accounting for inventories.inventories.

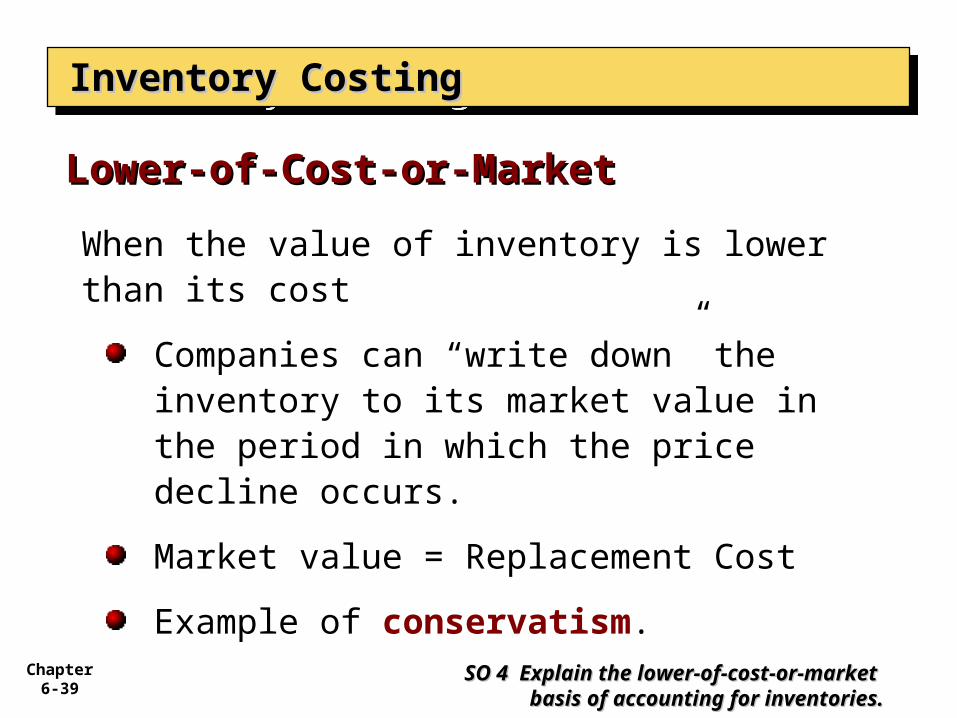

When the value of inventory is lower than its cost

Companies can “write down” the inventory to its market value in the period in which the price decline occurs.

Market value = Replacement Cost

Example of conservatism.

Chapter 6-40

Lower-of-Cost-or-MarketLower-of-Cost-or-Market

Inventory CostingInventory CostingInventory CostingInventory Costing

SO 4 Explain the lower-of-cost-or-SO 4 Explain the lower-of-cost-or-market basis of accounting for market basis of accounting for inventories.inventories.

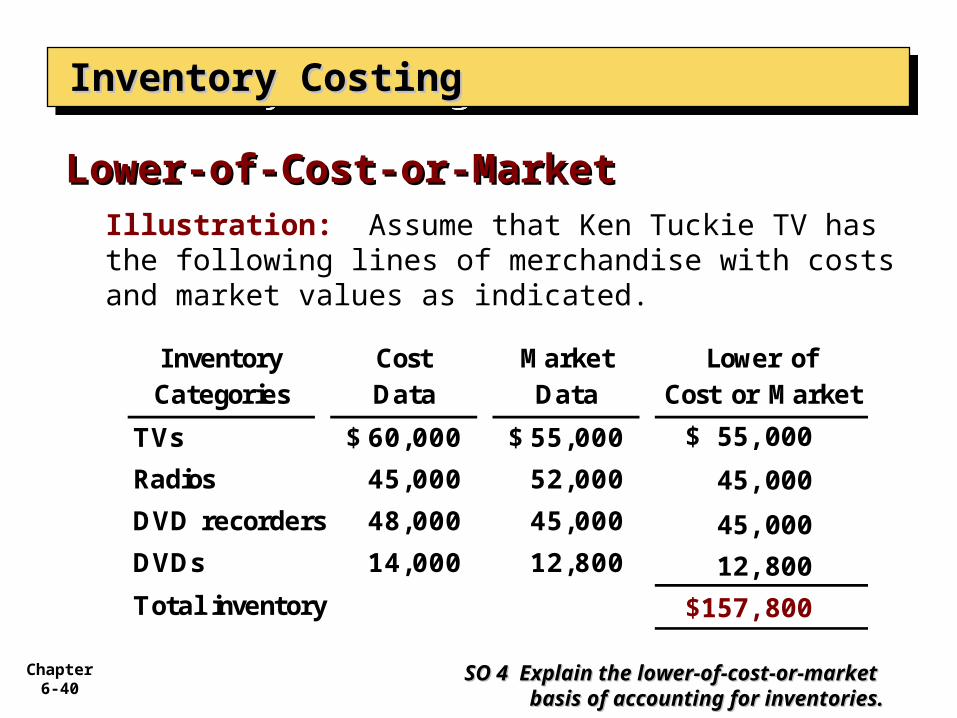

Illustration: Assume that Ken Tuckie TV has the following lines of merchandise with costs and market values as indicated.

Inventory Cost Market Lower ofCategories Data Data Cost or Market

TVs 60,000$ 55,000$

Radios 45,000 52,000

DVD recorders 48,000 45,000

DVDs 14,000 12,800

Total inventory

$ 55,000

45,000

45,000

12,800

$157,800

Chapter 6-41

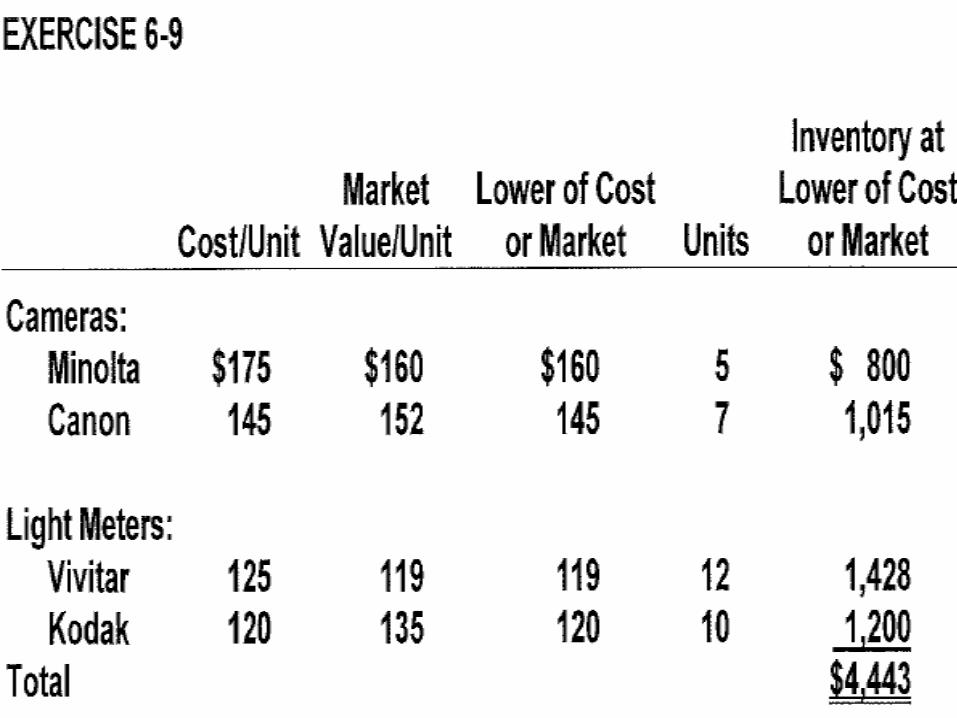

Ex 6-9 on page 309Ex 6-9 on page 309

Chapter 6-42

Chapter 6-43

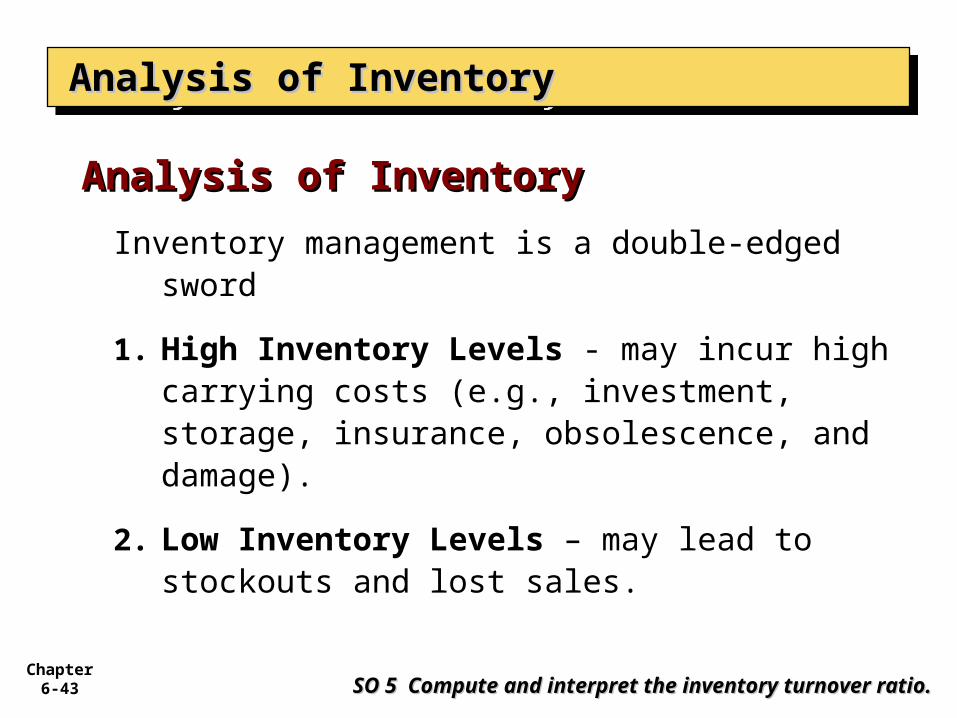

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

Inventory management is a double-edged sword

1. High Inventory Levels - may incur high carrying costs (e.g., investment, storage, insurance, obsolescence, and damage).

2. Low Inventory Levels – may lead to stockouts and lost sales.

Analysis of InventoryAnalysis of Inventory

SO 5 Compute and interpret the inventory turnover ratio.SO 5 Compute and interpret the inventory turnover ratio.

Chapter 6-44

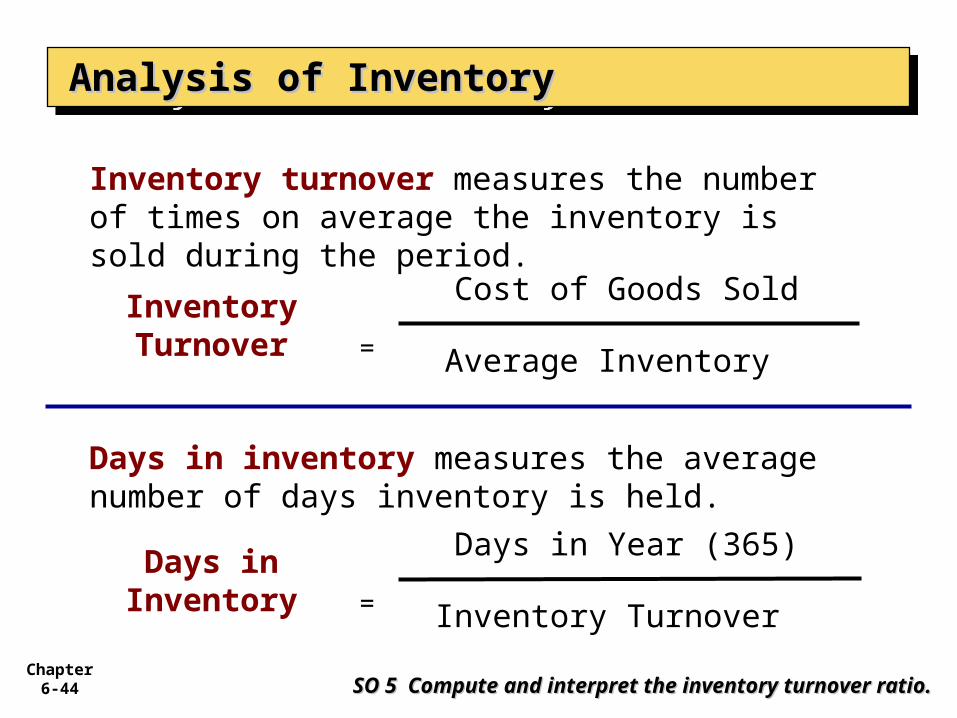

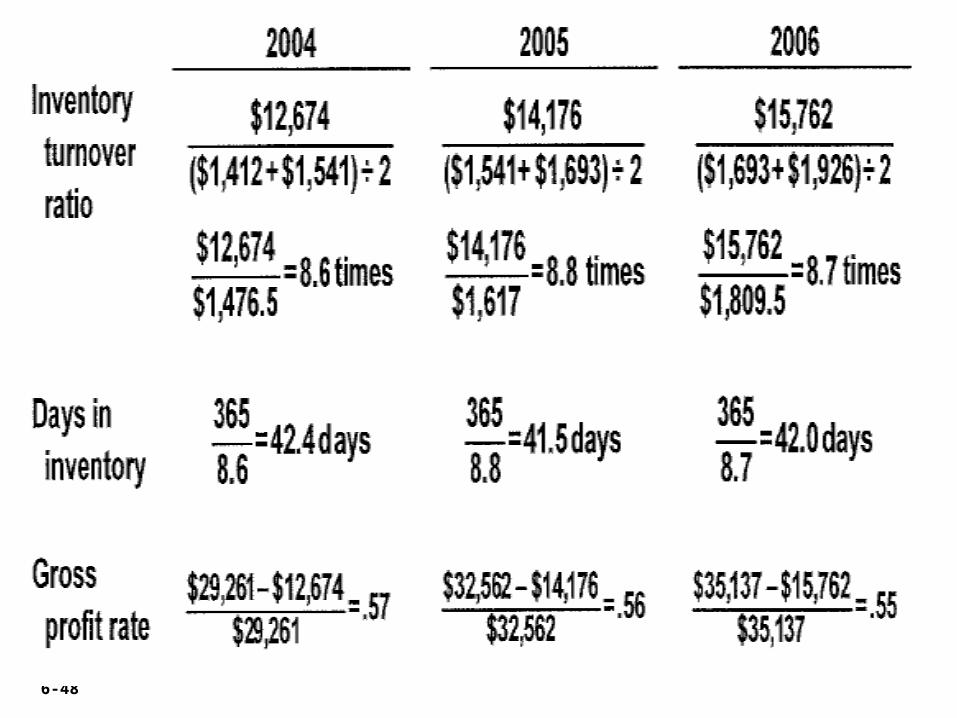

Inventory turnover measures the number of times on average the inventory is sold during the period.

Cost of Goods Sold

Average Inventory

Inventory Turnover

=

Days in inventory measures the average number of days inventory is held.

Days in Year (365)

Inventory Turnover

Days in Inventory

=

SO 5 Compute and interpret the inventory turnover ratio.SO 5 Compute and interpret the inventory turnover ratio.

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

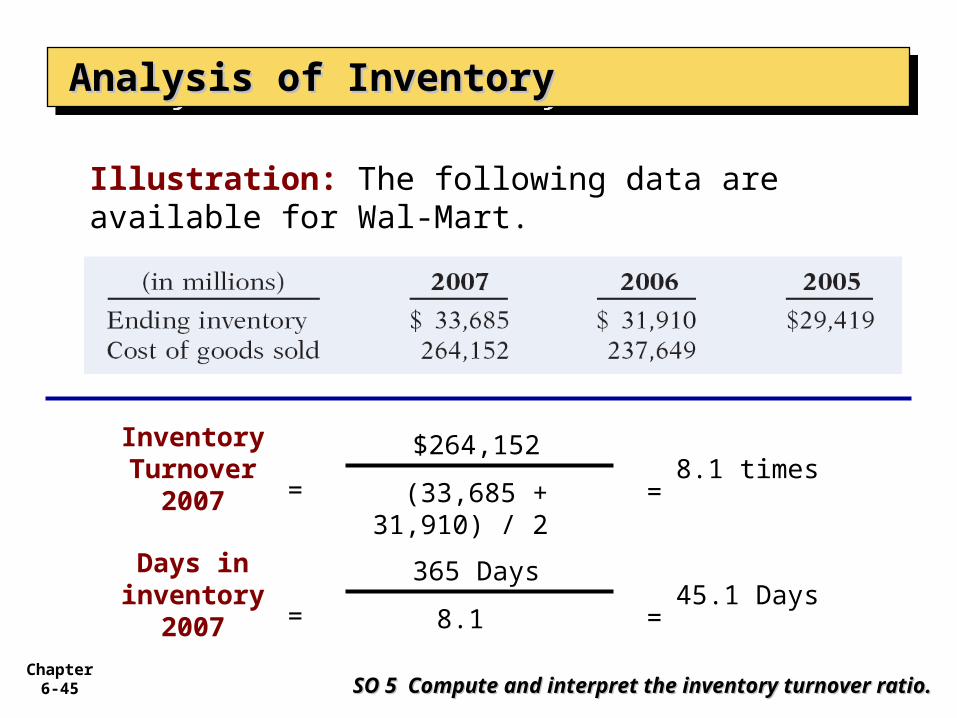

Chapter 6-45

Illustration: The following data are available for Wal-Mart.

$264,152

(33,685 + 31,910) / 2

Inventory Turnover

2007

=

SO 5 Compute and interpret the inventory turnover ratio.SO 5 Compute and interpret the inventory turnover ratio.

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

=

8.1 times

365 Days

8.1

Days in inventory

2007

=

=45.1 Days

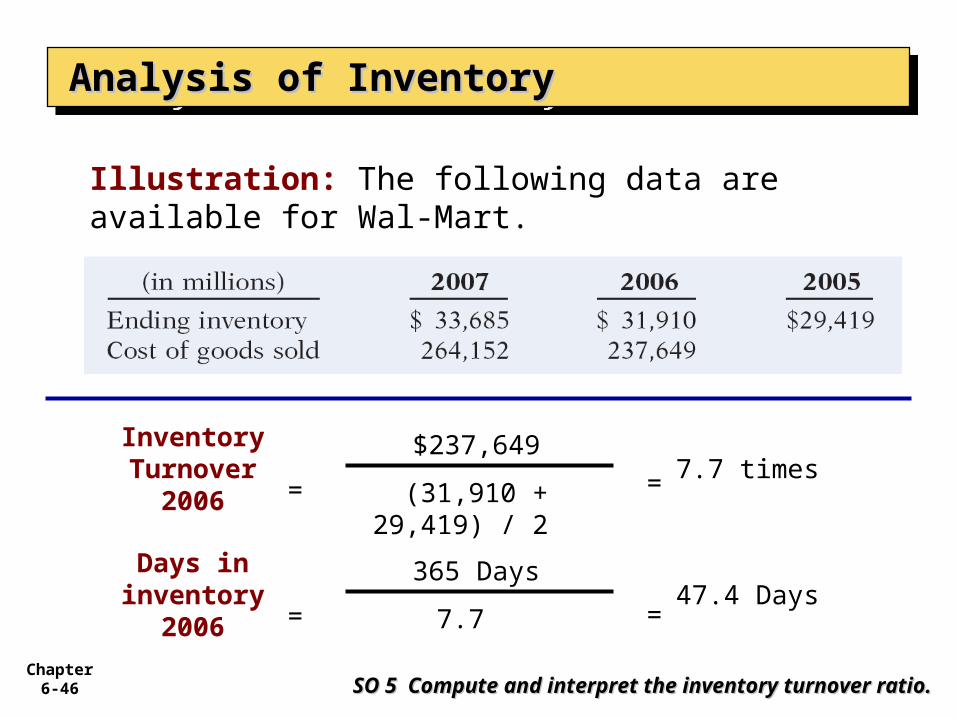

Chapter 6-46

Illustration: The following data are available for Wal-Mart.

$237,649

(31,910 + 29,419) / 2

Inventory Turnover

2006

=

SO 5 Compute and interpret the inventory turnover ratio.SO 5 Compute and interpret the inventory turnover ratio.

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

= 7.7 times

365 Days

7.7

Days in inventory

2006

=

=47.4 Days

Chapter 6-47

Ex 6-10 on page 309Ex 6-10 on page 309

Chapter 6-48

Chapter 6-49

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

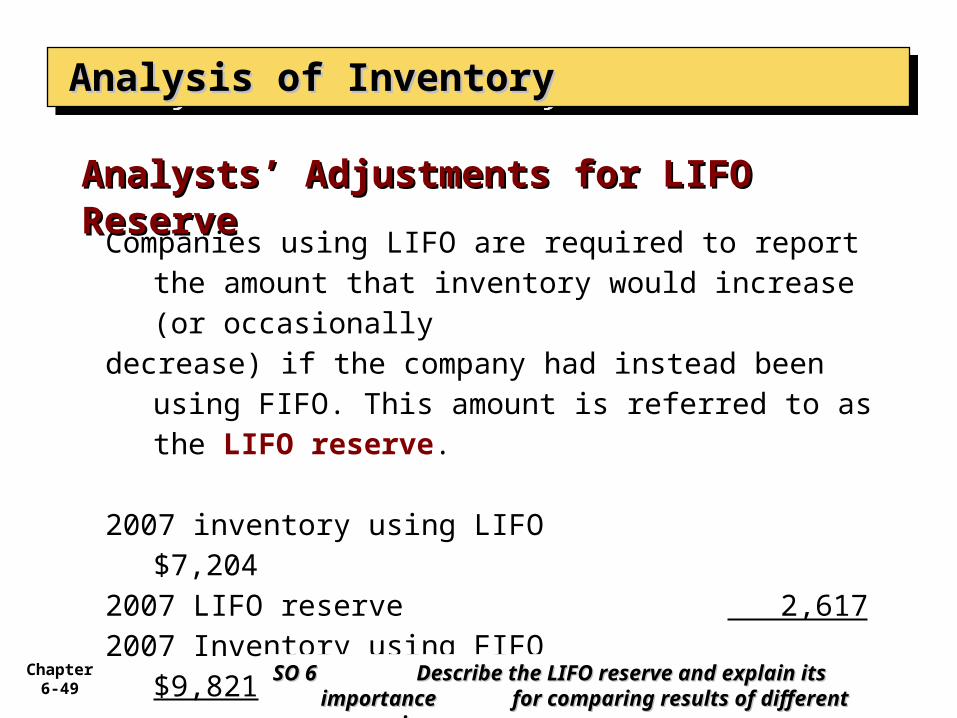

Companies using LIFO are required to report the amount that inventory would increase (or occasionally

decrease) if the company had instead been using FIFO. This amount is referred to as the LIFO reserve.

2007 inventory using LIFO $7,2042007 LIFO reserve 2,6172007 Inventory using FIFO $9,821

Analysts’ Adjustments for LIFO Analysts’ Adjustments for LIFO ReserveReserve

SO 6 SO 6 Describe the LIFO reserve and explain its Describe the LIFO reserve and explain its importance importance for comparing results of different for comparing results of different companies.companies.

Chapter 6-50

Analysis of InventoryAnalysis of InventoryAnalysis of InventoryAnalysis of Inventory

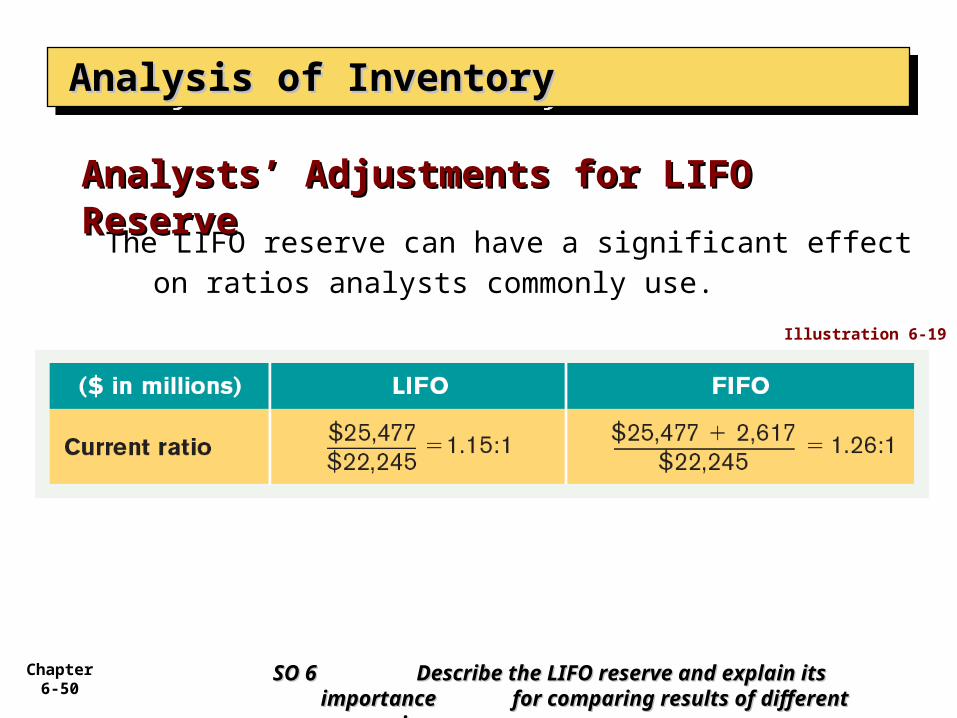

The LIFO reserve can have a significant effect on ratios analysts commonly use.

Analysts’ Adjustments for LIFO Analysts’ Adjustments for LIFO ReserveReserve

SO 6 SO 6 Describe the LIFO reserve and explain its Describe the LIFO reserve and explain its importance importance for comparing results of different for comparing results of different companies.companies.

Illustration 6-19

Chapter 6-51

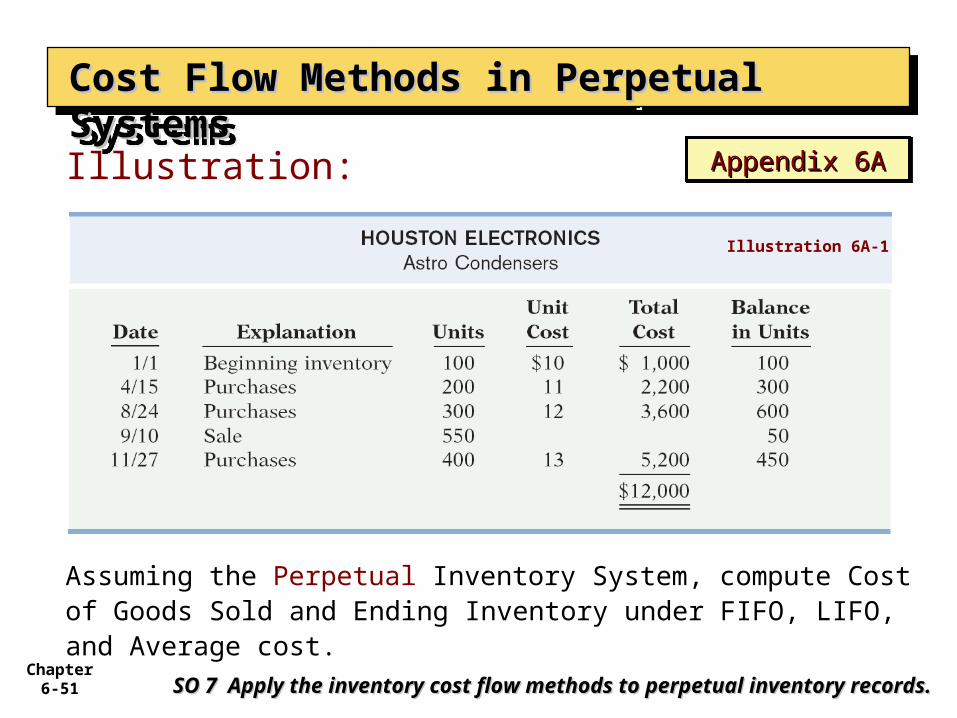

Illustration:

Cost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual Systems

SO 7 Apply the inventory cost flow methods to perpetual inventory SO 7 Apply the inventory cost flow methods to perpetual inventory records.records.

Assuming the Perpetual Inventory System, compute Cost of Goods Sold and Ending Inventory under FIFO, LIFO, and Average cost.

Appendix 6AAppendix 6AAppendix 6AAppendix 6A

Illustration 6A-1

Chapter 6-52

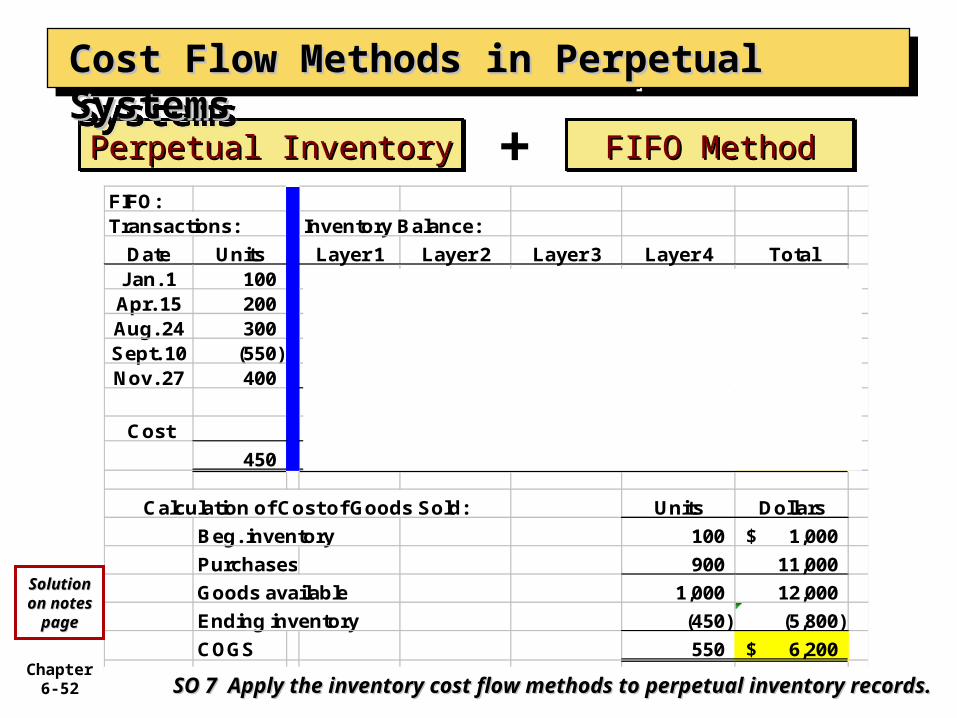

FIFO:Transactions: Inventory Balance:

Date Units Layer 1 Layer 2 Layer 3 Layer 4 TotalJan. 1 100 100 Apr. 15 200 200 Aug. 24 300 300 Sept. 10 (550) (100) (200) (250) Nov. 27 400 400

- - 50 400 450 Cost 10$ 11$ 12$ 13$

450 -$ -$ 600$ 5,200$ 5,800$

Calculation of Cost of Goods Sold: Units Dollars

Beg. inventory 100 1,000$

Purchases 900 11,000

Goods available 1,000 12,000

Ending inventory (450) (5,800)

COGS 550 6,200$

Perpetual InventoryPerpetual InventoryPerpetual InventoryPerpetual Inventory FIFO MethodFIFO MethodFIFO MethodFIFO Method+

Cost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual Systems

SO 7 Apply the inventory cost flow methods to perpetual inventory SO 7 Apply the inventory cost flow methods to perpetual inventory records.records.

SolutioSolution on n on

notes notes pagepage

Chapter 6-53

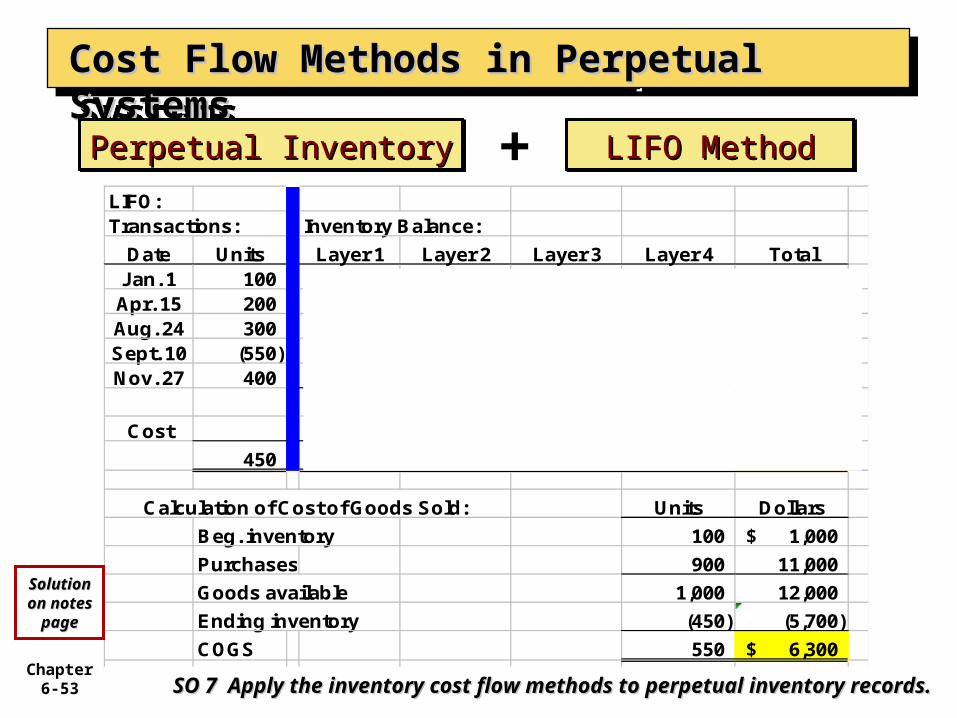

LIFO:Transactions: Inventory Balance:

Date Units Layer 1 Layer 2 Layer 3 Layer 4 TotalJan. 1 100 100 Apr. 15 200 200 Aug. 24 300 300 Sept. 10 (550) (50) (200) (300) Nov. 27 400 400

50 - - 400 450 Cost 10$ 11$ 12$ 13$

450 500$ -$ -$ 5,200$ 5,700$

Calculation of Cost of Goods Sold: Units Dollars

Beg. inventory 100 1,000$

Purchases 900 11,000

Goods available 1,000 12,000

Ending inventory (450) (5,700)

COGS 550 6,300$

LIFO MethodLIFO MethodLIFO MethodLIFO Method

Cost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual Systems

SO 7 Apply the inventory cost flow methods to perpetual inventory SO 7 Apply the inventory cost flow methods to perpetual inventory records.records.

Perpetual InventoryPerpetual InventoryPerpetual InventoryPerpetual Inventory +

SolutioSolution on n on

notes notes pagepage

Chapter 6-54

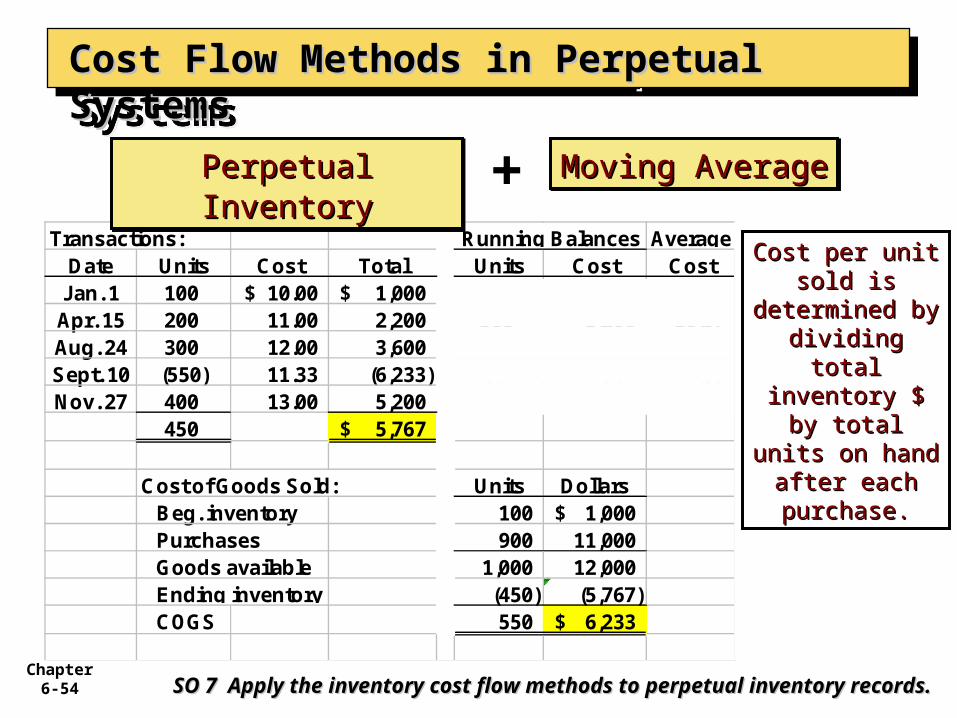

Transactions: AverageDate Units Cost Total Units Cost Cost

Jan. 1 100 10.00$ 1,000$ 100 1,000$ 10.00$ Apr. 15 200 11.00 2,200 300 3,200 10.67 Aug. 24 300 12.00 3,600 600 6,800 11.33 Sept. 10 (550) 11.33 (6,233) 50 567 11.33 Nov. 27 400 13.00 5,200 450 5,767 12.46

450 5,767$

Cost of Goods Sold: Units DollarsBeg. inventory 100 1,000$ Purchases 900 11,000 Goods available 1,000 12,000 Ending inventory (450) (5,767) COGS 550 6,233$

Running Balances

Perpetual InventoryPerpetual InventoryPerpetual InventoryPerpetual Inventory Moving AverageMoving AverageMoving AverageMoving Average

Cost per unit Cost per unit sold is sold is

determined by determined by dividing total dividing total

inventory $ by inventory $ by total units on total units on

hand after hand after each purchase.each purchase.

+

Cost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual Systems

SO 7 Apply the inventory cost flow methods to perpetual inventory SO 7 Apply the inventory cost flow methods to perpetual inventory records.records.

Chapter 6-55

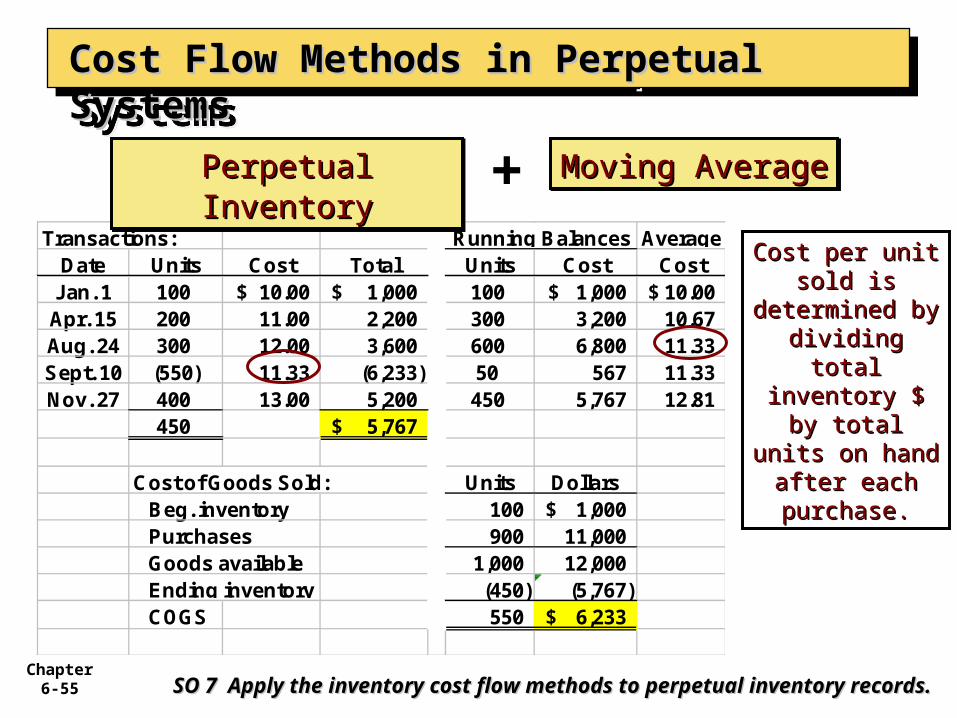

Transactions: AverageDate Units Cost Total Units Cost Cost

Jan. 1 100 10.00$ 1,000$ 100 1,000$ 10.00$ Apr. 15 200 11.00 2,200 300 3,200 10.67 Aug. 24 300 12.00 3,600 600 6,800 11.33 Sept. 10 (550) 11.33 (6,233) 50 567 11.33 Nov. 27 400 13.00 5,200 450 5,767 12.81

450 5,767$

Cost of Goods Sold: Units DollarsBeg. inventory 100 1,000$ Purchases 900 11,000 Goods available 1,000 12,000 Ending inventory (450) (5,767) COGS 550 6,233$

Running Balances

Perpetual InventoryPerpetual InventoryPerpetual InventoryPerpetual Inventory Moving AverageMoving AverageMoving AverageMoving Average

Cost per unit Cost per unit sold is sold is

determined by determined by dividing total dividing total

inventory $ by inventory $ by total units on total units on

hand after hand after each purchase.each purchase.

+

Cost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual SystemsCost Flow Methods in Perpetual Systems

SO 7 Apply the inventory cost flow methods to perpetual inventory SO 7 Apply the inventory cost flow methods to perpetual inventory records.records.

Chapter 6-56

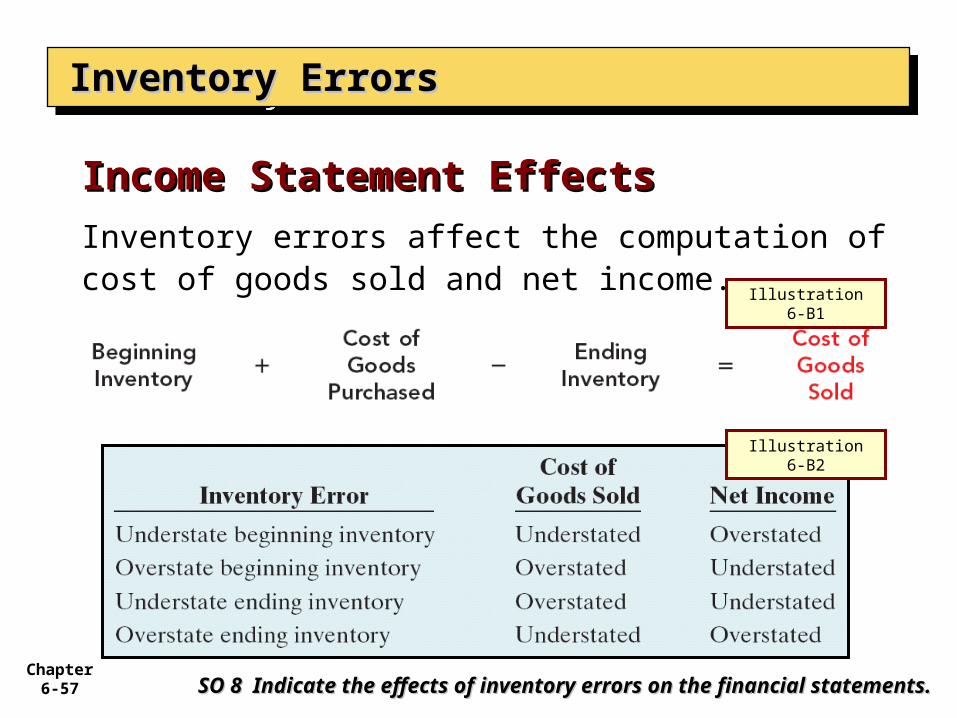

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

Common Cause:

Failure to count or price inventory correctly.

Not properly recognizing the transfer of legal title to goods in transit.

Errors affect both the income statement and balance sheet.

Appendix 6BAppendix 6BAppendix 6BAppendix 6B

Chapter 6-57

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

Inventory errors affect the computation of cost of goods sold and net income.

Income Statement EffectsIncome Statement Effects

Illustration 6-B2

Illustration 6-B1

Chapter 6-58

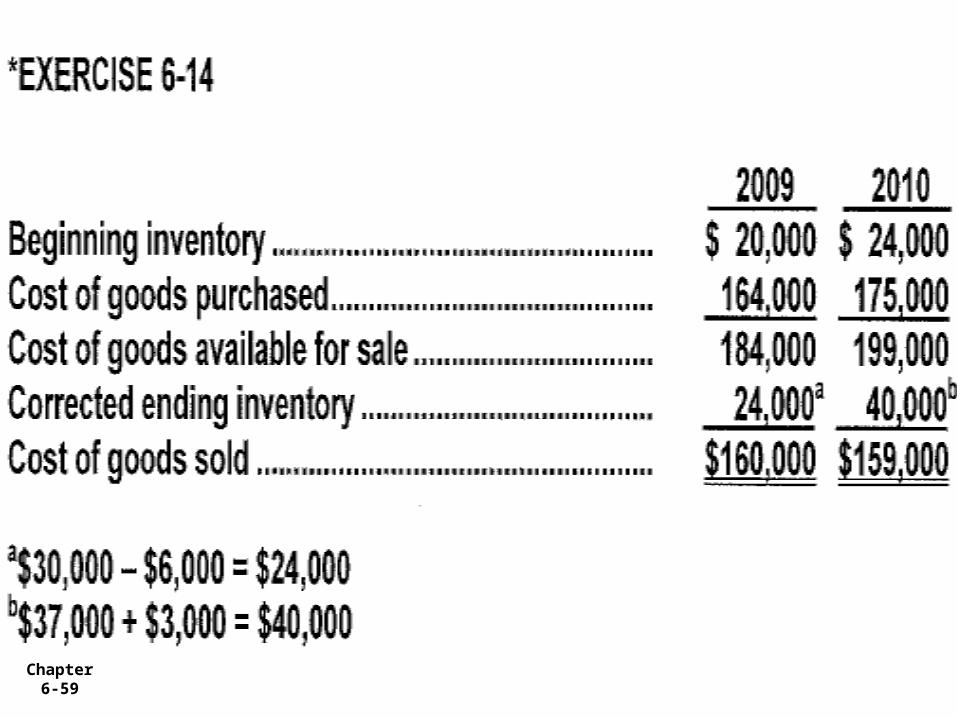

Ex 6-14 on page 310

Chapter 6-59

Chapter 6-60

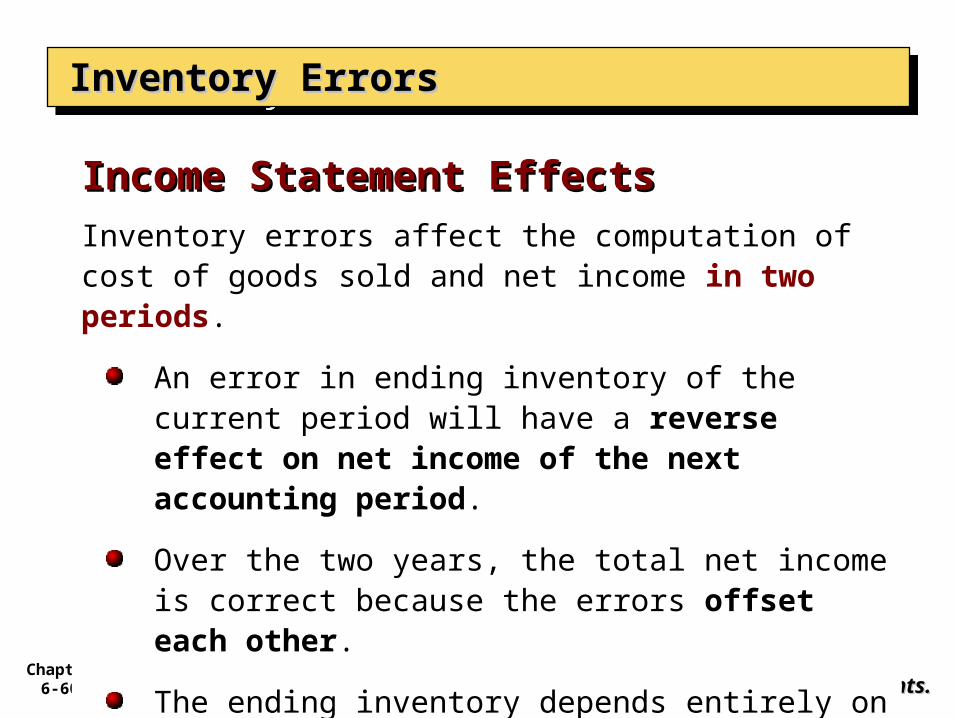

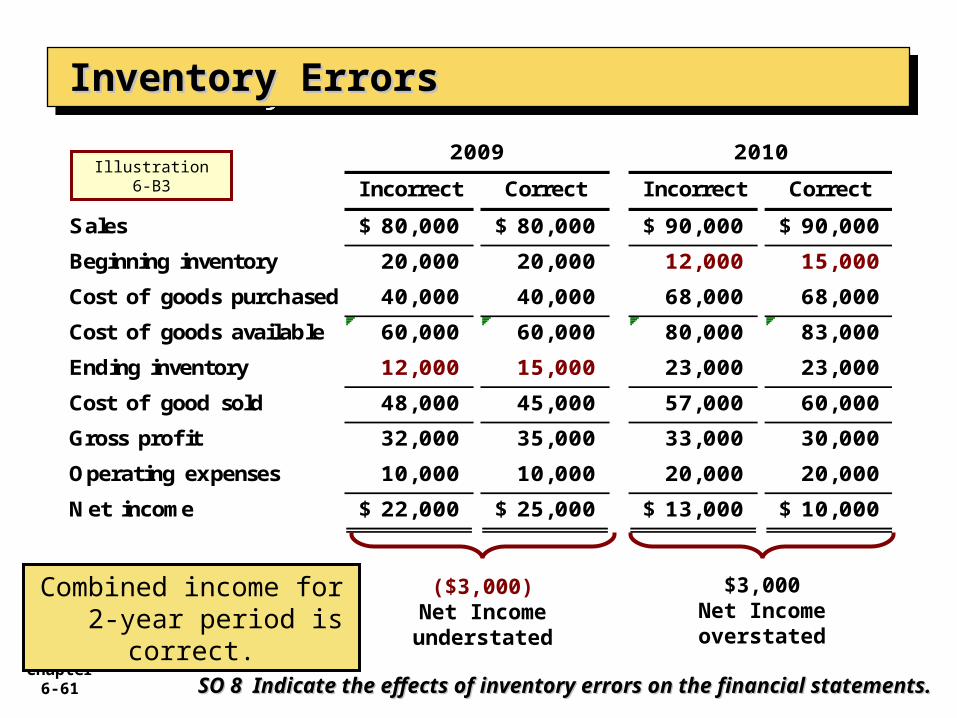

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

Inventory errors affect the computation of cost of goods sold and net income in two periods.

An error in ending inventory of the current period will have a reverse effect on net income of the next accounting period.

Over the two years, the total net income is correct because the errors offset each other.

The ending inventory depends entirely on the accuracy of taking and costing the inventory.

Income Statement EffectsIncome Statement Effects

Chapter 6-61

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

I ncorrect Correct Incorrect Correct

Sales 80,000$ 80,000$ 90,000$ 90,000$

Beginning inventory 20,000 20,000 12,000 15,000

Cost of goods purchased 40,000 40,000 68,000 68,000

Cost of goods available 60,000 60,000 80,000 83,000

Ending inventory 12,000 15,000 23,000 23,000

Cost of good sold 48,000 45,000 57,000 60,000

Gross profit 32,000 35,000 33,000 30,000

Operating expenses 10,000 10,000 20,000 20,000

Net income 22,000$ 25,000$ 13,000$ 10,000$

2009 2010

($3,000)Net Income understated

$3,000Net Income overstated

Combined income for 2-year period is

correct.

Illustration 6-B3

Chapter 6-62

Understating ending inventory will overstate:

a. assets.

b. cost of goods sold.

c. net income.

d. owner's equity.

Review QuestionReview Question

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

Chapter 6-63

Inventory ErrorsInventory ErrorsInventory ErrorsInventory Errors

SO 8 Indicate the effects of inventory errors on the financial SO 8 Indicate the effects of inventory errors on the financial statements.statements.

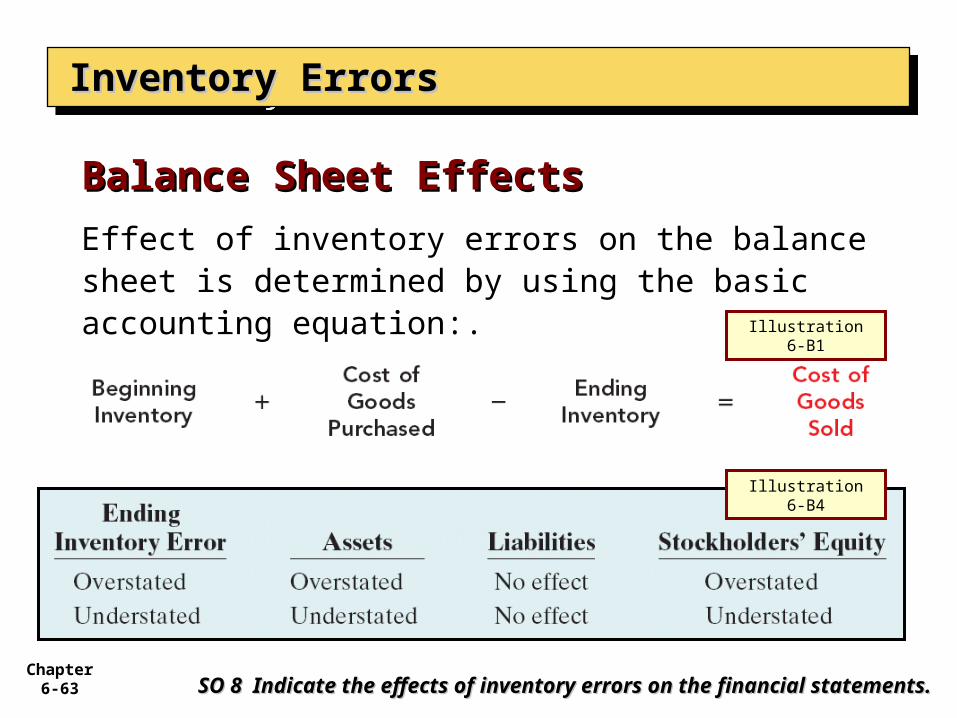

Effect of inventory errors on the balance sheet is determined by using the basic accounting equation:.

Balance Sheet EffectsBalance Sheet Effects

Illustration 6-B1

Illustration 6-B4