chapter 5-1 acct341, chapter 8 ais and business processes: part ii introduction the resource...

TRANSCRIPT

Chapter 5-1

ACCT341, Chapter 8 AIS and Business Processes: Part II

Introduction

The Resource Management Process

The Production Process

The Financing Process

Business Processes In Special Industries

Monitoring Business Processes

Chapter 5-2

Introduction

Many organizations need typical AIS requirements and some specialized information also

Focus of AISs formerly transaction processing presently capturing data around business processes

Two important transaction processing cycles are the production and financing cycles.

Chapter 5-3

The ResourceManagement Process

Organizations use resources to produce goods, to provide services, andto generate revenues.

An AIS must pay attention tothe inventory, human resources, and fixed assets.

Chapter 5-4

Human Resource Management

An organization’s human resource management activity includes

the personnel function hires employees, trains employees, and maintains personnel records maintains payroll records for employees

Chapter 5-5

the payroll function pays employees for their work maintains records of employees’ paychecks, complies with employee tax, reports on various deduction categories, and interacting with the personnel function

Human Resource Management

Chapter 5-6

Human ResourceManagement Objectives

Hiring, training, and employing workersMaintaining employee earnings recordsComplying with regulatory reporting requirementsReporting on payroll deductionsMaking timely and accurate paymentsto employeesProviding an interface for personnel and payroll activities

Chapter 5-7

Human ResourceManagement Inputs

Personnel Action Forms document the hiring of new employees or changes in

employee status

Time Sheets used to track hours worked

Payroll Deduction Authorizations authorize the payroll system to deduct certain amounts

Tax Withholding Forms authorize payroll to reduce gross pay by the

appropriate withholding tax (W-4).

Chapter 5-8

Financial Statement Information

Employee Listings shows current employees and may contain address and

other demographic information

Paychecks the final documents in the process; subject to strict internal

controls

Check Registers used to make journal entries for salary and payroll tax

expenses

Human ResourceManagement Outputs

Chapter 5-9

Human ResourceManagement Outputs

Deduction Reports contain summaries of deductions for employees as a

group

Tax (Regulatory) Reports reports the government requires for income tax,

social security tax, and unemployment tax information

Payroll Summaries used by management in

analyzing expenses

Chapter 5-10

Fixed Asset Management

Fixed assets assets with usable lives of more than one year.

A fixed-asset management system has to manage the assets in terms of their purchase, maintenance, valuation, and disposal.

Chapter 5-11

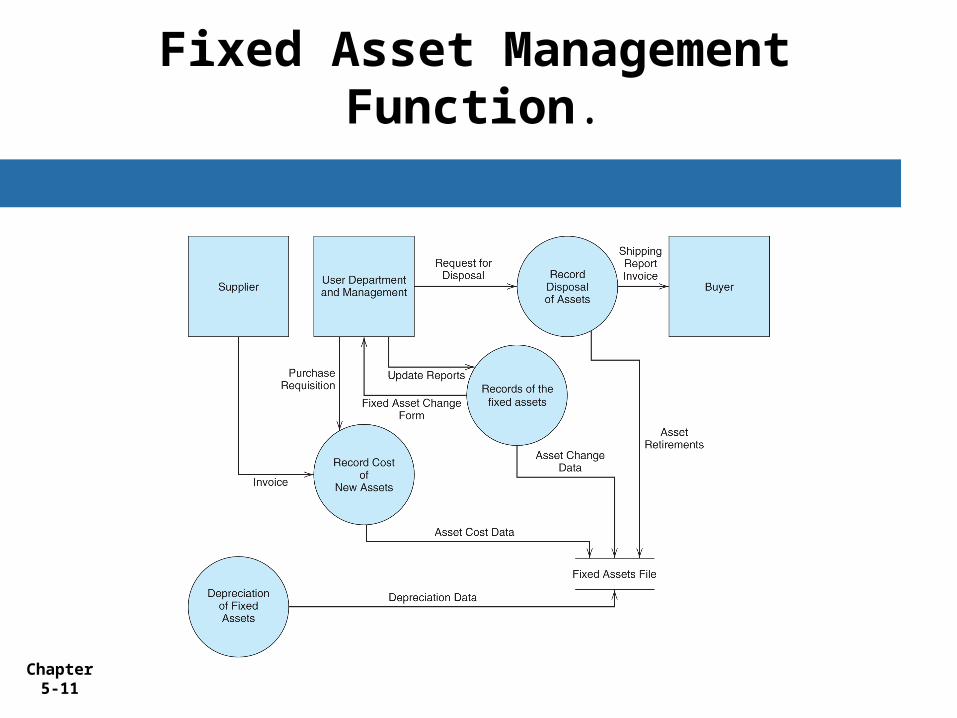

Fixed Asset Management Function.

Chapter 5-12

Fixed Asset Management Objectives

Tracking the purchase, maintenance, valuation, and disposal of the fixed assets

Calculating the depreciation for a company’sfinancial statements

Tracking repair costs, distinguishing between revenue and capital expenditures

Calculating the gain or loss upon disposal of individual fixed assets.

Chapter 5-13

Fixed Asset Management Inputs

Purchase Requisition requiring approval by one or more managers

Receiving Report upon receipt of a fixed asset

Supplier Invoice when it ships the asset

Chapter 5-14

Fixed Asset Management Inputs

Construction Work Orders if the company builds the asset

Repairs and Maintenance Reports update of expense accounts for repairs and

maintenance

Fixed Asset Change Forms basis for transferring fixed assets from one

location to another, retiring, selling or trading-in fixed assets

Chapter 5-15

Fixed Asset Management Outputs

Financial Statement Information gives the details of the valuation of the fixed assets

Fixed Asset Register lists identification numbers and location for

each fixed asset

Depreciation Register shows depreciation expense and

accumulated depreciation

Chapter 5-16

Fixed Asset Management Outputs

Repair and Maintenance Reports show the repair and maintenance

expenses and history

Retired Assets Report shows all assets disposed of

during the accounting period

Chapter 5-17

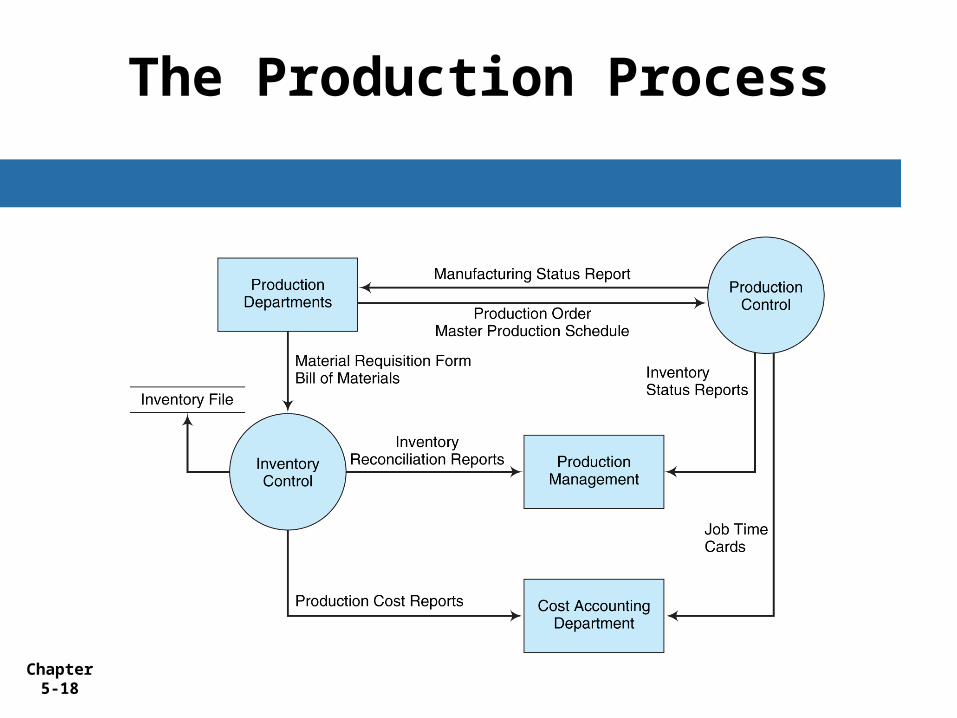

The Production Process

The production process begins with a request for raw material and ends with the transfer of finished goods to warehouses

This cycle, associated with producing goods concerns the capture of data and the reporting of information

Chapter 5-18

The Production Process

Chapter 5-19

Production Process - Objectives

Track purchases and sales of inventories

Monitor and control manufacturing costs

Control and coordinate the production process

Control inventory

Provide input for budgets

Chapter 5-20

Cost Accounting Subsystem

The cost accounting subsystemis an important part of the production processprovides important control information for the budgetcan vary depending upon the type of businessmanufacturing can have a job costing system process costing system activity-based costing system

Chapter 5-21

Just-in-Time (JIT)Inventory Systems

A Just-in-Time (JIT) Inventory Systemis a make-to-order inventory system

ensures that the production cycle processes inventory transactions appropriately

attempts to minimize inventory carrying costs.

Chapter 5-22

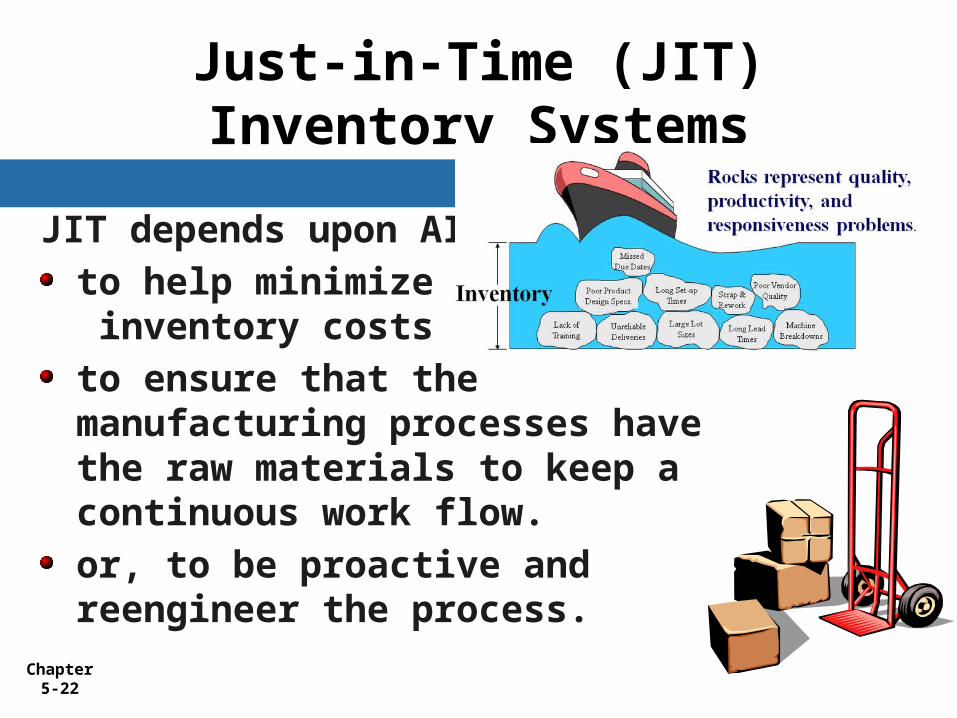

Just-in-Time (JIT)Inventory Systems

JIT depends upon AIS:

to help minimize inventory costs

to ensure that the manufacturing processes have the raw materials to keep a continuous work flow.

or, to be proactive and reengineer the process.

Chapter 5-23

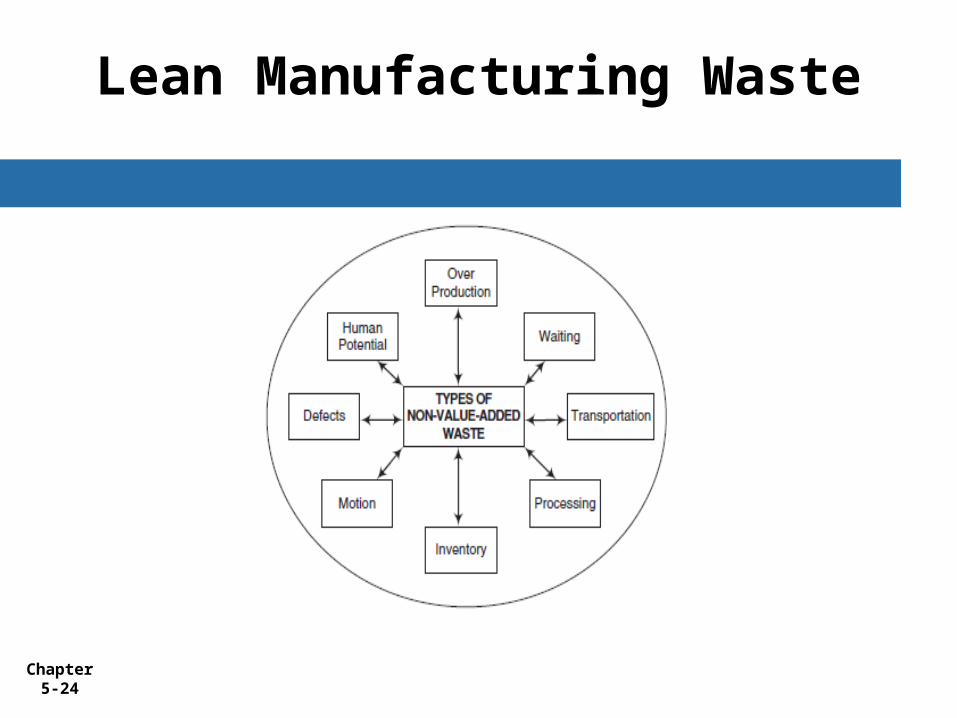

Lean Production/ Manufacturing

Concept Eliminate waste throughout the organization Focus on reduction of non-value-added waste

Lean Accounting Necessary in order to have lean accounting Data collection Evaluate performance measures

Chapter 5-24

Lean Manufacturing Waste

Chapter 5-25

Production Process - Inputs

Material Requisition Form directs stores to issue materials or parts to

designated work centers or authorized persons

Bill of Materials shows the types and quantities of parts needed to

make a single unit of product

Master Production Schedule shows the quantities of goods needed to meet sales

demands

Chapter 5-26

Production order shows prices charged for raw materials. incorporates data from sales orders or forecasts, operates lists and bills of materials in order to

authorize the production of an order or batch

Job Time Card shows the distribution of labor costs to

specific jobs or production orders

Production Process - Inputs

Chapter 5-27

PRODUCTION PROCESSES—TECHNOLOGICAL

ASSISSTANCE

ERP

Barcode scanners

Radio frequency technology (RFID)

Advanced electronic tags

Chapter 5-28

Production Process - Outputs

Financial Statement Information gives details of the costs and pricing

Materials Price List shows prices charged for raw materials

Periodic Usage Report provides managerial information on use of raw

materials

Inventory Reconciliation Report reconciles physical inventory with perpetual records

Chapter 5-29

Production Process - Outputs

Inventory Status Report allows purchasing and production managers

to monitor inventory levels

Production Cost Report details the actual costs for each production

operation, each cost element, and/or each separate job

Manufacturing Status Report provides managers with information about the status

of various jobs

Chapter 5-30

The Financing Process

The financing process is where a company acquires and uses

financial resources cash other liquid assets investments

The financing process includes the activities of;

borrowing cash selling ownership shares.

Chapter 5-31

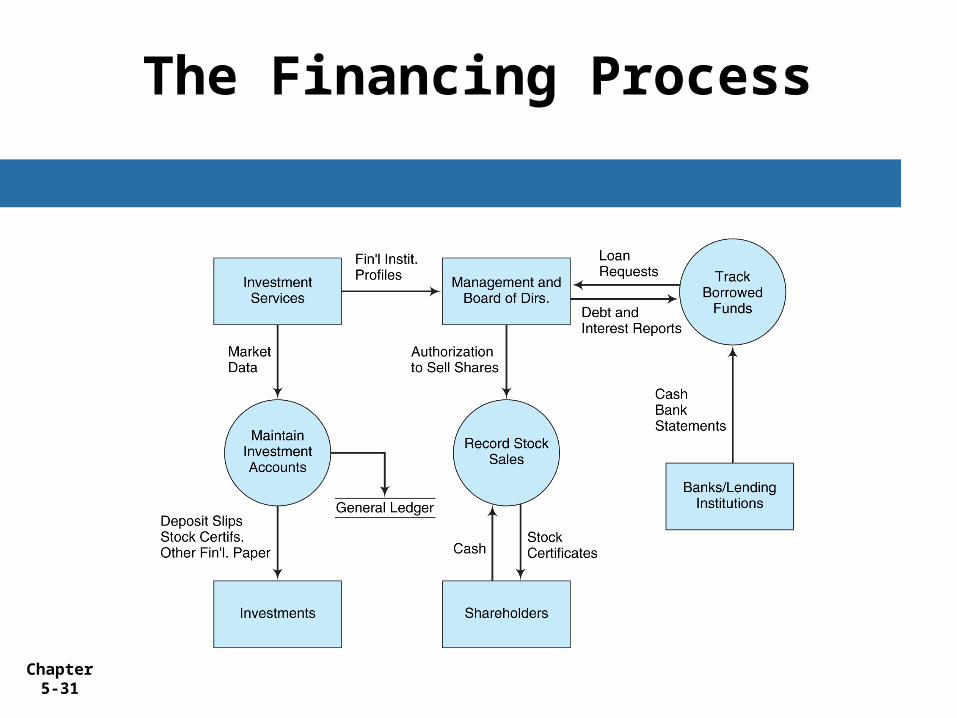

The Financing Process

Chapter 5-32

Financing Process - Objectives

Effective cash management making use of lockbox systems and

electronic funds transfer (EFT).

Minimizing cost of capital reducing the cost of obtaining

financial resources

Chapter 5-33

Maximizing return on investments using financial planning models

Project cash flows Consists of a cash receipts forecast and a

cash disbursements forecast.

Financing Process - Objectives

Chapter 5-34

Financing Process - Inputs

Remittance Advices

accompanies a customer’s payment

Deposit Slips banks provide to document account deposits

Checks companies receive and issue checks

Chapter 5-35

Financing Process - Inputs

Bank Statements

used to reconcile the cash balance in the company’s ledger against the cash balance in the bank account

Stock Market Data

Interest Data

Financial Institution Profiles

Chapter 5-36

Financing Process - Outputs

Financial Statement Information

Cash Budget

Investment Reports

Debt and Interest Reports

Financial Ratios

Financial Planning Model Reports

Chapter 5-37

Business Processes inSpecial Industries

Vertical market refers to markets or industries

services they provide or the goods they produce.

These organizations may require more information than is typically output from a

traditional AIS.

Examples of specialized information needs include time and billing systems, activity based costing systems, and point-of-sale systems.

Chapter 5-38

Industries with Specialized AISs

Professional service organizations have several unique operating characteristics:

a. No merchandise inventory

b. Professional employees

c. Difficulty in measuring output

d. Small size

Not-for-profit a. Professional employees and volunteers

b. Usually not affected by the market

c. Sometimes have a political environment

Chapter 5-39

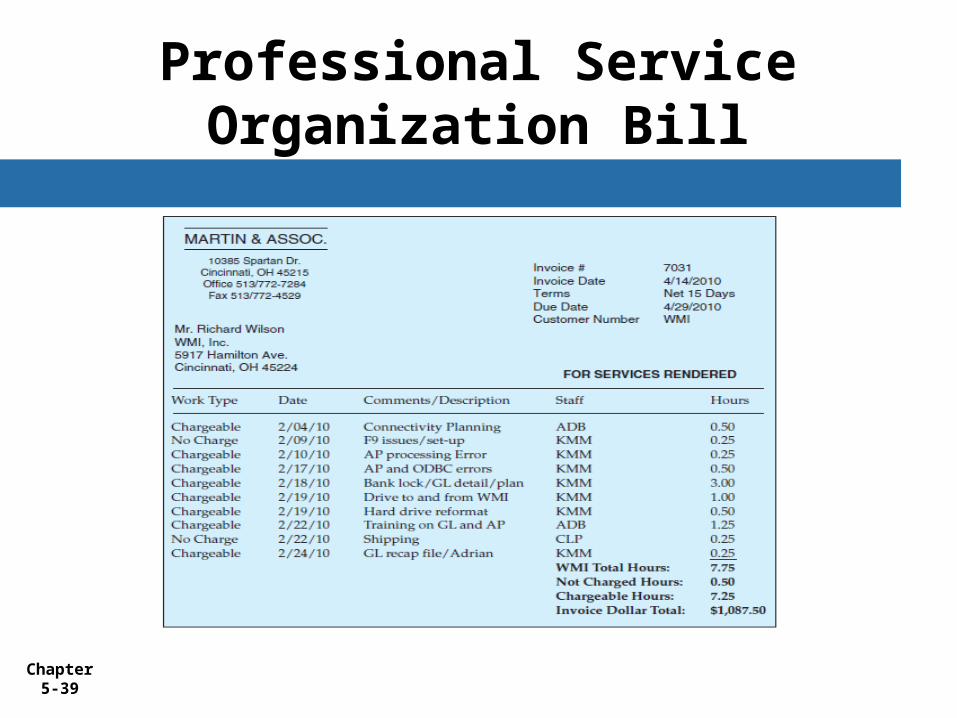

Professional Service Organization Bill

Chapter 5-40

INDUSTRIES WITH SPECIALIZED AISs

Health care a. Share many of the professional and not-

for-profit organizations’ special AIS needs

b. Special accounting needs because of third-party billing (private and government)

Chapter 5-41

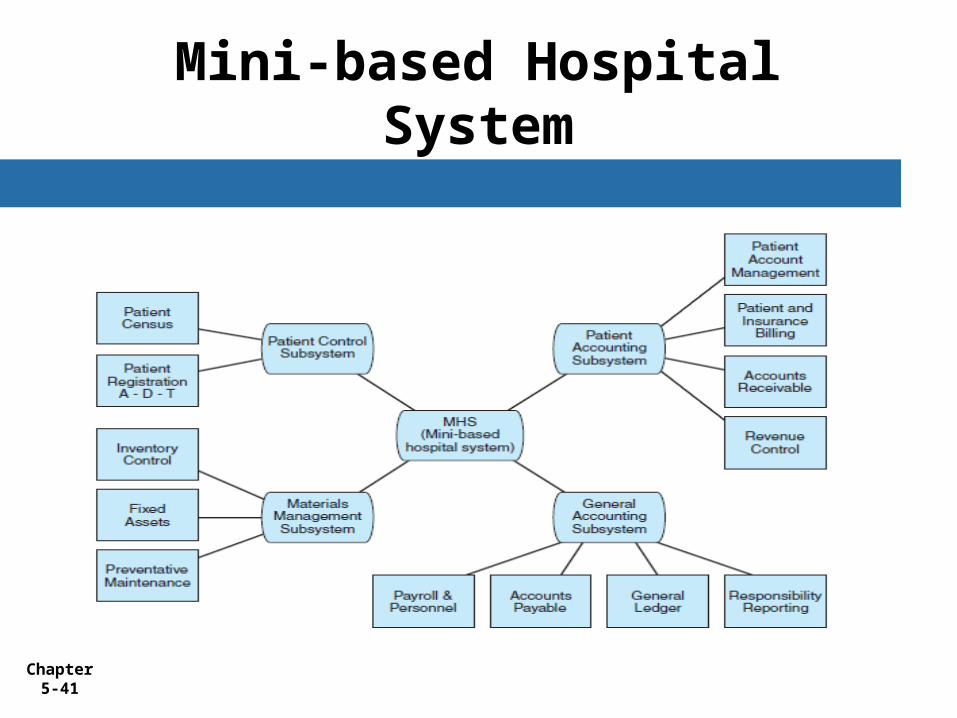

Mini-based Hospital System

Chapter 5-42

Business Process Reengineering

AISs were concerned with accounting transactions earlier are more concerned with business events now

Business events include important activities that affect the business are not captured by the financial accounting system

Business process reengineering (BPR) concerns redesigning business processes from scratch