chapter 4 financial reporting for a departmentalized business

TRANSCRIPT

Chapter 4Chapter 4

Financial Reporting for a Financial Reporting for a Departmentalized BusinessDepartmentalized Business

Terms that you need to knowTerms that you need to know

Fiscal PeriodFiscal Period The length of time which a business summarizes and The length of time which a business summarizes and

reports financial information.reports financial information.

Departmental Statement of gross profitDepartmental Statement of gross profit Provides a statement of revenue an cost information Provides a statement of revenue an cost information

for each department.for each department.

Interim departmental statement of gross profit.Interim departmental statement of gross profit. A statement that show revenue and cost information A statement that show revenue and cost information

for a shorter term than a fiscal period.for a shorter term than a fiscal period.

Why do we use Departmental Why do we use Departmental statements of gross profitstatements of gross profit

We use it to determine ending We use it to determine ending merchandise inventory.merchandise inventory. Two types of computing inventoryTwo types of computing inventory

• PeriodicPeriodic Physical inventoryPhysical inventory

• Perpetual Perpetual Book inventoryBook inventory We use the gross profit method of estimating an We use the gross profit method of estimating an

inventory with this type of inventory with this type of

Estimating Ending Merchandise Estimating Ending Merchandise inventoryinventory

Calculating Net Purchases and Net SalesCalculating Net Purchases and Net Sales Purchases – Purchase Return and Purchases – Purchase Return and

Allowances – Purchases Discount = Net Allowances – Purchases Discount = Net Purch.Purch.

Sales – Sales Return and Allowance – Sales Sales – Sales Return and Allowance – Sales Discount = Net SalesDiscount = Net Sales

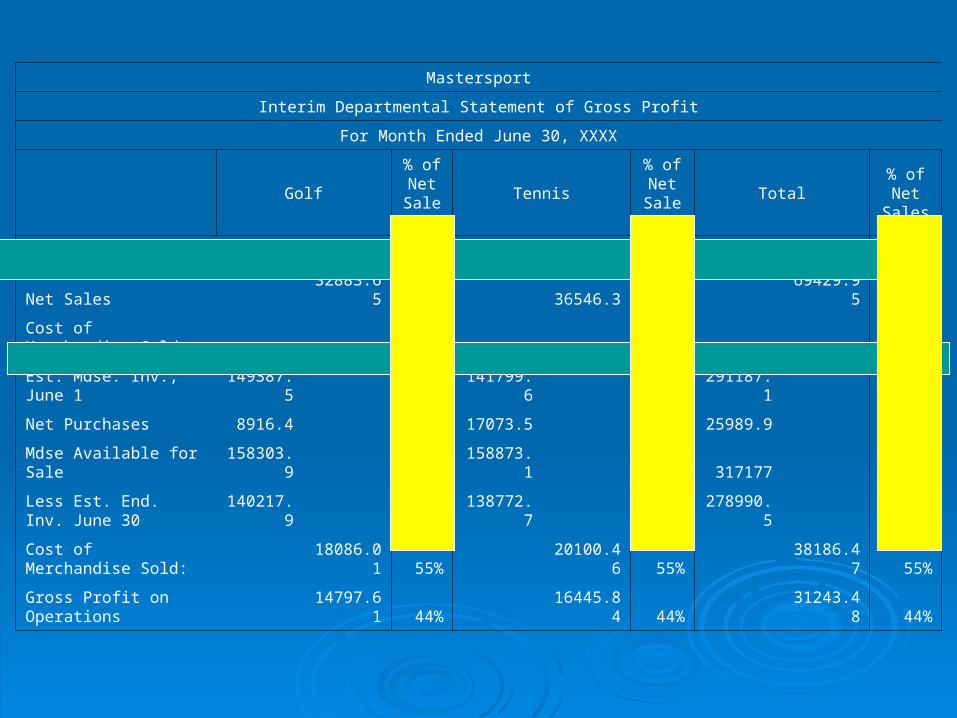

Mastersport

Interim Departmental Statement of Gross Profit

For Month Ended June 30, XXXX

Golf% of Net

SalesTennis

% of Net

SalesTotal

% of Net

Sales

Operating Revenue

Net Sales 32883.65 100% 36546.3 100% 69429.95 100%

Cost of Merchandise Sold:

Est. Mdse. Inv., June 1 149387.5 141799.6 291187.1

Net Purchases 8916.4 17073.5 25989.9

Mdse Available for Sale 158303.9 158873.1 317177

Less Est. End. Inv. June 30 140217.9 138772.7 278990.5

Cost of Merchandise Sold: 18086.01 55% 20100.46 55% 38186.47 55%

Gross Profit on Operations 14797.61 44% 16445.84 44% 31243.48 44%

4-2 4-2 Preparing a WorksheetPreparing a Worksheet for a for a Departmentalized BusinessDepartmentalized Business

Proving Accuracy between what our Proving Accuracy between what our Accounts Payable/Receivable accounts in Accounts Payable/Receivable accounts in our general ledger say versus what our our general ledger say versus what our schedule of accounts payable/receivable schedule of accounts payable/receivable say.say.

Remember that it is a check to make sure Remember that it is a check to make sure that there is balance between these that there is balance between these accounts and the records we keep. accounts and the records we keep.

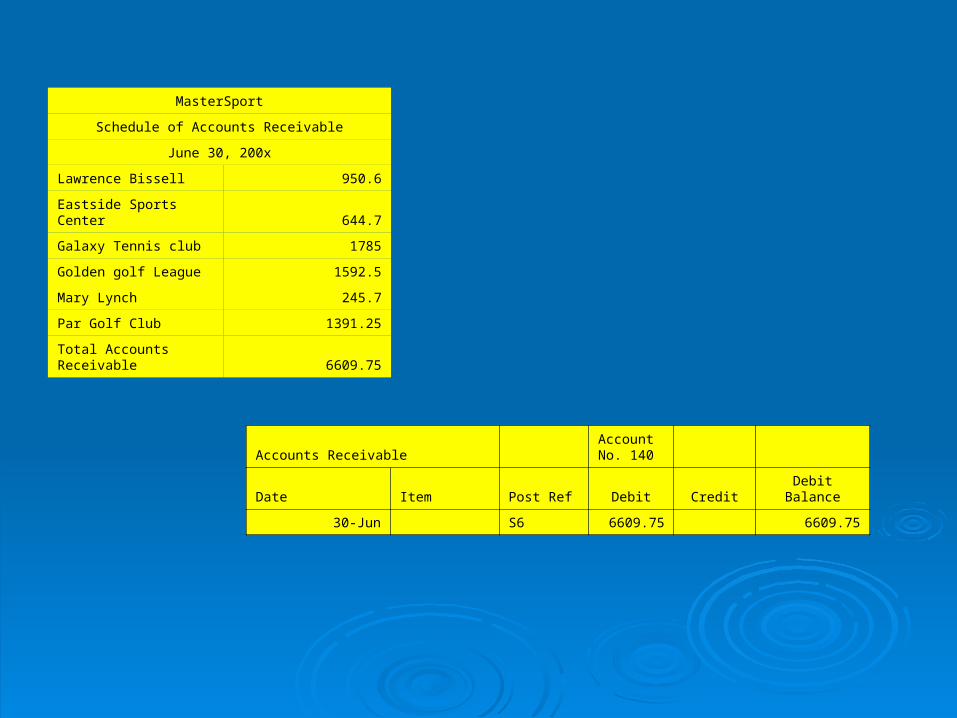

MasterSport

Schedule of Accounts Receivable

June 30, 200x

Lawrence Bissell 950.6

Eastside Sports Center 644.7

Galaxy Tennis club 1785

Golden golf League 1592.5

Mary Lynch 245.7

Par Golf Club 1391.25

Total Accounts Receivable 6609.75

Accounts Receivable Account No. 140

Date Item Post Ref Debit Credit Debit Balance

30-Jun S6 6609.75 6609.75

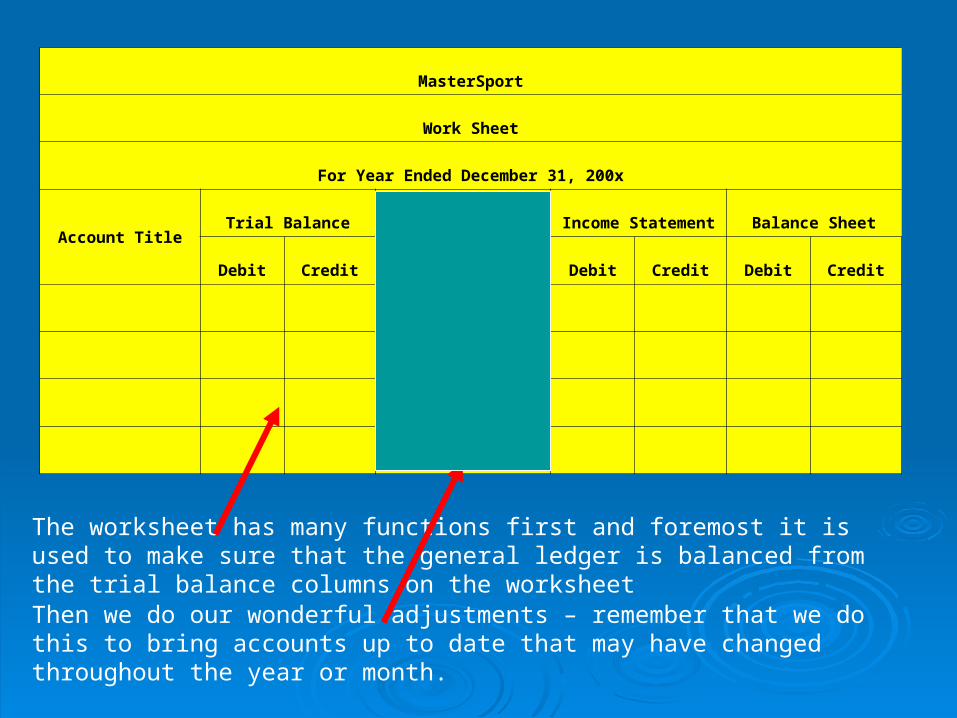

MasterSport

Work Sheet

For Year Ended December 31, 200x

Account TitleTrial Balance Adjustments Income Statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit

The worksheet has many functions first and foremost it is used to make sure that the general ledger is balanced from the trial balance columns on the worksheet

Then we do our wonderful adjustments – remember that we do this to bring accounts up to date that may have changed throughout the year or month.

Just what you wanted some more Just what you wanted some more adjustmentsadjustments

Uncollectible Accounts expense Uncollectible Accounts expense Adjustment- sometimes items are sold on Adjustment- sometimes items are sold on account to customers who later cannot be account to customers who later cannot be collected from customers are business collected from customers are business expenses. expenses.

From past experience that approximately From past experience that approximately 1% of the total sales on account will be 1% of the total sales on account will be uncollectibleuncollectible

Because people have not paid us it Because people have not paid us it becomes an expense to us at the end of becomes an expense to us at the end of the year. the year.

We also have to add it to the amount in We also have to add it to the amount in which we allow not to be collected for the which we allow not to be collected for the year. year.

Review of adjustments and there Review of adjustments and there corresponding accountscorresponding accounts

Allowance for Allowance for uncollectible accountsuncollectible accounts

Merchandise Merchandise Inventory – golf, Inventory – golf, tennistennis

Supplies – office, Supplies – office, storestore

Accumulated Accumulated Depreciation – store, Depreciation – store, office equipmentoffice equipment

Uncollectible Uncollectible accounts expenseaccounts expense

Income summary –Income summary –golf, tennisgolf, tennis

Supplies expense – Supplies expense – office, storeoffice, store

Depreciation expense Depreciation expense – store, office – store, office equipmentequipment

The only adjustment that is a little The only adjustment that is a little different is Federal income tax different is Federal income tax

expenseexpense We usually work from the top to the We usually work from the top to the

bottom of the worksheet, but this time we bottom of the worksheet, but this time we work from the bottom to the bottom. work from the bottom to the bottom.

Federal Income Tax ExpenseFederal Income Tax Expense Federal income tax payableFederal income tax payable Please look with me on page 104-105Please look with me on page 104-105

Why the worksheetWhy the worksheet

1.1. Check the balance of the general ledgerCheck the balance of the general ledger

2.2. Bring up to date accounts- using Bring up to date accounts- using adjustmentsadjustments

3.3. Determine what goes on what sheet- Determine what goes on what sheet- Income statement, balance sheet (does Income statement, balance sheet (does the income summary account remind you the income summary account remind you of anything?of anything?

4.4. Determine net income.Determine net income.

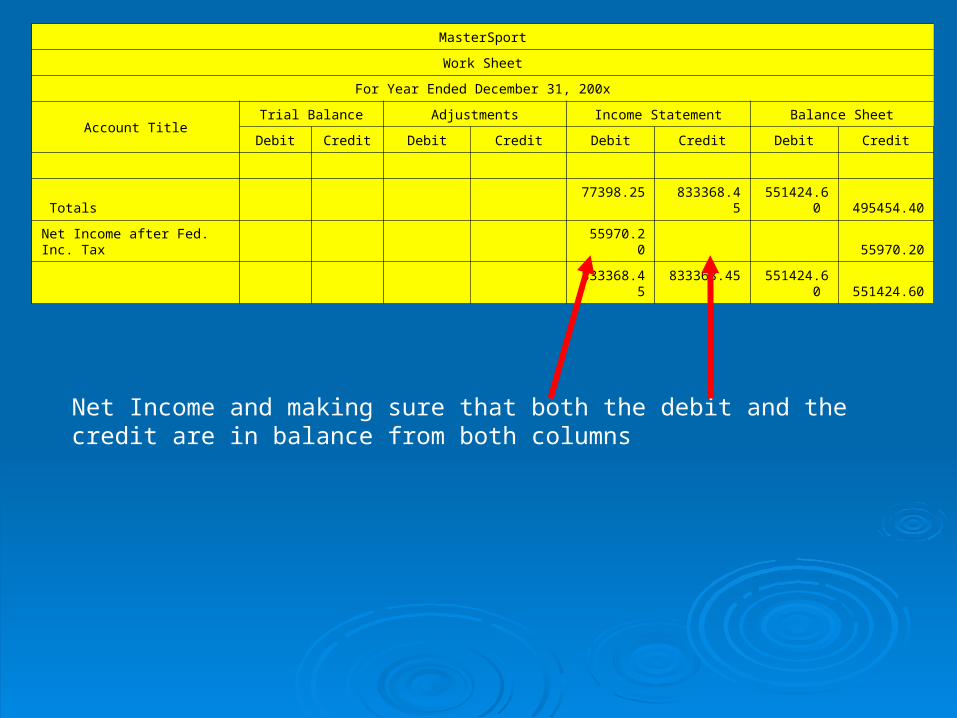

MasterSport

Work Sheet

For Year Ended December 31, 200x

Account TitleTrial Balance Adjustments Income Statement Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit

Totals 77398.25 833368.45 551424.60 495454.40

Net Income after Fed. Inc. Tax 55970.20 55970.20

833368.45 833368.45 551424.60 551424.60

Net Income and making sure that both the debit and the credit are in balance from both columns

4-3 Financial Statements for a 4-3 Financial Statements for a Departmentalized BusinessDepartmentalized Business

The 4 financial statements that you will The 4 financial statements that you will prepareprepare Departmental Statement of Gross ProfitDepartmental Statement of Gross Profit Income StatementIncome Statement Statement of Stockholders’ EquityStatement of Stockholders’ Equity Balance sheetBalance sheet

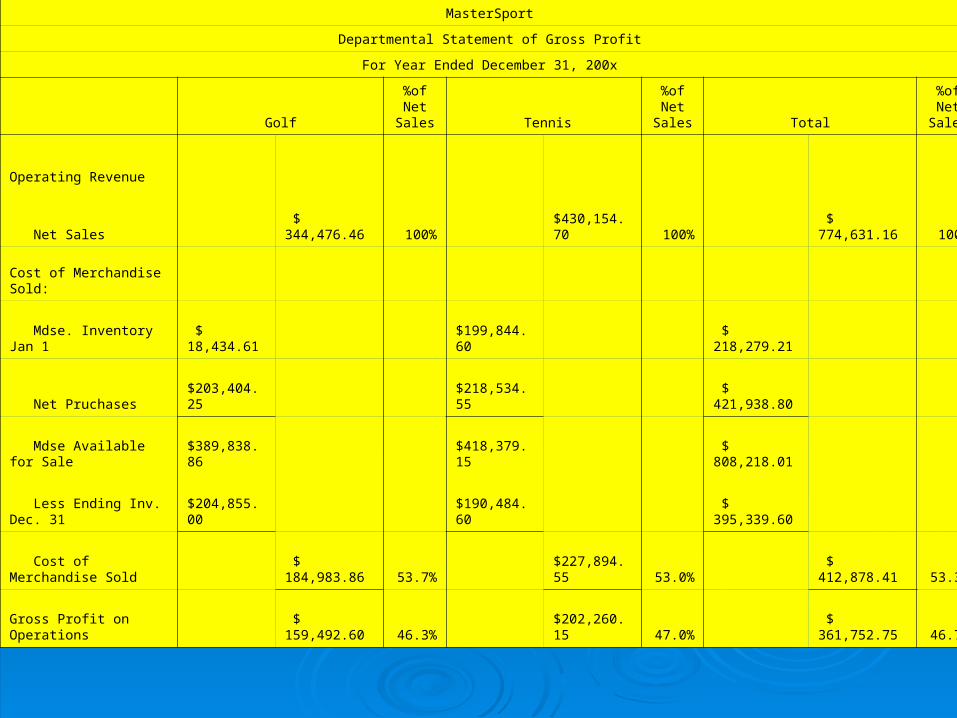

Departmental Statement of Gross Departmental Statement of Gross ProfitProfit

Used to help us determine the actual Used to help us determine the actual ending periodic inventories for each ending periodic inventories for each departmentdepartment

MasterSport

Departmental Statement of Gross Profit

For Year Ended December 31, 200x

Golf

%of Net

Sales Tennis

%of Net

Sales Total

%of Net

Sales

Operating Revenue

Net Sales $ 344,476.46 100% $430,154.70 100% $ 774,631.16 100%

Cost of Merchandise Sold:

Mdse. Inventory Jan 1 $ 18,434.61 $199,844.60 $ 218,279.21

Net Pruchases $203,404.25 $218,534.55 $ 421,938.80

Mdse Available for Sale $389,838.86 $418,379.15 $ 808,218.01

Less Ending Inv. Dec. 31 $204,855.00 $190,484.60 $ 395,339.60

Cost of Merchandise Sold $ 184,983.86 53.7% $227,894.55 53.0% $ 412,878.41 53.3%

Gross Profit on Operations $ 159,492.60 46.3% $202,260.15 47.0% $ 361,752.75 46.7%

Income statementIncome statement

Please look on page 114 Please look on page 114 Remember that the bottom line needs to Remember that the bottom line needs to

match the bottom line on the worksheet. match the bottom line on the worksheet. You are also using the Statement of gross You are also using the Statement of gross

profit to fill in some of the blanks but also to profit to fill in some of the blanks but also to help check your numbers.help check your numbers.

For example: net sales should equal what For example: net sales should equal what you have on your statement of gross profit. you have on your statement of gross profit.

Statement of Stockholders EquityStatement of Stockholders Equity

2 major sections2 major sections Capital StockCapital Stock

• Total shares of ownership in a corporations.Total shares of ownership in a corporations. Retained EarningsRetained Earnings

• An amount earned by a corporation and not yet An amount earned by a corporation and not yet distributed to stockholdersdistributed to stockholders

MasterSport

Statement of Stockholders Equity

For Year Ended December 31, 200x

Capital Stock:

$170.00 Per Share

January 1, 20-- 2,000 shares Issued $340,000.00

Issued during Current Year, None $ -

Balance December 31, 200x, 200 shares Issued $340,000.00

Retained Earnings:

Balance January 1, 200x $ 42,210.50

Net Income after Federal income tax for 200x $55,970.20

Less Dividends Declared during 200x $30,000.00

Net Increase during 200x $ 25,970.20

Balance, December 31, 200x $ 68,480.70

Total Stockholders Equity December 31, 200x $408,180.70

This is the number that we use to carry over to the Balance Sheet

3 more things to do to end out the 3 more things to do to end out the fiscal period.fiscal period.

Adjusting entriesAdjusting entries Remember those entries are exactly like what Remember those entries are exactly like what

we do on the worksheet.we do on the worksheet. Closing EntriesClosing Entries

This is new for us.This is new for us. Let look at what we need to do with this. Let look at what we need to do with this.

Closing Entries from accounting IClosing Entries from accounting I

1.1. Close all of the Credit Side Close all of the Credit Side accounts in the Income accounts in the Income Statement column to Income Statement column to Income Summary accountSummary account

2.2. Close all of the Debit Side Close all of the Debit Side accounts in the Income accounts in the Income Statement column to the Income Statement column to the Income Summary accountSummary account

3.3. Close the Income Summary Close the Income Summary Account to the Account to the Capital AccountCapital Account

4.4. CloseClose DrawingDrawing Account to the Account to the CapitalCapital AccountAccount

1.1. Close all of the Credit Side Close all of the Credit Side accounts in the Income accounts in the Income Statement column to Statement column to Income Income Summary-General accountSummary-General account

2.2. Close all of the Debit Side Close all of the Debit Side accounts in the Income accounts in the Income Statement column to Statement column to Income Income Summary-General accountSummary-General account

3.3. Close the Income Summary Close the Income Summary Account to the Account to the Retained Retained Earnings Earnings

4.4. Close Close DividendDividend Account to the Account to the Retained EarningsRetained Earnings Account Account

Accounting I Accounting II

Post-Closing Trial BalancePost-Closing Trial Balance

This is to make sure that all of the This is to make sure that all of the accounts that we have open are in accounts that we have open are in balance and ready for the next fiscal balance and ready for the next fiscal period. period.

Please look on page 122Please look on page 122

Here it is……Here it is……

Problems 4-1,2,3,4,5,6,8Problems 4-1,2,3,4,5,6,8 Computer Problem 4-7 (you must have 4-5 Computer Problem 4-7 (you must have 4-5

done before you can do( 4-7)done before you can do( 4-7)