chapter 2 companies and corporate regulation. lecture topics characteristics of a company types of...

TRANSCRIPT

Chapter 2 Chapter 2

Companies and Corporate Companies and Corporate

RegulationRegulation

Chapter 2 Chapter 2

Companies and Corporate Companies and Corporate

RegulationRegulation

Lecture TopicsLecture Topics

• Characteristics of a company• Types of companies and other regulated

entities• Historical evolution of the company and

corporate regulation• The Corporations Act and regulation of

financial reporting

Lecture TopicsLecture Topics

• Evolution of financial reporting requirements

• Other sources of authority in company accounting

• The thrust of legislative reforms

Lecture ReferencesLecture References

• Text - Chapter 2 • Corporations Act 2001

Key ConceptsKey Concepts

• Separate legal identity• Shares• Limited liability company• No liability company• Unlimited liability• Public and proprietary companies

Characteristics of a CompanyCharacteristics of a Company

• Legal personality• Limited liability• Ownership by shares• Perpetual succession• Ability to raise capital• Professional management

Types of CompaniesTypes of Companies

• Size of ownership– public company– proprietary company– small proprietary company

Types of CompaniesTypes of Companies

• Mode of participation– share company– guarantee company

• Extent of liability– limited liability– no liability– unlimited liability

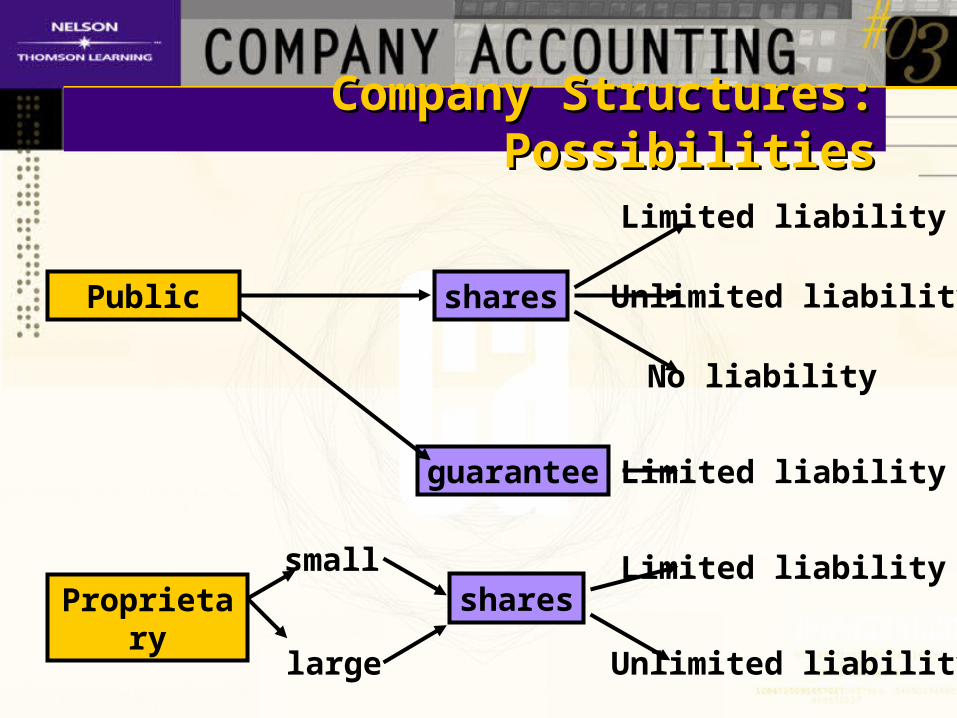

Company Structures: PossibilitiesCompany Structures: Possibilities

Public

Proprietary

shares

guarantee

Limited liability

Unlimited liability

No liability

Limited liability

small

large

Limited liability

Unlimited liability

shares

Types of CompaniesTypes of Companies

• Special types– investment– banking– life insurance– foreign

Other Forms of Regulated EntitiesOther Forms of Regulated Entities

• Managed investment schemes• Corporations formed by an Act of

Parliament• Disclosing entities

– enhanced disclosure securities– continuous disclosure requirements

Evolution of Companies and Evolution of Companies and Corporate RegulationCorporate Regulation

• Uncommon until late 19th century• Based on British system• Mainly restricted to govt./quasi-govt. and

religious organisations• Early concern over fraud and manipulation• Limited liability -> UK 1855

Evolution of Corporate RegulationEvolution of Corporate Regulation

• Australia– initially administered by states

• no uniformity until 1960’s• Uniform Companies Act

– National Cooperative Scheme (1981)• National Companies and Securities Commission

– Corporations Act 1989 and the Corporations Law

Evolution of Corporate RegulationEvolution of Corporate Regulation

• Present company law scheme– Corporations Act 2001

• effective 16 July 2001• federal legislation

– Corporations Regulations– Related legislation– Australian Securities and investment

Commission (ASIC)

Corporations Act and Financial Corporations Act and Financial ReportingReporting

• Recording of financial data• Compulsory reports• AASB standards

– carry ‘force of law’– nature and role of AASB– entities regulated by AASBs

Corporations Act and Financial Corporations Act and Financial ReportingReporting

• AASB standards– mandatory standards and a ‘true and fair view’– accounting standards with the force of law

• Framework for development of AASB– role of FRC and the AASB– Development of a conceptual framework– Due process

Corporations Act and Financial Corporations Act and Financial ReportingReporting

• Enforcement of reporting requirements– Enforcement of Accounting Standards

• embodied in the Law• non-compliance a breach• auditors must advise ASIC• ASIC can enforce

– Enforcement of other financial reporting-related requirements

Other Authority for Financial Other Authority for Financial ReportingReporting

• Urgent Issues Group abstracts – established within AARF in 1994– numerous abstracts– mandatory compliance

• Statements of Accounting Concepts– SACs 1-4– non mandatory

Other Authority for Financial Other Authority for Financial ReportingReporting

• Accounting Guidance Releases– advisory only– clarify accounting standards

• Accounting Bulletins– issued by AARF– provide guidance

Other Authority for Financial Other Authority for Financial ReportingReporting

• International Accounting Standards– IASC and IOSCO– International harmonisation– AASB and G4 + 1

• Australian Stock Exchange (ASX)• ASIC practice notes, policy statements and

class orders

IAS Standards

AASB Standards

UIG Abstracts

International Accounting Standards Committee

International Accounting Standards Committee

AustralianAccounting Standards

Board

AustralianAccounting Standards

Board

Standing Interpretation Committee

Standing Interpretation Committee

SICs

Urgent IssuesGroup

Urgent IssuesGroup

Accounting Interpretations

Accounting Bulletins

15 Day Disallowance

15 Day Disallowance

Evolution of Australian Financial Evolution of Australian Financial ReportingReporting

• The role of the accounting profession– regulation of financial reporting practice– non-mandatory statements of best practice– mandatory professional technical standards

Evolution of Australian Financial Evolution of Australian Financial ReportingReporting

• The role of legislation– the ASRB– AAS’s vs AARB accounting standards– the Corporations law and the AASB

• References to standards

Thrust of Legislative ReformsThrust of Legislative Reforms

• Streamlining reporting requirements• Specification in Accounting Standards

rather than the law• Simplification of corporate administration• Differential reporting requirements• Reorganisation of legal provisions

Thrust of Legislative ReformThrust of Legislative Reform

• Changes to corporate governance• 1st Corporations Law Simplification Act

1995• Company Law Review Act 1998• Corporations Act 2001

Where to get more informationWhere to get more information

• Other courses• List books, articles, electronic sources