chapter 15 monopoly. objectives 1.) learning the source of monopoly 2.) understand how a monopolist...

TRANSCRIPT

Chapter 15

Monopoly

Objectives1.) Learning the source of monopoly

2.) Understand how a monopolist sets price and output to maximize profits

3.) Evaluate the efficiency of monopoly

4.) Learn some of the various public policies toward a monopoly

5.) Understand how and why a monopolist would price discriminate

MONOPOLY Monopoly is a market structure

characterized by

1. One seller

2. Homogeneous product

3. Very much control over price(pricemaker)

4. Very great difficulty in entering or exiting the market .

Monopoly

A Pure Monopoly exists when a single firm is the only producer or seller of a product that has no close substitute.

Why Learn About Monopolies?

It is estimated that about five (5) percent of domestic output issupplied under monopoly conditions

It helps to understand morecommon market structures suchas monopolistic competition and oligopoly.

Why Monopolies Arise The fundamental cause of a monopoly

is Barriers to Entry.

Monopoly: Barriers to Entry

Ownership of Key Resource

Monopoly: Barriers to Entry

Ownership of Key Resource

Legal Barriers By Government

Monopoly: Barriers to Entry

Ownership of Key Resource

Legal Barriers By Government

Large Economies of Scale

Barrier: Monopoly Resources

A single owner of an important resource

that cannot be readily duplicated,

as with some natural resources.

Government-Created Monopolies Patent and copyright laws are a major

source of government-created monopolies.

– Certain new pharmaceutical drugs

Governments also restrict entry by giving a single firm the exclusive right to sell a particular good in certain markets.

– Local cable television

Natural Monopolies An industry is a natural monopoly

when a single firm can supply a good or service to an entire market at a smaller cost than could two or more firms.

– The minimum efficient scale of one firms plant is so large that only one firm can supply the market efficiently.

Cost

Quantity of Output

Averagetotal cost

0

Economies of Scale as aCause of Monopoly

Quick Quiz!

What are the three reasons that a market might have a monopoly?

Give two examples of monopolies, and explain the reason for each.

Monopoly BehaviorMonopoly verses Competitive Firm

Monopoly Sole Producer

Downward Sloping Demand Curve

Price Setter

Reduces Price to Increase Sales

Marginal Revenue curve below demand

Monopoly BehaviorCompetitive Firm verses Monopoly

Competitive Firm One of many Horizontal Demand

Curve Price Taker Sells a lot or a little

at same price Marginal Revenue

curve is horizontal

Quantity of Output

Demand

(a) A Competitive Firm’s Demand Curve

(b) A Monopolist’s Demand Curve

0

Price

0 Quantity of Output

Price

Demand

Demand Curves for Competitive and Monopoly Firms...

Monopoly’s Revenue

Total Revenue: Q x P = TR Average Revenue: TR ÷ Q = AR Marginal Revenue: TR ÷ Q = MR A monopolist’s Marginal Revenue is

always less than the price of its good, because of the downward sloping demand curve.

The Marginal-Revenue curve lies below its demand curve.

Price

1

2

3

4

5

6

7

8

9

10

1 2 3 4 5 6 7 8 9 10

$P1110

9876543210

Q0123456789

1011

$TR0

10182428303028241810

0

$MRN/A

1086420

-2-4-6-8

-10

Quantity

MarginalRevenue

Demand

Quality Price TotalRevenue

AverageRevenue

Marginal Revenue

12345678

Total, Average, and Marginal Revenue for a Competitive Firm

Q P (TR=P*Q) (AR=TR/Q)

$66666666

$612182430364248

$66666666

$66666666

gallon

(MR= TR / Q)

Demand

MarginalRevenue

$

inelasticportion

$

elasticportion

Quantity

Quantity

TotalRevenue

along the elasticalong the elasticportion of theportion of thedemand curve, demand curve, lower prices andlower prices andgreater quantitiesgreater quantitiesresult in risingresult in risingtotal revenuetotal revenue

along the inelasticalong the inelasticportion of theportion of thedemand curve,demand curve,lower prices andlower prices andgreater quantitiesgreater quantitiesresult in decliningresult in decliningtotal revenuetotal revenue

Monopoly’s Marginal Revenue

When a monopoly drops price to sell more product, the additional revenue received from previous amounts sold will decrease.

Two effects on revenue when price is dropped:

–The Output Effect

–The Price Effect

Profit Maximization of a Monopoly

The monopolist’s profit-maximizing quantity of output is determined by the intersection of the Marginal-Revenue curve and the Marginal-Cost curve.

Same rule of profit maximization as perfectly competitive firm

MR = MC

Monopoly’s Profit Maximization

Price

Quantity

D

MR

Monopoly’s Profit Maximization

Price

Quantity

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

MR=MC

MC = Supply

D

MR

Profit Maximization of a Monopoly

In competitive markets, price equals marginal cost. In Monopolized markets, price exceeds marginal cost.

– As long as Average Total Cost is below the monopolist’s price, economic profits will be earned.

Monopoly’s Profit Maximization Price

Price

Quantity

MC = Supply

D

MR

Monopoly’s Profit Maximization Price

Price

Quantity

PM

QM

MC = Supply

D

MR

Price consistent with profit

maximizing quantity

Profit Maximization of a Monopoly

In competitive markets, price equals marginal cost. In Monopolized markets, price exceeds marginal cost.

– As long as Average Total Cost is below the monopolist’s price, economic profits will be earned.

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Monopoly Price

Monopoly Quantity

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Monopoly Average Cost

Curve

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Monopoly Profit!

MC = Supply

D

MR

Comparing Monopoly and Competition

For a competitive firm, price equals marginal cost.

P = MR = MC For a monopoly firm, price exceeds

marginal cost.

P > MR = MC

A Monopoly’s Profit

Profit equals total revenue minus total costs.

Profit = TR - TC

Profit = (TR/Q - TC/Q) x Q

Profit = (P - ATC) x Q

Quick Quiz!

Explain how a monopolist chooses the quantity of output to produce and the price to charge.

The Welfare Cost of Monopoly

A monopoly leads to an inefficient allocation of resources, leading to a failure to maximize total economic well-being,

The monopolist produces less than the socially efficient quantity of output.

The Welfare Cost of Monopoly

At monopoly prices, some potential consumers value the good at more than its marginal cost but less than the monopolist’s price.

These consumers do not end up buying the good.

Monopoly pricing prevents some mutually beneficial trades from taking place.

The Welfare Cost of Monopoly: Deadweight Loss

Because a monopoly sets price above MC it places a wedge, similar to a tax.

The wedge causes the quantity sold to fall short of the social optimum.

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Monopoly Price

Monopoly Quantity

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Efficient Quantity!

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

MC = Supply

D

MR

Monopoly’s Profit Maximization

Price

Quantity

PM

QM

Monopoly Deadweight Loss

MC = Supply

D

MR

Monopolistic Deadweight Loss: Example

Cable TV market. Assume:– Competitive Market Price = $15

– Monopolist Market Price = $25

– Marginal Cost = $5

Deadweight loss to society is $10:– Consumer does not value cable TV at

more than its cost. Hence the consumer will not subscribe to cable TV.0

The Market for Drugs...

Costs and Revenue

Price during patent

lifePrice after

patent expires

Monopoly quantity

Competitive quantity

0 Quantity

Demand

Marginal cost

Marginal revenue

Public Policy Toward Monopoly: Government may intervene by. . .

Creating a competitive market

Implement/Enforce Anti-Trust Laws

Regulating the behavior of monopolies

Price control and regulation

Public Ownership

Government runs the monopoly itself

Doing Nothing

Loss

Marginal-Cost Pricing for aNatural Monopoly

Price

Quantity0

Marginal cost

Average total cost

Demand

Regulatedprice

Quick Quiz!

Describe the ways policymakers can respond to the inefficiencies caused by monopolies.

List a potential problem with each of these policy responses.

Price Discrimination: Monopoly Tool

The practice of selling the same good to different customers at different prices.

– Not possible in a competitive market.

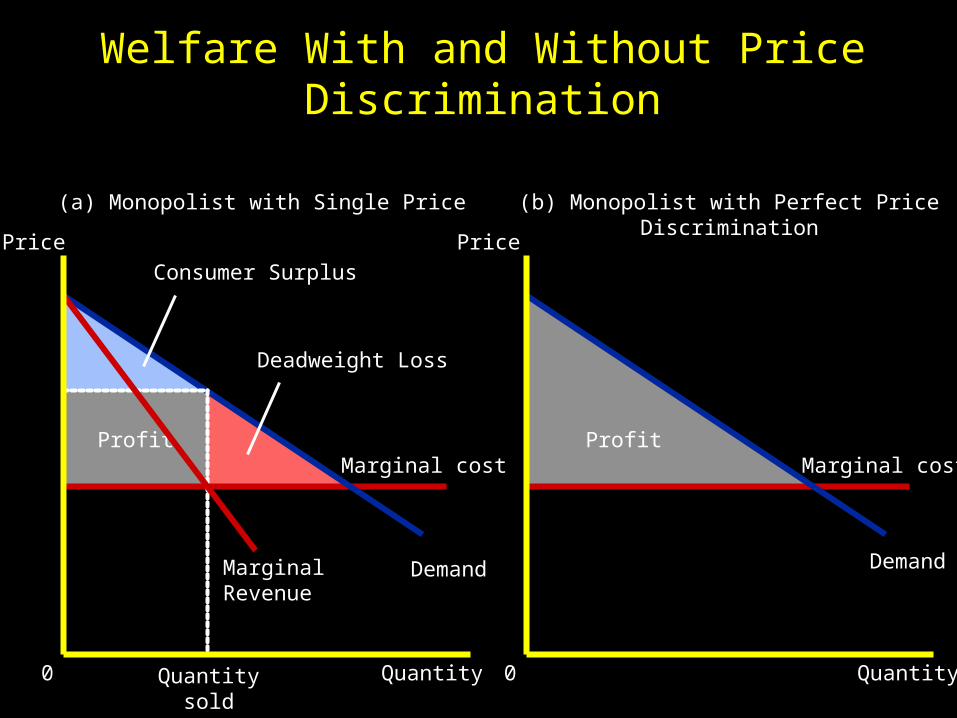

Two Important Effects:

– Can increase the monopolist’s profits

– Can reduce deadweight loss

A Parable About Pricing (Figure 15-10)

Profit Profit

Welfare With and Without Price Discrimination

Price

Quantity Quantity

Price

Marginal cost

DemandDemand

Marginal cost

Deadweight Loss

Consumer Surplus

MarginalRevenue

Quantitysold

0 0

(a) Monopolist with Single Price (b) Monopolist with Perfect PriceDiscrimination

Examples: Price Discrimination

Movie Tickets, i.e., children, adult, senior Citizens

Airline Tickets, i.e., first class, coach, stay over, one-way verses round-trip

Discount Coupons

Financial Aid

Two-Part Tariff, i.e., amusement park entrance fee, and then a fee for each ride

The Prevalence of Monopoly

How prevalent are the problems of monopolies?

Monopolies are common. Most firms have some control over their

prices because of differentiated products. Firms with substantial monopoly power

are rare. Few goods are truly unique.

Quick Quiz! Give two examples

of price discrimination.

How does perfect price discrimination affect consumer surplus, producer surplus, and total surplus?

The Prevalence of Monopoly How prevalent are the problems of

monopolies?– Monopolies are common. Most firms

have some control over the prices because of differentiated products. Ben & Jerry’s Ice Cream vs Breyer’s

– Firms with substantial monopoly power are rare. Few goods are truly unique.

Summary

A monopoly is a firm that is the sole seller in its market.

It faces a downward-sloping demand curve for its product.

A monopoly’s marginal revenue is always below the price of its good.

Summary

Like a competitive firm, a monopoly maximizes profit by producing the quantity at which marginal cost and marginal revenue are equal.

Unlike a competitive firm, its price exceeds its marginal revenue, so its price exceeds marginal cost.

Summary

A monopolist’s profit-maximizing level of output is below the level that maximizes the sum of consumer and producer surplus.

A monopoly causes deadweight losses similar to the deadweight losses caused by taxes.

Summary

Policymakers can respond to the inefficiencies of monopoly behavior with antitrust laws, regulation of prices, or by turning the monopoly into a government-run enterprise.

If the market failure is deemed small, policymakers may decide to do nothing at all.

Summary

Monopolists can raise their profits by charging different prices to different buyers based on their willingness to pay.

Price discrimination can raise economic welfare and lessen deadweight losses.