chapter 15 evaluating sales force performance. the sales audit...a comprehensive, periodic review...

TRANSCRIPT

CHAPTER 15

Evaluating Sales force Performance

THE SALES AUDIT

• ...a comprehensive, periodic review and evaluation of the sales function

THE SALES AUDIT

• The audit includes an appraisal of– objectives– personnel– tactics

STEPS IN THE SALES AUDIT

• Find out what happened

• Find out why it happened

• Decide what to do about it

EVALUATING EFFECTIVENESS

• Sales Volume Analysis

• Cost Analysis

• Profitability Analysis

• Productivity Analysis

SALES VOLUME ANALYSIS

• A study of the net sales section of the profit and loss statement.

• Examine sales by product lines, territories, key accounts, and general classes of customers.

SALES VOLUME ANALYSIS

• Two approaches:– Hierarchical Sales Analysis– Effectiveness Analysis

HIERARCHICAL SALES ANALYSIS

• A multistage analysis which proceeds from one sales organization level to the next by – identifying major deviations – investigating these in more detail at the

next lower level.

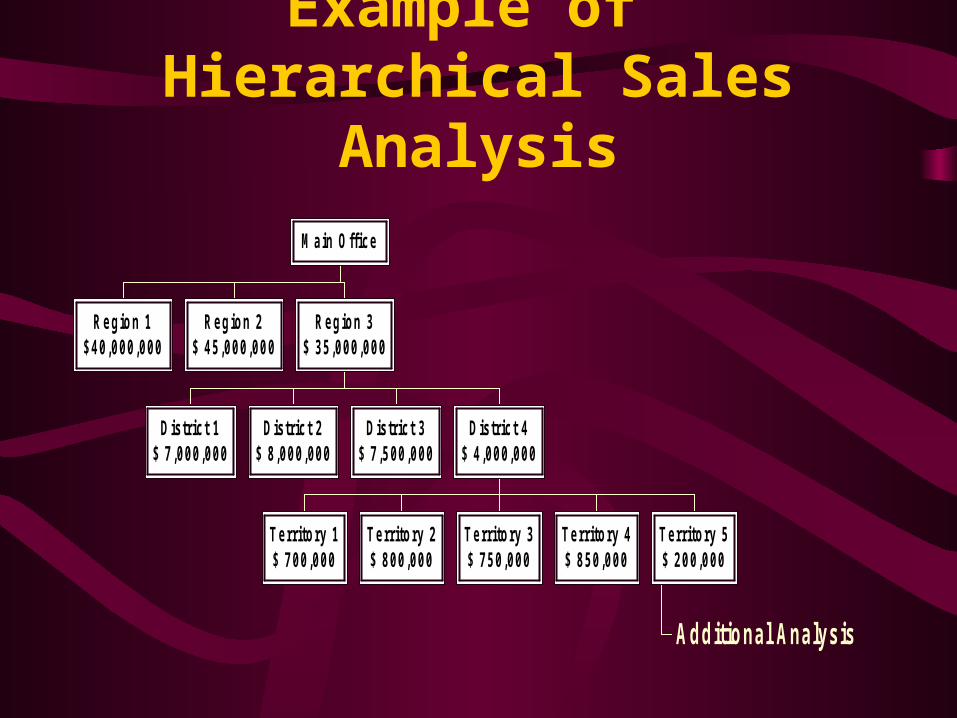

Example of Hierarchical Sales Analysis

Region 1$40,000,000

Region 2$ 45,000,000

District 1$ 7,000,000

District 2$ 8,000,000

District 3$ 7,500,000

T erritory 1$ 700,000

T erritory 2$ 800,000

T erritory 3$ 750,000

T erritory 4$ 850,000

Additional Analysis

T erritory 5$ 200,000

District 4$ 4,000,000

Region 3$ 35,000,000

M ain Office

EFFECTIVENESS INDEX

• Examine territory performance relative to potential

STEPS IN AN EFFECTIVENESS ANALYSIS

Select a market index that indicates what percentage of total sales should be obtained from each sales territory.

STEPS IN AN EFFECTIVENESS ANALYSIS

Determine the company’s actual total sales in dollars or units during the period being studied.

STEPS IN AN EFFECTIVENESS ANALYSIS

Multiply the territorial index by the total sales figure to determine the goal in each district.

STEPS IN AN EFFECTIVENESS ANALYSIS

Compare actual regional sales with the regional goals to see how much variation has occurred.

Example Effectiveness Analysis

Region MarketIndex

ActualSales

SalesGoals

% DollarVariance

A 27% $900 $1,215 74% $-315

B 22% 1,230 990 124 240

C 15% 828 675 123 153

D 20% 852 900 95 -48

E 16% 690 720 96 -30

Total $4,500

HIERARCHICAL AND EFFECTIVENESS ANALYSIS

• Territories

• Different products

• Sales by accounts

• Channels of distribution

MARKETING COST ANALYSIS

• A study of marketing expenses to determine profitability of marketing segments in the firm.

• Two Approaches– Variance Analysis– Percentage of Sales

VARIANCE ANALYSIS• Variance represents the difference

between actual costs and budgeted costs.

• High variances should be examined further.

PERCENTAGE OF SALES• Examines costs as a percentage of

sales.

PROFITABILITY ANALYSIS

• Return on Assets Managed (ROAM)

RETURN ON ASSETS MANAGED (ROAM)

• Measures how productively the assets in each segment of the business have been employed.

ROAM= Profit contribution/Assets Managed

ROAM Example

District 1 District 2 District 3

Sales $ 12,000,000 $ 12,000,000 $12,000,000

COGS 6,000,000 6,000,000 7,000,000

Gross Margin 6,000,000 6,000,000 5,000,000

Selling Expenses 3,600,000 4,800,000 2,600,000

Profit Contr’n 2,400,000 1,200,000 2,400,000

Acc’ts Receivable 4,000,000 2,000,000 8,000,000

Inventory 4,000,000 2,000,000 8,000,000

Assets Managed 8,000,000 4,000,000 16,000,000

Profit Contr’n % 20% 10% 20%

Asset Turnover 1.5 3.0 .75

ROAM 30% 30% 15%

PRODUCTIVITY ANALYSIS

• Additional productivity analysis may be required to get a fuller picture of organizational effectiveness.

• Measured in terms of inputs and outputs.

Example Productivity Analysis

District 1 District 2 District 3

Sales $ 10,000,000 $ 12,000,000 $ 10,000,000

Expenses 1,000,000 1,200,000 1,500,000

Sales Calls 5,000 4,500 4,500

Proposals 100 105 120

Salespeople 10 15 10

Sales/Person 1,000,000 800,000 1,000,000

Expenses/Person 100,000 80,000 150,000

Calls/Person 500 300 450

Proposals/Person 10 7 12

WHAT IS DONE WITH THIS INFORMATION?

• Adjust territorial boundaries

• Adjust product line

• Change classes of customers

FROM THE TEXT

• Read everything except Residual Income Analysis on pages 724 to 726.