chapter 13 homework

DESCRIPTION

Chapter 13 HOMEWORK. Exercise 13-3. Clemens County had the following revenue sources in 20X5: Required:Prepare a schedule computing the amount of general revenues and of program revenues that Clemens County should report in its government-wide statement of activities for the 20X5 - PowerPoint PPT PresentationTRANSCRIPT

Clemens County had the following revenue sources in 20X5:

Required: Prepare a schedule computing the amount of general revenuesand of program revenues that Clemens County should reportin its government-wide statement of activities for the 20X5fiscal year.

GENERAL PROPERTY TAXES…………..$8,000,000

•INCLUDES all taxes imposed, even those levied for a specific purpose. They are reported by TYPE OF TAX.

Restricted (for education) PROPERTY TAXES………. $570,000

Meals tax (restricted for economic development and tourism)….. $200,000

Fines and forfeits……….. $82,000

Federal Grant restricted for police protection……… $132,000

Federal Grant restricted for specific general government constructionprojects for specific functions………… $600,000

Unrestricted Investment Income………….. $75,000

$8,845,000$8,845,000 $814,000$814,000

The total of gr and pr

The following information was drawn from the accounts and records ofMosser Township:

Required: Prepare a schedule computing the amounts to be reported in eachof the three minimum program revenue classifications by Mosser Township.

CHARGES FOR SERVICES: Revenues from charges to customers, applicants,or others who purchase, use, or directly benefitfrom the goods, services, or privileges providedor are otherwise directly affected by the services.

OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

LOCAL GAS TAX RESTRICTED TO STREET MAINTENANCE

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

LOCAL GAS TAX RESTRICTED TO STREET MAINTENANCE

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

GRANT FROM STATE FOR WIDENINGAND REPAVING MAIN STREET

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

GRANT FROM STATE FOR WIDENINGAND REPAVING MAIN STREET

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

UNRESTRICTED CHARGES FOR AMBULANCESERVICES PROVIDED BY FIRE DEPARTMENT

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONSUNRESTRICTED CHARGES FOR AMBULANCE

SERVICES PROVIDED BY FIRE DEPARTMENT

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

CONTRIBUTIONS FROM LOCAL BUSINESSES-RESTRICTED FOR YOUTH RECREATIONPROGRAMS

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

CONTRIBUTIONS FROM LOCAL BUSINESSES-RESTRICTED FOR YOUTH RECREATIONPROGRAMS

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

INCOME FROM PERMANENT FUND ENDOWMENTRESTRICTED TO ECONOMIC DEVELOPMENTPURPOSES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

INCOME FROM PERMANENT FUND ENDOWMENTRESTRICTED TO ECONOMIC DEVELOPMENTPURPOSES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FINES THAT ARE UNRESTRICTED AS TO USE

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FINES THAT ARE UNRESTRICTED AS TO USE

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

PROPERTY TAXES RESTRICTEDFOR EDUCATION PURPOSES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

PROPERTY TAXES RESTRICTEDFOR EDUCATION PURPOSES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

SHARED REVENUES FROM THESTATE- RESTRICTED FOR EDUCATION

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

SHARED REVENUES FROM THESTATE- RESTRICTED FOR EDUCATION

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FEDERAL GRANT REVENUES- RESTRICTEDFOR HIRING POLICEMEN

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FEDERAL GRANT REVENUES- RESTRICTEDFOR HIRING POLICEMEN

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FEDERAL GRANT TO REPLACE WATER ANDSEWER LINES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

FEDERAL GRANT TO REPLACE WATER ANDSEWER LINES

CHARGES FOR SERVICES: OPERATING GRANTSAND CONTRIBUTIONS

CAPITAL GRANTS AND CONTRIBUTIONS

$281,000$1,825,000

$9,000,000

Dorrian County’s fund structure is as follows:

General Fund3 Special Revenue Funds1 Capital Projects Fund2 Debt Service Funds4 Private Purpose Trust Funds3 Internal Service Funds5 Enterprise Funds

GCA and GLTL accounts

Assume that Dorrian Countydetermines that Special RevenueFund A, its Capital Projects Fund,Enterprise Fund C, and EnterpriseFund D are its only major funds.

(a) What column headings would the county need to present in its GovernmentalGovernmentalFundsFunds statement of Revenues, Expenditures and Changes in Fund Balance?

1) A column for the GENERAL FUND

2) A column for EACH MAJOR FUND

4) A total column

GENERAL FUND SPECIAL REV. FUND A CAPITAL PROJECTS OTHER GOV TOTAL

3) An OTHER GOV column for total of nonmajor funds.

(a) What column headings would the county need to present in its GovernmentalGovernmentalFundsFunds statement of Revenues, Expenditures and Changes in Fund Balance?

1) A column for EACH MAJOR FUND

3) A total column

FUND C FUND D OTHER FUNDS TOTAL INTERNAL SERVICE

2) An OTHER column for total of nonmajor funds.

4) An Internal Service Column

(a) What column headings would the county need to present in its ProprietaryProprietaryFundsFunds statement of Revenues, Expenditures and Changes in Fund Balance?

Prepare the NET ASSETS section for GOVERNMENTAL ACTIVITIESin the GOVERNMENT-WIDE Statement of Net Assets for the city of Josiah atJune 30, 20X6, given the following information as of that date.

THE NET ASSETS SECTION IS MADE UP OF?

Invested in capital assets, net of related debt

Restricted net assets

Unrestricted net assets

Answer:

NET ASSETS:

Invested in capital assets, net of related debt…………….. $4,925,000

Restricted for: Debt Service………………………………… $2,000,000 Capital Projects ($400,000 - $300,000) 100,000 Specific Programs………………………….. 2,000,000 4,100,000

Unrestricted…………………………………………….. 7,175,000

Total Net Assets……………………………………. $16,200,000

Answer:

NET ASSETS:

Invested in capital assets, net of related debt…………….. $4,925,000

Restricted for: Debt Service………………………………… $2,000,000 Capital Projects ($400,000 - $300,000) 100,000 Specific Programs………………………….. 2,000,000 4,100,000

Unrestricted…………………………………………….. 7,175,000

Total Net Assets……………………………………. $16,200,000

Find UNRESTRICTED: Begin with adding up all the GOVERNMENTAL FUNDBALANCES whether restricted or not.

GF… $8M + SRF (rest) $2M + CPF (1/2 rest) $800K + DSF (rest) $2M = $12,800,000$12,800,000

Begin with adding up all the GOVERNMENTAL FUND BALANCES whetherrestricted or not.

Now take out any liabilitiesliabilities and/or restrictionsrestrictions related to these fund balances

- SRF all restricted……………………………. $2,000,000- SRF all restricted……………………………. $2,000,000

- CPF ½ restricted…………………………….. 400,000- CPF ½ restricted…………………………….. 400,000

- DSF all restricted……………………………. 2,000,000- DSF all restricted……………………………. 2,000,000

- Long-term claims/judgments payable…. 1,750,000- Long-term claims/judgments payable…. 1,750,000

- Long-term compensated absence pay.. 750,000- Long-term compensated absence pay.. 750,000

GF… $8M + SRF (rest) $2M + CPF (1/2 rest) $800K + DSF (rest) $2M = $12,800,000$12,800,000

RESTRICTIONS

LIABILITIESOn unrestricted NA

Begin with adding up all the GOVERNMENTAL FUND BALANCES whetherrestricted or not.

Now take out any liabilitiesliabilities and/or restrictionsrestrictions related to these fund balances

- SRF all restricted……………………………. $2,000,000- SRF all restricted……………………………. $2,000,000

- CPF ½ restricted…………………………….. 400,000- CPF ½ restricted…………………………….. 400,000

- DSF all restricted……………………………. 2,000,000- DSF all restricted……………………………. 2,000,000

- Long-term claims/judgments payable…. 1,750,000- Long-term claims/judgments payable…. 1,750,000

- Long-term compensated absence pay.. 750,000- Long-term compensated absence pay.. 750,000

GF… $8M + SRF (rest) $2M + CPF (1/2 rest) $800K + DSF (rest) $2M = $12,800,000$12,800,000

RESTRICTIONS

LIABILITIESOn Unrestricted NA

Now add in INTERNAL SERVICE FUND which services only the General Fund

Equity of ISF (given).......................................... $1,900,000Equity of ISF (given).......................................... $1,900,000

-Subtract capital assets of ISF (these will get shown inSubtract capital assets of ISF (these will get shown in Capital Asset section) $3M x 3.0....................... ($900,000)Capital Asset section) $3M x 3.0....................... ($900,000)

+ Add debt related to capital assets because it will be taken+ Add debt related to capital assets because it will be taken out in Capital Asset Section $1.1M x .25............... $275,000out in Capital Asset Section $1.1M x .25............... $275,000

TOTAL UNRESTRICTEDNET ASSETS

$7,175,000$7,175,000

Calculate RestrictedRestricted Net Assets:

Begin by listing out the restricted net assets:

Special Revenue Fund…………………… $2,000,000 (all restricted)Special Revenue Fund…………………… $2,000,000 (all restricted)

Debt Service Fund………………………. $2,000,000 (all restricted)Debt Service Fund………………………. $2,000,000 (all restricted)

Restricted for CPF (other ½)……………. $400,000 (total 800K x ½)Restricted for CPF (other ½)……………. $400,000 (total 800K x ½)

Now take out any debt related to these assets

Unexpended bond proceeds *given as “*” in problemUnexpended bond proceeds *given as “*” in problemmust be subtracted from the restricted assets……… ($300,000)must be subtracted from the restricted assets……… ($300,000)The cash is in the restricted for CPF above.The cash is in the restricted for CPF above.

TOTAL RESTRICTED NET ASSETS….. $4,100,000RESTRICTED NET ASSETS….. $4,100,000

Calculate Invested in Capital Assets net of related debt.Calculate Invested in Capital Assets net of related debt.

First list out the First list out the capital assetscapital assets

General capital assets……………… +$12,000,000General capital assets……………… +$12,000,000

Subtract Subtract accumulated depreciationaccumulated depreciation

Accumulated Depreciation…………..(5,000,000)Accumulated Depreciation…………..(5,000,000)

Add in Capital Add in Capital ISFISF assets assets

$3,000,000 x .30 capital = …………..+ $900,000$3,000,000 x .30 capital = …………..+ $900,000

Subtract General LONGTERM capital debtSubtract General LONGTERM capital debt

Bonds payable…………………. ($3,000,000)Bonds payable…………………. ($3,000,000)

+ add back in the + add back in the unexpended bond proceedsunexpended bond proceeds +$300,000 +$300,000(we already added the restricted cash and subtracted(we already added the restricted cash and subtractedunexpended proceeds in the restricted section).unexpended proceeds in the restricted section).THIS part of the LTD of $3M should NOT be subtractedTHIS part of the LTD of $3M should NOT be subtractedhere.here.

Subtract the Subtract the ISF capital debtISF capital debt related to capital assets $1,100,000 x .25 = $275,000 related to capital assets $1,100,000 x .25 = $275,000

Total Invested in Capital Assets net of related debt $4,925,000Invested in Capital Assets net of related debt $4,925,000

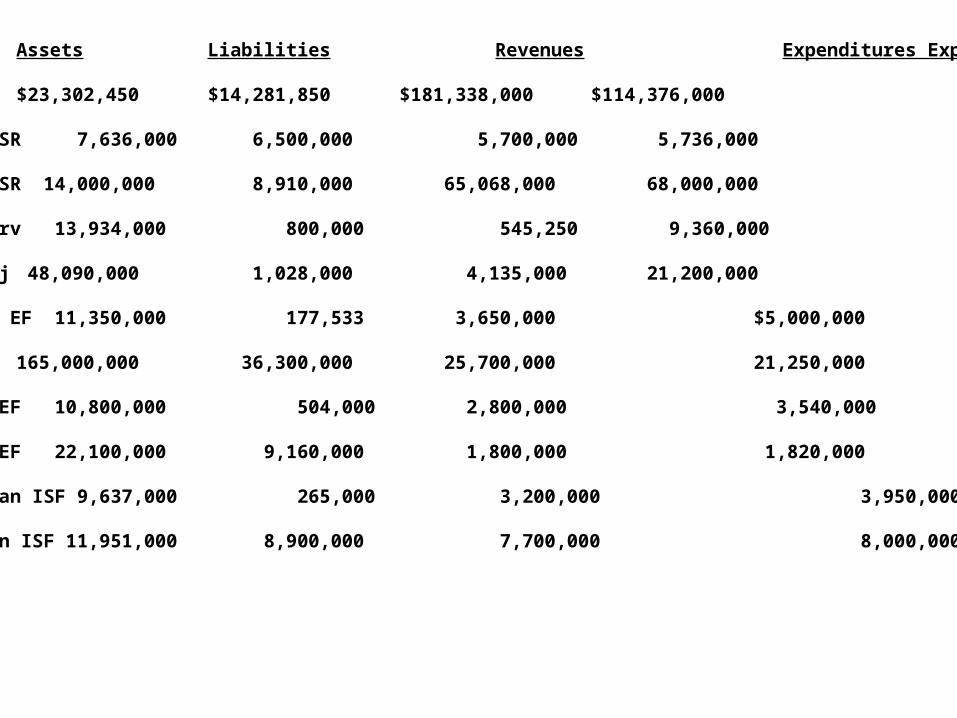

Presented in the table below is selected information from the 20X5 financialstatements of the various individual funds of Alderman City.

(a) Prepare a schedule computing the threshold amounts that shouldbe used to determine which of Alderman’s City’s funds must be reported as major funds. (b) Identify which funds are major funds.

Quantitative MAJOR FUND CRITERIAMAJOR FUND CRITERIA::1. Total assets, liabilities, revenues or expenditures/expenses

(excluding extraordinary items) of that individual governmental fund(or Enterprise Fund) are at least 10%are at least 10% of the corresponding total for allfunds of that category type.

2. The same element that met the 10% criterion in (a)is at least 5%is at least 5% of the corresponding element total forall governmental funds and enterprise funds combined.

Fund Assets Liabilities Revenues Expenditures Expenses

General $23,302,450 $14,281,850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Fund Assets Liabilities Revenues ExpendituresExpenses

General $23,302,450 $14.281,850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Column totals:

$106,962,450 $31,519,850 $256,786,250 $ $218,672,000

x .10 .10 .10 .10--------------------------------------------------------------------------------------------------------------

$10,696,245 $3,151,985 $25,678,625 $21,867,200

Fund Assets Liabilities Revenues ExpendituresExpenses

General $23,302,450 $14.281,850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Column totals:

$106,962,450 $31,519,850 $256,786,250 $ $218,672,000

x .10 .10 .10 .10--------------------------------------------------------------------------------------------------------------

$10,696,245 $3,151,985 $25,678,625 $21,867,200

(b) identify which funds of alderman city are MAJOR FUNDS.

which funds are greaterthan the thresholds?

GIVEN THIS TEST ALL GOVERNMENTAL FUNDS APPEAR TO BE MAJOR (it only takes 1 test)

But they But they must also pass the 5% test.must also pass the 5% test.

Fund Assets Liabilities Revenues ExpendituresExpenses

General $23,302,450 $14.281.850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Total 209,250,000 46,141,533 33,950,000 31,610,000

x .10 .10 .10 .10----------------------------------------------------------------------------------------------------------------------------

$20,925,000 $4,614,153 3,395,000 3,161,000

Which ones appear to be major funds for Enterprise Funds?

Again they would all appear to be not yet having done the 5% test.

2. The same element that met the 10% criterion in (a)is at least 5% of the corresponding element total forall governmental funds and enterprise funds combined.

Fund Assets Liabilities Revenues ExpendituresExpenses

General $23,302,450 $14.281.850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Total 209,250,000 E 46,141,533 E 33,950,000 E 31,610,000

x .10 .10 .10 .10----------------------------------------------------------------------------------------------------------------------------

$20,925,000 $4,614,153 3,395,000 3,161,000

2. The same element that met the 10% criterion in (a)is at least 5% of the corresponding element total forall governmental funds and enterprise funds combined.

+ 106,962,450 G -------------------- 316,212,450

+ 31,519,850 G---------------------- 77,661,383

+256,786,250 G---------------------290,736,250

+ 218,672,000 G----------------------250,282,000

x .05 .05 .05 .05

$15,810,623 $3,883,069 $14,536,813 $12,514,100

NO

NO

Fund Assets Liabilities Revenues ExpendituresExpenses

General $23,302,450 $14.281,850 $181,338,000 $114,376,000

Grants SR 7,636,000 6,500,000 5,700,000 5,736,000

School SR 14,000,000 8,910,000 65,068,000 68,000,000

Debt Serv 13,934,000 800,000 545,250 9,360,000

Cap Proj 48,090,000 1,028,000 4,135,000 21,200,000

Transit EF 11,350,000 177,533 3,650,000 $5,000,000

W&S EF 165,000,000 36,300,000 25,700,000 21,250,000

Civ CenEF 10,800,000 504,000 2,800,000 3,540,000

Pub Pk EF 22,100,000 9,160,000 1,800,000 1,820,000

Fleet Man ISF 9,637,000 265,000 3,200,000 3,950,000

Risk Man ISF 11,951,000 8,900,000 7,700,000 8,000,000

Column totals:

$106,962,450 $31,519,850 $256,786,250 $ $218,672,000

x .10 .10 .10 .10--------------------------------------------------------------------------------------------------------------

$10,696,245 $3,151,985 $25,678,625 $21,867,200

But they must also pass the 5% test.

$15,810,623

.05threshold from previous enterprise fund work.

$3,883,069 $14,536,813 $12,514,100

NO

NO

Final AnswerGovernmental Major Funds:

* General* Grants Special Revenue* School Special Revenue* Capital Projects

Enterprise Major Funds:

* Water & Sewer* Public Parks

P 13-3

P 13-3

P 13-3

Prepare a Statement of Activities for Tazewell County for calendar year20X9, given the following:

(see excel files)

Proceeds from sale of general government land..... $2,200,000

* The cost of the land that was sold was $350,000

Cash............. $2,200,000Land......................$350,000Gain................... 1,850,000

GLTL Principal retired................. $3,000,000

Longterm/p...........$16MCash......................$16M * NOT on activities statement

General Gov Capital Outlay expenditures....... $7,000,000

Assets...........$7MCash.............$7M *NOT on activities statement.

P 13-4

P 13-4

P 13-4

Another Statement of Activities this time for Travis County School Districtfor year ended December 31, 20X5.

nothing tricky just show the excel file.