chapter 1. the set up- revisited who issues your transcript? who issues the “transcript” for...

TRANSCRIPT

Chapter 1

The Set Up- Revisited

• Who issues your transcript? • Who issues the “transcript” for businesses? • You are going to hire someone. You know they

were able to issue their own transcript. How much do you trust it?

• Stock market crash -> SEC and auditors -> Enron -> SOX -> Subprime meltdown -> Dodd Frank

Types of Risk

• Business Risk: The risk that an entity will fail to meet its objectives.

• Information Risk: The probability that information circulated by the company will be false or misleading.

• See page 2 for four environmental conditions that increase the demand for relevant, reliable information.

Definitions

• Assurance: Lending of credibility to information• Attestation: Assurance provided over specific

assertions made by management• Auditing: Attestation over assertions embodied in

the financial statements• The product auditors deliver is an opinion (aka

audit report) about the fair presentation of the financial statements and related footnotes.

Auditing and Assertions

• Auditing def. on page 4. • Auditing is a logical, systematic process to

obtain and evaluate evidence. • There are implicit management assertions

behind every line item you see on a Balance Sheet, P&L, etc.

• Assertions are often tied to risks.

Auditing and Assertions (cont.)

• Auditors have to logically think about the applicable assertions and risks with every item in the financial statements to be able to determine 1) the relevant population to obtain a sample from and 2) the most appropriate audit procedure based on the risk and assertion.

• This is often very difficult at first, but becomes second nature with some practice.

• Ask yourself WCGW?

Auditing and Assertions (cont.)

• Inventory- Does it actually exist? Or has this balance been inflated by management?

• Revenue- Did the sales actually occur? Or is management improperly recognizing/recording revenue?

• Liabilities- Is this list complete? Or are there more liabilities that are not recorded on the Balance Sheet?

Auditing and Assertions (cont.)

• Obtaining evidence enables the auditor to determine the degree of correspondence between the information provided (e.g., financial statements) and the established criteria (e.g., GAAP).

• See Exhibit 1.1 page 5 and AICPA Auditing def. at bottom of page 5.

Assurance vs. Attestation vs. Audits

• Assurance Service: An independent professional service that improves the quality of information for decision makers.

• May involve non-financial information.• Ex: Secret shoppers, CPA’s counting votes at

the Oscars, CPA’s overseeing the determination of lottery winners.

Assurance vs. Attestation vs. Audits (cont.)

• Attestation Service: A practitioner issues a report on subject matter, or an assertion about subject matter that is the responsibility of another party.

• Ex: Audits of financial statements, Reviews of financial statements, Compliance Attestations (e.g., for debt covenant compliance).

• Reviews consist primarily of inquiry and analytical procedures. Auditors express limited (negative) assurance on the financial statements.

Assurance vs. Attestation vs. Audits (cont.)

• Exhibit 1.2 pg. 7. • Remember “STU” for Exhibit 1.4 diagram pg.

10. • Consulting services are not assurance services.

AB’s, SCOT’s, and Presentation and Disclosure

• Management’s assertions in the financial statements are related to1. Account Balances: Cash, Inventory, Accounts

Receivable. Think BS. 2. Significant Classes of Transactions: Sales,

Depreciation Expense. Think P&L.3. Presentation and Disclosure: Footnotes have

been prepared in accordance with GAAP (e.g., Roll-forward for Level 3 Instruments per ASC 820).

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• Pg 12. Second paragraph, first sentence. • The PCAOB and ASB assertions are fairly close,

but the ASB assertions are more detailed. • Note that in practice, slight variation exists

across firms in what they call assertions or exactly which assertions are used.

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• But all assertions/risks are tested regardless of this slight variation in name/approach.

• Similarly, some items in the financial statements may be called AB’s by one firm and SCOTs by another firm.

• Think about cash. Is this an account balance or class of transactions?

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• AB or SCOT depends on whether account tested throughout period or mainly at YE with substantive tests of details.

• Q: What are the different assertions you see for AB’s and SCOTS on page 13?

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• A: Rights and Obligations for AB’s; Cutoff for SCOTs; and Classification for SCOTs.

• Read def’s on pg. 13 for each assertion.• PCAOB assertions vs. ASB assertions like right

hand vs. straight right or overhand right.• Transcript example for completeness and

existence. Draw on board.

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• The Big 4 firm I worked at had the same assertions for both SCOTs and ABs so the distinction didn’t matter much as long as audit procedures were performed for all relevant risks.

• Show Planning Doc_CLASS_EXAMPLE. Pg 73.

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• Draw cutoff line on board.• Another Big 4 firm doesn’t have the cutoff

assertion. • Q: Why? Do they just not test for it? Or can

you argue that cutoff is a specific case of something else?

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

• A:• Note that some these tests must be done near

the end of the period and beginning of the next period to ensure that the cutoff assertion is tested.

• The real world is messier than textbooks. Understanding what you’re doing and why you’re doing it is more important than naming conventions.

AB’s, SCOT’s, and Presentation and Disclosure (cont.)

AB SCOT AB SCOT P & D

Big 4 A: Big 4 B:

Completeness X X X X

Existence X X X X

Accuracy X X

Measurement x

Valuation X X X

Obligations and Rights

X X x

Presentation and Disclosure

x X Separate

Just because neither firm has classification or cutoff does not mean half of the Big 4 doesn’t know to test for these!

Assertions

• Existence/Occurrence: Do the assets on the Balance Sheet exist? Is the revenue line item on the P&L the sum of individual sales that actually happened?

• Risk for these accounts is overstatement. • For the Existence assertion related to AB’s,

auditors will typically confirm the balances (Cash, AR) or will physically observe the item (Inventory).

Assertions (cont.)

• On page 14, the book says auditors also, “complete procedures to ensure that the reported sales transactions really did occur…”

• Q: What do you think auditors should do to test the existence/occurrence assertion for revenue?

Assertions (cont.)

• A: • Rights and Obligations: Does the company

actually own the assets? Are reported liabilities really the responsibility of the company to settle in the future?

Assertions (cont.)

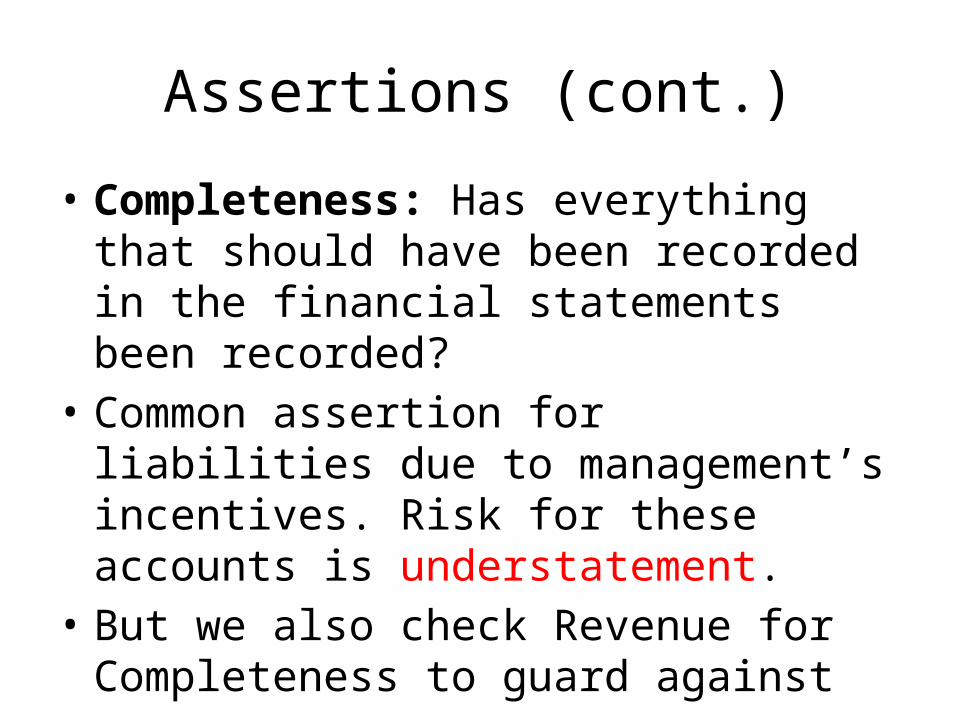

• Completeness: Has everything that should have been recorded in the financial statements been recorded?

• Common assertion for liabilities due to management’s incentives. Risk for these accounts is understatement.

• But we also check Revenue for Completeness to guard against errors.

Assertions (cont.)

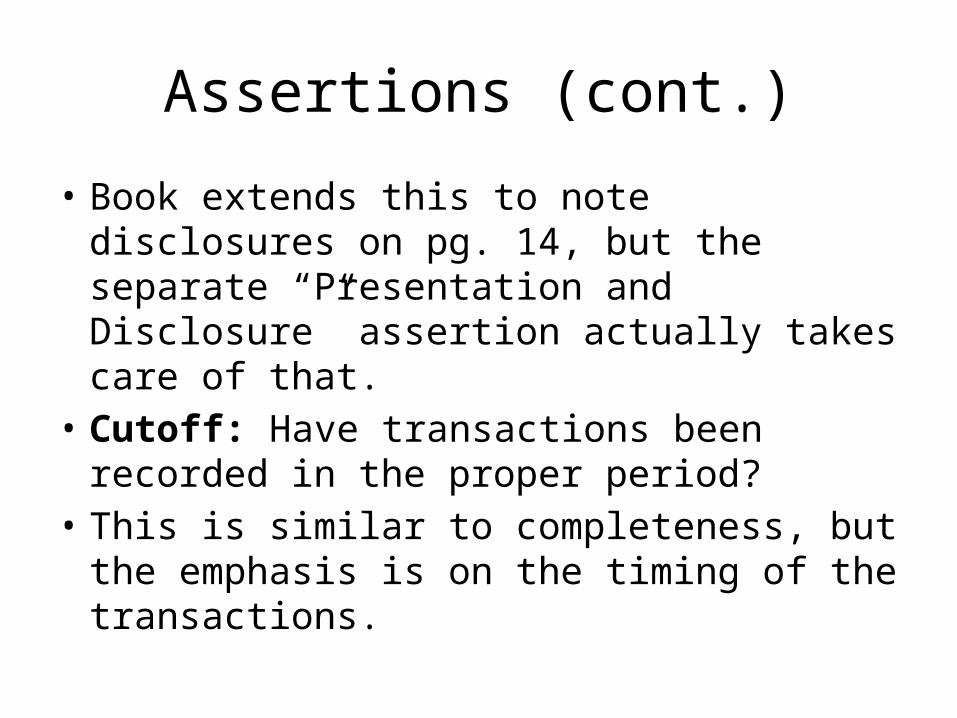

• Book extends this to note disclosures on pg. 14, but the separate “Presentation and Disclosure” assertion actually takes care of that.

• Cutoff: Have transactions been recorded in the proper period?

• This is similar to completeness, but the emphasis is on the timing of the transactions.

Assertions (cont.)

• Concern is that transactions have been booked in the wrong period.

• Note that the third and fifth examples on page 14 are actually completeness and not cutoff.

Assertions (cont.)

• Valuation, Allocation, Accuracy: Has a valuation method in accordance with GAAP been used? Is the math behind the balance accurate?

• Note that just about any error discovered by an auditor may be thought of as a violation of the accuracy assertion.

Assertions (cont.)

• Presentation and Disclosure: Have all required disclosures been made in the notes (e.g., commitments and contingencies, fair value roll-forwards, etc). Are items presented at gross or net when required?

Assertions (cont.)

• This is also related to “classification” where, for example, repairs and maintenance expenses are not capitalized.

• Q: If you were concerned about this, but your audit firm methodology didn’t have a separate “classification” assertion, what other assertions would be violated if R&M were capitalized for: 1. The R&M account?2. The applicable capitalized expenditure account?

Assertions (cont.)

• A: • The Big 4 firm I worked for had six assertions.

These were Completeness, Existence, Accuracy, Valuation, Obligations/Rights, and Presentation/Disclosure

• The acronym we used was CEAVOP.

Assertions (cont.)

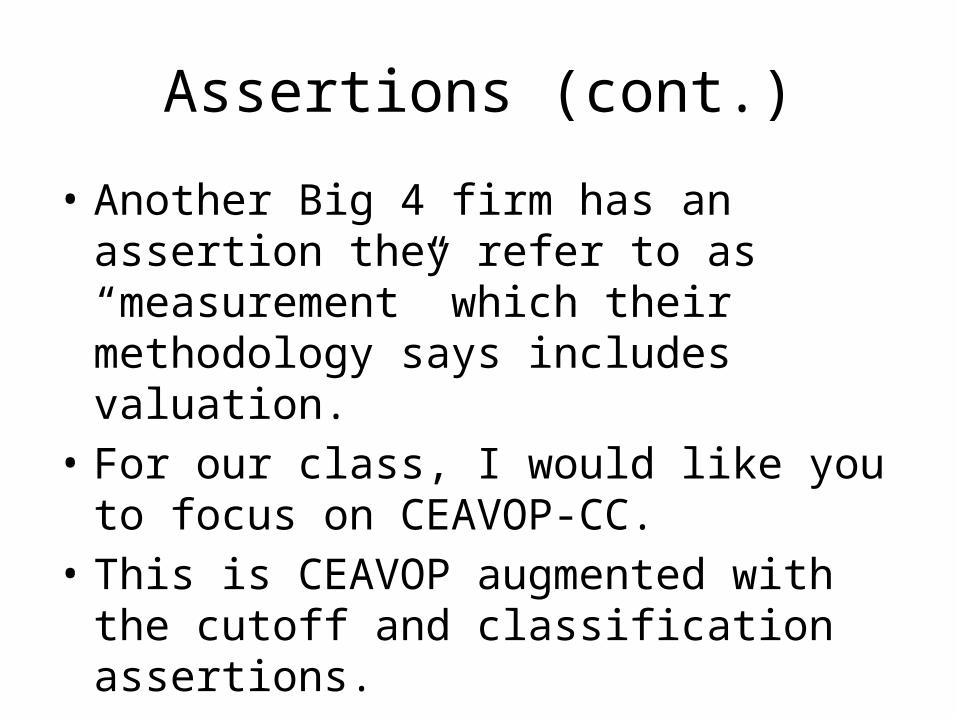

• Another Big 4 firm has an assertion they refer to as “measurement” which their methodology says includes valuation.

• For our class, I would like you to focus on CEAVOP-CC.

• This is CEAVOP augmented with the cutoff and classification assertions.

Assertions (cont.)

• Determining the appropriate assertions for each AB or SCOT drives the type of testing done and evidence gathered.

• If you decide that the primary risk for an account is understatement and then fail to conduct audit tests for completeness, then you have failed to appropriately audit the account.

Example

• Q: From a risk-based approach, what assertion would auditors be most concerned about for AP?

Example (cont.)

• A: • Q: Given that, from a risk standpoint, one

would assume management would want to understate AP, what relevant population should you sample from? What do you ask for (i.e., where do you start the completeness test from)?

Example (cont.)

• A: • Q: What are all the possible outcomes from

this test? How many do you think there are?

Example (cont.)

• A: • Draw examples of Cash and AP tests from old

notes.

Professional Skepticism

• Defined as, “including a questioning mind and a critical assessment of evidence.”

• Book says that auditors ask management to prove assertions with “documentary evidence.”

• Note that evidence may consist of verbal inquiries where management’s responses are included in the workpapers.

Professional Skepticism (cont.)

• There is a “sweet spot” with how your level of skepticism comes across to the people employed at your client.

• Be professional- not adversarial or confrontational.

• Ignore the rest of the chapter. • Work 1.40, 1.45, 1.47, 1.48, 1.49