chapter 07

DESCRIPTION

fmTRANSCRIPT

191 ©2011 Pearson Education, Inc. Publishing as Prentice Hall

CHAPTER 7

Valuation and Characteristics of Bonds

CHAPTER ORIENTATION

This chapter introduces the concepts that underlie asset valuation. We are specifically concerned with bonds. We also look at the concept of the bondholder's expected rate of return on an investment.

CHAPTER OUTLINE

I. Types of bonds

A. Debentures: unsecured long-term debt.

B. Subordinated debentures: bonds that have a lower claim on assets in the event of liquidation than do other senior debt holders.

C. Mortgage bonds: bonds secured by a lien on specific assets of the firm, such as real estate.

D. Eurobonds: bonds issued in a country different from the one in whose currency the bond is denominated; for instance, a bond issued in Europe or Asia that pays interest and principal in U.S. dollars.

E. Convertible bonds: Bonds that can be converted into common stock at a pre-specified price per share.

II. Terminology and characteristics of bonds

A. A bond is a long-term promissory note that promises to pay the bondholder a predetermined, fixed amount of interest each year until maturity. At maturity, the principal will be paid to the bondholder.

B. In the case of a firm's insolvency, a bondholder has a priority of claim to the firm's assets before the preferred and common stockholders. Also, bondholders must be paid interest due them before dividends can be distributed to the stockholders.

192 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

C. A bond's par value is the amount that will be repaid by the firm when the bond matures, usually $1,000.

D. The contractual agreement of the bond specifies a coupon interest rate that is expressed either as a percent of the par value or as a flat amount of interest which the borrowing firm promises to pay the bondholder each year. For example: A $1,000 par value bond specifying a coupon interest rate of nine percent is equivalent to an annual interest payment of $90.

1. When the investor receives a fixed interest rate, the bonds are called fixed-rate bonds.

2. Sometimes a company will issue bonds at a substantial discount from their $1,000 face value with a zero or very low coupon, thus the name zero-coupon bonds.

E. The bond has a maturity date, at which time the borrowing firm is committed to repay the loan principal.

F. A convertible bond allows the investor to exchange the bond for a predetermined number of the firm’s shares of common stock.

G. A bond is callable or redeemable when it provides the firm with the right to pay off the bond at some time before its maturity date. These bonds frequently have a call protection period which prevents the firm from calling the bond for a pre-specified time period.

H. An indenture (or trust deed) is the legal agreement between the firm issuing the bonds and the bond trustee who represents the bondholders. It provides the specific terms of the bond agreement such as the rights and responsibilities of both parties.

I. Bond ratings

1. Bond ratings are simply judgments about the future risk potential of the bond in question. Bond ratings are extremely important in that a firm’s bond rating tells much about the cost of funds and the firm’s access to the debt market.

2. Three primary rating agencies exist—Moody’s, Standard & Poor’s, and Fitch Investor Services.

3. A junk bond is high-risk debt with ratings of BB or below by Moody’s and Standard & Poor’s. The lower the rating, the higher the chance of default.

Foundations of Finance, Seventh Edition ♦ 193

©2011 Pearson Education, Inc. Publishing as Prentice Hall

III. Definitions of value

A. Book value is the value of an asset shown on a firm's balance sheet which is determined by its historical cost rather than its current worth.

B. Liquidation value is the amount that could be realized if an asset is sold individually and not as part of a going concern.

C. Market value is the observed value of an asset in the marketplace where buyers and sellers negotiate an acceptable price for the asset.

D. Intrinsic value is the value based upon the expected cash flows from the investment, the riskiness of the asset, and the investor's required rate of return. It is the value in the eyes of the investor and is the same as the present value of expected future cash flows to be received from the investment.

IV. Valuation: An Overview

A. Value is a function of three elements:

1. The amount and timing of the asset's expected cash flow

2. The riskiness of these cash flows

3. The investors' required rate of return for undertaking the investment

B. Expected cash flows are used in measuring the returns from an investment.

V. Valuation: The Basic Process

The value of an asset is found by computing the present value of all the future cash flows expected to be received from the asset. Expressed as a general present value equation, the value of an asset is found as follows:

V = 1 21 2

$ $ $(1 ) (1 ) (1 )

nn

C C Cr r r

+ + ++ + +

L

where Ct = the cash flow to be received at time t V = the intrinsic value or present value of an asset

producing expected future cash flows, Ct, in years 1 through N

r = the investor's required rate of return n = the number of periods

194 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

VI. Bond Valuation

A. The value of a bond is simply the present value of the future interest payments and maturity value discounted at the bondholder's required rate of return. This may be expressed as:

Vb = 1 2

1 2$ $ $ $

(1 ) (1 ) (1 ) (1 )n

n nb b b b

I I I Mr r r r

+ + + ++ + + +

L

where It = the dollar interest to be received in each payment

M = the par value of the bond at maturity rb = the required rate of return for the bondholder n = the number of periods to maturity

In other words, we are discounting the expected future cash flows to the present at the appropriate discount rate (required rate of return).

B. If interest payments are received semiannually (as with most bonds) the valuation equation becomes:

Vb = nb

nb

n

bb rM

r

I

r

I

r

I22

22

21

1

21

$

21

2/$

21

2/$

21

2/$

⎟⎠

⎞⎜⎝

⎛ +

+

⎟⎠

⎞⎜⎝

⎛ +

++

⎟⎠

⎞⎜⎝

⎛ +

+

⎟⎠

⎞⎜⎝

⎛ +

L

VII. Bond Yields

A. Yield to maturity

1. The yield to maturity is the rate of return the investor will earn if the bond is held to maturity, provided that the company issuing the bond does not default on the payments.

2 We compute the yield to maturity by finding the discount rate that gets the present value of the future interest payments and principal payment just equal to the bond's current market price.

B. Current yield

1. The current yield on a bond is the ratio of the annual interest payment to the bond’s current market price.

2 The current yield is not an accurate measure of the bondholder’s expected rate of return from holding the bond to maturity.

Foundations of Finance, Seventh Edition ♦ 195

©2011 Pearson Education, Inc. Publishing as Prentice Hall

VIII. Bond Value: Three Important Relationships

A. First relationship

A decrease in interest rates (required rates of return) will cause the value of a bond to increase; an interest rate increase will cause a decrease in value. The change in value caused by changing interest rates is called interest rate risk.

B. Second relationship

1. If the bondholder's required rate of return (current interest rate) equals the coupon interest rate, the bond will sell at par, or maturity value.

2. If the current interest rate exceeds the bond's coupon rate, the bond will sell below par value or at a "discount."

3. If the current interest rate is less than the bond's coupon rate, the bond will sell above par value or at a "premium."

C. Third relationship

A bondholder owning a long-term bond is exposed to greater interest rate risk than when owning a short-term bond.

ANSWERS TO

END-OF-CHAPTER QUESTIONS

7-1. The term debenture applies to any unsecured long-term debt. Because these bonds are unsecured, the earning ability of the issuing corporation is of great concern to the bondholder. They are also viewed as being more risky than secured bonds and, as a result, must provide investors with a higher yield than secured bonds provide. Often the issuing firm attempts to provide some protection to the holder through the prohibition of any additional encumbrance of assets. This prohibits the future issuance of secured long-term debt that would further tie up the firm's assets and leave the bondholders less protected. To the issuing firm, the major advantage of debentures is that the debt does not have to be secured by property. This allows the firm to issue debt and still preserve some future borrowing power. A mortgage bond is a bond secured by a lien on real property. Typically, the value of the real property is greater than that of the mortgage bonds issued. This provides the mortgage bondholders with a margin of safety in the event the market value of the secured property declines. In the case of foreclosure, the trustees have the power to sell the secured property and use the proceeds to pay the bondholders. In the event that the proceeds from this sale do not cover the bonds, the bondholders become general creditors, similar to debenture bondholders, for the unpaid portion of the debt.

196 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

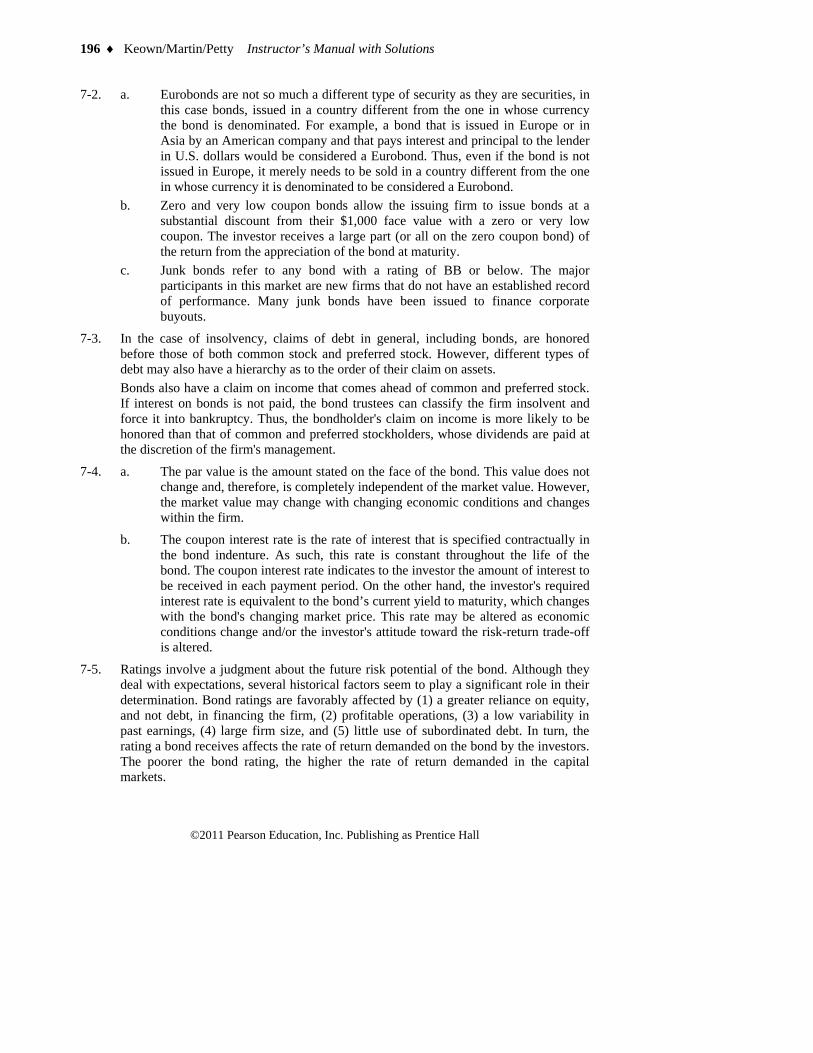

7-2. a. Eurobonds are not so much a different type of security as they are securities, in this case bonds, issued in a country different from the one in whose currency the bond is denominated. For example, a bond that is issued in Europe or in Asia by an American company and that pays interest and principal to the lender in U.S. dollars would be considered a Eurobond. Thus, even if the bond is not issued in Europe, it merely needs to be sold in a country different from the one in whose currency it is denominated to be considered a Eurobond.

b. Zero and very low coupon bonds allow the issuing firm to issue bonds at a substantial discount from their $1,000 face value with a zero or very low coupon. The investor receives a large part (or all on the zero coupon bond) of the return from the appreciation of the bond at maturity.

c. Junk bonds refer to any bond with a rating of BB or below. The major participants in this market are new firms that do not have an established record of performance. Many junk bonds have been issued to finance corporate buyouts.

7-3. In the case of insolvency, claims of debt in general, including bonds, are honored before those of both common stock and preferred stock. However, different types of debt may also have a hierarchy as to the order of their claim on assets. Bonds also have a claim on income that comes ahead of common and preferred stock. If interest on bonds is not paid, the bond trustees can classify the firm insolvent and force it into bankruptcy. Thus, the bondholder's claim on income is more likely to be honored than that of common and preferred stockholders, whose dividends are paid at the discretion of the firm's management.

7-4. a. The par value is the amount stated on the face of the bond. This value does not change and, therefore, is completely independent of the market value. However, the market value may change with changing economic conditions and changes within the firm.

b. The coupon interest rate is the rate of interest that is specified contractually in the bond indenture. As such, this rate is constant throughout the life of the bond. The coupon interest rate indicates to the investor the amount of interest to be received in each payment period. On the other hand, the investor's required interest rate is equivalent to the bond’s current yield to maturity, which changes with the bond's changing market price. This rate may be altered as economic conditions change and/or the investor's attitude toward the risk-return trade-off is altered.

7-5. Ratings involve a judgment about the future risk potential of the bond. Although they deal with expectations, several historical factors seem to play a significant role in their determination. Bond ratings are favorably affected by (1) a greater reliance on equity, and not debt, in financing the firm, (2) profitable operations, (3) a low variability in past earnings, (4) large firm size, and (5) little use of subordinated debt. In turn, the rating a bond receives affects the rate of return demanded on the bond by the investors. The poorer the bond rating, the higher the rate of return demanded in the capital markets.

Foundations of Finance, Seventh Edition ♦ 197

©2011 Pearson Education, Inc. Publishing as Prentice Hall

For the financial manager, bond ratings are extremely important. They provide an indicator of default risk that in turn affects the rate of return that must be paid on borrowed funds.

7-6. Book value is the asset's historical value and is represented on the balance sheet as cost minus depreciation. Liquidation value is the dollar sum that could be realized if the asset were sold individually and not as part of an ongoing concern. Market value is the observed value for an asset in the marketplace where buyers and sellers negotiate a mutually acceptable price. Intrinsic value is the present value of the asset's expected future cash flows discounted at an appropriate discount rate.

7-7. The intrinsic value of a security is equal to the present value of cash flows to be received by the investor. Hence, the terms value and present value are synonymous.

7-8. The first two factors affecting asset value (the asset characteristics) are the asset's expected returns and the riskiness of these returns. The third consideration is the investor's required rate of return. The required rate of return reflects the investor's risk-return preference.

7-9. The relationship is inverse. As the required rate of return increases, the value of the security decreases, and a decrease in the required rate of return results in a price increase.

7-10. The expected rate of return is the rate of return that may be expected from purchasing a security at the prevailing market price. Thus, the expected rate of return is the rate that equates future cash flows with the actual selling price of the security in the market, which is also called the yield to maturity.

198 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

7-1.

a. $875 = ∑= +

++

20

120

bt

b )r (1$1,000

)r (1$70

t

20 N

875 PV 70 PMT

1000 FV

CPT YI / → ANSWER 8.30%

b. Value (Vb) = ∑= +

++

20

1 t 2020 .10) (1

$1,000 .10) (1

$70

= $744.59

20 N

10 I/Y

70 PMT

1000 FV

CPT PV → ANSWER -744.59

c. You should sell the bond

7-2. Value (Vb) = ∑= +

++

14

1 t 1414 .10) (1

$1,000 .10) (1

$70

14 N

10 I/Y

70 PMT

1000 FV

CPT PV → ANSWER -779.00

Foundations of Finance, Seventh Edition ♦ 199

©2011 Pearson Education, Inc. Publishing as Prentice Hall

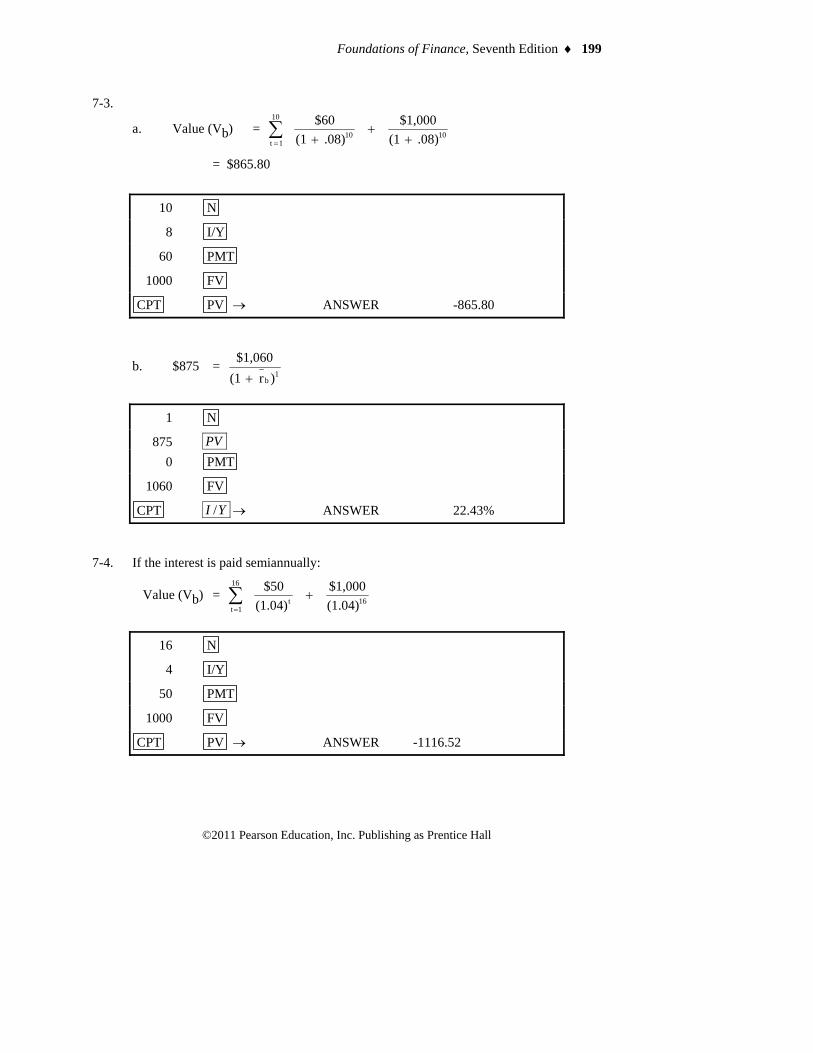

7-3.

a. Value (Vb) = ∑= +

++

10

1 t 1010 .08) (1

$1,000 .08) (1

$60

= $865.80

10 N

8 I/Y

60 PMT

1000 FV

CPT PV → ANSWER -865.80

b. $875 = 1

b )r (1$1,060+

1 N

875 PV 0 PMT

1060 FV

CPT YI / → ANSWER 22.43% 7-4. If the interest is paid semiannually:

Value (Vb) = 16

16

1tt (1.04)

$1,000 (1.04)

$50 +∑=

16 N

4 I/Y

50 PMT

1000 FV

CPT PV → ANSWER -1116.52

200 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

If interest is paid annually:

Value (Vb) = ∑=

+8

1 t 8t (1.08)

$1,000 (1.08)$100

8 N

8 I/Y

100 PMT

1000 FV

CPT PV → ANSWER 1114.93 7-5. a. Series A:

Value (Vb) = ∑=

+12

1 t 1212 (1.05)

$1,000 (1.05)

$85

Value (Vb) = ∑=

+12

1 t 1212 (1.08)

$1,000 (1.08)

$85

Value (Vb) = ∑=

+12

1 t 1212 (1.12)

$1,000 (1.12)

$85

12 N

I/Y = 5% 8% 12%

85 PMT

1000 FV

CPT PV →ANSWER 1,310.21 1,037.68 783.20

Foundations of Finance, Seventh Edition ♦ 201

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Series B:

Value (Vb) = ∑=

+1

1 t 11 (1.05)

$1,000 (1.05)

$85

Value (Vb) = ∑=

+1

1 t 11 (1.08)

$1,000 (1.08)

$85

Value (Vb) = ∑=

+1

1 t 11 (1.12)

$1,000 (1.12)

$85

1 N

I/Y = 5% 8% 12%

85 PMT

1000 FV

CPT PV →ANSWER 1,033.33 1,004.63 968.75

b. Longer-term bondholders are locked into a particular interest rate for a longer period of time and are therefore exposed to more interest rate risk

7-6. $900 = ∑= +

++

20

1 t 20

bt

b /2)r (1$1,000

/2)r (1$40

20 N

900 +/- PV

40 PMT

1000 FV

CPT I/Y → ANSWER 4.79 semiannual rate

The rate is equivalent to 9.6 percent annual rate compounded semiannually, or 9.8 percent (1.0482 - 1) compounded annually.

202 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

7-7. $1200 = 5

b

5

1 t 5

b )r (1$1,000

)r (1$90

++

+∑=

5 N

1200 +/- PV

90 PMT

1000 FV

CPT I/Y → ANSWER 4.45%

7-8. $945 = 20

b

20

1 t t

b )r (1$1,000

)r (1$90

++

+∑=

20 N

945 +/- PV

90 PMT

1000 FV

CPT I/Y → ANSWER 9.63

7-9. $1,150 = ∑= +

++

12

1 t 12

bt

b ) (1$1,000

)r (1$70

r

12 N

1150 +/- PV

70 PMT

1000 FV

CPT I/Y → ANSWER 5.28

Foundations of Finance, Seventh Edition ♦ 203

©2011 Pearson Education, Inc. Publishing as Prentice Hall

7-10. a. $1,085 = ∑= +

++

15

1 t 15

bt

b )r (1$1,000

)r (1$80

15 N

1085 +/- PV

80 PMT

1000 FV

CPT I/Y → ANSWER 7.06

b. Vb = ∑=

+15

1 t 15t (1.10)

$1,000 (1.10)

$80

15 N

10 I/Y

80 PMT

1000 FV

CPT PV → ANSWER -847.88

c. Since the expected rate of return, 7.06 percent, is less than your required rate of return of 10 percent, the bond is not an acceptable investment. This fact is also evident because the market price, $1,085, exceeds the value of the security to the investor of $847.48.

7-11. a. Value

Par Value $1,000.00 Coupon $ 100.00 Required Rate of Return 0.12 Years to Maturity 15 Market Value $ 863.78

b. Value at Alternative Rates of Return Required Rate of Return 0.15 Market Value $ 707.63 Required Rate of Return 0.08 Market Value $1,171.19

204 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

c. As required rates of return change, the price of the bond changes, which is the result of "interest-rate risk" Thus, the greater the investor's required rate of return, the greater will be his/her discount on the bond. Conversely, the less his/her required rate of return below that of the coupon rate, the greater the premium will be.

d. Value at Alternative Maturity Dates Years to Maturity 5 Required Rate of Return 0.12 Market Value $ 927.90 Required Rate of Return 0.15 Market Value $ 832.39 Required Rate of Return 0.08 Market Value $1,079.85

e. The longer the maturity of the bond, the greater the investor is exposed to

interest rate risk, resulting in greater premiums and discounts. 7-12. a. Value

Par Value $1,000.00 Coupon $ 80.00 Required Rate of Return 0.07 Years to Maturity 20 Market Value $1,105.94

b. Value at Alternative Rates of Return

Required Rate of Return 0.10 Market Value $829.73 Required Rate of Return 0.06 Market Value $1,229.40

c. As required rates of return change, the price of the bond changes, which is the

result of "interest-rate risk" Thus, the greater the investor's required rate of return, the greater will be his/her discount on the bond. Conversely, the less his/her required rate of return below that of the coupon rate, the greater the premium will be.

d. Value at Alternative Maturity Dates

Years to Maturity 10 Required Rate of Return 0.07 Market Value $1,070.24 Required Rate of Return 0.10 Market Value $877.11 Required Rate of Return 0.06 Market Value $1,147.20

Foundations of Finance, Seventh Edition ♦ 205

©2011 Pearson Education, Inc. Publishing as Prentice Hall

e. The longer the maturity of the bond, the greater the investor is exposed to interest rate risk, resulting in greater premiums and discounts.

7-13. PV = FVn ⎟⎟⎠

⎞⎜⎜⎝

⎛+ nr).1(1

PV = $1,000 ⎟⎟⎠

⎞⎜⎜⎝

⎛+ 7)09.1(

1

PV = $1,000(.547)

PV = $547

7-14. The solutions in this problem are based on the present value appendixes, rather than using a financial calculator. Either approach will provide the same answers, subject to rounding errors.

a. Percent 10at

Value BondA Bond

= ⎝⎜⎜⎛

⎠⎟⎟⎞Present Value

of InterestPayments

+ ⎝⎜⎜⎛

⎠⎟⎟⎞Present Value of

the Return of thePrincipal

=

⎟⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜⎜

⎝

⎛

====

2 m 3 n 10% r $50 PMT

+

⎟⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜⎜

⎝

⎛

====

2 m 3 n

10% r $1,000 FV

= PMT ⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

+=

⋅

∑t)

mr(1

1 1t

m n + FVnm

⎝⎜⎜⎛

⎠⎟⎟⎞1

(1 + i

m)nm

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )05.1(1

1

6+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .05)6

= $50(5.076) + $1000(.746) = $253.80 + $746 = $999.80

(Actually it is equal to $1000 but the calculations are off somewhat due to rounding error in the tables.)

206 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

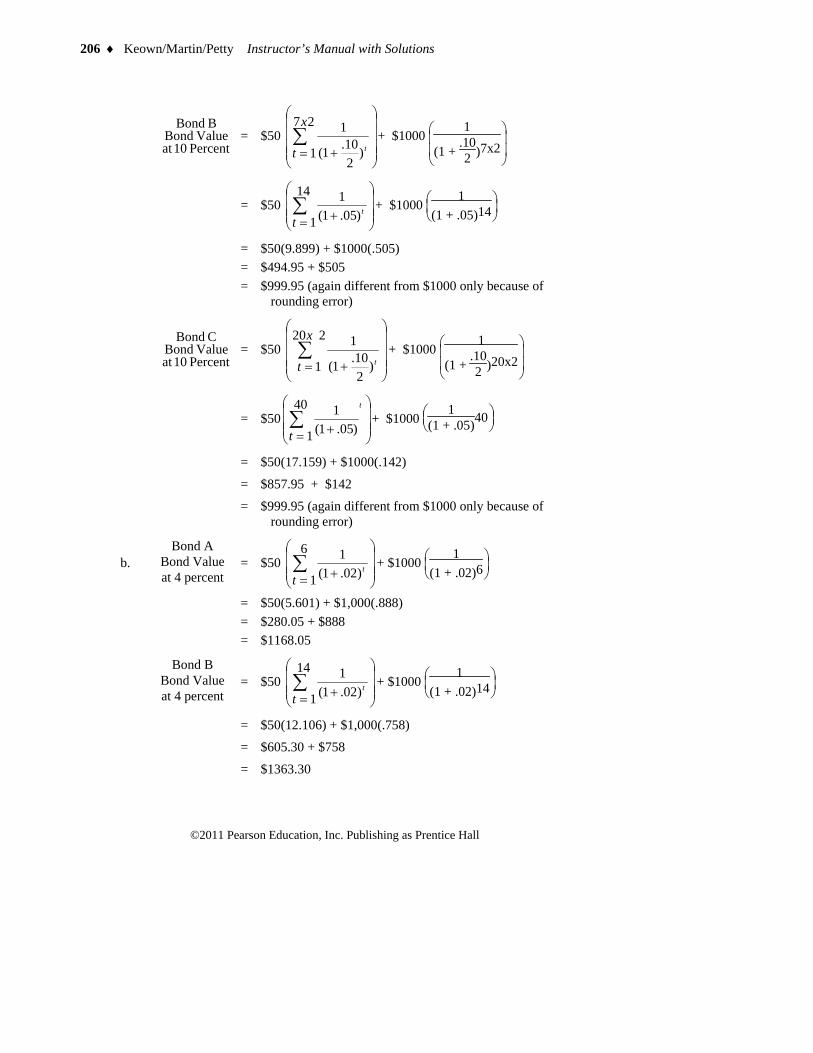

Percent 10at Value Bond

B Bond = $50

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

+=∑

tt

x

)210.1(

1

1

27+ $1000

⎝⎜⎜⎛

⎠⎟⎟⎞1

(1 + .102 )7x2

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )05.1(1

1

14+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .05)14

= $50(9.899) + $1000(.505) = $494.95 + $505

= $999.95 (again different from $1000 only because of rounding error)

Percent 10at Value Bond

C Bond = $50

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

+=∑

tt

x

)210.1(

1

1

220+ $1000

⎝⎜⎜⎛

⎠⎟⎟⎞1

(1 + .102 )20x2

= $50⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑

t

t )05.1(1

1

40+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .05)40

= $50(17.159) + $1000(.142)

= $857.95 + $142

= $999.95 (again different from $1000 only because of rounding error)

b. Bond A

Bond Valueat 4 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )02.1(1

1

6+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .02)6

= $50(5.601) + $1,000(.888) = $280.05 + $888 = $1168.05

Bond B

Bond Valueat 4 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )02.1(1

1

14+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .02)14

= $50(12.106) + $1,000(.758)

= $605.30 + $758

= $1363.30

Foundations of Finance, Seventh Edition ♦ 207

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Bond C

Bond Valueat 4 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )02.1(1

1

40+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .02)40

= $50(27.356) + $1,000(.453)

= $1367.80 + $453

= $1820.80

c. Bond A

Bond Valueat 16 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ tt )08.1(

1

1

6+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .08)6

= $50(4.623) + $1,000 (.630)

= $231.15 + $630

= $861.15

Bond B

Bond Valueat 16 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )08.1(1

1

14+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .08)14

= $50(8.244) + $1,000(.340)

= $412.20 + $340

= $752.20

Bond C

Bond Valueat 16 percent

= $50 ⎟⎟⎟

⎠

⎞

⎜⎜⎜

⎝

⎛

+=∑ t

t )08.1(1

1

40+ $1000

⎝⎜⎛

⎠⎟⎞1

(1 + .08)40

= $50(11.925) + $1,000(.046)

= $596.25 + $46

= $642.25

d. First, if the market discount rate and the bond’s coupon rate are identical, then the bond's value will be equal to its principal value, in this case $1,000. Second, when interest rates change, bonds with longer maturities change more in value than do bonds with shorter maturities.

208 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

7-15. $1,000 = 10

10tbt 1 b

$30 $900 (1 )(1 r ) r=

+++∑

10 N

900 +/- PV

30 PMT

1,000 FV

CPT I/Y → ANSWER 4.2 semiannually 8.5% annually

7-16. Current yield = annual dividend ÷ current price = ($35 x 2) ÷ $780

= 0.0897 = 9%

7-17. $700 = 16

t 16b bt 1

$30 $700 (1 r ) (1 r )=

++ +∑

16 N

700 +/- PV

30 PMT

1,000 FV

CPT I/Y → ANSWER 5.9% semiannually 11.9% annually

7-18. $820 = ∑= +

++

14

1 t 14

bt

b )r (1$1,000

)r (1$30

14 N

820 +/- PV

30 PMT

1,000 FV

CPT I/Y → ANSWER 4.7% semiannual 9.5% annual

Comment [u1]: Changed 5 to 10

Deleted: 5

Comment [u2]: Changed the 8 and 7 to 16

Deleted: 12.05

Deleted: 9

Foundations of Finance, Seventh Edition ♦ 209

©2011 Pearson Education, Inc. Publishing as Prentice Hall

7-19. $900 = ∑= +

++

10

1 t 10

bt

b )r (1$1,000

)r (1$60

10 N

900 +/- PV

60 PMT

1,000 FV

CPT I/Y → ANSWER 7.4 annual

7-20. $1,100 = ∑= +

++

14

1 t 14

bt

b )r (1$1,000

)r (1$40

14 N

1,100 +/- PV

40 PMT

1,000 FV

CPT I/Y → ANSWER 6.2

SOLUTION TO MINI CASE

a. Microsoft Bond Value (Vb) = 30

30

1 t i .06) (1

$1,000 .06) (1

$52.50 +

++∑

=

30 N

60 I/Y

52.50 PMT

1000 FV

CPT PV → ANSWER 896.76

Deleted: 5

210 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Ford Bond Value (Vb) = ∑= +

++

25

1 t 25)15. 1(

000,1$ )15.1(

25.71$ i

25 N

15 I/Y

71.25 PMT

1000 FV

CPT PV → ANSWER -$490.95

Xerox Value (Vb) = ∑= +

++

16

1 t 16i )10. 1(

000,1$ )10.1(

00.80$

16 N

10 I/Y

80.00 PMT

1000 FV

CPT PV → ANSWER -$843.53 b. To compute the expected rate of return for each bond, use a financial calculator to

solve the following equation:

Microsoft:

$1009.00 = 30b

30

1 t i

b )r (1$1,000

)r (1$52.50

++

+∑=

30 N

1009.00 +/- PV

52.50 PMT

1000 FV

CPT I/Y → ANSWER 5.2%

Foundations of Finance, Seventh Edition ♦ 211

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Ford:

$610.00 = ∑= +

++

25

125

bt

b )r (1$1,000

)r (1$71.25

t

25 N

1009 +/- PV

71.25 PMT

1000 FV

CPT I/Y → ANSWER 12.1% Xerox:

$805.00 = ∑= +

++

16

1 t 16

bt

b )r (1$1,000

)r (1$80.00

16 N

805 +/- PV

80.00 PMT

1000 FV

CPT I/Y ANSWER 10.6%

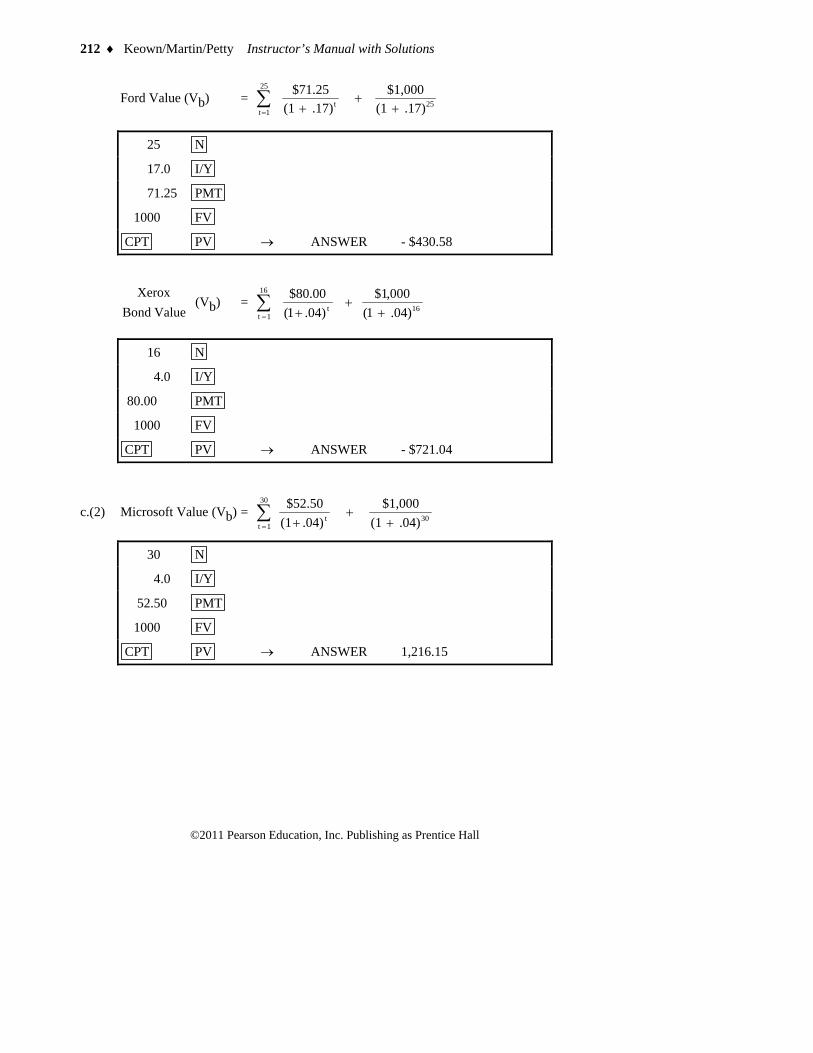

c.(1) Microsoft Value (Vb) = ∑= +

++

30

1 t t )08. 1(

000,1$ )08. 1(

50.52$

30 N

8.0 I/Y

52.50 PMT

1000 FV

CPT PV → ANSWER - $690.41

212 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Ford Value (Vb) = ∑= +

++

25

125t .17) (1

$1,000 .17) (1

$71.25 t

25 N

17.0 I/Y

71.25 PMT

1000 FV

CPT PV → ANSWER - $430.58

Value BondXerox

(Vb) = ∑= +

++

16

1 t 16t )04. 1(

000,1$ )04.1(

00.80$

16 N

4.0 I/Y

80.00 PMT

1000 FV

CPT PV → ANSWER - $721.04

c.(2) Microsoft Value (Vb) = ∑= +

++

30

1 t 30t .04) (1

$1,000 .04)(1

$52.50

30 N

4.0 I/Y

52.50 PMT

1000 FV

CPT PV → ANSWER 1,216.15

Foundations of Finance, Seventh Edition ♦ 213

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Ford Bond Value (Vb) = ∑= +

++

25

1 t 25t .13) (1

$1,000 .13) (1

$71.25

25 N

13.0 I/Y

71.25 PMT

1000 FV

CPT PV → ANSWER $569.36

Value BondXerox

(Vb) = ∑= +

++

16

1 t 16t .08) (1

$1,000 .08) (1

$80.00

11 N

8.0 I/Y

80.00 PMT

1000 FV

CPT PV → ANSWER $1000.00

d. As the interest rates rise and fall, we see the different effects on bond prices depending on the length of time to maturity and whether the investor's required rate of return is above or below the coupon interest rate. If the investor’s required rate of return is above the coupon interest rate, the bond will sell at a discount (below par value), but if the investor’s required rate of return is below the coupon interest rate, the bond will sell at a price above its par value (premium).

e. The Bell South, Dole and Xerox bonds have a lower expected rate of return than your required rate of return. So we would not buy all of them.

214 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

ALTERNATIVE PROBLEMS AND SOLUTIONS

ALTERNATIVE PROBLEMS

7-1A. (Bond Valuation) Calculate the value of a bond that expects to mature in 10 years and has a $1,000 face value. The coupon interest rate is 9 percent and the investors’ required rate of return is 15 percent.

7-2A. (Bond Valuation) Pybus, Inc. bonds have a 10 percent coupon rate. The interest is paid semiannually and the bonds mature in 11 years. Their par value is $1,000. If your required rate of return is 9 percent, what is the value of the bond? What is its value if the interest is paid annually?

7-3A. (Bond Yield: Bondholder Expected Rate of Return) The market price is $950 for an 8-year bond ($1,000 par value) that pays 9 percent interest (4.5 percent semiannually). What is the bond’s expected rate of return?

7-4A. (Bond Valuation) Doisneau 20-year bonds pay 10 percent interest annually on a $1,000 par value. If the bonds sell at $975, what is the bond’s expected rate of return?

7-5A. (Bond Yield: Bondholder Expected Rate of Return) Hoyden Co.’s bonds mature in 15 years and pay 8 percent interest annually. If you purchase the bonds for $1,175, what is your expected rate of return?

7-6A. (Bond Valuation) Fingen’s 14-year, $1,000 par value bonds pay 9 percent interest annually. The market price of the bonds is $1,100 and your required rate of return is 10 percent.

a. Compute the bond’s expected rate of return.

b. Determine the value of the bond to you, given your required rate of return.

c. Should you purchase the bond?

7-7A. (Bond Valuation) You own a bond that pays $75 in annual interest, with a $1,000 par value. It matures in 15 years. Your required rate of return is 6 percent.

a. Calculate the value of the bond.

b. How does the value change if your required rate of return (i) increases to 10 percent or (ii) decreases to 4 percent?

c. Explain the implications of your answers in part (b) as they relate to interest rate risk, premium bonds, and discount bonds.

d. Assume that the bond matures in 5 years instead of 15 years. Recompute your answers in part (b).

e. Explain the implications of your answers in part (d) as they relate to interest rate risk, premium bonds, and discount bonds.

7-8A. See Problem 7-7A for an alternative problem for Problem 7-8.

Foundations of Finance, Seventh Edition ♦ 215

©2011 Pearson Education, Inc. Publishing as Prentice Hall

SOLUTIONS TO ALTERNATIVE PROBLEMS

7-1A. Value (Vb) = ∑= +

++

10

1 t 10t .15) (1

$1,000 .15) (1

$90

= $90(5.018) + $1,000 (.247)

= $451.62 + $247.00

= $698.62

10 N

15 I/Y

90 PMT

1000 FV

CPT PV → ANSWER -698.87 7-2A. If the interest is paid semiannually:

Value (Vb) = ∑=

+22

1 t 22t (1.045)

$1,000 (1.045)

$50

Vb = $50 (13.784) + $1,000 (0.380)

Vb = $1,069.20

22 N

4.5 I/Y

50 PMT

1000 FV

CPT PV → ANSWER -1068.92

216 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

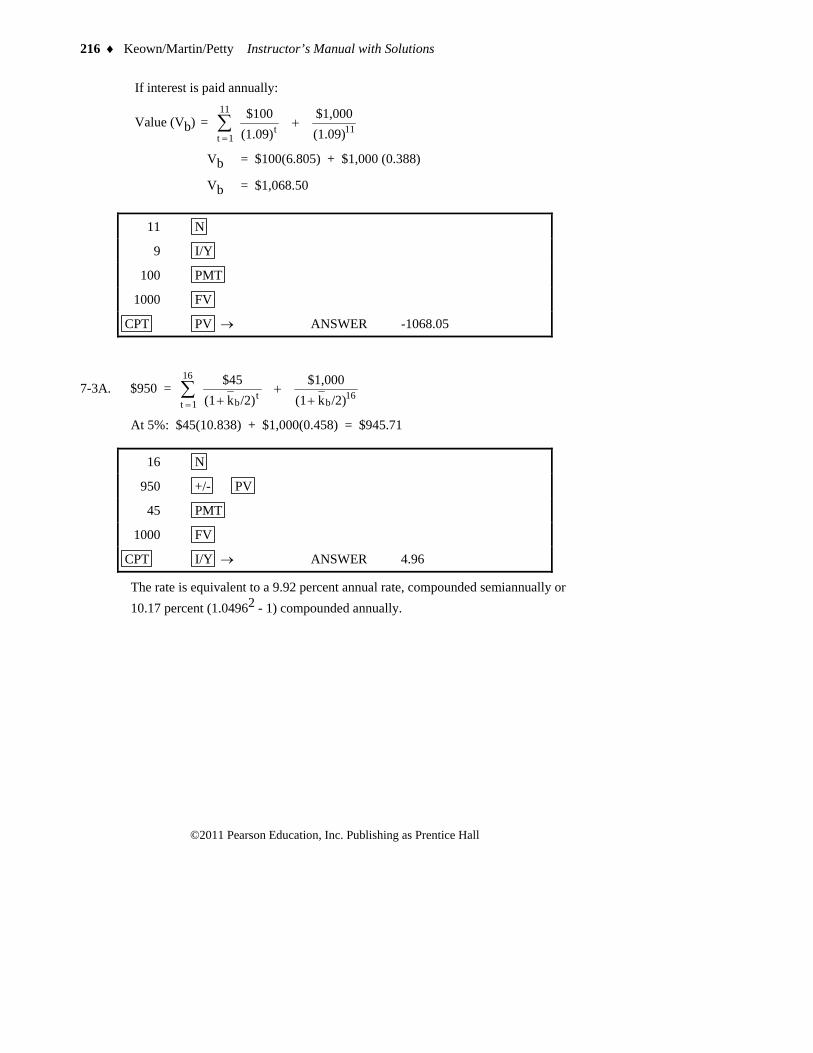

If interest is paid annually:

Value (Vb) = ∑=

+11

1 t 11t (1.09)

$1,000 (1.09)$100

Vb = $100(6.805) + $1,000 (0.388)

Vb = $1,068.50

11 N

9 I/Y

100 PMT

1000 FV

CPT PV → ANSWER -1068.05

7-3A. $950 = ∑= +

++

16

1 t 16

bt

b /2)k(1$1,000

/2)k(1$45

At 5%: $45(10.838) + $1,000(0.458) = $945.71

16 N

950 +/- PV

45 PMT

1000 FV

CPT I/Y → ANSWER 4.96

The rate is equivalent to a 9.92 percent annual rate, compounded semiannually or 10.17 percent (1.04962 - 1) compounded annually.

Foundations of Finance, Seventh Edition ♦ 217

©2011 Pearson Education, Inc. Publishing as Prentice Hall

7-4A. $975 = ∑= +

++

20

1 t 20

bt

b )k (1$1,000

)k (1$100

20 N

975 +/- PV

100 PMT

1000 FV

CPT I/Y → ANSWER 10.30

7-5A. $1,175 = ∑= +

++

15

1 t 15

bt

b )k (1$1,000

)k (1$80

15 N

1175 +/- PV

80 PMT

1000 FV

CPT I/Y → ANSWER 6.18

7-6A. a. $1,100 = ∑= +

++

14

1 t 14t b)k (1

$1,000 b)k (1

$90

14 N

1100 +/- PV

90 PMT

1000 FV

CPT I/Y → ANSWER 7.80

b. Vb = ∑=

+14

1 t 14t (1.10)

$1,000 (1.10)

$90

Vb = $90(7.367) + $1,000(0.263)

Vb = $926.03

218 ♦ Keown/Martin/Petty Instructor’s Manual with Solutions

©2011 Pearson Education, Inc. Publishing as Prentice Hall

14 N

10 I/Y

90 PMT

1000 FV

CPT PV → ANSWER -926.33

c. Since the expected rate of return, 7.82 percent, is less than your required rate of return of 10 percent, the bond is not an acceptable investment. This fact is also evident because the market price, $1,100, exceeds the value of the security to the investor of $926.03.

7-7A a. Value

Par Value $1,000.00 Coupon $ 75.00 Required Rate of Return 0.06 Years to Maturity 15 Market Value $ 1,145.68

b. Value at Alternative Rates of Return

Required Rate of Return 0.10 Market Value $ 809.85 Required Rate of Return 0.04 Market Value $1,389.14

c. As required rates of return change, the price of the bond changes, which is the

result of "interest-rate risk." Thus, the greater the investor's required rate of return, the greater will be his/her discount on the bond. Conversely, the less his/her required rate of return is below that of the coupon rate, the greater the premium will be.

d. Value at Alternative Maturity Dates

Years to Maturity 5 Required Rate of Return 0.06 Market Value $ 1,063.19 Required Rate of Return 0.10 Market Value $ 905.23 Required Rate of Return 0.04 Market Value $1,155.82

e. The longer the maturity of the bond, the greater the investor is exposed to

interest-rate risk, resulting in greater premiums and discounts.