challenges of the debt crisis from an … to deal with the debt crisis. as a consequence, ......

TRANSCRIPT

CHALLENGES OF THE DEBT CRISIS

FROM AN AMERICAN AND A GREEK PERSPECTIVE

Irene Kyriakopoulos, PhD

Distinguished Professor of National Security Policy Department of Economics, ICAF

National Defense University Washington, DC 20319

Presentation at

SYMPOSION GROWTH STRATEGIES FOR SOUTHERN EUROPE

VIENNA, JUNE 27, 2012

Austrian Marshall Plan Foundation and Austrian National Bank

*The views and opinions expressed are solely the author’s. They do not represent the views and opinions of the National Defense University, the Department of Defense or any other US government agency. This presentation draws on research conducted during the author’s tenure as Public Policy Scholar, Wilson International Center for Scholars, Washington, DC, September 2011-May 2012. Contact info: [email protected]

2

CHALLENGES OF THE DEBT CRISIS

FROM AN AMERICAN AND A GREEK PERSPECTIVE

Summary

The European Union (EU) has chosen austerity-oriented, pro-cyclical and structural

policies to deal with the debt crisis. As a consequence, European economic activity has

stalled and unemployment increased significantly, especially in countries of the EU

periphery. The EU’s policy choices will result in rebalancing of fiscal priorities over the

long term, placing Europe’s past achievements in material and social well being as well

as its common currency in peril. From an American perspective, the biggest challenge of

the debt crisis comes from the fact that the EU governance institutions have been

ineffective; their major flaw is the absence of a recognized sovereign with legitimate

authority to guarantee the euro and take responsibility for the EU’s macroeconomic

performance. Neither the Eurozone nor the EU are sovereign states. The euro's status as

a stateless currency is not sustainable. For Europe not to fail, "more Europe" requires

the attributes of a sovereign entity that can guarantee the euro. From a Greek

perspective, the biggest challenges of the crisis are, first, that the country’s admission to

the Eurozone imposed unrealistic standards that were beyond the Greek government’s

grasp and reach and, second, that the EU’s rescue loans damaged the Greek economy.

Although Greece’s political class bears the heaviest share of the blame for non-

performance, EU decision-makers bear responsibility for creating and imposing bailout

loans that worsened Greece’s economic performance and generated dangerous political

and social turmoil. The economic and political backlash against austerity and its

consequences have the potential to derail implementation of macroeconomic and

structural policies in the most heavily indebted countries, upset fragile political balances

in the Eurozone, and alter the course of European integration.

3

CHALLENGES OF THE DEBT CRISIS

FROM AN AMERICAN AND A GREEK PERSPECTIVE

Europe's post-World War II experiment in supranational governance is tested by a

multiplicity of challenges stemming from the financial crisis that erupted in the United

States in the fall of 2008. Resolution of Europe’s debt crisis is of vital importance to the

peoples of Europe and to the world economy. The United States and the European Union

(EU) are each other’s and the world’s largest partners in international trade, commerce,

investment, finance and economic development. Greece, on the other hand, is a small

country that has played a big role in triggering Europe’s sovereign debt crisis. Greece’s

dire finances have made her membership in the Eurozone the subject of extensive policy

debate both domestically and abroad, especially in Europe. This paper seeks to

contribute to a better understanding of the challenges of the debt crisis by examining

them from an American and a Greek perspective.

The Challenges of the Debt Crisis from an American Perspective

The European Union (EU) is mired in the worst financial and economic crisis since

the launch of the euro. Monetary union was meant to reflect the strength of the EU, an

economic superpower comparable to the United States in wealth, affluence and

preeminence in world trade. Larger in population and in share of global GDP, the EU has

achieved a high standard of living (per capita GDP about three-quarters that of the US),

pre-eminence in international trade, a superb infrastructure based on advanced

technology, and an extensive and comprehensive social welfare system, featuring public

health for all, generously subsidized education from primary level to university, and

substantial benefits to protect the unemployed, the old and the poor. With the unfolding

crisis engulfing most of the 27 member states of the EU, these achievements are in peril.

Austerity measures adopted in many countries are contributing to recession and

unemployment, have worsened the crisis, weakened a fragmented banking system and are

4

demolishing the post-WWII European social model. Thus, austerity measures are

eroding the political consensus of economic, monetary and political integration. 1

European policy makers have chosen pro-cyclical and structural policies aimed at

restoring fiscal discipline, especially in countries of the EU periphery (Greece, Ireland,

Portugal and Spain). These policies have exacerbated pre-existing imbalances, made

worse by recessionary forces. The level of indebtedness of Eurozone countries has risen

considerably since the crisis erupted. The ratio of government debt to GDP is highest in

Greece, at nearly 160 %. In Italy and Ireland, it stands at 120 and 112 %, respectively.

Portugal’s is just over 100. Debt levels across the Eurozone bloc have risen, from an

average of 85.3 % of national output in 2010 to 87.2 % at the end of 2011. As signatories

of the Maastricht Treaty, Eurozone members had agreed to keep this ratio at 60 %. This

has proved impossible for eleven of the seventeen states. Even the largest EU economies,

France and Germany, are more highly indebted than allowed.

A related symptom of the crisis is the number of countries with large government

deficits. Eurostat data released in late April 2012 showed that Ireland’s deficit-to GDP

ratio remained the largest, followed by Greece, Spain and the UK; these ratios (ranging

from highest, 13%, to lowest, 8%) exceed by far the limits proscribed by the currency

union (3%). 2 As a result of draconian measures enacted since 2010, the Eurozone’s

average deficit has fallen from 6.2 % in 2010 to 4.1 % in 2011 but the European

Commission expects that the continuing recession will add another percentage point to

the average Eurozone deficits and that even France will be among thirteen countries that

will miss the deficit targets set for 2013.

With the application of pro-cyclical measures, prospects for economic growth have

deteriorated. Growth estimates have been lowered across the board. Greece’s remain the

worst, with the recession continuing for the fifth year in 2012 and its economy expected 1 “Austerity measures” has become a popular phrase to describe policies involving cuts in public spending, increases in taxes and structural reforms aimed at liberalizing product and labor markets. I use this term as affirmative, not normative shorthand. 2 Eurostat, Provision of deficit and debt data for 2011, News release-Euroindicators http://epp.eurostat.ec.europa.eu/cache/ITY_PUBLIC/2-23042012-AP/EN/2-23042012-AP-EN.PDF

5

to shrink further (over 6% in the first quarter). Portugal, Italy and Spain are also in

recession. The latest addition is the Netherlands; its economy was deemed among the

strongest in Europe but is now in recession.

The most dramatic impact of pro-cyclical policies has been on unemployment, which

has risen sharply since 2010. Worst hit are Spain (its unemployment rate approaches

25%) and Greece (its unemployment rate has surpassed 20%). Youth unemployment is

over 50%. This was a predictable consequence of austerity policies aimed at restoring

competitiveness through internal devaluation, achieved by lower wages and falling

prices. Labor reforms that have transformed the landscape of Europe’s political economy

include: reduction of welfare benefits; expansion of temporary and part-time work; big

cuts to minimum wage (plus, companies are allowed to pay below minimum wage for

certain workers and youth wages can be set below the statutory minimum); pay freezes,

elimination of salary bonuses, cuts to pensions and increase in retirement age, drastic cuts

to severance pay and reduction of vacation days; easing of restrictions against firings and

layoffs and reduced duration and level of unemployment benefits; negotiation of salaries

and working hours at the company level, not by the unions; and collective bargaining

agreements no longer automatically applicable economy-wide.

Europe’s fiscal retrenchment is set to continue over the long term. According to a

study sponsored by the European Parliament, the EU may be at the beginning of two

decades of austerity for public budgets, including spending on defense.3 The economic

and financial crisis has led to drastic consolidation measures affecting military spending

in all EU member states except Sweden, Poland, France, Finland and Denmark.

Significant cuts in defense budgets are under way in Germany and the UK. Dramatic

cuts in the order of 30 % are planned in smaller states. The majority of middle sized

states are expected to enact average cuts of 10%. As a result, regional shifts in economic

power may be accelerated. Another recent study identified significant differences in

3 Directorate-General for External Policies of the Union, European Parliament, “The Impact of the Financial Crisis on European Defense”, April 2011, http://www.europarl.europa.eu/document/activities/cont/201106/20110623ATT22406/20110623ATT22406EN.pdf

6

defense spending priorities between countries and regions depending on the impact of the

current crisis. 4 While most East Asian countries’ defense budgets continue to grow in

parallel with the economy, governments in the US and Europe are reversing this trend.

The financial crisis has not only aggravated the under-financing of European defense

establishments, it has also affected the strategic calculations of many European states,

leading to the claim that austerity will “trump the strategy”. 5

The Eurozone’s banking system is fragile and dysfunctional. In the absence of a

banking union and EU-wide banking regulations and deposit insurance, several national

banking systems became weaker as a result of the financial crisis. Across the EU, a fragmented and weakened banking sector has contributed to the on-going recession.

Fragmentation of the banking system contributed to the restriction of credit in the

countries worst hit by recession, unemployment and business failures. The problems of

Spanish bank became more acute in May 2012, leading Spain to seek a bailout loan,

reportedly for €100 billion, for recapitalization of its banks.6 Deposit flight, on top of a

private sector debt write-down (PSI) arranged earlier in 2012, has devastated Greece’s

banks; bailout loan funds will be used for their recapitalization.

The fiscal impact of austerity has already affected electoral politics. In all countries

that have resorted to austerity (spending cuts, tax increases, structural and labor reforms)

in response to the crisis, governments have been voted out of office. In addition to the

governments of periphery countries, the Dutch government fell in late April 2012 as a

result of disagreements over the nature and extent of further fiscal tightening. On May 6,

4 “Defense Spending: Economy Trumps Strategy”, Swiss Federal Institute of Technology, Feb 15, 2012 http://ww w.isn.ethz.ch/isn/Current-Affairs/Special-Feature/Detail?lng=en&id=137230&contextid774=137230&contextid775=137227&tabid=137227 Swiss Federal Institute of Technology, International Relations and Security Network http://ww w.isn.ethz.ch/isn/Current-Affairs/Special-Feature/Detail?lng=en&id=137230&contextid774=137230&contextid775=137227&tabid=137227 Swiss Federal Institute of Technology, International Relations and Security Network 5 Ibid. 6 On 9 June, after emergency talks, Spain's Economy Minister stated that Spain would make a formal request for €100bn in loans from eurozone funds to shore up its banks. http://www.bbc.co.uk/news/business-13856580

7

French voters elected an anti-austerity president, Francois Hollande, the first socialist

prime minister in seventeen years. On the same day, Greek voters punished the

mainstream parties and elevated an anti-austerity, radical left-wing party to second place.

On 17 June, in a second round of elections that attracted worldwide attention for their

implications, Greece’s Syriza (socialist and radical left coalition) maintained its second

place and is about to become the main opposition party. The governing coalition of New

Democracy (center right), PASOK (center left) and DIMAR (socialists), formed on 21

June, is likely to be short lived.

The impact and consequences of austerity are forming Europe’s new fault lines.

Greece’s rescue from certain default in May 2010 delayed but did not avert a deeper

crisis or its contagion effects. Two years hence, the EU has three member states (Greece

plus Ireland and Portugal) on rescue loans, two large economies (Italy and Spain) in dire

financial condition, many states in protracted recession, rising unemployment and

joblessness, and political and social turmoil throughout. Spain is the fourth country in

need of a bailout to deal with deteriorating finances and a full blown banking crisis. In

the meantime, European policy makers have pledged even more austerity in the future.

At Germany’s initiative, a new Fiscal Compact has been signed by 25 of the 27 EU

states: it includes a “golden rule”, namely, a balanced budget requirement in national

constitutions and automatic correction mechanisms for the imposition of penalties if the

rule is breached. Earlier evidence on the efficacy of such rules is not encouraging. The

Growth and Stability Pact, which provided a set of fiscal rules to guarantee the viability

of the euro, was violated by most member states, including the pact’s prime architects,

France and Germany.

The specter of austerity and its consequences have reintroduced issues long

considered resolved: the size and membership of the Eurozone, the role of the euro as the

world’s second reserve currency and Europe’s economic prowess and global reach. Open

references to Greece’s exit from the Eurozone and preparations made by public and

private entities for such an eventuality have already cast serious doubt on the future of the

European project. Fears of contagion have persisted. Are Spain and Italy too big to be

8

rescued? Is there a mechanism and, above all, political will to contemplate rescue loans

for all who apply? The answers remain elusive. The European Stability Mechanism

(ESM), which will operate like a European Monetary Fund, has about €500 billion that

can be used for rescue loans, though not right away. 7 This sets a limit to the price of

solidarity –for now. The EU has an economy larger than and as advanced as the US.

Like the US, the EU could allocate fiscal and financial resources necessary to contain and

mitigate the effects of the debt crisis. Yet, to date, the US has had better success in

containing the crisis than the EU. This seems all the more paradoxical, considering that

the American economy has a higher level of indebtedness than the EU and a larger

deficit-to-GDP ratio. The difference is that the US is a sovereign state with a government

that can act to project and protect the state’s interests, including its currency. This is not

the case with the EU or the Eurozone.

The global financial crisis has exposed serious flaws in the economic governance of

the Eurozone. Its institutions and policies have proved ineffective in averting a sovereign

debt crisis and in facilitating its management; in mitigating the effects of recession and

unemployment; and in preventing a banking crisis. New and untested policies not

provided for or envisaged by the EU founding treaties, crafted on an ad hoc basis so as to

overcome the no-bailout clause of the Maastricht Treaty and incorporated in rescue loans

to Eurozone member states, have proved inadequate. Reluctance on the part of the EU to

shoulder the full cost of policies to stem the effects of the crisis led to the involvement of

the IMF, an extra-European institution, in the financing of the bailout loans, with US

support. What explains this scheme? The EU’s supranational governance: it was

created and remains without a sovereign. The EU has a foreign minister but still lacks a

finance minister, a treasury, a fiscal policy and a real budget commensurate with the

needs of the EU economy, and a real parliament with authority to tax and spend in

accordance with taxpayers’ demands. In addition, the EU is bound by a treaty that allows

7 These funds remain hypothetical until 2014. The amount of funds that may end up in ESM may change in the future. The key issue is which countries will contribute, when and how much. For an update on recent developments, see http://topics.nytimes.com/top/reference/timestopics/organizations/e/european_financial_stability_facility/index.html

9

member states to issue sovereign debt in a currency they do not control while prohibiting

the issuance of sovereign debt by a Eurozone entity or in its behalf.

The biggest challenge of the debt crisis comes mainly from the fact that the Eurozone

is not a state. Neither is the EU a state. The euro's status as a stateless currency, without

a recognized sovereign to back it up, is not sustainable. For Europe not to fail, "more

Europe" requires more of the attributes of a sovereign entity that can guarantee the euro.

Without political will to create a sovereign United States of Europe, the prospect of

perpetual austerity is likely to intensify forces of disintegration and instability that could

further undermine the viability of the euro. Will Germany, as Europe’s strongest

economic power, want to play the role of the EU’s sovereign? Alternatively, would

Europe’s sovereign states, to include Germany and France, delegate even more powers to

Brussels to act as the EU’s sovereign? These seem to be the two alternative paths that

can lead the EU out of the crisis. The choice of path will be a critical determinant of the

size, structure and the political, economic and social identity of post-crisis Europe.

Challenges of the Crisis from a Greek Perspective

Greece is in its worst ever economic downturn, financial disarray and political and

social turmoil since the end of WWI. In October 2009, Greece announced a budget

deficit 12.7 % of GDP. The Eurozone was presented with its first-ever possible default

of a member state. Greece became the subprime crisis of the EU. In May 2010,

following top level meetings in Washington to set the framework for rescue operations,

Eurozone governments and the IMF arranged €110 billion rescue loan for Greece with

strict austerity measures to reduce the government deficit and structural economic

reforms to improve competitiveness. The immediate goal was to prevent a Greek default.

The first troika (IMF, EU and ECB) program showed signs of failure after one year of

reform. The program’s aims and the ways in which they were perceived by the public,

the body politic and Greece’s lenders were diverging. By June 2011, it was evident that

10

the rescue loan was not meeting expectations and a second loan, larger than the first, was

in the works. The first rescue loan had failed to achieve its aims. The reforms that were

imposed as conditions for success were long overdue and could promote a more open,

transparent, meritocratic and competitive economy. But the attached timelines were

unrealistic: implementation of big, structural changes was tied to a short-term default

avoidance program, on top of severe fiscal contractionary measures.

In its March 14, 2011 review of Greece’s implementation of reforms, the IMF stressed

that tax collection must be improved, spending further curtailed and the privatization

program be scaled up. 8 Reform of the Greek public sector, which includes a historically

corrupt tax collection system and rampant tax evasion, had the potential to make a big

budgetary impact. But how long would it take to set up a new tax collection authority that

operated with integrity and transparency? How quickly could Greece’s bloated and

wasteful public sector be tamed, reduced in size and made more efficient? The Greek

government took its first-ever census of government employees in late 2009 to determine

the number of workers on the public payroll, their salaries and other compensation, and

their job responsibilities. It took months to organize and conduct the census, which is still

not complete. How long would it take to reorganize ministries, offices and jobs, even if

the Greek government were truly committed to such an undertaking? It took the US

Department of Defense, with its elaborate and comprehensive human resources

management system, more than two years to reform just the pay system covering defense

civilians. Reorganizations at the IMF and the World Bank in the 1990s were equally

demanding and time-consuming affairs that took years to complete. How could the Greek

government enact similar reforms in less time?

The rescue loans included requirements to secure €50 billion from privatizations of

companies, such as the Hellenic Post Bank and the Hellenic Telecom Organization,

among others. Privatization program timelines were highly unrealistic. How long might

it take to establish an agency to sell off public assets? Germany’s post-re-unification

experience suggests that such an undertaking could require years of work. Greece does

8 IMF Press Release No. 11/77 March 14, 2011

11

not have the capacity, organizational know-how and administrative experience that

Germany employed. Placing a foreign entity, the EU’s Task Force, in overt charge of

such an undertaking was politically unacceptable to the Greek people. For its part, the

Greek government had been unable to complete a national land registry in over a decade;

this was despite penalties imposed by the EU, which has funded the land registry project.

Even if lack of political will or administrative competence had not been factors, prompt

sale of public assets would have been complicated if not administratively and judicially

impossible because of incomplete or missing public property records.

In its May 2011 report, the Greek government stated that it had achieved “the largest

fiscal consolidation in the Eurozone; that it had undertaken deep expenditure cuts and tax

measures and implemented far-reaching structural reforms”, lowered public sector wages,

bonuses, pensions and benefits; eliminated positions; and increased taxes (VAT at 20%

across the board; excise taxes raised by 33% on fuel, cigarettes and alcohol). 9 It

remained unclear whether the Greek government was aware that these measures were

highly contractionary and bound to deepen the recession. But the Greek government did

fail in communicating it to the public at large and in not proposing a credible program to

offset even in part the contraction that was sure to follow. Real wages per capita fell by

almost 8 % in 2010 and the decline continued in 2011. Unemployment rose to 17%.

According to an estimate by the Financial Times10, by November 2011 the average

household income in Greece had been reduced by 14% (twice as much as the reduction

suffered by Irish and Portuguese households).

The rescue loan’s structural reform provisions were aimed at improving the

competitiveness of Greece’s economy through reductions in the cost of labor. Falling

living standards as a result of recession and joblessness do not necessarily lead to a more

competitive economy. Lowering the statutory minimum wage, freezing cost of living

increases and eliminating bonuses at a time of economic turmoil, deep recession and a 9 Hellenic Ministry of Finance Policy Programme Newsletter, 19 May 2011 10 Greek austerity plans threaten growth, Financial Times, 17 October 2011 http://im.media.ft.com/content/images/2081e0ae-f8e9-11e0-a5f7-00144feab49a.img?width=639&height=444&title=&desc=Household income graphic

12

negative economic outlook do not automatically lead to improved competitiveness.

Salary, compensation and benefit cuts may be a necessary condition but they do not

constitute a sufficient condition. Factors like know-how, research and development,

business organization, innovation and knowledge-based production, cultivation and

utilization of scientific and engineering talent, are at the heart of a modern, competitive

economy. 11 Unlike fiscal reforms, human resource development-oriented labor market

reforms require time; they cannot be had, made or applied over the short term or when a

country is on the verge of default, with its economic and political institutions outmoded,

dysfunctional and in disarray.

Unrealistic timelines for fundamental, long term changes may be indicative of a basic

flaw in the troika’s assumptions and recommendations: that there exists in Greece a

public administration with the capacity to carry them through. This, however, is not the

case. As an OECD review of Greece’s central administration concluded in December

2011, reforms depend crucially on a well functioning public administration: “Strong

measures, starting now, to improve the effectiveness, accountability and integrity of the

public administration so that it is "fit for purpose" are a priority. The success of reforms

such as privatisation, fiscal consolidation, debt reduction, tax collection and enhanced

competitiveness is at stake.” 12

A critical failure of the austerity implementation programs was the disregard for

fairness in the distribution of the adjustment burden. The Greek government’s choice of

across-the-board wage and pension cuts placed a disproportionate burden on lower

income earners and retirees, contributing to a widely shared perception of grave injustice.

Public sector employment remained shielded from firings as unemployment exploded in

the private sector. The burden of indirect taxes, to include a new property tax, increased

significantly. The administrative chaos and lack of records across the spectrum of

ministries was reflected in the Ministry of Finance decision to outsource the property tax

collection to the Public Power Company, DEH. Further, use of DEH’s customer data 11 The importance of these factors is stressed in a comprehensive OECD Report, Greece at a Glance Policies for a Sustainable Recovery, 2011, http://www.oecd.org/dataoecd/6/39/44785912.pdf 12 OECD, “Greece: Review of Central Administration”, 2 December 2011.

13

base to collect the tax linked failure to pay to electricity cut offs to businesses and

households. This tax, on top of other levies, surcharges and revelations of rampant tax

fraud, enraged the Greek public. On a poll taken in May 2011, a significant majority of

the people had a negative image of the IMF and felt that the program was a bad decision

that hurt the economy and the country; over 90 % feared for the future, their jobs and

their businesses; two thirds of respondents felt that the possibility of default was likely;

and over half said that the best solution to the debt problem is to repay only part of it after

negotiation with the lenders.13

The public’s assessment of the depth of the crisis was accurate. Greece’s economy has

continued to contract. It has shrunk by one fifth since the crisis began, receding by over

6% in the first quarter of 2012. Unemployment has risen to over 22%; unemployment for

women is 40% and youth unemployment is over 50%. Business failures are the highest

recorded in the post WWII period. By measures of the real economy, Greece was in

worse shape one year into the implementation of the Mnemonion, the memorandum

attached to the first bailout loan. Two more rounds of drastic austerity measures taken in

July of 2011 and February 2012, as required by the troika, deepened the recession and

increased unemployment even further while growth stalled across the whole of the

Eurozone. In March 2012, the troika determined the need for a second rescue loan of

€130 billion. In addition to austerity measures, this bailout included a large write-down

of Greece’s debt, or private sector haircut of €100 billion, yet still leaving Greece with a

debt-to-GDP ratio of 177%.

The bailout loans have not improved Greece’s growth prospects, even as the

country’s debt continues to rise. The first loan helped Greece to the extent that it helped

its creditors, to include European banks and taxpayers; without the loan, Greece would

have defaulted by summer of 2010. The second bailout produced similar effects. It

helped Greece’s foreign creditors minimize their losses but decimated domestic investors,

including Greek banks and insurance funds, which had been required to convert part of

13Public Issue, 18 May 2011, http://www.eklogika.gr/uploads/files/pdf_files/pi-skai-all-18-5-2011.pdf

14

their assets to Greek sovereign bonds, a practice that spanned several decades. The

structure of the second bailout was not aimed at reviving the Greek economy. It was

primarily oriented to meet the needs of international creditors, especially European

banks, who were in direct receipt of about one fourth of the loan. The remaining €100

billion, to be paid in installments contingent on successful program reviews, is meant to

facilitate debt repayment. It does not contain measures to promote growth. 14 The

prospects for future success are bleak; Greece’s official lenders have referred to the

bailouts as money thrown into a bottomless barrel. Comparisons of the bailout funds to

economic aid offered to European states, especially Germany, under the US-inspired

Marshall Plan can be misleading.15 Greece has not received Marshall Plan-type aid from

the EU. A strong case can be made that it should have on grounds that such aid could

have prevented the collapse of Greece’s economy and the social and political turmoil that

ensued. As matters stand, the economics and politics of Europe’s debt crisis are not

favorable to fundamental changes in Greece’s bailout program.

The biggest challenge of the crisis from a Greek perspective is that the country was

admitted to a club in which it did not belong to begin with, and that its economic and

financial performance would be judged on the basis of standards beyond its government’s

grasp and reach. Although Greece’s political class bears the heaviest share of the blame

for non-performance, EU decision-makers should remain cognizant of their own

responsibility for the resulting tragedy. The decision to admit Greece to the Eurozone

was premature if not altogether wrong. The EU sidestepped issues of transparency and

competence of Greece’s public administration, lack of competitiveness, structural

impediments and market dys-functionalities that have plagued Greece’s economy for

14 According to a German commentator, “[The € 100 billion] isn’t geared to what Greece needs in order to get back on its feet. It’s linked to an estimate of how much debt the Greek economy can bear without collapsing…with debts amounting to 120 percent … the country can just about go on servicing its debt. That’s the level at which the cow can go on supplying milk without dying…” See Christian Rickens, “The EU should admit Greece is bankrupt”, Der Spiegel, 20 February 2012. http://www.spiegel.de/international/europe/stop-the-second-bailout-package-eu-should-admit-greece-is-bankrupt-a-816498.html 15 Such a comparison is made by Hans-Werner Sinn in “Why Berlin is Balking on a Bailout”, International Herald Tribune, June 12, 2012. For a historical perspective, see Albrecht Ritchl, “Germany, Greece and the Marshall Plan”, The Economist, June 15, 2012.

15

decades. The EU’s monitoring and auditing mechanisms and authorities were slow in

enforcing macroeconomic discipline. Finally, faced with the prospect of Greece’s default

in the spring of 2010, both the Greek government and its official lenders signed up to

rescue loans containing harsh terms and unrealistic objectives. As a result of these fateful

decisions, Greece has taken on many of the characteristics of a failed state. This unhappy

legacy is the greatest challenge of Europe’s debt crisis.

16

APPENDIX

Tables and Figures

17

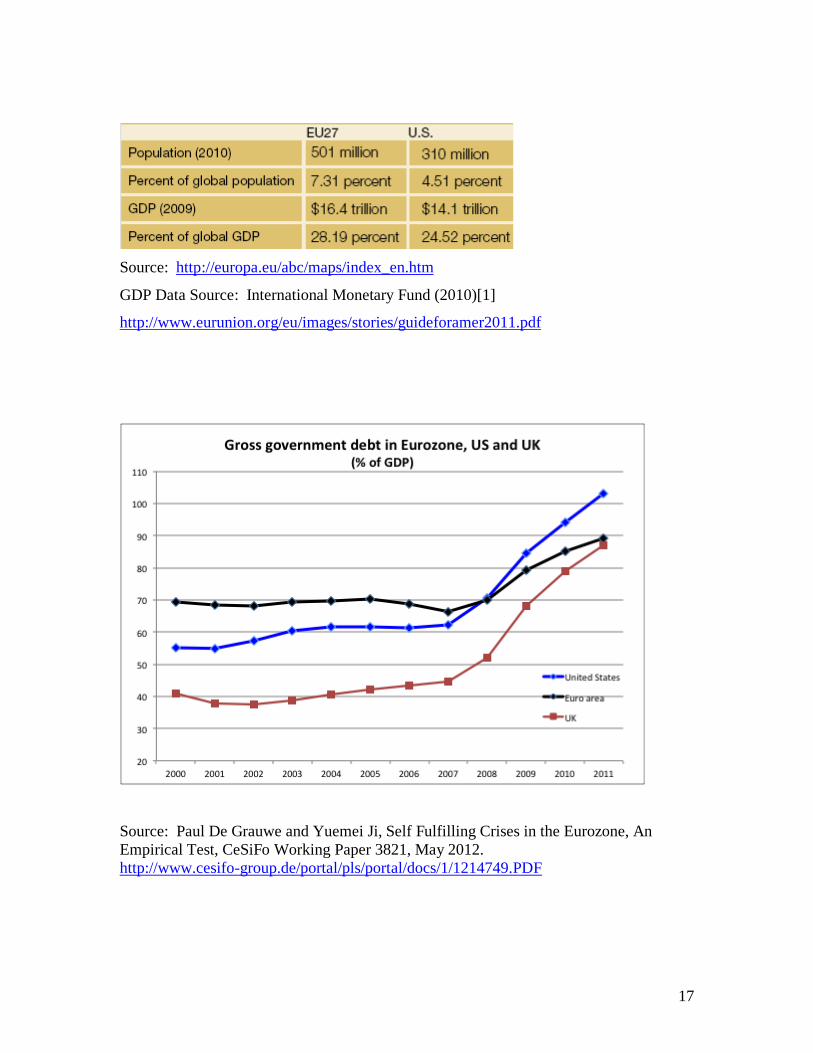

Source: http://europa.eu/abc/maps/index_en.htm

GDP Data Source: International Monetary Fund (2010)[1]

http://www.eurunion.org/eu/images/stories/guideforamer2011.pdf

Source: Paul De Grauwe and Yuemei Ji, Self Fulfilling Crises in the Eurozone, An Empirical Test, CeSiFo Working Paper 3821, May 2012. http://www.cesifo-group.de/portal/pls/portal/docs/1/1214749.PDF

18

4

Europe’s Economic Crisis in Figures: Deficits

Ireland -13.1%Greece -9.1%Spain -8.5%UK -8.3%France -5.2%

EZ 17 -4.1%EU 27 -4.7%

Government Deficit as % of GDP, 2011

Source: Eurostat. 23 April 2012 :

http://epp.eurostat.ec.europa.eu/cache/ITY_PUBLIC/2-23042012-AP/EN/2-

23042012-AP-EN.PDF

19

6

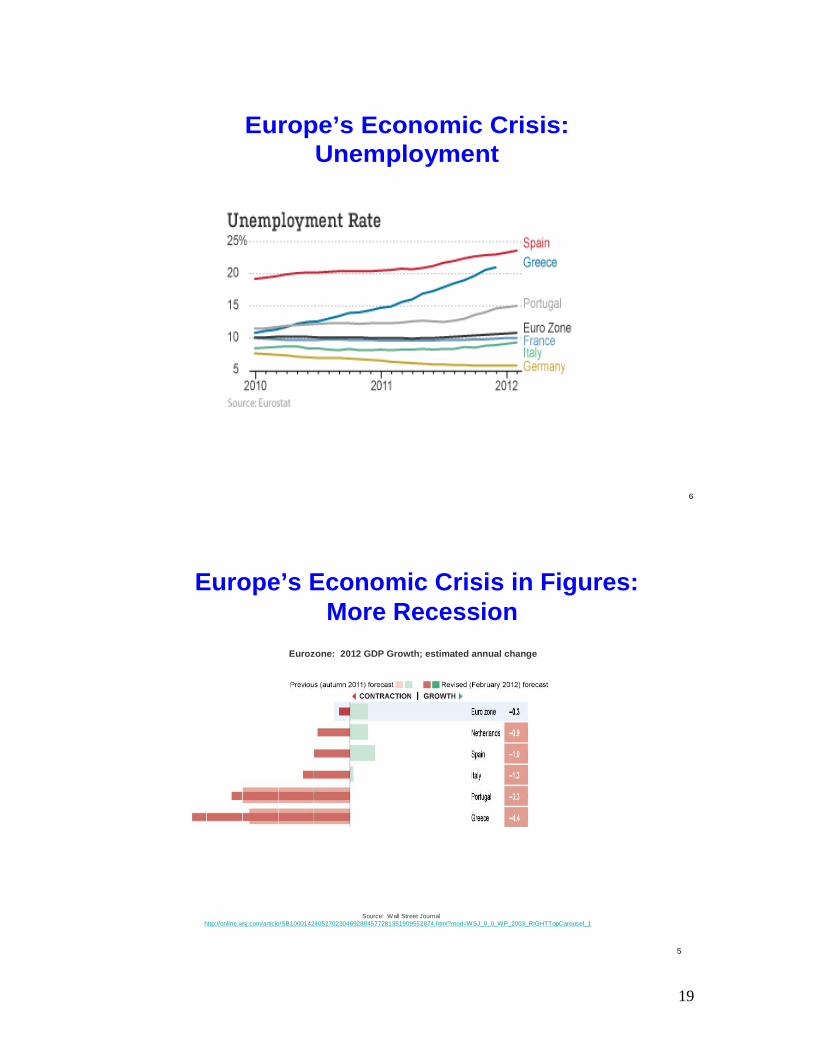

Europe’s Economic Crisis: Unemployment

5

Eurozone: 2012 GDP Growth; estimated annual change

Source: Wall Street Journalhttp://online.wsj.com/article/SB10001424052702304692804577281351909552874.html?mod=WSJ_0_0_WP_2003_RIGHTTopCarousel_1

Europe’s Economic Crisis in Figures: More Recession

20

Source: Ralph Atkins, Eurozone debt crisis weighs on Germany, Financial Times, 21 June 2012

21

11

GDP and Defense Spending, 1998-2010

Source : Swiss Federal Institute of Technology, “Defense Spending: Economy Trumps Strategy”, Feb 2012 http://www.isn.ethz.ch/isn/Digital-Library/Special-Feature/Detail/?lng=en&id=137230&contextid774=137230&contextid775=137227&tabid=137227%2520Swiss%2520Federal%2520Institute%2520of%2520Technology,%2520International%2520%2520Relations%2520and%2520Security%2520Network

22

Source: Wall Street Journal, 19 June 2012

http://online.wsj.com/article/SB10001424052702303379204577474652466408254.html?

mod=WSJ_hpp_LEFTTopStories

23

Source: Financial Times, 18 June 2012 http://www.ft.com/intl/cms/s/3/e945d040-b932-

11e1-9bfd-00144feabdc0.html#axzz1yHCNY8Fr

24

Der Spiegel, 19 June 2012, http://www.spiegel.de/international/europe/bild-839726-

365359.html

25

Source: OECD ECONOMIC OUTLOOK, V 6 OLUME 2011/2 © OECD 2011 –

PRELIMINARY VERSION 1 2 http://dx.doi.org/10.1787/888932541607