ch 8 cost and revenue

TRANSCRIPT

Cost and Revenue

Economy• Consumer has wants.• To satisfy wants a Producer produces goods and

services.• To produce goods and services a producer has to

bring together the factors of production.• The producer has to spend money to pay for

these factors of production.• The producer starts earning only after production

is over and he sells the goods and services.

Example

Land

1. The land can be the farmers own land.2. He may hire the land and pay rent.3. He may buy the land by paying money.4. In our example we will say that he hires the land and pays a rent of

Rs.5000/- for the entire period till harvesting.__________________________________________________________

So his cost on land = Rs. 5000/-

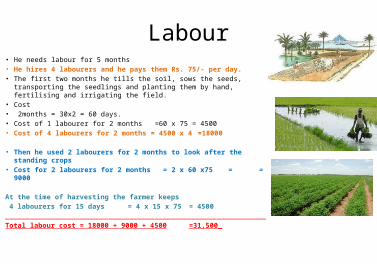

Labour• He needs labour for 5 months• He hires 4 labourers and he pays them Rs. 75/- per day.• The first two months he tills the soil, sows the seeds, transporting the seedlings and

planting them by hand, fertilising and irrigating the field.• Cost • 2months = 30x2 = 60 days.• Cost of 1 labourer for 2 months =60 x 75 = 4500• Cost of 4 labourers for 2 months = 4500 x 4 =18000

• Then he used 2 labourers for 2 months to look after the standing crops• Cost for 2 labourers for 2 months = 2 x 60 x75 =

= 9000

At the time of harvesting the farmer keeps 4 labourers for 15 days = 4 x 15 x 75 = 4500_______________________________________________________________Total labour cost = 18000 + 9000 + 4500=31,500_

Capital• To grow the crops he needs• Seeds• Fertilizers• Pesticides• Total cost of above materials = 3000• He needs a Tractor• He rents it for Rs. 2500/- =2500• ___________________________________• Total cost on capital

=5500

Total Cost

• Lets calculate his total cost• Items

Expenditure • Land =

5000• Labour =

31,500• Capital =

5500• Total cost = 42,000

Output

• The farmer was able to produce 30 quintals of

wheat.(1 quintal = 100kg1 kg = 1000gms)

Definition of Cost

• Cost is defined as the money expenditure

made by the producer

to buy or hire

factors of production

and raw materials

to produce goods and services

Type of CostsFixed and Variable

Fixed Cost: The farmer has rented the land for Rs.5000/- he may use it for farming or he may not. What ever he does he has to pay Rs. 5000/- that is fixed. Therefore it is called a fixed costs it does not depend on anything

Variable Cost : He has to hire a labourer he may hire 2 or 4 depending on the no. of labourers he hires he pays the wages. Therefore it can be different or it can vary , so labour cost is called a variable cost. Fixed VariableLand 5000

• Labour 31500

• CapitalTractor 2500SeedFertilizer 3000PesticideWater__________________________________________________

750034,500

Total cost Fixed cost + Variable cost = 42,000

Type of costsExplicit and Implicit

• Explicit Cost : The cost that the farmer pays for land, labour, raw material are all direct costs.

• So direct payments made by the farmer for land, labour and raw materials are called explicit costs.

• Implicit Cost : There may be things he uses which are his own, for which he did not have to pay

• Eg. If he had a tractor he would not have to hire it.But if he would rent it to somebody else he would get a rent of Rs.2500/-

• By using it himself he is losing the rent of Rs.2500/-.• So he will add this in his cost. Such a cost is called implicit cost or indirect

cost.• Implicit cost is the cost of self supplied factors

Total cost and average cost• Total cost = Fixed cost + variable cost = 42,000

• Average cost = Total cost/ Total output • 42,000/ 30 quintal

= 1400 per quintal is the cost

• This will give us cost per quintal (cost per unit)

Marginal cost

• If the producer wants to increase out put, then he has to hire one more labourer.

• This will lead to increase in total cost (because the labourer has to be paid wages).

• So, increase in total output will lead to increase in total cost.

• Marginal cost is defined as increase in the total cost due to increase in one extra unit of labour

Example• Suppose a tailor makes

10 shirts and his total cost was Rs. 1110/-.

• Then he increased shirt production to 11 pieces for which his total cost was Rs. 1199/-

• What is his marginal cost ?

• The marginal cost = 1199 - 1110 = 89

• The output increased by (11 -10 = 1) 1 shirt

Another example

• If 48 units of output are produced and • the total fixed cost is Rs. 180/-• The variable cost is Rs. 300/-• WHAT WOULD BE THE AVERAGE COST ?• Total cost/ total output 480/48 = 10• Average cost is the cost per unit of output, so the AC is Rs.10/- per unit of

output.• Let output increase to 49 units.• The variable cost increases to Rs.307/-• WHAT IS THE MARGINAL COST ?• Earlier cost = 180+300= 480 Current cost is 180 + 307 =487• MC = 487-480 = Rs.7/-.

Comparing Marginal cost and Average cost

• In the previous example we can calculate 2 average costs.

1. The average cost for 10 pieces of shirt with total cost = Rs.1110/- is AC = Total cost/total output =

1110/10 = Rs.111/-

2. The average cost for 11 pieces of shirt with total cost = Rs 1199/- isAC = Total cost/Total ouput= 1199/11 =

Rs.109/-Average cost is calculated for every given level of output.Marginal cost is calculated when a given level of output is increased by one unit.Units of output Total cost Average cost Marginal cost10 1110 111

--------11 1199 109

89 (1199 -1100)

Revenue• Revenue is defined as the amount a person receives by selling a

certain quantity of commodity.

• Revenue = Price of a commodity x Quantity of the commodity.• If a seller sells a shirt at Rs. 100/- per piece, • A customer comes and buys 4 shirts • Revenue to the seller is 100 x 4 = Rs.400/-

• During a week the seller sells total 20 shirts• So his Total revenue for that week will be 100 x 20 =Rs.2000/-• Let us denote each term with an alphabet• Total Revenue =TR; Price = P; Quantity = Q• Total Revenue = Price x Quantity So we can say TR = P x Q

Average and Marginal Revenue

• Average Revenue(AR) is calculated as • AR = Total Revenue/Quantity sold = TR/Q

• Take the case of a single commodity

• We know TR = P x Q• therefore AR = P x

Q/Q = P

• So Average Revenue and Price of a commodity are one and the same.

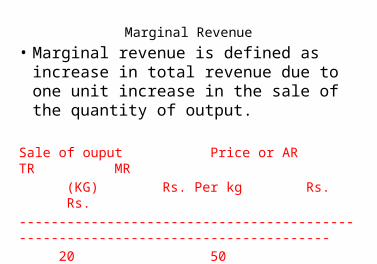

Marginal Revenue

• Marginal revenue is defined as increase in total revenue due to one unit increase in the sale of the quantity of output.

Sale of ouput Price or ARTR MR

(KG) Rs. Per kgRs. Rs.

--------------------------------------------------------------------------------- 20 50

1000----

21 501050

50

Comparing AR and MR

1. If the seller is able to sell quantities of output at the same price

Then AR =MR2. If Price of the commodity changes

Then AR and MR will be different.

Use of Revenue and Cost

• Cost is the expenditure incurred to produce a good or service during the production process.

• Revenue is the money received by the producer for selling that good or service.

• Cost is the sacrifice by the producer.

• Revenue is the gain for the producer.

• By getting the revenue he recovers the cost he incurred earlier.

• Profit is the surplus of revenue over the total cost of production

• Profit = Total Revenue – Total cost.

Thank you