cftc compliance following ‘harmonization’ – what mutual ... · pdf filecftc...

TRANSCRIPT

1

CFTC Compliance Following ‘Harmonization’ – What Mutual Fund Directors Need To Know

Michael Hoffman – Investment ManagementDaniel S. Konar II – Derivatives

August 28, 2013

2

Background

• On April 24, 2012, the CFTC narrowed the Rule 4.5 commodity pool operator (CPO) exclusion for registered investment companies (RICs) by adding marketing and de minimis trading restrictions and by requiring advisers to re-claim the exclusion annually.

• Legal challenges to the amendments to Rule 4.5 failed at both the district and appellate courts:

– Investment Company Institute v. CFTC, 891 F. Supp. 2d 162 (D.D.C. 2013)– Investment Company Institute v. CFTC, 720 F.3d 370 (C.A.D.C. 2013)

• Investment advisers of RICs that could not meet the marketing and de minimis trading restrictions in amended Rule 4.5 (RIC CPOs) were required to register as CPOs with the CFTC by December 31, 2012.

– The CFTC estimates that 418 advisers registered as RIC CPOs.• For these RIC CPOs, compliance with the CFTC’s CPO regulations was stayed

pending the adoption of the CFTC’s Harmonization Rule.• On August 13, 2013, the CFTC released its Harmonization Rule, which largely allows

a RIC CPO to substitute compliance with the SEC’s RIC regulations for compliance with the CFTC’s CPO regulations.

• The SEC staff issued companion guidance for RICs addressing related matters.

3

How Has Harmonization Changed the Rules for RIC CPOs?

• No change for RICs that satisfy Rule 4.5.

• For other RICs, the RIC CPO must:– file a notice of use of substituted compliance with the National Futures

Association (NFA);

– if the RIC has less than three years of operating history, disclose the performance of accounts or other pools with substantially similar investment objectives and policies in the RIC’s registration statement;

– modify certain legends in RIC disclosure documents; and

– file the RIC’s annual reports with the NFA.

• In addition, the Harmonization Rule means that RIC CPOs must:– file systemic risk reports on CFTC Form CPO-PQR;

– file a notice with the NFA if the CPO maintains books and records with a third-party service provider (as opposed to the CPO’s main place of business); and

– file a statement from the service provider agreeing to maintain books and records in accordance with CFTC requirements.

4

What Regulations Needed Harmonization?

• Timing of delivery of disclosure documents to investors

• Timing and filing of updates to disclosure documents

• Review and acceptance of disclosure documents by NFA

• Signed acknowledgement requirement for receipt of disclosure documents

• Use of summary prospectus by open-end RICs

• Content of prescribed risk disclosures

• Timing of financial reporting to investors

• Certain disclosures regarding fees

• Required disclosure of (unrelated) past performance

• Treatment of controlled foreign corporations (“CFCs”)

• Distribution and filing of financial statements

• Recordkeeping requirements

5

What Did Harmonization Do?

Original CFTC Requirement Harmonized RIC Requirement

1. Update disclosure document every nine months.

Comply with current SEC annual update requirement.

2. Correct material inaccuracies in disclosure documents within 21 days of discovering defect.

Comply with current SEC update requirements.

3. May not use a disclosure document until the NFA has reviewed and accepted.

Comply with current SEC review process. No need to file disclosure document with NFA for review or acceptance.

4. Must receive signed acknowledgment of receipt of disclosure document from prospective investors before accepting funds.

Comply with SEC disclosure document delivery requirements.

5. Not expressly permitted to use a summary prospectus.

May use summary prospectus that complies with SEC requirements.

6. Include CFTC prescribed legends in disclosure document.

Can use current SEC mandated legend provided a minor change is made to reference the CFTC.

7. Include CFTC-mandated risk disclosures in disclosure document.

Risk disclosure that satisfies SEC requirements deemed to satisfy CFTC requirement.

8. Disclose fees in “break-even table” (time needed to recoup fees and expenses applicable to investor in first year of investment).

Current SEC fee and expense disclosure deemed to satisfy CFTC requirement.

6

What Did Harmonization Do?

Original CFTC Requirement Harmonized RIC Requirement

9. Include past performance of the CPO’s other pools in a disclosure document of a RIC with less than three years operating history.

CPOs of RICs with less than three years of performance history required to provide performance of all accounts and pools that have substantially similar investment objectives, policies and strategies.

10. Disclose certain fees applicable to the RIC, including brokerage fees.

Compliance with SEC mandated fee and expense disclosures deemed sufficient.

11. CPOs of CFC subsidiaries of RICs required to prepare separate, CFTC-compliant disclosure documents (unless qualifying for an alternate exemption from CPO registration).

No special CFC disclosure required if RIC provides full disclosure of material information relating to CFC. CFC financial statements need not be separately filed with the NFA if consolidated with the RIC’s financial statements.

12. Distribute directly to investors monthly account statements and annual reports.

RICs need not comply, provided their “current net asset value per share” is available to investors and it furnishes annual and semi-annual reports as required by SEC.

13. File CFTC-compliant annual reports with the NFA.

RIC CPOs must submit the RIC’s annual reports to the NFA.

7

What Did Harmonization Do?

Original CFTC Requirement Harmonized RIC Requirement

14. Keep books and records at the CPO’s main office and make them available to investors.

RICs may continue to keep books and records at third-party service providers. The RIC’s adviser is required to make a notice of filing with the CFTC and service provider must agree to maintain books and records in accordance with CFTC requirements.

15. Make the RIC’s books and records available for inspection and copying by investors upon request.

RIC CPOs are exempted from this requirement.

8

When Are These Changes Occurring?

CPO Registration and Compliance Effective Date

Registration as a CPO if RIC cannot qualify for Rule 4.5 December 31, 2012

Substituted compliance concerning SEC annual reports August 22, 2013

Substituted compliance concerning the contents and distribution of SEC registration statement

September 23, 2013

Compliance with CPO disclosure, reporting and recordkeeping requirements

October 21, 2013*

* CFTC staff has confirmed that disclosure requirements need not be complied with until a RIC otherwise needs to update its prospectus under SEC rules.

9

What Obligations Flow From CPO Registration?

• RIC CPO compliance obligations fall into three categories:– Disclosure

– Reporting

– Recordkeeping

10

The Disclosure Requirements

• Substituted compliance disclosure for RIC CPOs:– File a notice of use of substituted compliance with NFA.

– Disclosure documents for a RIC with less than three-years operating history must disclose performance of the RIC CPO’s other “accounts and pools” with “substantially similar investment objectives, policies and strategies.”

– A disclosure document must include a hybridized prescribed legend indicating neither the CFTC nor the SEC has approved of the securities being offered.

• SEC staff has indicated the hybrid legend is permissible.

11

Performance History Disclosure

• The most intrusive new requirement is to disclose performance history of other “accounts and pools” with “substantially similar investment objectives, policies and strategies” for RICs with less than three years of operations.

– “Accounts and pools” do not appear to be limited to other RICs.– No guidance on “substantially similar investment objectives, policies and

strategies.”• The CFTC’s adopting release explains that any “subjectivity is tightly

constrained due to the guidance that SEC staff has provided in this area,” and cites to SEC no-action letters ITT Hartford Mutual Funds and Nicholas Applegate Mutual Funds, but these letters do not provide much color.

– No guidance on whether affiliated advisers are covered, and if so, under what circumstances.

• If disclosure of past performance of other accounts and pools is required by a RIC CPO, inclusion in the SAI presumably would satisfy this requirement.

12

Performance History Disclosure

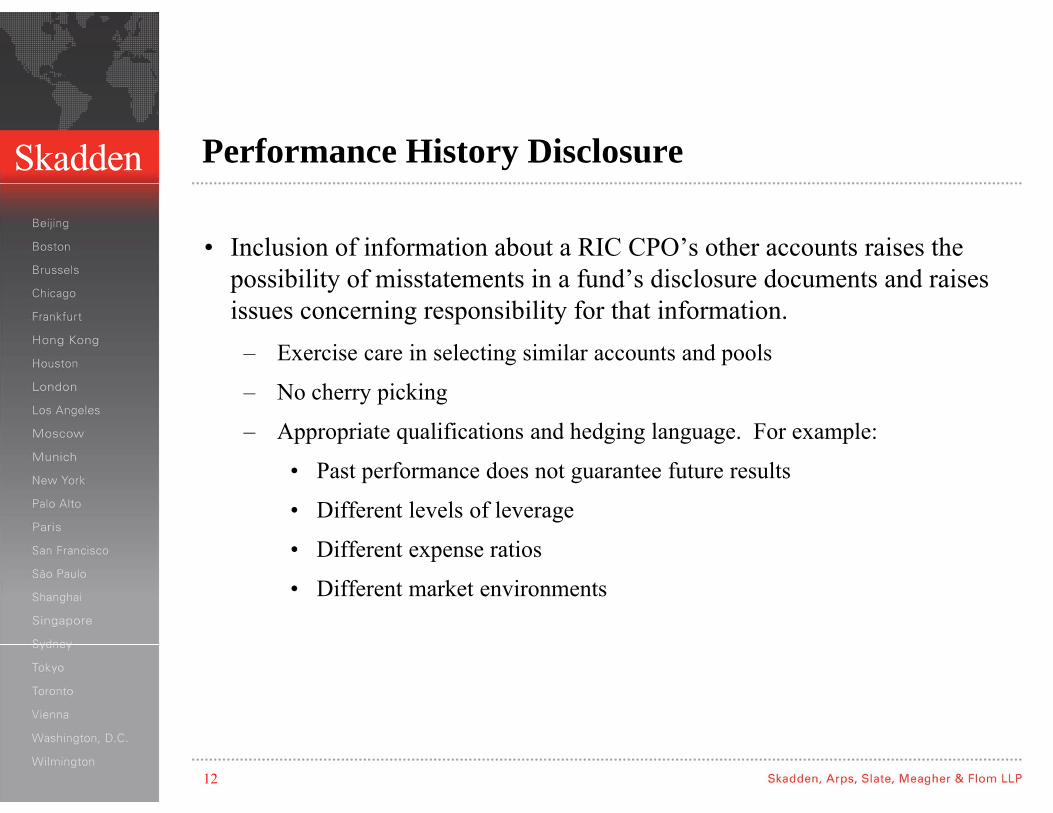

• Inclusion of information about a RIC CPO’s other accounts raises the possibility of misstatements in a fund’s disclosure documents and raises issues concerning responsibility for that information.

– Exercise care in selecting similar accounts and pools

– No cherry picking

– Appropriate qualifications and hedging language. For example:

• Past performance does not guarantee future results

• Different levels of leverage

• Different expense ratios

• Different market environments

13

Additional NFA Disclosure Requirements

• The NFA has disclosure rules which apply to registered CPOs in addition to the CFTC’s rules.

• Compliance with the NFA’s disclosure-related rules remains an open issue for RIC CPOs – NFA staff has temporarily allowed RIC CPOs to comply with applicable SEC rules in lieu of the following NFA rules:

– Rule 2-13 (certain disclosure document requirements regarding break-even analyses, “up-front fees,” and organizational and offering expenses);

– Rule 2-29 (promotional materials other than anti-fraud);

– Rule 2-34 (CTA performance reporting and disclosures for sub-advisers to RICs); and

– Rule 2-35 (contents and delivery of disclosure documents).

14

Additional NFA Disclosure Requirements

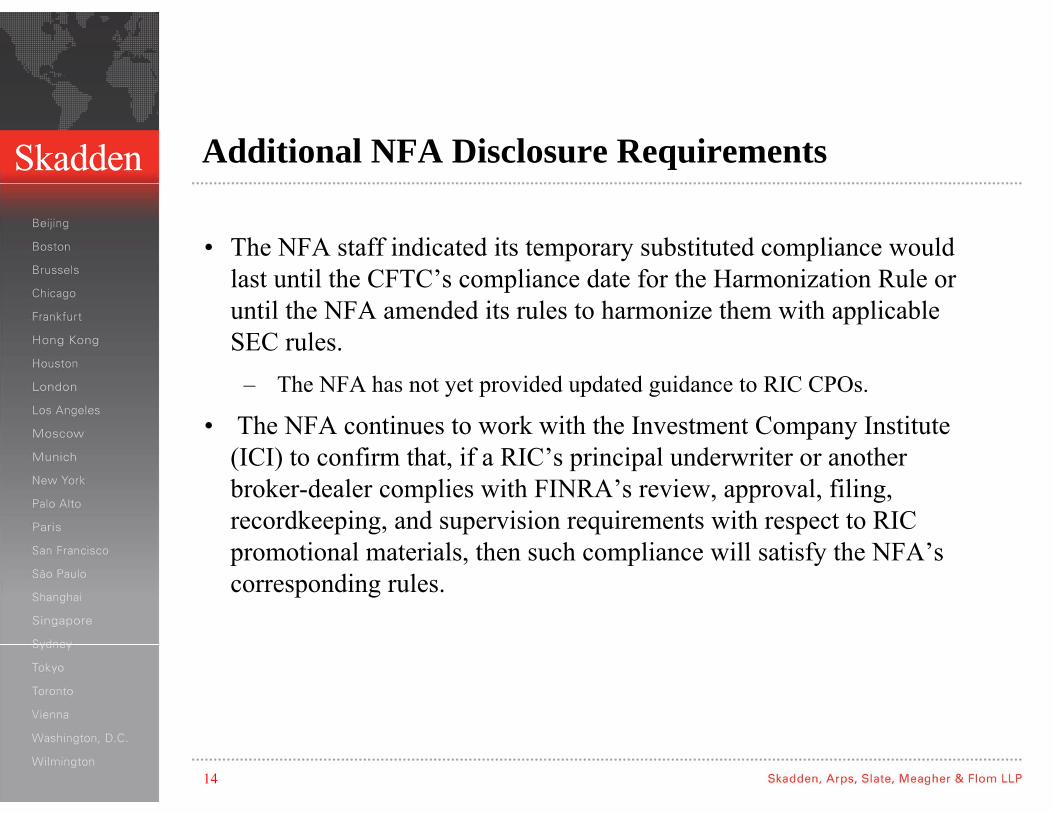

• The NFA staff indicated its temporary substituted compliance would last until the CFTC’s compliance date for the Harmonization Rule or until the NFA amended its rules to harmonize them with applicable SEC rules.

– The NFA has not yet provided updated guidance to RIC CPOs.

• The NFA continues to work with the Investment Company Institute (ICI) to confirm that, if a RIC’s principal underwriter or another broker-dealer complies with FINRA’s review, approval, filing, recordkeeping, and supervision requirements with respect to RIC promotional materials, then such compliance will satisfy the NFA’s corresponding rules.

15

The Reporting Requirements

• Substituted Compliance Reporting:– RICs must furnish their semi-annual and annual reports to investors and file

their periodic reports with the SEC, as required by the securities laws.

– The RIC CPO must cause the RIC’s “current” net asset value per share to be available to investors.

• No guidance on how frequently “current” NAV must be published to be “available to investors” (some closed-end funds, for example, do not publish NAVs daily).

– A RIC CPO must file with the NFA the financial statements the RIC has filed with the SEC.

• This substituted compliance obligation is not codified in the rule text; it appears only in the preamble of the adopting release; raising a question of whether, without further modification of CFTC Rule 4.22, a RIC CPO will be in technical non-compliance with the CFTC’s rules when taking advantage of this element of substituted compliance.

16

Form CPO-PQR Reporting

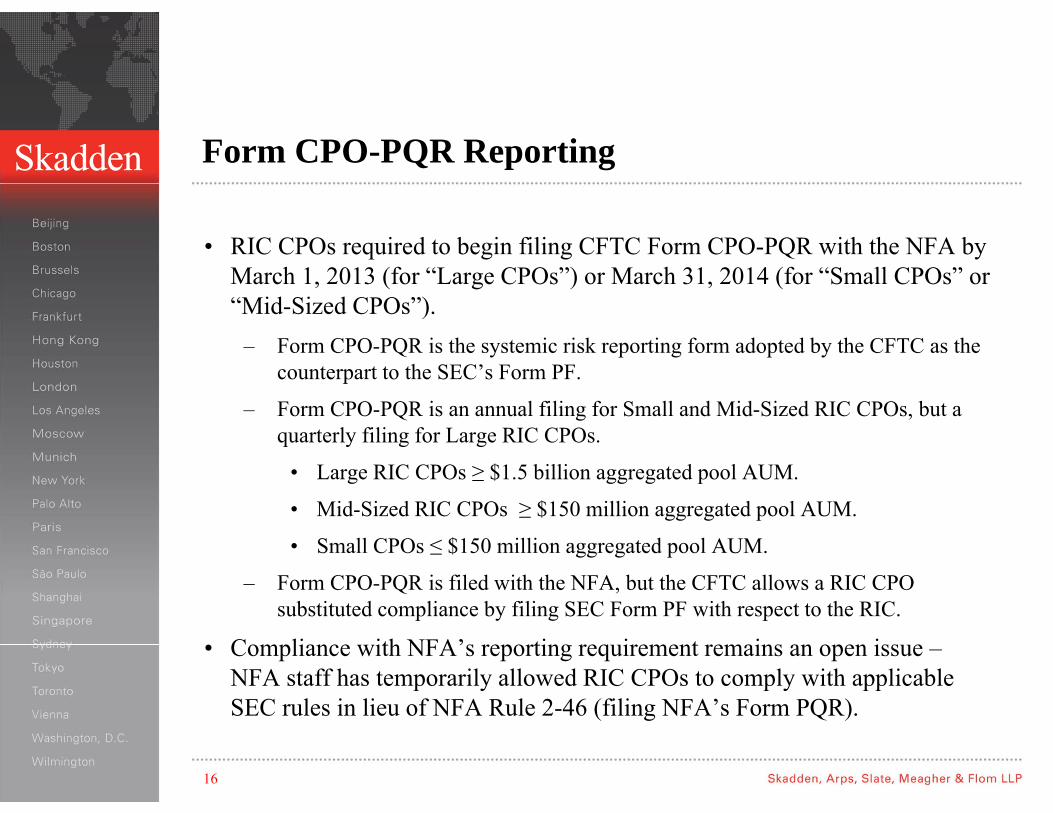

• RIC CPOs required to begin filing CFTC Form CPO-PQR with the NFA by March 1, 2013 (for “Large CPOs”) or March 31, 2014 (for “Small CPOs” or “Mid-Sized CPOs”).

– Form CPO-PQR is the systemic risk reporting form adopted by the CFTC as the counterpart to the SEC’s Form PF.

– Form CPO-PQR is an annual filing for Small and Mid-Sized RIC CPOs, but a quarterly filing for Large RIC CPOs.

• Large RIC CPOs ≥ $1.5 billion aggregated pool AUM.

• Mid-Sized RIC CPOs ≥ $150 million aggregated pool AUM.

• Small CPOs ≤ $150 million aggregated pool AUM.

– Form CPO-PQR is filed with the NFA, but the CFTC allows a RIC CPO substituted compliance by filing SEC Form PF with respect to the RIC.

• Compliance with NFA’s reporting requirement remains an open issue –NFA staff has temporarily allowed RIC CPOs to comply with applicable SEC rules in lieu of NFA Rule 2-46 (filing NFA’s Form PQR).

17

The Recordkeeping Requirements

• General Recordkeeping Relief:– A RIC CPO must file a notice of use of a third-party record-keeper with the

NFA, in which the RIC CPO represents that it will:

• agree to have the RIC’s records that are kept at the RIC CPO’s third-party service provider maintained in accordance with applicable CFTC requirements;

• agree to produce original books and records for inspection at the RIC CPO’s main business office within 48 hours of a request from the CFTC; and

• disclose in the RIC’s prospectus the location of the RIC CPO’s books and records.

– A RIC CPO must file a statement from the service provider agreeing to maintain books and records in accordance with CFTC requirements.

• Compliance with NFA’s recordkeeping requirement remains an open issue – NFA staff have temporarily allowed RIC CPOs to comply with applicable SEC rules in lieu of NFA Rule 2-10 (books and records).

18

Other NFA Obligations

• NFA Bylaw 1101 generally requires a registered CPO to conduct due diligence to determine that all of the investors in its funds, the counterparties with which its funds enter into commodity interest transactions, its sub-advisers and its solicitors are appropriately registered with the CFTC (or appropriately excluded or exempt from registration).

– This requirement applies to current investors, counterparties, sub-advisers and solicitors, as well as to new ones.

• The NFA has determined that a RIC CPO will be considered in compliance with Bylaw 1101 if the CPO's due diligence covers any futures commission merchant through which the RIC executes swaps or futures trades and any sub-adviser that provides investment management services to the RIC.

– Thus, a RIC CPO will not be required to conduct due diligence on the RIC's investors.

– The NFA has indicated that it intends to issue further guidance in this area.

19

Compliance Implications Under Rule 38a-1

• Rule 38a-1 requires RICs to adopt compliance policies and procedures reasonably designed to prevent violations of the federal securities laws, including oversight of compliance by the RIC’s investment advisers.

• Although the Commodity Exchange Act and its rules and regulations are not federal securities laws, a RIC’s intended use of derivatives and related risks are required to be disclosed in its prospectus and statement of additional information, which are subject to the federal securities laws.

• Advisers also are required to have policies and procedures that address portfolio management processes, and a RIC’s board and its CCO are required to oversee compliance by the investment adviser.

• SEC staff has stated that RIC policies and procedures should be designed to prevent material misstatements about its use of derivatives and related risks.

20

Compliance Implications Under Rule 38a-1

• If a RIC cannot satisfy the restrictions in Rule 4.5 or another exemption, its directors, through the RIC’s CCO, should:

– determine whether all applicable RIC CPO notice filings have been made– if a RIC has less than three years of operations, determine whether any

performance history for other pools or accounts managed by the RIC CPO are required to be disclosed in the RIC’s registration statement and consider responsibility for that disclosure

– ensure the RIC’s disclosure document is using the correct legend– ensure records maintained by service providers satisfy CFTC requirements and

the NFA has been notified of the records’ location– ensure the RIC CPO has obtained and filed with the NFA a statement from the

third-party record-keeper agreeing to maintain books and records in accordance with CFTC requirements

– ensure the RIC CPO is filing the RIC’s financial statements with the NFA– ensure the RIC CPO is filing a Form CPO-PQR with the NFA– ensure RIC CPO is complying with any additional NFA requirements (such as

diligence of future commission merchants used by the RIC)– consider any special facts and circumstances applicable to the RIC, such as for

funds of funds

21

Penalties for Violations of the CEA/CFTC’s Rules

• Violations of the Commodity Exchange Act (CEA) or the CFTC’s rules can result a wide variety of administrative, civil and/or criminal penalties for the RIC CPO, its officers and employees:

– Administrative/Civil:

• Civil monetary penalties up to $140,000 per violation;

• Suspension, denial, revocation or restriction of registration and/or exchange trading privileges; and

• Restitution (through the CFTC’s reparations program)

– Criminal:

• Monetary penalties up to $1 million and up to 10 years imprisonment per violation

• In addition, the NFA can bring “Business Conduct Committee” actions or “Membership Responsibility Actions” against a RIC CPO, either of which can result in a similar array of monetary penalties or injunctive remedies.

22

How Is a RIC Fund of Funds (FoF) impacted by the Trading Restrictions?

• A RIC that operates as a FoF can be a commodity pool if its portfolio funds trade commodity interests, even if the FoF itself does not trade commodity interests directly.

• A rescinded CFTC regulation had provided guidance on the application of the de minimis trading exception used by private funds (found in Rule 4.13(a)(3)).

– Rule 4.13(a)(3) has de minimis trading limitations substantially similar to those in the Rule 4.5, except that there is no blanket permission to engage in unlimited bona fide hedging transactions.

– In an August 2012 FAQ, the CFTC staff indicated that FoFs (including RICs) may continue to rely on rescinded Appendix A to establish compliance with the trading limitations in Rule 4.5 until revised guidance is provided.

– In November 2012, the CFTC staff indicated that it will not recommend that the CFTC take enforcement action against operators of FoFs for failure to register as a CPO until six months from the date the staff issues revised guidance on the application of the calculation of the de minimis thresholds in Rule 4.5.

• Managers must comply with certain requirements outlined in staff’s no-action letter to exploit the stay of enforcement.

23

How Is a RIC FoF Impacted by the Trading Restrictions?

• In February 2013, the ICI together with other interest groups submitted a letter to the CFTC regarding the impending guidance regarding the difficulties involved in applying the de minimis thresholds to managers of FoFs.

– The letter noted that the issue is compounded by the fact that interests in certain securitization vehicles, real estate investment trusts (REITs) and business development companies (BDCs) are now treated as interests in commodity pools.

• Even though the CFTC has provided relief for some of these investment vehicles, as discussed below, the CFTC has only extended such registration relief to operators of funds that invest in certain securitization vehicles.

– The comment letter recommends, among other things, that:• the CFTC staff craft the guidance to permit specified levels of investment for

FoFs without looking through to underlying funds managed by registered CPOs and CTAs, and to REITs, BDCs and securitization vehicles;

• include a reasonable belief standard for FoF managers; • provide a transition period for any FoF managers that determine they can no

longer comply with Rule 4.5; and • clarify the treatment of direct trading by FoF managers.

– To date, no further FoF guidance has been issued.

24

Review of Rule 4.5 – When Do RIC Advisers Need to Register as CPOs?

• There are two de minimis thresholds for non-bona fide hedging positions:

– Aggregate initial margin and premiums for futures and swaps cannot exceed 5% of the RIC’s liquidation value; or

– Aggregate net notional value of the RIC’s position in futures and swaps must not exceed 100% of the RIC’s liquidation value.

• Bona fide hedging positions are those used “for bona fide hedging purposes” within the “meaning and intent” of Rules 1.3(z)(1) or 151.5 under the CEA.

– There is no limit on bona fide hedging positions.

– The bona fide hedging definitions in Rules 1.3(z)(1) and 151.5 have been vacated by a federal District Court, but “re-applied” through CFTC Staff No-Action Letter 12-19.

25

Rule 4.5 – What Qualifies as Bona Fide Hedging?

• Rule 1.3(z)(1) defines bona fide hedging for financial commodities.– The actual text of the rule is extremely restrictive.

– However, a 1987 CFTC interpretation stated that financial commodities used for balance sheet hedging, duration management, portfolio insurance, “dynamic asset allocation strategies that provide protection equivalent to a put option for an existing portfolio of securities,” and other risk reducing trading strategies consistent with the interpretation are bona fide hedging.

– It appears that interest rate and currency hedging relating to a specific risk should be considered bona fide hedging, though CFTC staff has made public statements about possibly interpreting bona fide hedging even more restrictively.

• Rule 151.5 defines bona fide hedging for agricultural commodities, metals and energy commodities.

– Limited to five enumerated types of transactions that represent substitutes for physical market transactions.

– Unclear whether positions used by a RIC could ever constitute bona fide hedging under this rule.

26

Use of Swaps Under Rule 4.5

• In calculating the 100% aggregate net notional threshold, a RIC adviser may net:

– futures contracts with the same underlying commodity across designated contract markets and foreign boards of trade; and

– swaps cleared on the same derivatives clearing organization.

• In January 2013, the ICI, together with other interest groups, requested that the CFTC staff grant relief permitting operators of RICs and private funds to net certain uncleared swaps held by a fund when applying the net notional test in Rule 4.5.

– Without the requested relief, the letter states both the long exposure and the short exposure on offsetting swaps would have to be counted for purposes of the net notional test overstating a fund’s actual exposure to the underlying commodity interests.

– The CFTC has not yet responded to this request letter.

27

Rule 4.5 – What Is The Marketing Restriction?

• A RIC may not be marketed to the public as a commodity pool or “a vehicle for trading in the commodity futures, commodity options, or swaps markets.”

• The CFTC provided a non-exhaustive list of factors:– The name of the RIC (i.e., whether the name suggests the RIC is a vehicle for

trading futures or swaps)– Whether the RIC’s primary investment objective is tied to a commodity index– Whether the RIC makes use of a controlled foreign corporation (CFC) for its

derivatives trading– Whether the RIC’s marketing materials — including its prospectus — refer to

the benefits of using derivatives in a portfolio or make comparisons to a derivatives index

– Whether, during the course of its normal trading activities, the RIC or an entity on its behalf has a net short speculative exposure to any commodity through a direct or indirect investment in other derivatives

– Whether transactions in futures or swaps engaged in by the RIC or on behalf of the RIC will directly or indirectly be its primary source of potential gains (losses)

– Whether the RIC is explicitly offering a managed futures strategy

28

If a RIC Cannot Satisfy Rule 4.5, Then What?

• The RIC’s adviser must register as the RIC’s CPO, but may elect to claim a partial exemption without relying on the Harmonization Rule:

– CPOs of some privately offered RICs may qualify for a partial exemption from registration under CFTC Rule 4.7.

• This exemption requires a notice filing with NFA.

• Rule 4.7 exempts a CPO from almost all disclosure requirements, but continues to require a CPO to send CFTC-compliant quarterly account statements and annual reports to investors directly and to file CFTC-compliant annual reports to the NFA.

– CPOs of RICs that are ETFs (ETF CPOs) may qualify for an existing exemption under CFTC Rule 4.12 (ETF Rule).

• This exemption requires a notice filing with NFA.

• The ETF Rule provides disclosure, reporting and recordkeeping accommodation for ETF CPOs, but still requires a CFTC disclosure document to be reviewed and accepted by NFA prior to its first use and CFTC-compliant monthly account statements and annual reports.

29

Does a RIC’s CPO Also Need To Register as a Commodity Trading Advisor?

• If a RIC’s adviser is registered as the RIC’s CPO, then it would be exempt from registering as a commodity trading advisor (CTA).

• If a RIC has another adviser or a sub-adviser, neither the CEA nor the CFTC’s rules address whether CTA registration requirements should attach.

– Presumably, the other adviser or sub-adviser would need CTA registration or an exemption if it is providing commodity interest trading advice to a RIC.

– Advisers and sub-advisers to RICs that have claimed the Rule 4.5 exclusion may already be relying on the CTA registration exemption requirement in Rule 4.14(a)(8)(i)(A).

• If the RIC cannot rely on Rule 4.5, other exemptions may be available (as discussed above).

30

Michael [email protected]

Daniel S. Konar [email protected]

Thomas A. [email protected]

These materials are provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and are not intended and should not be construed as legal advice.