cement sector coverage - 18 february 2016

TRANSCRIPT

PRIME INVESTMENT RESEARCH AUTOMOTIVE |EGYPT

GB AUTO – INITIATION OF COVERAGE JANUARY, 14TH

2016

PRIME INVESTMENT RESEARCH

BUILDING MATERIALS |EGYPT CEMENT SECTOR COVERAGE – ARCC, SUCE & SVCE

FEBRUARY, 18TH 2016

HUGE POTENTIAL COUPLED WITH

UNCERTAINTY.

LOW DEMAND A KEY CHALLENGE AFTER

SOLVING ENERGY DILEMMA.

NEW LICENSES CONSIDERED A DOUBLE EDGE

DEPENDING ON FUTURE DEMAND.

ACC A PIONEER FAILING TO REAP BENEFITS

OF EARLY COAL CONVERSION.

SUEZ GROUP FINANCIAL POSITION

NEGATIVELY AFFECTED BY SUBSIDIARIES.

SOUTH VALLEY TO ELIMINATE RISK IN CASE

OF ACQUIRING NEW LICENSE.

2

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Bearish outlook despite huge potential The Egyptian cement industry has always held huge potential for

high returns with the Egyptian cement market being one of the main markets worldwide. Despite the

huge potential we are bearish over the sector. The witnessed decline in the EGX since 2015 has pushed

most stock prices towards all time lows and cement stocks weren’t different. We believe that the upside

for all our covered companies is attributed to the declining market price rather than companies’

performance. Fundamentally, however, companies are facing huge uncertainty despite great potential.

Expected demand depends on several market factors The Egyptian cement market has been hit by

oversupply during 2015 forcing selling prices towards a 15% drop. We estimate the market to reach

equilibrium by 2017 where the demand is set to equal the current total capacity. However, our demand

assumptions are based on the announced projects being completed within their announced time frame.

Several projects have already faced some delays, while the other projects related to the tourism sector

have been suspended following the latest events. Moreover, the economic uncertainty has scared away

foreign investors limiting their contribution to these projects.

Could new licenses turn into a threat? The new licenses which were offered by the IDA are seen by many

as an opportunity to capitalize on increasing demand. However, even with projects operating within time

frame we expect demand to reach 82mtpa by 2020. Granting all 14 licenses would add a significant

28mtpa which pushes capacity towards 96mtpa causing a supply-demand gap. It is noteworthy that, some

of the market players have the ability to exceed 100% utilization, which already took place before 2011. A

further oversupply without revisiting the idea of exporting creates a huge threat for the Egyptian cement

Industry.

FX a huge risk The EGP witnessed a significant devaluation during 2015 which caused a drag on the whole

economy. The coal integration has caused companies to need foreign currency for the coal imports. Any

shortage or further devaluation is considered a threat for companies’ operations. Furthermore,

companies in need of clinker imports might be forced to dismiss the idea and lose significant market share

as importing clinker might surpass the already declining selling prices which would be cost inefficient.

Despite the great potential there remains an uncertainty whether the oversupply situation could be

solved. The market potential depends greatly on the above mentioned factors which is a huge risk due to

the uncertainty of the economic outlook. Hence we opted to adopt a HOLD recommendation for the

companies covered in the report based on their fundamentals despite their “fake” upside. However, we

decided to put the whole sector on the watch list, waiting for any enhancement in performance to be

reported in 1Q 2016, in order to revise our assumptions and accordingly our recommendations.

Company Ticker Market Price Target Price

Arabian Cement ARCC 7.3 11.9

Suez Cement SUCE 16.8 29.6

South Valley Cement SVCE 3.5 5.5

3

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

URBAN POPULATION %

SOURCE: WORLD BANK

GLOBAL CEMENT CONSUMPTION

SOURCE: BLOOMBERG & PRIME CALCULATIONS

Global Industry Overview

Cement industry was one of the largest

growing industries in the past decades. The

rapidly growing demand for housing and

infrastructure in addition to the growing

urbanization levels in emerging economies

provided the main incentive for this growth.

Since there is no other material discovered till

now can replace cement in its role, cement is

the major building material in meeting this

huge demand. Hence, the low urbanization

levels, like that in Asia & Africa, compared to

that of developed nations, promises more

demand growth for cement in the coming years.

However, the slowing growth rates in China’s economy that hit the country in the last two years led

to a global slowdown in the whole world’s economic growth. As China was the largest importer of

many commodities from emerging markets, the lower growth rates in the Chinese economy

negatively affected most of these emerging economies which resulted in a slowdown in housing and

construction sector, hence, a lower demand for cement.

Derived by China’s demand, Asia led the global consumption for cement in the last decade, as it

represented more than 70% of the world’s consumption. Europe comes second as the second largest

consumer of cement. The Americas come in the third place derived by the increasing consumption

levels of cement in emerging countries in South America like Brazil. Africa comes fourth in the global

consumption. By 2015, world’s cement consumption reached 4276.1mn ton, growing by a CAGR of

25.24% over 2010-2015.

0

10

20

30

40

50

60

70

80

90

100

1994

2004

2014

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2010 2011 2012 2013 2014 2015

Mn

To

n

America

EU

ME

Africa

Asia

World

3585.2 3745.7

4033.5 4139.5 4276.1

3311.7

4

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

GLOBAL CEMENT PRODUCTION

SOURCE: BLOOMBERG & PRIME CALCULATIONS

SOURCE: BLOOMBERG & PRIME CALCULATIONS

MKT SHARE BY REVENUE

SOURCE: BLOOMBERG & PRIME CALCULATIONS

The unprecedented growth in China’s

cement demand urged the country to

increase its production to meet this

demand. In the past 8 years cement

production in China increased by more

than 80%, it recorded 2,344.4mn ton in

2015 as the largest cement producer in

the world. India is in the second place with

274.5mn ton followed by USA, Iran and

Indonesia, respectively

Asia dominates global cement market

share; derived by huge Chinese

production and consumption, Asia

controls 54.1% of the world’s cement

production. Asia is followed by North

America, Europe, Middle East & Africa

and South America, respectively.

0

500

1000

1500

2000

2500

3000

3500

4000 M

n T

on

Indonesia Japan Vietnam Russia Brazil Iran Egypt Saudi Arabia US Turkey India China

Europe, 14.4

Asia, 54.1

North America,

16.8

South America,

6.8

Middle East & Africa,

7.7

Cement Production (Mn ton) 2008 2009 2010 2011 2012 2013 2014 2015

China 1300.2 1561.4 1748.7 1942.1 2193.4 2404.2 2465.6 2344.4

India 182.7 201.8 213.2 225 243.5 254.8 270.4 274.5

Turkey 51.4 54 62.7 62.2 63.9 70 70.4 58.6

US 78.6 57 60.4 61.9 67.8 69.9 75 69.6

Saudi Arabia 31.8 40 42.3 48.4 50 57 55 55

Egypt 39.93 47.4 48.32 48.72 49.71 45.15 47.79 38.97

Iran 44.4 50 50 61 70 72 65 65

Brazil 57.9 57.7 59.1 64.1 68.8 70 72 72

Russia 53.6 44.3 50.4 55.6 61.5 66.4 68.4 69

Vietnam 37 47.9 50 59 60 58 60.5 61

Japan 31.85 51.53 51.29 54.74 57.96 57.91 49.9

Indonesia 37 40 22 30 32 56 65 65

5

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

An Overview on Egyptian economy and growth expectations

The Egyptian economy has been unstable facing several challenges since the 2011 revolution despite

government’s efforts to ensure stable growth. FY 2014/2015 witnessed slightly enhanced performance

with GDP growth reaching 4.2% jumping from 2.2% recorded a year earlier. However, the economy is still

facing several challenges such as:

Foreign currency shortage as the net foreign reserves amounting to USD16.4 billion, barely covering

3 months of imports.

Widening trade deficit at USD38.8bn recorded in FY-2014/2015

Shortage in energy supply, which directly affects the cement sector as well as other industries such

as steel, fertilizers and ceramics.

Foreign exchange risk. Highlighted by a widening spread between the official and the parallel

market to reach 9%.

Decreasing Gulf countries’ support. Official transfers from Gulf countries in the form of cash and in-

kind grants declined by 77% in FY15. Furthermore, the pressure caused by the declining oil prices

and the Saudi Arabia/Iran conflict adds further possibility to more decline to be expected.

Slowdown due to declining oil prices in 2015.

Facing those challenges there are still key positives that lead us to forecast an economy growth in the following year. The parliament had its first sessions in January 2016. This would help to enforce economic reforms and add political stability to ensure foreign investors. Moreover, the new gas discoveries as well as the arrival of second gasification ship at Ain Sokhna Port will help solving energy shortage constrains and boost the economy. Triggered by political stability and the serious steps taken by the government to pay back investors’ pending backlogs especially in the oil sector, we see growth rate for FY15/16 to be 3.9%, taken into consideration facts such as delayed reforms (tax, investment laws) and production halts caused by lack of energy especially with energy intensive industries. As a result, we expect GDP to pick up soon by FY-2016/2017 on the back of the new Eni’s gas discovery reaching 30 trillion cubic feet gas reserves. This will help to solve energy crisis and may be government allocate a portion of its output for export to gain foreign currency. However, the global prices will be a major obstacle if the current tren continues. A further trigger for demand are the projects which were offered at the EEDC (Egypt Economic Development Conference) that was held last March, as the government succeeded in sealing deals worth over USD 33bn. This is in addition to the MoUs that were signed which were valued at USD 111.4bn. Most of the major sectors including the Real Estate and Building Materials will benefit from such projects driving demand. In addition, issuing the new investment law will increase domestic and foreign investors ‘confidence and hence induce FDI.

6

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

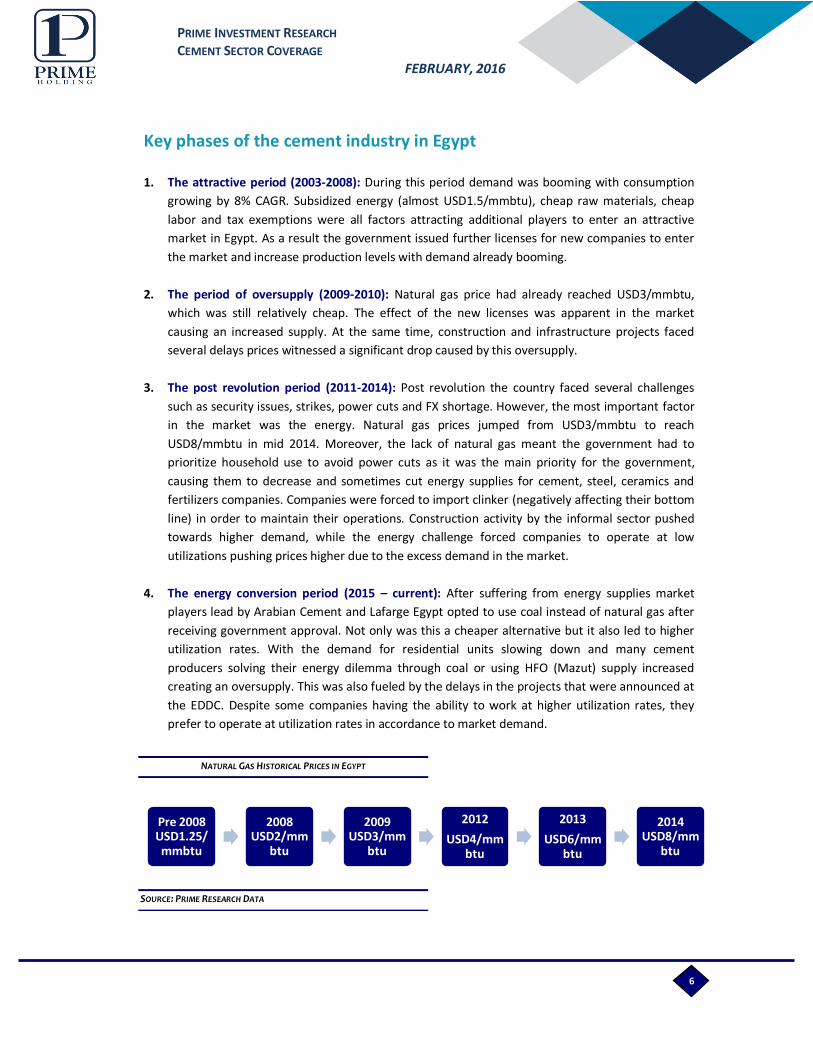

NATURAL GAS HISTORICAL PRICES IN EGYPT

SOURCE: PRIME RESEARCH DATA

Key phases of the cement industry in Egypt

1. The attractive period (2003-2008): During this period demand was booming with consumption

growing by 8% CAGR. Subsidized energy (almost USD1.5/mmbtu), cheap raw materials, cheap

labor and tax exemptions were all factors attracting additional players to enter an attractive

market in Egypt. As a result the government issued further licenses for new companies to enter

the market and increase production levels with demand already booming.

2. The period of oversupply (2009-2010): Natural gas price had already reached USD3/mmbtu,

which was still relatively cheap. The effect of the new licenses was apparent in the market

causing an increased supply. At the same time, construction and infrastructure projects faced

several delays prices witnessed a significant drop caused by this oversupply.

3. The post revolution period (2011-2014): Post revolution the country faced several challenges

such as security issues, strikes, power cuts and FX shortage. However, the most important factor

in the market was the energy. Natural gas prices jumped from USD3/mmbtu to reach

USD8/mmbtu in mid 2014. Moreover, the lack of natural gas meant the government had to

prioritize household use to avoid power cuts as it was the main priority for the government,

causing them to decrease and sometimes cut energy supplies for cement, steel, ceramics and

fertilizers companies. Companies were forced to import clinker (negatively affecting their bottom

line) in order to maintain their operations. Construction activity by the informal sector pushed

towards higher demand, while the energy challenge forced companies to operate at low

utilizations pushing prices higher due to the excess demand in the market.

4. The energy conversion period (2015 – current): After suffering from energy supplies market

players lead by Arabian Cement and Lafarge Egypt opted to use coal instead of natural gas after

receiving government approval. Not only was this a cheaper alternative but it also led to higher

utilization rates. With the demand for residential units slowing down and many cement

producers solving their energy dilemma through coal or using HFO (Mazut) supply increased

creating an oversupply. This was also fueled by the delays in the projects that were announced at

the EDDC. Despite some companies having the ability to work at higher utilization rates, they

prefer to operate at utilization rates in accordance to market demand.

Pre 2008 USD1.25/mmbtu

2008 USD2/mm

btu

2009 USD3/mm

btu

2012

USD4/mmbtu

2013

USD6/mmbtu

2014 USD8/mm

btu

7

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

OUR CEMENT DEMAND ESTIMATES

SOURCE: PRIME RESEARCH

The Cement consumption in Egypt

Cement consumption in Egypt is spread out into three sectors; residential, infrastructure and non-

residential sectors with 85%, 5% and 10% of cement consumption respectively. Therefore, we initially

forecasted the building & construction sector based on its substantially well-built historical relationship

with GDP as a stable and consistent percentage of the GDP. Cement as a value is forecasted through as a

percentage of construction part of the Real GDP. Through our inflation adjusted price forecasts we

acquired a value for market consumption between 2015 and 2020. We believe that cement consumption

would reach 82mtpa by 2020 growing at a CAGR of 8.1%. This growth is justified by the construction

activity anticipated through the megaprojects planned by the government between 2015-2020. We

expect cement demand to witness two periods:

Reaching equilibrium (2015-2017): During 2015 the market has been suffering from oversupply

in the market which caused increased prices. The conversion to coal by several market players

enabled them to operate at higher utilization rates compared to 2014. An example would be

Arabian Cement, which has already converted to cheaper and more available coal as an energy

source. Meanwhile, other companies who have not converted to coal yet, have used HFO

witnessing a more steady supply in comparison to natural gas. Moreover, the economic

slowdown witnessed in 2015 also contributed to a lower than expected cement consumption

leading to a total sales volume of 53mn tons from a total capacity of 70mn tons. In 2016 we

expect total cement sales to witness a significant 11% increase. This increase continues until

2017 where cement demand is expected to be equal to the total capacity of Egyptian market

players. This would enable most market players to operate at full utilization.

Demand Growth (2018-2020): Starting 2018 almost all cement makers would have converted to

coal enabling 100% utilization. However, with most projects (even the ones facing delays) being

in operations during this period in addition to the GDP growth. However, starting 2018 the

construction as a percentage of GDP would face a slight decline. This is caused by a boom in

other sectors as more major problems such as energy and political instability are expected to be

solved. This has been a trend even historically with the construction percentage averaging

between (2.8%-3.6%) between 2005 and 2008 which is the economic peak for Egypt. Meanwhile

construction has represented an average of 4.2% since 2009, a period affected by the economic

slowdown and the revolution in Egypt. The cement consumption would still increase to reach an

expected sales volume of 82mn tons in 2020. The extra 13.5mn tons are either to be acquired

through imports (at a higher cost) or more likely through licenses which were announced

recently by the government.

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

GDP (Real), EGP bn 1,528 1,558 1,592 1,626 1,678 1,746 1,818 1,902 1,995 2,095 2,146

Construction & Building (Real) 64 66 69 71 74 77 80 83 83 83 81

% of GDP 4.2% 4.2% 4.4% 4.4% 4.4% 4.4% 4.4% 4.4% 4.2% 4.0% 3.8%

Cement Demand, mn tons 49 49 51 50 51 53 60 69 74 78 82

Inflation adjusted Cement Prices 387 440 465 453 456 546 675 543 499 459 425

Cement Value mn 14,850 21,029 23,012 22,057 23,337 27,352 34,617 28,784 30,071 31,456 31,486

Cement % of Construction Value 29.0% 36.0% 36.1% 33.4% 33.7% 38.4% 47.1% 37.6% 37.7% 37.7% 37.7%

8

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

REAL GDP (EGP, BN ) & GROWTH CEMENT DEMAND (TONS,MN) & GROWTH

SOURCE: PRIME RESEARCH

CONSTRUCTION% OF GDP IN BOOM AND

SLOWDOWN PERIODS

0%

1%

2%

3%

4%

5%

6%

-

500

1,000

1,500

2,000

2,500

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020 -4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

10

20

30

40

50

60

70

80

90

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Oversupply explained

Lower than expected demand poses a great risk for the industry as it directly affects prices which in

turn have suffered during 2015. The delays for the start date for certain projects in addition to the hit

that was taken by the tourism industry has led to a slowing demand which forced the companies to

operate at lower average utilization rate of 78% during 2015. Furthermore, our main export

destinations (Libya and Sudan) have been suffering from political and market instability denying

Egyptian producers the opportunity to export their excess supply. It is unlikely that cement players

would lower their supply. For example, during 2015 many companies maintained their supply level

despite suffering from losses. (Torah, Helwan, Sinai and Alex Cement). However, we believe this

situation of oversupply would be resolved by 2017 where market consumption is expected to finally

equal total capacity. On the other hand, most cement companies would have converted to coal by then

allowing the companies to reach equilibrium with demand equaling supply. Post 2017 we expect

demand to surpass the total market capacity which offers the perfect chance for the added capacity

acquired through the new licenses.

How much added capacity would is needed?

Projects: The increased demand estimation by 2020 to reach 82mtpa is based on the expected

infrastructure investments pledged and agreed upon in the form of MoUs during the EEDC. This is in

addition to the projects that are going to be implemented in the developmental area around the New

Suez Canal. We anticipate a hike in construction demand over the upcoming period reflected in a total

of USD 173.4bn according MEED worth of projects to be implemented over 2015-2025. These projects

will cause a significant increase in demand. The Residential and Non-residential projects alone stand at

a net value

9

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

UPCOMING PROJECTS AND REQUIRED CEMENT

SOURCE: MEED PROJECTS

of USD117.2bn, while power related projects stand USD 24.7bn with transportation projects standing at

USD 31.9bn. While residential projects require 20% of cement other two segments require 10%. As a

result, we do believe that despite some delays these projects still supports the idea of increased demand.

2012 2013 2014 2015 2016 2017 2018 2019 2020

Average Mkt Price 456 546 675 575 575 587 604 622 635

Growth

20% 24% -15% 0% 2% 3% 3% 2%

Value in USD, bn Required Cement %

Residential & Non-Residential 117.2 20%

Transportation Projects 31.9 10%

Power & Water Projects 24.4 10%

Total 173.4

The new licenses: The government announced the issuance of new 14 cement licenses at an estimated

capacity of 2mtpa with details to be announced later. Several market players haven’t shown their willingness

to apply for the new licenses due to its high cost, having to ensure their own electricity and the already

existing oversupply in the market. However, after adding such capacities for other market players like South

Valley Cement who are willing to add the total. Our demand forecast of 82mn tons by 2020 means that the

government only needs to add licenses worth 13.5mtpa to cater for the growing demand. Any further

addition would pose a threat of further oversupply. It is noteworthy, that the IDA has announced that all new

licenses are obliged to use energy sources other than natural gas (coal, RDF, HFO). This capacity expansion is

needed for the high investments and projects previously mentioned. The investment cost per line was valued

at EGP 150mn.

Prices expected to grow conservatively after significant drop in 2015

During 2015 average price dropped significantly as a result of a) oversupply and b) slowdown in global cement

prices. The oversupply has pushed prices to 15% decline. The slower than expected project executions coupled

with the blow to the tourism industry mean that demand would grow at a slower rate than expected pushing

the market to remain at a state of oversupply until it reaches equilibrium in 2017. We believe that prices

would remain stable during 2016 at EGP 575/ton, grow in accordance with population growth rates at 2% for

the following year. For 2017-2018 prices are expected to grow at 3% each year. This would be coupled with

reaching market equilibrium in 2017. Growth is expected to slow down slightly growing at 2% to finally reach

EGP 635/ton. Average market prices are expected to grow at a 5-year CAGR of 2%. We do not expect any

extraordinary price hike as the demand will be met by the increased utilization rates. In addition, the new

licenses dismissing the idea of supply shortage in the long term. It is noteworthy that many companies sell at

premium or a discount to the average market price depending on location, distribution and other factors.

Moreover, these price forecasts would be subject to change in case of delays of the projects and the amount

of new licenses that are taken by the companies.

10

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

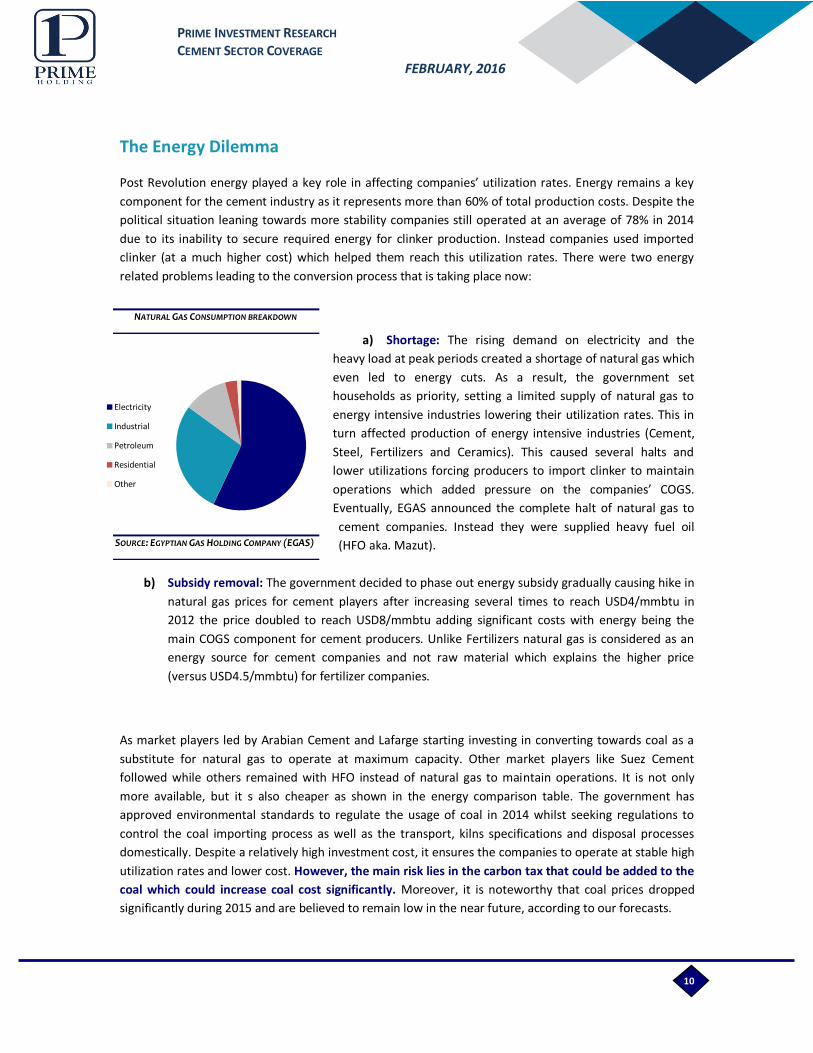

NATURAL GAS CONSUMPTION BREAKDOWN

SOURCE: EGYPTIAN GAS HOLDING COMPANY (EGAS)

The Energy Dilemma

Post Revolution energy played a key role in affecting companies’ utilization rates. Energy remains a key

component for the cement industry as it represents more than 60% of total production costs. Despite the

political situation leaning towards more stability companies still operated at an average of 78% in 2014

due to its inability to secure required energy for clinker production. Instead companies used imported

clinker (at a much higher cost) which helped them reach this utilization rates. There were two energy

related problems leading to the conversion process that is taking place now:

a) Shortage: The rising demand on electricity and the

heavy load at peak periods created a shortage of natural gas which

even led to energy cuts. As a result, the government set

households as priority, setting a limited supply of natural gas to

energy intensive industries lowering their utilization rates. This in

turn affected production of energy intensive industries (Cement,

Steel, Fertilizers and Ceramics). This caused several halts and

lower utilizations forcing producers to import clinker to maintain

operations which added pressure on the companies’ COGS.

Eventually, EGAS announced the complete halt of natural gas to

cement companies. Instead they were supplied heavy fuel oil

(HFO aka. Mazut).

b) Subsidy removal: The government decided to phase out energy subsidy gradually causing hike in

natural gas prices for cement players after increasing several times to reach USD4/mmbtu in

2012 the price doubled to reach USD8/mmbtu adding significant costs with energy being the

main COGS component for cement producers. Unlike Fertilizers natural gas is considered as an

energy source for cement companies and not raw material which explains the higher price

(versus USD4.5/mmbtu) for fertilizer companies.

As market players led by Arabian Cement and Lafarge starting investing in converting towards coal as a

substitute for natural gas to operate at maximum capacity. Other market players like Suez Cement

followed while others remained with HFO instead of natural gas to maintain operations. It is not only

more available, but it s also cheaper as shown in the energy comparison table. The government has

approved environmental standards to regulate the usage of coal in 2014 whilst seeking regulations to

control the coal importing process as well as the transport, kilns specifications and disposal processes

domestically. Despite a relatively high investment cost, it ensures the companies to operate at stable high

utilization rates and lower cost. However, the main risk lies in the carbon tax that could be added to the

coal which could increase coal cost significantly. Moreover, it is noteworthy that coal prices dropped

significantly during 2015 and are believed to remain low in the near future, according to our forecasts.

Electricity

Industrial

Petroleum

Residential

Other

11

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

COAL PRICE (USD/TON) AND FORECASTS BRENT PRICE (USD/B) AND FORECASTS

SOURCE: BLOOMBERG & PRIME RESEARCH ESTIMATES

So why the sudden drop in coal prices?

The oil price decrease had a direct effect on coal prices to decrease as well. Further, the lower/higher coal

prices will have a positive/negative direct effect in Egyptian cement industry in general, and for

companies using coal in particular. Oil and coal are theoretically considered substitutes, however, by

looking at historical consumption and price movement the trends tell a different story. As indicated by the

below trend line, there is a positive correlation between oil and coal. We expect coal prices to be in

correlation with oil prices and to reach USD62/ton by 2019. This in turn would lower production costs

compared to previous higher prices adding to its already cheaper price compared to natural gas or mazut.

This shows clearly as Arabian Cement enjoys one of the lowest COGS/ton of the market.

96 95 96

88

47 48 45 50 52

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

20

40

60

80

100

120

117

93

80 73

57 58 56 60 62

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

20

40

60

80

100

120

140

12

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

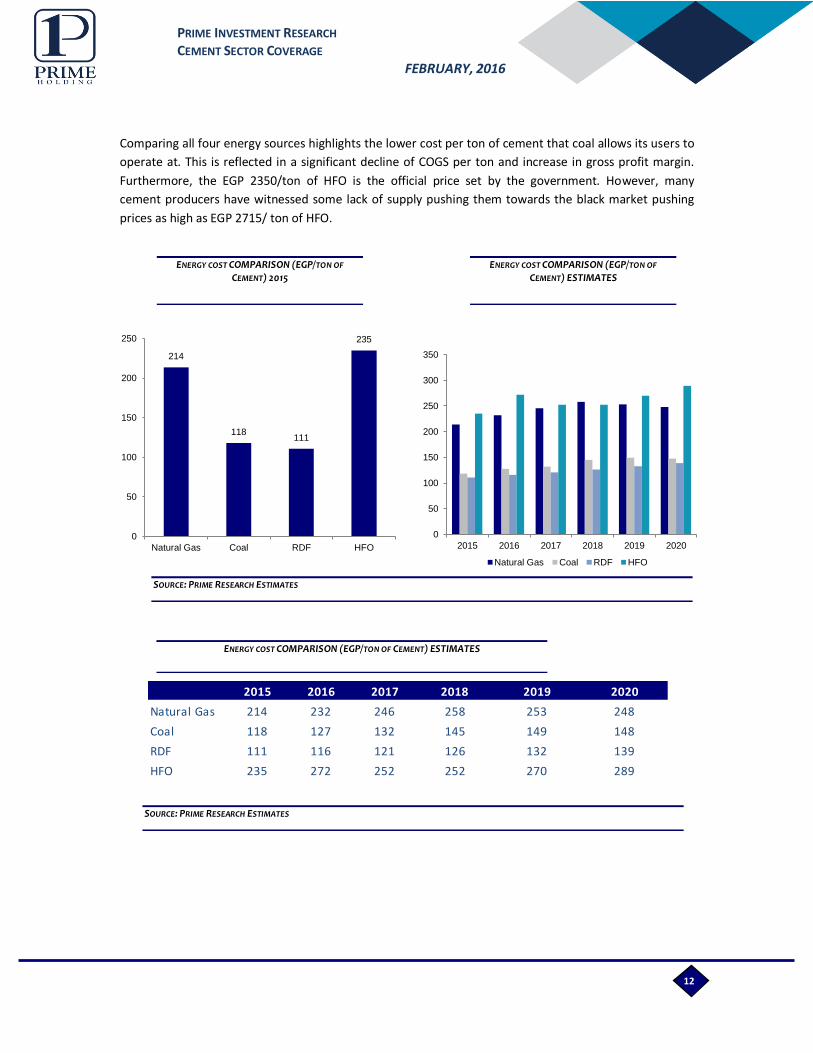

ENERGY COST COMPARISON (EGP/TON OF

CEMENT) 2015

ENERGY COST COMPARISON (EGP/TON OF

CEMENT) ESTIMATES

ENERGY COST COMPARISON (EGP/TON OF CEMENT) ESTIMATES

SOURCE: PRIME RESEARCH ESTIMATES

SOURCE: PRIME RESEARCH ESTIMATES

Comparing all four energy sources highlights the lower cost per ton of cement that coal allows its users to

operate at. This is reflected in a significant decline of COGS per ton and increase in gross profit margin.

Furthermore, the EGP 2350/ton of HFO is the official price set by the government. However, many

cement producers have witnessed some lack of supply pushing them towards the black market pushing

prices as high as EGP 2715/ ton of HFO.

2015 2016 2017 2018 2019 2020

Natural Gas 214 232 246 258 253 248

Coal 118 127 132 145 149 148

RDF 111 116 121 126 132 139

HFO 235 272 252 252 270 289

214

118 111

235

0

50

100

150

200

250

Natural Gas Coal RDF HFO

0

50

100

150

200

250

300

350

2015 2016 2017 2018 2019 2020

Natural Gas Coal RDF HFO

13

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

EGYPTIAN CEMENT MARKET DATA AS OF 2015

SOURCE: COMPANY FINANCIALS, IDA DATA

Company Name Capacity Production Utilization Sales Marketshare Sales YoY

Total suez cement group domistic 12.0 8.0 67% 7.9 15% 0.3%

National Cement Co. 3.5 1.8 50% 1.9 4% 16.9%

Assiut Cement Co. 6.0 4.6 77% 4.7 9% -9.5%

Amreyah Cement 3.5 3.4 97% 3.4 6% -9.1%

Alex &Bani Swaif Cement Co. 4.5 3.9 86% 3.9 7% 28.7%

Lafarge Cement Co. 10.0 7.5 75% 7.4 14% 16.4%

Sina Cement Co. 3.0 2.1 70% 2.0 4% -6.1%

Qena Cement Co. 1.9 1.8 95% 1.7 3% -12.7%

Masr Bani Swaif Cement Co. 3.0 2.8 93% 2.7 5% 12.7%

Arabian Cement Co. 5.0 4.2 84% 4.2 8% 2.4%

South Vally Cement 1.5 1.5 99% 1.5 3% 34.6%

Shoura Cement 0.6 0.3 50% 0.3 1% 0.0%

Medecom Aswan 0.8 0.7 100% 0.7 1% -6.2%

Sinai whitecement 1.5 0.1 6% 0.1 0% 120.3%

Elsewedy Cement Co. 1.5 2.4 162% 2.4 5% 10.0%

Wadi El Nile Cement Co. 2.0 1.7 83% 1.7 3% 18.1%

El-Areish Cement Co. 3.0 1.6 54% 1.6 3% -32.5%

El Nahda Industries Co. 1.5 1.3 87% 1.3 2% -13.6%

Building Materials Ind. Co. 1.8 1.6 91% 1.6 3% 9.6%

ASEC Minya Cement Co. 1.9 1.9 98% 1.9 4% 0.0%

Total 68.5 53.2 78% 53.0 100% 3.4%

14

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

FINANCIAL & MULTIPLE COMPARISON

SOURCE: COMPANY FINANCIALS, PRIME RESEARCH ESTIMATES

Company 2013 2014 2015 2016 2017 2018 2019 2020

COGS/Ton

ARCC 309 401 354 354 363 370 381 389

SUCE 486 565 495 389 375 381 415 356

SVCE 296 340 439 417 470 487 513 537

Sales/Ton

ARCC 528 635 543 541 557 586 610 628

SUCE 517 593 548 498 503 545 580 513

SVCE 516 601 585 585 592 610 628 641

P/E

ARCC 6.55 7.33 8.35 7.14 6.00 4.68 4.22 4.01

SUCE 6 6 -51 25 11 5 5 4

SVCE 12.75 11.26 19.93 8.35 6.84 5.99 7.82 7.70

Ev/EBITDA

ARCC 5.1 4.5 4.9 4.3 3.5 2.6 2.2 1.8

SUCE 1 2 7 3 2 1 1 2

SVCE 9.8 8.4 11.4 7.2 5.9 4.7 4.6 4.5

Ev/Ton

ARCC 1042 956 849 735 631 524 461 398

SUCE 199 240 340 249 215 119 163 195

SVCE 1944 1966 1324 1381 799 679 625 556

GPM

ARCC 42% 37% 35% 35% 35% 37% 38% 38%

SUCE 26% 25% 16% 20% 23% 26% 24% 27%

SVCE 43% 43% 33% 36% 25% 25% 23% 21%

EBITDA Margin

ARCC 39% 33% 32% 32% 32% 34% 35% 35%

SUCE 30% 31% 24% 29% 32% 35% 33% 36%

SVCE 38% 41% 23% 34% 23% 24% 22% 20%

NPM

ARCC 20% 15% 14% 16% 17% 20% 21% 22%

SUCE 12% 8% -1% 2% 5% 8% 7% 9%

SVCE 23% 23% 10% 22% 14% 15% 11% 11%

EPS

ARCC 1.1 1.0 0.9 1.0 1.2 1.5 1.7 1.8

SUCE 2.96 2.71 (0.33) 0.67 1.47 3.06 3.20 3.96

SVCE 0.3 0.3 0.2 0.4 0.5 0.6 0.5 0.5

DPS

ARCC 0.4 0.5 0.6 0.7 0.8 1.1 1.2 1.3

SUCE 0.27 0.25 - 0.17 0.51 8.27 9.13 7.46

SVCE 0.22 0.00 0.00 0.04 0.13 0.15 0.11 0.11

15

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Stock Data Outstanding Shares [in mn] 378.7 Mkt. Cap [in mn] 2,745.9 Bloomberg – Reuters ARCC EY / ARCC.CA 52-WEEKS EGP 7.14/EGP18.5 DAILY AVERAGE TURNOVER (2015) EGP 2.2MN

Ownership Aridos Jativa SLU 60% Al Borini Family 17.5% Free Float 22.5%

Source: ARCC, Prime Estimates All prices are as of 16 February 2016

Source: Bloomberg

ource: GB AUTO, Prime Estimates

0

5

10

15

20

ARCC EGX30 - Rebased

“BUY” MARKET PRICE EGP XX FAIR VALUE EGP XX POTENTIAL XX% UPSIDE

Relatively higher utilization and sales volume offset by declining prices: After solving the

energy problem ACC is able to maintain stable operations using an energy mix of 77% coal/pet

coke, 8% RDF and 22% HFO in 9M 2015. This caused to a 9% Y-o-y increase in volume sold to

reach 3.2mn tons. The company maintained a utilization rate of 85% in 9M 2015 due to the

lack of cement demand with the companies shift to coal causing an oversupply coupled with

slow demand. Meanwhile, prices witnessed a 14% y-o-y decline to reach EGP541 during 9M

2015 caused by the oversupply in the market. This caused a 4% decline in revenues to reach

EGP1, 735.2mn despite the increased volume sold. COGS/ton also declined to reach

EGP357/ton due to declining coal prices which dropped significantly in 2015 in addition to the

imported clinker in 2014 which caused a higher than usual COGS in 2014. Coal, a main energy

component for the Egyptian cement industry is expected to remain at a lower price according

to market forecasts causing maintaining a low energy COGS/ton. However, the problem facing

cement makers is acquiring the foreign currency needed for importing the coal in addition to

the unstable EGP/USD rate which is expected to reach EGP9.4/USD by 2019. EBITDA declined

by 10% y-o-y to EGP536mn in 9M15, whereas EBITDA margin recorded 31% versus 33% in

9M14. Furthermore, the recent adjustment in income tax law resulting in a reduction in the

income tax from 30% to 22.5%. Therefore net profit stood at EGP246.3mn, recording a 22% Y-

o-y increase. We estimate the company net profit to reach EGP 291.5mn in 2015. Gross profit

margin is expected to drop to 35% on the back of lower prices despite full implementation of

coal in 2015 while EBITDA margin is expected to stand at 32%. Net profit margins would stand

at 14% despite high margins due to FX losses and interest expense.

ACC pioneered shifting towards coal after the energy crisis in 2014 gaining competitive

advantage Egypt suffered from a shortage in energy in 2013 causing the constant power cuts.

As a result the government decided to change policy and dedicate all the required natural gas

supply for households. Meanwhile, cement producers were unable to operate at full utilization

due to the lack of their main energy source. The company operated at a utilization rate of 64%

due to the continuous energy cuts. Furthermore, natural gas prices were raised from

USD6/mmbtu to USD8/mmbtu (versus USD0.75/mmbtu in KSA) Furthermore, this helped the

company operate at one the market’s lowest COGS/ton of EGP 354 due to the contribution of

coal which cut the costs significantly.

Dropping coal prices benefit ACC From a global view, coal prices continued to decline, as

China alone consumes 50% of coal; currently china is having a slow-down in its GDP growth in

general and in industrial sector in specific. Moreover, the Chinese government has recently

devaluated its currency, a one-time correction as the government stated, in attempt to

support their industrial sector through boosting export with cheaper products. This is

perceived as an advantage for companies which operate using coal as they are able to import

coal at a lower cost. Coal has contributed as 70% of ACC’s energy and its price decline led to a

direct decrease in ACC’s COGS/ton. With its correlation to oil coal is expected to grow at a

slower rate. The main risk for ACC would be the further devaluation of the EGP which will

increase the coal cost.

INVESTMENT GRADE “VALUE” ARABIAN CEMENT

“HOLD” MARKET PRICE EGP 7.25 FAIR VALUE EGP 11.88 POTENTIAL 64% UPSIDE

Company Profile

Arabian Cement Company (ACC) (ARCC.CA)

was founded in 1997 by a group of Egyptian

investors and was later acquired by Spanish

company Cementos La Union. The firm

acquired a license for a production line of

2.5mtpa capacity (Cement) in its plant in Ain El

Sokhna. After the acquisition the plan was

adjusted to add a second line to reach a full

capacity of 5mtpa (Cement). In 2014 the firm

was offered for sale to the public via an IPO

that priced common equity at EGP 9/share.

Following the government’s decision to allow

the use of coal as a substitute for the

unavailable natural gas ACC was one of the

first market players to shift towards a

coal/RDF energy mix gaining a competitive

advantage with other suppliers suffering from

a shortage in natural gas.

16

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

ACC PRODUCTION AND UTILIZATION ACC COGS/TON & COGS-TO-SALES

COGS/TON COMPARISON ACC EBITDA & NET PROFIT MARGINS

SOURCE: COMPANIES FINANCIALS, IDA, PRIME RESEARCH ESTIMATES

ACC to maintain stable margins and operate fully once equilibrium is reached: Despite already

implementing coal during 2014, ACC couldn’t take advantage and was opted to operate at 85% cement

utilization. Demand hasn’t picked up as expected during 2015 while prices were dropped significantly on

the back of oversupply in the market. For instance ACC’s selling price dropped almost 13% during 2015 to

reach EGP 542/ton. However, operating at one of the lowest COGS/ton in the market meant that ACC was

one the companies that suffered the least from this price drop. Our expectation of the market to reach

equilibrium during 2017 means that ACC would be able to operate at full utilization. This will enable the

company to reap the benefit of the coal conversion. ACC has enjoyed one of the highest gross profit

margins in the market and is expected to maintain an average of 35% between 2015 and 2017. With the

prices picking up ACC’s GPM is expected to increase slightly averaging at 38% between 2018 and 2020.

Despite our expectation of the prices growth and ACC selling at a slight discount to the market average,

the company will maintain a COGS-to-Sales ratio as low as 66%. This is attributed to the low COGS/ton

which will grow at a 5 year CAGR of only 2% to reach EGP 388/ton by 2020. EBITDA is expected to grow at

a 5-year CAGR of 8.4% with EBITDA margin averaging at 34%. Net profit margin is expected to increase

from 14% in 2015 to reach 22% by 2020. Operating at higher utilization would help the company, while

interest expense is eased due to the debt repayment causing less pressure on the company’s bottom line.

This is also shown by the net profit growing at a 5-year CAGR of 16%.

48%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

0

50

100

150

200

250

300

350

400

450

2012 2013 2014 2015 2016 2017 2018 2019 2020

COGS/ton COGS to Sales

353.0

420 430

570 535

0

100

200

300

400

500

600

ARCC SVCE Suce stand Torah Helwan

ARCC SVCE Suce stand Torah Helwan

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2012 2013 2014 2015 2016 2017 2018 2019 2020

EBITDA Margin Net Profit Margin

0%

20%

40%

60%

80%

100%

120%

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Production Utilization

17

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

SOURCE: PRIME RESEARCH ESTIMATES

ACC CAPEX & CAPEX-TO-SALES

ACC facing both country and company specific

risk: Company: Arabian Cement has an ongoing

legal case over its plant license with the IDA.

ACC is currently paying EGP8m/month. The case

has been most recently moved for international

arbitration and is yet to receive a ruling. If the

company loses the case, this could result in an

immediate payment of EGP450mn, putting

temporary pressure on cash flow. In August this

year there were negotiations with Mehlab

government to solve this conflict but they

reached nothing and then the government

resigned and the new government did not made

any negotiations yet.

Country: The EGP rate versus USD has been

fluctuating since the beginning of 2015 starting at EGP7.15/USD to reach a high of EGP7.93/USD last

November. Moreover, there is a high risk of not acquiring the required foreign currency. This is much

needed for the importing of coal from South Africa. With our expectation of further hike in the EGP/USD

rate, it is believed that the coal price would increase which would put further pressure on the gross profit

margin. Furthermore, some of the company’s debt is in USD. Due to the recent energy crisis and the

FX situation they agreed with the bank to pay installments in 4 years not 1.5 years in 16 installments.

Furthermore, prices have remained lower than expected with no sign of drastic increase as we expect

them to grow at a CAGR of 3% by 2020.

Upside Risk Downside Risk 1) Leader in coal conversion process and now fully operational

1) Government intervention through introducing price cap

using coal/RDF/HFO mix. Following coal price decline. 2) Higher than average market utilization rate 85% (9M 2015)

2) Setting an increased carbon tax which would affect the Energy cost.

3) Distribution in high demand areas like Cairo and Delta.

3) FX risk affecting coal imports.

4) One of the lowest Cogs/Ton in the market.

Valuation

We Initiate Coverage for Arabian Cement reaching a fair value of EGP 11.9; implying an upside potential

of 64%, using a DCF valuation methodology. We valued ARCC utilizing an average WAAC over our

forecasted horizon of 14.05%, a risk free rate of 9.7%, an equity risk premium of 8% and a perpetual

growth rate of 3%. We preferred to use a Beta of 0.65 rather than a statistical Beta due to the company

short trading history on EGX.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

-

50,000

100,000

150,000

200,000

250,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

CAPEX CAPEX to revenues

18

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

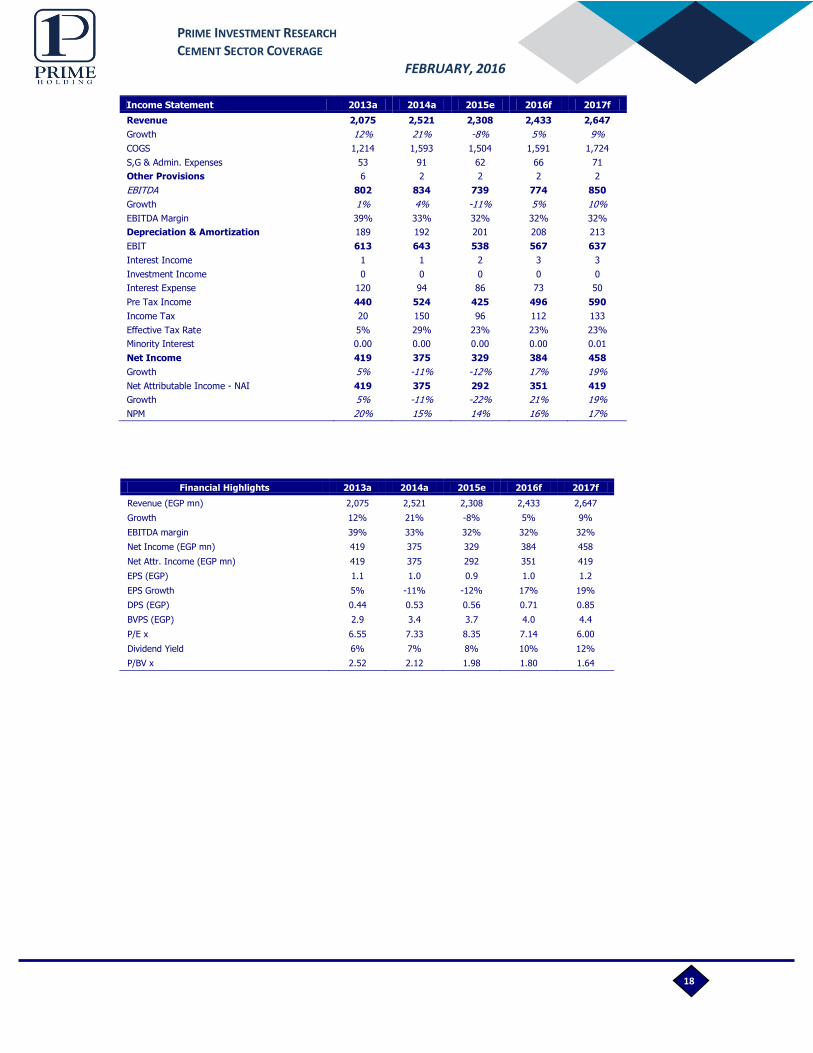

Income Statement 2013a 2014a 2015e 2016f 2017f

Revenue 2,075 2,521 2,308 2,433 2,647

Growth 12% 21% -8% 5% 9%

COGS 1,214 1,593 1,504 1,591 1,724

S,G & Admin. Expenses 53 91 62 66 71

Other Provisions 6 2 2 2 2

EBITDA 802 834 739 774 850

Growth 1% 4% -11% 5% 10%

EBITDA Margin 39% 33% 32% 32% 32%

Depreciation & Amortization 189 192 201 208 213

EBIT 613 643 538 567 637

Interest Income 1 1 2 3 3

Investment Income 0 0 0 0 0

Interest Expense 120 94 86 73 50

Pre Tax Income 440 524 425 496 590

Income Tax 20 150 96 112 133

Effective Tax Rate 5% 29% 23% 23% 23%

Minority Interest 0.00 0.00 0.00 0.00 0.01

Net Income 419 375 329 384 458

Growth 5% -11% -12% 17% 19%

Net Attributable Income - NAI 419 375 292 351 419

Growth 5% -11% -22% 21% 19%

NPM 20% 15% 14% 16% 17%

Financial Highlights 2013a 2014a 2015e 2016f 2017f

Revenue (EGP mn) 2,075 2,521 2,308 2,433 2,647

Growth 12% 21% -8% 5% 9%

EBITDA margin 39% 33% 32% 32% 32%

Net Income (EGP mn) 419 375 329 384 458

Net Attr. Income (EGP mn) 419 375 292 351 419

EPS (EGP) 1.1 1.0 0.9 1.0 1.2

EPS Growth 5% -11% -12% 17% 19%

DPS (EGP) 0.44 0.53 0.56 0.71 0.85

BVPS (EGP) 2.9 3.4 3.7 4.0 4.4

P/E x 6.55 7.33 8.35 7.14 6.00

Dividend Yield 6% 7% 8% 10% 12%

P/BV x 2.52 2.12 1.98 1.80 1.64

19

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

B alance Sheet 2013a 2014a 2015e 2016f 2017f

Cash & M arketable Securities 161 159 179 229 249

Trade Receivables-Net 42 56 50 52 57

Inventory 97 202 222 215 222

T o tal C urrent A sset 299 417 450 496 528

Net Fixed Assets 2,653 2,677 2,561 2,537 2,447

Projects Under Implementation 144 99 123 29 0

Other Assets 162 140 118 95 73

T o tal A ssets 3,259 3,334 3,252 3,158 3,048

Short Term Bank Debt 407 364 246 290 284

Accounts Payable 96 138 105 111 121

Other Current Liabilities 223 329 357 369 387

T o tal C urrent Liabilit ies 726 830 708 769 791

Long-Term Debt 1,097 844 793 497 213

Provisions 345 361 363 365 368

T o tal Shareho lders' Equity 1,090 1,298 1,388 1,526 1,676

T o tal Liab.& Shareho lders' Equity 3,259 3,334 3,252 3,158 3,048

20

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

“HOLD” MARKET PRICE EGP 16.8 FAIR VALUE EGP 29.6 POTENTIAL 76% UPSIDE

INVESTMENT GRADE “VALUE”

SUEZ CEMENT

Stock Data Outstanding Shares [in mn] 181.86 Mkt. Cap [in mn] 3,049.7 Bloomberg – Reuters SUCE EY / SUCE.CA 52-WEEKS EGP 16.5/EGP 42.5 DAILY AVERAGE TURNOVER (2015) EGP 0.7MN

Ownership Italecemnti Group 55% Abd El Menaam Rashed 7.9% Gazelle 7.61% Free Float 29.4%

Source: SUCE, Prime Estimates All prices are as of 16 February 2016

Source: Bloomberg

0

10

20

30

40

50 SUCE EGX30 - Rebased

Turning to net loss in FY2015, as a result of a compressed gross profit and soaring cogs:

Suez Cement indicators reported a net loss of EGP 60mn for the FY2015, a decline by

112% y.o.y compared to a net profit of EGP 492.6mn in FY2014. Gross profit declined by

61% y.o.y in FY2015 to be EGP 423mn from EGP 1,086mn in FY2014. This plunge in gross

profit is for two main reasons: a- The company sought a decrease of its sales revenues by

8.28% to be EGP 5,642mn in FY2015 from EGP 6,151mn in FY2014. b- Cogs soared by 3%

y.o.y, from EGP 5,065mn in FY2014 to be EGP 5,219mn. The lower sales revenue and

higher cogs are because of: 1- lower selling price which, on average, declined by about 9%

in FY2015 compared to FY2014. 2- Higher cost of energy which soared by 30%. c- Lower

sales volume in FY2015 compared to FY2014. Turning from using HFO to use coal by the

half of 2015, allowed Suez Cement facility to increase its utilization rates. However, as

Tourah still depends on HFO in 2015 and Helwan depends on a mix of HFO and natural

gas as their main sources of energy, cement utilization rates declined in FY2015 for the

two plants. This affected the total sales volume in FY2015 which recorded, in our

estimates, about 8mn ton for Suez Group. All of this resulted in a compressed gross profit

margin of 7.5% in FY2015 compared to a gross profit margin of 17.7% in FY2014. Taking a

closer look on FY2015 results we found that, 4Q was a negative one for SUCE as it turned

from recording net profit of EGP 69mn in 9M 2015, to record net loss of EGP 60mn in the

FY2015 according to the company’s released indicators. This indicates that the company

recorded net loss of more than EGP 120mn in 4Q only. In our opinion, this huge plunge in

the company’s margins in 4Q is mainly stemmed from the increase in cogs. We believe

that, there was a shortage in the government supply of HFO to the plants, this shortage

prompted the facilities to seek HFO supply from other sources, rather than the

government, at higher prices than the official price, and hence, increasing cogs. xx

A market leader aims to maintain its share. Suez Cement with its five cement plants

dominates the local cement industry in Egypt, with a total capacity of over 12mn ton of

cement. Despite of the lower prices in 2015, Suez Cement opted to maintain its leading

market share of 15% through operating at high utilization rates. We believe that, Suez

plant will increase its utilization rates in the coming years, starting 2016, until it reaches

100% utilization rate by 2019. On the other hand, the company’s management informed

us that they received all the required approval to use coal as source of energy in Helwan

and Tourah. And hence, we do not expect any increase in their utilization rates before

conversion is completed in 2018, according to our estimates.

Company Profile

Suez Cement was established in 1977 with a

production capacity of 4 mtpa. The company

started its operations by building its first plant

Suez followed by the Kattameya plant. The

company is traded in the EGX under the

symbol (SUCE) with a paid in capital of EGP

909mn and a par value of EGP 5. Suez Cement

is the largest cement producer in Egypt with a total cement capacity of 12 mtpa through its

five plants: Suez, Kattameya, Tourah, Helwan

and El Minya. The main shareholder of Suez

cement is Italcementi group, ranked as the

fifth cement producer in the world, acquires

55% of the total shares in Suez Cement.>

21

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

SOURCE: COMPANY FINANCIALS

SOURCE: COMPANY FINANCIALS

The plan to upgrade Tourah and Helwan into using coal provides a key for growth. As mentioned before

Tourah plant depends on HFO and Helwan plant depends on a mix of HFO and NG as main sources of

energy. As both Tourah and Helwan convert into using coal which is in a lower cost relative to both HFO

and NG, the cost/ton is expected to decline for Suez cement on the consolidated level. In addition, Suez

plants converted to use coal in 2015 which will also reduce cost/ton for the group. However, changing to

use coal in both Tourah and Helwan will not be before 2018, which will affect the cost/ton in the coming 2

years for the two plants affecting the whole company. The inclusion of 100% coal conversion in Tourah

and Helwan plants by 2018 would improve margins for the company. Gross profit margin would increase

by about 4% y.o.y, Meanwhile, EBITDA margin would jump to be 35% in 2018 compared to 24% in 2015

while net profit margin surge to be 7% in 2018.

The main risk to our valuation is the company’s ability to implement conversion plan in Tourah and

Helwan. As the plants are located in resedential areas, this may enforece the government to revoke

theapproval the company received.

One of the main advantages of Suez group is that it is a fully integrated player. Suez Cement has 11

subsidiaries providing complementary services, in addition to its cement plants, such as delivery services

and retail shops outlets for cement.

Company Suez Tourah Helwan

Location It operates 2 plants, one in Kattameya and the other is

in Suez.

It operates 2 plants, one in Al Minya which is 245Km away

from Cairo and the other one is in Tourah.

The plant is in Helwan

Lines 2 lines 2 lines 1 line Capacity 4.9mtpa 3mtpa 4.4mtpa

Company Main Activity Suez Cement Ownership

Tourah Portland Cement Cement production with a total capacity of 3mtpa 66%

Suez Bags the manufacture of bags that is used in packing cement and different products

56%

Helwan Cement Cement production with a total capacity of 4.4mtpa 100%

Ready Mix Concrete El Alamya Ready mix and building materials manufacture 52%

Hilal Cement Group Import, storage and distribution of cement and other building materials

51%

Egyptian Company for Development and Building Materila (DECOM)

The Manufacture of cement and Building materials 52%

Suez for Transportation and Trade Company Transporting and trading cement & building materilas

96%

Development for Industries Company Investing in all types of industrials fields 98%

Axim Egypt Investing in all types of industrials fields 98%

Suez for Imports & Exports Importing & Exporting cement and all kinds of building materials

96%

Suez Lime Company Producing and trading lime with all its different types 50%

22

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

SUEZ CEMENT

SOURCE: IDA

TOURAH CEMENT HELWAN CEMENT

SOURCE: COMPANY FINANCIALS & PRIME RESEARCH ESTIMATES

SUEZ CEMENT CONS EBITDA & NPM SUEZ CEMENT CONS CAPEX & CAPEX/SALES

Sales 2009 2010 2011 2012 2013 2014 11M 2015

Suez Sales 12,773,656

11,056,751

9,818,893

8,295,759

7,578,536

7,924,753

7,285,625

Mkt sales 51,031,184

47,846,951

48,214,200

51,135,005

50,094,510

51,283,842

48,591,368

Mkt Share 25% 23% 20% 16% 15% 15% 15%

0%

20%

40%

60%

80%

100%

120%

0

1000

2000

3000

4000

5000

6000

2012

2014

2016

2018

2020

Mn

To

n

Production Utilization

0%

20%

40%

60%

80%

100%

120%

0

500

1,000

1,500

2,000

2,500

3,000

3,500 20

12

2014

2016

2018

2020

Mn

To

n

Production Utilization

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2013 2014 2015 2016 2017 2018 2019 2020

CAPEX CAPEX to revenues

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mn

To

n

Production Utilization

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2012 2013 2014 2015 2016 2017 2018 2019 2020

EBITDA Margin Net Profit Margin

23

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Valuation

We Initiate Coverage for Suez Cement Group reaching a fair value of EGP 29.6; implying an upside

potential of 76%, using a DCF valuation methodology. We valued SUCE utilizing an average WAAC over

our forecasted horizon of 14.9%, a risk free rate of 9.7%, an equity risk premium of 8% and a perpetual

growth rate of 3%. We preferred to assign SUCE a beta of 0.75 above the statistical Beta of 0.59, we

preferred to increase beta to reflect the risk stemmed of the uncertainty regarding conversion plan in

Tourah and Helwan.

Income Statement 2013a 2014a 2015e 2016f 2017f

Revenue 5,049 6,152 5,561 5,797 6,138

Growth 9.8% 21.8% -9.6% 4.2% 5.9%

COGS 3,736 4,617 4,694 4,625 4,743

S,G & Admin. Expenses -335 -436 -479 -502 -534

EBITDA 1,099 1,187 382 664 854

Growth -1.4% 7.9% -67.8% 73.5% 28.7%

EBITDA Margin 22% 19% 7% 11% 14%

Depreciation & Amortization 379 448 462 486 503

EBIT 720 738 -79 178 351

Interest Expense 13 23 28 58 60

Pre Tax Income 729 765 -83 130 317

Income Tax 221 285 -15 28 71

Effective Tax Rate 30% 37% 18% 21% 23%

Net Income 538 493 -61 85 227

Growth 2.6% -8.5% -112.5% -238.0% 167.9%

Net Attributable Income - NAI 538 493 -61 76 204

Growth 2.6% -8.5% -112.5% -224.2% 167.9%

NPM 10.7% 8.0% -1.1% 1.5% 3.7%

Upside Risk Downside Risk

1) Stability of NG supply for Helwan plants.

1) Withdrawl of the coal licenses in Tourah & Helwan plants, since

2) Higher than expected demand the two plants are located in resedential areas.

3) Higher selling price based on location 2) FX risk for imported coal

3) Lower Demand in Upper Egypt with most of projects

in Cairo and Delta areas

24

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Balance Sheet 2013a 2014a 2015e 2016f 2017f

Cash & Marketable Securities 1,817 1,626 1,265 1,633 1,767

Trade Receivables-Net 204 220 168 166 170

Inventory 844 1,194 1,345 1,325 1,359

Total Current Asset 3,129 3,488 3,128 3,487 3,680

Net Fixed Assets 3,523 3,886 3,788 3,570 3,385

Projects Under Implementation 536 607 319 381 600

Total Assets 9,971 10,765 10,019 10,223 10,449

Short Term Bank Debt 3 67 481 490 479

Total Current Liabilities 1,265 1,953 1,958 2,042 2,034

Long-Term Debt 58 147 149 119 89

Provisions 670 720 785 833 880

Total Shareholders' Equity 7,930 7,865 7,030 7,114 7,311

Total Liab.& Shareholders' Equity 9,971 10,765 10,019 10,223 10,449

Year 2013a 2014a 2015e 2016f 2017f

Revenue (EGP mn) 5,049 6,152 5,561 5,797 6,138

Growth 10% 22% -10% 4% 6%

EBITDA margin 22% 19% 7% 11% 14%

Net Income (EGP mn) 538 493 -61 85 227

Net Attr. Income (EGP mn) 538 493 -61 76 204

EPS (EGP) 3.0 2.7 -0.3 0.5 1.2

EPS Growth 2.6% -8.5% -112.5% -238.0% 167.9%

DPS (EGP) 0.3 0.2 0.0 0.1 0.4

BVPS (EGP) 43.6 43.2 38.7 39.1 40.2

P/E x 5.67 6.19 -49.70 36.01 13.44

Dividend Yield 2% 1% 0% 1% 3%

P/Book x 0.38 0.39 0.43 0.43 0.42

25

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

“HOLD” MARKET PRICE EGP 3.53 FAIR VALUE EGP 5.49 POTENTIAL 55% UPSIDE

INVESTMENT GRADE “VALUE” SOUTH VALLEY CEMENT

Stock Data Outstanding Shares [in mn] 482.3 Mkt. Cap [in mn] 1,703.4 Bloomberg – Reuters SVCE EY / SVCE.CA 52-WEEKS EGP 3.3/EGP 7.2 DAILY AVERAGE TURNOVER (2015) EGP 2.3MN

Ownership Blue Nile LTD 37.7% GAZELLE LTD INC 9.3% Al Nahla Co 8.2% Free Float & Others 44.8%

Source: SVCE, Prime Estimates All prices are as of 16 February 2016

Source: Bloomberg

0

2

4

6

8

10 SVCE EGX30 - Rebased

Company Profile

South Valley Cement Company was

established in 1997 to produce top quality

cement and its associated products, as well

as a wide range of other premium building

materials products such as Ready Mix,

beside owning and managing a huge

portfolio of diverse multi sector direct and

indirect investments. The company has

been listed on the EGX since 1998 and

currently operates at a clinker capacity of

1.6mtpa equivalent to 1.76mtpa cement

capacity

Declining net profit for 9M 2015 on the back of lower gross profit and higher Marketing

expenses SVCE reported a 27% y-o-y decline in net profit to reach EGP72.5mn. Despite

maintaining almost an unchanged gross profit the company suffered from a declining

gross profit margin to reach 19% (versus 30% in 9M 2014). The company enjoyed a 56%

revenue increase on the back of increased volume. Like most Egyptian cement producers

the company suffered from natural gas shortage in 2014 causing them to operate at

lower utilization rates with SVCE operating as low as 61%. However during 2015 the

government has ensured the supply of HFO as a substitute for natural gas, which despite

being more costly ensures the continued operations for the companies leading to a

utilization of 87%. In terms of production costs, the company has endured higher costs

due to the increased energy costs after using HFO. The increase in selling and marketing

expenses is also a main reason for the declining net profit which surged 192% to reach

EGP48mn in 9M 2015 causing an additional burden on the company’s EBITDA and net

profit. We expect SVC to record a net profit of EGP 85.4mn in 2015. This is caused by the

declining gross profit due to the its high COGS/ton of EGP 439. The high marketing

expenses are expected to remain and pressure the EBITDA which is expected to drop 33%

y-o-y. As a result EBITDA margin is expected to drop significantly to 20%, while the net

margin is expected to also drop significantly to reach 10%.

Coal conversion key to future improvement of financial position. SVC’s declining gross

margin in 2015 has been mainly caused by the decreasing gross profit margin. While

revenues declined on lower prices COGS inflated mainly based on energy. South Valley

Cement has been operating on a natural gas/ HFO energy mix in 2014, however due to

the lack of natural gas the company was forced to use HFO for 100% of its energy needs

which stands between EGP235/ton – EGP272/ton of cement compared to EGP214/ton of

cement for natural gas. Going forward we expect a complete surge in operations as a

result of coal conversion. SVC is expected to include coal in its energy mix by 2016 with a

much lower current value EGP118/ton of cement. Such conversion would be key to a

higher gross profit margin. The inclusion of coal for 45% of required energy would cause a

5% y-o-y decline for COGS/ton to reach EGP417 by 2016. In 2016 EBITDA margin jumps to

reach 33% (versus 20% in 2015) while net profit margin surge to reach 22%. It is

noteworthy, that global coal forecasts have been cut significantly as we showed

previously in correlation with declining oil prices. That would set a further advantage for

companies converting to coal. COGS/ton would drop further to reach EGP385 by 2017.

However, this stands only for the first production line as the second line relies on

imported clinker at a much higher cost. This explains the significant drop in gross profit

margin which remains at an average of 24% between 2017-2020 compared to 36% in

2016. Both EBITDA and net margins drop as a result of the high cost of imported coal to

average at 22% and 13% for this same period (2017-2020), respectively.

26

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

SVC PRODUCTION & UTILIZATION SVC COGS/TON & COGS-TO-SALES

SOURCE: SVC FINANCIALS & PRIME RESEARCH ESTIMATES

South Valley to double capacity by 2017 SVCE is expected to add a further capacity at a total cement

capacity of 1.76mtpa starting 2017. This added capacity is set to increase the company’s market share

after reaching a total capacity of 3.4mtpa. Adding to the companies sold volume would signal improved

the company’s profits due to its higher selling prices. Moreover, the new projects and added demand

which is expected to surpass market capacity by the end of 2017 ensures a market for the increased

production capacity. However, a main concern for this line is that it relies on imported clinker as it doesn’t

own a silo to produce clinker. Imported clinker costs is significantly higher than produced clinker which

would force the company to maintain lower utilization rates for the second line in case it becomes value

destructive. This could be caused by a further devaluation for the Egyptian pound or even the FX shortage

that remains a concern.

New licenses represent key opportunity SVC would benefit from acquiring one of the new licenses as it

enables them to produce clinker for the second line instead of importing them cutting the COGS

significantly in addition to removing any FX risk. Furthermore, SVC would be able to operate at full

utilization for the second line and take advantage of its relatively higher selling prices. Such a key change

would add significant value to the company. We note that such value was not take into our valuation of

the company since no official steps have been taken however if such action occurs it would cause a

revision for the company’s target price.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100

200

300

400

500

600

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EGP

COGS/ton

COGS/ton (excluding import Cost)

COGS to Sales

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

mn

to

ns

Production Utilization

27

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

SVC EBITDA & NET MARGINS SVC CAPEX & CAPEX-TO-REVENUES

SOURCE: SVC FINANCIALS & PRIME RESEARCH ESTIMATES

Upside Risk Downside Risk 1) Conversion to coal to ensure lower production costs

1) FX risk for imported coal

2) Obtaining a license would be a great opportunity & would require a revision for current value

2) Lower Demand in Upper Egypt with most of projects

in Cairo and Delta areas

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EBITDA Margin Net Profit Margin

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

(200,000)

-

200,000

400,000

600,000

800,000

1,000,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

EGP

, mn

CAPEX CAPEX to revenues

Valuation

We Initiate Coverage for South Valley Cement reaching a fair value of EGP 5.5; implying an upside

potential of 55%, using a DCF valuation methodology. We valued SVCE utilizing an average WAAC over

our forecasted horizon of 16.59%, a risk free rate of 9.7%, an equity risk premium of 8% and a perpetual

growth rate of 3%. We calculated SVCE’s adjusted statistical Beta which came at 1.10.

28

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Income Statement 2013a 2014e 2015f 2016f 2017f

Revenue 572 662 875 926 1,757

Growth 9% 16% 32% 6% 90%

COGS 329 375 589 592 1,327

S,G & Admin. Expenses 23 14 16 17 19

EBITDA 220 273 271 317 412

Growth 56% 18% -33% 77% 31%

EBITDA Margin 38% 41% 31% 34% 23%

Depreciation & Amortization 50 61 68 69 70

EBIT 170 212 203 248 342

Interest Income 2 2 1 15 0

Interest Expense 29 27 19 48 81

Non-Operating Income 0 1 0 0 0

Non-Operating Expenses 0 2 46 0 0

Extra-Ordinary Items -10 -23 -1 0 0

Pre Tax Income 133 163 138 215 262

Net Income 133 163 138 215 262

Growth 25% 13% -44% 139% 22%

Net Attributable Income - NAI 133 163 138 215 262

Growth 25% 13% -44% 139% 22%

NPM 23% 25% 16% 23% 15%

Financial Highlights 2013a 2014e 2015f 2016f 2017f

Revenue (EGP mn) 572 662 875 926 1,757

Growth 9% 16% 32% 6% 90%

EBITDA margin 38% 41% 31% 34% 23%

Net Income (EGP mn) 133 163 138 215 262

EPS (EGP) 0.3 0.3 0.2 0.4 0.5

EPS Growth 26% 14% -44% 139% 22%

DPS (EGP) 0.2 0.0 0.0 0.0 0.1

BVPS (EGP) 6.8 6.7 6.9 7.3 7.8

P/E x 12.75 11.26 19.93 8.35 6.84

Dividend Yield 6% 0% 0% 1% 4%

P/BV x 0.52 0.53 0.51 0.48 0.45

29

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

Balance Sheet 2013a 2014e 2015f 2016f 2017f

Cash & Marketable Securities 88 113 304 81 234

Trade Receivables-Net 4 5 6 6 12

Inventory 55 71 71 74 145

Other Current Asset 4 4 7 7 13

Total Current Asset 151 194 388 168 403

Net Fixed Assets 1,683 1,654 1,646 1,596 1,545

Projects Under Implementation 29 24 0 435 870

Subsidiaries & Other Long Term Investments 1,884 1,825 1,790 1,808 1,862

Other Assets 254 257 263 263 263

Total Assets 4,000 3,953 4,087 4,271 4,944

Short Term Bank Debt 230 239 182 90 216

Accounts Payable 75 75 88 89 199

Other Current Liabilities 139 161 162 162 163

Total Current Liabilities 444 476 432 341 577

Long-Term Debt 250 234 325 395 604

Other Non Current Liabilities 1 1 3 3 3

Total Shareholders' Equity 3,305 3,242 3,328 3,531 3,760

Total Liab.& Shareholders' Equity 4,000 3,953 4,087 4,271 4,944

30

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

31

PRIME INVESTMENT RESEARCH CEMENT SECTOR COVERAGE

FEBRUARY, 2016

PRIME SALES TEAM

Hassan Samir Managing Director

+202 3300 5611 [email protected]

Mohamed Ezzat Head of Sales & Branches

+202 3300 5784 [email protected]

Shawkat Raslan Heliopolis Branch Manager

+202 3300 5110 [email protected]

Amr Saber Team Head-Institutions

Desk

+202 3300 5659 [email protected]

Amr Alaa, CFTe Manager

+202 3300 5609 [email protected]

Mohamed Elmetwaly Manager

+202 3300 5610 [email protected]

Emad Elsafoury Manager

+202 3300 5624 [email protected]

RESEARCH TEAM

+202 3300 5728

HEAD OFFICE

PRIME SECURITIES S.A.E. Regulated by CMA license no. 179 Members of the Cairo Stock Exchange 2 Wadi El Nil St., Liberty Tower, 7th-8th Floor, Mohandessin, Giza, Egypt Tel: +202 33005700/770/650/649 Fax: +202 3760 7543

Disclaimer Information included in this report has no regard to specific investment objectives, financial situation, advices or particular needs of the report users. The report is published for information purposes only and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Unless specifically stated otherwise, all price information is only considered as indicator. No express or implied representation or guarantee is provided with respect to completeness, accuracy or reliability of information included in this report. Past performance is not necessarily an indication of future results. Fluctuation of foreign currency rates of exchange may adversely affect the value, price or income of any products mentioned in this report. Information included in this report should not be regarded by report users as a substitute for the exercise of their own due diligence and analysis based on own assessment and judgment criteria. Any opinions given are subject to change without notice and may significantly differ or be contrary to opinions expressed by other Prime business areas as a result of using different assumptions and criteria. Prime Group is under no obligation responsible to update or keep current the information contained herein. Prime Group, its directors, officers, employees or clients may have or have had interests or long or short positions in the securities and/or currencies referred to herein, and may at any time make purchases and/or sales in them as principal or agent. Prime Group, its related entities, directors, employees and agents accepts no liability whatsoever for any loss or damage of any kind arising from the use of all or part of these information included in this report. Certain laws and regulations impose liabilities which cannot be disclaimed. This disclaimer shall, in no way, constitute a waiver or limitation of any rights a person may have under such laws and/or regulations. Furthermore, Prime Group or any of the group companies may have or have had a relationship with or may provide or have provided other services, within its objectives to the relevant companies. Prime Group 2016 all rights reserved. You are hereby notified that distribution and copying of this document is strictly prohibited without the prior approval of Prime Group.