cement outlook: 2007 annual concrete pavement workshop january 2007 salt lake city, ut steven ko pca...

TRANSCRIPT

Cement Outlook: 2007

Annual Concrete Pavement WorkshopJanuary 2007

Salt Lake City, UT

Steven Ko

PCA Senior Regional Economist

Key Points of Analysis

U.S. Economic Outlook

Construction Outlook

Cement Outlook

Residential

Nonresidential

Public

Demand

Operating Conditions

Residential

Nonresidential

Public

Regional Perspective

Economic Outlook : Real GDP Growth

-2

-1

0

1

2

3

4

5

6

7

8

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2004: 4.2%

Real GDP Annual Growth Rate

----------2004---------- -------2005------- -------2006------ -------2007-------

2005: 3.5%

2006: 3.1%

2007: 2.6%

Economic Growth Conclusions

Consumption Growth Slows 2006-2007Consumption Growth Slows 2006-2007

Interest Rates Gradually RiseInterest Rates Gradually Rise

Snap Shot of Economic Activity

Investment15%

Government18%

Consumer69%

Consumption acts as the anchor for US economic activity.Consumption acts as the anchor for US economic activity.

Any retrenchment in consumer spending will lead to slower economy-wide growth rates

Consumer Spending

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2000 2002 2004 2006 2009

Consumer Spending Outlook

Job & income Job & income growthgrowth

Oil prices, Oil prices,

inflation and inflation and interest ratesinterest rates

Affordability Affordability erosion erosion

Housing & refinancing

Oil Price Outlook

$10

$20

$30

$40

$50

$60

$70

$80

2000 2002 2004 2006 2008 2010

$ Per Barrel, West Texas Intermediate

Oil Prices are Oil Prices are declining as declining as projectedprojected

Strong International Strong International DemandDemand

Supply Disruptions Supply Disruptions ContinueContinue

OPEC ActionsOPEC Actions

2006: $65.85 per 2006: $65.85 per barrel WTI 2007: barrel WTI 2007: $60.30$60.30

Federal Reserve Policy Actions

0

1

2

3

4

5

6

7

2000 2002 2004 2006 2008

Federal Funds Interest Rate, Annual Percentage Rate

Overall Economy & Job Overall Economy & Job Growth SlowingGrowth Slowing

Inflation a growing Inflation a growing concern concern

Dilemma: Inflation or Dilemma: Inflation or Growth?Growth?

Do not count out further Do not count out further Fed TighteningFed Tightening

Risk of Fed over-Risk of Fed over-

reactionreaction

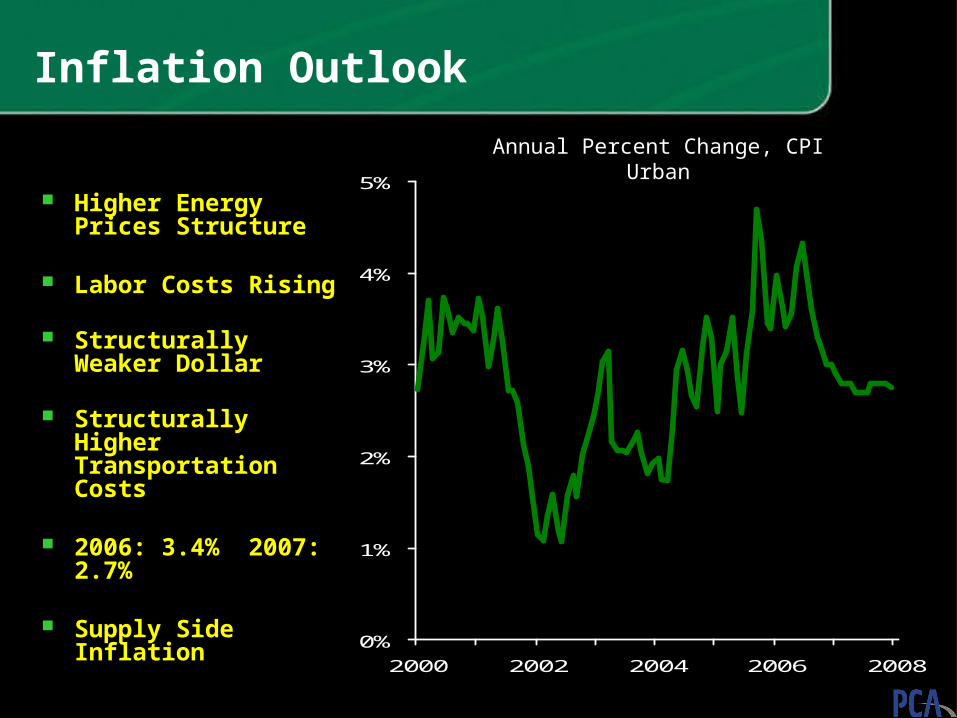

Inflation Outlook

0%

1%

2%

3%

4%

5%

2000 2002 2004 2006 2008

Annual Percent Change, CPI Urban

Higher Energy Higher Energy Prices StructurePrices Structure

Labor Costs RisingLabor Costs Rising

Structurally Weaker Structurally Weaker Dollar Dollar

Structurally Higher Structurally Higher Transportation Transportation CostsCosts

2006: 3.4% 2007: 2006: 3.4% 2007: 2.7%2.7%

Supply Side InflationSupply Side Inflation

Single Family Housing Starts

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

(000) Units

Growing Downside Risks

Inventory Draw Required

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2000 2001 2002 2003 2004 2005 2006

Homes on Market/Monthly Selling Rate

Ten Year Average

Inventory Build

Required

Inventory Draw

Required

Highest Level Highest Level Since 1997Since 1997

Mortgage Rate History: 30 Year Conventional

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

2000 2001 2002 2003 2004 2005 2006 2008

Annual Growth Rate, 30 Year Conventional

Peak to Peak to Trough Trough

294 Basis 294 Basis Point Point

DeclineDecline

Last 12 Last 12 Months Months

Reflect a Reflect a 100 Basis 100 Basis

Point Point IncreaseIncrease

Growing Home Price & Income Gap

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

1990 1992 1994 1996 1998 2000 2002 2004

Annual Growth Rate Comparison

Home Prices

Household Income

Sub-Prime Mortgage Resets

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Total Loans Scheduled for Reset

Period of Emerging Period of Emerging TroubleTrouble

Single Family Permits - Utah

0

5,000

10,000

15,000

20,000

25,000

30,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

# of units

Multi-Family Permits - Utah

3,300

3,400

3,500

3,600

3,700

3,800

3,900

4,000

4,100

4,200

2001 2002 2003 2004 2005 2006 2007 2008 2009

# of units

Residential Cement ConsumptionUtah

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Metric Tons

Affordability Index

Most Affordable

Pacific

MountainWest North Central East North

Central

SouthAtlantic

East South

Central

West South Central

NewEngland

Middle Atlantic

Affordability Ratio

2nd Tier 3rd Tier 4th Tier Least Affordable

Economic Growth Conclusions

Consumption Growth Slows 2006-2007Consumption Growth Slows 2006-2007

Interest Rates Gradually RiseInterest Rates Gradually Rise

Investment Sector Strength Continues Investment Sector Strength Continues

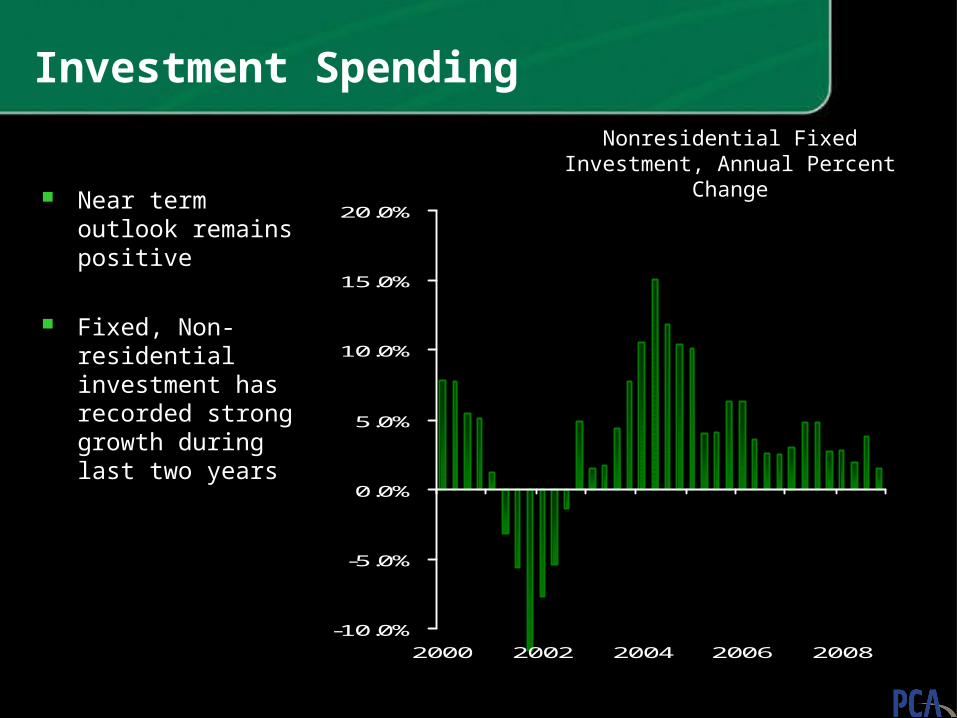

Investment Spending

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2000 2002 2004 2006 2008

Nonresidential Fixed Investment, Annual Percent Change

Near term outlook Near term outlook remains positiveremains positive

Fixed, Non-residential Fixed, Non-residential investment has investment has recorded strong recorded strong growth during last two growth during last two yearsyears

Nonresidential Construction

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1999 2000 2001 2002 2003 2004 2005 2006

Annual Growth Rate+9.2% 2006 First Half

6.8% Projected 2006

Nonresidential Outlook

Lodging OutlookLodging Outlook

Retail OutlookRetail Outlook

Health Construction Outlook Health Construction Outlook

Office Building OutlookOffice Building Outlook

Industrial OutlookIndustrial Outlook

Labor Market Outlook

-600

-400

-200

0

200

400

600

2000 2002 2004 2006 2008

Monthly Net Job Creation, Payroll Survey

Job growth slowingJob growth slowing

Unemployment risesUnemployment rises

Slow down in trend Slow down in trend

of accelerating of accelerating wageswages

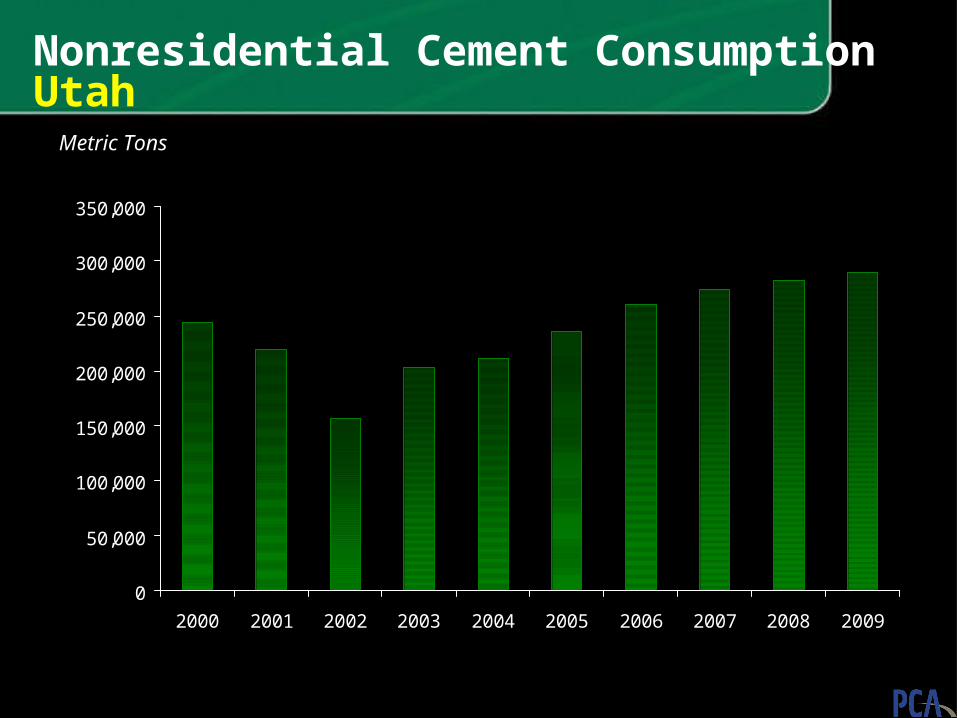

Nonresidential Cement ConsumptionUtah

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Metric Tons

Economic Growth Conclusions

Consumption Growth Slows 2006-2007Consumption Growth Slows 2006-2007

Interest Rates Gradually RiseInterest Rates Gradually Rise

Investment Sector Strength Continues Investment Sector Strength Continues

Large Trade Deficit and Federal Deficit Act as Drag on Large Trade Deficit and Federal Deficit Act as Drag on

GrowthGrowth

Foundations for Growth remainFoundations for Growth remain

Public Construction Outlook:State & Local Share of Public Construction

85%

87%

89%

91%

93%

1990 1992 1994 1996 1998 2000 2002 2004

Percent of Total Public Construction Spending

Public Construction Outlook

-60

-40

-20

0

20

40

60

80

1979Q1 1991Q1 2003Q1

93% of public construction 93% of public construction performed at state/local performed at state/local level.level.

State/Local fiscal problems State/Local fiscal problems

fading.fading.

Revenue growth improves Revenue growth improves with economy and job with economy and job growth.growth.

Highway Bill adds strengthHighway Bill adds strength 2006: +4.8% 2007: +5.5%2006: +4.8% 2007: +5.5% Note: 2005: +1.9%Note: 2005: +1.9%

Billion $ State Surplus/Deficit, NIPA

MARI

NH

0-9% 20-29% 30-39%

Pacific

MountainWest North Central

East North Central

SouthAtlantic

East South

Central

District of Columbia

West South Central

NewEngland

Middle Atlantic

10-19%

Deficit as percentage of budget

$.85

$.11

$1.0

$.16$0

$.36

$.4 $.98

$0$1.5

$.05

$.38

$.3

$.12

$38

$3.7

$3.6

$.6

$.22

$.41

$1.0

$.09

$2.4$0

$2.0

$.75

$.5

$.49

$1.3

$1.7

$.2

$.2

$2.4

$9.3

$2.0

$.74

$4.6

$.14$.4

$.15$3.0$.17

$.85$.2

NJ$1.9CT

MDDE

VT

$.25$1.1

$2.0

$.03

$.08

Primary Source: Newsweek July 28, 2003

Secondary Sources:Nat’l Conf. of State Leg., Center on Budget and Policy Priorities, Nat’l Assn. of State Budget Officers, Calif. Budget Project

Dollar figures, in billions, indicate amount states had to save to balance 2004 budget.

KEY

Public Construction Outlook: State Deficit Estimates Fiscal Year 2004

MARI

NH

Public Construction Outlook: State Deficit Estimates Fiscal Year 2005

0-9% 20-29% 30-39%

Pacific

MountainWest North Central

East North Central

SouthAtlantic

East South

Central

District of Columbia

West South Central

NewEngland

Middle Atlantic

10-19%

Deficit as percentage of budget

$0

$0

$0

$0

$.3

$1.1

$.17

$15

$0

$2

$.5

$.34

$.71

$.19

$.0

$.6

$.62

$.17

$.9

$0

$5.1

$5

$.14

$0$1.5$.19

$.74

NJ$.2CT

MD$.93

$.8

Secondary Source: National Association of Budget Officers

Dollar figures, in billions, indicate amount states had to save to balance 2005 budget.

KEY

No availabledata

DE $0

$0

$.9

$0

$.6$.2

$.9

$0

$.21

$0

$0

$0

$.3

$0

$.5

$0

$0

VT $0

$.12

$0

Primary Source: Center on Budget Policy and Priorities Feb / 04

Public Cement Consumption Utah

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Metric Tons

Changing Composition of Construction Spending

Growth Leader: ResidentialGrowth Leader: Residential

Public: Weak Tax Public: Weak Tax RevenuesRevenues

Growth Laggard: Growth Laggard: NonresidentialNonresidential

Growth Leader : Growth Leader : NonresidentialNonresidential

Public: Tax Revenues Public: Tax Revenues RecoverRecover

Growth Laggard : Growth Laggard : ResidentialResidential

2001-2005 2006-2009

Low Interest Rates, Weak Economy

Rising Interest Rates, Strong Economy

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2000 2002 2004 2006 2008 2010

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Growth Rate Yellow Line Volume, Green Bar

Portland Cement Outlook

Thousand Metric TonsAnnual Percent Change

No Shortage Tight Supplies

Cement Supply Survey Summer 2006

Spot Tight Supplies

Market Balances: Trend

0

20000

40000

60000

80000

100000

120000

140000

160000

2002 2004 2006 2008 2010

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

2002 2004 2006 2008 2010

0

5

10

15

20

25

Inventory Adjustment

Adjusted Supply Vs ConsumptionGreen: Domestic Yellow: Imports

Green: Inventory Red: Day Supply

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

1980 1985 1990 1995 2000 2005 2010

$5.0 Billion Committed to Expansion

Thousand Metric Tons Clinker

Cement Capacity Outlook

Domestic Supply Conclusions

Tight market conditions dramatically reducedTight market conditions dramatically reduced

Characterized by high operating ratesCharacterized by high operating rates

Persistently lean inventory positionPersistently lean inventory position

Major expansion does not materialize until 2008.Major expansion does not materialize until 2008.

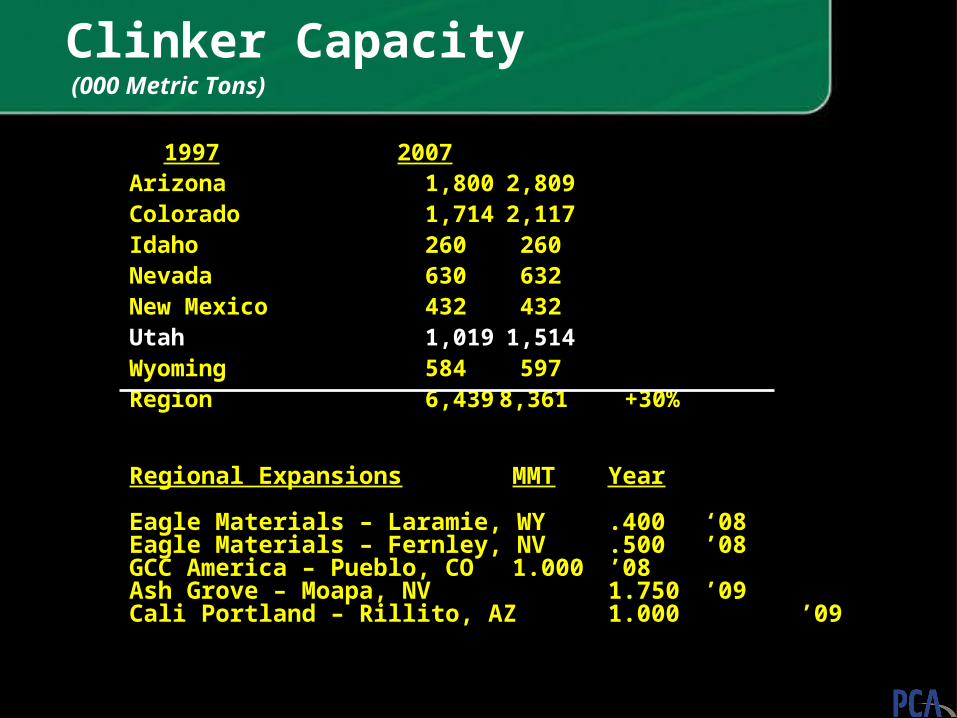

Clinker Capacity (000 Metric Tons)

19971997 20072007ArizonaArizona 1,8001,800 2,8092,809ColoradoColorado 1,7141,714 2,1172,117IdahoIdaho 260260 260260NevadaNevada 630630 632632New MexicoNew Mexico 432432 432432UtahUtah 1,0191,019 1,5141,514WyomingWyoming 584584 597597RegionRegion 6,4396,439 8,361 8,361 +30%+30%

Regional Expansions MMT Year

Eagle Materials – Laramie, WY .400 ‘08Eagle Materials – Fernley, NV .500 ’08GCC America – Pueblo, CO 1.000 ’08Ash Grove – Moapa, NV 1.750 ’09Cali Portland – Rillito, AZ 1.000 ’09

20032003 20042004 20052005 20062006 20072007

ArizonaArizona 3.613.61 4.124.12 4.674.67 4.614.61 4.714.71 %Change%Change 10%10% 14%14% 13%13% -1%-1% 2%2%

ColoradoColorado 2.292.29 2.442.44 2.592.59 2.612.61 2.692.69% Change% Change -12%-12% 7% 7% 6%6% 1%1% 3%3%

IdahoIdaho 0.590.59 0.690.69 0.710.71 0.710.71 0.700.70 %Change%Change 4%4% 16%16% 3%3% 1%1% -1%-1%

NevadaNevada 2.032.03 2.382.38 2.602.60 2.652.65 2.702.70 %Change%Change 10%10% 18%18% 9%9% 2%2% 2%2%

New MexicoNew Mexico 0.810.81 0.940.94 0.900.90 0.920.92 0.940.94 %Change%Change -1%-1% 16%16% -4%-4% 3%3% 1%1%

UtahUtah 1.201.20 1.371.37 1.541.54 1.601.60 1.661.66 %Change%Change 3%3% 14%14% 12%12% 4% 4% 4%4%

WyomingWyoming 0.420.42 0.460.46 0.480.48 0.480.48 0.490.49 %Change%Change 3%3% 9%9% 4%4% 1%1% 2%2%

U.S.U.S.%Change%Change 4%4% 7%7% 6%6% 1%1% 1%1%

Regional Portland Cement Consumption(Million Metric Tons)

Key Markets Exposure - Utah

Cement Consumption as % of Total State Cement Consumption

Residential: Residential: 27 %27 % National: 35%National: 35%

Nonresidential: Nonresidential: 16%16% National: 18%National: 18%

Public: Public: 56%56% National: 47%National: 47% Highway: Highway: 34%34% National: 30%National: 30%

Cement per Capita U.S.: .41

Cement per Capita Utah: .64

Residential Spending: Regional

1 Idaho 39.5%

United States 35.2%

2 New Mexico 32.1%

3 Arizona 31.2%

4 Colorado 28.6%

5 Utah 27.4%

6 Nevada 26.7%

7 Wyoming 13.0%

Cement Consumption as % of Total State Cement Consumption

Nonresidential Spending: Regional

1 Wyoming 38.7%

2 Colorado 27.6%

3 New Mexico 26.6%

4 Idaho 25.7%

5 Nevada 21.2%

6 Arizona 19.7%

United States 18.1%

7 Utah 16.3%

Cement Consumption as % of Total State Cement Consumption

Public Spending: Regional

1 Utah 56.0%

2 Nevada 52.0%

3 Arizona 48.9%

4 Wyoming 48.2%

United States 47.0%

5 Colorado 43.7%

6 New Mexico 41.1%

7 Idaho 34.3%

Cement Consumption as % of Total State Cement Consumption

Street & Highway Spending: Regional

1 Wyoming 38.5%

2 Utah 33.6%

3 Nevada 32.5%

United States 29.9%

4 Arizona 26.4%

5 Idaho 23.5%

6 Colorado 23.3%

7 New Mexico 23.3%

Cement Consumption as % of Total State Cement Consumption

Cement Outlook - Utah

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Metric TonsYear

2005 12.2%

2006 3.6%

2007 4.1%

2008 0.1%

Conclusions

Slower Economic Growth AheadSlower Economic Growth Ahead

Construction Market FlatteningConstruction Market Flattening

Cement Supply Slow to Adjust to Slower Growth Cement Supply Slow to Adjust to Slower Growth

Environment Environment

Slower Growth in Cement ConsumptionSlower Growth in Cement Consumption

Cement Outlook: 2007

Annual Concrete Pavement WorkshopJanuary 2007

Salt Lake City, UT

Steven Ko

PCA Senior Regional Economist