ccim investment trends quarterly - 3q 2010

TRANSCRIPT

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 1/25

Sponsored by:

RERCs CCIM

InvestmentTrendsQUARTERLY Third Quarter 2010 Report s Vol. 6, No. 3

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 2/25

1Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

August 2010

Dear Readers,

As mid-year data has suggested, the economic recovery has lost its steam. Growth remains positive, but momen-tum has slowed, and even the Federal Reserve has lowered their growth expectations for the rest of the year. Weunderstand that this slowdown is part of the recovery process, and that there will be more ups and downs beforewe achieve stabilization, but it is still disheartening to recognize that there is likely to be little if any job growth for the rest of 2010.

Even so, there are some positive trends to point out in the commercial real estate market, as investors continue toseek the general stability that this asset class offers. Transaction volume for the national of ce market increasedby nearly 30 percent during second quarter 2010 on a 12-month trailing basis. In addition, the of ce sector saw its

rst pricing increase on a 12-month trailing basis in several years, with the size-weighted average price increas -ing by approximately 15 percent. The industrial sector has not seen much improvement yet in either volume or pricing, but volume did increase for the retail, apartment, and hotel sectors on a 12-month trailing basis, alongwith some increase in size-weighted average pricing. As one would expect, transaction activity for the of ce mar -ket was heaviest in the East region, and activity in the industrial market was heaviest in the West region.

We would also like to thank those who responded to RERC’s research surveys. The comments, data, and ratingsyou provide offer exceptional insight to the changes occurring in the commercial real estate industry, and we ap-

preciate your willingness to share information for the bene t of all.

Sincerely,

Kenneth P. Riggs, Jr., CCIM, CRE, MAIPresident & CEOReal Estate Research Corporation (RERC)

Richard E. Juge, CCIM, CIPS, SIOR2010 CCIM Institute PresidentPresident, RE/MAX Commercial Brokers, Inc.

F o r e w o r d

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 3/25

2Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Recovery Losing Momentum

As the various economic reports came in during the pastmonth, it was obvious that the economic recovery hadlost its momentum. Even so, it was disappointing to hear that second quarter gross domestic product (GDP) growthslowed to 2.4 percent from an upwardly-revised rst quarter growth rate of 3.7 percent on an annualized basis. Althoughthe decline in growth was due mostly to stronger importsand slower inventories, there is concern about the resil-ience of the recovery.

Further, consumer spending, still considered the growth en-gine for the U.S. economy and comprising about 70 percentof its annual growth, declined in second quarter. With stim-ulus funds subsiding, government spending also declinedslightly. Business spending remained strong, however, withgrowth at more than 20 percent for the second consecutivequarter.

This slowdown led the Federal Open Market Committee(FOMC) to lower its GDP growth forecast to between 3.0and 3.5 percent in 2010, but even this may be optimistic.The fact that the National Bureau of Economic Research(NBER) has been reluctant to declare the recession of cial -ly over adds to the economic uncertainty and chatter aboutthe risk of a double-dip recession. (The risk of a double-dip recession increased slightly in June 2010, bringing thelikelihood up to 27 percent, according to analysis of surveyresults conducted by Moody’s Economy.com.)

Consumer Con dence Wanes

Flat home values, battered retirement accounts, stagnantwage growth, and the weak job market are having a decid-edly negative effect on consumer con dence and spending,as re ected by the Conference Board’s Consumer Condence Index, which dropped to 52.9 in June 2010 from theMay reading of 62.7. In addition, consumer spending re-mained at in June, and June retail sales declined 0.5 per cent from May, although sales were still 4.8 percent higher than year-ago reports. Both the Consumer Con dence Index and retail sales gures had been on the rise during the3 months prior to June, but concerns about the strength andsustainability of the economic recovery, along with expecta-tions of slower job growth, led to declines in both of theseimportant indicators by the end of second quarter. On the other hand, consumers increased their personalsavings rate to 6.4 percent, or $725.9 billion, in June, ac-cording to the Commerce Department. Some economistsview increased savings as an indication that consumershave made good progress toward repairing their nancesand will be in a position to increase their spending duringthe second half of the year, while other economists believethe savings rate re ects the bleak economic outlook andconsumers’ desire to prepare for an uncertain future.

Job Growth Lacking

Although the unemployment rate dropped to 9.5 percent inJune 2010 and the U-6 unemployment rate ticked down to

I n v e s t m e n t E n v i r o n m e n t

With the slowing momentum in the economic recovery mademore evident in second quarter 2010, we are seeing further bifurcation in the investment environment. The labor marketis weak, yet there are signi cant increases in corporate prof -its. Consumers are pulling back, yet the stock market hasbeen positive. With respect to commercial real estate, weare seeing some of the highest prices ever being paid for properties, like the recent sale of a Chicago of ce tower for $655 million ($500 per square foot), as well as some of thebiggest losses, like the Peter Cooper Village and StuyvesantTown apartment complexes in New York that were nancedat $5.4 billion at the peak of the market, and were returnedto creditors earlier this year at an estimated value of $1.8billion. And while there is strong demand at the top of theinstitutional market for investment real estate (and in fact, ascarcity premium is being paid for such properties), we areseeing little demand in many of the tertiary markets.

In his Semiannual Monetary Policy Report to Congress inJuly 2010, Federal Reserve Chairman Ben Bernanke de-scribed the economic outlook in the U.S. as “unusually un-certain.” Besides causing another huge drop in the stockmarket the day the phrase was uttered, the term seems tohave reinforced the lack of con dence that Americans havebeen feeling about the economic recovery, the government’shandling of the recession, and their own nancial wellbeing.

Although there are still some positive indicators in the in-vestment environment, we have received a host of nega-tive reports of late, and there is concern about the resilienceof the economic recovery. This is especially discouraging,given that the signs of recovery had been more positive justa few months ago. On the other hand, even in challengingtimes with multiple risks dominating the investment environ-ment, there are opportunities for investors

E c o n o m i c H i g h l i g h t s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 4/25

3Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

16.5 percent, the Bureau of Labor Statistics (BLS) notedthat total nonfarm payroll employment declined by 125,000during the month, primarily due to the loss of 225,000 Cen-sus jobs. The decline in the unemployment rate was due tothe fact that the labor force decreased by 652,000 (despite

an increase in population), with the majority of these work-ers dropping out of the labor force altogether, as they havesimply given up looking for jobs. However, one encouragingsign of future employment growth is that the second-leadingsource of job growth in June was temporary help in profes-sional and business management and technical/consultingservices, suggesting that the additional need for temporaryworkers will eventually translate to more permanent jobsbeing created (and an increase in commercial propertyspace requirements).

The rst half of 2010 saw payroll growth of approximately100,000 workers a month, but according to Federal ReserveChairman Bernanke, this is “insuf cient to reduce the un -employment rate materially,” and it will take years to recover the 8.5 million jobs lost in 2008 and 2009. A GDP growthrate of 3.0 percent is traditionally considered the minimumrequired to create enough jobs to even keep up with normalpopulation growth.

In ation or De ation?

Federal Reserve Chairman Bernanke’s remarks to Con-gress in July 2010 indicated that the Federal Reserve ex-pects subdued in ation over the next several years, within ation projected to average about 1 percent in 2010 andto remain low during 2011 and 2012. This is in keeping withthe Consumer Price Index (CPI) reading for June 2010, re-

ecting that the index increased 1.1 percent before season -al adjustment over the past 12 months. However, despite a0.2 percent increase in core in ation in June 2010, the CPIdeclined 0.1 percent on a seasonally-adjusted basis. Due tothe weakness in energy and food prices, CPI has remainedmired in de ation territory for the third straight month.

Although there has been considerable criticism of busi-nesses sitting on cash reserves and not investing in hiringnew employees during the recovery, increasing numbers of economists are suggesting that the lack of demand in theeconomy at present does not warrant additional employ-ment. This lack of demand, along with the fact that priceincreases declined further in second quarter 2010, further suggest that the environment for de ation is increasing.

Housing Market Still in Doubt

Although the housing market remains weak, sales of newsingle-family homes and building permits increased as ex-pected in June 2010, as buyers rushed to take advantageof low interest rates and the $8,000 tax credit that expired

June 30, 2010. Sales of new homes increased 23.6 percentover May’s gures to a seasonally-adjusted annual rate of 330,000 homes, while building permits increased by 2.1percent from May to a seasonally-adjusted annual rate of 586,000 permits in June, reported the U.S. Department of Commerce.

According to the National Association of REALTORS®(NAR), however, sales of existing homes slowed in June,falling 5.1 percent from May to a seasonally-adjusted an-nual rate of 5.37 million units, although June’s 2010 sales

gures remain 9.8 percent higher than year-ago sales. As aresult, the total housing inventory rose 2.5 percent in Juneto nearly 4 million existing homes for sale, representing an8.9-month supply, while the median existing home pricewas $183,700. In addition, pending home sales dropped 2.6percent from the previous month.

Unfortunately, the number of foreclosures increased 38percent during second quarter 2010 from year-ago gures,reports RealtyTrac, Inc. At this rate, lenders will take backmore than 1 million homes this year. Mortgage rates remainat record lows, and re nancing activity has increased, butthe jury is still out as to whether low rates are enough todraw buyers in or whether home values will decline further without the sustenance that tax credits have provided. For now, the sector remains on the watch list.

How CCIM Members View the Economy

CCIM members rated the national economy at 4.1 on ascale of 1 to 10, with 10 being high, during second quarter 2010, which was down slightly from the previous quarter,and indicates that survey respondents believe the economyis struggling. However, the East, Midwest, South, and Westregional economies individually were rated the same or higher than the previous quarter, and all were rated higher than the national economy, indicating that CCIM membershave more con dence in their regional economies. The Eastregional economy was the highest-rated economy and theonly economy with a rating higher than 5.0. At 4.3, the Mid-west economy received the lowest rating, while the Westeconomy saw the biggest change from the previous quarter.

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 5/25

4Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

According to the July 28, 2010 Beige Book , commercial andindustrial real estate markets continued to struggle in all 12districts during second quarter, with vacancy rates rangingfrom at to slightly increased and exerting pressure on rents.According to the FOMC, the outlook for commercial and in-dustrial real estate remains uncertain.

Lending Continues to Stabilize

The banking system has improved greatly since the begin-ning of the recession, and according to the FOMC, loss rateson most types of loans seem to be peaking. However, manybanks continue to have a high number of troubled loans ontheir books, and bank lending standards remain tight. Withcredit demand weak and with banks writing down problem

credit, bank loans outstanding have continued to contract,which is particularly dif cult for those small businesses thatdepend on bank credit.

As for the number of troubled loans, the loan delinquencyrate continues to increase. According to Moody’s, the de-linquency rate for commercial mortgage-backed securities(CMBS) reached 7.71 percent, with a 3-month increase of 129 basis points. The hotel sector leads the way in delin-quency rates, with 13.75 percent of loans defaulting, fol-lowed by the multi-family sector at 13.19 percent. The retail,of ce, and industrial sectors are more stable, with loan de -fault rates of 6.18 percent, 5.92 percent, and 5.42 percent,

respectively.

On a regional basis, the South and the West continue tohave the highest number of loan defaults, climbing to 9.63percent and 8.89 percent, respectively. Defaults in the Eastincreased slightly, but the East region continues to be themost stable, with a default rate of 5.92 percent, followed bythe Midwest region with a default rate of 8.12 percent.

Unfortunately, almost every weekend we hear of severalmore banks closed by the Federal Deposit Insurance Cor-poration (FDIC). Just recently, the number of failed nan -cial institutions passed the 100-mark for the year. This time

last year, the number of failed banks numbered 64. There ismore pain to come too, as the number of problem banks onthe FDIC’s list of troubled banks continues to increase, total-ing 775 at the end of rst quarter 2010.

How CCIM Members View Real Estate

Despite the uncertain economic environment and the morethan 30-percent average loss in value that this sector hasendured during the past couple years, commercial real es-tate seems to be the ideal asset class for adding stability

to an investment portfolio, according to CCIM members.As noted in Exhibit 1, commercial real estate maintained itslead over other investment alternatives, earning a rating of 6.1 on a scale of 1 to 10, with 10 being high, during secondquarter 2010. At 5.7, cash earned the second highest rating,while stocks and bonds tied for last place among the invest-ment alternatives.

RERC’s institutional investment survey respondents havenoted that billions of dollars in funds have been raised topurchase commercial real estate. Since banks have imple-mented “extend and pretend” programs to restructure loanson what would eventually be considered troubled assets,fewer distressed properties are available to investors at bar-gain prices, driving prices upward. In addition, top-tier com-

mercial real estate properties have also become increasing-ly attractive, and investors looking to place capital for suchproperties are nding a low supply of such properties, alongwith elevated competition.

As shown in Exhibit 2, when RERC’s institutional investmentsurvey respondents were asked whether to buy, sell, or holdcommercial real estate, the predominant answer in second

0

2

4

6

8

10

0

2

4

6

8

10

HoldSellBuy

2 Q 2 0

1 0

2 Q 2 0

0 9

2 Q 2 0

0 8

2 Q 2 0

0 7

2 Q 2 0

0 6

2 Q 2 0

0 5

2 Q 2 0

0 4

2 Q 2 0

0 3

2 Q 2 0

0 2

2 Q 2 0

0 1

Exhibit 2. RERC Historical Buy, Sell, Hold Recommenda

Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source:RERC Institutional Investment Survey, 2Q 2010.

R a

t i n g

Exhibit 1. CCIM Respondents Rate Investments

2Q 2010 1Q 2010

Commercial Real Estate 6.1 6.0Stocks 4.5 5.1

Bonds 4.5 4.6

Cash 5.7 5.2

Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC/CCIM Investment Trends Quarterly Survey, 2Q 2010.

C o m m e r c i a l R e a l E s t a t e H i g h l i g h t s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 6/25

5Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

quarter 2010 was to hold. This was the rst time in severalquarters that holding property was recommended over buy-ing, and with a rating of 6.8 on a scale of 1 to 10, with 10 be-ing high, this was also a slightly higher hold rating than thatfor the previous quarter. In contrast, the buy rating fell to 6.1

in second quarter from 6.8 in the previous quarter. Althoughinstitutional respondents have shifted their views somewhat,they gave the sell option a rating of 4.0, which is still consid-ered a generally weak option.

In looking more closely at the individual property sectors,CCIM members increased their investment conditions rat-ings for all property types during second quarter 2010. Asdemonstrated in Exhibit 3, the apartment sector continuedto receive the highest investment conditions rating, and witha rating of 5.9 on a scale of 1 to 10, with 10 being high, far out-distanced the ratings of the other property sectors. Theindustrial sector received the second-highest rating at 4.4,

while the retail and hotel sectors followed closely, each witha rating of 4.2. At 4.0, the of ce sector received the low -est investment conditions rating among the property typesRERC surveyed.

The return versus risk rating for commercial real estate over-all increased to 5.4 on a scale of 1 to 10, with 10 being high,as reported for second quarter 2010 and shown in Exhibit 4.Although the return for investment in commercial real estateslightly outweighs the risk for this asset class, investors re-main cautious.

The apartment sector retained the highest return versus risk

rating, and as noted in Exhibit 4, this was the only propertytype with a return versus risk rating above 5.0 on a scale of 1 to 10, with 10 being high, during second quarter 2010. Theof ce, industrial, retail, and hotel sectors were rated lower than 5.0, indicating that the risk for these property sectors isgreater than the return. At 4.8, the industrial sector earnedthe second highest rating, followed closely by the retail sec-tor, which saw the biggest rating increase from the previousquarter. The of ce and hotel sectors received the lowest rat -ings, at 4.4 each, indicating that while the ratings are stilllow, CCIM members are beginning to see more potential for returns from these sectors for investors who can take therisk.

CCIM members lowered their rating for value versus pricefor commercial real estate overall to 5.2 on a scale of 1 to10, with 10 being high, during second quarter 2010, alsoshown in Exhibit 4. Although the rating has declined, CCIMmembers believe that the value of commercial real estate isslightly greater than the price of this asset class.

The value versus price rating for the apartment sector de-clined to 5.2 on a scale of 1 to 10, with 10 being high, dur-ing second quarter 2010, with the sector barely retaining its

highest ranking. The industrial sector was the only propertytype where the value versus price rating increased duringthe quarter, earning it the second highest rating of 5.1. Theratings for the of ce and retail sectors decreased to 4.7 and4.5, respectively. The value versus price ratings for the hotelsector did not vary from rst quarter 2010 to second quarter.CCIM members believe that price is generally greater thanthe value of of ce, retail, and hotel properties, which indi

cates that con dence remains low.

Transaction volume increased for all property types in sec-ond quarter 2010 on a 12-month trailing basis. Volume in-creased the most for the of ce sector, with a nearly 30-per cent increase over rst quarter volume, while the propertytype in which transaction volume increased the least dur-ing second quarter was the industrial sector. The 12-monthtrailing size-weighted average price per square foot/unitincreased in the of ce, retail, apartment, and hotel sectorsduring second quarter, but declined slightly in the industrial

Exhibit 4. Historical Return/Risk and Value/Price Rati2Q 2010 1Q 2010 4Q 2009 3Q 2009 2

Return vs. RiskOverall 5.4 5.1 4.8 5.0 4.7

Office 4.4 4.1 4.1 4.2 4.0Industrial 4.8 4.7 4.7 4.9 5.0Retail 4.7 4.1 3.9 4.0 3.6Apartment 6.2 6.1 5.8 5.8 5.2Hotel 4.4 3.9 3.9 3.8 3.4

Value vs. PriceOverall 5.2 5.5 4.7 4.8 4.9

Office 4.7 5.0 4.3 4.4 4.5

Industrial 5.1 5.0 4.7 5.0 4.9

Retail 4.5 4.9 4.2 4.4 4.3

Apartment 5.2 5.6 4.9 5.3 4.8Hotel 4.7 4.7 4.0 4.1 3.9Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC/CCIM Investment Trends Quarterly Survey, 2Q 2010.

Exhibit 3. Real Estate Investment Conditions Ratings2Q

20101Q

20104Q

20093Q

20092Q

2009Office 4.0 3.8 3.8 3.8 3.5

Industrial 4.4 4.2 4.1 4.3 4.3Retail 4.2 3.7 3.8 3.8 3.4Apartment 5.9 5.5 5.4 5.5 5.1Hotel 4.2 3.8 3.8 3.6 3.4Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC/CCIM Investment Trends Quarterly Survey, 2Q 2010.

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 7/25

6Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

sector. In addition, the 12-month trailing weightedaverage capitalization rates declined for the of ce,apartment, and hotel sectors, but increased for theindustrial and retail sectors.

The Dow Jones Industrial Average (DJIA) declineddrastically for the year, falling 5.0 percent to 9,687by June 30, 2010, the lowest it had been since Au-gust 2009. As shown in Exhibit 5, the other stockmarket indices also showed losses for the year.However, the major U.S. stock indices saw signi -cantly higher readings in July 2010, generally re-porting their biggest monthly gains in a year, as themajority of corporate earnings surpassed expecta-tions. These stock market increases came in spiteof the avalanche of weak economic data reported inJuly, which showed the recovery is slowing.

With such volatility in the stock market, the stabilitythat commercial real estate offers investors is evenmore valuable, and the second quarter 2010 returnsreported by the National Association of Real EstateInvestment Trusts (NAREIT) and the National Coun-cil of Real Estate Investment Fiduciaries (NCRIEF)in Exhibit 5, look attractive in comparison.

Exhibit 5. What Do the Financial Markets Tell Us?

Compounded Annual Rates of Return as of 6/30/2010

Market Indices YTD 1-Year 3-Year 5-Year10-Year 15-YearConsumer Price Index 1 -0.28% 1.13% 1.53% 2.30% 2.34% 2.3

10-Year Treasury Bond2 3.60% 3.43% 3.62% 4.04% 4.31% 4.8

Dow Jones Industrial Average -5.00% 18.94% -7.39% 1.66% 1.68%

NASDAQ Composite3 -7.05% 14.94% -6.77% 0.50% -6.12% 5.5

NYSE Composite3 -9.96% 9.56% -13.14% -2.16% -0.49% 5.0

S&P 500 -6.65% 14.43% -9.81% -0.79% -1.59% 6

NCREIF Index 4.10% -1.48% -4.70% 3.79% 7.16%

NAREIT Index (Equity REITS) 5.56% 53.90% -9.00% 0.20% 9.86%

1Based on the published data from the Bureau of Labor Statistics (Seasonally Adjusted).2Based on Average End of Day T-Bond Rates.3Based on Price Index, and does not include the dividend yield.Sources: BLS, Federal Reserve Board, S&P, Dow Jones, NCREIF, NAREIT, compiled by RE

We are at an in ection point in the current real estate cycle,and while there are strong headwinds facing the economyand the commercial real estate market, we are starting tosee some tailwinds with respect to increases in volume andpricing. Given this environment, RERC concludes:

• GDP is slowing, and while there were growth contribu -tions from business and government in second quarter 2010, growth from consumers, which comprises approxi-mately 70 percent of the economy, is lacking. Until wesee consumer spending strengthen, growth will be mini-mal.

• The unemployment rate is expected to remain at or near current levels throughout the remainder of the year. Pri-vate businesses seem to be in no hurry to start hiringuntil demand for their goods and services increases.

• In light of the slowing in the economy, interest rates areexpected to remain at current low rates throughout therest of the year.

• Investors wary of the volatility driving the stock and bondmarkets, are turning toward the stability of commercialreal estate and reliable cash ows to help round out their portfolios.

• Bank lending remains tight, but much private capital islooking for distressed property at bargain prices, or for high-quality fully-leased properties in top-tier markets atnearly any price.

• The vacancy rate for the apartment sector is startingto decline. Vacancy for the of ce and retail sectors isexpected to remain at current levels or even increase

slightly throughout the rest of the year.

• Transaction volume and pricing on a 12-month trailingbasis are starting to increase, particularly in the of cesector.

S u m m a r y

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 8/25

7Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Snapshot of Real Estate Market Performance – 2Q 2010

Performance Indicator Recent Data Impact on Commercial Real Estate

Vacancy Rates

Office: 17.4%Industrial: 10.0%Retail: 10.9%Apartment: 7.8%Hotel: 65% (occupancy)

According to Reis, Inc., vacancy rates for the office and retail prsectors increased during second quarter 2010, while vacancy foapartment sector decreased. Vacancy in the industrial property scontinued to decline from the previous quarter, according to the CGroup. Smith Travel Research reported that hotel occupancy incr

during second quarter.

Rental Rates(RERC’s surveyed rentgrowth expectations)

Office: 1.3% to 1.8%Industrial: 0.9% to 1.4%Retail: 0.9% to 1.3%Apartment: 2.2%Hotel: 1.7%

RERC’s second quarter 2010 rental rate expectations were slightlyer for the office, retail, apartment, and hotel sectors, when compa those for first quarter 2010.

Real Estate Returns

RERC Required Returns:Office: 8.9% to 9.8%Industrial: 9.4% to 10.1%Retail: 9.1% to 9.6%

Apartment: 8.6%Hotel: 11.4%

NCREIF Realized Returns:Office: -4.6% to 2.4%Industrial: -4.1% to 2.8%Retail: -0.8% to -0.5%

Apartment: -0.1%Hotel: -5.8%

RERC’s second quarter 2010 required returns for the retail sectorlower than first quarter returns, while those for the office, induapartment, and hotel sectors were higher. NCREIF’s realized rcontinued to improve for all property sectors during second quartepositive returns being seen in the office and industrial sectors.

Capitalization Rates

RERC Realized Cap Rates:Office: 7.2%Industrial: 8.5%Retail: 8.6%Apartment: 6.8%Hotel: 8.7%

NCREIF Implied Cap Rates:Office: 6.6% to 7.1%Industrial: 7.3% to 7.6%Retail: 6.9% to 7.7%Apartment: 5.8%Hotel: 5.6%

RERC’s second quarter 2010 realized cap rates were lower thanquarter rates for the office, apartment, and hotel sectors, and were hfor the industrial and retail sectors. NCREIF’s implied capitalizatifor second quarter were higher in each sector compared to the prevquarter.

0%

2%

4%

6%

8%

10%

12%

0%

2%

4%

6%

8%

10%

12%

UnemploymentGoing-In Cap Rate

2 Q 2 0 1 0

2 Q 2 0 0 9

2 Q 2 0 0 8

2 Q 2 0 0 7

2 Q 2 0 0 6

2 Q 2 0 0 5

2 Q 2 0 0 4

2 Q 2 0 0 3

2 Q 2 0 0 2

2 Q 2 0 0 1

2 Q 2 0 0 0

2 Q 1 9 9 9

2 Q 1 9 9 8

2 Q 1 9 9 7

2 Q 1 9 9 6

2 Q 1 9 9 5

2 Q 1 9 9 4

2 Q 1 9 9 3

2 Q 1 9 9 2

2 Q 1 9 9 1

2 Q 1 9 9 0

2 Q 1 9 8 9

2 Q 1 9 8 8

2 Q 1 9 8 7

2 Q 1 9 8 6

2 Q 1 9 8 5

2 Q 1 9 8 4

2 Q 1 9 8 3

2 Q 1 9 8 2

2 Q 1 9 8 1

2 Q 1 9 8 0

Sources: RERC, BLS, NBER, 2Q 2010.

Going-In Cap Rates vs. Unemployment

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 9/25

8Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

National Transaction Breakdown12-Month Trailing Averages (07/01/09 - 06/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $1,301 $2,414 $2,447 $1,062 $65Size Weighted Avg. ($ per sf/unit) $84 $48 $83 $48,731 $26,318Price Weighted Avg. ($ per sf/unit) $120 $76 $126 $70,474 $35,219Median ($ per sf/unit) $89 $57 $86 $51,250 $23,636

$2 - $5 Million

Volume (Mil) $1,694 $2,607 $2,695 $2,032 $314Size Weighted Avg. ($ per sf/unit) $113 $53 $137 $56,106 $33,619Price Weighted Avg. ($ per sf/unit) $191 $86 $238 $106,339 $43,796Median ($ per sf/unit) $157 $73 $198 $86,275 $33,712

> $5 MillionVolume (Mil) $21,777 $6,442 $15,521 $16,271 $4,112Size Weighted Avg. ($ per sf/unit) $198 $53 $159 $98,100 $114,411Price Weighted Avg. ($ per sf/unit) $345 $99 $238 $202,993 $174,495Median ($ per sf/unit) $180 $71 $158 $89,286 $93,941

All TransactionsVolume (Mil) $24,771 $11,462 $20,663 $19,365 $4,492Size Weighted Avg. ($ per sf/unit) $177 $52 $141 $86,501 $94,027Price Weighted Avg. ($ per sf/unit) $323 $91 $225 $185,584 $163,327Median ($ per sf/unit) $113 $61 $112 $68,500 $58,629

Capitalization Rates (All Transactions)Range (%) 4.8 - 12.9 4.2 - 13.1 4.2 - 13.3 4.0 - 11.1 6.5 - 13.1Weighted Avg. (%) 7.2 8.5 8.6 6.8 8.7Median (%) 8.2 8.8 7.7 7.0 9.0Source: RERC.

N a t i o n a l M a r k e t A n a l y s i s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 10/25

9Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

National Transaction BreakdownCurrent Quarter Rates (04/01/10 - 6/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $329 $581 $653 $292 $25Size Weighted Avg. ($ per sf/unit) $85 $46 $78 $46,491 $32,764Price Weighted Avg. ($ per sf/unit) $125 $73 $122 $67,164 $43,946Median ($ per sf/unit) $88 $56 $84 $51,250 $31,933

$2 - $5 Million

Volume (Mil) $440 $635 $711 $597 $91Size Weighted Avg. ($ per sf/unit) $110 $57 $132 $54,773 $34,690Price Weighted Avg. ($ per sf/unit) $185 $88 $238 $99,463 $42,190Median ($ per sf/unit) $149 $72 $202 $76,371 $34,091

> $5 MillionVolume (Mil) $8,450 $1,782 $3,536 $3,792 $2,078Size Weighted Avg. ($ per sf/unit) $244 $53 $166 $111,702 $134,839Price Weighted Avg. ($ per sf/unit) $400 $117 $272 $188,265 $176,151Median ($ per sf/unit) $185 $79 $168 $110,066 $109,172

All TransactionsVolume (Mil) $9,220 $2,998 $4,900 $4,681 $2,194Size Weighted Avg. ($ per sf/unit) $217 $52 $140 $91,554 $116,740Price Weighted Avg. ($ per sf/unit) $380 $103 $247 $169,384 $169,096Median ($ per sf/unit) $114 $61 $107 $69,962 $76,920

Capitalization Rates (All Transactions)Range (%) 4.8 - 12.9 5.8 - 12.2 6.3 - 12.6 4.4 - 9.9 –Weighted Avg. (%) 6.6 8.1 8.3 6.3 –Median (%) 7.9 8.6 7.8 6.6 –Source: RERC.

N a t i o n a l M a r k e t A n a l y s i s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 11/25

10Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

w Many respondents to the RERC/CCIM Investment TrendsQuarterly survey stated that of ce properties are the mostavailable property type now because of distressed salesand foreclosures, although prices are a little above marketvalue. In addition, a few respondents reported that inroadsare being made into reducing of ce inventory.

w Twelve-month trailing of ce sector volume started to increase in 2010, after declining since third quarter 2007. Inaddition, the of ce sector saw its rst increase in 12-monthtrailing pricing during second quarter 2010. Capitalizationrates also reversed direction this quarter.

w Twelve-month trailing volume increased by nearly 30 per-

cent over rst quarter volume, while the size-weighted average price increased by approximately 15 percent. Theweighted average capitalization rate decreased to 7.2 per-cent, while the median capitalization rate remained stableat 8.2 percent.

w According to Reis, Inc, second quarter 2010 of ce vacancy rose to 17.4 percent, a level unseen since 1993.This is the 10th consecutive quarterly increase in vacancyfor the of ce sector. In addition, effective rent declines exceeded asking rent declines, with second quarter askingrents down 0.2 percent while effective rents were down 0.8

percent.

6%

7%

8%

9%

6%

7%

8%

9%NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$0

$100

$200

$300

$400

$500

$0

$100

$200

$300

$400

$500NationalWest

Midwest

SouthEast

2Q101Q104Q093Q092Q09

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

$25

$75

$125

$175

$225

$275

$25

$75

$125

$175

$225

$275NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

N a t i o n a l O f f i c e Pr o p e r t y S e c t o r

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 12/25

11Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

w Respondents to the RERC/CCIM Investment Trends Quar-terly survey commented that industrial properties werereasonably priced, and because of distressed sales andforeclosures, the supply of industrial properties was quiteample. The national industrial vacancy rate declined dur-ing second quarter 2010, the rst decrease in more than 2years according to CoStar Group.

w It appears that volume in the industrial sector has leveledoff after slight increases during the rst part of 2010. The12-month trailing size-weighted average price per squarefoot of industrial property has been declining for the past

ve quarters, but began to show signs of stabilization in2010. The capitalization rates for this property sector have

been steadily increasing since rst quarter 2009.

w RERC’s analysis of 12-month trailing and current quar-ter industrial property transactions showed no signi cantchange in either volume or pricing during second quarter 2010. The 12-month trailing weighted average and me-dian capitalization rates increased to 8.5 percent and 8.8percent, respectively.

w According to CoStar Group, the national industrial vacan-cy rate declined by 10 basis points to 10.0 percent, dur-ing second quarter 2010. Rental rates continued to fall,

though at a slower pace than during previous quarters.The industrial warehouse sector continues to struggle, asrental rates are not expected to increase until 2011. Sec-ond quarter 2010 net absorption was reported to be 13million square feet.

7.0%

7.5%

8.0%

8.5%

9.0%

7.0%

7.5%

8.0%

8.5%

9.0%

NationalWest

Midwest

SouthEast

2Q101Q104Q093Q092Q09

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$25

$50

$75

$100

$125

$150

$25

$50

$75

$100

$125

$150NationalWest

MidwestSouthEast

2Q101Q104Q093Q092Q09

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

$0

$25

$50

$75

$100

$0

$25

$50

$75

$100NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

N a t i o n a l I n d u s t r i a l P ro p e r t y S e c t o r

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 13/25

12Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

6%

7%

8%

9%

10%

6%

7%

8%

9%

10%NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$100

$150

$200

$250

$300

$100

$150

$200

$250

$300NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

w According to respondents to the RERC/CCIM Investment Trends Quarterly survey, the retail sector continues to facedif culties. The effects of the poor economy and slow jobgrowth are negatively impacting the retail sector, as evi-denced by the increasing vacancy rate. As such, respon-dents commented that retail properties are abundantlyavailable.

w After showing signs of stabilization since fourth quarter 2009, 12-month trailing volume for the retail sector beganto increase in second quarter 2010. The 12-month trailingsize-weighted average price for the sector has also beenincreasing since fourth quarter 2009, while the capitaliza-tion rates have been increasing since third quarter 2009.

w

The 12-month trailing transaction volume increased morethan 10 percent for the retail property sector during sec-ond quarter 2010. The 12-month trailing size-weighted av-erage price per square foot also increased during secondquarter, while the 12-month trailing weighted average andmedian capitalization rates increased to 8.6 percent and7.7 percent, respectively.

w According to Reis, Inc., the retail vacancy rate increasedby 10 basis points during second quarter 2010, althoughthis increase is the smallest since the beginning of 2008.In addition, the negative net absorption of 2.2 millionsquare feet for the quarter is modest in comparison to

fourth quarter 2009. Completions have nearly stopped at355,000 square feet, and are at the lowest quarterly levelsince Reis began reporting this data 10 years ago. Askingand effective rents are comparable to rst quarter 2010results, and the pace of decline has continued to slow.

$50

$75

$100

$125

$150

$175

$200

$50

$75

$100

$125

$150

$175

$200

NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

N a t i o n a l R e t a i l P r o p e r t y S e c t o r

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 14/25

13Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

w Many respondents to the RERC/CCIM Investment TrendsQuarterly survey said that the apartment sector remains asafe investment with little risk, and that it has held up rela-tively well during the downturn. Apartments are increasingin demand and value due to low vacancy rates, few newhousing starts, and an illiquid market.

w According to RERC’s transaction analysis, the apartmentsector has been showing steady improvement since fourthquarter 2009. Twelve-month trailing volume and price per unit have been steadily increasing for the past 3 quarters.

w The weighted-average capitalization rate has been de-creasing slightly during the rst half of 2010, with the sec

ond quarter 2010 rate decreasing by 10 basis points to6.8 percent. The median capitalization rate remained un-changed at 7.0 percent during second quarter.

w The vacancy rate for the apartment sector declined 20 ba-sis points during second quarter 2010, bringing vacancy to7.8 percent, according to Reis, Inc. This is the rst time in 2years that the vacancy rate has been this low. In addition,net absorption increased by more than 46,000 units. Ask-ing and effective rents grew at an accelerated rate duringsecond quarter, increasing by 0.4 percent and 0.7 percent,respectively.

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Price-Weighted Average PPU(12-Month Trailing Average)

$25,000

$50,000

$75,000

$100,000

$125,000

$25,000

$50,000

$75,000

$100,000

$125,000NationalWest

MidwestSouth

East

2Q101Q104Q093Q092Q09

RERC Size-Weighted Average PPU(12-Month Trailing Average)

N a t i o n a l A p a r t m e n t P ro p e r t y S e c t o r

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 15/25

14Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

w Many respondents to the RERC/CCIM Investment TrendsQuarterly survey reported that the hotel sector continuedto struggle due to the weak economy and a continued lackof jobs. However, a few respondents noted that the hotelsector is beginning to see some strengthening due to theturnaround in occupancy and because the hotel sector isundercapitalized.

w RERC’s transaction analysis shows the hotel sector begana slow turn-around during the rst half of 2010. Twelve-month trailing volume and the size-weighted price per unitboth increased for the past 2 quarters. Transaction volumehit bottom in fourth quarter 2009, after peaking during fourthquarter 2007.

w Transaction volume for the hotel sector increased by morethan 25 percent on a 12-month trailing basis during secondquarter 2010. The 12-month trailing size-weighted priceper unit increased from the previous quarter. The 12-monthtrailing weighted average and median capitalization ratesdecreased 50 basis points each to 8.7 percent and 9.0 per-cent, respectively.

w According to Smith Travel Research, occupancy in the ho-tel sector increased by 6.9 percent to 65.0 percent in June2010. The average daily rate (ADR) increased 1.0 percent

to $98.33, and the revenue per available room (RevPAR)increased by 8.0 percent to $63.87.

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

National

East

2Q101Q104Q093Q092Q09

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Price-Weighted Average PPU(12-Month Trailing Average)

$25,000

$50,000

$75,000

$100,000

$125,000

$25,000

$50,000

$75,000

$100,000

$125,000NationalWest

Midwest

South

East

2Q101Q104Q093Q092Q09

RERC Size-Weighted Average PPU(12-Month Trailing Average)

N a t i o n a l H o t e l Pr o p e r t y S e c t o r

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 16/25

15Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

East Transaction Breakdown12-Month Trailing Averages (07/01/09 - 06/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $276 $598 $651 $178 $8Size Weighted Avg. ($ per sf/unit) $76 $46 $84 $47,175 $25,236

Price Weighted Avg. ($ per sf/unit) $112 $76 $122 $63,179 $30,248Median ($ per sf/unit) $77 $53 $85 $45,833 $28,750

$2 - $5 MillionVolume (Mil) $420 $663 $791 $618 $61Size Weighted Avg. ($ per sf/unit) $123 $50 $135 $71,298 $30,158

Price Weighted Avg. ($ per sf/unit) $206 $81 $250 $101,651 $34,600Median ($ per sf/unit) $157 $67 $206 $78,667 $29,828

> $5 Million

Volume (Mil) $10,530 $1,817 $4,939 $6,491 $1,318Size Weighted Avg. ($ per sf/unit) $250 $55 $162 $134,118 $122,114

Price Weighted Avg. ($ per sf/unit) $422 $96 $259 $237,815 $184,802Median ($ per sf/unit) $224 $66 $158 $118,497 $92,444

All TransactionsVolume (Mil) $11,226 $3,077 $6,380 $7,286 $1,387Size Weighted Avg. ($ per sf/unit) $228 $52 $145 $119,790 $105,615

Price Weighted Avg. ($ per sf/unit) $406 $89 $244 $222,016 $177,314Median ($ per sf/unit) $118 $56 $114 $80,000 $70,862

Capitalization Rates (All Transactions)Range (%) 4.8 - 10.5 5.8 - 12.3 4.2 - 10.0 4.5 - 9.3 6.5 - 9.0Weighted Avg. (%) 7.0 8.3 7.9 6.5 8.0Median (%) 8.0 8.8 7.5 7.0 7.4Source: RERC.

E a s t R e g i o n Tr a n s a c t i o n B r e a k d o w n

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 17/25

16Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

South Transaction Breakdown12-Month Trailing Averages (07/01/09 - 06/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $354 $520 $734 $181 $17Size Weighted Avg. ($ per sf/unit) $84 $41 $79 $35,359 $28,898

Price Weighted Avg. ($ per sf/unit) $112 $59 $119 $50,227 $36,923Median ($ per sf/unit) $87 $47 $79 $39,063 $25,818

$2 - $5 MillionVolume (Mil) $315 $401 $698 $308 $89Size Weighted Avg. ($ per sf/unit) $97 $37 $122 $30,335 $30,640

Price Weighted Avg. ($ per sf/unit) $152 $56 $203 $48,294 $41,481Median ($ per sf/unit) $118 $48 $171 $31,852 $28,846

> $5 Million

Volume (Mil) $2,603 $930 $4,816 $4,188 $1,179Size Weighted Avg. ($ per sf/unit) $128 $51 $141 $65,882 $93,982

Price Weighted Avg. ($ per sf/unit) $192 $85 $212 $137,717 $157,276Median ($ per sf/unit) $145 $58 $144 $59,028 $89,669

All TransactionsVolume (Mil) $3,272 $1,850 $6,247 $4,676 $1,285Size Weighted Avg. ($ per sf/unit) $118 $44 $127 $59,324 $80,072

Price Weighted Avg. ($ per sf/unit) $179 $72 $200 $128,446 $147,623Median ($ per sf/unit) $100 $49 $99 $45,603 $47,947

Capitalization Rates (All Transactions)Range (%) 6.9 - 10.4 7.0 - 10.7 5.8 - 10.8 5.6 - 10.6 –Weighted Avg. (%) 8.1 8.8 8.8 7.4 –Median (%) 8.5 9.0 8.0 7.6 –Source: RERC.

S o u t h R e g i o n Tr a n s a c t i o n B r e a k d o w n

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 18/25

17Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Midwest Transaction Breakdown12-Month Trailing Averages (07/01/09 - 06/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $208 $356 $361 $119 $12Size Weighted Avg. ($ per sf/unit) $61 $30 $63 $34,071 $18,125

Price Weighted Avg. ($ per sf/unit) $87 $45 $101 $41,836 $21,790Median ($ per sf/unit) $65 $37 $63 $32,946 $14,024

$2 - $5 MillionVolume (Mil) $167 $366 $263 $183 $37Size Weighted Avg. ($ per sf/unit) $64 $34 $113 $27,274 $25,889

Price Weighted Avg. ($ per sf/unit) $102 $54 $217 $43,833 $32,167Median ($ per sf/unit) $84 $42 $168 $33,244 $23,869

> $5 Million

Volume (Mil) $2,150 $736 $1,412 $787 $515Size Weighted Avg. ($ per sf/unit) $129 $33 $148 $67,385 $107,826

Price Weighted Avg. ($ per sf/unit) $257 $53 $211 $104,267 $135,532Median ($ per sf/unit) $118 $41 $154 $57,915 $102,409

All TransactionsVolume (Mil) $2,526 $1,458 $2,036 $1,090 $564Size Weighted Avg. ($ per sf/unit) $111 $32 $116 $49,753 $82,260

Price Weighted Avg. ($ per sf/unit) $232 $51 $192 $87,267 $126,404Median ($ per sf/unit) $73 $38 $79 $36,066 $35,317

Capitalization Rates (All Transactions)Range (%) 7.0 - 10.0 6.8 - 11.0 5.9 - 10.5 6.0 - 10.1 –Weighted Avg. (%) 7.7 8.9 8.6 7.3 –Median (%) 8.6 8.9 8.0 8.0 –Source: RERC.

M i d w e s t R e g i o n Tr a n s a c t i o n B r e a k d o w n

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 19/25

18Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

West Transaction Breakdown12-Month Trailing Averages (07/01/09 - 06/30/10)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $463 $939 $702 $584 $28Size Weighted Avg. ($ per sf/unit) $111 $77 $107 $62,073 $31,078

Price Weighted Avg. ($ per sf/unit) $146 $97 $151 $84,807 $41,455Median ($ per sf/unit) $117 $85 $113 $67,673 $35,673

$2 - $5 MillionVolume (Mil) $787 $1,174 $943 $923 $128Size Weighted Avg. ($ per sf/unit) $141 $82 $164 $86,430 $42,444

Price Weighted Avg. ($ per sf/unit) $218 $109 $259 $141,257 $53,104Median ($ per sf/unit) $199 $96 $209 $125,000 $42,593

> $5 Million

Volume (Mil) $6,476 $2,953 $4,355 $4,806 $1,100Size Weighted Avg. ($ per sf/unit) $212 $63 $184 $113,816 $140,544

Price Weighted Avg. ($ per sf/unit) $313 $116 $252 $229,012 $198,841Median ($ per sf/unit) $192 $85 $191 $106,675 $127,932

All TransactionsVolume (Mil) $7,727 $5,067 $6,000 $6,313 $1,256Size Weighted Avg. ($ per sf/unit) $192 $69 $167 $101,308 $107,017

Price Weighted Avg. ($ per sf/unit) $294 $111 $242 $202,837 $180,523Median ($ per sf/unit) $150 $87 $146 $87,500 $65,942

Capitalization Rates (All Transactions)Range (%) 6.0 - 12.9 4.2 - 13.1 6.0 - 13.3 4.0 - 11.1 –Weighted Avg. (%) 7.6 8.5 9.2 6.6 –Median (%) 8.1 8.6 7.5 6.7 –Source: RERC.

We s t R e g i o n Tr a n s a c t i o n B r e a k d o w n

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 20/25

19Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

-7

-5

-3

-1

1

3

5

7

9

-7

-5

-3

-1

1

3

5

7

9

2 Q 2 0

1 0

4 Q 2 0

0 9

2 Q 2 0

0 9

4 Q 2 0

0 8

2 Q 2 0

0 8

4 Q 2 0

0 7

2 Q 2 0

0 7

4 Q 2 0

0 6

2 Q 2 0

0 6

4 Q 2 0

0 5

2 Q 2 0

0 5

4 Q 2 0

0 4

2 Q 2 0

0 4

4 Q 2 0

0 3

2 Q 2 0

0 3

4 Q 2 0

0 2

2 Q 2 0

0 2

4 Q 2 0

0 1

2 Q 2 0

0 1

4 Q 2 0

0 0

2 Q 2 0

0 0

P e r c e n

t C h a n g e

Q u a r t e r

A g o

According to the Bureau of Economic Analysis, real gross domestic product (GDP) growthwas revised upward to 3.7% in first quarter 2010 and increased 2.4% on an annualized basisin second quarter 2010. This was the fourth consecutive quarterly increase. Growth slowed insecond quarter due to stronger imports and lower inventories, but was buoyed by homebuild-ing, business investment, and spending by federal, state, and local governments.

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

J u n - 1 0

M a y - 1

0 A p

r - 1 0

M a r - 1

0 F e b

- 1 0 J a n

- 1 0 D e

c - 0 9

N o v - 0

9 O c

t - 0 9

S e p - 0

9 A u

g - 0 9 J u l

- 0 9

P e r c e n

t C h a n g e

M o n

t h A g o

The Consumer Price Index (CPI) decreased 0.1% to 218.0 in June 2010, the third consecutivemonth it has fallen. However, compared to a year ago, the CPI was up 1.1%. Deflation is a con-cern due to the decline in gas prices and in food prices remaining flat. Consumer spending hasdropped, and the rest of the year looks challenging. One positive sign is the shelter index, whichis finally showing strength. Though deflation is unlikely, the risk will continue until employmentstrengthens. Core inflation is expected to increase again in 2011.

Source: Bureau of Labor Statistics.

P e r c e n

t

2

4

6

8

10

12

2

4

6

8

10

12

J u n -

1 0

F e b -

1 0

O c t - 0

9

J u n -

0 9

F e b -

0 9

O c t - 0

8

J u n -

0 8

F e b -

0 8

O c t - 0

7

J u n -

0 7

F e b -

0 7

O c t - 0

6

J u n -

0 6

F e b -

0 6

O c t - 0

5

J u n -

0 5

F e b -

0 5

O c t - 0

4

J u n -

0 4

F e b -

0 4

O c t - 0

3

J u n -

0 3

F e b -

0 3

O c t

- 0 2

J u n -

0 2

F e b -

0 2

O c t

- 0 1

J u n -

0 1

F e b -

0 1

O c t

- 0 0

J u n -

0 0

F e b -

0 0

The unemployment rate increased to 9.9% in April 2010 before improving to 9.5% in June,due primarily to the contraction in the labor force of 652,000 workers. Despite this decline, the

employment report was weaker than expected, with payroll gains tepid.

Source: Bureau of Labor Statistics.

Source: Bureau of Economic Analysis.

P e r c e n t

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

Discount Rate

Fed Funds Rate

J u n - 1 0

D e c - 0

9 A u

g - 0 9 M a

r - 0 9

A u g - 0 8

J a n - 0 8

A u g - 0 7

J a n - 0 7

A u g - 0 6

J a n - 0 6

A u g - 0 5

F e b - 0 5

A u g - 0 4

J a n - 0 4

A u g - 0 3

J a n - 0 3

A u g - 0 2

J a n - 0 2

S e p - 0 1

A p r - 0

1 N o

v - 0 0

M a y - 0

0

In the June 2010 meeting, the Federal Open Market Committee (FOMC) s tated would continue “at a moderate pace.” The federal funds rate remained in the 0range and the discount rate remained at 0.75%. However, there is greater concrecovery, as deflation concerns increased during second quarter 2010. The FOM to keep the federal funds rate at its current range into the spring of 2011.

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

J u n - 1 0

A p r - 1 0

F e b -

1 0

D e c - 0

9

O c t - 0

9

A u g - 0 9

J u n -

0 9

A p r - 0

9

F e b -

0 9

D e c - 0

8

O c t - 0

8

A u g - 0 8

J u n -

0 8

A p r - 0

8

F e b -

0 8

D e c - 0

7

O c t - 0

7

A u g - 0 7

Y e a r

T o

Y e a r

P e r c e n

t C h a n g e

Retail sales fell for the second consecutive month in June 2010, decreasing 0.cates that the momentum for spending growth has slowed, although retail sales higher than a year ago. Consumers remain cautious, and it is expected that wgrowth does resume, it will be modest.

Source: Census Bureau.

60

65

70

75

80

85

60

65

70

75

80

85

J u n -

1 0

F e b -

1 0

O c t - 0

9

J u n -

0 9

F e b -

0 9

O c t - 0

8

J u n -

0 8

F e b -

0 8

O c t - 0

7

J u n -

0 7

F e b -

0 7

O c t - 0

6

J u n -

0 6

F e b -

0 6

O c t - 0

5

J u n -

0 5

F e b -

0 5

O c t - 0

4

J u n -

0 4

F e b -

0 4

O c t - 0

3

J u n -

0 3

F e b -

0 3

O c t - 0

2

J u n -

0 2

F e b -

0 2

O c t - 0

1

J u n -

0 1

F e b -

0 1

O c t - 0

0

J u n -

0 0

F e b -

0 0

P e r c e n

t

Manufacturing utilization increased to 71.6% in June 2010, and over the past by more than 6%, the largest annual rise in more than a quarter-century. Howe

activity stalled in June, and there are concerns about the extent of the slowing. Tis that although consumer spending has weakened, spending by businesses hasAlso, auto production is expected to rebound in July.

Source: Federal Reserve.

Source: Federal Reserve.

Unemployment

GDP

Consumer Price Index

Manufacturing Utilization

FOMC Policy Decisions

Retail Sales

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 21/25

20Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

M i l l i o n s

4.0

5.0

6.0

7.0

8.0

4.0

5.0

6.0

7.0

8.0

J u n - 1 0

F e b -

1 0

O c t - 0 9

J u n - 0 9

F e b -

0 9

O c t - 0 8

J u n - 0 8

F e b -

0 8

O c t - 0 7

J u n - 0 7

F e b -

0 7

O c t - 0 6

J u n - 0 6

F e b -

0 6

O c t - 0 5

J u n - 0 5

F e b -

0 5

O c t - 0 4

J u n - 0 4

F e b -

0 4

O c t - 0 3

J u n - 0 3

F e b -

0 3

O c t - 0 2

J u n - 0 2

F e b -

0 2

O c t - 0 1

J u n - 0 1

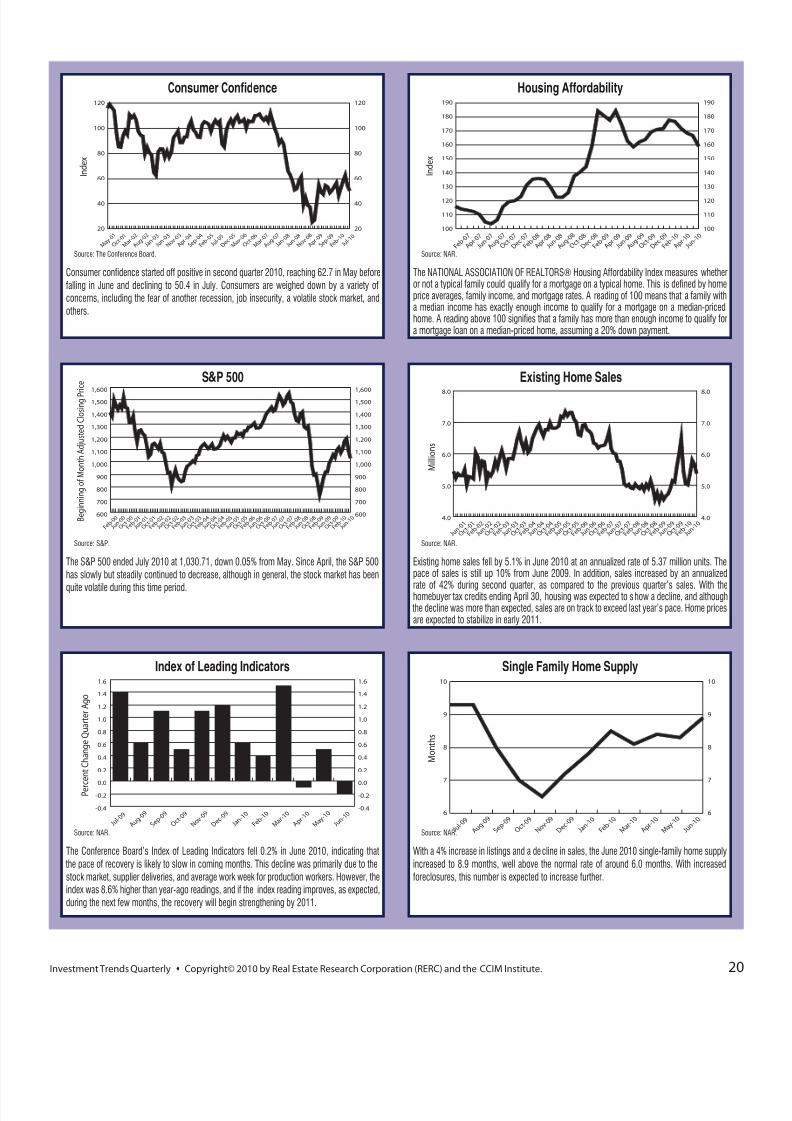

Existing home sales fell by 5.1% in June 2010 at an annualized rate of 5.37 mipace of sales is still up 10% from June 2009. In addition, sales increased by

rate of 42% during second quarter, as compared to the previous quarter’s sahomebuyer tax credits ending April 30, housing was expected to show a declin the decline was more than expected, sales are on track to exceed last year’s paceare expected to stabilize in early 2011.

Source: NAR.

100

110

120

130

140

150

160

170

180

190

100

110

120

130

140

150

160

170

180

190

J u n -

1 0

A p r - 1 0

F e b -

1 0

D e c - 0 9

O c t - 0 9

A u g - 0 9

J u n -

0 9

A p r - 0 9

F e b -

0 9

D e c - 0 8

O c t - 0 8

A u g - 0 8

J u n -

0 8

A p r - 0 8

F e b -

0 8

D e c - 0 7

O c t - 0 7

A u g - 0 7

J u n -

0 7

A p r - 0 7

F e b -

0 7

I n d

e x

The NATIONAL ASSOCIATION OF REALTORS® Housing Affordability Inor not a typical family could qualify for a mortgage on a typical home. This is dprice averages, family income, and mortgage rates. A reading of 100 means thaa median income has exactly enough income to qualify for a mortgage on a mhome. A reading above 100 signifies that a family has more than enough incoma mortgage loan on a median-priced home, assuming a 20% down payment.

Source: NAR.

6

7

8

9

10

6

7

8

9

10

J u n - 1 0

M a y - 1

0 A p

r - 1 0

M a r - 1

0 F e b

- 1 0 J a n

- 1 0 D e

c - 0 9

N o v - 0

9 O c

t - 0 9

S e p - 0

9 A u

g - 0 9 J u l

- 0 9

M o n t h s

With a 4% increase in listings and a decline in sales, the June 2010 single-familincreased to 8.9 months, well above the normal rate of around 6.0 months. Wforeclosures, this number is expected to increase further.

Source: NAR.

20

40

60

80

100

120

20

40

60

80

100

120

J u l - 1 0

F e b - 1 0

S e p - 0 9

A p r - 0

9 N o

v - 0 8

J u n - 0 8

J a n - 0 8

A u g - 0 7

M a r - 0

7 O c

t - 0 6

M a y - 0

6 D e

c - 0 5

J u l - 0 5

F e b - 0 5

S e p - 0 4

A p r - 0

4 N o

v - 0 3

J u n - 0 3

J a n - 0 3

A u g - 0 2

M a r - 0

2 O c

t - 0 1

M a y - 0

1

I n d

e x

Consumer confidence started off positive in second quarter 2010, reaching 62.7 in May beforefalling in June and declining to 50.4 in July. Consumers are weighed down by a variety ofconcerns, including the fear of another recession, job insecurity, a volatile stock market, andothers.

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

J u n - 1 0

M a y - 1

0 A p

r - 1 0

M a r - 1

0 F e b

- 1 0 J a n

- 1 0 D e

c - 0 9

N o v - 0

9 O c

t - 0 9

S e p - 0

9 A u

g - 0 9 J u l

- 0 9

P e r c e n

t C h a n g e

Q u a r t e r

A g o

The Conference Board’s Index of Leading Indicators fell 0.2% in June 2010, indicating that the pace of recovery is likely to slow in coming months. This decline was primarily due to thestock market, supplier deliveries, and average work week for production workers. However, theindex was 8.6% higher than year-ago readings, and if the index reading improves, as expected,during the next few months, the recovery will begin strengthening by 2011.

Source: NAR.

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

J u n - 1 0

F e b -

1 0

O c t - 0

9

J u n - 0

9

F e b -

0 9

O c t - 0

8

J u n - 0

8

F e b -

0 8

O c t - 0

7

J u n - 0

7

F e b -

0 7

O c t - 0

6

J u n - 0

6

F e b -

0 6

O c t - 0

5

J u n - 0

5

F e b -

0 5

O c t - 0

4

J u n - 0

4

F e b -

0 4

O c t - 0

3

J u n - 0

3

F e b -

0 3

O c t - 0

2

J u n - 0

2

F e b -

0 2

O c t - 0

1

J u n - 0

1

F e b -

0 1

O c t - 0

0

J u n - 0

0

F e b -

0 0 B e g

i n n

i n g o

f M o n

t h A d j u s t e d

C l o s i n g

P r i c e

The S&P 500 ended July 2010 at 1,030.71, down 0.05% from May. Since April, the S&P 500has slowly but steadily continued to decrease, although in general, the stock market has been

quite volatile during this time period.

Source: S&P.

Source: The Conference Board.

Consumer Confidence Housing Affordability

S&P 500 Existing Home Sales

Index of Leading Indicators Single Family Home Supply

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 22/25

21Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

The analysis provided in theRERC/CCIM Investment Trends Quarterly is conducted by Real Estate Research Corporation (RERC). The information is gathered in raw form from suCCIM designees and candidates, and from sales transactions collected from various sources, including CCIM members, various key commercial information exchange ormedia, assessors’ offices, RERC contacts in the marketplace, and other reliable public and private resources. All sales transactions are aggregated, analyzed, and reporteddata and forecasts are provided courtesy of the REALTORS® Commercial Alliance and Torto Wheaton Research.

Published quarterly, theRERC/CCIM Investment Trends Quarterly report provides timely insight into transaction volume, pricing, and capitalization rates for the core income-produ

RERC DefinitionsCapitalization Rate:The capitalization rate is defined as the first year “stabilized” net operating income (NOI) (NOI is before capital expenditures – tenant improvements, lreserves – and debt service) divided by the present value (or purchase price). Capitalization rates included are transaction-based medians and price-weighted averages.

RERC Capitalization Rate and Ranges:Capitalization rates and ranges listed throughout this report are based on RERC’s proprietary realized capitalization rate model, wh transaction-based capitalization rates, NCREIF Index Returns, and other market factors, but is heavily weighted toward transaction-based capitalization rates for each prope

Price-Weighted Average:The price-weighted average is developed through weighting each asset based on the gross sales price. Therefore, larger dollar properties are given msmaller dollar properties, with the weighted average reflecting more weight towards institutional real estate.

Size-Weighted Average:The size-weighted average is developed through weighting each asset based on its gross square footage – simply an aggregation of all the gross sale the aggregation of the gross square footage.

National/Regional Market Analysis:RERC ranks the investment potential of the metros and property types it covers based on various space market and financial market critecapitalization rates, vacancy rates, and other factors.

Investment Conditions Rating:A rating of 1 through 10 (with 10 being high) reflecting survey respondents’ collective views of the investment environment for a particular prowith other property types. The rating may take into account supply and demand, economic conditions, pricing, rental rates, or other factors.

NCREIF DefinitionsNCREIF:The National Council of Real Estate Investment Fiduciaries (NCREIF) is an independent organization dedicated to the compilation, validation, and distribution oinstitutional real estate investment community.

Total Return:The total return includes appreciation (or depreciation), realized capital gain (or loss), and income. It is computed by adding the income and capital appreciatbasis.

Implied Cap Rate (Income Return):The implied capitalization rate measures the portion of return attributable to each property’s NOI. It is computed by dividing the total NOIinvestment.

Capital Appreciation Return:The capital appreciation return measures the change in market value adjusted for any capital improvements/expenditures and partial sales dividequarterly investment.

Annual and Annualized Returns:Annual returns are computed by chain-linking quarterly rates of return to produce time-weighted rates of return for the annual and annualizeFor time periods beyond 1 year, the annualized returns are expressed as the annual compounded rate of return.

Allocation:The distribution, expressed as a percentage of the overall investment, in a particular geographic area by property type.For a detailed description of the proceeding returns, as well as the calculations used by NCREIF to derive these figures, please visit http://www.ncreif.org/indices.

The combined returns are the weighted average of the returns for each property type according to the proportionate market value of properties surveyed relative to the totaduring a time period.

RERC Defined Regions and MSAsWest:Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington, Wyoming

Midwest:Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin

South:Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, Oklahoma, Tennessee, Texas

East:Connecticut, Delaware, Kentucky, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South CWashington D.C., West Virginia

Metropolitan Statistical Area (MSA):A geographic unit comprised of one or more counties around a central city or urbanized area with 50,000 or more population. Contiguousincluded if they have close social and economic links with the area’s population nucleus.

With a few exceptions, the MSAs within this report coincide with the U.S. Office of Management and Budget’s December 2005 definitions for each MSA. For example, ington, Minn., as well as many other suburbs, are included within the Minneapolis MSA.

Note of Caution:It is imperative to exercise caution when comparing the data contained herein to previous reports published by RERC. The data herein is not “fixed,” and wchanged as additional transaction information is gathered and analyzed.

Disclaimer: This publication is designed to provide accurate information in regard to the subject matter covered. It is sold with the understanding that the publisher is not enlegal or accounting service. The publisher advises that no statement in this issue is to be construed as a recommendation to make any real estate investment or to buy or sinvestment advice. The examples contained in the publication are intended for use as background on the real estate industry as a whole, not as support for any particular rsecurity. Although the RERC/CCIM Investment Trends Quarterly uses only sources that it deems reliable and accurate, Real Estate Research Corporation (RERC) does nthe information contained herein.

S c o p e & M e t h o d o l o g y

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 23/25

22Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

RERC s CCIM Investment Trends QUARTERLY RERC Editorial Staff

Publisher Kenneth P. Riggs, Jr.CFA®, CRE, FRICS, MAI, CCIM

Editor-in-Chief Barb Bush

Lead AnalystBrian Velky

Research AnalystsGreg PhilippCliff CarlsonJeff Carr Charles Gohr David KellyLindsey KuhlmannAaron RiggsMeredith SteffenYe ThwayMorgan Westpfahl

Design Editor Michelle Houlgrave

Data ManagementScott HamerlinckBen NeilDaniel Warner

Production CommitteeTerri Cotter

Research AssistantsJeffrey HarmsChris Riggs

CCIM Institute

PresidentRichard Juge, CCIM

President-ElectFrank Simpson, CCIM

First Vice PresidentLeil Koch, CCIM

Treasurer Craig Blorstad, CCIM

Chief Executive Of cer Susan Groeneveld, CCIM

Copyright Notice for RERC ~CCIM Investment Trends Quarterly

Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute. All rightsreserved. No part of this publication may be reproduced, duplicated, or copied in any form, includ-ing electronic forwarding or copying, xerography, micro lm, or other methods, or incorporated intoany information retrieval system, without the written permission of RERC and the CCIM Institute.

Real Estate Research CorporationFounded more than 75 years ago, Real Estate Research Corporation(RERC) was the nation’s rst independent real estate rm that specializedin both real estate research and analysis. Recognized as a pioneer in theart of real estate management and for monitoring key sectors of the econ-omy that in uence the real estate industry, RERC has retained its place asone of the industry’s leading real estate investment trends analysts throughthe publication of such reports as Expectations & Market Realities in Real Estate and the RERC Real Estate Report . Today, RERC is known for itsresearch publications and market studies, commercial property valuations,complex consulting assignments, portfoliomanagement and technology services, andindependent duciary services.

The CCIM InstituteSince 1969, the Chicago-based CCIM Institute has conferred the Certi-

ed Commercial Investment Member (CCIM) designation to commercialreal estate and allied professionals through an extensive curriculum of 200classroom hours and professional experiential requirements. Currently,there are 9,000 CCIMs in 1,000 markets in the U.S. and 31 additional coun-tries. Another 7,000 practitioners are pursuing the designation, making theinstitute the governing body of one of the largest commercial real estatenetworks in the world. An af liate of the National Association of Realtors®,the CCIM Institute’s recognized curriculum, networking programs, andpowerful technology tools such as the Site To Do Business (site analysisand demographics resource) and CCIMREDEX (commercial property dataexchange), impact and in u -ence the commercial real es-tate industry. Visit www.ccim.

com, www.stdbonline.com,and www.ccimredex.com for more information.

The RERC/CCIM Investment Trends Quarterly is produced by

Real Estate Research Corporation (RERC) in association withand for members of the CCIM Institute.

A c k n o w l e d g e m e n t s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 24/25

23Investment Trends Quarterly s Copyright© 2010 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Jay Amoruso RE/MAX Precision Realty Hartford, CT

Beau Beery AMJ Inc. of Gainesville Alachua County, FL

Bart Binning Prudential Alliance Realty Oklahoma City, OK

Chip Bonghi Tri-State Security AssetAdvisors West

Latchezar Boyadjiev California Realty San Diego, CA

Jay Boyle Cassidy Turley San Diego, CA

Josh Breaux K W Commercial Los Angeles, CA

Taro Chellaram Coldwell Banker

Commercial UnitedHouston, TX

Ben Cherry Manor Real Estate St. Louis, MO

George Chronakis Prudential Fox & Roach,Realtors South Jersey

Tim Churchwell Prudential Towne Realty Norfolk, VA

Ralphael MarieClarke

Atlantic Coast RealtyAdvisors, Inc. Tampa, FL

Greg Clauson Coldwell Banker Commercial United Destin, FL

Coba C. Craig SILVESTRI-CRAIG,Realtors Midwest

John DeStefano CommercialInvestment Group, LLCSouth Carolina

William T. Ellis Concord Properties, LLC San Antonio, TX

J.W.(Bill) Ernst Charter CommercialRealty Group Indianapolis, IN

Tony Fluhr NTS DevelopmentCompany Louisville, KY

William E Gamble Gamble Real Estate South

Todd Gannet Century 21 Golden PostCommercial Northern New Jersey

Robert Glaser PICOR CommercialReal Estate Services Tucson, AZ

Chad Gleason Retail Realty Services Seattle, WA

Roger Gray Capital AssetProperties, LC San Antonio, TX

Rob GreenM&I Marshall & IlsleyBank Indianapolis, IN

Jeff Greischar Tech Builders Inc. Minneapolis, MN

Mike Habib Coldwell Banker Commercial San Diego, CA

Chris Harris Mutual of Omaha Bank Las Vegas, NV

Jack Hayes Jordan-HartCommercial Real EstateColumbus, GA

Toni L. Heiden Heiden Homes Realty &Associates Denver, CO

Cindy Hopkins K W Commercial San Antonio, TX

Gary Hunter Capital Financial, LLC Seattle, WA

Chris Jacobson Northmarq Minneapolis, MN

Charles Kelly Coldwell Banker Commercial Dallas, TX

James Kinsey ERG PropertyAdvisors New York, NY

Glen Kitto Kitto Realty Group Dallas, TX

Kenneth Krawczyk K.S.K. Services, Inc. Milwaukee, WI

Gary J. Lee Carter & Associates Atlanta, GA

Chris Leon Realty World San Francisco, CA

Bruce LindquistThe Linco Group -K W CommercialTemecula

San Diego, CA

Mike Liyeos Quattro Development,L.L.C. Midwest

Karl Dee Maret Coldwell Banker Commercial NRT Tampa, FL

Steve Maygar CBC TradeMark Raleigh, NC

Daryl Mccubbin Recap Advisors Nashville, TN

Melissa Molyneaux Colliers International Reno, NV

Dan Montgomery Western Properties Portland, OR

Chris Napier Foster Pepper PLLC Seattle, WA

C o n t r i b u t o r s

8/8/2019 CCIM Investment Trends Quarterly - 3Q 2010

http://slidepdf.com/reader/full/ccim-investment-trends-quarterly-3q-2010 25/25

Scott NaugleReal PropertyInvestment Mgmt., LLCWashington, DC

Tom O’Connor O’Connor MortgageInvestments Inc. West

Michael OvertonColdwell Banker CommercialCoastalMark

Raleigh, NC