cbdt issues a circular on indirect transfer provisions clarifying applicability to offshore funds

TRANSCRIPT

Vol. 13 Issue 1.1 January 9, 2017

About BMR Advisors | BMR Newsletters | BMR Insights | Events | Contact Us | Feedback

CBDT issues a circular on indirect transfer provisions clarifying

applicability to offshore funds

The Central Board of Direct Taxes (‘CBDT’): India’s apex tax administration body has

issued a Circular No 41 of 2016 (the ‘New Circular’) on December 21, 2016 clarifying

various aspects of the indirect transfer provisions that are codified in the Indian

income-tax law1. The CBDT had set-up a Working Group on June 15, 2016 to study

the scope and the concerns raised by various stakeholders in relation to the indirect

transfer provisions; the clarifications provided in the New Circular are based on the

comments of the Working Group. The New Circular is in the form of FAQs and

contains 19 clarifications on applicability of the indirect transfer provisions to (i)

various investment funds that conduct portfolio investments in India through different

fund structures, and (ii) on other salient aspects of the indirect transfer provisions.

At the outset, it is important to note that the New Circular does not state anything new

in relation to the manner in which the indirect transfer provisions, as are currently

codified in the income-tax law, ought to be interpreted. It merely reiterates the law

and unfortunately, does not provide any relief to offshore funds.

Background

The indirect transfer provisions were introduced in the Indian income-tax law in 2012,

with retrospective effect from April 1, 1961. As per the indirect transfer provisions,

any share or interest in an offshore entity that substantially derives its value from

underlying Indian assets, is deemed to be situated in India; consequently, a transfer

of such a share / interest in the offshore entity should be subject to tax in India. The

indirect transfer provisions were introduced with the intent to repudiate the ruling of

the Supreme Court of India in the case of Vodafone2, where the Supreme Court had

held that Vodafone was not liable to withhold taxes on the purchase of shares in an

offshore company from a non-resident seller, resulting in Vodafone acquiring indirect

ownership in the seller’s Indian telecom business, which was held by the seller

through a network of foreign entities. The indirect transfer provisions were intended

to apply to transactions that are routed through low tax or no tax countries, with which

India does not have a tax treaty3.

Since 2012, the indirect transfer provisions have been subject matter of considerable

debate and have created much angst amongst offshore investors, such as Public

Market funds and private equity funds that manage India-focused funds and / or

deploy an India-focused investment structure, by setting-up an India-focused SPV to

invest into India. The concerns were manifold, ranging from (i) extra-territorial

applicability of the Indian income-tax law, (ii) double taxation of income where the

offshore fund has paid tax on its India-sourced income, (iii) applicability of Vodafone

tax principles to non-Vodafone like structures, as in these cases there was an actual

direct transfer of shares / securities of Indian companies etc. Over the past few

Share

Connect

India’s Economic Performance and

Business Imperatives: Onboarding GST

– One Nation, One Tax

EBG & BMR Advisors Webinar: Impact of

GST on businesses in India

GST: Is India Inc Ready?

GST: Are states ready?

Sectorial analysis of the Model GST Law

Draft Model GST Law - A BMR Phone

Conference

A BMR Webinar on India Mauritius Tax

Treaty Amendment

CNBC TV-18 & BMR Advisors CEO Poll

on 2 Years of Modi Government

India’s Economic Performance and

Business imperatives: Making India

Business Friendly

Managing Tax Disputes in India

Taxand Global Survey 2015

2017:

years, the Indian Government, at its end, has tried to allay the concerns of foreign

investors, as regards various issues with the indirect transfer provisions by:

(a) Extending the reference made to the committee that was set-up by the Indian

Government and which was headed by Dr Parthasarthi Shome (‘Shome

Committee’) to examine the GAAR provisions, to also examine the issues

associated with the indirect transfer provisions4;

(b) Constituting a high-level committee to consider assessment of income (arising

prior to April 1, 2012) arising from the retrospective applicability of the indirect

transfer provisions;

(c) Amending the indirect transfer provisions in the Union Budget 2015 to provide

various safeguards against the trigger of the indirect transfer provisions, such as,

carve-outs for small investors, providing that the indirect transfer provisions will

apply only to those offshore entities that derived at least 50% of their value from

Indian assets, and providing for taxation of income on account of indirect

transfers only on a proportionate basis;

(d) Clarifying that dividends declared and paid by an offshore company outside India

in respect of shares that derive substantially their value from India assets, do not

come within the purview of the indirect transfer provisions; and

(e) Introducing valuation rules for determining the value of shares / interest in the

offshore entity under the indirect transfer provisions.

Unfortunately, the aforesaid measures taken by the Government have not really

addressed the concerns raised by foreign investment funds, as regards the

applicability of the indirect transfer provisions to their cases. The New Circular issued

by the CBDT does not provide any relief to foreign investment funds, and does not

address their concerns with the indirect transfer provisions.

Summary of the New Circular and our comments

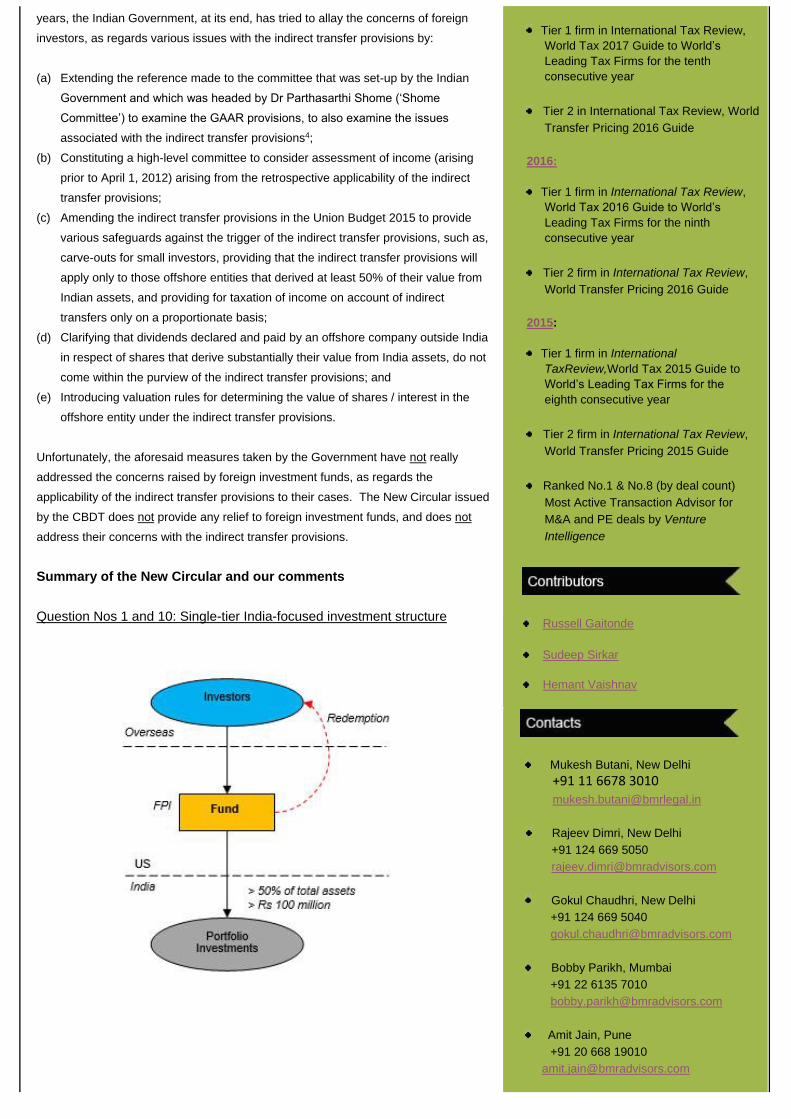

Question Nos 1 and 10: Single-tier India-focused investment structure

Tier 1 firm in International Tax Review,

World Tax 2017 Guide to World’s

Leading Tax Firms for the tenth

consecutive year

Tier 2 in International Tax Review, World

Transfer Pricing 2016 Guide 2016:

Tier 1 firm in International Tax Review,

World Tax 2016 Guide to World’s

Leading Tax Firms for the ninth

consecutive year

Tier 2 firm in International Tax Review,

World Transfer Pricing 2016 Guide

2015:

Tier 1 firm in International

TaxReview,World Tax 2015 Guide to

World’s Leading Tax Firms for the

eighth consecutive year

Tier 2 firm in International Tax Review,

World Transfer Pricing 2015 Guide

Ranked No.1 & No.8 (by deal count)

Most Active Transaction Advisor for

M&A and PE deals by Venture

Intelligence

Mukesh Butani, New Delhi

+91 11 6678 3010

Rajeev Dimri, New Delhi +91 124 669 5050 [email protected]

Gokul Chaudhri, New Delhi

+91 124 669 5040

Bobby Parikh, Mumbai

+91 22 6135 7010

Amit Jain, Pune +91 20 668 19010 [email protected]

Russell Gaitonde

Sudeep Sirkar

Hemant Vaishnav

Facts

Fund is set up in a popular jurisdiction, say US and is registered in India as a

Foreign Portfolio Investor (‘FPI’).

It pools money from retail / institutional investors and invests in shares of listed

Indian companies.

More than 50% of total assets of the Fund are in India.

Value of assets of the Fund are greater than Rs 100 million (~US$ 1.47

million).

The Fund buys and sells shares on the Indian bourses and pays tax as per the

income-tax law or applicable tax treaty rates.

The Fund redeems the units / shares held by investors on an ongoing basis.

Questions framed to the Indian Government

Q1 - Will the indirect transfer provisions apply to redemption of shares / units

by the Fund?

Q10 - FPIs are not strategic investors and pay taxes in India on capital gains

earned by them. Applying the indirect transfer provisions in the case of FPIs

could lead to double taxation of the same income ie tax on gains earned on

direct transfer of Indian securities and tax on gains earned by investors of the

FPIs on redemption of shares / units in the FPI. Hence, exemption from the

indirect transfer provisions should be provided for FPIs.

CBDT clarification

The indirect transfer provisions will be applicable to the investors of the Fund

on the redemption of shares / units of the Fund.

However, the carve-out prescribed in the income-tax law for ‘small investors’

will be available ie investors:

(i) Holding 5% or less voting power or share capital or interest in the Fund;

and

(i) Not holding any right of management or control in the Fund

will not be subject to the indirect transfer provisions.

Kalpesh Maroo, Bengaluru

+91 80 4032 0090

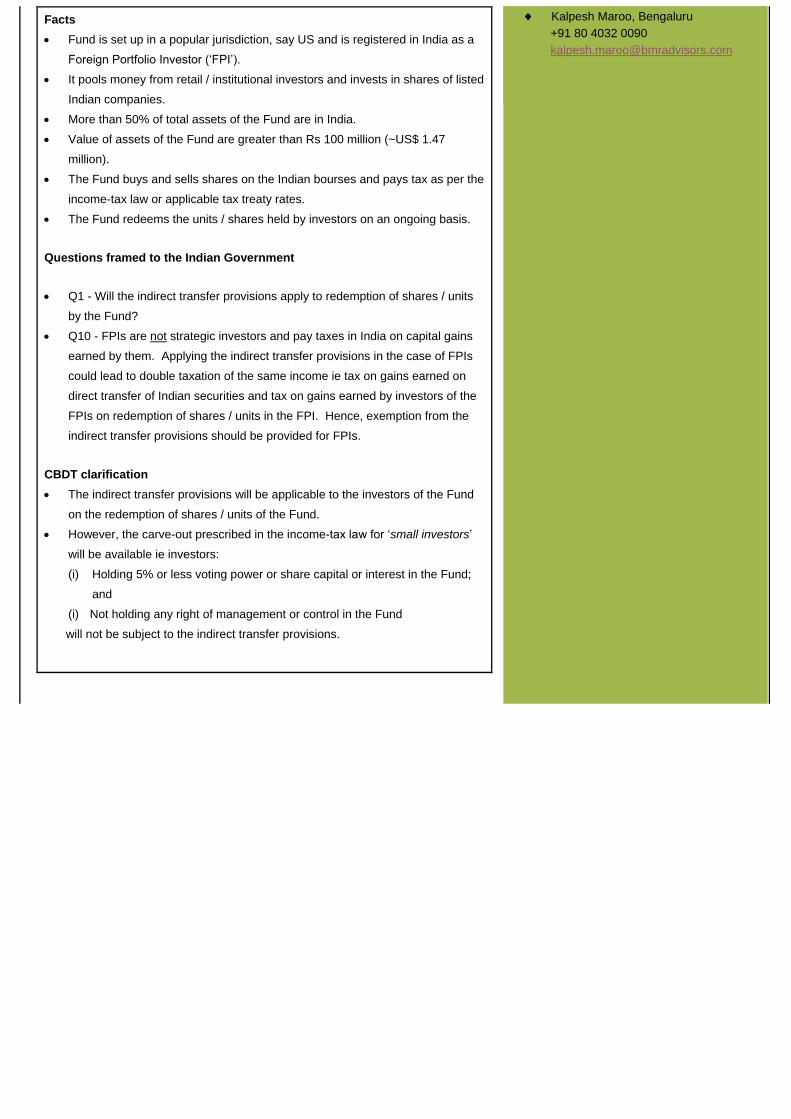

Question No 2: Multi-layered India-focused investment structure

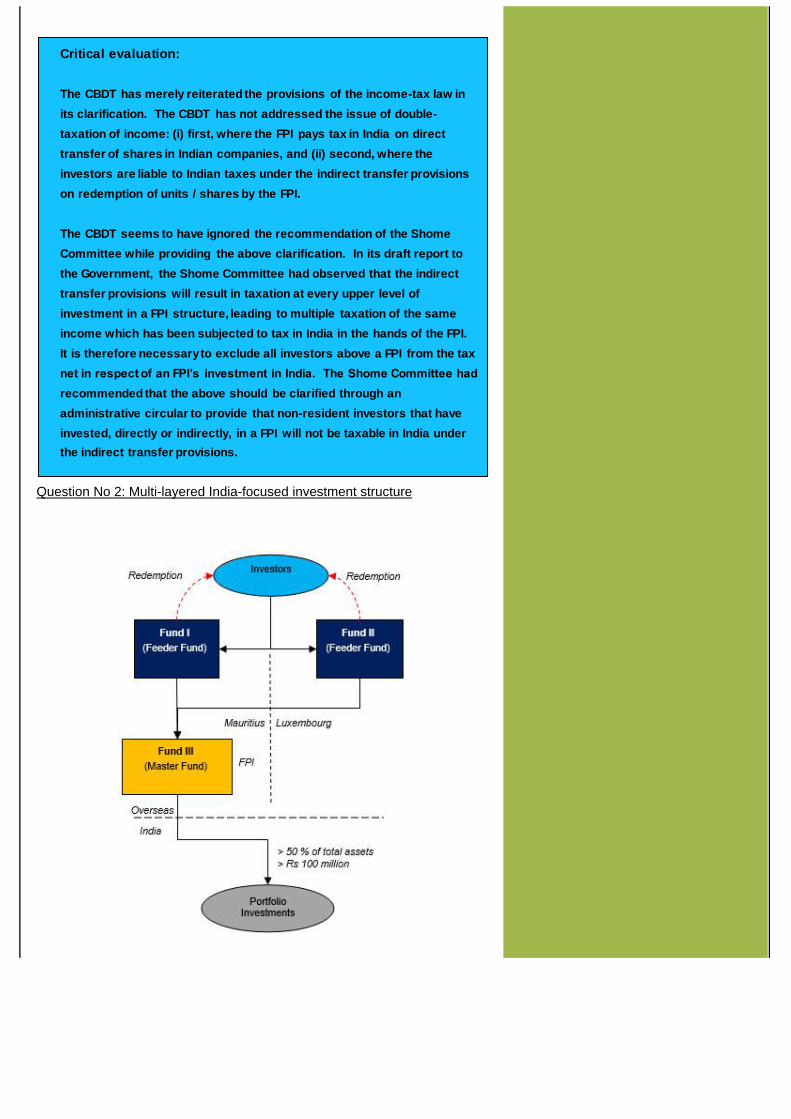

Critical evaluation:

The CBDT has merely reiterated the provisions of the income-tax law in

its clarification. The CBDT has not addressed the issue of double-

taxation of income: (i) first, where the FPI pays tax in India on direct

transfer of shares in Indian companies, and (ii) second, where the

investors are liable to Indian taxes under the indirect transfer provisions

on redemption of units / shares by the FPI.

The CBDT seems to have ignored the recommendation of the Shome

Committee while providing the above clarification. In its draft report to

the Government, the Shome Committee had observed that the indirect

transfer provisions will result in taxation at every upper level of

investment in a FPI structure, leading to multiple taxation of the same

income which has been subjected to tax in India in the hands of the FPI.

It is therefore necessary to exclude all investors above a FPI from the tax

net in respect of an FPI’s investment in India. The Shome Committee had

recommended that the above should be clarified through an

administrative circular to provide that non-resident investors that have

invested, directly or indirectly, in a FPI will not be taxable in India under

the indirect transfer provisions.

Facts

Fund I and Fund II are feeder funds that have been set-up in different

countries, say Mauritius and Luxembourg, respectively.

They pool money from investors for onward investment into India through

Fund III, situated in Mauritius and registered in India as a FPI.

None of the investors of Fund I and Fund II have the right of control or

management in Fund III or hold voting power or share capital or interest,

directly or indirectly, exceeding 5% in Fund III; a declaration to this effect is

provided by Fund I and Fund II, to Fund III.

More than 50% of total assets of Fund III are in India.

Value of assets of Fund III are greater than Rs 100 million (~US$ 1.47 million).

Question framed to the Indian Government

Will the indirect transfer provisions apply to investors in master-feeder

structures, given that the investors do not have the right of control or

management in Fund III or hold voting power or share capital or interest,

directly or indirectly, exceeding 5% in Fund III?

CBDT clarification

Prima facie, the indirect transfer provisions will not be applicable on the

redemptions undertaken by Fund I and Fund II to the investors, because the

investors fall within the carve-out prescribed in the income-tax law for ‘small

investors’ ie investors:

(i) Do not hold more than 5% voting power or share capital or interest in Fund III;

and

Do not hold any right of control or management in Fund III.

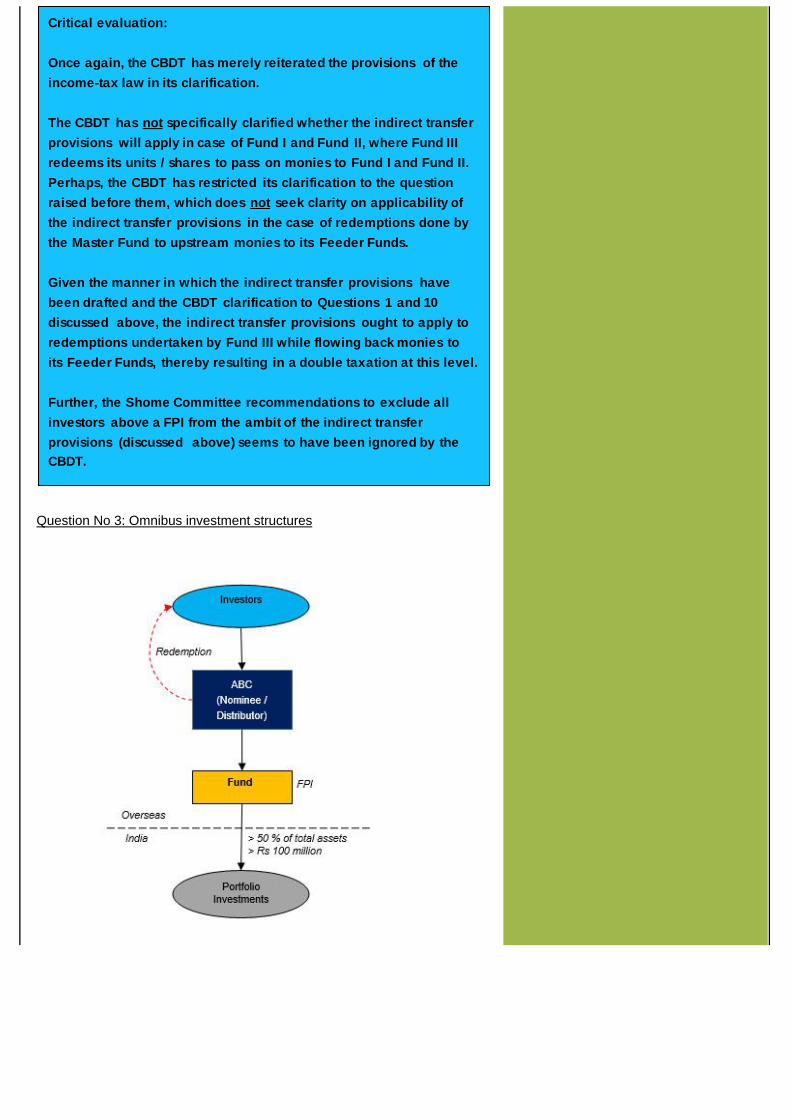

Question No 3: Omnibus investment structures

Critical evaluation:

Once again, the CBDT has merely reiterated the provisions of the

income-tax law in its clarification.

The CBDT has not specifically clarified whether the indirect transfer

provisions will apply in case of Fund I and Fund II, where Fund III

redeems its units / shares to pass on monies to Fund I and Fund II.

Perhaps, the CBDT has restricted its clarification to the question

raised before them, which does not seek clarity on applicability of

the indirect transfer provisions in the case of redemptions done by

the Master Fund to upstream monies to its Feeder Funds.

Given the manner in which the indirect transfer provisions have

been drafted and the CBDT clarification to Questions 1 and 10

discussed above, the indirect transfer provisions ought to apply to

redemptions undertaken by Fund III while flowing back monies to

its Feeder Funds, thereby resulting in a double taxation at this level.

Further, the Shome Committee recommendations to exclude all

investors above a FPI from the ambit of the indirect transfer

provisions (discussed above) seems to have been ignored by the

CBDT.

Facts

ABC is a foreign nominee / distributor that pools money from investors for

investment into the Fund.

None of the investors has the right of control or management in the Fund or

hold voting power or share capital or interest, directly or indirectly, exceeding

5% in the Fund; a declaration to this effect is furnished by the nominee /

distributor to the Fund.

ABC is recorded as registered shareholder in the books of the Fund.

More than 50% of total assets of the Fund are in India.

Value of assets of the Fund are greater than Rs 100 million (~US$ 1.47

million).

Question framed to the Indian Government

Will the indirect transfer provisions apply to nominee / distributor type

structures, where the investors do not have the right of control or

management in the Fund or hold voting power or share capital or interest,

directly or indirectly, exceeding 5% in the Fund?

CBDT clarification

Prima facie, the indirect transfer provisions will not be applicable on the transfer of

interest in ABC by investors, as the investors fall within the carve-out prescribed in

the income-tax law for ‘small investors’ ie investors:

(i) Do not hold more than 5% voting power or share capital or interest in the

Fund; and

Do not hold any right of management or control in the Fund.

Question No 4: India-focused sub-fund investment structure

Facts

The Fund is established in say US and pools money of its investors for

implementing investments in Asia.

The Fund directly invests 90% of its corpus in Asia (ie non-India). The

balance 10% of the corpus has been allocated towards Indian investments.

The Indian investments are implemented through a step-down entity based in

say Mauritius (ie Sub-fund); Sub-fund exclusively invests in Indian securities.

More than 50% of total assets of the Sub-fund are in India.

Value of assets of the Sub-fund are greater than Rs 100 million (~US$ 1.47

million).

Question framed to the Indian Government

Will the indirect transfer provisions apply to Fund which uses a separate

India-focused sub-fund for India investments, where none of the investors

have the right of control or management in the Fund or hold voting power or

share capital or interest, directly or indirectly, exceeding 5% in the Fund?

CBDT clarification

The indirect transfer provisions will apply in the case of the Fund, as the value of

shares held by it in the Sub-fund derives its value substantially from assets

located in India, irrespective of the shareholding of the ultimate investors.

Critical evaluation:

The CBDT has not clarified whether the indirect transfer provisions

will apply to ABC, when redemptions are implemented by the Fund.

Strictly tax technically, the indirect transfer provisions should

apply at the ABC level as ABC is not covered by the aforesaid

carve-out provisions. This will result in double taxation at the Fund

level, where the Fund redeems its shares held by ABC, to flow back

monies to ABC.

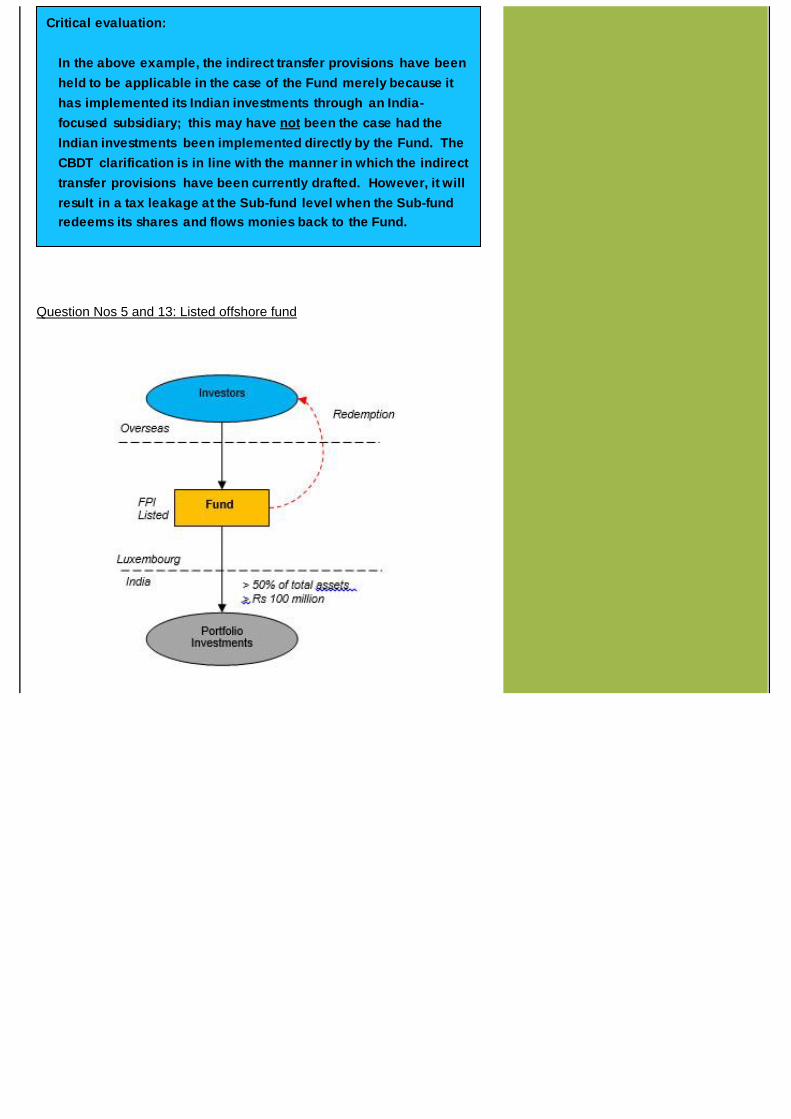

Question Nos 5 and 13: Listed offshore fund

Critical evaluation:

In the above example, the indirect transfer provisions have been

held to be applicable in the case of the Fund merely because it

has implemented its Indian investments through an India-

focused subsidiary; this may have not been the case had the

Indian investments been implemented directly by the Fund. The

CBDT clarification is in line with the manner in which the indirect

transfer provisions have been currently drafted. However, it will

result in a tax leakage at the Sub-fund level when the Sub-fund

redeems its shares and flows monies back to the Fund.

Facts

Fund is a listed fund in say Luxembourg and is registered in India as a FPI.

More than 50% of total assets of the Fund are in India.

Value of assets of the Fund are greater than Rs 100 million (~US$ 1.47

million).

The investors in the Fund keep changing on a daily basis, buying and selling

of the units / shares in the Fund through the stock exchange on which the

Fund is listed.

Questions framed to the Indian Government

Q5 – Will the indirect transfer provisions apply on transfer of shares or units

of an offshore listed entity?

Q13 - FPIs that are regulated and listed on a recognized stock exchange

should be excluded from the purview of the indirect transfer provisions.

CBDT clarification

The indirect transfer provisions will be applicable to the investors of the Fund

on the redemption of shares / units of the Fund. However, the carve-out for

small investors (discussed earlier) will be available.

A specific carve-out for FPIs that are regulated and listed on a recognized

stock exchange is not feasible.

Question No 6: Overseas merger of corporate entities

Critical evaluation:

Given the offshore listed entities are not specifically exempted

from the indirect transfer provisions, the CBDT has clarified the

above question in light of the extant indirect transfer provisions.

This is going to create practical challenges for investors in Fund,

as they will need to withhold Indian tax on payments that they will

make to the sellers in the Fund, even though they may not know

the identity of the sellers.

Pertinently, the Shome Committee had recommended that

exemption from the indirect transfer provisions may be provided

to a foreign company which is listed on a recognized stock

exchange and its shares are frequently traded therein. However,

once again, the Shome Committee’s recommendation has not

been considered in the New Circular.

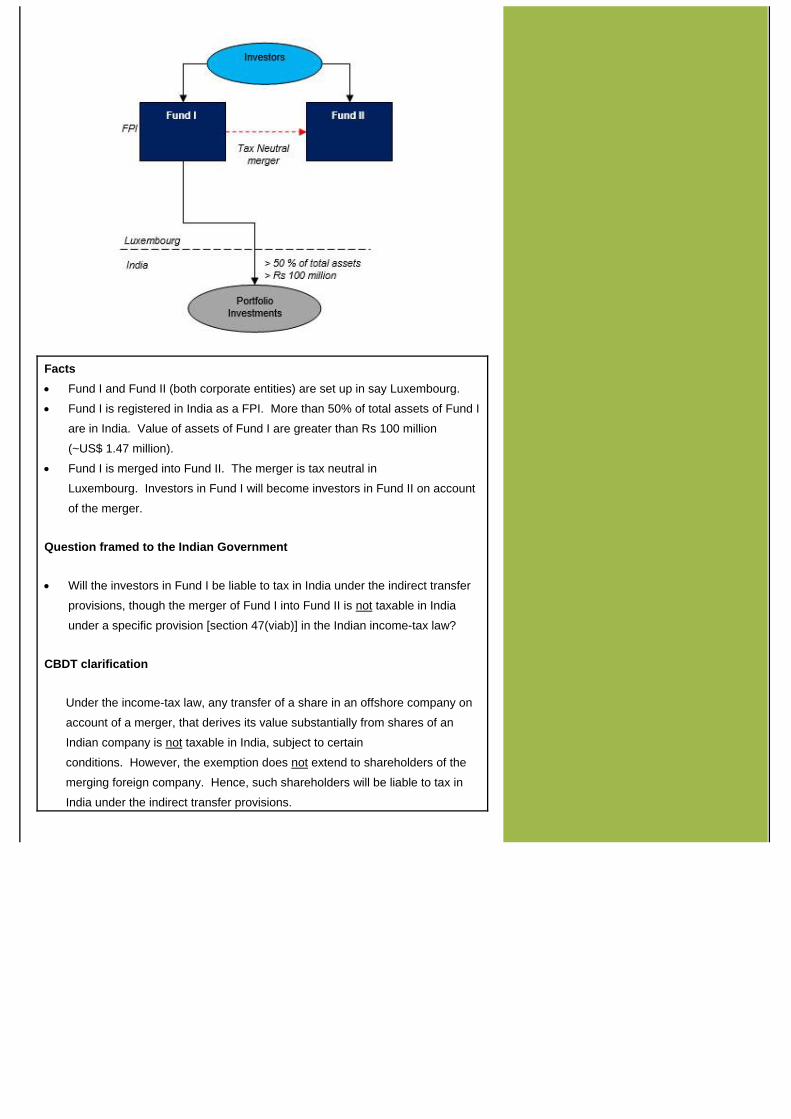

Facts

Fund I and Fund II (both corporate entities) are set up in say Luxembourg.

Fund I is registered in India as a FPI. More than 50% of total assets of Fund I

are in India. Value of assets of Fund I are greater than Rs 100 million

(~US$ 1.47 million).

Fund I is merged into Fund II. The merger is tax neutral in

Luxembourg. Investors in Fund I will become investors in Fund II on account

of the merger.

Question framed to the Indian Government

Will the investors in Fund I be liable to tax in India under the indirect transfer

provisions, though the merger of Fund I into Fund II is not taxable in India

under a specific provision [section 47(viab)] in the Indian income-tax law?

CBDT clarification

Under the income-tax law, any transfer of a share in an offshore company on

account of a merger, that derives its value substantially from shares of an

Indian company is not taxable in India, subject to certain

conditions. However, the exemption does not extend to shareholders of the

merging foreign company. Hence, such shareholders will be liable to tax in

India under the indirect transfer provisions.

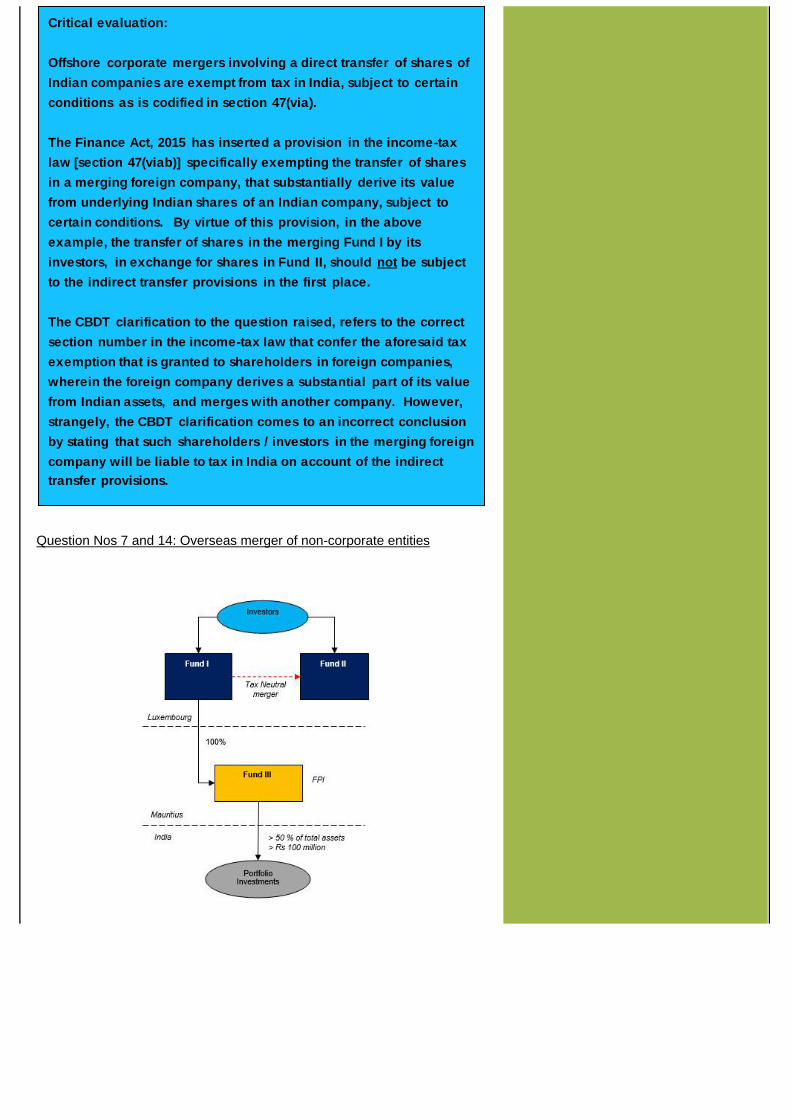

Question Nos 7 and 14: Overseas merger of non-corporate entities

Critical evaluation:

Offshore corporate mergers involving a direct transfer of shares of

Indian companies are exempt from tax in India, subject to certain

conditions as is codified in section 47(via).

The Finance Act, 2015 has inserted a provision in the income-tax

law [section 47(viab)] specifically exempting the transfer of shares

in a merging foreign company, that substantially derive its value

from underlying Indian shares of an Indian company, subject to

certain conditions. By virtue of this provision, in the above

example, the transfer of shares in the merging Fund I by its

investors, in exchange for shares in Fund II, should not be subject

to the indirect transfer provisions in the first place.

The CBDT clarification to the question raised, refers to the correct

section number in the income-tax law that confer the aforesaid tax

exemption that is granted to shareholders in foreign companies,

wherein the foreign company derives a substantial part of its value

from Indian assets, and merges with another company. However,

strangely, the CBDT clarification comes to an incorrect conclusion

by stating that such shareholders / investors in the merging foreign

company will be liable to tax in India on account of the indirect

transfer provisions.

Facts

Fund I and Fund II (both non-corporate entities) are set up in say

Luxembourg.

Fund I holds 100% of the shares in Fund III; Fund III has been set-up in say

Mauritius and is an India-focused entity.

Fund I is merged into Fund II. The merger is tax neutral in

Luxembourg. Investors in Fund I will become investors in Fund II on account

of the merger.

Questions framed to the Indian Government

Q7 - Will the indirect transfer provisions apply in case of offshore merger or

demerger of foreign non-corporate entities?

Q14 - Offshore merger of corporate entities involving a transfer of shares in

an Indian company is exempt from tax in India. Can this benefit be extended

to non-corporate FPIs and to the shareholders or unitholder of all the FPIs?

CBDT clarification

The indirect transfer provisions will be applicable to the merger of Fund I into Fund

II as there is no specific exemption from Indian taxes for an offshore merger of

non-corporate entities.

Question Nos 8 and 16: Clarification on “specified date” for valuation of

assets in India

Critical evaluation:

Offshore mergers of non-corporate entities involving a transfer of

shares of Indian companies are not specifically exempt from tax in

India.

The CBDT has remained silent on the applicability of the indirect

transfer provisions in the case of the unitholders of Fund I. Tax

technically, even the unitholders in Fund I should be subject to the

indirect transfer provisions.

The Shome Committee had recommended that all group

reorganizations that do not result in the change in ownership,

should be exempt from the indirect transfer provisions. However,

this aspect has not been considered while clarifying the question

on reorganizations involving non-corporate entities.

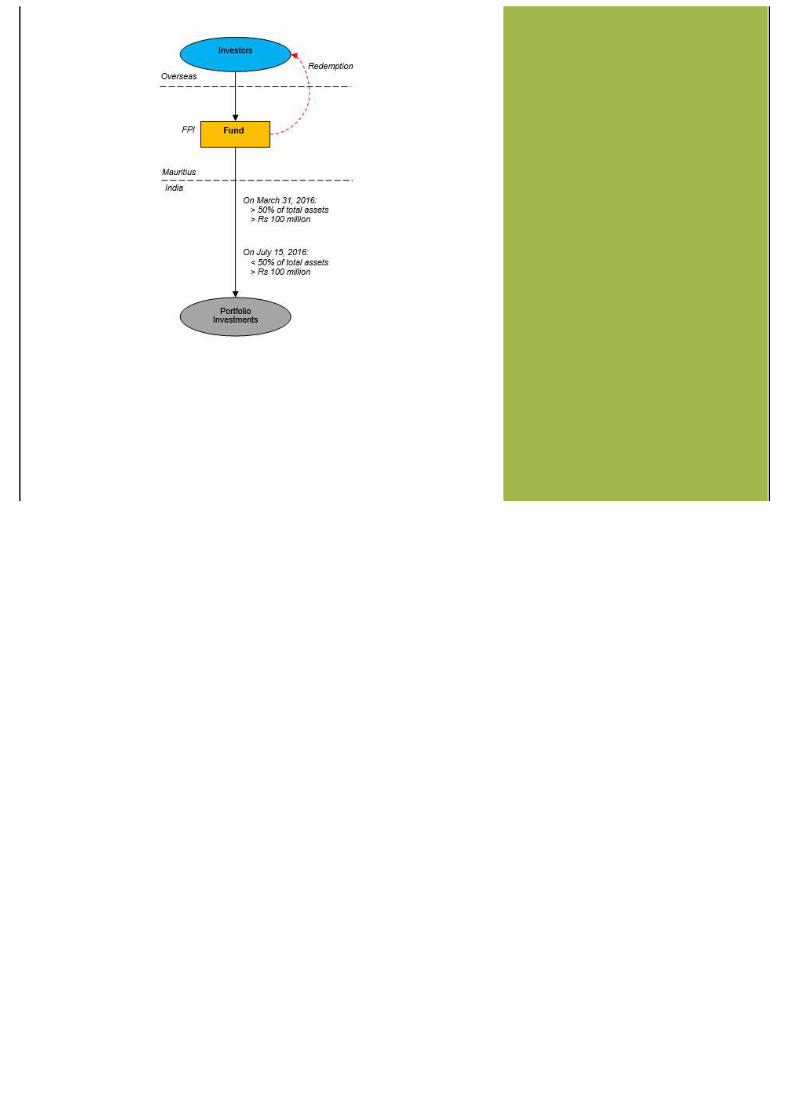

Facts

Fund I is registered in India as a FPI.

On the last date of preceding accounting period say March 31, 2016, the fund

has:

(i) More than 50% of total assets of the Fund in India; and

(ii) Value of assets of the Fund are greater than Rs 100 million (~US$ 1.47

million).

However, as on date of transfer (ie redemption) say July 15, 2016, only 47%

of the total assets of the Fund are in India.

The book value of the assets on the date of transfer does not exceed the book

value of assets as on the last day of the preceding accounting period by 15%.

Questions framed to the Indian Government

Q8 – Will the indirect transfer provisions apply even if the offshore transfer

does not fulfil the substantial value test (ie Indian assets should be more than

50% of the total assets of a fund) as on the date of transfer?

Q16 – Specified date for the purpose of the indirect transfer provisions means

the date on which the accounting period of the company or entity ends,

preceding the date of transfer of share or interest. The specified date should

be the date of transfer.

CBDT clarification

The value of the assets of the Fund in India will be computed as on the

“specified date” which will be:

(i) the last date of the accounting period preceding the date of transfer of the

shares/units of the Fund; or

(ii) the date of transfer, if the book value of the assets of the company on the

date of transfer exceeds the book value of the assets as on the last date

of the above mentioned accounting period by 15%.

Hence, in the example given, the specified date on which the value of the

Fund in India is to be seen in this case would be on March 31, 2016; not the

date of transfer ie July 15, 2016.

The indirect transfer provisions will apply since the offshore transfer fulfils the

substantial value test as on the specified date.

Adopting the specified date as on the date of transfer alone, may result in

abuse of the indirect transfer provisions.

Question No 9: Reporting requirements for Indian companies under the

indirect transfer provisions

Facts

A listed Indian company has received investment from several FPIs (including

offshore listed funds). At the offshore level, the shares / units of the FPIs are

purchased and sold on a daily basis and the investors in the FPIs keep

changing frequently.

Questions framed to the Indian Government

How should the Indian company determine whether the value of assets in

India of a FPI exceeds 50% of its total assets?

Where a FPI has invested into multiple Indian companies, there are practical

challenges for Indian companies to comply with the reporting requirements.

CBDT clarification

The specific reporting requirements have been recently introduced in the

Income-tax Rules, and their practical implementation should first seen.

Critical evaluation:

Indian companies are required to undertake an annual filing with

the CBDT, providing a plethora of information under the indirect

transfer provisions. These include, inter-alia,:

(a) Group structure of the offshore investor.

(b) Holding structure of the shares in the Indian company by the

offshore investor before and after an indirect transfer has been

implemented.

(c) Financial and accounting statements of the offshore investor

for two years prior to the date of an indirect transfer.

(d) Information regarding the offshore investor and its subsidiaries

such (i) business operation, (ii) personnel, (iii) finance and

properties, etc.

(e) Asset valuation report along with supporting documents.

The reporting requirements are fairly onerous and most Indian

companies may struggle to provide the information to the CBDT.

Failure to furnish the prescribed information to the CBDT could

lead to penal consequences for the Indian company.

Critical evaluation:

The CBDT’s clarification is a reproduction of the law, as it

currently stands. Accordingly, to determine the applicability of

the indirect transfer provisions; the valuation of the assets of the

Fund will have to be undertaken twice ie (i) on the date of transfer,

and (ii) on the last date of the preceding accounting period.

Question Nos 11 and 12: Threshold limits for small investors and value of

assets in India

Questions framed to the Indian Government

The threshold value of Rs 100 million (~US$ 1.47 million) specified for the

share / interest in an overseas entity for triggering the indirect transfer

provisions should be increased to Rs 1 billion (~US$ 14.5 million).

The carve-out prescribed in the income-tax law for “small investors” which is

5% or less of the voting power or share capital or interest in the company /

entity (whether individually or along with associated enterprises) should be

increased.

The term “associated enterprise” should be defined in line with what is

reckoned by the Securities and Exchange Board of India for the purpose of

ascertaining the common beneficial ownership of 50% in case of FPIs.

CBDT clarification

The 5% threshold limit for excluding the “small investors” from the ambit of

the indirect transfer provisions is reasonable and cannot be increased.

Alignment from the definition of “associated enterprise” with the SEBI

definition is not required as the definition under the Indian income-tax law is

well-founded and is based on the concept of management, control and

capital of an enterprise.

The monetary limit of Rs 100 million (~US$ 1.47 million) is reasonable

Question Nos 15, 17 and 18: Rules to determine the fair value of the Indian

assets vis-a-vis global assets

Critical evaluation:

The concerns of the stakeholders, especially FPIs, for an increased

threshold has been summarily rejected by the CBDT.

Pertinently, the Shome Committee had recommended that the

threshold for “small investors” should be in line with the Indian

transfer pricing provisions ie 26%.

Facts

Rules to determine the fair market value of India assets vis-à-vis global

assets should be prescribed.

The manner of determining the cost of acquisition in the hands of the non-

resident transferor including clarity on indexation benefit and foreign

exchange fluctuation should be provided.

The indirect transfer provisions should be operationalized only after

necessary rules have been prescribed.

CBDT clarification

The CBDT has vide notification S.O.2226(E) dated June 28, 2016 has

prescribed the relevant Rules 11UB and 11UC under the Income-tax Rules,

1962, providing the method for determining the value of assets and

apportionment of income under the indirect transfer provisions.

The availability of indexation benefit and foreign exchange fluctuation will be

as per the Indian income-tax laws.

The indirect transfer provisions have already been operationalized.

Question No 19: Applicability of withholding tax provisions, interest and

penalty in case of FPIs

Critical evaluation:

The questions relating to prescribing valuation rules seems to

have been raised to the Indian Government, before the CBDT had

prescribed the valuation rules in June 2016.

At present, cost indexation benefits are available for tax payers on

transfer of long-term capital assets. There is no inherent bar for

non-resident tax payers from claiming cost indexation benefits,

which should apply in case of transfer of shares in an offshore

entity.

Question framed to the Indian Government

FPIs may find it difficult to comply with the indirect transfer

provisions. Hence, FPIs should be relieved from withholding tax

requirements; alternatively, the threshold for enforcing withholding tax

requirements should be increased in case of FPIs.

No penalty of interest should apply to FPIs for failure to withhold taxes, on

account of retrospective application of the indirect transfer provisions and a

FPI should not be treated as an ‘assessee-in-default’ or the ‘representative

assessee’ on account of retrospective application of the indirect transfer

provisions.

CBDT clarification

The provisions of withholding tax, interest and penalty shall apply as per law.

Critical evaluation:

Since the introduction of the indirect transfer provisions in 2012,

offshore investment funds that get impacted by the indirect

transfer provisions, have not been withholding taxes on

redemption of shares / units held by their investors, based on the

recommendations that were made by the Shome Committee to the

Indian Government on the indirect transfer provisions and their

applicability to offshore investment funds. Indian tax officers have

also not actively probed this issue / questioned FPIs on this issue.

However, the above CBDT circular, which is binding on tax

officers, could create complications. One will need to wait and

watch to see how tax officers react to the above CBDT

clarification.

1 Income-tax Act, 1961

2 Vodafone International Holdings BV vs UOI (341 ITR 1) (SC)

3 Speech of the Finance Minister in the lower house of the Parliament on May 7, 2012

4 Draft Report on Retrospective Amendments Relating to Indirect Transfer – Expert Committee (2012)

Conclusion:

The present Government’s election manifesto stated that, inter-

alia, it was committed to providing a simple, rationale, non-

adversarial, stable and predictable tax regime in India. The New

Circular issued by the CBDT seems to go against the

Government’s aforesaid stated objectives of providing a

predictable and stable tax regime. The New Circular merely

reiterates the existing law in relation to the indirect transfer

provisions that was enacted by the previous Indian Government;

contrary to general expectations, the New Circular does not grant

any relief to FPIs, from the indirect transfer provisions.

The New Circular seems to have ignored some of the

recommendations of the Shome Committee for rationalizing the

indirect transfer provisions and specifically, exempting FPIs from

the applicability of these provisions.

This is something the Government should consider remedying on

a priority basis. This could be done by way of an amendment to

the income-tax law, in the Union Budget 2017 which is to be tabled

before the Parliament on February 1, 2017.

In closing, one should also keep in mind that foreign investors that

are impacted by the aforesaid indirect transfer provisions, should

be eligible to claim tax treaty relief, under their respective tax

treaties that they will be able to access. However, for investors

that do not have access to tax treaties or whose tax treaties are not

beneficial, such investors are likely to be impacted by the

aforesaid circular. Additionally, even where taxes are paid in India

on account of the indirect transfer provisions, such taxes may not

be creditable in the investors’ home country, resulting in an

additional tax burden being case upon the foreign investors.

BMR Business Solutions Pvt. Ltd.

36B, Dr. RK Shirodkar Marg, Parel, Mumbai 400012, India

Tel: +91 22 6135 7000 | Fax: +91 22 6135 7070

BMR and Community

BMR has a strong commitment to good citizenship and community service. We are as dedicated to community work as we are to client

work. Wherever appropriate we partner with our clients in fulfilling our social responsibility. Through the firm’s ‘Go Green Initiative’ we

adopt environment friendly practices at our work place. The firm actively supports SOS Children’s Village, Indian Red Cross Society and

MillionTrees Gurgaon campaign. For more details on our social and environmental responsibility programme, click here.

Disclaimer:

This newsletter has been prepared for clients and Firm personnel only. It provides general information and guidance as on date of

preparation and does not express views or expert opinions of BMR Advisors. The newsletter is meant for general guidance and no

responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in this newsletter will be

accepted by BMR Advisors. It is recommended that professional advice be sought based on the specific facts and circumstances. This

newsletter does not substitute the need to refer to the original pronouncements.

Copyright 2016. BMR Business Solutions Pvt. Ltd. All Rights Reserved

In case, you do not wish to receive this newsletter, click here to unsubscribe