caveat venditor: trust asymmetries in acquisitions of ... · caveat venditor: trust asymmetries in...

TRANSCRIPT

CAVEAT VENDITOR: TRUST ASYMMETRIES INACQUISITIONS OF ENTREPRENEURIAL FIRMS

MELISSA E. GRAEBNER

University of Texas at Austin

I explore the role of trust in acquisitions of entrepreneurial firms, taking a dyadic viewthat gives equal attention to buyers and sellers. The two parties have asymmetric viewsregarding whether their counterparts are trustworthy. I outline how these asymmetriesemerge, persist, and influence behavior, including tendencies to behave deceptivelyand to guard against deception. I also find that buyers’ and sellers’ beliefs concerningwhether their counterparts are trustworthy and trusting are often erroneous. I explorethe implications of these findings for developing a theory of trust asymmetries andargue that selecting buyers on the basis of trust increases rather than diminishesentrepreneurs’ vulnerability.

Interorganizational trust is a subject of substan-tial interest to organizational and managementscholars. Previous research has focused primarilyon trust in the context of long-term alliances, par-ticularly long-lasting relationships between buyersand suppliers (e.g., Dyer & Chu, 2000; Sako &Helper, 1998; Saparito, Chen, & Sapienza, 2004).Scholars have examined how trust develops be-tween alliance partners (e.g., Doz, 1996; Ring & Vande Ven, 1994), influences subsequent partner selec-tion (Gulati & Gargiulo, 1999), and shapes out-comes such as governance structures (Gulati &Singh, 1998), information sharing (Larson, 1992;Uzzi, 1996), satisfaction with partnerships (Ander-son & Narus, 1990; Mohr & Spekman, 1994), andfinancial performance (Luo, 2002).

Interfirm trust has received much less attentionin the context of an equally significant set of interor-ganizational transactions, mergers and acquisitions(M&A). Acquisitions are important strategic toolsthat enable companies to obtain valuable technol-ogy (Puranam, Singh, & Zollo, 2006), spur innova-tion (Ahuja & Katila, 2001; Paruchuri, Nerkar, &Hambrick, 2006), penetrate international markets(Birkinshaw, Bresman, & Hakanson, 2000; Ver-meulen & Barkema, 2001), and reconfigure firmresources (Capron, Dussauge, & Mitchell, 1998).Yet, despite the importance of these transactions,mergers and acquisitions have received little atten-tion in the organizational trust literature (Stahl &Sitkin, 2005).

Similarly, trust has received little attention in thelarge literature on mergers and acquisitions. The

M&A literature provides some hints that trust playsa role in mergers and acquisitions, but ultimatelythese hints raise more questions than they answer.Case study data suggest that acquisition targets fa-vor acquirers they trust (Graebner & Eisenhardt,2004), and larger-scale studies indicate that acqui-sition deals are more likely to occur when a buyerand seller have a prior direct relationship (Schildt& Laamanen, 2006; Vanhaverbeke, Duysters, &Noorderhaven, 2002) or shared network ties(D’Aveni & Kesner, 1993), circumstances that mayfoster trust (Gulati, 1995; Larson, 1992; Uzzi, 1997).Yet despite these signs that trust may be presentbetween buyers and sellers, authors have describeddeception by buyers as “standard practice” (Buono& Bowditch, 1989: 256) and noted that distrustoften emerges after deals close (Buono, Bowditch, &Lewis, 1985; Haspeslagh & Jemison, 1991), whenbuyers’ “prior promises mean nothing” (Marks &Mirvis, 2001: 87).

The apparent coexistence of trust and deceptionin acquisitions is puzzling. On the one hand, ifbuyer deception is common, it is not surprising thatsellers would prefer buyers they trust. But if sellersfavor buyers they trust, how can deception by buy-ers remain so common? If buyers and sellers oftenhave prior direct relationships or shared third-party ties, why are sellers so often mistaken in theirassessments of buyers? Moreover, knowing they aretrusted by sellers, why do buyers not feel the senseof moral obligation to behave in good faith thathas been observed in alliances (Larson, 1992)? Whyaren’t buyers more concerned with the negativeimplications of deception for postdeal cooperationby acquired employees, or for their firms’reputations?

My thanks go to Editor Sara Rynes and the three anon-ymous reviewers for their helpful comments, and toPersephone Doliner for her heroic copyediting.

� Academy of Management Journal2009, Vol. 52, No. 3, 435–472.

435

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download or email articles for individual use only.

These questions are especially perplexing for ac-quisitions of knowledge-based, technology-inten-sive firms, an important source of innovation andgrowth in high-technology industries (Ahuja &Katila, 2001; Puranam et al., 2006). In knowledge-intensive markets, firm leaders have more discre-tion to choose their acquirers (Coff, 2003), suggest-ing acquisition targets may be particularly able toselect buyers they trust. Technology-intensive in-dustries are often tightly networked (Castilla,Hwang, Granovetter, & Granovetter, 2000; Powell,1990), implying that sellers should have easy ac-cess to information about buyers. Moreover, thesuccess of a technology-based acquisition dependson the continued presence and cooperation of ac-quired employees (Granstrand & Sjolander, 1990;Ranft & Lord, 2002), raising the potential costs tobuyers of behaving deceptively. These factorsshould make the coexistence of trust and deceptioneven less likely.

In the current work, I seek to unravel these puz-zles. The purpose of this study is to explore trustand deception in acquisitions of technology ven-tures, giving equal attention to the views of buyersand sellers. In examining these issues, I aim toaddress calls for more context-specific examina-tions of trust (Kramer, 1999; Krishnan, Martin, &Noorderhaven, 2006; Schoorman, Mayer, & Davis,2007). I find that trust and deception can coexist inthe context of acquisitions because of a complex setof asymmetries and errors in both parties’ viewsregarding trust and trustworthiness. I examine howthese patterns both emerge from and influence ac-quisition events and behavior. A central theoreticalcontribution of this research is a greater under-standing of trust asymmetries, a topic that has beenidentified as a “pressing unanswered question” intrust theory (Gulati & Sytch, 2008: 277). Prior interor-ganizational trust research rests on an implicit as-sumption that trust between partners is symmetric,yet it “has not examined the empirical validity ofthis assumption nor the antecedents and the out-comes of asymmetric trust in interorganizationalrelationships” (Zaheer & Harris, 2005: 193). Thecurrent study begins to address these gaps by de-scribing how trust asymmetries emerge, persist,and influence decision making and behavior in thestrategically important setting of mergers and ac-quisitions. In addition, this study helps to developa dyadic perspective on acquisitions by givingequal attention to the viewpoints and actions ofselling firms (Graebner, 2004; Graebner & Eisen-hardt, 2004), a group largely neglected by priorresearch.

METHODS

This study grew out of a broader research en-deavor examining acquisition processes and deci-sion making from the viewpoints of both buyersand sellers. Trust was not a concept that was iden-tified a priori as being of interest but one thatemerged from the data as an important influence onacquisition decision making. A subsequent reviewof the interorganizational trust literature revealedvery little previous work on trust in acquisitions,suggesting the need to extend theory in this area.

The general approach of this study is “theoryelaboration” (Lee, Mitchell, & Sablynski, 1999).Drawing upon prior research, I define trust as apositive expectation regarding the conduct of an-other party in a situation involving risk or vulner-ability (Lewicki, McAllister, & Bies, 1998; Rous-seau, Sitkin, Burt, & Camerer, 1998; Zaheer,McEvily, & Perrone, 1998). I adopt the perspectivethat trust is a multilevel concept (Currall & Inkpen,2002) and define interorganizational trust as the“collectively-held orientation” of a group’s individ-ual members toward another group or firm (Zaheeret al., 1998: 143). By this definition, groups andorganizations as well as individuals can both trustand be trusted. Trust at the top management teamlevel may be particularly critical in interorganiza-tional transactions, since senior management is re-sponsible for major strategic actions such as alli-ances and acquisitions (Schoorman et al., 2007;Zaheer, Lofstrom, & George, 2002). Therefore, inthis study, I focus specifically on trust between thetop management teams of the buyer and seller en-gaged in an acquisition (or, if the buyer is a verylarge firm, the top management team of the relevantbusiness unit).

The research design is a qualitative, multiple-case study (Eisenhardt, 1989). Case studies are apreferred research strategy for examining complexsocial phenomena because they allow researchersto develop a holistic understanding of real-lifeevents (Yin, 2003) and to elucidate dynamic pro-cesses involving multiple causal chains (Pettigrew,1992). In comparison to single-case, ethnographicstudies, the multiple-case method trades off a de-gree of detail in favor of greater generalizability(Yin, 2003).

Setting

The research setting was acquisitions of entrepre-neurial, technology-based ventures. This setting of-fered several advantages. As stated previously, ac-quisitions of technology ventures have particularrelevance for developing theory on trust in acqui-

436 JuneAcademy of Management Journal

sitions. Trust may be especially pertinent in thesetransactions because technology-intensive firmsare more able to choose their own buyers (Coff,2003) and have access to dense industry networksthat may supply useful information about potentialpartners (Powell, 1990). In addition, privately heldtargets represent the majority of acquisition activityin the United States (Capron & Shen, 2007), andacquisitions of entrepreneurial firms are the subjectof substantial and growing research interest (e.g.,Puranam et al., 2006; Schweizer, 2005).

The current study focuses on the acquisitionwave of 1999–2000. Most merger and acquisitionactivity occurs in waves (e.g., Andrade & Stafford,2004; Rhodes-Kropf & Viswanathan, 2004). Thesewaves are often triggered by technological advance-ment or other industry shocks (Harford, 2005),coincide with peak market valuations, and arefollowed by market declines (Rhodes-Kropf, Rob-inson, & Viswanathan, 2005). Following this pat-tern, the 1999–2000 acquisition wave was triggeredby a significant technological advance (the growthof the Internet) and coincided with a “boom-bust”cycle in the financial markets.

Sample

The primary sample included 12 entrepreneurialfirms and eight acquirers. Table 1 summarizes var-ious characteristics of the firms in this sample.Three entrepreneurial firms were sampled in eachof four industries: networking hardware, commu-nications software, financial software, and onlinecommerce. The sampled industries differed on keystrategic dimensions such as cost structure, cus-tomer profile, and method of sales and distribution.In each industry, two of the entrepreneurial firmswere acquired (for a total of eight acquisitions), andthe remaining firm received interest from buyersbut remained independent. The eight completedacquisitions provided a dyadic view of the entireacquisition process. However, to understand iftrust influences whether an acquisition occurs atall, it was also useful to examine deals that wereconsidered but never realized. I therefore gathereddata on deals that any of the eight buyers and 12potential targets considered but did not complete.

Entrepreneurial activity is spatially concentrated(Schoonhoven & Romanelli, 2001; Sorenson & Stu-art, 2001). Since regional clustering could influ-ence the dynamics of trust in acquisitions, I sam-pled both target-acquirer pairs that were located inthe same region and pairs that were located inregions distant from one another (e.g., a Europeanfirm acquiring a Silicon Valley start-up). The com-pleted acquisitions included four target-acquirer

pairs located in the same local region and four pairslocated in distant regions. All acquisitions tookplace less than six months prior to data collection,improving the likelihood that informants accu-rately remembered events that had occurred (Huber& Power, 1985). Six acquisitions were ongoing dur-ing data collection. This allowed incorporation ofboth real-time and retrospective data, a useful com-bination for understanding the sequence and flowof events (Pettigrew, 1992). Retrospective data al-low for efficiency in data collection, and real-timedata improve depth of understanding of how eventsevolve over time (Leonard-Barton, 1990).

The mean acquisition price in the sample was$175 million, which is very similar to the averageacquisition price of $155 million for U.S. venture-funded companies in the study time period, ac-cording to the database VentureSource. All acqui-sitions involved the purchase of 100 percent of thetargets’ equity. The sampled acquisitions were paidfor with the buyers’ equity, as was typical duringthe study time period (Schultz & Zaman, 2001) andis typical during merger waves in general (Rhodes-Kropf & Viswanathan, 2004).

Agency theory suggests that the acquisitionmotives and preferences of a target firm’s manag-ers and its shareholders may differ (Jensen &Meckling, 1976). I therefore collected informa-tion about the ownership structure of the targetfirms. Of the eight companies that were acquired,management owned a controlling share in four,and investors owned a controlling share in four.Five acquired firms had received venture capital,and the remaining three were funded throughother sources, such as self-financing and angelinvestment. I also collected information on ac-quired firm board composition. The mean num-ber of directors was 5.1; 32 percent of the direc-tors were active company managers; 44 percent,investors; and 24 percent, outsiders. This break-down was similar to the board composition re-ported in other studies of entrepreneurial firms(Kaplan & Stromberg, 2003; Lerner, 1995).1

The buyers in the sample were more diverse andincluded both young entrepreneurial firms and es-tablished multinational corporations. There weresix publicly traded and two privately held buyers.The average number of employees among buyers

1 Lerner (1995) reported an average of 5.0 directors inhis sample (including 27 percent active managers, 46percent investors, and 25 percent outsiders), and Kaplanand Stromberg (2003) reported an average of 6.0 directors(35 percent active managers, 41 percent investors, 23percent outsiders).

2009 437Graebner

TABLE 1Cases

Seller, Industry Seller Profilea, b Buyer, Price Buyer Profileb Interviewees

MonetNetworking

hardware

175 employees; four yearsVenture capital; investor-

controlledEastern United StatesExperience: TMT; board

Picasso $500M 16,000 employeesPublicDistant regionExperience: Firm; TMT; board

Seller: CEO (board member); CFO;venture capitalist (boardmember)

Buyer: VP, business development;VP, technical integration; chieftechnology officer (boardmember)

RocketNetworking

hardware

20 employees; three yearsSelf-funded; manager-

controlledSilicon ValleyExperience: Board

North $57M 50,000 employeesPublicDistant regionExperience: Firm; TMT; board

Seller: CEO (board member); chieftechnology officer; outsideboard member

Buyer: VP, line of business;head of business unit; M&Amanager

JunketNetworking

hardware

335 employees; four yearsVenture capital,

institutional investors;investor-controlled

Silicon ValleyExperience: TMT; board

Acquisition wasnot completed

Seller: CEO (board member);venture capitalist (boardmember)

TrendFinancial

software

50 employees; three yearsVenture capital; investor-

controlledSilicon ValleyExperience: TMT; board

Armor $400M 400 employeesPublicLocal regionExperience: Board

Seller: CEO (board member); VP,services; VP, sales; venturecapitalist (board member)

Buyer: CEO (board member); VP,business development

IsleFinancial

software

40 employees; two yearsVenture capital; manager-

controlledSilicon ValleyExperience: None

Harbor$125M

300 employeesPublicLocal regionExperience: Board

Seller: CEO (board member); VP,business development (boardmember); chief technologyofficer, product manager

Buyer: director businessdevelopment; M&A manager;manager of strategy

Modelc

Financialsoftware

95 employees; three yearsVenture capital; investor-

controlledWestern United StatesExperience: Board

Armor;Acquisition wasnot completed

400 employeesPublicDistant regionExperience: Board

Seller: CEO (board member); twoventure capitalists (one boardmember)

Buyer: CEO (board member); VP,business development

Concept 35 employees; three years Karma 150 employees Seller: CEO (board member); VP,Communications

softwareVenture capital and angel

investors$125M Private, became public three

months after acquisitionbusiness development (boardmember); angel investor (board

Investor-controlled Local region member); venture capitalistSilicon ValleyExperience: TMT; board

Experience: TMT; board (board member)Buyer: CEO (board member); VP,

sales; industry expert

Fastlane 120 employees; four years Craze $140M 700 employees Seller: CEO (board member); VP,Communications

softwareVenture capital; investor-

controlledEastern United StatesExperience: TMT; board

PublicDistant regionExperience: Firm; TMT; board

sales; venture capitalist (boardmember)

Buyer: VP, business development;VP, M&A; VP, technology;director of integration

Regimenc 70 employees; two years Karma;Acquisition wasnot completed

150 employees Seller: CEO (board member)

Continued

438 JuneAcademy of Management Journal

was 8,500, with a range of 150 to 50,000. Becausesome research has suggested that prior acquisi-tions may create routines that shape buyers’ be-havior in subsequent deals (Zollo & Singh, 2004),I collected data on buyers’ acquisition experi-ence. I gathered information on whether a firm asa whole had conducted prior acquisitions, as wellas whether individual members of the firm’s topmanagement team or board of directors had ac-quisition experience. Three of the eight buyershad acquisition experience at the firm level andhad developed dedicated M&A staff. Of the re-maining five buyers, three had acquisition expe-rience among both the top management team andthe board of directors. The remaining two buyershad acquisition experience within the board ofdirectors only. For completeness, I gathered thesame experience information for sellers. Al-though no seller had acquisition experience atthe firm level, 10 of the 12 sellers had acquisitionexperience within their top management team,board of directors, or both.

Data Collection

I used several data sources: (1) quantitative andqualitative data from semistructured interviewswith key acquisition participants from both sellingand buying firms, (2) e-mails and phone calls toclarify interviews and track real-time processes,and (3) archival data, including company websites,business publications, and regulatory filings. I con-ducted more than 80 interviews. The first phaseincluded 15 pilot interviews with managers whohad sold their companies, managers who had pur-chased companies, investors in companies thatwere sold, and acquisition intermediaries. The pi-lot interviews indicated that sellers’ acquisition de-cisions were usually made by a small set of people,typically the chief executive officer and two orthree key executives and/or board members. Buy-ers’ decision processes involved somewhat broaderparticipation, but decisions were ultimately madeby the top management team of the firm or, if thebuyer was very large, the top management team of

TABLE 1(Continued)

Seller, Industry Seller Profilea, b Buyer, Price Buyer Profileb Interviewees

Communicationssoftware

Venture capital; investor-controlled

Silicon ValleyExperience: TMT

PrivateLocal regionExperience: TMT; board

Buyer: CEO (board member); VP,sales; industry expert

GoalieOnline

commerce

25 employees; two yearsAngel investors; manager-

controlledEastern United StatesExperience: TMT

Ciao $15M 200 employeesPrivateDistant regionExperience: TMT; board

Seller: CEO (board member); VP,business development (boardmember); angel investor (boardmember)

Buyer: CEO (board member); VP,business development; venturecapitalist (board member)

Spur/Primed

Onlinecommerce

25 employees; three yearsAngel investors; manager-

controlledSilicon ValleyExperience: TMT; board

Checkmate$35M

350 employeesPublicLocal regionExperience: TMT; board

Seller: CEO—Spur (boardmember); CEO—Prime (boardmember); VP, businessdevelopment; two angelinvestors (both board members).

Buyer: CEO (board member), VP,business development

EvergreenOnline

commerce

127 employees; threeyears

Venture capital; investor-controlled

Western United StatesExperience: None

Acquisitionwas notcompleted

Seller: CEO (board member); twoventure capitalists (both boardmembers).

a “Years” refers to time since founding. “Control” (manager vs. investor) refers to ownership majority (50 percent or more of the firm’sequity). “TMT” is “top management team.”

b “Experience” refers to prior acquisition experience by firm, top management team members, and/or members of board of directors.c In the cases of Model and Regimen, buyer profiles appear for Armor and Karma because these potential buyers were interviewed,

although the acquisitions were not completed.d Spur and Prime were both acquired by Checkmate, in a combined deal.

2009 439Graebner

the relevant business unit. Other individuals atboth firms had limited awareness of the eventstaking place until late in the acquisition process.

In the primary data collection, I interviewed mul-tiple senior-level informants from each firm. (SeeTable 1 for a list of the positions of these interview-ees.) Use of multiple informants mitigates subjectbiases (Golden, 1992; Miller, Cardinal, & Glick,1997) and leads to a richer, more elaborated model(Schwenk, 1985). The pilot interviews guided myidentification of the informants who were the mostinfluential in each acquisition process. To furtherensure that the sample included the most impor-tant individuals, I used snowball sampling. My ini-tial entry was typically made through either theCEO of the selling firm or the head of businessdevelopment at the buying firm. Each informant thennamed other individuals who had been actively in-volved in the acquisition within both the buyer andseller. Selling firm informants typically included theCEO and senior vice presidents (VPs), as well as oneor more investors who were board members and/orhad led a funding round. Buying firm informantstypically included the CEO or business unit head, thevice president of business development, and one ormore other senior managers or board members whowere involved with the acquisition.

The interviews were 60 to 90 minutes in length.Interviews began with background information andthen asked the informant for an open-ended chro-nology of the company’s acquisition-related activi-ties and decisions. Open-ended questioning leadsto higher accuracy in retrospective reports (Lipton,1977; Miller et al., 1997). Examples of questionsinclude, “When did you first begin thinking aboutacquisition?” “What alternatives to acquisition didyou consider?” “What potential buyers/targets didyou consider, and what kind of interaction did youhave with them?” “Could you describe the negoti-ation process?” and “What happened after the ac-quisition closed?” No questions specifically men-tioned trust, deception, or related issues. However,these topics emerged unprompted in informants’discussions of the pros and cons of various poten-tial partners and their descriptions of negotiationprocesses. Each interview concluded with severalclosed-ended questions about the firm, includingits founding date and number of employees. Inaddition to the buyers and sellers, I interviewedseveral individuals who had extensive acquisitionexperience, such as the head of technology mergersat a prominent investment bank. These interviewsincluded questions that were idiosyncratic to theexpertise of the informant.

All interviews were audiotaped and transcribed.The transcriptions totaled 1,260 double-spaced

pages. I asked follow-up questions via phone ore-mail when clarification was required. If acquisi-tion events were ongoing, I conducted subsequentinterviews when a major event occurred, such asclosure of the deal or the departure of an acquiredexecutive. This procedure allowed me to captureevents and viewpoints as they emerged. I inter-viewed informants as many as three times.

Throughout data collection, I took steps to min-imize informant biases. First, as noted above, thesample comprised cases in which the events ofinterest had occurred no more than six monthsprior to data collection. Prior research has sug-gested that informant recollections are stable overperiods of this length (Huber, 1985). Second, thesample included real-time as well as retrospectivecases. During the analysis phase, I compared thereal-time and retrospective cases and confirmedthat no differences were present. Third, the infor-mants included multiple individuals from eachselling and buying firm. Such individuals are likelyto have different perspectives on and interests inthe acquisition process. If retrospective (or other)bias were an issue, I would have seen significantdifferences in their event descriptions (Seidler,1974). I did not. Fourth, I took care to interviewindividuals at the center of the acquisition process.Highly influential and knowledgeable informantsare the most reliable, particularly when they arerecalling important, recent events (Huber & Power,1985; Kumar, Stern, & Anderson, 1993; Seidler,1974). Fifth, I promised confidentiality to encour-age candor (Glick, Huber, Miller, Doty, & Sutcliffe,1990; Huber & Power, 1985; Miller et al., 1997).Finally, I addressed potential subject bias by em-ploying multiple data sources (Jick, 1979). I com-pared informants’ responses not only with those ofother informants, but also with archival data (fromsources such as acquisition announcements andregulatory filings) where appropriate.

Data Analysis

Data analysis was partly planned and partlyemergent. Throughout the analysis, I shifted backand forth between the raw data, the patterns emerg-ing from the data, and extant theory on trust ininterorganizational transactions. The analysis tookan iterative rather than a linear path but for sim-plicity is presented here in distinct stages.

Stage 1. Because the purpose of this study was toexamine the role of trust throughout the acquisitionprocess, a first analytical step was to understandand organize key acquisition events. I began bywriting detailed case studies (Eisenhardt, 1989).The case studies were 40 to 70 pages in length and

440 JuneAcademy of Management Journal

included informant quotes as well as tables andtimelines summarizing the key facts of each acqui-sition. A second researcher also examined the rawdata and formed an independent perspective,which was incorporated into each case.

I used a temporal bracketing strategy to distill aprocess model from the cases (Denis, Lamothe, &Langley, 2001; Langley, 1999). This strategy in-volves identifying discrete time periods, or phases,within a process. In this study, phases were demar-cated by changes in the individuals involved, thenature of the activities taking place, and the phys-ical location of these activities. Five acquisitionphases emerged from this analysis. The first phaseis screening, in which CEOs and business develop-ment officers initially evaluate both potential part-ners and potential partnership structures (i.e., ac-quisition versus alliance). The second phase issocializing, in which the CEOs or business unitheads of the two firms informally interact in non-work settings. The third phase, which may overlapwith socializing, is agreeing in principle. In thisphase, the top managers’ discussions shift frompersonal topics to drafting the outlines of the ac-quisition agreement. The fourth phase is legaliza-tion, in which managers work with attorneys andfinancial advisors to create formal, legally bindingacquisition documents. This phase concluded withthe official closing of a deal. The last phase isimplementation, in which managers from the twofirms begin integrating the businesses.

Stage 2. The second stage of analysis was aimedat understanding how informants described andconceptualized trust in the context of acquisitions.Prior research has used many different dimension-alizations and measures of trust (e.g., Cummings &Bromiley, 1996; Currall & Judge, 1995; Mayer,Davis, & Schoorman, 1995). Because none of thesemeasures has emerged as dominant (McEvily &Tortoriello, 2007), and because many wereuniquely tailored to their original settings, I ini-tially cast a broad net. I examined each interviewtranscript in detail, using existing interorganiza-tional trust research in a “sensitizing” role (Miles &Huberman, 1984; Strauss & Corbin, 1998). The trustliterature drew my attention to comments regardingtrust, vulnerability, integrity, deception, commit-ment fulfillment, reliability, and other related con-cepts. In this process, I discovered a correspondencebetween informants’ comments and the trust dimen-sions developed and validated by Cummings andBromiley, who described trust as “an individual’sbelief or common belief among a group of individualsthat another individual or group (a) makes good-faithefforts to behave in accordance with any commit-ments both explicit and implicit, (b) is honest in

whatever negotiations preceded such commitments,and (c) does not take excessive advantage of anothereven when the opportunity is available” (1996: 303).

In the present context, evidence of trust on Cum-mings and Bromiley’s (1996) “a,” “b,” and “c” di-mensions (described above) included the followingexamples: (a) “We totally trusted them. We likedhow they did business—they do what they say theyare going to do”; (b) “When we got into the detailsof the deal [during negotiations] . . . [the CFO] . . .was just unbelievable to us. He was a straight shot”;and (c) “You can trust them. . . . If we thought [buy-er’s management] were out to get us and wanted todrive us to the bone and sweat us out and were outto screw us over, I wouldn’t have done the deal.”Evidence of distrust on these dimensions includedcomments such as: (a) “There’s never a sure thing.[The deal] is not done until it’s signed and deliv-ered,” (b) “During the courtship, everyone putstheir best foot forward. Then you find out later,”and (c) “You get the feeling that they are going totake you for a ride, chip away at your value—andthat leaves you exposed.” As in Cummings andBromiley (1996), the three dimensions were closelyrelated; in no case did leaders from a firm expresstrust toward a given counterpart on one dimensionand distrust toward the same counterpart on anyother dimension.

Stage 3. In the final stage of analysis, I integratedthe findings from the preceding stages to under-stand how the presence or absence of trust influ-enced the unfolding of the acquisition process, andvice versa. The process model developed in stage 1served as an analytical guide. I examined each ofthe phases, noting how buyers’ and sellers’ beliefsconcerning trust and trustworthiness both emergedfrom and affected the activities taking place. I usedstandard cross-case analysis techniques (Eisen-hardt, 1989) to look for patterns and revisited thedata often, using charts and tables to facilitate com-parisons between cases (Miles & Huberman, 1984;Yin, 2003).

FINDINGS

Trust Asymmetries and the Acquisition Process

In this section, I address how buyers’ and sellers’trust-related views both emerge from and influenceevents throughout the phases of the acquisitionprocess. I find asymmetries between buyers andsellers regarding whether trust is important in thetransaction and find both asymmetries and errorsin firms’ assessments of whether their counterpartsare trustworthy and trusting. In the screeningphase, sellers eliminate distrusted partners, but

2009 441Graebner

buyers do not. This creates a fundamental asymme-try in which most sellers trust their buyers, butmost buyers distrust their sellers. During the nexttwo phases of the acquisition process, socializingand agreeing in principle, trust asymmetries growand deception is common, particularly among buy-ers. Deception ranges from negotiation-relatedbluffing to more serious, material deception. Theoccurrence and form of deception are related towhether the deceiver trusts and feels trusted by theother party. However, beliefs about whether theother party is trustworthy and/or trusting are ofteninaccurate. In the legalization phase, asymmetricviews of one another’s trustworthiness lead mostbuyers, but few sellers, to engage in extensive duediligence and to implement protective deal terms.During postdeal implementation, deception may berevealed and trust damaged. I explore why buyersare willing to behave deceptively, despite potentialrisks to postdeal cooperation and industry reputa-tion. Finally, I outline the complex relationshipsbetween trust asymmetries, trust errors, and acqui-sition behavior and explore implications for devel-oping a broader theory of trust asymmetry in interor-ganizational transactions.

Screening: Emergence of Trust Asymmetries

For both buyers and sellers, the acquisition pro-cess began with the decision to pursue some formof partnership with another firm. Firm leadersviewed partnerships as opportunities to obtaintechnologies, products, and expertise more quicklythan they could be developed internally. As a busi-ness development executive at Checkmate com-mented, “It is all about timing. It is like a race inthis market.” Having decided to seek a partnership,firm leaders faced two intertwined, and often si-multaneous, sets of decisions: choosing the bestform of partnership, and choosing the best partner.

Forms of partnership. Although partnershipscan take many forms, leaders of both buyers andsellers focused their initial decision making on thebroad choices of acquisition or alliance. Prior workhas proposed several theoretical explanations forfirms’ decisions to acquire rather than ally (for re-views, see Schilling and Steensma [2002], Villa-longa and McGahan [2005], and Wang and Zajac[2007]), and these theories have differing implica-tions for the role of trust in acquisitions. One ex-planation draws upon transaction cost economics(Williamson, 1975, 1985), focusing on a firm’s needto minimize opportunistic behavior by transactionpartners. If concerns over opportunism are rela-tively low, alliance is considered more efficientthan acquisition (Alston & Gillespie, 1989; Schill-

ing & Steensma, 2002). However, alliances mayenable partners to misappropriate knowledge(Steensma & Corley, 2000), particularly in technol-ogy-intensive industries (Villalonga & McGahan,2005). In addition, alliances often require renegoti-ation at a later date, subjecting a firm to “small-numbers bargaining” and possible exploitation byits partner (Pisano, 1990). Acquisition avoids bothproblems, since it provides the acquirer with theability to monitor and control the acquired organi-zation and to redirect its activities without engag-ing in renegotiation. Therefore, if the risk of oppor-tunism is high, transaction cost arguments favoracquisition over alliance.

A second explanation for the choice between al-liances and acquisitions draws from real optionstheory (Folta & Miller, 2002; McGrath, 2000). Alli-ances may offer firms greater flexibility since theyare easier to reverse than acquisitions, yet still offerthe larger firm the option of later acquiring thetarget (Kogut, 1991). Such flexibility is particularlyimportant if there is uncertainty regarding whethera technology will work or will have commercialsuccess (Steensma & Corley, 2001).

A third theoretical explanation for firms’ choicebetween acquisition and alliance draws on the re-source-based (Wernerfelt, 1984) and knowledge-based (Grant, 1996) views of the firm. These per-spectives focus on creating sustainable competitiveadvantage and suggest that acquisitions offer twoadvantages over alliances. First, the hierarchicalcontrol resulting from an acquisition may promotefaster and more effective coordination of knowl-edge-based resources across multiple individuals(Conner & Prahalad, 1996). Second, acquisitionprovides the buyer with exclusive access to thetarget’s technology and expertise, providing thebuyer with a resource that is unique and difficult toimitate (Kale & Puranam, 2004). In contrast, evenan exclusive alliance leaves open the possibilitythat a partner could eventually be acquired by acompetitor of the larger firm.

To the extent that acquisitions are motivated bytransaction cost concerns, we might expect buyersto be likely to distrust their targets. In contrast, realoptions and resource-based explanations for acqui-sition versus alliance decisions have no clear im-plications for whether trust would or would not bepresent in an acquisition (Conner & Prahalad,1996). In the current study, both transaction costand real options explanations received some lim-ited support. Harbor’s leaders expressed a transac-tion cost logic for choosing between alliance andacquisition, while Picasso’s leaders expressed areal options logic, indicating that alliances and mi-nority investments were useful for exploring uncer-

442 JuneAcademy of Management Journal

TABLE 2Reasons for Acquisition vs. Alliance

Buyer Buyer Rationale Illustrative Quotes SellerSeller

Rationale Illustrative Quotes

Picasso Closer coordination “This market was going tobe strategic for us. Weneeded to have a fullset of products in our

Monet Closercoordination,Signaling

Acquisitions allow closer coordination.“Alliances don’t work very well inour industry. Partnerships just don’tseem to work very well.” (CEO).

portfolio. . . . You needto have the technologyin-house so that youcan provide an end-to-end solution. You can’tdo that with a partner’sproduct.” (VP, businessdevelopment)

Alliances don’t establish credibility aseffectively as acquisition: “[Customers]were not willing to bet their networkon a 100 person start-up.” (CEO)

North Block competition “They had money from[our competitor] on thetable. [Our competitor]was the one we didn’twant to see on thetable. . . . We had theinterest in keepingcompetition out.” (headof business unit)

Rocket Closercoordination

Alliances would not provide sufficientcoordination of manufacturing andinventory: “As time went on,acquisition became more likely becausewe were a box company, which meanswe would have to manage inventory, asales channel and manufacturing,which would get to be a problem whenwe turned up the volume.” (CEO)

Armor Block competition “We tripped over the factthat one of ourcompetitors wasactually in the midst ofattempting to do anacquisition of them. . . .We can’t let thishappen.” (VP, businessdevelopment)

Trend Blockcompetition

Wanted to ensure that Armor did notpartner with a competitor instead: “Ithink if we had not been acquired byArmor, they would have acquiredsomeone else. And maybe it would bea company that was a year behind usin technology, but with Armor’sbacking in the market, having the besttechnology isn’t always the mostimportant thing . . . we could easilylose just because somebody else had astronger arm.” (VP, services)

Harbor Limit opportunism,blockcompetition

“If we help [alliancepartner] grow theirbusiness are we lockedin, now they’re themarket leader and we’velost all power? . . . Ourcompetitor called themand said they’d pay lotsmore money, so ourpartner went over tothem.” (M&A manager)

Isle Blockcompetition

Wanted exclusive access to Harbor’sresources. Acquisition would tieHarbor to Isle, ensuring Harbor wouldnot partner with one of Isle’scompetitors instead: “Basically,whoever could get Harbor was going tobe automatically the leader in thespace. . . . So that was what drove ourdecision making.” (VP, businessdevelopment)

Karma Closer coordination “Our first attempt was tosign partnerships with allthese guys. . . . What westarted to realize was thatbecause our customerswere purchasers ofsoftware, the natural thingwas to have a combinedsystem. . . . We startedlooking at the marketplaceto see if there is acompany we couldacquire.” (CEO)

Concept Closercoordination

Combining the firms ensured that theproducts would be integrated andcompatible. This was desirablebecause customers typically neededboth products: “Every time we sold acopy of our software, we had to sell acopy of theirs, or something like it.”(VP, business development)

Continued

2009 443Graebner

tain technologies without the commitment of anacquisition. No other firms mentioned either trans-action cost or real options rationales for choosingacquisition rather than alliance. Table 2 summa-rizes the rationales for the studied acquisitions.

As in other research on technology acquisitionsduring this time period (Uhlenbruck, Hitt, & Sema-deni, 2006), resource- and knowledge-based per-spectives played a more prominent role in acquir-

ers’ decisions. The desire to keep a target’s skillsand expertise out of the hands of competitors was amotivator for five of the eight acquirers. A vicepresident at Craze explained, “We’ve created aportfolio of the best companies. . . . We’ve acquiredthe best companies off the market, so no one elsecould.” A need for closer coordination also moti-vated buyers to seek acquisition rather than alli-ance. A business development executive at Picasso

TABLE 2(Continued)

Buyer Buyer Rationale Illustrative Quotes SellerSeller

Rationale Illustrative Quotes

Craze Block competition “There is so much premiumplaced on first-moveradvantage in thisspace. . . . We’ve created aportfolio of the bestcompanies. . . . We’veacquired these companiesoff the market, so nobodyelse could. . . . We’resetting the direction forour competitors.” (VP,M&A)

Fastlane Signaling Alliances don’t establish credibilitywith customers. “In the telecomindustry, scale is tremendouslyimportant. . . . With size comes theperception of reliability, thepossibility of better terms andconditions on deals, and to getinto transactions that you wouldotherwise not be able to get into,and attract money at valuationsthat are exceptionally better.”(CEO)

Ciao Signaling “We want to do enough[acquisition] deals nowthat prove to themarketplace that we’reserious . . . and we’re notjust doing businessdevelopment deals. Wethink the market sees rightthrough businessdevelopment deals. . . .The acquisition of Goalieput a stake in the ground:we can acquire companies,we can integratecompanies, we know howto think about synergisticbusinesses.” (venturecapitalist/board member)

Goalie Closercoordination

Alliances do not promote the samedegree of coordination: “Whenyou’re just a partner withsomeone, in many ways, althoughyou go into the partnership sayingboth companies are going to get alot from it, both parties almost putin the minimum amount, justbecause they have so many otherpartnerships, and it’s hard toreally maintain them. But whenyou really have a team that’sworking together on a daily basis,it becomes different.” (VP,business development)

Checkmate Block competition “We believe that to thewinner go the spoils inthese markets. We will notenter a market in whichwe think we will not bethe leader. . . . Who thecompetition is matters. Ifyou have the opportunityto acquire someone who isthe market leader, youhave improved your timeto market and you havetaken out a potentialcompetitor. So that is areason for acquisition.”(CEO)

Spur/Prime

Closercoordination

“It was clear that it would bedifficult for us to work with[multiple companies] in as close arelationship as we needed to. . . .You have to ally with one andpick the best one and make themarriage work. The logicalextension [is] to be acquired byone of them.” (Spur CEO)

444 JuneAcademy of Management Journal

reasoned, “This market was going to be strategic forus. We needed to have a full set of products in ourportfolio. . . . You need to have the technology in-house so that you can provide an end-to-end solu-tion. You can’t do that with a partner’s product.”

Sellers also played an important role in the de-cision to engage in an acquisition rather than analliance. Like buyers, sellers viewed acquisition asa means to achieve closer coordination and to en-sure their partners did not combine with competi-tors instead. An executive at Isle explained, “Basi-cally, whoever could get Harbor was going to beautomatically the leader in the space. . . . So thatwas what drove our decision making.” In addition,both buyers and sellers mentioned that acquisitionsplayed a signaling role that could not be fulfilled byan alliance. Buyers viewed acquisitions as a signalto financial analysts that their firms were able toaggressively enter new markets. A board member atCiao reasoned, “The market sees right through busi-ness development deals. . . . The acquisition ofGoalie put a stake in the ground: we can acquirecompanies, we can integrate companies, we knowhow to think about synergistic businesses.” Sellersviewed merging with a larger firm as signaling scaleand credibility to potential customers in a way thatalliances could not.

In sum, these acquisitions were primarily moti-vated by resource-based and signaling concerns,and only secondarily by transaction cost logic.Thus, the decision to participate in an acquisitionversus an alliance was not in itself an indication ofdistrust. Nonetheless, as discussed below, clearpatterns of trust and distrust began to emerge asbuyers and sellers evaluated the pros and cons ofspecific partners.

Choice of partners. In tandem with decidingwhether acquisition or alliance was more attrac-tive, firm leaders evaluated specific partners. Bothbuyers and sellers often considered many possiblepartners. A leader at a seller, Concept, recalled,“We had a list of people we thought would be goodcandidates to get acquired by. . . . Somebody knowssomebody, that sort of thing.” Both buyers andsellers narrowed their lists of potential partners onthe basis of strategic fit, including such character-istics as product line complementarity and technol-ogy platform similarity. For sellers, however, trust-worthiness was also an important criterion forscreening partners. Potential buyers were favored ifthey were perceived as trustworthy and were elim-inated if perceived as not trustworthy. Table 3Asummarizes the role of trust in sellers’ screening ofbuyers. Sellers based their judgments of trustwor-thiness on prior direct relationships, includingfriendships and business partnerships; shared

third-party ties; industry reputation; and impres-sions formed during initial partnership-relatedconversations.

For example, Monet’s leaders favored one buyer,Picasso, because of its industry reputation for trust-worthiness. According to Monet’s chief financialofficer, “Screwing companies is not Picasso’s rep-utation.” Conversely, Monet’s leaders refused toconsider acquisition by a potential buyer that theydid not trust, as Monet’s CEO explained:

We have the same board chairman as they do, butwe didn’t like their CEO. He’s dishonest. He tries tonegotiate deals with employees behind the backs ofinvestors. He is just not somebody our managementteam wanted to do business with.

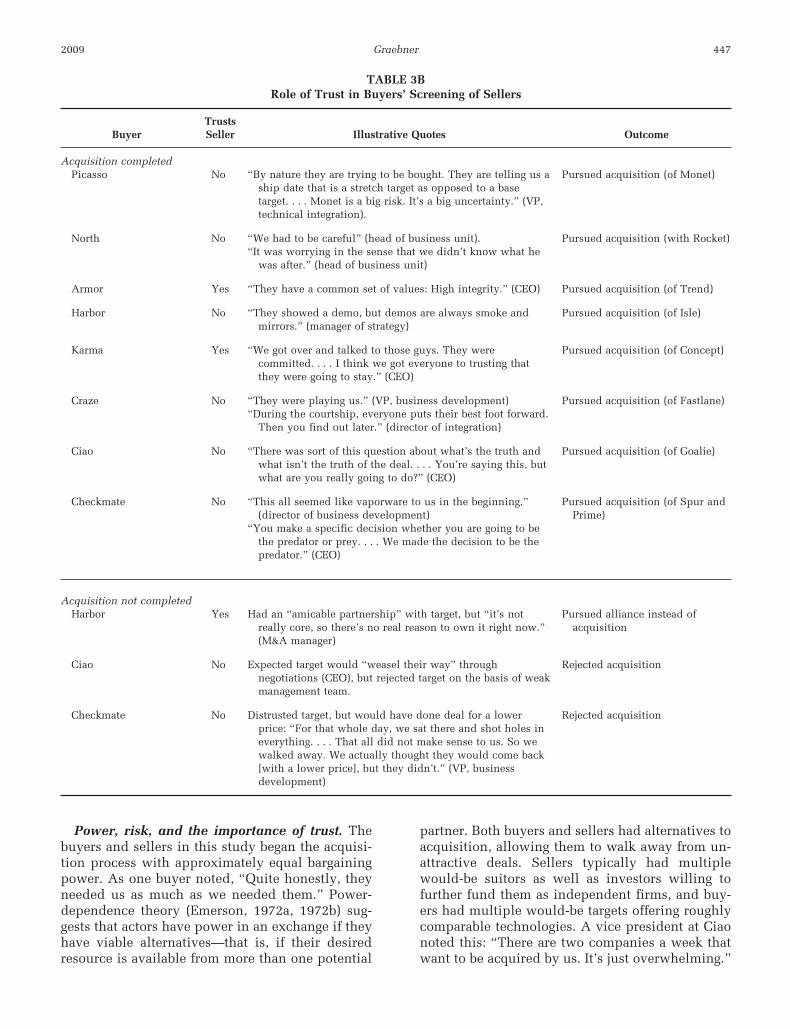

Monet was not unusual. Eleven of the 12 sellers,including both management-controlled and inves-tor-controlled firms, indicated that trust was a sig-nificant criterion for screening buyers. If a sellerdistrusted a buyer, talks ended quickly. Sellers whodistrusted all of the buyers approaching them sim-ply rejected all offers and remained independent.The CEO of Evergreen explained why she rebuffedall of her company’s potential suitors thus: “Wewere really suspicious of them. We trusted themzip.”

Buyers did not demonstrate a reciprocal concernfor the trustworthiness of sellers, however. Table3B summarizes the role of trust in buyers’ screeningof sellers. Although buyers were not acquiring tar-gets because of distrust per se, lack of trust was notviewed as a reason to eliminate a target, either. Sixof the eight buyers expressed distrust in their even-tual targets. Buyers suspected these sellers of hid-ing their motives, exaggerating the state of theirtechnology development, and secretly negotiatingwith other parties. Typical buyer comments includ-ed: “This all seemed like ‘vaporware,’” “Theyshowed a demo, but demos are always smoke andmirrors,” and “They were playing us.” Nonethe-less, buyers were willing to acquire these targets.

Why might buyers and sellers assess the impor-tance of trust in acquisitions so differently? Onepotential explanation is that buyers chose to ac-quire precisely because they distrusted the target.However, as noted earlier, fear of opportunism wasnot the primary motivator for these acquisitions. Asecond explanation is that sellers were younger,less experienced firms, and perhaps were more na-ıve than buyers about acquisitions. These distinc-tions likely had an impact, but the data suggestdisparities in experience cannot be the entire ex-planation. First, both seasoned (e.g., Picasso) and

2009 445Graebner

novice (e.g., Harbor) acquirers were willing to ne-gotiate with distrusted targets. Moreover, althoughno selling firm had previously been acquired, manyindividual selling firm leaders had experience withacquisitions at other firms. Yet both more- and less-experienced selling firm leaders valued trustwor-thiness in their buyers.

A final explanation arises from considering theroles that buyers and sellers have in the acquisition

process, the risks that are involved, and the shift inpower that occurs after deals close. In the course ofan acquisition, sellers lose power while buyers gainpower. This asymmetry is an inherent feature ofacquisitions, regardless of the motivation for a dealor the experience levels of either buyer or seller.This shift in power seems to have engendered buy-ers’ and sellers’ disparate views of the importanceof trustworthiness.

TABLE 3ARole of Trust in Sellers’ Screening of Buyers

SellerTrustsBuyer Illustrative Quotes Outcome

Acquisition completedMonet Yes “We totally trusted them.” (CFO) Pursued acquisition (with Picasso)

“They do what they say they’re going to do. . . . We figured thatPicasso would treat us fairly.” (CFO)

Rocket Yes “An honorable company, and ethical” (outside board member). Pursued acquisition (with North)“We got to trust them.” (CEO)

Trend Yes “Neither environment has a lot of fear or distrust. They’repretty open.” (VP, services)

Pursued acquisition (with Armor)

Isle Yes Buyer has “lots of goody-goody stuff,” is “dripping withwholesomeness.” (chief technology officer)

Pursued acquisition (with Harbor)

Concept Yes “Once you’re on his team, he will do whatever it takes to makesure you’re covered.” (VP, business development)

Pursued acquisition (with Karma)

Fastlane No “You get the feeling that they are going to take you for a ride,chip away at your value—and that leaves you exposed.”(CEO)

Pursued acquisition (with Craze)

Goalie Yes “There was a lot of good faith being shown on both sides.”(VP, business development)

Pursued acquisition (with Ciao)

“It was a good-faith agreement.” (CEO)

Spur/Prime Yes “High-integrity, tremendously honest.” (Prime CEO) [It isimportant to] “sell to the right company and their level ofintegrity and commitment.” (Prime CEO)

Pursued acquisition (withCheckmate)

“We looked each other in the eye and knew our intentions.”(Spur angel investor/board member)

Acquisition not completedMonet No “[Their CEO] is dishonest. . . . He is just not somebody that our

management team wanted to do business with.” (CEO)Rejected acquisition

Trend No “There wasn’t a trust that was building there.” (VP, services) Rejected acquisition

Junket No [Potential buyers] “had their own agendas. They wanted tohave more access to technology, have us give them ourintellectual property. . . . We were never willing to do that.”(CEO)

Pursued alliance instead ofacquisition

Evergreen No “We were really suspicious of them. We trusted them zip.”(CEO)

Rejected acquisition

Model No “For the second time in the meeting, they changed their storyvery quickly. . . . I’m going to tell them, “I don’t believe youguys.” (CEO)

Rejected acquisition

446 JuneAcademy of Management Journal

Power, risk, and the importance of trust. Thebuyers and sellers in this study began the acquisi-tion process with approximately equal bargainingpower. As one buyer noted, “Quite honestly, theyneeded us as much as we needed them.” Power-dependence theory (Emerson, 1972a, 1972b) sug-gests that actors have power in an exchange if theyhave viable alternatives—that is, if their desiredresource is available from more than one potential

partner. Both buyers and sellers had alternatives toacquisition, allowing them to walk away from un-attractive deals. Sellers typically had multiplewould-be suitors as well as investors willing tofurther fund them as independent firms, and buy-ers had multiple would-be targets offering roughlycomparable technologies. A vice president at Ciaonoted this: “There are two companies a week thatwant to be acquired by us. It’s just overwhelming.”

TABLE 3BRole of Trust in Buyers’ Screening of Sellers

BuyerTrustsSeller Illustrative Quotes Outcome

Acquisition completedPicasso No “By nature they are trying to be bought. They are telling us a

ship date that is a stretch target as opposed to a basetarget. . . . Monet is a big risk. It’s a big uncertainty.” (VP,technical integration).

Pursued acquisition (of Monet)

North No “We had to be careful” (head of business unit). Pursued acquisition (with Rocket)“It was worrying in the sense that we didn’t know what he

was after.” (head of business unit)

Armor Yes “They have a common set of values: High integrity.” (CEO) Pursued acquisition (of Trend)

Harbor No “They showed a demo, but demos are always smoke andmirrors.” (manager of strategy)

Pursued acquisition (of Isle)

Karma Yes “We got over and talked to those guys. They werecommitted. . . . I think we got everyone to trusting thatthey were going to stay.” (CEO)

Pursued acquisition (of Concept)

Craze No “They were playing us.” (VP, business development) Pursued acquisition (of Fastlane)“During the courtship, everyone puts their best foot forward.

Then you find out later.” (director of integration)

Ciao No “There was sort of this question about what’s the truth andwhat isn’t the truth of the deal. . . . You’re saying this, butwhat are you really going to do?” (CEO)

Pursued acquisition (of Goalie)

Checkmate No “This all seemed like vaporware to us in the beginning.”(director of business development)

Pursued acquisition (of Spur andPrime)

“You make a specific decision whether you are going to bethe predator or prey. . . . We made the decision to be thepredator.” (CEO)

Acquisition not completedHarbor Yes Had an “amicable partnership” with target, but “it’s not

really core, so there’s no real reason to own it right now.”(M&A manager)

Pursued alliance instead ofacquisition

Ciao No Expected target would “weasel their way” throughnegotiations (CEO), but rejected target on the basis of weakmanagement team.

Rejected acquisition

Checkmate No Distrusted target, but would have done deal for a lowerprice: “For that whole day, we sat there and shot holes ineverything. . . . That all did not make sense to us. So wewalked away. We actually thought they would come back[with a lower price], but they didn’t.” (VP, businessdevelopment)

Rejected acquisition

2009 447Graebner

Yet after the deal closed, a buyer’s and seller’srelative power would be very different. The buyertypically dominates key managerial positions aswell as the board of directors of the combined firm(Harford, 2003; Hartzell, Ofek, & Yermack, 2004;Wulf, 2004). Given their prospects of heightenedpower, buyers viewed sellers’ trustworthiness asnonessential. A leader of Craze explained that if hedid not trust a seller, Craze would simply planmore intensive postdeal intervention:

If we are to acquire this, we need to come in immedi-ately with an integration team, pour effort into beefingthis up and making it work. . . . If the motivation isthere from a revenue and market perspective, the out-look is pretty much, “You have to make it work, nomatter what.” We could have swooped in right awayand “Oh my God, this is going to be hard” and fixed it.

Sellers, however, lose power after acquisitionsclose. Sellers face the risk that buyers will imposeunwelcome practices and strategies on acquiredfirms (Jemison & Sitkin, 1986), replace acquiredmanagers, change leadership succession plans(Hartzell et al., 2004), or even close acquired firmsentirely (Santos & Eisenhardt, 2009). If a buyer haddeceived them during negotiations, the seller’s topmanagement team and employees would suffer. Avice president at Trend commented on the sense ofobligation she felt toward her employees: “You feelan incredible amount of responsibility for helpingthese employees. . . . My biggest concern was thatthey not be disregarded, that they be given goodpositions.” Similarly, the CEO of Model remarked:

When I think of [employee], I think, “He deservesthe best possible place to work that the world canpossibly give him, because he’s that kind of person.”I feel that tremendous debt of gratitude for the em-ployees. . . . I’m looking for a company that valuespeople as well as results.

Although these arguments help explain manag-ers’ preferences for trustworthy buyers, an intrigu-ing question is why sellers’ investors would sup-port such preferences. Agency theory suggests thatalthough selling firm executives might prefer atrustworthy buyer for the sake of themselves ortheir employees, investors would be concernedonly with obtaining the highest price (Jensen &Ruback, 1983).2 However, in this sample, bothmanager-controlled (e.g., Rocket, Isle, Goalie, Spur)and investor-controlled (e.g., Monet, Trend, Con-

cept, Junket) firms screened buyers on the basis oftrust. Investors in these ventures believed that onlysenior management could decide whether and towhom to sell a company. A venture capitalist andboard member in Junket, an investor-controlledfirm, commented: “This is a personal philosophyissue. I will not make any decisions for manage-ment. They have to make that call.” One reason thatventure capitalists did not want to force the handsof managers was concern about access to futureinvestment opportunities. Venture capitalists com-pete for access to attractive investments, and a neg-ative reputation among entrepreneurs could be acompetitive liability. A venture capital investor inEvergreen explained, “As a venture investor, yourreputation is part of what makes you successful,and entrepreneurs, if you do wrong by them, theyare not going to come back to work with you.”

A final question is why buyers so often distrustedtheir sellers. Assuming that concerns over oppor-tunism were not the primary reason for acquiring,there is no a priori reason why buyers would bemore likely to acquire distrusted versus trustedcompanies. The explanation seems to be twofold.First, buyers (and sellers) had a generalized distrustof most potential partners. The firms were engagedin rapidly changing and intensely competitive mar-kets. As technologies developed, adjacent marketsand products converged, and partners who beganin slightly different sectors could quickly becomecompetitors. Experimental evidence suggests thatas conflict becomes more salient, exchange part-ners are less likely to be viewed as trustworthy(Molm, Peterson, & Takahashi, 2003). Similarly,competitive industry dynamics seemed to foster a“predator or prey” mind-set that encouraged wari-ness of outside firms. Second, selling firms weregenerally younger and smaller than buyers. As aresult, buyers were somewhat more likely than tar-gets to feel that they lacked sufficient knowledge totrust their counterparts (cf. Kotha, Rajgopal, & Ven-katachalam, 2004). One buyer commented about atarget thus: “We tried to dig out information onthem. . . . But the best we could find was they wereworking at an apartment on Sand Hill Road.”

Socializing: Trust Asymmetries andConflicting Interpretations

Once a buyer and seller had identified acquisi-tion as an attractive means of partnering and iden-tified one another as attractive partners, the nextphase was typically socializing between the leadersof the two firms. In six of the eight completedacquisitions, buyer and seller leaders met infor-mally in nonoffice settings, including restaurants,

2 “[Selling firm] stockholders have no loyalty to in-cumbent managers; they simply choose the highest dollarvalue offer from those presented to them” (Jensen &Ruback, 1983: 6).

448 JuneAcademy of Management Journal

coffeehouses, a CEO’s home, and even a vacationretreat. Though acquisition was on the minds ofboth buyer and seller, the conversation topics were

much more personal, including college memories,hobbies, and life philosophies.

Buyers and sellers had distinct and often con-

TABLE 4Socializing: Differing Interpretations

Seller/Buyera Social Interaction

Seller Perception: BuildRelationship through

Honest TalksBuyer Perception: Ingratiate, Gather

Information, Gain Bargaining Advantage

Monet/Picasso Dinner at restaurant “We totally trusted them. . . . Itstarted out very low-key overdinner. We told them that wewould let them know aboutany problems. . . . The wholeprocess was friendly andopen.” (CFO)

Gather information. Initial relationshipbuilding is intended to provide informationon seller’s prospects: “The acquisition isnot preordained.” (chief technology officer)“We want the team to prove that they candeliver a product.” (VP, technicalintegration)

Rocket/North Series of meetingsat a coffeehouse

“We met off and on from Januaryto July. It was a good time forus both to learn. We werepretty open, too. We got totrust them that way. Opennessis the best policy.” (CEO)

Gather information, ingratiate. “We were justfishing information from them. . . . I thinkmy role and actions were to keep friendlyconversation open and daily contact. . . . Isat with [seller CEO] a couple of times inthe Starbucks cafe across the street andhaving conversations about life and theuniverse and everything. . . . It was just thisendless discussion. . . . It worked reallywell.” (head of business unit)

Trend/Armor Informal evening atArmor CEO’shome

On the basis of this interaction,trusted Armor enough todecline another acquisitionoffer prior to formal writtenoffer from Armor. (CEO)

Ingratiate. “What our CEO did is, he sat downwith [Trend CEO] personally. He asked himto come over later that evening and sit downand talk. I think [Trend CEO] very muchenjoyed the conversation. A very good

Disclosed a potential accountingissue to buyer early on, beforeengaging in full negotiations.(venture capitalist/boardmember)

move we made during that process was thatwe bear-hugged them at just the rightmoment. Those two days that we spentwith their people were very effective.” (VP,business development)

Concept/Karma Breakfast atrestaurant

During breakfast discussion, “Iwas being very direct andhonest.” (CEO)

Gather information. “We tried to dig outinformation on them. We’ve been a littlesecretive. It became a funny dance, a trickyone.” (CEO)

Goalie/Ciao Dinner at restaurant “We were very open andhonest.” (VP, businessdevelopment)

Gain bargaining advantage. Socialized tocircumvent seller’s financial advisors: “Imet with them on a weekend in Chicago. I

“We went to the same college,[and] it was like a ‘click.’ Helooked at me and said, ‘We’regoing to do big things.’ I said,‘I have no doubt.’” (CEO)

called her at home—I said, hey, you guyshave a few minutes, let’s talk. That waspartly because we felt that one, they weregetting bad advice, and two, we thoughtthat would just raise the price sooner orlater.” (venture capitalist/board member)

Spur/Prime/Checkmate Lunch meeting,weekend at sellerCEO’s vacationhome

“We [buyer and seller] lookedeach other in the eye andknew our intentions and feltthe certainty of that.” (Spurangel investor/board member)

Ingratiate. “I had to get his affection for thisdeal. They arranged a lunch which endedup taking four hours with me just trying towin him over on the deal. . . . He wantedSpur to run its own course, to reach a

“Conversations were over cigarson my deck. They were alwaysfriendly.” (Prime CEO)

billion dollars someday. . . . I had to makehim think we could pull this off. Once I gothim on board, it made the whole deal a loteasier.” (CEO)

a Cases not listed (Fastlane/Craze and Isle/Harbor) did not involve social interaction prior to the signing of letters of intent.

2009 449Graebner

flicting interpretations of these social interactions.Sellers viewed socializing through the lens of trustformation, and they perceived social interaction asbuilding deeper relationships through honest ex-change of information. Buyers viewed the sameevents through the lens of bargaining and saw so-cial interaction as a way to gain influence oversellers. As a result, the disparity between buyers’and sellers’ views of one another’s trustworthinessgrew. At the same time, socializing influenced bothparties’ emerging beliefs regarding whether theywere trusted by their counterparts. Firm leaders’views of whether their counterparts were trusting,as well as trustworthy, played an important role inshaping subsequent behavior, particularly deceit.Table 4 presents case information and exemplaryquotations about socializing and its interpretation.

Deepening of sellers’ trust. For sellers, socializ-ing was an opportunity to deepen trust by develop-ing sincere personal relationships with buyers. Forbuyers, informal interaction was an opportunity togain bargaining leverage by gathering information,engaging in ingratiation, and isolating sellers fromtheir legal and financial advisors. Trend and itsbuyer, Armor, offer an example. Early in the twofirms’ acquisition talks, Armor’s CEO invitedTrend’s CEO to his home for an evening. An Armorvice president observed that the conversationstrayed from acquisition: “[The CEOs] just shotthe s—. We didn’t talk much about the company.”On the basis of this personal interaction, Trend’sleaders trusted Armor sufficiently to refuse an at-tractive offer from a competing bidder, even beforereceiving a formal written offer from Armor’sboard. Armor’s leaders, however, viewed socializ-ing with Trend’s CEO as a negotiating tactic in-tended to prevent Trend from accepting an acqui-sition offer from Armor’s biggest competitor.Armor’s vice president of business developmentexplained:

We tripped over the fact that one of our competitorswas actually in the midst of attempting to do anacquisition of them. I called our CEO and said, “Getyour butt down here! This company is off the chartscompared to everything else we’ve looked at. Wecan’t let this happen.” What our CEO did, which iswhat he does so well, is he sat down with [Trend’sCEO] personally. They spent the afternoon together.And then he asked [Trend’s CEO] to come over laterthat evening and sit down and talk with him. Wespent the rest of the evening talking about thingsother than the acquisition. We talked about his as-pirations, our aspirations. I think [Trend’s CEO]very much enjoyed the conversation.

The vice president regarded this socializing, or“bear hugging,” as an excellent persuasion tool:

It stood out as a very good move that we made. We“bear-hugged” them at just the right moment. Thosetwo days that we spent with their people were veryeffective. Slowly but surely, the management beganrealizing they didn’t want to work for the otherbuyer.

Fortunately for Trend’s leaders, Armor’s state-ments to Trend during the socializing process wereessentially accurate. This was not true for otherbuyers. Most buyers neither expected sellers to betrustworthy during social interactions, nor felt ob-ligated to be trustworthy themselves. An illustra-tion of this pattern is the case of Rocket and North.Rocket was in the process of raising a round ofventure capital financing when approached byNorth about a potential partnership, possibly in-cluding an acquisition. Rocket’s CEO and North’sbusiness unit head began a series of informal meet-ings at a nearby coffeehouse. Rocket’s CEO viewedthese talks as an honest exchange of informationthat built a personal relationship and reinforced histrust in North. He recalled:

We met off and on from January to July. It was agood time for us both to learn. We were pretty open,too. We got to trust them that way. We told them wewere on an IPO track and talking with venture cap-italists. Openness is the best policy.

North’s representative felt quite differentlyabout the meetings, saying, “We were just fishinginformation from them.” He explained that heviewed the coffeehouse sessions as a way to im-prove North’s bargaining position by convincingRocket not to take additional venture capital in-vestment, which would have increased Rocket’svaluation. As a stalling tactic, he intentionallymisled Rocket’s CEO by suggesting that Northwould be willing to provide capital to Rocket asan independent firm:

That was a tricky time. [Rocket] had some [venturecapital] term sheets on the table. The companywould have been more expensive after VCs got in.North pretended [we were] interested in throwing in$5 to $10 million for a VC round. That was theofficial story. I think my role and actions were tokeep friendly conversation open and daily contact. Iwas making sure they didn’t sign the VC stuff. I satwith [Rocket CEO] in the Starbucks cafe having con-versations about life and the universe and every-thing. It was this endless discussion.

North’s representative concluded that the infor-mal conversations had “worked really well” inpersuading Rocket to decline financing and pur-sue acquisition.

Perceptions of counterpart’s trust. In addition toasymmetrically deepening sellers’ trust in their

450 JuneAcademy of Management Journal

TABLE 5Buyers’ and Sellers’ Actual and Perceived Trusta

Seller Buyer

BuyerTrustsSeller

(Table 3B)

SellerBelieves

It IsTrusted

by Buyer Illustrative Evidence

SellerTrustsBuyer

(Table 3A)

BuyerBelieves

It IsTrustedby Seller Illustrative Evidence

Monet Picasso No Yes Believed that buyerresponded to seller CEO’ssignals regarding fairnessand equity: “[Our CEO]wouldn’t violate anagreement. . . . Picassounderstood exactly whathe was saying.” (sellerCFO)

Yes Yes Buyer believed that seller trustedthem to follow through onnonbinding agreement: “Thereis a well-understood socialcontract in place.” (buyer chieftechnology officer/boardmember)

Rocket North No Yes Believed buyer trusted sellerbecause buyer seemed todisclose sensitiveinformation: “[Buyerexecutive] probably toldus more than he shouldabout their businessstrategy and how we fitin.” (seller CEO)

Yes No “I don’t believe that [seller] wasnaıve that nothing was goingon.” (buyer head of businessunit)

Trend Armor Yes Yes Believed that buyer wouldnot acquire a companythey didn’t trust: “Armor’sphilosophy is that culturecomes first. . . . Culturallythe companies were verysimilar. . . . Neitherenvironment has a lot ofdistrust. They’re prettyopen environments.”(seller VP, services)

Yes Yes Buyer believed seller was willingto turn down higher competingoffer because distrustedcompetitor and trusted Armor.“They were quite worriedabout working for the othercompany.” (buyer VP, businessdevelopment)

Isle Harbor No No Believed buyer would notagree to alliance, ratherthan acquisition, becausebuyer did not trust sellerand wanted total control.“They felt like just doinga partnership wasn’t goingto be strong enough, bothin terms of control and ifthey did something andwe did something else,they could lose thepartnership.” (seller VP,business development)

Yes Yes Believed seller accepted buyer’sstatements at face value:“[Seller] thought they wereselling just a normal businessdevelopment deal. . . . Theulterior motive I had was that Ithought we probably wanted tobuy them.” (buyer manager ofstrategy)

Concept Karma Yes No “It got a little uncomfortableat one point, I remember,because I asked sometough questions . . . and Ithink maybe that was oneof the reasons why theywere nervous about me.”(seller CEO)

Yes No Believed seller distrusted thembecause Karma had backed outof previous negotiations: “Wehad to tell them that as oftoday, we will not have anymore acquisition discussions.. . . I think they were prettypissed off at us because we hadbrought them along for twomonths.” (buyer CEO)

Continued

2009 451Graebner

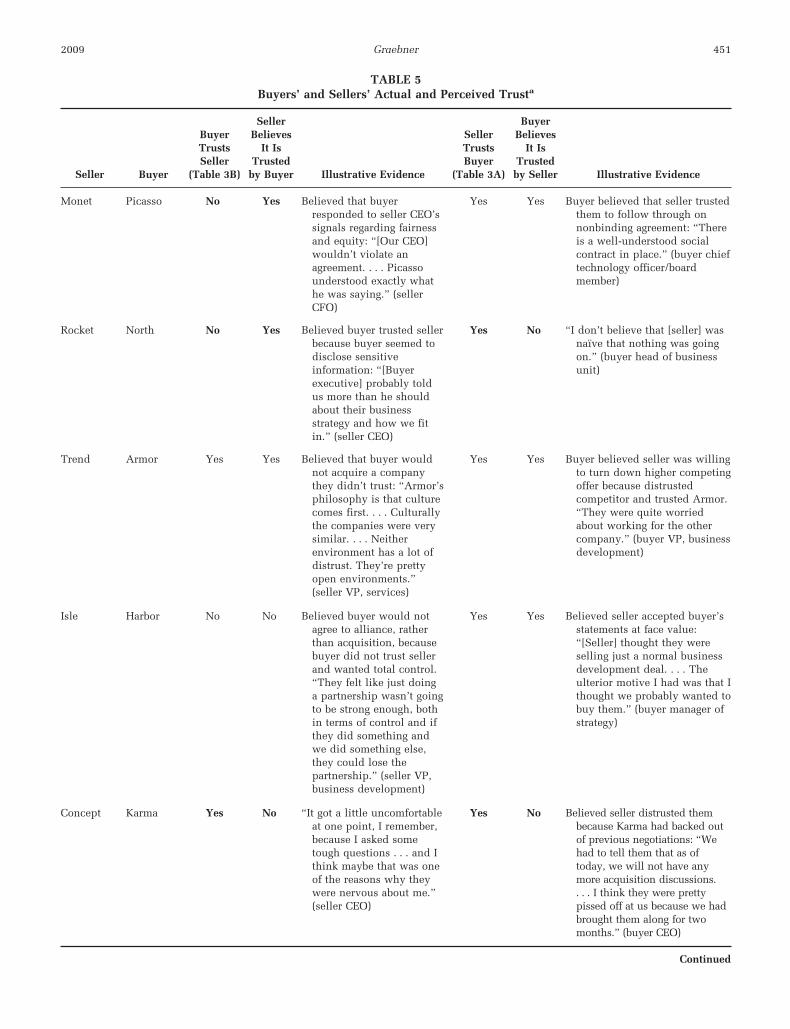

buyers, socializing provided an opportunity forboth buyers and sellers to develop beliefs regardingwhether they were trusted by their counterparts.Surprisingly, these assessments were often wrong.Table 5 contrasts the actual and perceived trust ofboth parties. Five sellers (Monet, Rocket, Concept,Goalie, and Prime) misread whether their buyerstrusted them. Four of these five sellers believedthey were trusted by buyers, when the opposite wastrue. Two buyers (North and Karma) also madeerrors. In both cases, buyers mistakenly believedthat sellers did not trust them.

In the case of Rocket and North, both buyer andseller were mistaken. Their informal interactionat the coffeehouse left Rocket’s CEO feeling thatNorth’s leader was demonstrating his trust inRocket by being very forthcoming. Rocket’s CEOcommented that North’s leader “probably told usmore than he should about their business strategyand how we fit in.” In fact, North’s representativedistrusted Rocket’s CEO, commenting, “We hadto be careful . . . it was worrying that we didn’tknow what he was after.” For his part, North’s

leader erroneously believed that Rocket’s CEOviewed him with skepticism and knew that hewas not being entirely honest. Although Northpretended to be interested in providing venturecapital rather than acquiring Rocket, North’sleader believed that Rocket’s CEO was savvyenough to know better: “I don’t believe that he wasnaıve enough [to think] nothing was going on.”

Whether correct or not, leaders’ views of theother firm’s trust, as well as its trustworthiness,influenced leaders’ behavior in important ways.Specifically, leaders’ views of whether theircounterparts were trustworthy and/or trustingshaped decisions regarding whether to behavedeceptively. This influence became particularlyapparent during the next phase of the acquisitionprocess.

Agreeing in Principle: Trust, Distrust,and Deception

Agreeing in principle, which often followedquickly after socializing, involved signing a non-

TABLE 5(Continued)

Seller Buyer

BuyerTrustsSeller

(Table 3B)

SellerBelieves

It IsTrusted

by Buyer Illustrative Evidence

SellerTrustsBuyer

(Table 3A)

BuyerBelieves

It IsTrustedby Seller Illustrative Evidence

Fastlane Craze No No Seller interpreted all buyers’extensive informationrequests as signs ofdistrust: “The enormousamount of hours that youhave to spend to begin thedue diligence, all thecalls.” (seller venturecapitalist/board member)

No No Believed seller had chosen to usean investment bank becausethey did not trust potentialbuyers. “It’s always nicerwhen there’s no investmentbanker involved.” (buyer VP,business development)

Goalie Ciao No Yes “You start to learn, ‘Hmmm,I trust Goalie, they’redoing a kick-ass job.’ I’mguessing that’s what[buyer CEO] is thinking.”(seller CEO)

Yes Yes ‘They really trusted [our boardmember]. . . . to some extentthey trusted him more thanthey trusted their ownfinancial advisors.” (buyer VP,business development)

Spur/Prime Checkmate No Yes Seller firm leaders believedbuyer was willing to trusttheir statements: “Theykind of took it on goodfaith from ourconversation.” (PrimeCEO)

Yes Yes Believed seller trusted thembecause seller agreed to extendno-shop for a long period.“The point was that Spur’sboard had to believe thatCheckmate was a goodcompany. . . . That was thefirst thing they wanted to talkabout.” (buyer VP, businessdevelopment)

a Bold indicates examples in which there are trust errors (i.e., a “yes” and a “no”).

452 JuneAcademy of Management Journal

binding acquisition letter of intent, or term sheet,3

outlining the proposed deal. Signing a letter ofintent could be a risky matter, particularly for sell-ers. Term sheets typically include a legally binding“no-shop” clause that requires the two firms tonegotiate exclusively until either the deal closes ora specified time period expires. If the acquisitionfails to come to fruition, both buyer and sellercould lose valuable time in their searches for suit-able partners. For sellers, an even more criticalissue was delays in raising additional capital. Sell-ers often put fundraising plans on hold during ac-quisition talks, which put their solvency at risk ifthe buyer withdrew from the deal.

However, because most sellers trusted their buy-ers, they viewed an agreement in principle as tan-tamount to a completed deal. Sellers expected thatonce a letter of intent had been signed, the remain-ing details were formalities. A Goalie founder ex-plained that he had no doubt that Ciao would fulfillits promise to complete the acquisition: “Eventhough we [still] had to talk to the lawyers a lot, webasically had agreed to compromise on all the is-sues. If you can trust them, you feel like they’regood people, and all of the small little details willbe worked out.”