cautionary statement: etango-8 project scoping study · 2 commenting on the etango-8 scoping study...

TRANSCRIPT

Cautionary Statement: ETANGO-8 PROJECT SCOPING STUDY

The Scoping Study referred to in this ASX release has been undertaken for the purpose of initial evaluation of a

potential 8Mtpa development of the Etango uranium deposit, owned by Bannerman Resources Limited (Bannerman).

It is a preliminary technical and economic study of the potential viability of a smaller initial-scale configuration of the

Etango Project, which has previously been the subject of Definitive Feasibility Study at a larger 20Mtpa development

scale. The Scoping Study outcomes, production target and forecast financial information referred to in this release

are based on low accuracy level technical and economic assessments that are insufficient to support estimation of

Ore Reserves. While each of the modifying factors was considered and applied, there is no certainty of eventual

conversion to Ore Reserves or that the production target itself will be realised. Further exploration and evaluation

work and appropriate studies are required before Bannerman will be in a position to estimate any Ore Reserves or to

provide any assurance of an economic development case. Given the uncertainties involved, investors should not

make any investment decisions based solely on the results of the Scoping Study.

Of the Mineral Resources scheduled for extraction in the Scoping Study production plan, approximately 13.7% are

classified as Measured, 83.9% as Indicated and 2.4% as Inferred. There is a low level of geological confidence

associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the

determination of Indicated Mineral Resources or that the production target itself will be realised. Inferred Resources

comprise less than 2.2% of the production schedule in the first year of operation and an average of less than 2.1%

over the first three years of operation. Bannerman confirms that the financial viability of the Etango Project is not

dependent on the inclusion of Inferred Resources in the production schedule.

The Mineral Resources underpinning the production target in the Scoping Study have been prepared by a competent

person in accordance with the requirements of the JORC Code (2012). The Competent Person’s Statement is found

in Appendix A of this ASX release. For full details of the Mineral Resources estimate, please refer to Bannerman

ASX release dated 11 November 2015, Outstanding DFS Optimisation Study Results. Bannerman confirms that it is

not aware of any new information or data that materially affects the information included in that release. All material

assumptions and technical parameters underpinning the estimates in that ASX release continue to apply and have

not materially changed.

This release contains a series of forward-looking statements. Generally, the words "expect," “potential”, "intend,"

"estimate," "will" and similar expressions identify forward-looking statements. By their very nature forward-looking

statements are subject to known and unknown risks and uncertainties that may cause our actual results, performance

or achievements, to differ materially from those expressed or implied in any of our forward-looking statements, which

are not guarantees of future performance. Statements in this release regarding Bannerman’s business or proposed

business, which are not historical facts, are forward-looking statements that involve risks and uncertainties, such as

Mineral Resource estimates, market prices of metals, capital and operating costs, changes in project parameters as

plans continue to be evaluated, continued availability of capital and financing and general economic, market or

business conditions, and statements that describe Bannerman’s future plans, objectives or goals, including words to

the effect that Bannerman or management expects a stated condition or result to occur. Forward-looking statements

are necessarily based on estimates and assumptions that, while considered reasonable by Bannerman, are inherently

subject to significant technical, business, economic, competitive, political and social uncertainties and contingencies.

Since forward-looking statements address future events and conditions, by their very nature, they involve inherent

risks and uncertainties. Actual results in each case could differ materially from those currently anticipated in such

statements. Investors are cautioned not to place undue reliance on forward-looking statements, which speak only as

of the date they are made.

Bannerman has concluded that it has a reasonable basis for providing these forward-looking statements and the

forecast financial information included in this ASX release. This includes a reasonable basis to expect that it will be

able to fund the development of the Etango Project upon successful delivery of key development milestones and

when required. The detailed reasons for these conclusions are outlined throughout this ASX release (including

Section 16) and in Appendix B. While Bannerman considers all of the material assumptions to be based on

reasonable grounds, there is no certainty that they will prove to be correct or that the range of outcomes indicated by

the Scoping Study will be achieved.

To achieve the range of outcomes indicated in the Scoping Study, pre-production funding in excess of A$250M will

likely be required. There is no certainty that Bannerman will be able to source that amount of funding when required.

It is also possible that such funding may only be available on terms that may be dilutive to or otherwise affect the

value of Bannerman’s shares. It is also possible that Bannerman could pursue other value realisation strategies such

as a sale, partial sale or joint venture of the Etango Project. These could materially reduce Bannerman’s proportionate

ownership of the Etango Project.

No Ore Reserve has been declared. This ASX release has been prepared in compliance with the current JORC Code

(2012) and the ASX Listing Rules. All material assumptions, including sufficient progression of all JORC modifying

factors, on which the production target and forecast financial information are based have been included in this ASX

release.

For

per

sona

l use

onl

y

ABN 34 113 017 128

Suite 7, 245 Churchill Avenue Subiaco, WA 6008, Australia

T +61 8 9381 1436

F +61 8 9381 1068

bannermanresources.com.au

1

ASX Announcement

5 August 2020

ETANGO-8 PROJECT SCOPING STUDY

Bannerman Resources Limited (ASX:BMN, OTCQB:BNNLF, NSX:BMN) (Bannerman or the Company)

is pleased to advise of the completion of a Scoping Study for an 8Mtpa development of its flagship Etango

Uranium Project in Namibia (Etango-8 Project).

KEY OUTCOMES

Primary outcome of recent scaling evaluation work on Etango; provides an alternate, streamlined development model to the 20Mtpa development assessed to DFS level in 2015

Demonstrates the strong technical and economic viability of conventional open pit mining and heap leach processing of the world class Etango deposit at 8Mtpa throughput

Life-of-mine (LOM) production of 51.1 Mlbs U3O8 (48.5 – 53.7 Mlbs) with annual average production of 3.5 Mlbs U3O8 (3.4 – 3.7 Mlbs)

Forecast pre-production capital expenditure of US$254M (US$241 – 267M), delivering an attractive upfront capital intensity of approx. US$71/lb average annual U3O8 production

Life-of-mine of approx. 14 years (114.1 Mt plant feed at 232 ppm U3O8)

Average final product cash operating cost (ex-royalties) of US$37/lb U3O8 (US$36 – 39/lb)

Attractive projected economics at forecast US$65/lb U3O8 realised price:

‒ Ungeared, real, post-tax NPV8% of US$212M (US$201 – 223M)

‒ Post-tax internal rate of return (IRR) of 21.2% (20.1 – 22.3%) and payback of 3.6 years

‒ Forecast net project cashflow (post-capex, post-tax) of US$604M (US$574 – 634M)

Further upside potential from:

‒ Future life extension and/or scale-up expansion

‒ Additional processing efficiency and cost opportunities

Vast body of previous technical work enables fast-tracking of feasibility studies; all resource drilling, geotechnical, metallurgical and environmental work already complete

Heap leach process route has also been comprehensively de-risked via operation of the Etango Heap Leach Demonstration Plant

Bannerman Board has approved commencement of a Pre-Feasibility Study (PFS) with completion targeted for Q2 2021

Long-term scalability of Etango Project (up to 20Mtpa) confirmed by previous definitive level studies; provides strong optionality and leverage to upside-case uranium market

For

per

sona

l use

onl

y

2

Commenting on the Etango-8 Scoping Study results, Bannerman Chief Executive Officer,

Brandon Munro, said:

“Last year we commenced a review of various project scaling opportunities that might exist for the Etango

Project. This Etango-8 Scoping Study represents the successful culmination of that work.

“Developing the world-class Etango Project at an initial 8Mtpa throughput offers significant advantages. It

sharply reduces the upfront capital and funding hurdle compared to that associated with the original

20Mtpa Etango development evaluated in the DFS in 2012, and the DFS Optimisation Study in 2015. It

also enables us to predominantly mine shallower, higher-grade ore, which significantly reduces stripping

and lifts the average feed grade to the processing facility. The combined result is that the upfront capital

intensity of the Etango Project per pound of annual production capacity has fallen materially whilst

maintaining robust project economics.

“The Etango-8 Project is expected to deliver over 3.5Mlbs U3O8 per annum over an initial operating life of

more than 14 years. This may be a reduced scale compared with the original Etango, but it is still a world-

class uranium project and amongst the largest development projects in the sector. With a post-tax IRR

north of 20%, the Etango-8 Project delivers attractive projected investment returns on a lower initial capital,

funding and development risk profile.

“Importantly, while the Etango-8 Project provides a reduced scale of production entry, it does so without

removing the option of subsequent expansion, including to the originally envisaged 20Mtpa Etango scale.

In short, the scalability of the world class Etango resource remains robust even with a more modular

approach to development of the project.

“We are now proceeding to undertake a PFS on the Etango-8 Project. This process will benefit significantly

from the fact that the Etango Project has already been the subject of a definitive level of feasibility study,

at a larger scale, in recent years. As a result, we are targeting completion of a comprehensive PFS in Q2

2021.”

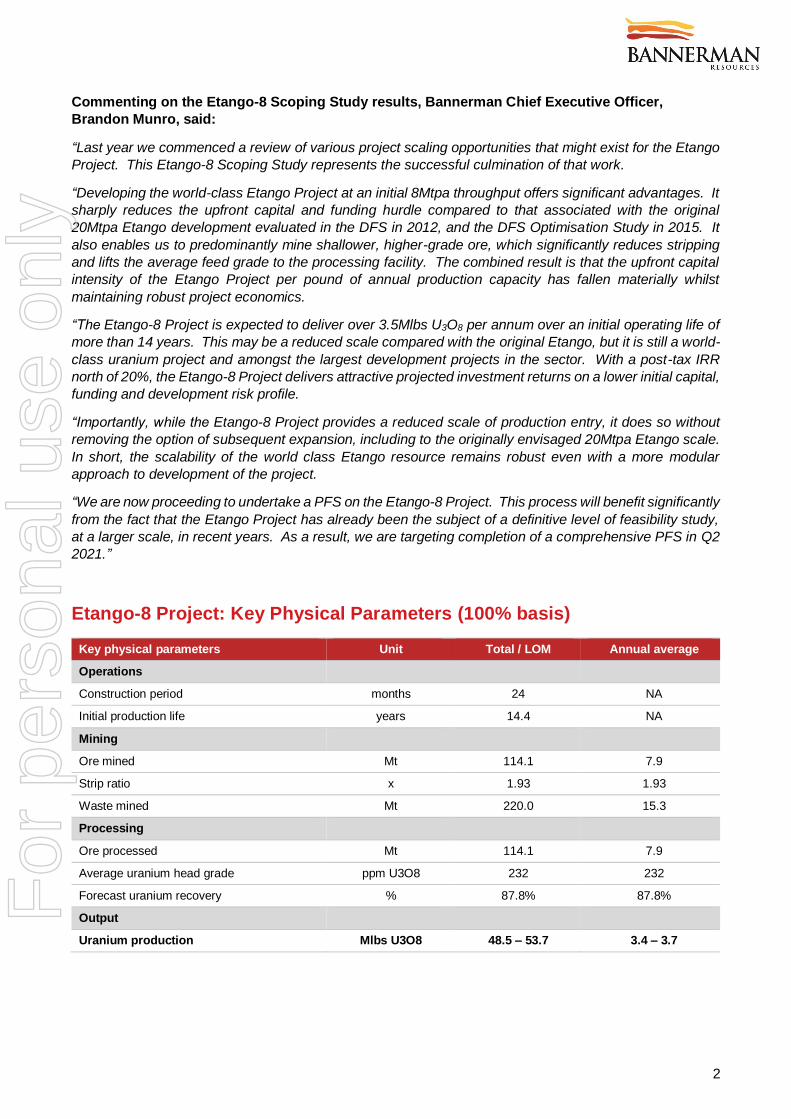

Etango-8 Project: Key Physical Parameters (100% basis)

Key physical parameters Unit Total / LOM Annual average

Operations

Construction period months 24 NA

Initial production life years 14.4 NA

Mining

Ore mined Mt 114.1 7.9

Strip ratio x 1.93 1.93

Waste mined Mt 220.0 15.3

Processing

Ore processed Mt 114.1 7.9

Average uranium head grade ppm U3O8 232 232

Forecast uranium recovery % 87.8% 87.8%

Output

Uranium production Mlbs U3O8 48.5 – 53.7 3.4 – 3.7

For

per

sona

l use

onl

y

3

Forecast mine schedule for Etango-8 Project

Forecast LOM production and final product cash operating cost (ex-royalties) for Etango-8

Project

0

50

100

150

200

250

300

350

400

450

5.0

10.0

15.0

20.0

25.0

30.0

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Min

ed G

rade (

U3O

8 p

pm

)

To

nnes (

Mt)

Material Movements and Mined Grade

Ore Waste Mined Grade (U3O8 ppm)

-

10.0

20.0

30.0

40.0

50.0

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Fin

al P

roduct C

ash O

pera

ting C

ost (U

S$/lb)

Ura

niu

m P

roduction (

U3O

8 lbs)

Uranium Production and Final Product Cash Operating Cost (excl. Levies & Royalties)

Uranium production (U3O8) Final Product Cash Operating Cost (excl Royalties & Levies)For

per

sona

l use

onl

y

4

Etango-8 Project: Key Economic Outcomes (100% basis)

Key financial outcomes Unit Total

Price inputs

LOM average uranium price US$/lb U3O8 - 65

US$/N$ N$ - 16

Valuation, returns and key ratios Range Mid point

NPV8% (post-tax, real basis, ungeared) US$M 201 - 223 212

NPV8% (pre-tax, real basis, ungeared) US$M 354 - 392 373

IRR (post-tax, real basis, ungeared) % 20.1 - 22.2 21.2

IRR (pre-tax, real basis, ungeared) % 25.5 - 28.1 26.8

Payback period (post-tax, from first production) years 3.4 - 3.8 3.6

Payback period (pre-tax, from first production) years 3.2 - 3.6 3.4

Pre-tax NPV / Pre-production capex x 1.4 - 1.5 1.5

Pre-production capital intensity US$/lb U3O8 pa capacity 67 - 75 71

Cashflow summary Range Mid point

Sales revenue (gross) US$M 3,154 - 3,486 3,320

Mining opex US$M (813 - 899) (856)

Processing opex US$M (816 - 902) (859)

G&A opex US$M (134 - 150) (143)

Product transport, port, freight, conversion US$M (53 - 59) (56)

Royalties and export levies US$M (139 - 153) (146)

Project operating surplus US$M 1,197 - 1,323 1,260

Pre-production capital expenditure US$M (241 - 267) (254)

LOM sustaining capital expenditure US$M (29 - 33) (31)

Project net cashflow (pre-tax) US$M 926 - 1,024 975

Tax paid US$M (352 - 390) (371)

Project net cashflow (post-tax) US$M 574 - 634 604

Unit cash operating costs Range Mid Point

Mining US$/t material mined - 2.56

Mining US$/lb U3O8 - 16.8

Processing US$/t ore - 7.53

Processing US$/lb U3O8 - 16.8

G&A US$/lb U3O8 - 2.8

Product transport, port, freight, conversion US$/lb U3O8 - 1.1

Total cash operating cost (ex-royalties/levies) US$/lb U3O8 35.5 - 39.3 37.4

Royalties and export levies US$/lb U3O8 2.8 - 3.0 2.9

Total cash operating cost US$/lb U3O8 38.3 - 42.3 40.3

All-in-sustaining-cost (AISC) US$/lb U3O8 38.9 - 42.9 40.9

For

per

sona

l use

onl

y

5

This ASX release was authorised on behalf of the Bannerman Board by:

Brandon Munro, Chief Executive Officer

CONTACT DETAILS:

Investors Media

Brandon Munro Michael Vaughan

Chief Executive Officer Fivemark Partners

+61 8 9381 1436 +61 422 602 720

[email protected] [email protected]

ABOUT BANNERMAN

Bannerman Resources Limited (Bannerman) is an Australian and Namibian listed uranium development

company. Its flagship asset is the world-class Etango Uranium Project located in the Erongo Region of

Namibia (Etango).

Etango has benefited from extensive exploration and feasibility activity over the past 15 years. The Etango

tenements possess a globally large-scale uranium mineral resource* of 271 Mlbs U3O8 (14.4 Mlbs

Measured, 150.2 Mlbs Indicated and 106.1 Mlbs Inferred) inclusive of the Ondjamba and Hyena satellite

deposits. A 20Mtpa development at Etango was the subject of a Definitive Feasibility Study (DFS)

completed in 2012 and a DFS Optimisation Study completed in 2015. Bannerman has also constructed

and operated a Heap Leach Demonstration Plant at Etango, which has heavily de-risked the acid leach

process to be utilised on the Etango material.

In August 2020, Bannerman completed a Scoping Study on an 8Mtpa development of Etango (Etango-8

Project). The Scoping Study has demonstrated that this accelerated, streamlined project is strongly

amenable to development – both technically and economically. A Pre-Feasibility Study on the Etango-8

Project is underway with targeted completion during 2Q 2021.

* For full details of the Mineral Resources estimate, please refer to Bannerman ASX release dated 11 November 2015, Outstanding DFS

Optimisation Study Results. Bannerman confirms that it is not aware of any new information or data that materially affects the information

included in that release. All material assumptions and technical parameters underpinning the estimates in that ASX release c ontinue to

apply and have not materially changed.

For

per

sona

l use

onl

y

For

per

sona

l use

onl

y

2

CONTENTS

1. Project overview and study introduction....................................................................................... 4

2. Study team ........................................................................................................................................ 5

3. Tenement status ............................................................................................................................... 5

4. Geology and Mineral Resource estimate ....................................................................................... 6

4.1 Local geology ............................................................................................................................ 6

4.2 Mineral Resource ...................................................................................................................... 8

5. Mining studies................................................................................................................................. 10

5.1 Pit optimisation ........................................................................................................................ 10

5.2 Mining method and schedule .................................................................................................. 10

5.3 Geotechnical............................................................................................................................ 13

5.4 Hydrogeological ....................................................................................................................... 14

6. Processing ...................................................................................................................................... 14

6.1 Metallurgical testwork .............................................................................................................. 14

6.2 Process flowsheet ................................................................................................................... 15

6.3 Processing assumptions ......................................................................................................... 16

6.4 Plant location ........................................................................................................................... 16

7. Infrastructure .................................................................................................................................. 18

7.1 On-site infrastructure ............................................................................................................... 18

7.2 Heap leach residue ................................................................................................................. 18

7.3 Power ...................................................................................................................................... 19

7.4 Water ....................................................................................................................................... 19

7.5 Roads ...................................................................................................................................... 19

7.6 Port infrastructure .................................................................................................................... 19

8. Environmental and social .............................................................................................................. 21

9. Operating costs .............................................................................................................................. 21

9.1 Mining ...................................................................................................................................... 22

9.2 Acid and other reagents .......................................................................................................... 22

9.3 Maintenance and consumables .............................................................................................. 22

9.4 Water and power ..................................................................................................................... 23

9.5 Labour costs ............................................................................................................................ 23

9.6 General and administration expenses .................................................................................... 23

10. Capital costs ................................................................................................................................... 23

11. Financial analysis ........................................................................................................................... 24

11.1 Basis of estimates ................................................................................................................... 24

11.2 Uranium market outlook and product marketing ..................................................................... 24

11.3 Economic analysis ................................................................................................................... 26

For

per

sona

l use

onl

y

3

12. Sensitivity analysis ........................................................................................................................ 28

13. Development schedule .................................................................................................................. 30

14. Project risks .................................................................................................................................... 31

15. Project opportunities ..................................................................................................................... 32

15.1 Future expansion ..................................................................................................................... 32

15.2 Processing efficiency and cost upside .................................................................................... 33

16. Reasonable basis for funding assumption.................................................................................. 33

17. Conclusions and next steps .......................................................................................................... 34

APPENDIX A: COMPETENT PERSON’S STATEMENT ......................................................................... 35

APPENDIX B: REASONABLE BASIS FOR FORWARD-LOOKING STATEMENTS ............................. 36

For

per

sona

l use

onl

y

4

1. Project overview and study introduction

The Etango Uranium Project (Etango Project) is located in the Erongo Region of Namibia, approximately

30 kilometres to the east-south-east of Swakopmund. It is positioned within a highly established uranium

mining jurisdiction, where the mining and export of uranium via the Walvis Bay deep-sea port facility has

been ongoing for over 40 years. The Etango Project is owned by Bannerman Resources Limited, through

its 95% owned subsidiary Bannerman Mining Resources Namibia (Pty) Ltd.

Figure 1 shows the location of the Etango Project in relation to surrounding uranium mines and projects,

and the towns of Swakopmund and Walvis Bay.

Figure 1: Location of the Etango Project

Planned development of the Etango Project involves bulk open pit mining of a large, relatively homogenous

uranium deposit followed by crushing, acid heap leaching, Ion Exchange (IX) with Nano Filtration (NF),

and uranium recovery into yellowcake product (U3O8).

In April 2012, Bannerman Mining Resources Namibia (Pty) Ltd (Bannerman) completed a Definitive

Feasibility Study (DFS 2012) for the Etango Project. The DFS was based on a 20Mtpa mine and heap

leach process throughput. Mine planning, engineering design and capital and operating cost estimation

was undertaken to an accuracy of ±15%.

In March 2015, Bannerman commissioned an industrial scale plant to demonstrate the heap leach

configuration and assumptions. The results of the trials demonstrated strong support for the DFS 2012

metallurgical parameters.

For

per

sona

l use

onl

y

5

In November 2015, Bannerman completed a DFS Optimisation Study (OS 2015). The OS 2015 saw a

pre-production capital cost estimate of US$793M for average life-of-mine (LOM) production of 7.2 Mlbs

U3O8 per annum at a LOM average C1 cash cost of US$38/lb.

In 2019, Bannerman commenced an evaluation of various project scaling and scope opportunities under

a range of potential development parameters and market conditions. Indicative outcomes of this work

highlighted strong potential for a scaled-down initial development of the Etango Project. As a result,

Bannerman commenced work on a Scoping Study into such a development.

This Scoping Study provides an early stage assessment of the technical and commercial viability for

development of the Etango Project at an 8Mtpa throughput rate (Etango-8 Project). Importantly, much of

this Scoping Study evaluation is heavily informed by the detailed study work undertaken across all relevant

disciplines as part of the DFS 2012 and OS 2015. This Scoping Study development also, critically,

maintains the real option of modular expansion, up to potentially the 20Mtpa scale envisaged by the DFS

2012 and OS 2015.

2. Study team

The Scoping Study team was led and managed by Bannerman personnel.

Key external contributors and consultants involved in the preparation of the Scoping Study included:

Qubeka Mining Consultants Geology review, pit inventory estimates, mine planning and financial analysis

DRA-SENET Process plant design and related infrastructure, plant capital cost estimate

A. Speiser Environmental Consultants

Environmental and social impacts and management

Genis Business Consulting External infrastructure

Nuclear Fuel Associates LLC Uranium marketing and advisory

Fivemark Partners Commercial and strategic advisory

3. Tenement status

The Etango Project is located on Mineral Deposit Retention Licence 3345 (MDRL 3345), which is owned

by the Namibian company, Bannerman Mining Resources (Namibia) (Pty) Ltd (Bannerman).

Australian Securities Exchange listed Bannerman Resources Limited owns 95% of Bannerman with the

residual 5% owned by the One Economy Foundation, a Namibian not-for-profit organisation.

MDRL 3345 provides strong and exclusive rights to tenure and the right (without obligation) to continue

with exploration or development work. It has a five-year extendable term and was granted on 7 August

2017, with an initial expiry date of 6 August 2022. The licence covers an area of 7,295 hectares.

Figure 2 below shows the boundary of MDRL 3345. For

per

sona

l use

onl

y

6

Figure 2: MDRL 3345 boundary with planned Etango development (DFS 2012)

Bannerman’s Exclusive Prospecting Licence 3345 (EPL 3345) is adjacent to MDRL 3345 (as shown in

Figure 1) and expires in April 2021.

4. Geology and Mineral Resource estimate

4.1 Local geology

Uranium mineralisation at the Etango Project is predominantly hosted by a stacked sequence of

leucogranitic bodies (generally referred to as alaskite) that have intruded the host Damara Sequence of

metasedimentary rocks on the western flank of the Palmenhorst Dome. The main mineralised bodies are

associated with the Khan Formation and the lower part of the Chuos Formation (as shown in Figure 3) but

also occur within 400 metres of the contact between the Etusis and Khan Formations (Mouillac et al, 1986).

Uranium mineralisation at Etango is defined within an approximately +5km long zone trending south-east

to north-east that dips moderately (30° to 50°) to the west (see Figure 4).

The dominant primary uranium mineral at Etango is uraninite (UO2), with minor primary uranothorite

((Th,U)SiO4) as well as some uranium in solid solution in thorite (ThO2). Minor uranium is also present in

the minerals monazite, xenotime and zircon, either as minute inclusions or in crystal lattice substitution.

Secondary uranium-bearing minerals observed include coffinite and betauraniphane (both uranium silicate

minerals).

Approximately 90% of logged mineralised intervals (>50 ppm U3O8) at the Etango Project occur within

alaskite (Alaskite Dominant (AD)), however not all of the alaskite is mineralised, with only about 60%

mineralised in total. Minor uranium mineralisation is also found in the metasedimentary sequences

(Alaskite Sub-Dominant (ASD)) close to the alaskite contacts, almost certainly from metasomatic alteration

and in minor thin alaskite stringers within the metasediments.

For

per

sona

l use

onl

y

7

Figure 3: Outcrop of uranium-bearing alaskite

Figure 4: Selected cross section of Etango mineralisation

For

per

sona

l use

onl

y

8

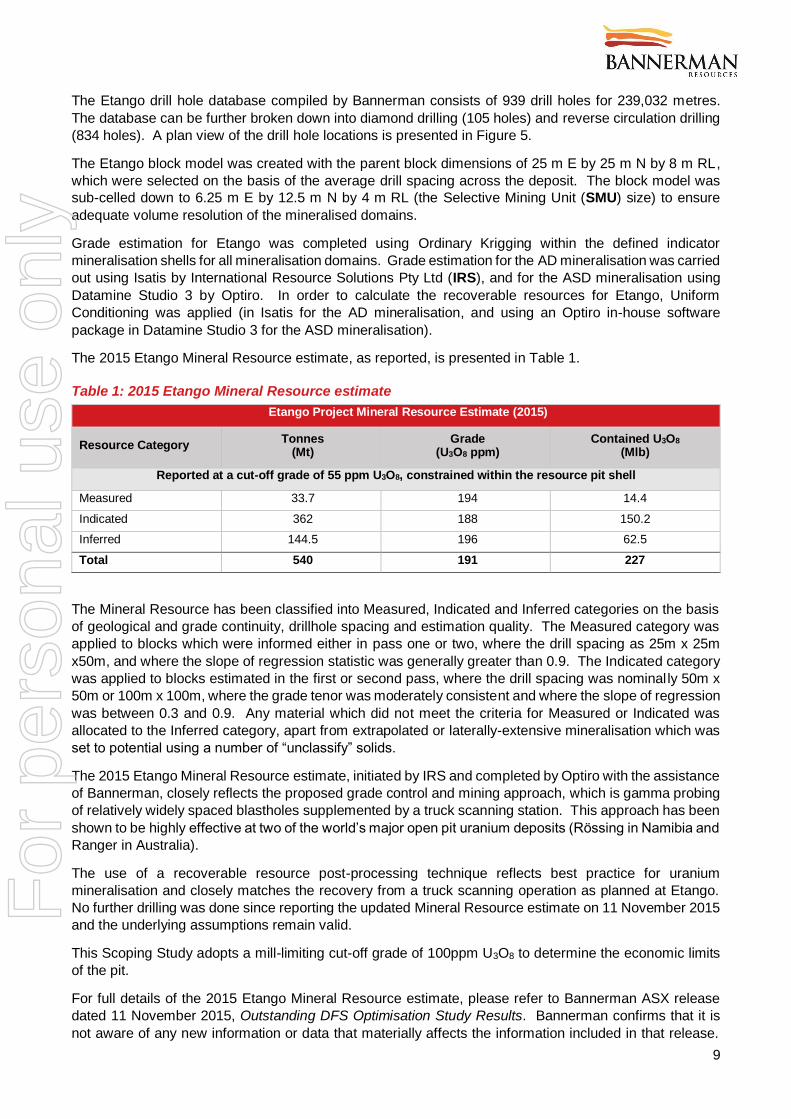

4.2 Mineral Resource

During 2015, and as part of the OS 2015, Bannerman completed an update of the Mineral Resource for

the Etango Project, as released to the ASX on 11 November 2015 (2015 Etango Mineral Resource).

This included review of the previously reported DFS 2012 Mineral Resource model (completed in October

2010 by Coffey Mining) and several in-house resource estimates generated using Ordinary Kriging and

Multiple Indicator Kriging techniques.

The 2015 Etango Mineral Resource estimate was used for this Scoping Study.

Figure 5: Plan view of drill holes used in the 2015 Etango Mineral Resource estimate

For

per

sona

l use

onl

y

9

The Etango drill hole database compiled by Bannerman consists of 939 drill holes for 239,032 metres.

The database can be further broken down into diamond drilling (105 holes) and reverse circulation drilling

(834 holes). A plan view of the drill hole locations is presented in Figure 5.

The Etango block model was created with the parent block dimensions of 25 m E by 25 m N by 8 m RL,

which were selected on the basis of the average drill spacing across the deposit. The block model was

sub-celled down to 6.25 m E by 12.5 m N by 4 m RL (the Selective Mining Unit (SMU) size) to ensure

adequate volume resolution of the mineralised domains.

Grade estimation for Etango was completed using Ordinary Krigging within the defined indicator

mineralisation shells for all mineralisation domains. Grade estimation for the AD mineralisation was carried

out using Isatis by International Resource Solutions Pty Ltd (IRS), and for the ASD mineralisation using

Datamine Studio 3 by Optiro. In order to calculate the recoverable resources for Etango, Uniform

Conditioning was applied (in Isatis for the AD mineralisation, and using an Optiro in-house software

package in Datamine Studio 3 for the ASD mineralisation).

The 2015 Etango Mineral Resource estimate, as reported, is presented in Table 1.

Table 1: 2015 Etango Mineral Resource estimate

Etango Project Mineral Resource Estimate (2015)

Resource Category Tonnes

(Mt) Grade

(U3O8 ppm) Contained U3O8

(Mlb)

Reported at a cut-off grade of 55 ppm U3O8, constrained within the resource pit shell

Measured 33.7 194 14.4

Indicated 362 188 150.2

Inferred 144.5 196 62.5

Total 540 191 227

The Mineral Resource has been classified into Measured, Indicated and Inferred categories on the basis

of geological and grade continuity, drillhole spacing and estimation quality. The Measured category was

applied to blocks which were informed either in pass one or two, where the drill spacing as 25m x 25m

x50m, and where the slope of regression statistic was generally greater than 0.9. The Indicated category

was applied to blocks estimated in the first or second pass, where the drill spacing was nominal ly 50m x

50m or 100m x 100m, where the grade tenor was moderately consistent and where the slope of regression

was between 0.3 and 0.9. Any material which did not meet the criteria for Measured or Indicated was

allocated to the Inferred category, apart from extrapolated or laterally-extensive mineralisation which was

set to potential using a number of “unclassify” solids.

The 2015 Etango Mineral Resource estimate, initiated by IRS and completed by Optiro with the assistance

of Bannerman, closely reflects the proposed grade control and mining approach, which is gamma probing

of relatively widely spaced blastholes supplemented by a truck scanning station. This approach has been

shown to be highly effective at two of the world’s major open pit uranium deposits (Rössing in Namibia and

Ranger in Australia).

The use of a recoverable resource post-processing technique reflects best practice for uranium

mineralisation and closely matches the recovery from a truck scanning operation as planned at Etango.

No further drilling was done since reporting the updated Mineral Resource estimate on 11 November 2015

and the underlying assumptions remain valid.

This Scoping Study adopts a mill-limiting cut-off grade of 100ppm U3O8 to determine the economic limits

of the pit.

For full details of the 2015 Etango Mineral Resource estimate, please refer to Bannerman ASX release

dated 11 November 2015, Outstanding DFS Optimisation Study Results. Bannerman confirms that it is

not aware of any new information or data that materially affects the information included in that release.

For

per

sona

l use

onl

y

10

All material assumptions and technical parameters underpinning the resource estimate continue to apply

and have not materially changed.

5. Mining studies

5.1 Pit optimisation

The Scoping Study pit optimisations were carried out by Qubeka Mining Consultants (Qubeka) using the

Whittle Four-X (Whittle) pit optimisation software. The Whittle software package, utilising the Lerchs

Grossman algorithm, is considered to be leading practice and is widely used in the mining industry for

open pit optimisation.

By inspection of the incremental pit shells and resultant financial metrics, the ultimate pit shell and the

mining sequence is determined, which in turn guides individual stage or pushback designs. These

intermediate mining stages allow the pit to be developed in a practical and incremental manner, while at

the same time targeting the highest value ore, and deferring waste stripping.

Table 2 lists the parameters used for the pit optimisation work and the analysis of the optimisation results.

Table 2: Key pit optimisation inputs

Item Unit Parameter

Mill throughput Mtpa 8

Uranium price US$/lb 65

Royalty % 3

Export levy % 0.25

Royalty (3rd Party) % 1.17

Transport, shipping, marketing and sales US$/lb 1.10

Processing costs US$/t ore 7.53

Average mining cost (contractor only) US$/t material 2.48

Total owner’s cost US$/t ore 1.21

Processing overall recovery % 87.80

Mining dilution % 0 (dilution in model)1

Mining recovery % 100 (recovery in model)1

Overall pit wall slope angle degrees 43 - 48

1: The process of creating the grade shells used for estimating the panel grades of the resource model incorporated dilution into the grade

shells by applying a below economic cut-off grade and relatively low probability of 0.4. As a haul truck load will effectively be the SMU of

the grade control process by employing radiometric truck scanning, dilution and mining loss has been incorporated by the larger block size.

5.2 Mining method and schedule

Under the Scoping Study parameters, the Etango deposit is planned to be mined as a conventional truck

and shovel open pit operation via contract mining. Annual throughput is 8Mtpa ROM ore feed to the

processing plant at a LOM average stripping ratio of 1.93.

Radiometric truck scanning (discrimination) will be employed as the definitive grade control process, as is

common practice in large scale open pit uranium mines in Australia and Namibia. This means that the

SMU in the mining process will be a single truck load.

The mine schedule employs a variable cut-off grade approach to maximise Net Present Value (NPV). In

accordance with this approach, the cut-off grade is flexed during the mine schedule to maximise metal

production as early as possible.

For

per

sona

l use

onl

y

11

The mine plan and schedule support average annual production of 3.55Mlb U3O8 over an initial mine life

of 14.4 years. A summary of the mine schedule and LOM production profile are presented in Table 3.

Table 3: Mine schedule and production targets

Mining Total Yr. 1 Yr. 2 Yr. 3 Yr. 4 Yr. 5 Yr.6 Yr. 7 Yr. 8

Ore Mt 114.11 7.92 9.23 11.19 7.97 5.86 10.88 4.83 10.10

Waste Mt 220.0 9.65 15.88 13.92 17.14 19.32 14.23 20.28 15.02

Total Mined Mt 334.1 17.57 25.11 25.11 25.11 25.18 25.11 25.11 25.11

Grade ppm 232 222 229 242 245 230 278 206 200

Strip Ratio Ratio 1.93 1.22 1.72 1.24 2.15 3.30 1.31 4.20 1.49

Metal U3O8 Mlbs 51.08 3.06 3.76 4.24 3.89 3.27 4.94 2.92 3.34

Mining

Yr. 9 Yr. 10 Yr. 11 Yr. 12 Yr. 13 Yr.14 Yr. 15

Ore Mt 7.17 5.96 9.02 7.06 9.69 7.02 0.23

Waste Mt 18.01 19.15 16.10 18.05 15.49 7.71 0.07

Total Mined Mt 25.18 25.11 25.11 25.11 25.18 14.73 0.30

Grade ppm 233 232 240 229 212 220 382

Strip Ratio Ratio 2.51 3.21 1.79 2.56 1.60 1.10 0.32

Metal U3O8 Mlbs 3.49 3.23 3.91 3.39 3.53 3.26 0.85

Respective material movements and average annual mine grades are presented in Figure 6. An initial

ramp-up period of 12 months has been incorporated for the processing plant to attain nameplate capacity

of 8Mtpa. A strategic ROM ore stockpile will be used to manage tonnage and grade of the ore feed to the

processing plant.

Figure 6: Life-of-mine profile for waste and ore material movements

1.0

2.0

3.0

4.0

5.0

6.0

5.0

10.0

15.0

20.0

25.0

30.0

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Str

ip R

atio

(w

:o t

onnes)

To

nnes (

Mt)

Material Movement Schedule

Ore Waste Strip Ratio

For

per

sona

l use

onl

y

12

Critically, the Scoping Study mine schedule still delivers real optionality for potential future phases of

expansion, including right up to the 20Mtpa production rate and scheduled pit pushbacks envisaged by

the OS 2015.

Figure 7: Etango-8 Project mine schedule by resource classification

Of the Mineral Resources scheduled for extraction in the Scoping Study production plan, approximately

13.7% are classified as Measured, 83.9% as Indicated and 2.4% as Inferred (see Figure 7). There is a

low level of geological confidence associated with Inferred Mineral Resources and there is no certainty

that further exploration work will result in the determination of Indicated Mineral Resources or that the

production target itself will be realised. Inferred Resources comprise less than 2.2% of the production

schedule in the first year of operation and an average of less than 2.1% over the first three years of

operation. Bannerman confirms that the financial viability of the Etango Project is not dependent on the

inclusion of Inferred Resources in the production schedule.

Figure 8 provides the comparison between the final 20Mtpa Etango pit as defined in the OS 2015, the first

6 pushbacks of the 20Mtpa Etango pit from the OS 2015, as well as the final pit design for the Etango-8

Scoping Study pit.

The contractor mining fleet is planned to consist of approximately 20 – 24 haul trucks (100 tonne class)

and 4 – 5 excavators (200 tonne class), with associated support equipment.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Composition of Mined Ore Schedule by Resource Classification

Measured Indicated Inferred LOM Measured & Indicated %

For

per

sona

l use

onl

y

13

Figure 8: Comparison between the 20Mtpa (OS 2015) and Etango-8 Scoping Study pit outlines

5.3 Geotechnical

As part of the DFS 2012, Coffey Mining completed the geotechnical assessment for the proposed Etango

open pit in October 2011. The results of this work were:

The geotechnical data from which the geotechnical domains have been derived is based primarily

on geotechnical logging of drill core and surface structural mapping;

A total of 26 geotechnical drill holes were drilled from the Anomaly A, Oshivelo and Onkelo deposits

(see Figure 5) to collect rock quality and structural data;

The fault planes generally dip at shallow to moderate planes towards the west and are interpreted

to daylight on both the southeast and northeast walls;

Two types of geological contacts have been identified on the Etango deposit, namely the:

‒ Alaskite – meta-sediment contact; and the

‒ Meta-sediment – lithology contacts (Chuos / Khan / Etusis)

Kinematic analysis was undertaken where three modes of failure were examined for each of the

sectors, and a slope configuration calculated based upon the selected bench height; and

Inter-ramp stability was also assessed using probabilistic techniques.

In general, the geotechnical investigations demonstrated that the fresh rock mass conditions are good and

will allow for steep slopes to be excavated. On the smaller bench scale, there is potential to develop

wedge or planar failures in areas due to the intersection of joints and batters. However, the calculated

factors of safety have highlighted that these should not present a significant issue. The risk associated

with these types of failures can be mitigated by maintaining good blasting practices and batter slopes.

The recommended pit slope designs developed for the Etango Project are summarised in Table 4 below.

For

per

sona

l use

onl

y

14

Table 4: Recommended pit slope designs

Etango Uranium Project – Etango Slope Design

Domain Design

Sector Weathering

BFA

(°)

BW

(m)

BH

(m)

IRSA

(°)

IRSH/Decouple

(m)

OSH

(m)

OSA

(°)

North/South All

Slopes

Weathered 55 6 12 39.8 20 380 50.5

Fresh 70 9.5 24 52.8 120

Legend: BFA - Batter Face Angle IRSH - Inter-Ramp Slope Height

BW - Berm Width OSH - Overall Slope Height

BH - Batter Height OSA - Overall Slope Angle

IRSA - Inter-Ramp Slope Angle

The bench height study in the DFS 2012 resulted in the adoption of 12m benches mined in 3 – 4m flitches

to minimise ore loss and dilution. This Scoping Study maintains this approach. The loading equipment,

consisting of 200 tonne excavators, is suitable for this design. The design also allows for progression to

larger equipment in the event of expanded production rates in the future.

5.4 Hydrogeological

Aquaterra undertook a detailed assessment of hydrogeological conditions and requirements for

depressurising (dewatering) the pit walls as part of the DFS 2012. The conclusions from this work remain

equally applicable to this Scoping Study.

It was determined that the relevant hydrogeological units are generally low hydraulic conductivity basement

rocks. It was concluded that there will be limited natural drainage to the pit face, thus little lowering of

piezometric heads in the rocks behind the pit wall and elevated values may persist at, below and behind

the pit walls over the life of the mine.

Modelling demonstrated that the steepest gradients in predicted heads will develop immediately under the

base of the deepest part of the pit over the mine life. Additionally, a seepage face is predicted to develop

on both pit walls and lie 100 to 200 metres above the base of the final pit depth at the end of mining.

The modelling assisted in identifying those areas where pressures will be high and where potential

additional depressurisation might be required. However, in general, groundwater is not expected to

present a significant issue for mining activities.

6. Processing

6.1 Metallurgical testwork

Bannerman has performed various metallurgical testwork programs both at ALS Ammtech in Perth,

Australia, and Bureau Veritas in Swakopmund, Namibia. The construction of the Heap Leach

Demonstration Plant at the Etango Project in 2014 has also demonstrated, at a significantly larger scale,

the robustness of the assumptions used in the DFS 2012 and OS 2015 for the design of a commercial

heap leach operation.

Testwork has included comminution, heap leach column and crib testwork, acid consumption variability

testwork, Solvent Extraction (SX), Ion Exchange (IX) and Nano-Filtration (NF) testwork. Results of the

testwork have been reported continuously as they became available.

The critical process design parameters used in this Scoping Study include:

Heap leach crush size P80 5.3 mm

Leach duration 30 - 32 days

For

per

sona

l use

onl

y

15

U3O8 recovery 87.8%

Acid consumption 16.8 kg/t

Heap leach pad height 5 m

Heap irrigation rate 12.6 L/m2/h

6.2 Process flowsheet

ROM ore is delivered to a gyratory primary crusher, followed by two secondary cone crushers and two

tertiary HPGR (high pressure grinding roll) units to produce the target P80 product size of 5.3mm.

The crushed ore is conveyed to a fine ore surge bin and then fed to a single agglomerating drum. Water,

sulphuric acid and binder agent are added, and the agglomerated ore is transferred to the heap leach

stacking system. Grasshopper conveyors, stacker feed conveyor and a radial stacker will stack the ore to

a height of 5m.

Ore is stacked in modules, where each module represents one day of stacking. Intermediate leach solution

produces Pregnant Leach Solution (PLS) which is pumped to IX columns for the recovery of uranium, and

the barren solution is recirculated to the heap to build up uranium tenor. Once the heap is depleted of

uranium, it is drained, rinsed and drained again, drippers are then removed, and the exhausted heap

reclaimed. Figure 9 shows the basic Etango process flow sheet.

Figure 9: Basic Etango-8 Project process flow sheet

For

per

sona

l use

onl

y

16

Following the IX process, the uranium bearing solution proceeds through Nano-Filtration (NF), precipitation

and drying/calcining. Filling, lidding, washing and weighing of the product transportation drums is largely

automated. The drums are conveyed through an airlock into the packing module under negative pressure.

The Membrane Study Testwork completed early in 2020 successfully confirmed that substantial economic

and operational advantages can be obtained with an optimised flowsheet consisting of an IX process

followed by NF. The details of the testwork were reported on the ASX on 9 April 2020. Over 80% acid

recovery from the concentrated eluate stream of the IX plant is achieved while also obtaining the required

uranium upgrade for the precipitation process. The design of the NF plant has already been completed to

definitive level and is suitable for the 8Mtpa scale.

Forecast average LOM U3O8 production is 3.55Mlb per annum, with a peak in Year 6 of 4.95Mlb. Figure

10 depicts the forecast LOM production profile.

Figure 10: Forecast LOM head grade profile and U3O8 production volumes

6.3 Processing assumptions

This Scoping Study utilises an overall uranium recovery of 87.80% based on the extensive testwork done

with columns (2m, 4m, 5m and 7m) and cribs (2m x 2m x 5m), as well as applying appropriate scale-up

factors to simulate reduced performance on a commercial heap.

Following extensive acid consumption testwork with columns and cribs, combined with the acid recovery

process via nano-filtration, and applying scale-up factors, a relatively conservative overall sulphuric acid

consumption of 16.8 kg/t is assumed. There exists clear potential for this estimate to be further optimised.

As per the flow sheet, triuranium octoxide (U3O8) is the final product that will be drummed and shipped.

6.4 Plant location

The site layout is shown in Figure 11 and remains at the same location as in the OS 2015. The selected

location is driven largely by the typical economic imperative to restrict waste and ore haulage distances.

-

50

100

150

200

250

300

350

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 Y13 Y14 Y15

Pla

nt head g

rade (

U3O

8 p

pm

)

Ura

niu

m P

roduction (

U3O

8 lb

s)

Uranium Production and Plant Head Grade

Uranium production (U3O8 lbs) Head grade (U3O8 ppm)

For

per

sona

l use

onl

y

17

The waste rock dumps are sited adjacent to the open pit and are situated as far as possible to the south

of the Swakop river catchment. Dump design and location have been informed by the need to limit height

to minimise visual impact, and to avoid sterilisation of uranium prospects to the south.

The primary crusher is located adjacent to the open pit (to minimise ore haulage) and is linked to the

process plant by a 3 km overland conveyor passing through the waste dump areas. The plant and

infrastructure are located away from any sensitive environmental and archaeological zones. The current

location also reduces the visual impact from both the C28 road to the south, the D1991 and the Moon

Landscape tourist lookout to the north.

The heap leach pads are located southwest of the main plant to suit the topography of the site and minimise

earthworks. The chosen location is in a valley, gently sloping in a general south-westerly direction. The

collection ponds for the heap are located at the lower end of the heap to allow drainage by gravity.

The heap leach residue facility is located at the southern extremity of the waste rock dumps, adjacent to

the heap leach pad.

Figure 11: Site layout (OS 2015)

For

per

sona

l use

onl

y

18

7. Infrastructure

7.1 On-site infrastructure

This Scoping Study includes the following on-site facilities to support both the mining and processing

operations:

Primary security gate, gate house and security fencing;

Diesel storage tank and fuelling facilities;

Operations and maintenance site offices;

Processing plant maintenance workshops;

On-site acid storage tanks with sufficient storage for 28 days usage;

Warehouse and reagent storage facilities;

Administration offices and emergency response facilities as well as change houses, laundry and

sanitary facilities;

Sewage treatment plant;

On-site fresh water tanks;

Compressed air services;

Process, raw, fire and fresh water services; and

Electrical reticulation and communications.

7.2 Heap leach residue

As part of the DFS 2012, a net percolation study and basal seepage analysis was undertaken, using rainfall

and other climate data from a nearby site to develop a simulated 18 year climate model for the Etango

Project. The basal seepage model was run over an 80-year period. The results of this work indicated:

Percolation rates within the heap leach residue (ripios) dump are low (<7 mm/a).

Seepage from the ripios dump will be high for the initial layer, due to the water content within the

ripios. However, seepage will decrease significantly after placement of the basal layer.

Rainfall has minimal percolation into the ripios dump, due to high evaporation rates and a salt crust

forming on the surface.

Based on ripios geochemical characterisation and seepage studies, Bannerman elected to proceed with

an unlined ripios dump.

The ripios dump design will include the following infrastructure:

Construction of a ramp using crushed gneiss left over from the heap leach drainage pad

construction.

Construction of internal stormwater V-drains and delineation bunds to direct stormwater run-off

from the ripios dump to a localised collection pond. These drains will be constructed outside the

ripios dump toe.

Construction of external seepage and stormwater management systems.

No geotechnical investigation has been carried out over the ripios dump location. Prior to detailed design,

a full geotechnical investigation will be carried out to determine soil strata and foundation conditions below

the ripios dump.

For

per

sona

l use

onl

y

19

7.3 Power

Power is to be provided by Nampower, the national power utility company of Namibia. Since the OS 2015,

Nampower has significantly upgraded the power supply and distribution capacity to cater for the now-

operating Husab Mine and the increased power usage of the port facilities at Walvis Bay. The power

infrastructure is within 30km of the Etango Project.

Power for the Etango Project site is to be sourced from the 220 kV national grid through Nampower’s

Kuiseb substation, which has recently been upgraded to 132 kV. Nampower proposes a 29 km, 132 kV

transmission line from the Kuiseb substation to the Etango Project site where a 132/33 kV switchyard,

transformer(s) and indoor Etango substation will be installed. The transformer size will be reviewed during

detailed engineering as the load list is finalised.

7.4 Water

Water will be sourced from NamWater and is set to be supplied from its sources to the Base Reservoir in

Swakopmund. The Etango water infrastructure consists of a pipeline and pumping system to transport the

water to the Etango Project site, and terminal water storage system on site. The route of the pipeline is to

follow the route as provided for in the Environmental Clearance Certificate.

The water supply system is still to be optimised for diameter of pipe and configuration of pump stations.

The Base Pump Station to be situated adjacent to the NamWater Base Reservoir site in Swakopmund,

and a Booster Pump Station, if required, should be sited to minimise cost of power supply to these stations.

The terminal storage is also to be optimised in regard to siting and capacity. The proposed position of the

storage is preferably on higher ground. Capacity is expected to provide for storage of at least four days

consumption to allow for upstream supply interruptions.

Although the DFS 2012 had proposed “Pioneer Style” tanks, this Scoping Study proposes consideration

of geomembrane plastic lined storage dams. This could be combined with the construction of the process

retention dams, which will also be plastic lined earth dams.

7.5 Roads

The C28 road from Swakopmund passes a few kilometres to the south of the Etango Project. Construction

of a spur road to the mine site is planned, parallel to the power line and water pipeline services route.

Figure 12 depicts all existing infrastructure routes and the proposed Etango Project power, water and road

connections. The D1984 is currently being upgraded to a sealed double highway with a safe fly-over onto

the C28. This will provide a safe route for the transportation of sulphuric acid and other reagents from the

Walvis Bay port to site, as well as trucking of the final product for shipment from Walvis Bay.

7.6 Port infrastructure

The Port of Walvis Bay is a highly established uranium export facility. Walvis Bay has been handling Class

7 cargo for over 40 years both from Namibia and neighbouring countries such as Malawi. Specific areas

within the controlled port environment have been designated for Class 7 cargo, which Bannerman would

also be using.

Regular container services operate from Walvis Bay to Europe, Asia and the United States. Bannerman

plans to utilise the services of an experienced local Namibian shipping agent. Consistent with standard

practice, Bannerman expects to pay for all shipping and transport of U3O8 to the conversion facility, and

then for the weighing, sampling and assaying at the converter.

The key reagent for the Etango process, sulphuric acid, is to be imported in bulk to the Walvis Bay port.

One storage tank has been allowed for as part of dedicated port facilities. The transport of bulk

concentrated sulphuric acid (98% w/w) from the port to Etango Project site is via bulk tanker trucks. There

it is transferred to acid storage tanks on site, which are designed to provide sufficient storage for 28 days

usage in mild steel tanks.

For

per

sona

l use

onl

y

20

Figure 12: External infrastructure corridor to Etango

For

per

sona

l use

onl

y

21

8. Environmental and social

Bannerman received its Environmental Clearance in March 2010 for the Etango Project. The

Environmental Clearance was based on the Environmental and Social Impact Assessment (ESIA) and

Environmental and Social Management Plan (ESMP), which were developed by A. Speiser Environmental

Consultants cc (ASEC) with a team of 14 specialists. The ESIA and ESMP were subjected to external

peer reviewed by the Southern African Institute for Environmental Assessments.

The Environmental Clearance for the location and design of infrastructure ancillary to the Etango Project

(including the access road, water pipeline and power lines) was granted by the Ministry of Environment

and Tourism in July 2011.

A revised ESIA, reflecting the project detailed in the DFS 2012, was prepared by ASEC and Environmental

Resource Management (ERM) and submitted in April 2012, with the Environmental Clearance granted in

July 2012 valid for three years. This has subsequently been renewed on two further occasions and is

currently valid until October 2021. Environmental Clearance for linear infrastructure was granted in

February 2013 (valid for three years) – it has also been renewed twice and is currently valid until June

2022.

The 2012 ESIA processes saw extensive public consultations for the larger Etango Project. The Etango-

8 Project is essentially a smaller version of the larger project and thus focus groups with key stakeholders

will be held once the Project moves to the next feasibility stage, with subsequent input included in the

Environmental Clearance renewal.

Baseline monitoring of groundwater and air quality started in 2008 and has continued over subsequent

years.

Bannerman has a core value to build enduring and mutually beneficial relationships with its neighbouring

communities in Namibia. It has invested in Namibia since 2006 and in this time has contributed

substantially to the communities in which it operates. Selected initiatives include:

Early Learner Assistance Program – over 3,000 pre-primary learners in remote communities have

received assistance via this program with school clothing and basic necessities.

Bannerman pioneered cooperation with the Hospitality Association of Namibia and Coastal

Tourism Association of Namibia and has supported the tourism sector in numerous ways and in

2019 Bannerman’s Managing Director, Werner Ewald, received the accolade of ‘Tourism

Personality of the Year’.

Erongo Development Foundation – Bannerman has been an active member of the Erongo

Development Foundation for many years; an organisation supporting the development of poor

communities within the Erongo Region where the Etango Project is located.

9. Operating costs

Contributors to the operating cost estimate were as follows:

Mine operating costs Qubeka Mining Consultants & Bannerman

Plant and site infrastructure DRA-SENET & Bannerman

External infrastructure Genis Business Consulting & Bannerman

Owner's (G&A) costs Bannerman

Acid costs Bannerman

Table 5 provides a breakdown of key individual components of forecast LOM and unit final product cash

operating cost.

For

per

sona

l use

onl

y

22

Table 5: Life-of-mine final product cash operating costs (ex-royalties/levies)

Description LOM US$M

US$/t ore

US$/lb %

Mining - Contractor 829 7.3 16.2 43%

Maintenance & consumables 190 1.7 3.7 10%

Power 172 1.5 3.4 9%

Sulphuric acid 168 1.5 3.3 9%

Reagents (not including acid) 127 1.1 2.5 7%

Raw Water 94 0.8 1.8 5%

General & Admin expenses 83 0.7 1.6 4%

Corporate & Owner's Labour 59 0.5 1.2 3%

Labour - Plant Operations 50 0.4 1.0 3%

Labour - Plant Maintenance 37 0.3 0.7 2%

Mining - Owner's cost 27 0.2 0.5 1%

Miscellaneous 17 0.1 0.3 1%

Product transport, port, conversion 56 0.5 1.1 3%

Total (ex-royalties/levies) 1,908 16.7 37.4 100%

The projected final product cash operating cost (ex royalties and levies) totals US$37.4/lb U3O8 produced.

9.1 Mining

This Scoping Study proposes a contract mining operation. This includes drilling, blasting, loading and

hauling of ore and waste. The OS 2015 mining cost estimate was US$1.69/t material mined and was

based on an owner mining operation. This Scoping Study utilises a forecast unit mining cost of US$2.48/t

material mined (US$2.56/t inclusive of minor owners’ costs). This is based on a bottom-up contract mining

cost model built by Qubeka and also benchmarked against contractor operations with similar sized

equipment operating elsewhere in Namibia and South Africa.

9.2 Acid and other reagents

Sulphuric acid consumption remains a major operating cost driver for the Etango-8 Project. As noted in

Section 6, extensive acid consumption testwork has been performed on the Etango ore (and previously

released to the ASX as part of the DFS 2012 and OS 2015).

The larger scale test work at Bannerman’s Heap Leach Demonstration Plant is viewed as providing the

most appropriate indication of what average acid consumption should be expected for a commercial heap

operation. Average acid consumption of 14.7kg/t was achieved at the Heap Leach Demonstration Plant.

Taking into account appropriate scale-up factors, and acid consumption downstream in the process

flowsheet, a final acid consumption value of 16.8kg/t has been utilised for this Scoping Study. As noted

earlier, this estimate retains significant potential for further optimisation.

The forecast price of sulphuric acid (delivered to Walvis Bay) is US$75/t, with an additional US$13/t

transport cost for delivery to the Etango Project site.

The consumption of other reagents is based on the mass balance and design criteria. Updated quotes

from vendors were obtained for the unit costs of each reagent, including sulphuric acid.

9.3 Maintenance and consumables

The abrasion index of the Etango ore, and in particular the metasediments, is towards the higher end of

the scale. As with the OS 2015, this Scoping Study cost estimates allow for generally higher levels of

maintenance input and consumables replacement to adequately reflect this.

For

per

sona

l use

onl

y

23

9.4 Water and power

As per the OS 2015, the water demand per tonne of ore processed remains at 0.216 m3/t, which equates

to an annual water demand of approximately 1.8 Mm3. This equates to a daily requirement of 5,000

m3/day, and therefore an equivalent demand of 250 m3/hr calculated over 20 hours per day to provide for

maintenance downtimes.

The water tariff of US$3.5/m3 used in this Scoping Study is based on discussions between Bannerman

and NamWater. It reflects the estimated cost of desalination and water transport operating and

maintenance costs included in the delivery to site.

Absorbed power was determined by applying a load factor supplied by vendors to the installed load. Where

the absorbed power was not supplied by the vendors, an assumed factor was used.

The utility power cost assumed is US$0.0129 per kWh, which is the blended energy cost based on

Nampower’s Time of Use tariff schedule for customers taking energy directly from Nampower. This

includes all fixed charges, capacity charges and energy charges.

9.5 Labour costs

The personnel schedule was developed by DRA-SENET with input from Bannerman. It is structured to

fulfil all requirements for technical, supervisory, operating and maintenance personnel, in order to run and

maintain the mine and process operations in a safe, efficient and cost-effective manner.

9.6 General and administration expenses

These expenses include provisions for National Parks and road maintenance, insurance, government fees,

environmental monitoring, training, catering and community work.

10. Capital costs

Forecast pre-production capital expenditure to develop the Etango Project as reflected in this Scoping

Study is estimated at US$254M. The breakdown of this estimate is provided in Table 6.

The pre-production capital cost estimate was developed to achieve an accuracy level of ±30%.

The main pre-production capital expenditure items include the processing plant infrastructure and

equipment costs, pre-production owners’ costs, EPCM and accuracy provision, and the external

infrastructure costs which include the water and power supply, road access and port infrastructure.

Table 6: Pre-production capital cost

Description US$'000 %

Direct Processing Plant capital 131,875 52%

External & Internal Infrastructure 34,023 13%

Accuracy provision 31,460 12%

Pre-production owners & EPCM 17,754 7%

Mining - owner's cost 11,206 4%

Owners direct cost 11,473 5%

Temporary Services, Construction Camp 9,752 4%

Commissioning, operational & insurance spares 6,802 3%

Total 254,344 100%

For

per

sona

l use

onl

y

24

Total sustaining capital across the 15-year LOM is projected at US$31M (approximately US$0.27/t ore).

This is based on forecast sustaining activities, particularly for the port infrastructure and progressive

rehabilitation.

11. Financial analysis

The financial estimates for the Etango Project as reflected in this Scoping Study were developed by

Qubeka, DRA-SENET, Genis Business Consulting and Bannerman using a discounted cash flow model.

The modelling assumes contract mining while the rest of the operation is owner-operated.

The intended estimation accuracy of this Scoping Study is ± 30%.

11.1 Basis of estimates

The financial estimates were prepared under the following assumptions:

A real discount rate of 8% was used for discounted cash flow modelling;

Costs are quoted in real US dollar 2020 terms;

Cash flow periods are expressed annually in calendar years;

Uranium sales revenue is assumed to be realised approximately 4 months after production;

All financial assessments have been undertaken on a 100% project ownership basis (noting that

Bannerman’s attributable interest in the Etango Project is 95%);

All costs are stated exclusive of VAT;

Namibian Government royalties (3%) and export levy (0.25%) have been applied to gross revenue

while external party royalties (1.17%) have been applied to pre-tax cash flow and Namibian

corporate tax (37.5%) has been applied to pre-tax post-royalty cash flow;

A Namibian inflation rate of 5.4% p.a. is assumed solely for the purposes of calculating forecast

depreciation and taxation schedules; and

Quantities stated are metric (SI units), excepting the final product which is converted to pounds

(lbs).

11.2 Uranium market outlook and product marketing

The uranium market has been characterised by over-supply and a resultant bear market cycle that

commenced with the nuclear accident at Fukushima-Daiichi nuclear power plant in 2011 and a rapid

reduction of demand for nuclear fuel in Japan, Germany and elsewhere. After several years of oversupply

in which consumers and intermediaries built substantial inventories, the uranium market returned to

structural balance in 2018 and is currently experiencing significant structural deficits.

Whilst demand for nuclear fuel has recovered to pre-2011 levels, the pricing response to these deficits has

been muted by the draw-down of excess inventory. The uranium spot price bottomed in 2017 and has

experienced modest recovery since then, trading at levels last seen in 2016. In 2020, supply disruption For

per

sona

l use

onl

y

25

caused by COVID-19 mine closures exacerbated the deficit causing the draw-down of inventories to

historically normal levels.

Most market commentators expect uranium long term contract prices to substantially and sustainably

increase to their assumed long-term price forecast or beyond in the next 24-48 months due to a number

of factors, including:

(a) A substantial proportion of global uranium production is uneconomic at current prices;

(b) Uranium demand is projected to grow steadily to 2040 and beyond, in particular in the growth

markets of China, India and Russia;

(c) Uranium supply is expected to undergo significant depletion over the next decade, despite the

capacity for care and maintenance mines to return to production, as several large uranium mines

will be exhausted of ore and secondary supply reduces; and

(d) Under-investment in uranium exploration and development over the last decade coupled with

onerous political, environmental and social approval processes has resulted in an inadequate

development pipeline that requires prices in excess of the assumed long term contract price to

incentivise sufficient replacement of depleted production.

Consistent with industry practice, Bannerman plans to obtain a diversified portfolio of long-term supply

contracts with a blend of fixed-term escalated prices and market price mechanisms, subject to floor prices.

Prior to commencement of construction, a sufficient proportion of production is expected to be contracted

with high-quality counterparties to enable conventional financing of the project, potentially in combination

with off-take related financing.

Bannerman has pursued an active marketing strategy since 2016, resulting in a substantial profile in the

nuclear power industry and membership of the World Nuclear Association, World Nuclear Fuel Cycle,

World Nuclear Fuel Market and Namibian Uranium Association. Implementation of this strategy

commenced with the engagement in 2016 of Nuclear Fuel Associates as Strategic Uranium Marketing

Consultants and notably benefitted from Bannerman Resources Limited’s Chief Executive Officer, Brandon

Munro, being appointed in 2018 as Co-Chair of the World Nuclear Association’s Nuclear Fuel Report

uranium demand working group.

The realised LOM uranium price forecast adopted for this Scoping Study is US$65/lb U3O8. This compares

with the price estimate utilised for the OS 2015 of US$75/lb. The LOM price assumption for this Scoping

Study was estimated as follows:

The 2024 uranium spot price forecast data was sourced from Consensus Economics (15 June

2020). The 2024 estimate represented the longest-dated single year estimate in the Consensus

Economics forecast uranium data set. There were 8 estimates comprising this 2024 forecast price

data ranging from US$33.50/lb to US$60.00/lb. The average estimate was US$47.10/lb and the

median estimate was US$47.64/lb.

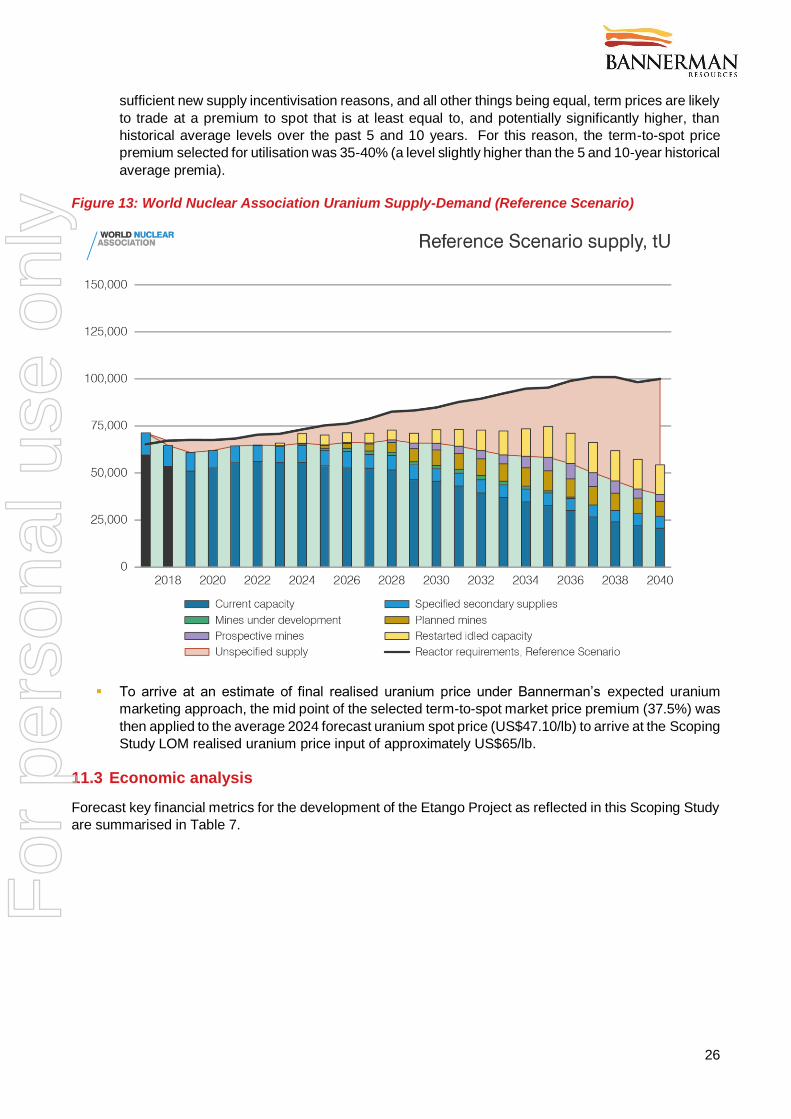

Price series for historical spot and term uranium prices were then sourced from www.cameco.com

(a data set which Cameco has assembled based on price data published by the two leading

uranium industry price index providers, TradeTech and Ux Consulting). The market premium of

term-to-spot uranium prices was then calculated on a monthly basis for the past 10 years (July

2010 to June 2020). The monthly average of this premium ranged from as low as -2% to as high

as +89% over this 10-year period. The 10-year historical average premium was 32.5% and the 5-

year average was 34.4%.

The current Reference Scenario from the World Nuclear Association’s (WNA) Nuclear Fuel Report

2019 was then evaluated alongside this historical premia data. The WNA baseline case highlights

a rapid divergence (into significant deficit) between forecast nuclear reactor requirements and

expected global uranium supply from 2024 (see Figure 13). These conditions suggest that, for

For

per

sona

l use

onl

y

26

sufficient new supply incentivisation reasons, and all other things being equal, term prices are likely

to trade at a premium to spot that is at least equal to, and potentially significantly higher, than

historical average levels over the past 5 and 10 years. For this reason, the term-to-spot price

premium selected for utilisation was 35-40% (a level slightly higher than the 5 and 10-year historical

average premia).

Figure 13: World Nuclear Association Uranium Supply-Demand (Reference Scenario)

To arrive at an estimate of final realised uranium price under Bannerman’s expected uranium

marketing approach, the mid point of the selected term-to-spot market price premium (37.5%) was

then applied to the average 2024 forecast uranium spot price (US$47.10/lb) to arrive at the Scoping

Study LOM realised uranium price input of approximately US$65/lb.

11.3 Economic analysis

Forecast key financial metrics for the development of the Etango Project as reflected in this Scoping Study

are summarised in Table 7.

For

per

sona

l use

onl

y

27

Table 7: Key financial metrics (100% basis)

Key financial outcomes Unit Total

Price inputs

LOM average uranium price US$/lb U3O8 - 65

US$/N$ N$ - 16

Valuation, returns and key ratios Range Mid point

NPV8% (post-tax, real basis, ungeared) US$M 201 - 223 212

NPV8% (pre-tax, real basis, ungeared) US$M 354 - 392 373

IRR (post-tax, real basis, ungeared) % 20.1 - 22.2 21.2

IRR (pre-tax, real basis, ungeared) % 25.5 - 28.1 26.8

Payback period (post-tax, from first production) years 3.4 - 3.8 3.6

Payback period (pre-tax, from first production) years 3.2 - 3.6 3.4

Pre-tax NPV / Pre-production capex x 1.4 - 1.5 1.5

Pre-production capital intensity US$/lb U3O8 pa capacity 67 - 75 71

Cashflow summary Range Mid point

Sales revenue (gross) US$M 3,154 - 3,486 3,320

Mining opex US$M (813 - 899) (856)

Processing opex US$M (816 - 902) (859)

G&A opex US$M (134 - 150) (143)

Product transport, port, freight, conversion US$M (53 - 59) (56)

Royalties and export levies US$M (139 - 153) (146)

Project operating surplus US$M 1,197 - 1,323 1,260

Pre-production capital expenditure US$M (241 - 267) (254)

LOM sustaining capital expenditure US$M (29 - 33) (31)

Project net cashflow (pre-tax) US$M 926 - 1,024 975

Tax paid US$M (352 - 390) (371)

Project net cashflow (post-tax) US$M 574 - 634 604

Unit cash operating costs Range Mid Point