catalyzing job creation development in the deauville ... · catalyzing job creation and growth...

TRANSCRIPT

Catalyzing Job Creationand Growth Through MSME

Development in the Deauville Partnership Countries

Volume 2: Good Practices in Entrepreneurship Development and MSME Support

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

i

Unemployment was a key factor fueling the

popular discontent leading to the 2011

revolutions in Egypt and Tunisia, and the

transformational processes in Jordan, Libya,

Morocco, and Yemen. The transitions that these

countries have been going through since 2011

have compounded the problem, and they

are now in need, more than ever, of support

to create employment opportunities for all.

They need to foster home-grown sources

of employment and income generation,

particularly by promoting entrepreneurship and

the development of micro, small and medium

enterprises (MSMEs), a sector that comprises

the majority of enterprises in the Middle East

and North Africa region, in addition to being a

major source of private sector employment.

At their Summit in Deauville, France, in May

2011, the G8 countries made a commitment to

provide support for the political and economic

transformation of the Arab Countries in

Transition – Egypt, Jordan, Libya, Morocco,

Tunisia, and Yemen – through the launch of the

Deauville Partnership. Gulf countries Kuwait,

Qatar, Saudi Arabia, and the United Arab

Emirates, as well as Turkey, joined the Deauville

Partnership subsequently.

A group of 10 international financial institutions

(IFIs) supporting the Deauville Partnership

countries agreed in September 2011 to

establish an operational platform, with a flexible

non-bureaucratic structure, to coordinate

responses to the countries’ urgent needs. The

coordination platform is supported by a

secretariat, which was hosted by the North

Africa Department of the African Development

Bank (AfDB) during its inception phase from

September 2011 to September 2012. Against

this backdrop and on behalf of its IFI partners,

the Bank has prepared this report to lay

the ground for better provision and more

coordinated and strategic MSME support in

Deauville Partnership countries, with a

particular focus on MSMEs with the highest

employment-creation potential. The first volume

of the report addresses several knowledge

gaps on MSME development in the region. To

inform policy and project interventions, it

provides a detailed analysis of current

knowledge concerning the link between MSME

development and job creation.

The second volume of the report focuses on

identification of good practices and success

stories in MSME support instruments and

programs in the region, profiling a selection of

these as examples for replication or adaption

in other Deauville Partnership countries. It

builds on the findings and recommendations

of Volume I and aims to provide concrete

examples of policy responses and how

interventions by IFIs and other donors could

be implemented. The objective is to share the

“how-to” of innovative and high-performing

Foreword

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

ii

entrepreneurship and MSME support

programs with a view to transferring lessons

learned to other Deauville Partnership

countries. It is intended to function as a

vehicle to facilitate an exchange between

Deauville Partnership countries/ partners and

the “good practice” proponents on possible

replication or adaption in the different country

contexts.

AfDB has always looked for multifaceted,

innovative, and efficient ways of supporting

SMEs. Recent initiatives have included the

African Guarantee Fund, which provides

partial guarantees, and other important risk-

sharing initiatives, such as the growth-oriented

women enterprises facilities. Others initiatives

include the provision of dedicated lines of

credit to financial intermediaries for lending to

SMEs, to improve their access to finance,

credit enhancement schemes, and capacity-

building activities. The Bank will continue to

collaborate with development partners to

ensure that, as we provide support to the

region, we integrate the latest thinking on

support to MSMEs in our activities, especially

in terms of creating a meaningful environment

for employment generation.

Jacob Kolster,

Director, North Africa Regional Department

(ORNA)

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

iii

This report was prepared by Lois Stevenson,

Senior Consultant, North Africa Department

(ORNA), African Development Bank (AfDB),

under the lead and supervision of Florian Theus

(Economist, ORNA). Overall guidance was

provided by Jacob Kolster (Director, ORNA).

Petra Menander Ahman (former Head, IFI

Secretariat, ORNA) and Yasser Ahmad (Chief

Country Portfolio Officer, ORNA) played an

instrumental role for the project during the initial

coordination efforts with other international

financial institutions (IFIs). The report

benefited from valuable comments on the

analytical framework and the executive

summary by Thouraya Triki (Chief Country

Economist, ORNA) and Vincent Castel (Chief

Country Economist, Morocco, ORNA). Philippe

Trape (Principal Country Economist, Tunisia,

ORNA) and Mickaëlle Chauvin, (Consultant,

ORNA) reviewed the report and provided

technical inputs as well as preliminary editing

and quality control. The final editing of the report

was done by Diana Saltarelli.

The project has also been served by the

collaboration with other IFIs and the Organisation

for Economic Co-operation and Development

(OECD). For initial coordination in the design

phase, the Deauville Partnership’s Small and

Medium Enterprise (SME) Working Group played

an important role. AfDB is also thankful to IFI

partners for the sharing of information, studies

and projects related to micro, small and medium

enterprise (MSME) development in the MENA

region, in particular Laurent Gonnet (Financial

Sector Specialist, MENA, World Bank), Hermann

Bender (Program Manager, West MENA, IFC),

Eman Omran (Small and Medium Enterprises

Team Leader, Canadian International

Development Agency, Egypt), Reem ElSaady

(Manager, Business Advisory Services Program

Egypt, European Bank for Reconstruction and

Development) and Monica Carco (Head,

Investment and Technology Unit, United Nations

Industrial Development Organization). The report

also benefited from the review of the draft by

Jorge Galvez Mendez (Policy Analyst, Private

Sector Development, OECD).

The report furthermore relied on the inputs

received from representatives of the Egyptian,

Jordanian, Moroccan and Tunisian governments,

namely Alaya Bettaieb (former Secretary of

State, Ministry of Development International

Cooperation) and Sadok Bejja (General Director

for SME Development, Ministry of Industry and

Technology) from Tunisia; Aicha Bouanani

(Ministry of Economy and Finance), as well as

Abdelkrim Belkadi (National Agency for the

Promotion of Employment and Skills - ANAPEC)

and Houria Nadifi (National Agency for the

Promotion of Small and Medium Enterprises –

ANPME) from Morocco; Hana Uraidi (Director

of Cross Cutting Support Directorate, Jordan

Enterprise Development Corporation) from

Jordan; and Ghada Waly (former Managing

Acknowledgements

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

iv

Director), Mohamed Abdel Aziz (Policy and

Coordination Specialist), Dr. Hatem Zaki (Head

of Non-Financial Services, Small Enterprises

Development Group), Marwan Abdel Razek

(Head of Franchise Development Department),

Dr. Raafat Abbas Shehata (Head of the

Technical Office) Hanaa El Hilaly (Director

General, Planning and International

Cooperation Group), all from the Social Fund for

Development in Egypt.

AfDB would also like to thank all individuals

and corporations that were available for

meetings, interviews and information sharing,

without whom the good practice profiles could

not have been completed. Gratitude goes

especially to Deema Bibi (Chief Executive

Officer, INJAZ, Jordan) and Shadin Hamaideh

(Head of Development Unit, INJAZ, Jordan),

Hassan Charraf (Manager of Development,

Fondation Création d’Entreprises, Morocco),

Abdelhamid Rouini (Conseiller Réseau and

Partenaires Investissement, Fondation Création

d’Entreprises, Morocco), Mohamed Zakaria

(Chief Director of Training, Egyptian Banking

Institute, Egypt), Dr. Khattar (Chairperson of the

Board and General Manager, Kafalat SAL,

Lebanon), Ralph Stephan (Officer - Energy and

Technology Department, Kafalat SAL,

Lebanon), Hicham Zanati Serghini (Secretary

General, Caisse Centrale de Garantie,

Morocco), Djamila Laaroussi (Chef du

Département de la Communication et du

Marketing, Caisse Centrale de Garantie,

Morocco), Kamel Krimi (Directeur des

Engagements, Tunisie Leasing, Tunisia), Ayman

Mahmoud (Executive Director, El Mobadara,

Egypt), Pierre Lucante (Project Manager,

German Agency for International Cooperation –

GIZ, Morocco), and Houria Nadifi (Chef de

Division, Cooperation Etudes, ANPME,

Morocco).

This report was made possible by the

generous financial support of the Department

of International Development, United Kingdom.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

v

Table of Contents

i Foreword

iii Acknowledgements

v Table of Contents

vi Abbreviations

viii Executive summary

1 1. INTRODUCTION

5 2. FOSTERING ENTREPRENEURSHIP AND BUSINESS CREATION

6 2.1 Strengthening the Culture of Entrepreneurship through the Education System

8 INJAZ, Jordan

22 2.2 Supporting Business Creation

23 Fondation Création d’Entreprises, Morocco

31 Souk At-Tanmia Entrepreneurship Development Initiative, Tunisia

46 3. ACCESS TO FINANCING FOR MSMEs

48 3.1 Loan Guarantee Schemes

48 Caisse Centrale de Garantie, Morocco

60 Kafalat SAL, Lebanon

71 3.2 Lease Financing

72 Tunisie Leasing, Tunisia

82 3.3 Capacity Building to Facilitate Bank Lending to SMEs

83 Egyptian Banking Institute, Egypt

93 4. BUSINESS DEVELOPMENT SUPPORT SERVICES FOR SMEs

95 El Mobadara Community Development and Small Enterprises Association, Egypt

108 5. DEVELOPMENT OF WOMEN ENTREPRENEURS/ WOMEN-OWNED MSMEs

111 Entre Elles en Régions Program, Morocco

122 6. CONCLUDING REMARKS

124 References

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

vi

Abbreviations

African Development Bank

Association of Women Entrepreneurs of Morocco/ Association des

Femmes Entrepreneurs du Maroc

National Agency for the Promotion of Employment and Skills/ Agence

Nationale de Promotion de l’Emploi et des Compétences

National Agency for the Promotion of Small and Medium Enterprises/

Agence Nationale pour la Promotion de la Petite et Moyenne Entreprise

Business development support

Business Development Services Support Project

Banque de Financement des petites et moyennes entreprises/ Bank

for Financing Small and Medium Enterprises

Banque Tunisienne de Solidarité

Central Guarantee Fund/ Caisse Centrale de Garantie

Canadian International Development Agency

Center for Young Business Leaders/ Centre des jeunes dirigeants

d’entreprise

National Center for Scientific and Technical Research/ Centre National

pour la Recherche Scientifique et Technique

Confederation of Tunisian Citizen Enterprises/ Confédération des

Entreprises Citoyennes de Tunisie

Regional Committees for Business Creation / Comités Régionaux pour

la Création d’Entreprises

Regional investment centers/ Centres régionaux des investissements

Civil society organization

Department for International Development, United Kingdom

Deloitte Touche Tohmatsu

Egyptian Banking Institute

European Bank for Reconstruction and Development

Egypt Enterprise Development Project

Espace Point de Départ: Association pour la Promotion de l’Entreprise

Féminine

Fondation Création d’Entreprises du Groupe Banque Populaire

German Agency for International Cooperation/ Deutsche Gesellschaft

für Internationale Zusammenarbeit

International Bank for Reconstruction and Development

Information and communications technologies

AfDBAFEM

ANAPEC

ANPME

BDSBDSSPBFPME

BTSCCGCIDACJD

CNRST

CONECT

CRPCE

CRICSODFIDDTTEBIEBRDEEDPESPOD

FCEGIZ

IBRDICT

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

vii

IFCIFIILOKAFDMDMMENAMFIMISMSEsMSMEsNIGDNPLOECDOFPPT

QMSREDECSAPSFDSMEsSMEDUPTLGUNDPUNIDOUNRWA

USAIDVSEWEF

Currencies

CADEGPEURGBPLBPMADTNDUS$

International Finance Corporation

International financial institution

International Labour Organization

King Abdullah II Fund for Development

Marocains du Monde

Middle East and North Africa

Microfinance institution

Management information system

Micro and small enterprises

Micro, small and medium enterprises

National Institute for the Guarantee of Deposits

Non-performing loan

Organisation for Economic Co-operation and Development

Office of Vocational Training and Employment Promotion/ Office

de la Formation Professionnelle et de la Promotion du Travail

Quality Management System

Regional Enterprise Development Center

School Adoption Program

Social Fund for Development

Small and medium enterprises

Small and Micro Enterprise Development in Upper Egypt Project

Tunisie Leasing Group

United Nations Development Programme

United Nations Industrial Development Organization

United Nations Relief and Works Agency for Palestine Refugees

in the Near East

United States Agency for International Development

Very small enterprise

World Economic Forum

Canadian dollar

Egyptian pound

Euro

British pound sterling

Lebanese pound

Moroccan dirham

Tunisian dinar

United States dollar

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

viii

The African Development Bank (AfDB),

on behalf of the international financial

institutions (IFIs) participating in the

Deauville Partnership with Arab Countries

in Transition, launched a two-volume study

aimed at enhancing knowledge exchange

and coordination among all Deauville

Partners and improving interventions

supporting the development of micro,

small and medium enterprises (MSMEs).

The study also seeks to lay the foundation

for further joint operations and research,

including actions by the Deauville

Partnership countries1 themselves. As it

covers activities by governments and

bilateral donors, it will help to streamline

the different initiatives around MSMEs in

the region, as well as across the various

pillars of the Deauville Partnership.

Volume I of this study, Catalyzing Job

Creation and Growth through MSME

Development in Deauville Partnership

Countries: A Gap Analysis of Policy

and Program Support in Morocco and

Tunisia, discusses the latest research on

the links between MSME development and

job creation, delineates policy implications

for MSME development in the two focus

countries, and makes recommendations

for future initiatives to address identified

gaps in MSME development support.

Building on the findings and

recommendations of Volume I, this

companion volume highlights nine good

practice initiatives from within the Middle

East and North Africa (MENA) region

geared to supporting entrepreneurship

and MSME development. This in itself

makes the publication unusual because

traditionally MENA countries have sought

to emulate good practices from outside

the region.

Good Practices in MSME SupportAreas

The good practices highlighted in Volume II

are found in initiatives focused on four

critical MSME support areas in the Deauville

Partnership countries, as outlined below:

(i) Fostering entrepreneurship and

business creation

• INJAZ, Jordan. A leading youth

economic education organization in

Executive Summary

1 Countries covered by the Deauville Partnership are Egypt, Libya, Jordan, Morocco, Tunisia, and Yemen.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

ix

Jordan and across the Arab world,

INJAZ offers entrepreneurship courses

and programs in secondary schools

and youth centers, and provides

capacity building to university and

college students in business and social

entrepreneurship through practical

training and independent projects. It

has achieved impressive results in

terms of reaching students and

vulnerable youth nationwide, and

engaging corporate sponsors and

volunteers to support its activities.

• Fondation Création d’Entreprises

(FCE), Morocco. The FCE, part of

Morocco’s Groupe Banque Populaire,

has the principal mission of promoting

an entrepreneurial culture and supporting

enterprise creation in Morocco. It

provides advice, counseling, coaching,

mentoring and training support to

Moroccan youth to encourage the

creation of new enterprises. Its

success in terms of start-ups, jobs

created, investments, and facilitating

access to financing for its supported

entrepreneurs derives, in part, from its

ability to expand its reach through a

network of regional offices.

• Souk At-Tanmia (“market for

development”) Entrepreneurship

Development Initiative, Tunisia. The

Initiative is an innovative pilot partnership

between AfDB and 20 other donors,

public and private stakeholders, and

Tunisian civil society to provide an

effective response to the post-Arab

Spring unemployment challenges in

Tunisia, particularly for youth. It uses

a competitive process to identify

entrepreneurial projects, and provides

entrepreneurial training, start-up grants

to help defray initial costs and/ or

enable entrepreneurs to meet the

equity requirements to qualify for

additional bank financing, and one year

of post-creation coaching support.

It can be considered an “emerging

good practice” to address the low

entrepreneurial culture and level of

activity in the underdeveloped regions

of Tunisia.

(ii) Access to financing for MSMEs

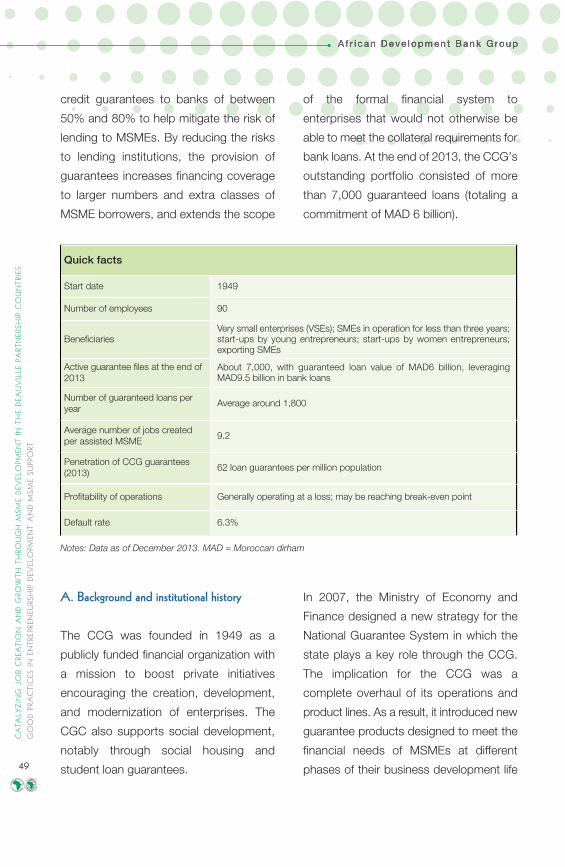

• Caisse Centrale de Garantie (CCG),

Morocco. The CCG is a public institution

that provides credit guarantees to

banks of between 50% and 80% to

help mitigate the risk of lending to

MSMEs. Through more than a dozen

guarantee products, it extends

financing coverage to larger numbers

of start-ups and MSMEs and extra

classes of MSME borrowers than

previously, while extending the scope

of the formal financial system to

enterprises, including very small

enterprises, that would otherwise not

be able to meet the collateral

requirements for bank loans. It is a

good example of how continuous

improvement of a guarantee program

leads to performance gains in terms of

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

x

attracting both MSMEs and banks to

participate, such as innovating with

new guarantee products, streamlining

the approval processes with the banks,

and reducing approval turnaround times

to 2–10 days on most guarantee files.

• Kafalat SAL, Lebanon. Kafalat is a

private for-profit financial company with

the broad development objective of

assisting SMEs in accessing commercial

bank funding by providing loan

guarantees based on business plans/

feasibility studies that demonstrate the

viability of the proposed business

activity. The company constantly

innovates with new guarantee products

to respond to the identified needs of

SMEs at different stages of development.

It currently offers six guarantee

products targeting SMEs in five

sectors: agriculture, high tech, industry,

tourism, and traditional crafts.

• Tunisie Leasing, Tunisia. The foremost

leasing company in the country, Tunisie

Leasing, entered the leasing market in

1984 in the belief that leasing was a

key source of finance to SMEs. With no

requirement for loan collateral, and a

generally lower risk burden to lenders,

leasing has essentially substituted for

bank credit for a number of SMEs. The

company has maintained its position

as market leader even while the leasing

industry has expanded and competitors

have established themselves in the

market. Its success is in part due to the

systematic approach it has developed

to assessing the leasing risk for SMEs

in the absence of complete financial

information.

• Egyptian Banking Institute (EBI),

Egypt. EBI is the official training arm of

the Central Bank of Egypt, serving the

professional development needs of all

banks in the country. Its mission is to

enhance the capabilities of the banking

sector and other financial stakeholders

through interactive educational programs,

training, up-to-date knowledge, and

consultancy. It is unique in the Deauville

Partnership countries (and in fact in the

MENA region) for having established an

SME Department and implemented a

complete range of training courses,

certification programs, and technical

assistance to increase the capacity of

banks for SME banking, while also

strengthening SME capacity to deal

with banks and develop bankable

proposals.

(iii) Business development support

(BDS) services for SMEs

• El Mobadara Community Development

and Small Enterprises Association,

Egypt. The Association has evolved

from a donor-funded project in the late

1990s into a self-sustaining non-profit

organization to support micro and

small enterprises (MSEs) through the

design and delivery of microcredit,

training, BDS services, technical

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

xi

assistance, and facilitation of access to

markets, financing and technology. The

case study illustrates good practice in

the provision of market-driven and fee-

based BDS services to MSEs. It also

underscores that effective BDS

provision is attained by experimenting

with different approaches, building the

capacity of BDS providers, ensuring

the quality of services, and being

sensitive to the specific BDS needs of

women-owned MSEs.

(iv) Development of women entrepreneurs/

women-owned MSMEs

• EntreElles en Régions, Morocco.

The program is implemented by the

government’s National Agency for the

Promotion of Small and Medium

Enterprises (ANPME), in partnership

with the German Agency for

International Cooperation (GIZ). Its

objectives are to build the capacity of

women entrepreneurs and their very

small and early-stage enterprises

through coaching, mentoring and the

formation of networks. The program is

an example of how dedicated efforts to

target improvements in the management

capacity of women can lead to

demonstrable results in terms of

enterprise development.

Concluding remarks

MSME development is increasingly

becoming a high priority for policymakers

in the Deauville Partnership transition

countries, given that the MSME sector

constitutes the backbone of the

economies and is the major source of

employment in these countries. Structural

deficiencies, both on the supply and

demand side, need to be resolved in order

to create both the quantity and quality

of jobs needed, and put the countries

on a pathway to an innovation-driven

knowledge economy. Learning from and

adapting good practices of institutions and

projects with a track record from within the

region, such as those profiled in this

publication, is of increased interest for

policymakers and affiliated agencies.

With transition countries making MSME

development a priority area since 2011,

a number of other new initiatives have

emerged, some supported by IFIs/ donors

and others by Deauville Partnership

governments and the private sector. These

include projects to address the equity gap

faced by promising new and growth-

oriented enterprises by increasing the

availability of early-stage venture capital

and angel investment; strengthen the

capacity of BDS providers; foster

entrepreneurship and business creation

among young people and women; promote

equality of economic opportunity in

disparate regions; and assist governments

in improving the business environment

for private sector growth.

At the present time, a great deal of

experimentation is taking place to determine

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

xii

the most effective approaches to stimulating

and strengthening entrepreneurial capacity

in Deauville Partnership countries. Efforts

should be made to monitor these

developments in order to identify the good

practice models from which all Deauville

Partnership countries and partners can

benefit. To advance learning about what

works best, more focus in the future

should be placed on performing impact

evaluations and sharing the results broadly

among Deauville Partnership partners.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

1

The African Development Bank (AfDB),

on behalf of the international financial

institutions (IFIs) participating in the

Deauville Partnership, launched a two-

volume study to lay the ground for more

coordinated and strategic support for

the development of micro, small and

medium enterprises (MSMEs) in Deauville

Partnership countries, especially those with

a strong employment-creation potential.

The objectives of the study are to enhance

knowledge exchange and coordination

among Deauville Partners and to improve

MSME development support interventions.

The study also lays the foundation for

further joint operations and research,

including actions by the Deauville

Partnership countries themselves. As it

covers activities by governments and

bilateral donors, it will help to streamline

the different current and emerging

initiatives around MSMEs in the region, as

well as across the various Deauville

Partnership pillars.

The study has four components:

i. A review of the recent literature on the

job-creating impacts of MSMEs.

ii. An analysis of the MSME landscapes

in Morocco and Tunisia, which

particularly requested this analysis,

including identification of the major

constraints to MSME development.

About the Deauville Partnership: The Deauville Partnership with Arab Countries in

Transition is an international effort launched in 2011 by the G8 at the Leaders Meeting in

Deauville, France, to support countries in the Arab world engaged in transitions toward

“free, democratic and tolerant societies.” During the G8 Finance Ministers’ meeting in

Marseille, France, in September 2011, ten international financial institutions agreed to set

up a coordination platform to facilitate joint operations and maximize synergies among

institutions in the region. The objectives of the platform, known as the Deauville

Partnership platform, are: (i) information sharing and coordination of activities among IFIs;

(ii) proactive identification of joint projects, policy and analytical work; (iii) regular

development of knowledge products; and (iv) monitoring and reporting on joint operations

in the region. The six transition countries targeted by the Deauville Partnership are: Egypt,

Jordan, Libya, Morocco, Tunisia and Yemen.

1. Introduction

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

2

iii. Mapping and analysis of current and

pipeline MSME support initiatives of

governments and IFIs/ donors in

Morocco and Tunisia to identify gaps in

addressing MSMEs’ constraints.

iv. Identification of good practices and

success stories in MSME support

instruments and programs (financial

and non-financial) in the region, and

profiling of a selection of these as

examples for replication or adaption in

other Deauville Partnership countries.

Results of the first three components are

published in Volume 1 of the study, Catalyzing

Job Creation and Growth through MSME

Development in Deauville Partnership

Countries: A Gap Analysis of Policy

and Program Support in Morocco and

Tunisia (AfDB, 2014a). This companion

volume, focusing on good practices in

entrepreneurship development and MSME

support, builds on the findings and

recommendations of Volume I, and aims to

provide concrete examples of policy

responses and how interventions by IFIs

and other donors could be implemented.

The objective is to share the “how-to”

of innovative and high-performing

entrepreneurship and MSME support

programs with a view to transferring

lessons learned to other Deauville

Partnership countries.

The sharing of good practices can

produce much value in helping countries

learn from each other’s effective approaches

in fostering start-ups and the growth of

MSMEs and alleviating constraints. Good

practices can be used to demonstrate

what works as well as supply knowledge

about how and why they work in different

situations and contexts. The exchange of

good practices can be a key instrument for

shaping policy and program actions, either

through the replication or adaptation of the

good practices or stimulation of policy

improvements in existing programs and

measures.

Hence, Volume II discusses nine good

practice initiatives from within the Middle

East and North Africa (MENA) region

geared to supporting entrepreneurship

and MSME development. This makes

the publication unusual because, more

traditionally, the region seeks traditionally

MENA countries have sought to emulate

good practices from outside the region.

There are a number of merits in selecting

good practices from within the region: (i)

there are few knowledge exchanges

between the countries, so awareness of

regional good practices is limited; (ii)

good practices from within the region

may be easier to adapt due

to the existence of contexts and histories

in MSME development support that

share similarities; (iii) good practices in

the region are not well documented,

but of increasing interest to MENA

countries; and (iv) it may be easier to

promote the role-modeling effect (i.e. if

Morocco can do it, then we, in another

MENA country, ought to be able to do it

as well).

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

3

For the purposes of this study a good

practice is broadly defined as one that

is well-documented, able to provide

evidence of success/ impact, and has the

potential to be scaled-up or serve as a

model for adaptation and transfer. The

good practices profiled were selected

using the following general criteria:

• Is it a policy, project, instrument or

other measure introduced by public

authorities or non-governmental MSME

support organizations at the national,

regional or local level with the aim of

supporting entrepreneurship and

MSME development?

• Is it particularly targeted at MSMEs (to

include new business creation) and

taking the needs of new entrepreneurs

and/ or MSMEs into account?

• Has it delivered tangible results (e.g.

created jobs, fostered entrepreneurship,

stimulated the creation of new businesses,

improved access to financing, improved

the operating performance and capacity

of MSMEs)?

• Is it a model or approach with useful

lessons for other Deauville Partnership

countries and potential for replication

or transfer?

Against the backdrop of the most

critical areas to be addressed in MSME

development in the Deauville Partnership

countries, examples of good practice were

identified in two ways. First, the Deauville

Partnership Secretariat sent a request to

the Partner countries, asking: (i) what types

of good practices they would like to know

more about from the other Deauville

Partnership countries, i.e. priority areas

where knowledge about what works well

would be of benefit to them; and (ii) for

nominations of good practice initiatives

from within their own country, according

to the set of criteria, with their reasons

for considering this as a good practice.

Second, AfDB conducted study missions

in Egypt, Morocco and Tunisia to validate

the list of nominated good practices. This

involved meetings with stakeholders to

gather more information on each of the

organizations/ practices put forward for

nomination.

The profiles cover some of the critical

MSME support areas in the Deauville

Partnership countries: stimulating an

entrepreneurial culture by promoting

entrepreneurship in the education system;

support for the creation of new enterprises;

improving access to MSME financing; the

offer of business development support to

existing micro and small enterprises; and

fostering the development of women’s

entrepreneurship (Table 1). The profiled

good practices have been particularly

beneficial in a national context and could

be of interest to other Deauville Partnership

countries.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

4

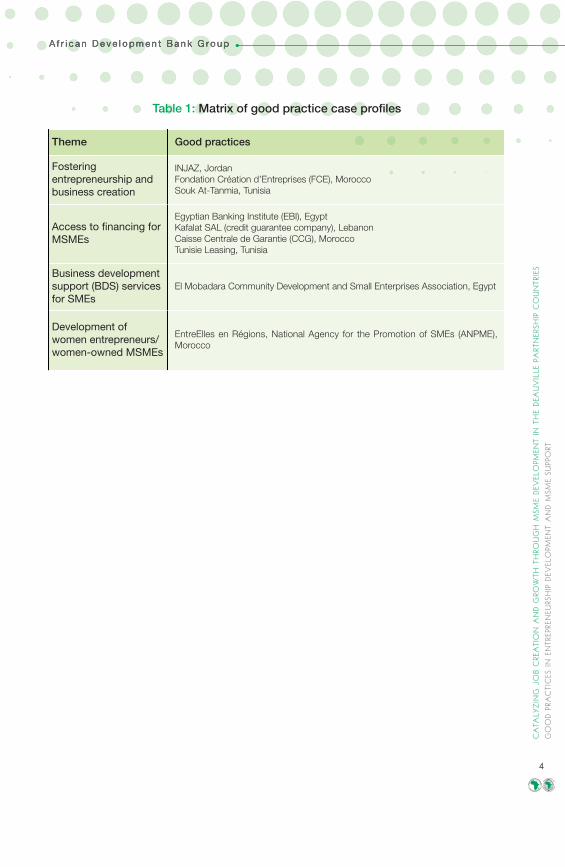

Theme Good practices

Fostering entrepreneurship andbusiness creation

INJAZ, JordanFondation Création d’Entreprises (FCE), MoroccoSouk At-Tanmia, Tunisia

Access to financing forMSMEs

Egyptian Banking Institute (EBI), EgyptKafalat SAL (credit guarantee company), LebanonCaisse Centrale de Garantie (CCG), MoroccoTunisie Leasing, Tunisia

Business developmentsupport (BDS) servicesfor SMEs

El Mobadara Community Development and Small Enterprises Association, Egypt

Development ofwomen entrepreneurs/women-owned MSMEs

EntreElles en Régions, National Agency for the Promotion of SMEs (ANPME), Morocco

Table 1: Matrix of good practice case profiles

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

5

2. Fostering Entrepreneurship and Business Creation

Stakeholders in all the Deauville

Partnership countries suggest that

the culture of entrepreneurship is weak.

Although governments have implemented

initiatives to bolster the role of micro, small

and medium enterprises (MSMEs) in

private sector development, none of

the countries has an approved national

policy in place for entrepreneurship and

MSME development to specifically guide

comprehensive, integrated actions in the

field.

As noted in Volume 1 of this study,

research carried out in a number of

countries reveals that start-ups and young

enterprises (less than five years old) are

responsible for the majority of gross and

net new jobs. Although failure rates among

new start-ups are higher than among

established MSMEs, the jobs created by

the new enterprises that survive more than

compensate for the total job loss resulting

from the downsizing and death of

enterprises of all sizes and ages. There is

also evidence that the survival rate of new

start-ups can be improved by offering skills

development, training, advisory and

coaching support to entrepreneurs during

the pre-start-up, start-up and post-start-

up stages. To grow the economy, new

start-ups are needed to replace exiting

firms of all ages and sizes, generate

economic renewal, and introduce

innovativeness in products and services to

enhance overall productivity.

Increasing the start-up rates in an

economy should therefore be a policy

priority of governments. This is even more

important in countries with a low density of

MSMEs, such as the case in Deauville

Partnership countries where, even though

MSMEs make up over 99% of all private

enterprises, the private sector is not

growing fast enough to absorb surplus

labor. This calls for interventions geared to

altering the trajectory of start-up rates,

which unattended are unlikely to change

substantially. Experience in other countries

indicates that effective actions include

promoting a stronger culture of

entrepreneurship and putting in place

specific support systems to inspire future

entrepreneurs and equip them with the

knowledge, skills, and competencies to

identify high-potential business ideas,

develop these into viable business models,

and mobilize the necessary resources to

launch them into the marketplace.

One of the key mechanisms for building a

stronger entrepreneurship culture is

integrating entrepreneurship in the

education system. This introduces a large

number of young people to the issue of

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

6

entrepreneurship and plants the seed

of “creating your own job” and becoming

an employer rather than an employee

working for someone else. In the Deauville

Partnership countries, where youth

unemployment rates are exceedingly high

and there are limited opportunities for

new labor market entrants to secure paid

jobs in the formal sector of the economy

(especially graduates), increasing the

level of entrepreneurship-related knowledge

and skills should be a policy imperative.

In addition, it is critical to implement

support programs to build the level of

entrepreneurial capacity, and specifically to

assist young people in the business

creation process. This can be achieved by

offering entrepreneurship training programs

that are combined with coaching,

mentoring and other forms of technical

and financial assistance to assist the new

entrepreneurs through all parts of the start-

up process, including the post-creation

phase.

The good practice profiles in this section

focus on initiatives to integrate business

and entrepreneurship in the educational

system and to foster the business creation

process.

2.1 Strengthening the Culture ofEntrepreneurship through the EducationSystem

In the Deauville Partnership countries and

across the Middle East and North Africa

(MENA) region, a common challenge to

MSME development is the lack of

entrepreneurial and management capacity.

Considerable public resources are often

invested in programs to upgrade the

management quality and productive

capacity of MSMEs so they are able to

compete and survive in the globalization

era, such as training, counseling and

consultancy services. However, relatively

few businesses are reached by these

support mechanisms.

Over the past two decades, international

organizations and governments have come

to recognize that cultural aspects need to be

taken into account as one of the important

factors influencing the development of

entrepreneurship and enterprise creation.

The major policy question was about

how to create a more favorable societal

climate for entrepreneurship to unleash

the entrepreneurial potential of young

people. This led to an examination of the role

of the education system in developing

entrepreneurial mind-sets and key areas of

competence. Entrepreneurship education is

now widely considered as one of the

determinants of the level of entrepreneurship

in a country and an indicator of its

entrepreneurship performance (OECD,

2009b). By introducing entrepreneurship in

the educational curriculum, countries can

build their entrepreneurial capacity and

ability.

The goals of entrepreneurship education

policies are to promote an entrepreneurial

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

7

mind-set from an early age, adopt

entrepreneurship as a key competency in

curriculum outcomes and expose students

to the principles and practices of

entrepreneurship and starting a business.

Education for entrepreneurship is expected

to enhance the supply of entrepreneurs

through three mechanisms (Levie and

Autio, 2008):

• A cultural effect on students’ attitudes

and behavioral dispositions (mind-set

aspects);

• Enhanced cognitive ability to recognize

and assess opportunities; and

• Provision of the required skills to start

and grow a business.

The World Economic Forum (WEF) argues

convincingly that entrepreneurship education

is essential for developing the human

capital necessary for the society of

the future, and that by making

entrepreneurship education available to

young people (and adults), countries are

preparing the next wave of entrepreneurs

“to enable them to shape our institutions,

businesses and local communities”

(WEF, 2009). In addition to evidence that

students who take entrepreneurship

courses are more likely to become future

entrepreneurs, the skills and knowledge

learned in these courses can provide

better preparation for all forms of work

(European Commission, 2012).

Governments in a number of developed

(and developing) countries have made

entrepreneurship education a priority of

their entrepreneurship policy efforts. These

include implementing national strategies

on entrepreneurship education to integrate

entrepreneurship into the curriculum at

all levels of the educational system

from kindergarten through to university.

However, there is limited evidence of

entrepreneurship education policies in

the Deauville Partnership countries. The

WEF (2011) has recommended that

entrepreneurship be brought into

classrooms throughout the Arab world

with the aim of teaching every student in

high school and university the principles of

entrepreneurship.

In the meantime, there are some bottom-

up and often donor-led initiatives to bring

entrepreneurship content into schools and

college classrooms in some of the Deauville

Partnership countries. The International

Labour Organization (ILO), for example, has

made inroads into the educational system in

Egypt and Jordan, to offer its Know About

Business curriculum. In addition, a few

universities are now offering credit courses

in entrepreneurship and encouraging

students to start their own businesses.

The most comprehensive attempt to bring

economic, financial literacy, business,

and entrepreneurship education into

classrooms across Deauville Partnership

countries is the INJAZ program. INJAZ is

the Arab affiliate of Junior Achievement, a

US-based non-profit entity started in 1919

with a mission to foster work readiness,

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

8

entrepreneurship and financial literacy skills

to students from kindergarten to the final

year of high school, through the volunteer-

delivery of experiential learning programs

to inspire students to dream big and reach

their potential. Currently, INJAZ programs

have been launched in Jordan (1999),

Egypt (2003), Morocco (2007), Tunisia

(2010) and Yemen (2011). These programs

provide education and training to Arab

youth in work readiness, financial literacy

and entrepreneurship, working closely with

ministries of education and the corporate

community. A national board of directors

leads each INJAZ country operation, with

the INJAZ Al-Arab regional board

responsible for directing overall strategy

and organizational governance.

INJAZ Jordan was nominated and

selected as a good practice for this

study because, first of all, it is the oldest

and most established INJAZ operation in

the Deauville Partnership countries;

second, it has made impressive efforts in

expanding the reach of its programs to

students and vulnerable youth in all

regions of the country, engaging corporate

sponsors and volunteers, and partnering

with the Ministry of Education, as well as

the Ministry of Planning and International

Cooperation; and finally, because it is

recognized as a leading youth economic

education organization in Jordan and

across the Arab world.

INJAZ, Jordan

Overview: INJAZ is a non-profit organization

with the mission to “inspire and prepare

young Jordanians to become productive

members of society and accelerate the

development of the national economy”2.

It aims to unite Jordanians and key

stakeholders around “the common goals

of creating jobs, building a stable economy,

and providing a higher standard of living”.

INJAZ delivers a range of experiential

learning programs through three main

program units that develop students’ soft

skills, professional ambitions, and passion

for achievement: (i) the Skills Building

Program, targeting students in grades

7-11 in public and military schools, and in

schools run by the United Nations Relief

and Works Agency for Palestine Refugees

in the Near East (UNRWA); (ii) the Work

Readiness Program, reaching out to youth

in vocational training centers and youth

centers; and (iii) the Entrepreneurship and

Employment Program, for university and

college students. INJAZ works in full

cooperation with the Ministry of Education,

the Ministry of Higher Education, and the

King Abdullah II Fund for Development

(KAFD).

2 INJAZ website at: http://www.injaz.org.jo/

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

9

A. Background and institutional history

INJAZ was introduced in Jordan in 1999

as a Save the Children project funded by

the United States Agency for International

Development (USAID). In 2001, it was

re-launched as an independent, non-profit

Jordanian organization under the patronage

of Her Majesty Queen Rania Al Abdullah.

Through cooperation with its partners in

government, the private sector, civil

society, and the formal educational

system, INJAZ seeks to empower youth

with the skills and knowledge needed to

successfully transition from the education

system to the workplace, both as

professionals and entrepreneurs.

One of INJAZ’s most important

achievements was to secure the decision

Quick facts

Start date 1999

Number of employees 63

Number of volunteersIn total, 22,000 qualified volunteers have been recruited to deliver programs;3,636 volunteers were involved in the programs during the 2012/13 academicyear

Beneficiaries

School students at public, military, and UNRWA schools, and in centers foryouth with disabilitiesStudents at public and private universities and collegesYouth at vocational training centers and youth centers

Total number of students reachedthrough INJAZ programs sinceinception

900,000

Number of schools and universities offering INJAZ programs (2012/13)

More than 200 schools; 36 universities and community colleges

Number of students/ youth participating in INJAZ programs(2012/13)

127,452 students in schools, universities and colleges; 6,103 youth in youthcenters

Number of strategic partnerships (2012/13)

More than 300 with the private and public sector

Number of universities and community colleges participatingin entrepreneurship-related programs (2012/13)

36

Number of university and community college students participating in entrepreneurship-related programs

8,221

Number of students in Entrepreneurial Master Class/ My Entrepreneurial Project (2012/13)

12,165 in 120 public schools; 2,501 in 26 youth centers (total 14,766)

Number of students participatingin the Business EntrepreneurshipCompany Program (2012/13)

309 school students running 10 ventures (Company Program)1,815 university and college students running 77 ventures (Company Start-upProgram)1,574 students with 66 ventures (“We Are Social Leaders” Program)

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

10

of the Ministry of Education in 2003 to

mainstream INJAZ programs in the public

school system. Prior to this, INJAZ had to

offer its programs to students as an

extracurricular activity. With the Ministry’s

approval, INJAZ was allowed to deliver one

class a week in schools, now more than

200 schools, to students in grades 7-12.

INJAZ programs focus mostly on skills

development (work readiness, financial

literacy, soft skills, leadership, and

entrepreneurship), and include several

business and social entrepreneurship-

related programs and projects, such as the

Social Leaders Program, the Entrepreneurial

Master Class, and the Company Start-up

Program (where students start and run

a company for an academic year). The

Ministry has requested INJAZ to expand

into more schools and to train teachers on

the use of participative teaching-learning

approaches. Since 2006, INJAZ has been

a member of the Curricula and Training

Unit within the Ministry’s Committee for

Curricula Development.

Also critical in the development of INJAZ is

its partnership with the KAFD, which dates

back to 2004. Through this partnership

the two organizations have coordinated

their efforts to help youth at Jordanian

universities and colleges develop their life

skills and prepare to enter the job market.

Its partnership with the KAFD has also

greatly facilitated INJAZ’s access to

students in 36 universities and community

colleges across Jordan.

Through its various growth phases, INJAZ

has adjusted its organizational structure,

added new courses and programs, and

expanded it services to include job and

career fairs, social and business

entrepreneurship competitions, start-up

support, and opportunities for students to

dialogue with and learn from social and

business leaders in the community. For

example, in the 2005/06 academic year, it

introduced job shadowing and work

placements for students. In 2006/07, it

reviewed its curriculum, overhauled key

components, introduced new courses, and

entered Jordanian colleges for the first time,

primarily through the Company Start-up

Program. It began with four colleges, where

INJAZ programs provided the first

opportunities for these students to benefit

from economic/ entrepreneurial education

of any kind. In May 2006, it introduced the

School Adoption Program that became an

important part of its sustainability strategy.

With this approach, corporate sponsors

could align their financial contribution to

specific schools in specific regions, which

strengthened their commitment to their

local communities and to INJAZ’s programs.

During the 2009/10 year, INJAZ realized that

it needed to restructure its organization to

achieve its growth and expansion targets.

This involved hiring additional staff,

outsourcing human resources to improve

management of human resource affairs, and

expanding into a new office. INJAZ also

developed a Quality Management Plan,

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

11

to monitor, evaluate, and improve its

operations, programs, and impact more

systematically. Key performance indicators

were also defined for INJAZ’s operations,

programs, and activities to foster

improvements in staff productivity, work

quality, teamwork, and problem solving.

INJAZ has received certification from the

International Organization for Standardization

(ISO). Its approach to ISO certification and

the regular external and internal audits of its

organization and operations provide a

systematic mechanism for assessing the

strengths and weaknesses of its governance,

management, and systems, and for working

towards continuous improvement.

Objectives: INJAZ defines its objectives in

the form of intermediate outcomes:

• Secondary school students (ages 11-

18) have developed their financial,

ethical leadership and business skills to

become more competent and aware of

their career choices.

• Students in vocational training centers

have enhanced their work-readiness

skills and career-planning abilities, and

have better access to employment

opportunities.

• University and college students

have access to better job opportunities,

including self-employment, by developing

their business entrepreneurship, social

leadership and employment skills.

• Jordanian society is more appreciative

and enthusiastic about volunteerism,

rooting it deeply in traditional beliefs

and community practices.

• The Jordanian private sector is

increasingly engaged in youth

development, realizes the value of

investing in youth, and is more socially

responsible.

• INJAZ’s impact and outreach is scaled

up to address national needs through

partnership with the government,

making it a key player in youth

advancement and volunteerism.

• INJAZ’s sustainability and growth is

attained by enhancing the quality of

its operations, institutional capacity,

governance, financial position, and

brand equity.

Beneficiaries: INJAZ programs are

implemented for students in secondary

schools, colleges/ universities and

vocational training centers. In recent years,

INJAZ has also focused on more inclusive

outreach, adapting many programs for

implementation in various social institutions

and youth centers (including centers for

orphans and for youth with disabilities),

and targeting youth who have exited the

education system early or otherwise find

themselves at the cusp of adulthood and

entry into the job market. While many

programs are designed for a particular

age set, some programs such as Job

Placement under the Work Readiness

Main Program have a broader beneficiary

pool and target all unemployed persons

between 16 and 30, regardless of their

educational background.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

12

B. Organizational model

INJAZ management is led by its Chief

Executive Officer and its Board of Trustees.

The organization is structured in eight

major units including three program

implementation units – Skills Building

Program, Work Readiness Program, the

Entrepreneurship and Employment Program

– and three support units Communications

and Partnership Unit, Business Development

Unit (responsible for the quality management

system, monitoring, evaluation and impact

assessment, and developing the growth

and sustainability plan), and Finance and

Administration Unit.

The Board of Trustees consists of 48

members who represent leading local and

international organizations and private

companies. Its functions are to provide

insight into the local business and political

environment, guide the design of INJAZ

programs, and establish the direction of

future growth. Having such a large Board

of Trustees is an effective strategy both for

engaging the corporate community in the

vision of INJAZ and its activities, and for

garnering sponsorship for its various

programs and initiatives. The 11-member

Board of Directors is elected from among

members of the Board of Trustees and

works closely with management to achieve

INJAZ’s mission and goals.

INJAZ prepares an annual action plan,

assigning responsibilities and setting

strategies and targets for each

implementation and support unit, as well

as targets for the delivery of each INJAZ

program (including the number of

educational institutions to be served, the

number of students to be reached with

each course/ program, and the number of

volunteers to be recruited). At the end of

each program year, INJAZ prepares an

annual report measuring its actual

achievements against these planned targets.

Staffing: INJAZ has 63 employees,

located in eight offices and working in 12

governorates across Jordan. The team

ensures proper implementation of the

programs and prepares INJAZ volunteers

to reach out to INJAZ students. Supervision

and direction of the staff is provided by the

Chief Executive Officer under the guidance

and support of the Board of Directors.

Responsibilities include recruiting and

training volunteers to teach the INJAZ

programs; organizing extracurricular

events and activities to inspire and

motivate students to strive for success

(e.g. job fairs, seminars, exchanges);

recruiting business leaders to mentor

students in INJAZ’s entrepreneurial, career

development, and inspirational programs;

attracting corporate sponsors; liaising

with the Ministry of Education, the KAFD,

universities/ colleges and schools; and

developing all necessary partnerships to

realize expansion of the programs to more

schools and students.

INJAZ is committed to building the

knowledge and skills of its staff by supporting

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

13

their participation in training and capacity-

building workshops (e.g. time management,

presentation skills, mentoring, quality

management systems, client service),

internal review and assessment workshops,

and visits to similar programs outside

Jordan in order to learn from their

experiences. It has also developed

personnel manuals and implemented a

performance evaluation system.

C. Operational model

Products and services: INJAZ has

adopted a number of successful programs

from several international organizations.

It examines the list of offerings and

determines which particular courses to

introduce in Jordan. Course materials are

then translated into Arabic and adapted

to the Jordanian context. Many INJAZ

programs have also been developed by

the INJAZ Program Development team

to ensure that they serve the needs of a

wide range of youth of different ages,

educational backgrounds, and abilities.

INJAZ Jordan programs (see Table 2) are

clustered in three streams: Skills Building,

Work Readiness and Entrepreneurship and

Employment.

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

14

Main Program Unit Tracks Programs Target Group

Skills Building Program

Schools andspecial education centers

Financial and socialeducation

More Than MoneyMy Well Being

Grade 7

Economics for Success Social ResponsibilityArtlink

Grade 8

My Money Business Leadership Course

Grade 9

Exploring Economics Creative Problem SolvingDebate

Grade 10

My Financial Career OptionsYoung Volunteers Day

Grade 7-11

Business and entrepreneurship

It’s My Business Grade 7

Be Entrepreneurial Grade 8Enterprise Business Challenge and Competition

Grade 9

Presentation Skills and CompetitionCompany Program and Trade Fair/Competition

Grade 10

Entrepreneurial Master ClassMy Entrepreneurial Project

Grade 11

TEAM Program and Competition Youth with disabilities

Career guidance

Personal Life Planning Grade 7

My Career Options Grade 8

Career Month Grade 9

Job ShadowBusiness Leaders Campaign

Grades 10–11Grades 10–11

INJAZ teacher awards

Work Readiness

Vocational trainingcenters and youthcenters

Soft skills

Professionalism at Work

Youth ages 15–25 in vocational training centers and youth centers

Business Ethics

Work Skills

Career development

Ask the Expert

Job for a Day

Career Wellness

Job placementJob Matching

Internship Program

Entrepreneurshipand Employment

Universities andcolleges

Business andentrepreneurship

Company Start-Up Program and TradeFair/ Competition

Youth ages 18–25 in universities and colleges

Enterprise Development Program

Socialentrepreneurship

We Are Social Leaders and Competition

Social Leaders Program and Competition

Employment

My Path to Employment

Communication Skills

Ethical Business

7iwar Al Ajyal

Link2Job

Source: INJAZ officials

Table 2: INJAZ Jordan programs by topic and age group or level of education

CATA

LYZING

JOBCRE

ATION

ANDGRO

WTH

THRO

UGH

MSM

EDEV

ELOPM

ENTIN

THEDEA

UVILLE

PART

NER

SHIP

COUNTR

IES

GOODPRACTICES

INEN

TREPRE

NEU

RSHIP

DEV

ELOPM

ENTANDMSM

ESU

PPORT

15

Every university in every governorate offers

INJAZ courses and the majority offers the

Company Start-up Program. However,

only the German Jordanian University has

institutionalized the INJAZ courses for

credit. In 2013, Mu’tah University piloted a

model that embeds INJAZ soft skills

workshops/ courses within accredited

university courses. Mu’tah University is

now considering accrediting INJAZ soft

skills courses in the coming years.

In 2012/13, INJAZ established a new

Enterprise Development Program to

support the successful development of

enterprises arising from the Company

Start-up Program and INJAZ’s other social

and business entrepreneurship programs,

through an array of business support

services and resources coordinated by the

Business Development Unit. This takes

INJAZ into a new role beyond awareness-

raising and skills training.

Based on surveys of the evolving needs

and requirements of beneficiaries and

stakeholders, INJAZ is constantly reviewing

its menu of programs, adding new options,

and adapting approaches. For example, in

2011/12, it launched the Enterprise

Business Challenge Program, which aims

to inspire young people from deprived

communities to realize their talents and

potential. The program uses innovative

computer simulation training that allows

students to create and manage their own

virtual companies and perform virtual

financial transactions and trading. The

eight-school pilot in 2011/12 is being

expanded to 40 classes across Jordan.

Another program introduced in 2011/12 is

the Intel Youth Enterprise Challenge, which

helps students gain knowledge in

identifying key social issues and how they

could be addressed by innovative solutions

using technology.

Approach: Courses are taught by qualified

volunteers, so one of the major INJAZ

activities is recruiting and training the

volunteers who deliver all the courses in

schools and participate in some of the

extracurricular programs. The volunteers

spend one hour a week in school,

university or college classrooms to teach

the courses, assisted by the normal

classroom teachers. Training sessions

are held on an annual basis to prepare

as many as 750 new volunteers. The

performance of volunteers in the classroom

also has to be monitored, as well as efforts

made to retain them on an ongoing basis.

In 2006/07, only 40% of volunteers came

from the corporate sponsors; by 2011/12,

this had increased to 80%, reflecting

growth in the number of corporate

sponsors and their greater engagement in

the program.

INJAZ staff also provide training and

orientation to regular classroom teachers

who assist or aid the volunteers.

INJAZ organizes a number of annual

competitions for students participating in

programs that result in projects. In these

competitions, student teams compete with

each other for various awards associated

with project performance and outcomes.

These competitions can be motivating for

the students and contribute to developing

their confidence and presentation skills, as

well as exposing them to networks and

contacts that can be of value to them in

the future.

In promoting its programs, INJAZ makes

extensive use of social media (Facebook,

Twitter) to ensure that all its campaigns,

activities, programs, events and success

stories are broadly covered.

D. Financial model

INJAZ’s annual income comes from its

patrons (Board of Trustee members), the

government, corporate sponsors and

donor organizations. Its ability to offer (and

expand) programs depends on the amount

of funding it is able to raise, and so

financial sustainability is a major concern.

INJAZ has been innovative in its approach

to attracting funds. For example, increasing

the number of members on the Board of

Trustees is part of the sustainability plan.

Each member not only brings expertise

into the organization, but also pays an

annual fee of US$10,000 to the INJAZ

endowment fund, which builds the capital

of the organization. Aggressive recruiting is

done to sign on more corporate sponsors.

INJAZ develops a fundraising menu which

is presented to the public and private

sectors to help them in identifying various

funding opportunities. Thus sponsorship

can be tied to specific programs, to specific

governorates, or to specific schools.

In 2007, Credit Suisse support enabled

INJAZ to deliver the My Money Business

course to Grade 9 students; in 2009/10,

HSBC Bank granted INJAZ the funds to

adapt the More than Money curriculum for

delivery to about 1,000 students in 28

classes at ten schools; and the 2011/12

Enterprise Business Challenge Program

was funded by the British Embassy in

Amman. The School Adoption approach,

introduced in 2006 and supported with a

national media campaign (newspaper ads,

billboards), has been successful in attracting

corporate sponsors. In its first year, 37

schools were adopted, rising to more than