cassandra cole and kathleen mccullough co-editors · while capital provides a safety net that helps...

TRANSCRIPT

Journal of Insurance Regulation

Cassandra Cole and Kathleen McCulloughCo-Editors

Vol. 34, No. 6

Integrated Determination of Insurer Capital, Investment and Reinsurance Strategy

Hong MaoJames M. Carson

Krzysztof M. Ostaszewski

JIR-ZA-34-06

Accounting & ReportingInformation about statutory accounting principles and the procedures necessary for fi ling fi nancial annual statements and conducting risk-based capital calculations.

Consumer InformationImportant answers to common questions about auto, home, health and life insurance — as well as buyer’s guides on annuities, long-term care insurance and Medicare supplement plans.

Financial Regulation Useful handbooks, compliance guides and reports on fi nancial analysis, company licensing, state audit requirements and receiverships.

LegalComprehensive collection of NAIC model laws, regulations and guidelines; state laws on insurance topics; and other regulatory guidance on antifraud and consumer privacy.

Market RegulationRegulatory and industry guidance on market-related issues, including antifraud, product fi ling requirements, producer licensing and market analysis.

NAIC ActivitiesNAIC member directories, in-depth reporting of state regulatory activities and offi cial historical records of NAIC national meetings and other activities.

For more information about NAIC publications, view our online catalog at:

http://store.naic.org

Special StudiesStudies, reports, handbooks and regulatory research conducted by NAIC members on a variety of insurance-related topics.

Statistical ReportsValuable and in-demand insurance industry-wide statistical data for various lines of business, including auto, home, health and life insurance.

Supplementary ProductsGuidance manuals, handbooks, surveys and research on a wide variety of issues.

Capital Markets & Investment AnalysisInformation regarding portfolio values and procedures for complying with NAIC reporting requirements.

White Papers Relevant studies, guidance and NAIC policy positions on a variety of insurance topics.

© 2015 National Association of Insurance Commissioners. All rights reserved.

Printed in the United States of America

No part of this book may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or any storage or retrieval system, without written permission from the NAIC.

NAIC Executive Offi ce444 North Capitol Street, NWSuite 700Washington, DC 20001 202.471.3990

NAIC Central Offi ce1100 Walnut StreetSuite 1500Kansas City, MO 64106816.842.3600

NAIC Capital Markets& Investment Analysis Offi ceOne New York Plaza, Suite 4210New York, NY 10004212.398.9000

The NAIC is the authoritative source for insurance industry information. Our expert solutions support the efforts of regulators, insurers and researchers by providing detailed and comprehensive insurance information. The NAIC offers a wide range of publications in the following categories:

The following companion products provide additional information on the same or similar subject matter. Many

customers who purchase the Journal of Insurance Regulation also purchase one or more of the following

products:

Companion Products

Federalism and Insurance Regulation

This publication presents a factual historical account of the development of the

framework for insurance regulation in the United States. It does so in part by

using illustrative early statutes, presenting them chronologically, and in part by

using cases that illustrate the interpretation of the crucial later statutes.

Copyright 1995.

Regulation and the Casualty Actuary

This anthology reprints 20 important papers from past issues of the Journal of

Insurance Regulation that are most relevant for practicing actuaries and state

insurance regulators. It covers a wide range of issues, such as ratemaking,

auto insurance pricing, residual markets, reserving and solvency monitoring.

This invaluable reference explains these complex topics in straightforward,

non-technical language. Copyright 1996.

International orders must be prepaid, including shipping charges. Please contact an NAIC Customer Service Representative, Monday - Friday, 8:30 am - 5 pm CT.

Editorial Staff of the Journal of Insurance Regulation Co-Editors Case Law Review Editor Cassandra Cole and Kathleen McCullough Jennifer McAdam, J.D. Florida State University NAIC Legal Counsel II Tallahassee, FL

Editorial Review Board Cassandra Cole, Florida State University, Tallahassee, FL

Lee Covington, Insured Retirement Institute, Arlington, VA

Brenda Cude, University of Georgia, Athens, GA

Robert Detlefsen, National Association of Mutual Insurance Companies, Indianapolis, IN

Bruce Ferguson, American Council of Life Insurers, Washington, DC

Stephen Fier, University of Mississippi, University, MS

Kevin Fitzgerald, Foley & Lardner, Milwaukee, WI

Robert Hoyt, University of Georgia, Athens, GA

Alessandro Iuppa, Zurich North America, Washington, DC

Robert Klein, Georgia State University, Atlanta, GA

J. Tyler Leverty, University of Iowa, Iowa City, IA

Andre Liebenberg, University of Mississippi, Oxford, MS

David Marlett, Appalachian State University, Boone, NC

Kathleen McCullough, Florida State University, Tallahassee, FL

Charles Nyce, Florida State University, Tallahassee, FL

Mike Pickens, The Goldwater Taplin Group, Little Rock, AR

David Sommer, St. Mary’s University, San Antonio, TX

Sharon Tennyson, Cornell University, Ithaca, NY

Purpose

The Journal of Insurance Regulation is sponsored by the National Association

of Insurance Commissioners. The objectives of the NAIC in sponsoring the

Journal of Insurance Regulation are:

1. To provide a forum for opinion and discussion on major insurance

regulatory issues;

2. To provide wide distribution of rigorous, high-quality research

regarding insurance regulatory issues;

3. To make state insurance departments more aware of insurance

regulatory research efforts;

4. To increase the rigor, quality and quantity of the research efforts on

insurance regulatory issues; and

5. To be an important force for the overall improvement of insurance

regulation.

To meet these objectives, the NAIC will provide an open forum for the

discussion of a broad spectrum of ideas. However, the ideas expressed in the

Journal are not endorsed by the NAIC, the Journal’s editorial staff, or the

Journal’s board.

* Shanghai Second Polytechnic University; [email protected]. ** Terry College of Business, University of Georgia; [email protected]. *** Illinois State University; [email protected]. **** State Farm Insurance and Illinois State University; [email protected].

© 2015 National Association of Insurance Commissioners

Integrated Determination of Insurer

Capital, Investment and Reinsurance Strategy

Hong Mao* James M. Carson**

Krzysztof M. Ostaszewski*** Wei Hao****

Abstract

Based on the criteria of the Swiss Solvency Test, Solvency II, RBC and minimizing total frictional cost, we establish integrated models to determine the adjustment capital required, investment strategy and reinsurance strategy by numerically analyzing the effect of several important parameters. Results illustrate that when the cost of reinsurance is low or the frictional cost of capital is high, reinsurance is especially attractive as an effective instrument for capital management. However, when the cost of reinsurance is high or the frictional cost of capital is low, capital can partly or fully substitute for reinsurance. Furthermore, in most cases, setting the regulatory capital level either by Solvency II or the Swiss Solvency Test leads to greater prudence than determining insurer capital level by minimizing total frictional cost, except when the cost of capital is very low.

1

Journal of Insurance Regulation

© 2015 National Association of Insurance Commissioners

Introduction Insurers use various strategies, methods and tools to manage risk, including

reinsurance, increasing the amount of capital held and optimizing the investment portfolio. In this light, insurer risk management may be viewed as a system engineering project whereby managers assess the costs and benefits of various financial tools to determine optimal risk management strategies to achieve overall profitability and financial strength.

While capital provides a safety net that helps an insurer reduce the likelihood of financial distress, increasing the amount of capital held is costly (Staking and Babbel, 1995). Developments in global insurance regulation are aimed at risk-based supervision that accounts for all financial, insurance and business risks, particularly asset and liability risks. For example, the Swiss Solvency Test (SST) proposes the concept of target capital.1 Solvency II, the European Union (EU) framework for prudential regulation of insurers, presents the concept of the solvency capital requirement (SCR).2 In the U.S., necessary economic capital is defined by the NAIC in terms of an insurer’s RBC. Eling, Schmeiser and Schmit (2007), Eling and Holzmuller (2008), Holzmuller (2009), Cummins and Phillips (2009), and Gatzert and Wesker (2012) analyze and compare the recent developments in global solvency regulation.

Dhaene et al. (2003) discuss the determination of optimal capital by minimizing the capital cost above risk-free interest and insolvency cost. Chandra and Sherris (2006) note that minimizing frictional cost of capital produces an optimal capital level based on value at risk (VaR) at much lower levels than observed.3 They established single-period and multiple-period optimization models under the assumption that the return on insurer assets is deterministic. For a discussion of other research addressing capital and capital allocation, see Mao and Ostaszewski (2010).

1. As discussed in Luder (2005), the Swiss Solvency Test (SST) is a stochastic risk model

that includes scenarios for market risk, insurance risk and credit risk in order to determine target capital.

2. Solvency II aims to be a forward-looking, risk-sensitive regulatory structure, focusing on capital adequacy, governance and overall risk management through a total balance sheet approach. Solvency II further develops insurance regulation, similar to developments in bank regulation in Basel II.

3. Frictional cost of capital is defined as taxation and investment cost on assets backing the required capital over the projected lifetime of underlying risk. See: Smith (2010) and www.pwc.com/gx/en/actuarial-insurance-services/pdf/european-insurance-cfo-forum-mcev.pdf.

2

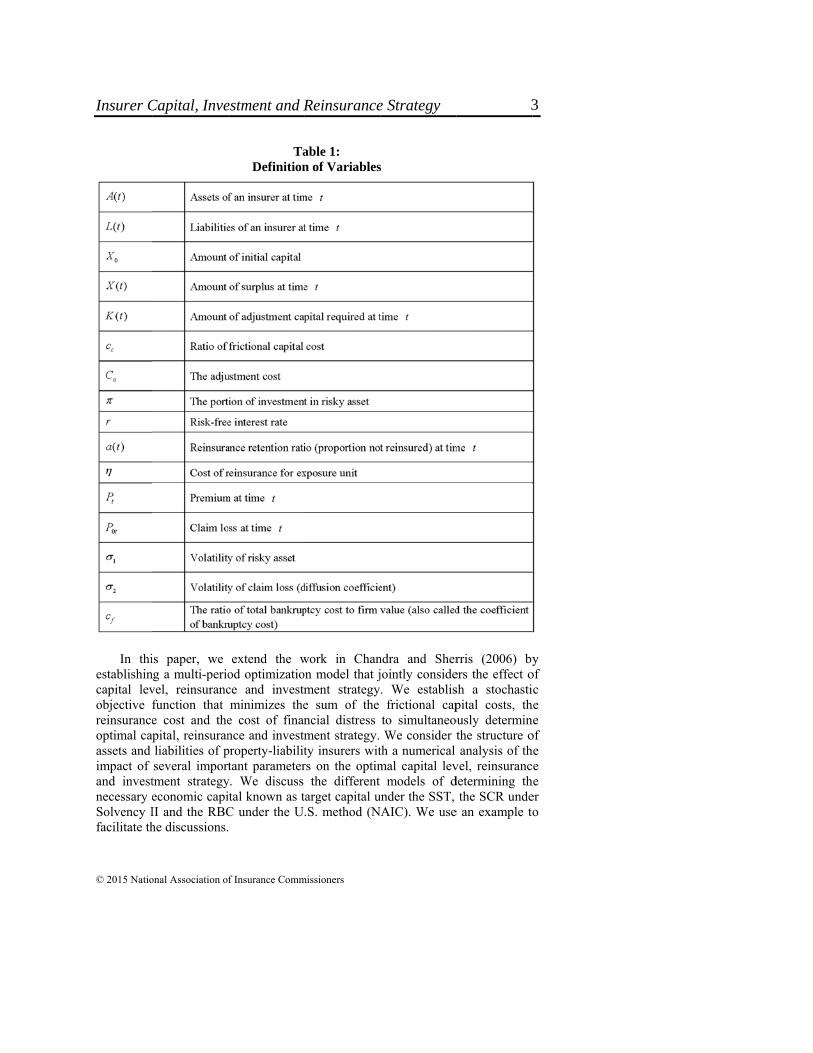

Insurer C

© 2015 Natio

In thi

establishincapital levobjective reinsuranceoptimal caassets and impact of and investnecessary eSolvency Ifacilitate th

Capital, Inve

onal Association o

is paper, we ng a multi-periovel, reinsurancfunction that e cost and the

apital, reinsuranliabilities of pseveral importtment strategyeconomic capiII and the RBChe discussions.

estment and R

f Insurance Comm

TaDefinition

extend the wod optimizatioce and investmminimizes the

e cost of finannce and investmproperty-liabilittant parameter

y. We discuss ital known as tC under the U

Reinsurance

missioners

able 1: n of Variables

work in Chanon model that jment strategye sum of the ncial distress ment strategy. ty insurers witrs on the optim

the different target capital u.S. method (N

e Strategy

s

ndra and Sherjointly conside. We establisfrictional cap

to simultaneoWe consider t

th a numerical mal capital lev

models of dunder the SST, NAIC). We use

rris (2006) byers the effect osh a stochastipital costs, th

ously determinthe structure oanalysis of th

vel, reinsurancdetermining th

the SCR undee an example to

y of ic he ne of he ce he er o

3

Mothe

The

O

level.cost, tand tdetermhighegenerexpecfrictiosome determinsure

WMcCureinsuBeyonhedgiintegrmodeand ininvest

Tof thebankr

where

4

bankrureorgacosts rcosts ocredit, new op

odel Basee Friction

Optimizatio

Our optimizatio We considerthe expected tothe amount ofmine the optimer levels of caprally decreasescted bankruptconal cost of ca

capital (whichmined optimal er needs to deteWhile reinsuraullough and Caurance to adjusnd the use ofing underwritirating risk mael for the simulnvestment strated by the insu

The expected toe reinsurance ruptcy4 at time

e the surplus X

4. Bankruptcy couptcy costs. Direanization/liquidatirelated to the liquof lost managemand/or possibly

pportunities. (See

ed on Mn Cost

on Model wit

on model dealr the relationshotal frictional cf adjustment c

mal amount of cital increases ithe probabilit

cy cost. Howeapital. In practh we refer to capital level.

ermine the optance allows iarson (2013) pst capital acrosf reinsurance, ing risks. In anagement andltaneous determategy. We assuurer, with variaotal frictional ccost, the frictt, with t = 1,2,

X(t) is also calle

osts can be definect bankruptcy cion process, incluidation of the fir

ment energies, whthe inability of the Chandra and Sh

Jou

© 2015 Nation

Minimizin

th No Const

ls with determhip between bcost (the differcapital requirecapital to hold,its frictional coty of insolvencever, higher letice, the insureas adjustmentThus, the insu

timal level of cinsurers to mprovide empiriss affiliated firmeffective invewhat follows

d capital manamination of theume proportionables as definedcost at time t, Ftional cost of ,…T, that is:

ed RBC (Schm

ned broadly as eicosts are those eluding legal, accrm’s assets. Indirhich could lead the enterprise to oherris, 2006.)

urnal of Insu

nal Association of

ng

traint of Inso

mining the insubankruptcy corence between ed. It is impor, since capital i

ost. Holding higcy, with a resuevels of capiter decides whet in capital requrer faces a tracapital to hold. mitigate underical evidence thms within inteestment strategs, we will takagement to este optimal capitnal reinsuranced in Table 1. FCt,t=1,2,…T i

capital and th

meiser and Sieg

ither direct bankexplicit costs paicounting, filing arect bankruptcy cto lost sales, lost

obtain credit or is

rance Regul

Insurance Commi

olvency

urer's optimal cost, frictional cthese first two rtant for insuris costly and hgher levels of c

ulting decrease tal will increaether to raise oquired) based oade-off for whi

rwriting risks,hat insurers al

ernal capital magy also can hke the approatablish an intetal level, reinsue and one risky

is defined as thhe expected c

gel, 2013).

kruptcy costs or id by the debtorand other adminicosts are the oppot profits, higher

ssue securities to

lation

ssioners

capital capital costs)

rers to holding capital in the

ase the or shed on the ich the

, Fier, lso use arkets.

help in ach of egrated urance y asset

he sum cost of

indirect r in the istrative ortunity cost of finance

4

Insurer C

© 2015 Natio

By estreinsurancewe can finreinsurancecapital.5

The ob

where K(t)refer to it associated property-li

with the bowith drift coefficientinvestmentobtain the strategy fo

The Opti

We us

II. Given clevel 1 – exceeding

5. The

and risk, the 6. For

because the (Please see Lthank an ano

Capital, Inve

onal Association o

tablishing the se cost, the frict

nd the optimal e, the optima

bjective functio

) is the capitalas the adjustmwith raising o

iability insurers

oundary conditof and vol

t of 2, W1 andt in risky asse

optimal solutr t, where t = 1

imization M

se VaR (1 – confidence lev is given by th

l is not larger

factors affectingunderwriting riskmulti-period optadjustment cost Leary and Rober

onymous reviewer

estment and R

f Insurance Comm

stochastic objetional cost of cportion of risk

al capital leve

on is:

l needed to bement capital reor shedding exs satisfies the f

tion X (0) = x,latility of 1, W2

are indepeets. Substitutintions of adjus1,2,…T.

Model with Co

= 99.5%) of thel (0,1) ,

he smallest numthan . The SC

g retention rate ofk, and the price antimization modelwill affect the in

rts, 2005; Flanner for this commen

Reinsurance

missioners

ctive function capital and the ky asset to inveel and, theref

e raised or to bquired. Ca, (C

xternal capital.following stoch

where W1 is aW2 is a diffu

endent of each ng equation (3stment capital,

onstraint of

he net asset as the VaR of the

mber l such thaCR at time t is

f reinsurance incnd quantity demals, it is importannterval of adjustiery and Rangan, nt.

e Strategy

of minimizingexpected cost

est, the optimafore, the optim

be reduced at Ca ≥ 0) is the a

6 Assume thathastic different

a geometric Brusion process other, and is

3) into equatioreinsurance a

f Solvency II

the SCR define net assets at at the probabili:

clude the investmanded of insurancnt to consider theing the capital to2006; and Streb

g the sum of tht of bankruptcyal proportion omal risk-based

time t, and wadjustment cost the surplus otial equation:

rownian motionwith diffusion

s the portion oon (2), we canand investmen

ned in Solvencythe confidenc

ity of the loss X

ment rate of returce products. e adjustment coso the target valuebulaev, 2007). W

he y, of d

we st of

n n

of n

nt

y ce X

rn

st e.

We

5

whereX(t–1

Sminimthat is

subje

W

retentdefine The

T

capitaduringbetweliabili

Btarget

whereexpecintegr

e X (t) satisfie).

Similar to themizing the totas,

ct to:

With simulatiotion ratio and ted in Solvency

Optimizatio

The SST propoal defined as g a one-year een the markeities.

Based on the dt capital (TC) a

e Xt satisfies stcted shortfall wral.

es stochastic d

e discussion aal frictional cos

on, we can rethe proportion

y II.

on Model wit

oses the concepthe expected period. The ri

et-consistent va

definitions aboat time t:

tochastic differwith confidenc

Jou

© 2015 Nation

differential equ

above, we estst with the con

each the optimof risky asset

th Constrain

pt of target capishortfall of th

risk-bearing caalue of the as

ove, we establi

rential equationce level of .

urnal of Insu

nal Association of

uation either (3

tablish the obnstraint that Pr

mal solutions ts invested by

nt of the SST

ital, which equhe change in

apital is definessets and the b

ish the formula

n (3), Xt = Xt We use as

rance Regul

Insurance Commi

3) and Xt =

bjective functir (Xt –SCR

of the reinsuthe insurer and

T

uals the one-yerisk-bearing c

ed as the diffbest estimate

a for calculatin

– Xt–1 and ESs the variable

lation

ssioners

X(t) –

ion of t) = ,

urance d SCR

ear risk capital

ference of the

ng the

is the of the

6

Insurer C

© 2015 Natio

We esthe followi

That is,

subject to:

Nume In this

make compthe ratio oaverage ratof Kielholzwho emplbankruptcyindex dataestimate ththe risk-freChandra acapital reqsimilar to assume thacapital anddistress. Ta

7. The

estimates ma

Capital, Inve

onal Association o

stablish the objing constraint:

erical An

s section, we parisons amon

of capital cost,tio of capital cz (2000).) For loys sample y cost to firm va and rates of rhe drift and theee interest rate.and Sherris (2quired in the f

the single-perat there are nod consider onlable 2 lists the

information used

ade by the author

estment and R

f Insurance Comm

ective function

nalysis B

present an exng models base, we use the rost for nonlife the bankruptc

data from 19value. We use return for Trea

e volatility of th. For other data

2006). We focfirst year, whicriod model in o costs associaly the frictionainput data for

d in the numericas; the results may

Reinsurance

missioners

n of minimizin

Based on

ample to illusd on different results from Kinsurance com

cy cost, we use985–2005 to Standard & Poasury bills durhe rate of retura (described becus on calculach can be seen

Chandra and ated with adjual cost of capithe analysis.

al analysis here iy vary with differ

e Strategy

g the total frict

n an Exam

strate the optimcriteria discuss

Kielholz (2000)mpanies in 199e the results ofestimate the

oor’s (S&P) 50ring the periodrn on risky asseelow), we rely ating the optimn as the singleSherris (2006

usting to the opital and the co

s drawn from prient underlying as

tional cost with

mple

mal results andsed above.7 Fo), which is th

98. (See Table f Lewis (2009)

ratio of tota00 stock marked 1983–2007 toets (stocks) andon results from

mal adjustmene-period mode6). That is, wptimal level oost of financia

ior studies and osssumptions.

h

d or he 1 ), al et o d

m nt el

we of al

on

7

R

may compcalculrangedoes frictioTableand thWhenoptimpartia

Reinsurance covary widely.

plicated. Becaulate optimal so

e of the rate onot satisfy th

onal cost and e 4 and Table he premium inn the rate of re

mal retention raally or complet

The Inp

ontracts are prThe factors

use exact ratesolutions based of reinsurance he requiremenvice versa. T5. From Table

ncome, P1, are einsurance cosate a* is smalltely replaces ca

Jou

© 2015 Nation

Table 2:put Data for t

rivately negotiaffecting the s of reinsurancon a range of vcost, which isnt of insolven

The optimal soe 3, we find thimportant fact

st is small or l or equal to zapital to transfe

urnal of Insu

nal Association of

the Example

iated, and the rate of reinsu

ce cost are values for eachs not economicncy regulationolutions, *, arhat the rate of tors that affectthe premium i

zero, which meer claim risk.

rance Regul

Insurance Commi

contract condurance cost isunknown to u

h . We also gical to the insun with lowestre listed in Taf reinsurance cot the optimal rincome is smaeans the reinsu

lation

ssioners

ditions s very us, we ive the urer or t total able 3, ost, , results. all, the urance

8

Insurer C

© 2015 Natio

From in our casincrease ofto increasedecrease thcapital held

Optima

From

(P1 = 10 incase), the means thareinsurancecost increaconservativWhen underwritindue to high

Finallyhigher (P2 means thatcapital cosaddition, thcost is lowthat the proffset inso

Capital, Inve

onal Association o

Table 3, we alse), the adjustmf the rate of ree capital so as he net incomed so as to reduc

al Solutions O

Table 3, we an our case) and

optimal retentt it is optimale due to the lowases, the invesve, the retentio 0.2, the optimng risk is reduher reinsurancey, from Table = 20, and P3

t it is optimal t. Also, higherhe optimal ret

wer or higher. Aremium incomlvency risk.

estment and R

f Insurance Comm

so find when tment capital reinsurance cost

to offset undee of the insurece the insolven

Tabtained by Op

also find that wd when the ratetion rate is zel for the insurw reinsurance stment strategon portion is inmal retention uced by increae cost.

3, we found = 25 in our cafor the insure

r premium incotention rate is

And all surplus me and the retu

Reinsurance

missioners

the level of preequired is post. This means ierwriting risk. er and also prncy risk caused

able 3: ptimization M

when the levee of reinsurancero, and there rer to transfer cost. Howevery changes fro

ncreasing, and rate is 1, the

asing capital in

that when the ases), the optimer to reduce come can be useequal to 1 whis invested in r

urn of risk-fre

e Strategy

emuim income sitive and incrit is necessary Higher reinsu

rompt the insud by higher rein

Model Without

el of premuim e cost is low (is no risky inall underwrit

r, when the rateom more aggrethe capital heloptimal capitanstead of buyi

level of premmal capital is napital held so

ed to offset insohether the rate risk-free assets

ee assets are g

is low (P1 = 10reases with th

y for the insureurance cost wilurer to increasnsurance cost.

t Constraint

income is low = 0.05 in ou

nvestment. Thiting risk to the of reinsurancessive to morld is increasingal is great, anding reinsuranc

mium income inegative, which

as to decreasolvency risk. Inof reinsuranc

s. This suggestgreat enough to

0

he er ll

se

w ur is

he ce re g. d

ce

is h

se n

ce ts o

9

Op

Note: Prequire

Note: Prequire

ptimal Solution

P1 – premium inced; * – the optima

Optimal So

P1 – premium inced; * – the optima

ns Obtained b

come; – the rate al portion of risky

olutions Obtaion the

come; – the rate al portion of risky

Jou

© 2015 Nation

Table 4: by Optimizatio

of reinsurance coassets; a* – the op

Table 5: ined by the O

e Swiss Solven

of reinsurance coassets; a* – the op

urnal of Insu

nal Association of

on Model Bas

ost; K(1)* – the optimal portion of r

ptimization Mcy Test

ost; K(1)* – the optimal portion of r

rance Regul

Insurance Commi

ed on Solvenc

ptimal adjustmentretention.

Model Based

ptimal adjustmentretention.

lation

ssioners

cy II

t capital

t capital

10

Insurer Capital, Investment and Reinsurance Strategy

© 2015 National Association of Insurance Commissioners

From Table 4 and Table 5, we find that the optimal adjustment capital required is greater with the constraints of Solvency II and the SST than without these constraints of insolvency. The tables illustrate that Solvency II and the SST tend to be more prudent in terms of determining optimal capital level.

From Table 4 and Table 5, we also find that the investment strategies are more aggressive when optimal adjustment capital required is greater or the premium income is greater. The higher capital and higher premium income can help the insurer to hedge the investment risk so as to allow for more aggressive investment strategies. All of these findings provide insight on the decision of optimal capital, investment and reinsurance strategies.

Next, we perform a sensitivity analysis of the optimal adjustment capital required, investment and reinsurance strategies to the change in several critical parameters, including the ratio of the frictional cost of capital, cc; the rate of reinsurance cost, ; the drift of the rate of return on risky assets, ; the volatility of the return rate of the risky assets invested, ; the volatility of claim loss rate, 1; and the ratio of total bankruptcy cost to firm value, cf.

The Effect of Changes in cc,

Table 6 and Table 7 display the optimal values of the proportions of reinsurance retention and the risky assets invested and the capital adjusted by the insurer for different values of the ratio of capital cost cc and the rate of reinsurance cost , when we use the criteria of minimizing the total control cost. The confidence level is set equal to 0.5% for Solvency II and 1% for the SST. We present the results for the second scenario of premium income. (The analyses of the other two scenarios of premium income are similar.)

The results in Table 6 show that the optimal investment strategy, *, tends to be more aggressive when the ratio of capital cost, cc, is small and the optimal adjustment capital required, K(1)*, is large with the optimization model without constraint of insolvency. (The optimal portion of risky assets (*) equals 0.55 when the ratio of capital cost, cc, is 0.02, and the optimal adjustment capital required, K(1)*, is 13.5.) However, the investment strategies tend to be more conservative with increases in the ratio of capital cost and with decreases in the optimal adjustment capital required. The portion of risky assets becomes zero when the optimal adjustment capital required is very small or negative. Because lower capital level means higher insolvency risk, the insurer should select a more conservative investment strategy in order to reduce investment risk and further to reduce insolvency risk. However, based on the estimation from the second and third model (with constraint of insolvency), the optimal capital levels are much higher than those estimated by the first model (without constraint of insolvency).

11

an

Optimd Risky Asset

mal Capital Lets Invested by

Cost i

Jou

© 2015 Nation

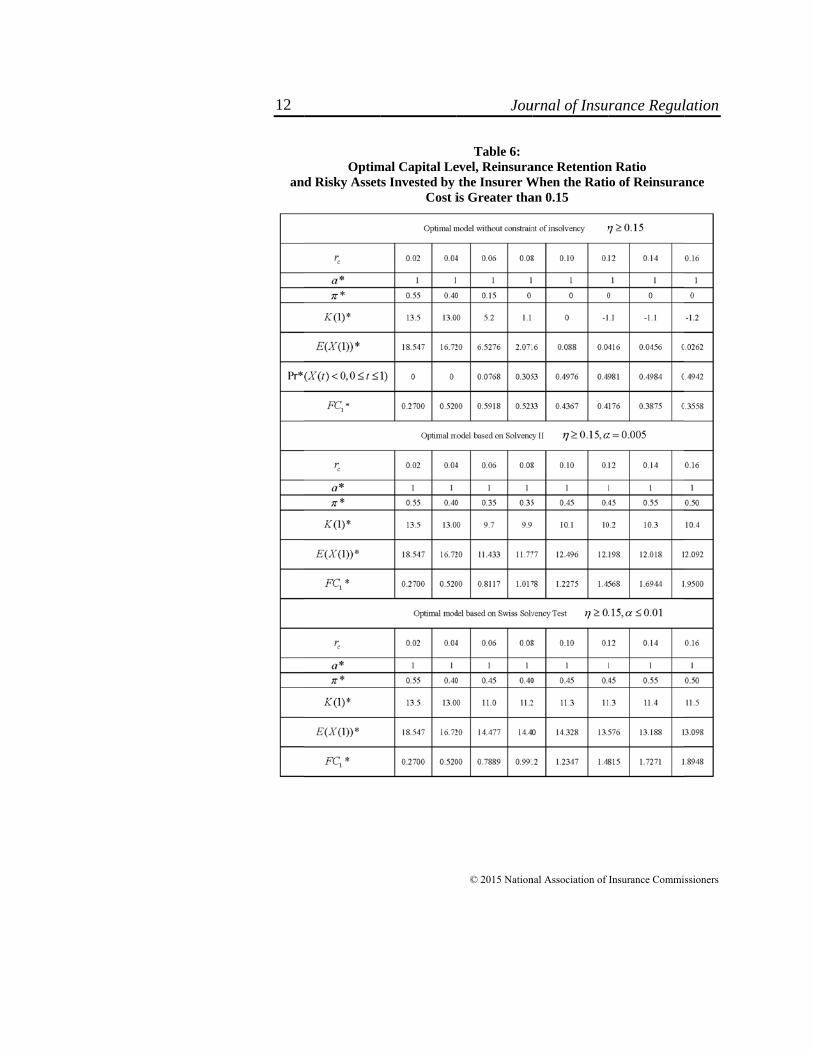

Table 6: evel, Reinsurathe Insurer Wis Greater tha

urnal of Insu

nal Association of

ance RetentionWhen the Ratian 0.15

rance Regul

Insurance Commi

n Ratio io of Reinsura

lation

ssioners

ance

12

Insurer Capital, Investment and Reinsurance Strategy

© 2015 National Association of Insurance Commissioners

Table 6 note: – the confidence level; – the rate of reinsurance cost; K(1)* – the optimal adjustment capital required; * – the optimal portion of risky assets; a* – the optimal portion of retention; FC1* – the optimal total friction cost; E(X(1))* – the optimal expected surplus at time 1; Pr*(X(t)0,0t1) – the optimal insolvency probability; – the drift of return rate of risky assets; 1 – the volatility of return rate of risky assets; r – the risk-free interest rate; 2 – the volatility of claim loss; cc – the ratio of frictional capital cost; cf – the ratio of the total bankruptcy cost to firm value.

However, it is slightly decreasing with the increase of the rate of capital cost, and the optimal investment strategies are more aggresive than those determined by the first model for most cases—except for two cases in which the rate of capital cost is very low (rc = 0.02, 0.04 in our cases). Given the constraint of low probability of insolvency, the insurer must hold more capital to reduce insolvency risk, even though the capital is expensive. The higher capital level allows the insurer to follow a more aggressive investment strategy so as to increase investment return and decrease total frictional cost.

In addition, the total cost FC1 (frictional cost of capital and the cost of bankrupcty) is larger for Solvency II and the SST than that for the optimization model without constraint of insolvency. The exceptions are the cases in which the ratio of capital cost cc 0.04 and the optimal adjustment capital required by Solvency II and the SST, K(1)*, is higher than what was determined by the optimal model without constraint of insolvency—except for the cases where the ratio of capital cost cc 0.04. That is, in most cases, Solvency II and the SST are more prudent in determining optimal adjustment capital required than by only minimizing the total frictional cost.

The results of Table 6 also show that the optimal insolvency probabilities, Pr* (X(t) 0, 0 t 1), determined by the optimization model without constraint of insolvency, become larger when the ratio of capital costs increases. Therefore, regulation based on Solvency II or the SST appear to be more binding in this situation. Finally, the results show that the optimal adjustment capital required by the SST is slightly greater than that from the Solvency II results.

The results in Table 7 indicate that if the frictional cost of capital is very high or the reinsurance cost is very low, reinsurance can partially replace the capital need and effectively serve as an instrument of capital management. (See the values in the last four columns corresponding optimal retention ratios a*, which are small.) Table 7 indicates that most of the premium is ceded to the reinsurer so as to transfer claim risk.

13

O

Optimal CapitInvested by th

tal Level, Reinhe Insurer Wh

Jou

© 2015 Nation

Table 7: nsurance Retehen the Ratio

urnal of Insu

nal Association of

ention Ratio anof Reinsuran

rance Regul

Insurance Commi

nd Risky Assece Cost is 0.05

lation

ssioners

ets 5

14

Insurer C

© 2015 Natio

Table 7 note:capital requirthe optimal tothe optimal ireturn rate of frictional cap

Table

model andmodel for m(rc = 0.02reinsuranceallow the investment

Figurethe probabinsolvencynumerical

Thethe Pr

In

Capital, Inve

onal Association o

– the confidencred; * – the optimotal friction cost; insolvency probabf risky assets; r – thital cost; cf – the ra

7 also indicated third model most cases—e2, 0.04 in oue can decreaseinsurer to ta

t return and dece 1 depicts the bility of insoly, and the conresults of the e

e Relationshiprobability of Innsolvency, and

estment and R

f Insurance Comm

ce level; – the ramal portion of riskE(X(1))* – the op

bility; – the drifhe risk-free interesatio of the total ba

es that the inveare more aggxcept for two c

ur cases). Hige probability oake more aggcrease total fricrelationship b

lvency based nfidence level

example.

Figp Between the nsolvency Bas

d the ConfidenSwiss Solven

Reinsurance

missioners

ate of reinsurance ky assets; a* – the ptimal expected suft of return rate ost rate; 2 – the voankruptcy cost to fi

estment strategressive than thcases that the r

gher capital leof insolvency agressive investctional cost. etween the raton optimal m

l of Solvency

gure 1: Rate of Fricti

sed on a Modence Levels for cy Test ( 0

e Strategy

cost; K(1)* – the ooptimal portion o

urplus at time 1; Pof risky assets; 1 olatility of claim lofirm value.

gies determinedhose determinrate of capital cevel or a highand underwirintment strategy

te of frictional model withouty II and the

ional Cost of Cel Without CoSolvency II a.15)

optimal adjustmenof retention; FC1* Pr*(X(t)0,0t1)

– the volatility ooss; cc – the ratio o

d by the secondned by the firscost is very lowher portion o

ng risk so as toy, obtain mor

cost of capitalt constraint oSST from th

Capital, nstraint of nd the

nt – –

of of

d st w of o

re

l, of he

15

FmodebasedSST iThe rSolvethan dthe ca

FdetermSolvereinsuexamdetermas thecapitacapita

Th

8

equal discussmalle

Figure 1 showsel without consd on Solvency in most cases—results also indency II or the determining caases where the Figure 2 descrmined by the oency II and theurance for each

mple. The resumined by the oe rate of frictioal will make thal in order to k

he Relationshi

8. The reason thatto 1 when s the cases witho

er value of and

s that the probstraint of insolII and with ta

—except for thdicate that settSST leads to

apital by only ratio of capital

ribes the relatioptimization me SST and the rh exposure lts in Figure optimization monal cost of cahe total controeep the total co

ip Between OpCapital Cost

t we choose 00.15. In order to

out reinsurance. Idiscuss the cases

Jou

© 2015 Nation

bability of insolvency is muchail value at rishe cases whereting the regulagreater prudenminimizing th

l cost is very sionship betwee

model without rate of friction 0.158 and ot2 indicate tha

model without apital, cc, increol cost increasontrol cost min

Figure 2: ptimal Adjustof Three Mod

0.15

is that the op

o make analysis In Figure 3 and F with reinsurance

urnal of Insu

nal Association of

olvency based h greater than sk (TVaR) cone the ratio of caatory capital lence toward thhe total frictionmall. en the optimaconstraint of i

nal cost of capither data as deat the optimalconstraint of iases, since largse, and it is nenimized.

tment Capital dels ( 0.15)

ptimal retention p and comparison

Figure 5 (also seee.

rance Regul

Insurance Commi

on the optimiwith VaR con

nstraint based apital cost cc evel based on e risk of insolnal cost—exce

al adjustment cinsolvency, basital when the c

escribed above l adjustment cinsolvency decger frictional cecessary to de

and the Ratio)

portion of reinsurn conveniently, we Table 7), we w

lation

ssioners

ization nstraint on the 0.04.

either lvency ept for

capital sed on cost of in the

capital creases cost of ecrease

o of

rance is we first

will set a

16

Insurer C

© 2015 Natio

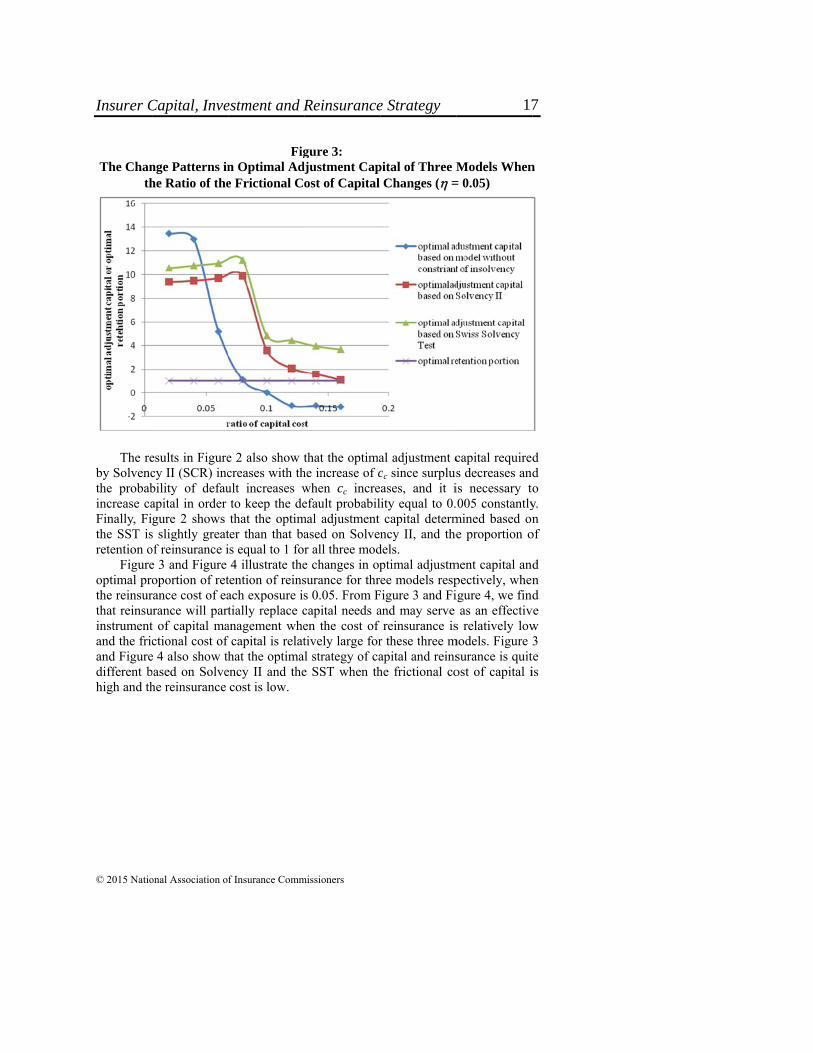

The Chanth

The re

by Solvencthe probabincrease caFinally, Fithe SST isretention o

Figureoptimal prothe reinsurthat reinsuinstrumentand the fricand Figuredifferent bhigh and th

Capital, Inve

onal Association o

nge Patterns inhe Ratio of the

esults in Figurecy II (SCR) incbility of defauapital in order gure 2 shows

s slightly greatof reinsurance ie 3 and Figure oportion of retrance cost of eaurance will partt of capital mactional cost of

e 4 also show thbased on Solvehe reinsurance

estment and R

f Insurance Comm

Fign Optimal Ade Frictional C

e 2 also show tcreases with thult increases wto keep the dethat the optim

ter than that bais equal to 1 fo4 illustrate the

tention of reinsach exposure istially replace c

anagement whef capital is relathat the optima

ency II and thecost is low.

Reinsurance

missioners

gure 3: djustment Capost of Capital

that the optimahe increase of cwhen cc increefault probabil

mal adjustment ased on Solvenr all three mode changes in opsurance for thrs 0.05. From Fcapital needs aen the cost of tively large forl strategy of cae SST when th

e Strategy

pital of Three MChanges ( =

al adjustment ccc since surplusases, and it iity equal to 0.capital determ

ncy II, and thedels. ptimal adjustmee models resp

Figure 3 and Fiand may serve

reinsurance isr these three mapital and reinshe frictional co

Models When= 0.05)

capital requireds decreases andis necessary to005 constantly

mined based one proportion o

ment capital andpectively, whenigure 4, we findas an effectiv

s relatively lowmodels. Figure 3

surance is quitost of capital i

n

d d o y. n

of

d n d

ve w 3 te is

17

The

The E

Tpropowhenresperequirrisky optiminvestvolatiincreaunchathe fir

ItFC1* claimwhat cost (in the

e Change PattWhen the Rat

Effect of Cha

Table 8, Table ortions of reinsn the parametectively. The dred, K(1)*, remassets, *, is

mal adjustmenttment, all optility of risky asases, but optimanged when thrm value, cf, int is important tincrease, but t

m loss, 2, increvalue of claim

( = 0.15 in oue situations of

terns in Optimtio of the Fric

anges in ,

9 and Table 10surance retentiers of , 1, data in Table

mains constant zero when part capital requtimal solutionsssets, and 1

mal probability he risk-free intncrease. to notice that tthe optimal capeases, and optimm loss, 2, takur cases) will lef greater claim

Jou

© 2015 Nation

Figure 4: mal Proportionctional Cost of

1, r, 2 and

0 list the optimion and the rir, 2 and cf

e 8 show thawhen paramet

rameters changuired is negats remain unch1, change. The of insolvency

terest rate, r, a

the optimal valpital level remmal retention p

kes. These resuead the insurer m risk. The o

urnal of Insu

nal Association of

n of Retentionf Capital Chan

cf

mal adjustment sky assets inv

f change baseat the optimalters change. Thge, and the maative. Becausehanged when optimal total f, Pr* (X(t) 0,

and the ratio o

lues of Pr* (X(mains unchangeportions are allults illustrate th

to retain all proptimal econom

rance Regul

Insurance Commi

n of Three Monges ( = 0.05

t capital requirevested by the id on three ml adjustment che optimal portain reason is the there is no

the return ratfrictional cost, 0 t 1), is af bankruptcy c

(t) 0, 0 t ed as the volati equal to 1 no hat high reinsuremium incommic strategy f

lation

ssioners

odels )

ed, the insurer

models, capital tion of hat the

risky te and FC1*,

almost cost to

1) and ility of matter urance e even

for the

18

Insurer Capital, Investment and Reinsurance Strategy

© 2015 National Association of Insurance Commissioners

insurer is to keep capital unchanged, but this approach will increase the insurer's probability of insolvency when the volatility of claim loss, 2, increases. This is the limitation of model one. Minimizing total frictional cost from the insurer's perspective may conflict with the objective of regulation. The data in Table 8 also show that the optimal investment strategy is that all surplus is invested in risk-free assets. The return of risk-free assets can help to offset part of claim risk and help to reduce total frictional cost.

Table 9 indicates that with the constraint of Solvency II, the optimal capital, K(1)*, slightly decreases with the increase of the drift of return rate of risky assets, , and slightly increases with the increase of volatility of return rate of risky asset, 1, and risk-free interest rate, r. And the optimal adjustment capital is much greater than determined earlier based on the optimization model without constraint of insolvency. From Table 9, we also observe that the optimal solution of K(1)* greatly increases as the volatility of claim loss, 2, increases. The increase of claim risk will lead to increased capital in order to keep the insolvency probability within the criterion of Insolvency II. But the optimal retention portion are all equal to 1 for all values of 2, meaning that it is optimal for the insurer to raise capital instead of purchasing reinsurance in order to reduce underwriting risk due to higher rate of reinsurance cost. Therefore, based on the analysis above, we illustrate based on various assumptions and with regard to varying regulatory standards that capital and reinsurance can be substitutes. On the one hand, when reinsurance cost is rather low but capital cost is rather high, reinsurance can partially or fully substitute for capital, as shown in Table 7. On the other hand, capital can partially or fully substitute for reinsurance when capital cost is rather low but the reinsurance cost is rather high, as in Table 6. Finally, we find from Table 9 that optimal adjustment capital remains fairly constant when the ratio of total bankruptcy cost to firm value, cf, increases, but the total frictional cost, FC1*, increases with the increase of cf.

From Table 10, we find that the change patterns are similar to those in Table 9 when the parameters change. However, the optimal adjustment capital, K(1)*, and the optimal total frictional cost, FC1*, are slightly greater than those in Table 9. That is, the criteria of the SST are slightly more prudent in determining the optimal adjustment capital.

It should be noticed that Table 8, Table 9 and Table 10 indicate that the optimal total frictional cost (and other optimal solutions) are very sensitive to the change of the volatility of claim loss, 2, but the optimal frictional cost (and other optimal solutions) changes very slightly as other paramters change, given the condition that the rate of reinsurance cost = 0.15. So, 2 is the most important parameter affecting total frictional cost. In the following, we will further discuss the sensitivity of the optimal solutions as 2 increases when takes smaller values ( = 0.10) for three models, respectively.

19

OpRisk

an

ptimal Adjustmky Assets Invend cf Based on

ment Capital Rested by the Inn the Optimiza

Jou

© 2015 Nation

Table 8: Required, Rei

nsurer with Vaation Model W

urnal of Insu

nal Association of

insurance Retarying Param

Without Insolv

rance Regul

Insurance Commi

tention Ratio ameters of , 1,vency Constra

lation

ssioners

and , r, 2 aint

20

Insurer C

© 2015 Natio

Note: – therequired; * optimal total optimal insolrate of risky frictional cap

Capital, Inve

onal Association o

e confidence level;– the optimal porfriction cost; E(X

lvency probabilityassets; r – the risital cost; cf – the ra

estment and R

f Insurance Comm

Table 8

; – the rate of rertion of risky asse

X(1))* – the optim; – the drift of rsk-free interest raatio of the total ba

Reinsurance

missioners

(Continued)

einsurance cost; K(ets; a* – the optimal expected surplureturn rate of risky

ate; 2 – the volatankruptcy cost to fi

e Strategy

(1)* – the optimalmal portion of reteus at time 1; Pr*(Xy assets; 1 – the tility of claim lossfirm value.

l adjustment capitatention; FC1* – thX(t)0,0t1) – thvolatility of returs; cc – the ratio o

al he he rn of

21

OpRisk

ptimal Adjustmky Assets Inve

and cf

ment Capital Rested by the Inf Based on the

Jou

© 2015 Nation

Table 9: Required, Rei

nsurer with Vae Optimal Mo

urnal of Insu

nal Association of

insurance Retarying Param

odel with Solve

rance Regul

Insurance Commi

tention Ratio ameters of , 1,

ency II

lation

ssioners

and , r, 2

22

Insurer C

© 2015 Natio

Note: – therequired; * optimal total optimal insolrate of risky frictional cap

Capital, Inve

onal Association o

e confidence level;– the optimal porfriction cost; E(X

lvency probabilityassets; r – the risital cost; cf – the ra

estment and R

f Insurance Comm

Table 9

; – the rate of rertion of risky asse

X(1))* – the optim; – the drift of rsk-free interest raatio of the total ba

Reinsurance

missioners

(Continued)

einsurance cost; K(ets; a* – the optimal expected surplureturn rate of risky

ate; 2 – the volatankruptcy cost to fi

e Strategy

(1)* – the optimalmal portion of reteus at time 1; Pr*(Xy assets; 1 – the tility of claim lossfirm value.

l adjustment capitatention; FC1* – thX(t)0,0t1) – thvolatility of returs; cc – the ratio o

al he he rn of

23

OpRisk

ptimal Adjustmky Assets Inve

and cf Based

ment Capital Rested by the Ind on the Optim

Jou

© 2015 Nation

Table 10: Required, Rei

nsurer with Vamal Model wi

urnal of Insu

nal Association of

insurance Retarying Paramith the Swiss S

rance Regul

Insurance Commi

tention Ratio ameters of , 1,Solvency Test

lation

ssioners

and , r, 2

24

Insurer C

© 2015 Natio

Note: – therequired; * optimal total optimal insolrate of risky frictional cap

Table

is still equfrom 0.15 reinsurancestill retainincrease inmodel 2 baportion decin that the and Table satisfying t

Capital, Inve

onal Association o

e confidence level;– the optimal porfriction cost; E(X

lvency probabilityassets; r – the risital cost; cf – the ra

11 lists the resual to 1 as 2 i

to 0.1 for mode cannot help

ns all preimumncome and reduased on Insolvcreases with thrate of reinsu10.) The insu

the regulation r

estment and R

f Insurance Comm

Table 10

; – the rate of rertion of risky asse

X(1))* – the optim; – the drift of rsk-free interest raatio of the total ba

sults. Table 11increases, althodel 1 (withoutthe insurer to

m income but uce the risk of

vency II and mhe increase of rance cost is lurer reduces trequirement.

Reinsurance

missioners

0 (Continued)

einsurance cost; K(ets; a* – the optimal expected surplureturn rate of risky

ate; 2 – the volatankruptcy cost to fi

indicates that ough the rate oconstraint of

decrease total invests all su

f claim loss. Tamodel 3 based o2 and optimaarger ( = 0.1the capital cos

e Strategy

(1)* – the optimalmal portion of reteus at time 1; Pr*(Xy assets; 1 – the tility of claim lossfirm value.

the optimal reof reinsuranceinsolvency). Tfrictional costurplus in riskable 11 also inon the SST, opal capital level 5) when 2 4st through rein

l adjustment capitatention; FC1* – thX(t)0,0t1) – thvolatility of returs; cc – the ratio o

etention portione cost decreaseThis means that, so the insurek-free assets tondicates that foptimal retentionl is much lowe4. (See Table 9nsurance whil

al he he rn of

n es at er o

or n

er 9 le

25

OpRisky

ptimal Adjustmy Assets Inves

on Three O

ment Capital Rsted by the InsOptimization

Jou

© 2015 Nation

Table 11: Required, Reisurer with VarModels Respe

urnal of Insu

nal Association of

insurance Retrying Parameectively (Give

rance Regul

Insurance Commi

tention Ratio aeter of 2 and en = 0.10)

lation

ssioners

and Based

26

Insurer C

© 2015 Natio

Note: – therequired; * optimal total optimal insolrate of risky frictional cap

Summ In this

optimal adperformed an examplinstrumentis high ansubstitute f

We finrisk when larger. Settgreater prfrictional research m

Capital, Inve

onal Association o

e confidence level;– the optimal porfriction cost; E(X

lvency probabilityassets; r – the risital cost; cf – the ra

mary and

s paper, we edjustment capinumerical ana

le. The resultt of capital mad/or the reinsufor reinsurancend that the optithe optimal adting the regulatudence than cost in most

may benefit from

estment and R

f Insurance Comm

Table 11

; – the rate of rertion of risky asse

X(1))* – the optim; – the drift of rsk-free interest raatio of the total ba

d Conclu

established inteital required, alysis using simts show that ranagement, parurance cost is e when capital imal investeme

djustment capittory capital levdetermining icases, except

m numerical an

Reinsurance

missioners

1 (Continued)

einsurance cost; K(ets; a* – the optimal expected surplureturn rate of risky

ate; 2 – the volatankruptcy cost to fi

usion

egrated modelreinsurance a

mulation with reinsurance mrticularly when

low. Howevecost is low andent strategy is tal required anvel either by Soinsurer capital

when capitalnalysis for life

e Strategy

(1)* – the optimalmal portion of reteus at time 1; Pr*(Xy assets; 1 – the tility of claim lossfirm value.

ls to determinand investmenta property-liab

may be used an the frictionaler, capital can d reinsurance cfor the insurer

nd/or the premiolvency II or thl level by mil cost is veryinsurers.

l adjustment capitatention; FC1* – thX(t)0,0t1) – thvolatility of returs; cc – the ratio o

ne the insurer’t strategy. Wbility insurer aas an effectivl cost of capita

partly or fullycost is high.

to accept morium income arhe SST leads toinimizing tota

y small. Futur

al he he rn of

s We

as ve al y

re re o al re

27

Journal of Insurance Regulation

© 2015 National Association of Insurance Commissioners

References

Chandra, V., and M. Sherris, 2006. “Capital Management and Frictional Costs in Insurance,” Australian Actuarial Journal, 12(4): 344–399.

Cummins, J.D., and R.D. Phillips, 2009. “Capital Adequacy and Insurance Risk-Based Capital Systems,” Journal of Insurance Regulation, 28(1): 25–72.

Dhaene, J., M.J. Goovaerts, and R. Kaas, 2003. “Economic Capital Allocation Derived from Risk Measures,” North American Actuarial Journal, 7: 44–59.

Eling, M., and I. Holzmüller, 2008. “An Overview and Comparison of Risk-Based Capital Standards,” Journal of Insurance Regulation, 26(4): 31–60.

Eling, M., H. Schmeiser, and J. Schmit, 2007. “The Solvency II Process: Overview and Critical Analysis,” Risk Management and Insurance Review, 10(1): 69–85.

Fier, S., K. McCullough, and J.M. Carson, 2013. “Internal Capital Markets and the Partial Adjustment of Leverage,” Journal of Banking and Finance, 37(3): 1029–1039.

Flannery, M.J., and K.P. Rangan, 2006. “Partial Adjustment Toward Target Capital Structures,” Journal of Financial Economics, 79: 469–506.

Gatzert, N., and H. Wesker, 2012. “A Comparative Assessment of Basel II/III and Solvency II,” The Geneva Papers, 37: 539–570.

Holzmüller, I., 2009. “The United States RBC Standards, Solvency II and the Swiss Solvency Test: A Comparative Assessment,” Geneva Papers on Risk and Insurance: Issues and Practice, 34: 56–77.

Kielholz, W., 2000. “The Cost of Capital for Insurance Companies,” Geneva Papers on Risk and Insurance, 25(1): 4–24.

Leary, M.T., and M.R. Roberts, 2005. “Do Firms Rebalance Their Capital Structures?,” Journal of Finance, 60(6): 2575–2619.

Lewis, C.M., 2009. “Firm-Specific Estimates of the Ex Ante Bankruptcy Discount,” working paper at SSRN: http://papers.ssrn.com/sol3/papers.dfm?abstract_id=1372284.

Luder, T., 2005. “Swiss Solvency Test in Non-Life Insurance,” working paper at: www.finma.ch/archiv/bpv/download/e/SST_Astin_colloquium_Luder_Thomas.pdf.

Mao, H., and K. Ostaszewski, 2010. “Pricing Insurance Contracts and Determining Optimal Capital of Insurers,” The Proceedings of International Conference of Industrial Engineering and Industrial Management, pp. 1–5.

Schmeiser, H., and C. Siegel, 2013. “Regulating Insurance Groups: A Comparison of Risk-Based Solvency Models,” Journal of Financial Perspectives, 1:119–131.

Smith, M. J-H, 2010. “Solvency II: The Ambitious Modernization of the Prudential Regulation of Insurers and Reinsurers Across the European Union (EU),” Connecticut Insurance Law Journal, 16(2): 357–398.

28

Insurer Capital, Investment and Reinsurance Strategy

© 2015 National Association of Insurance Commissioners

Staking, K., and D. Babbel, 1995. “The Relation Between Capital Structure, Interest Rate Sensitivity and Market Value in the Property-Liability Insurance Industry,” Journal of Risk and Insurance, 62: 690–718.

Strebulaev, Illya A., 2007. “Do Tests of Capital Structure Theory Mean What They Say?,” Journal of Finance, 62(4): 1747–1787.

29

Journal of Insurance Regulation

Guidelines for Authors

Submissions should relate to the regulation of insurance. They may include

empirical work, theory, and institutional or policy analysis. We seek papers that advance research or analytical techniques, particularly papers that make new research more understandable to regulators.

Submissions must be original work and not being considered for publication elsewhere; papers from presentations should note the meeting. Discussion, opinions, and controversial matters are welcome, provided the paper clearly documents the sources of information and distinguishes opinions or judgment from empirical or factual information. The paper should recognize contrary views, rebuttals, and opposing positions.

References to published literature should be inserted into the text using the “author, date” format. Examples are: (1) “Manders et al. (1994) have shown. . .” and (2) “Interstate compacts have been researched extensively (Manders et al., 1994).” Cited literature should be shown in a “References” section, containing an alphabetical list of authors as shown below.

Cummins, J. David and Richard A. Derrig, eds., 1989. Financial Models of

Insurance Solvency, Norwell, Mass.: Kluwer Academic Publishers. Manders, John M., Therese M. Vaughan and Robert H. Myers, Jr., 1994.

“Insurance Regulation in the Public Interest: Where Do We Go from Here?” Journal of Insurance Regulation, 12: 285.

National Association of Insurance Commissioners, 1992. An Update of the NAIC

Solvency Agenda, Jan. 7, Kansas City, Mo.: NAIC. “Spreading Disaster Risk,” 1994. Business Insurance, Feb. 28, p. 1.

Footnotes should be used to supply useful background or technical information that might distract or disinterest the general readership of insurance professionals. Footnotes should not simply cite published literature — use instead the “author, date” format above.

Tables and charts should be used only if needed to directly support the thesis of the paper. They should have descriptive titles and helpful explanatory notes included at the foot of the exhibit.

Journal of Insurance Regulation

Papers, including exhibits and appendices, should be limited to 45 double-spaced pages. Manuscripts are sent to reviewers anonymously; author(s) and affiliation(s) should appear only on a separate title page. The first page should include an abstract of no more than 200 words. Manuscripts should be sent by email in a Microsoft Word file to:

Cassandra Cole and Kathleen McCullough [email protected]

The first named author will receive acknowledgement of receipt and the

editor’s decision on whether the document will be accepted for further review. If declined for review, the manuscript will be destroyed. For reviewed manuscripts, the process will generally be completed and the first named author notified in eight to 10 weeks of receipt.

Published papers will become the copyrighted property of the Journal of Insurance Regulation. It is the author’s responsibility to secure permission to reprint copyrighted material contained in the manuscript and make the proper acknowledgement.

NAIC publications are subject to copyright protection. If you would like to reprint an NAIC publication, please submit a request for permission via the NAIC Web site at www.naic.org. (Click on the “Copyright & Reprint Info” link at the bottom of the home page.) The NAIC will review your request.