cashflow analysisttsmedia.ttstrain.com/cucashflow031815.pdf · class rules •ask questions ... •...

TRANSCRIPT

1

CASHFLOW ANALYSIS

Developed By Vin DiCara

DiCara Training and Consulting Inc.

PO Box 963

Brunswick, Maine 04011

207 607‐4129

CLASS RULES

• Ask Questions

• Participate

• Relax and enjoy yourself

• Share your experiences

2

PROGRAM OBJECTIVES

• Review the fundamentals of Cashflow

• Use Cashflow statements to understand the needs of borrowers

• Understand the value of projections to predict future cashflow challenges

• Structure complex financial deals

CASHFLOW/SIMPLE VIEW

• The P & L contains the major elements of cashflow and repaymentability. The most common view of repaymentability:

Profit After Tax

+ Depreciation

+ Interest and other hidden cashflow (rent savings, officer’s salaries savings and non‐recurring charges)

‐ Distributions

= Cashflow (CF)Available For Debt Service

3

DOES THE BUSINESS HAVE ADDITIONAL CASHFLOW?

• Rent

• Officer’s Salary

• Non‐recurring expenses

DEBT COVERAGE RATIO

• The Debt Coverage Ratio (DCR) is determined by using the following formula:

Available Cashflow = DCR

Annual Debt Service

Most credit unions look for a DCR of 1.25/1 or better. It is important how you calculate cashflow and if you include all debt as debt service or just senior debt.

4

PERMANENT WORKING CAPITAL EXAMPLE

PWC Required:

A/R (Projected A/R – Current A/R)

+ Inv. (Projected Inv.‐ Current Inv.)

‐ A/P (Projected A/P – Current A/P)

‐ Acc. (Projected Acc. –Current Acc.)

= New Investment in PWC

PWC can be calculated on either an historical or projected basis

PERMANENT WORKING CAPITAL

• Increases in PWC can be calculated on an historical basis or on a projected basis. Projected increases in PWC provide an indication of what kind of financing a business will require in the future for its operating needs as defined by its operating cycle. Historical increases in PWC show where some of a business’ cashflow has been used in previous periods of time

5

REPAYMENTABILITY ADJUSTMENTS

• Businesses use cashflow for purposes other than just debt service

• Cashflow is also required to fund the operations of a business (Permanent Working Capital increases) and to pay for investments in fixed assets, when 100% financing is not available

• To account for these other uses of a business’ cashflow, a number of adjustments need to be made

CASHFLOW/ADJUSTED FORMULA

Profit After Tax

+ Depreciation

+ Other cashflow (non‐recurring charges)

‐ Distributions

‐ Increase in Permanent Working Capital

‐ Cash outlays for fixed assets

= Cashflow Available For Debt Service

6

GLOBAL CASHFLOW

• Also referred to as consolidated cashflow

• Takes into account both the business’ cashflow and the personal cashflow of owner/guarantors

• Important for closely held businesses

• Some business expenses flow through to the personal income tax return for those individuals who own S‐Corporations, Partnerships, and LLC’s

GLOBAL CASHFLOW

• Methodology uses information from the following:

1. The business’ tax returns

2. The tax returns of the owner/guarantors

3. The Personal Financial Statement of the guarantor(s)

4. The personal credit report

7

GLOBAL CASHFLOW

• By taking personal cashflow into account, an analyst might find additional means to service business debt

• On the contrary, an excessive lifestyle may reduce the ability to service debt if the owner/guarantor is too highly leveraged personally

THE CASHFLOW STATEMENT

8

THE CASHFLOW STATEMENT

• The Cashflow statement is contained in the financial statements that accountants prepare. It is page three of the spreadsheet package

• It shows how a company has generated cash and how it has used it

• It identifies the sources and uses of funds between two periods of time (usually the end of fiscal years)

• It reconciles the balance sheets of the business by showing the inflows and outflows of cash

CASHFLOW STATEMENT/ METHODOLOGY

1. Calculate Gross Funds Flow (GFF)

Profit after Tax (PAT)

+ Depreciation and amortization

2. Reconcile Net Worth (Spreadsheet Page 2, line 67)

3. Reconcile Capital Expenditures (Spreadsheet Page 2, line 71).

9

CASHFLOW STATEMENT/ METHODOLOGY

4. All other items on Page 3 are derived from the balance sheet, comparing the various accounts between consecutive periods of time

5. Account for each item on the balance sheet (except for fixed assets and net worth accounts)

6. Line 103 should equal the year to year change in cash (Line 1, Page 1)

7. Do not make entries for the first year of balance sheet information. Begin with the second year

CASHFLOW STATEMENT ANALYSIS

• Inflows of cash include:

Gross Funds Flow (Line 74)

Operating Sources of Cash (line 80)

Non‐operating sources of cash (line 102)

• Outflows of cash include:

Operating needs/uses of cash (Line 86)

Non‐operating uses of cash (Line 96)

10

CASHFLOW STATEMENT KEYPOINTS1. Net Operating Cashflow (Line 87) represents the cash

that a business has after it has generated a profit (or loss) and met its operational needs

2. Growth increases the operational needs for cash for a business in most circumstances, unless that business can make operational changes, such as decreasing its receivables and/or inventory, or increasing its payables

3. Increases in operating uses of funds should be met by increases in operating sources of funds (except when increases in Permanent Working Capital occur)

CASHFLOW STATEMENTKEYPOINTS

4. Increases in non‐operating cash uses should be met by increases in non‐operating sources of funds

5. Net operating Cashflow should be sufficient to pay the current portion of long‐term debt (principal) that is due (line 91)

6. Officer debt (or equity accounts) should not be repaid when net operating Cashflow is negative

11

FINANCIAL PROJECTIONS

FINANCIAL PROJECTIONS

Financial projections are important for a number of reasons

1. They often form the basis for determining a business’ ability to repay loans

2. They demonstrate the financial knowledge and understanding of a loan applicant

3. Projections also can increase credibility

12

PROJECTIONS• Represent the final step in building on the results of historical analysis

• They are a look into the future

• Need to be based on reasonable and reliable assumptions

KINDS OF FINANCIAL PROJECTIONS

1. Profit and Loss Statement

2. Balance Sheet

3. Cash Budget

13

PROJECTED PROFIT AND LOSS STATEMENT

Projects sales and all expense items that are tax‐deductible

Usually does not include non‐tax deductible items such as principal payments on term‐debt or some meals and entertainment expenses

The projected P&L shows how a company expects to utilize its resources

DEVELOPING A PROJECTED P& L

Step 1. Project Sales based on:

Trends

Orders

Increased capacity

Recent sales history

Management objectives

External competitive environment

14

DEVELOPING A PROJECTED P & L (cont’d)

Step 2

Project COGS based on :

The business’ most recent trends (%)

Any efficiencies

Step 3

Project SGA based on:

The business’ most recent trends (%)

Any efficiencies

DEVELOPING A PROJECTED P & L (cont’d)

Step 3:Project depreciation based on the expected depreciation of existing assets as well as assets that are to be purchased

Example: A business has assets (buildings and M&E) which are being depreciated annually for an amount of $50,000. The business expects to purchase additional M & E for $150,000 to be depreciated over 5 years. Total projected depreciation = $80K

15

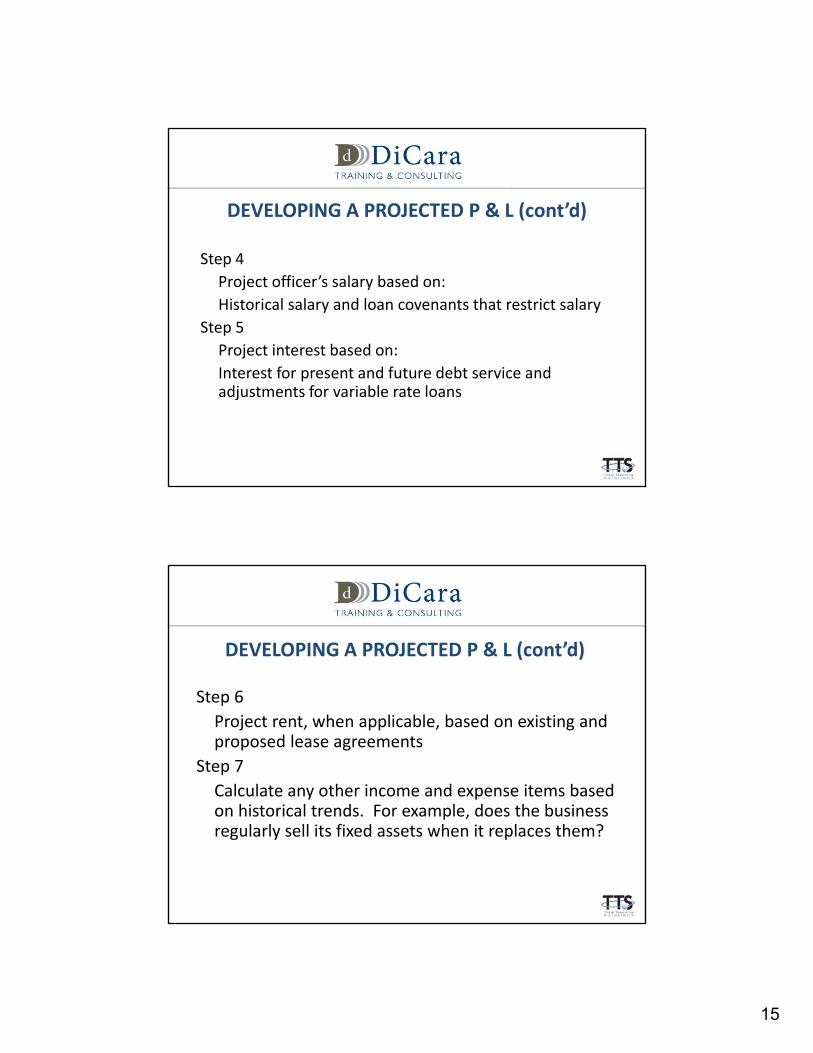

DEVELOPING A PROJECTED P & L (cont’d)

Step 4

Project officer’s salary based on:

Historical salary and loan covenants that restrict salary

Step 5

Project interest based on:

Interest for present and future debt service and adjustments for variable rate loans

DEVELOPING A PROJECTED P & L (cont’d)

Step 6

Project rent, when applicable, based on existing and proposed lease agreements

Step 7

Calculate any other income and expense items based on historical trends. For example, does the business regularly sell its fixed assets when it replaces them?

16

DEVELOPING A PROJECTED P & L (cont’d)

Step 8

Calculate earnings before tax (EBT)

Step 9

Project taxes (for C‐corporations) using the appropriate federal and state tax tables and adjusting for any loss carryover or credits

Step 10

Calculate profit after tax (PAT)

PROJECTING THE BALANCE SHEET

Step 1

Project Net Worth by adjusting net worth accounts for projected PAT and any new equity injections or payment of dividends or other withdrawals of equity. Calculate Total Net Worth

Step 2

Project long term debt (LTD) and current portion of long‐term debt

17

PROJECTING THE BALANCE SHEET (cont’d)

Step 2 (cont’d)

Take into account both existing long term debt and any proposed long term debt. Remember to calculate the current portion of any long term debt and subtract any debt that will be paid off during the time period that the projections cover. Remember to include any long‐term leases, if applicable

PROJECTING THE BALANCE SHEET (cont’d)

Step 3

Project accounts payable based on projected days accounts payable and projected COGS from P & L statement. Use the following formula

Projected A/P=

Projected Days A/P X Projected. COGS

360

18

PROJECTING THE BALANCE SHEET (cont’d)

Step 4

Project accruals based on projected days accruals and projected COGS. Use the following formula:

Projected Accruals=

Projected Days Acc. X Projected. COGS

360

PROJECTING THE BALANCE SHEET (cont’d)

Step 5

Project Short term debt (Note Payable Bank and others). Base on historical debt and owner’s needs

Step 6

Project other liabilities items such as officer debt, income taxes, deposits, etc.

19

PROJECTING THE BALANCE SHEET (cont’d)Step 7

Calculate current liabilities and total liabilities

Step 8

Add total liabilities to Net Worth

Step 9

Insert the result of Step 8 in the Total Assets line

Remember the accounting equation

Assets = Liabilities + Net Worth

PROJECTING THE BALANCE SHEET (cont’d)

Step 10

Calculate projected net fixed assets using the following formula:

Current Net Fixed Assets (NFA)

‐ Projected Depreciation (from P & L)

+ Projected Cap. Expenditures

= Projected Net Fixed Assets

20

PROJECTING THE BALANCE SHEET (cont’d)

Step 11

Calculate any other long term assets; e.g. intangibles based on history and the business’ plan

Step 12

Subtract long term assets from total assets. The result is total current assets

PROJECTING THE BALANCE SHEET (cont’d)

Step 13

Calculate other current assets such as prepaids or deposits

Step 14

Calculate any notes receivable, either as current or long‐term assets

21

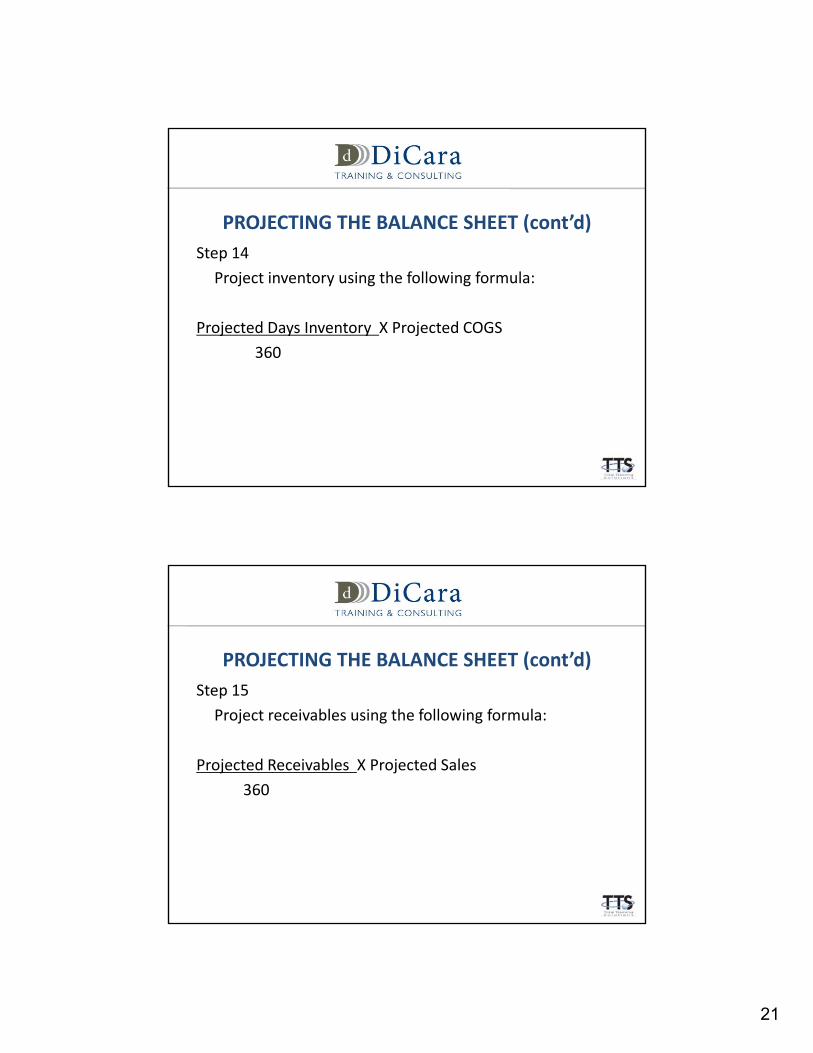

PROJECTING THE BALANCE SHEET (cont’d)

Step 14

Project inventory using the following formula:

Projected Days Inventory X Projected COGS

360

PROJECTING THE BALANCE SHEET (cont’d)

Step 15

Project receivables using the following formula:

Projected Receivables X Projected Sales

360

22

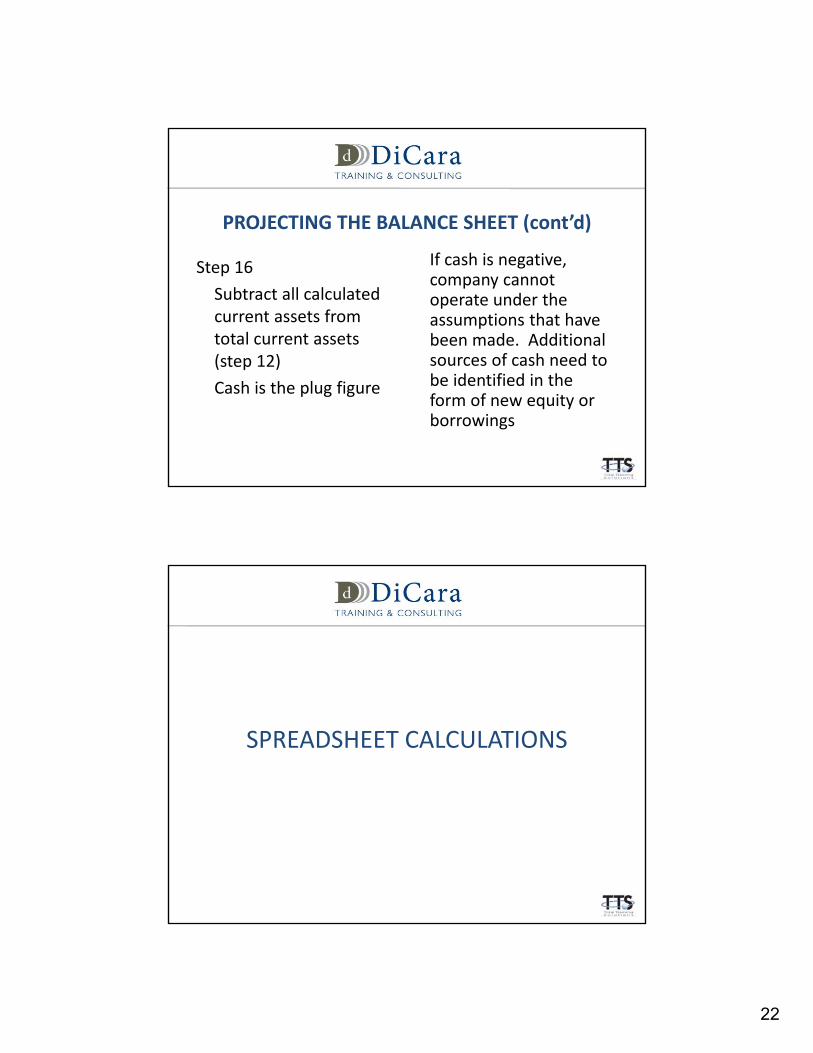

PROJECTING THE BALANCE SHEET (cont’d)

Step 16

Subtract all calculated current assets from total current assets (step 12)

Cash is the plug figure

If cash is negative, company cannot operate under the assumptions that have been made. Additional sources of cash need to be identified in the form of new equity or borrowings

SPREADSHEET CALCULATIONS

23

SPREADSHEET CALCULATIONS

Days Receivable= Receivables/sales X360

Days Inventory= Inventory/COGS X360

Days Payables= Payables/COGS X 360

Days Accruals= Accruals/COGS X360

Working Capital = CA‐CL

Current Ratio= CA/CL

Quick Ratio= Cash + Receivables/CL

Days Cash= Cash/Sales X360

SPREADSHEET CALCULATIONS (cont’d)% Sales Growth=

current year’s sales ‐ previous years sales

previous year’s sales

Debt/equity ratio=

Total Liabilities – Sub. Officer Loans

NW + Sub. Officer loans –Intangibles

24

SPREADSHEET CALCULATIONS (cont’d)Recon. Net Worth= Ending NW

‐ Profit After Tax

‐ Beginning NW

= New Equity (withdrawals)

Cap. Expenditures= Ending Net Fixed Assets

+Depreciation

‐ Beginning Net Fixed Assets

=Net Capital Expenditures

SPREADSHEET CALCULATIONS FOR PROJECTIONS

Projected Receivables= Projected Days Receivables/360 X Projected Sales

Projected Inventory= Projected Days Inventory/360 X projected COGS

Projected Payables= Projected Days Payables/360 X Projected COGS

Projected Accruals= Projected Days Accruals/360 X projected COGS

25

SPREADSHEET CALCULATIONS FOR PROJECTIONS (cont’d)

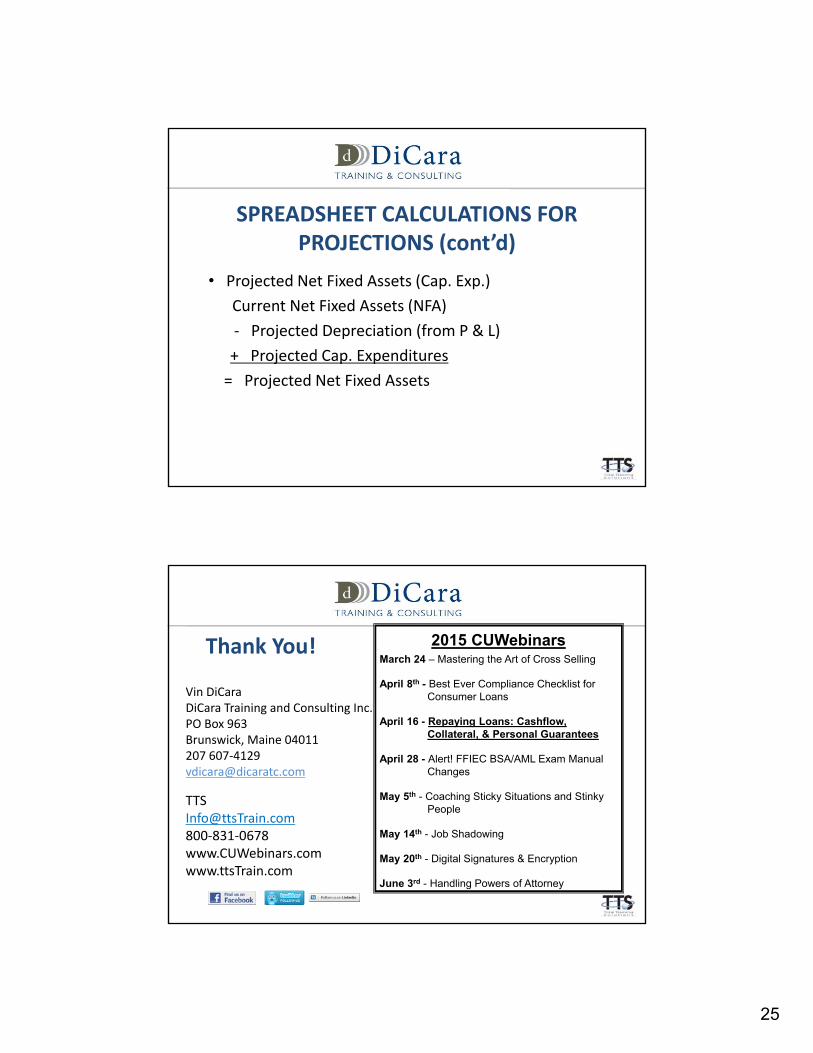

• Projected Net Fixed Assets (Cap. Exp.)

Current Net Fixed Assets (NFA)

‐ Projected Depreciation (from P & L)

+ Projected Cap. Expenditures

= Projected Net Fixed Assets

Thank You! 2015 CUWebinarsMarch 24 – Mastering the Art of Cross Selling

April 8th - Best Ever Compliance Checklist for Consumer Loans

April 16 - Repaying Loans: Cashflow, Collateral, & Personal Guarantees

April 28 - Alert! FFIEC BSA/AML Exam Manual Changes

May 5th - Coaching Sticky Situations and Stinky People

May 14th - Job Shadowing

May 20th - Digital Signatures & Encryption

June 3rd - Handling Powers of Attorney

[email protected]‐831‐0678www.CUWebinars.comwww.ttsTrain.com

Vin DiCaraDiCara Training and Consulting Inc.PO Box 963Brunswick, Maine 04011 207 607‐[email protected]