case study-tom tsee_eh

TRANSCRIPT

Tom Tsee

October, 2014

PROJECT DUTY LBO Investment Analysis

An independent LBO investment assessment by industry, firm’s operation, and uncertain risks.

Table of Contents

Portable Toilet Rental & Septic Tank Cleaning Industry ............................................................... 2

Market Position ............................................................................................................................... 6

Revenue, Expense, EBITDA, CAPEX and Return Rate ................................................................ 6

Uncertain Risks – Oil Production and Customer Concentration .................................................... 9

Appendix: LBO Model

Executive Summary:

Majority interest makes it possible to explore new market strategy and deviate from its heavily

dependence on the performance of oil industry in Bakken formation.

Portable Toilet Rental & Septic Tank Cleaning Industry

Basic Industry Data

Annual Revenue: $5bn Annual Growth (09-14): 6.0%

Employment: 33,927 Businesses: 4,482

Estimated portable restrooms: 3million Fleet: over 10,000 trucks

Business Breakdowns—Toilet Rentals or Septic Tank Service

Most of major players in this industry don’t provide residential or commercial septic tank

cleaning service. The reason is simple. Only toilet rental business, which is the major

source of business in this industry, can create opportunities for companies to grow bigger.

However, toilet rental business, which depends mainly on construction and entertainment

events activities, are usually concentrated in urban area where there are complete public

septic systems. On the other hand, while septic tank service providers, who serve areas

where public septic system isn’t able to reach, also provide toilet rental service, the

business is usually limited by less construction and events in their service areas.

However, companies focusing on industrial service in some particular regions, such as

active mines or oil &gas wells, are able to take advantage of the favorable business

circumstance by providing both services. Coupled by fast population growth, those

companies can gain steady revenue from septic tank service and as well huge potentials

to grow from toilet rentals.

Portable Toilet Rental Sector

Market Segments:

Main revenue sources for Portable Toilet Rental companies come from constructions

(60%), entertainment events (20%), and Recreation parks, agriculture and industrial

service (20%). Among those segments, agriculture and industrial service account for a

small percentage and generally play less important roles due to their seasonal and

regional nature. Constructions and events explain for most of revenues.

Growth Drivers:

Entertainment event has been providing steady revenue for this industry and presented

strong resistance to recession in the past several years. However, hit by the downturn of

housing market, this industry has suffered until the construction activities rebound since

2012. While the whole industry has benefited from the broad economic recovery,

segment analysis indicates that increasing construction activities is the major driver

behind this sector’s growth in the past several years. The increasing toilet rental business

is consistent with national hot housing market. Geographic analysis by region shows that

business activity is concentrated in the Southeast region (22.9% of establishments), Great

Lakes (18.1% of establishments), Mid-Atlantic (14.4% of establishments) and the West

(12.7% of establishments).

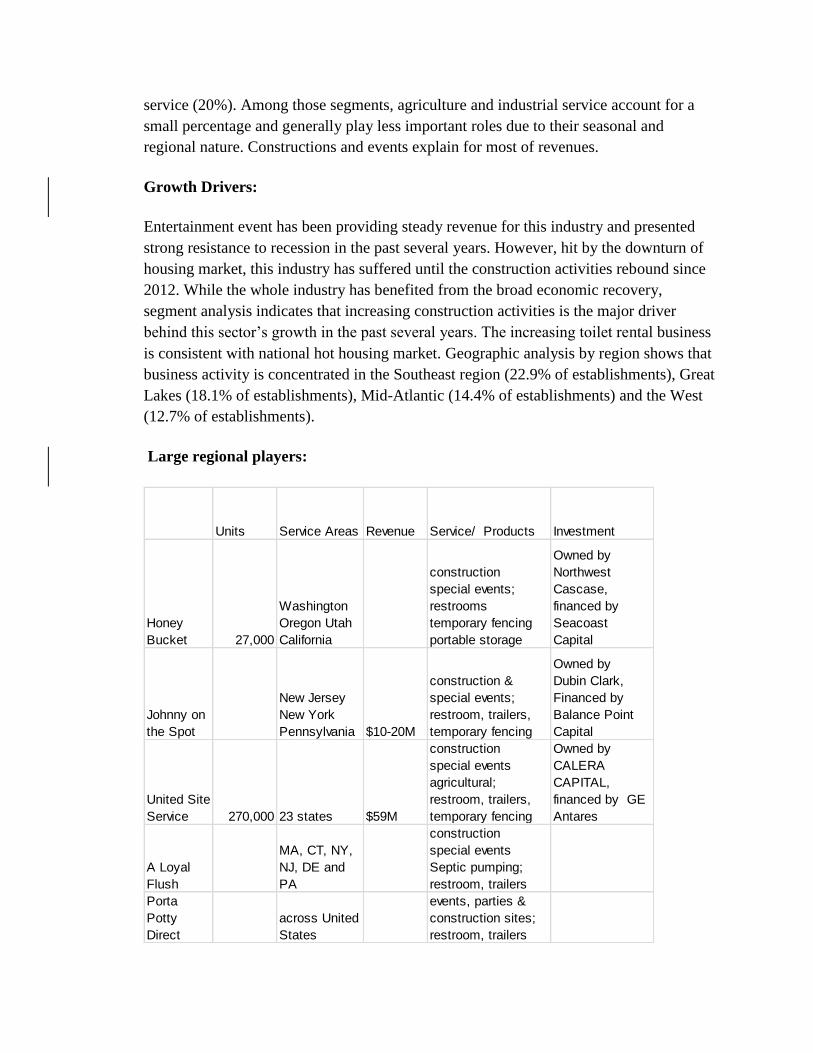

Large regional players:

Units Service Areas Revenue Service/ Products Investment

Honey

Bucket 27,000

Washington

Oregon Utah

California

construction

special events;

restrooms

temporary fencing

portable storage

Owned by

Northwest

Cascase,

financed by

Seacoast

Capital

Johnny on

the Spot

New Jersey

New York

Pennsylvania $10-20M

construction &

special events;

restroom, trailers,

temporary fencing

Owned by

Dubin Clark,

Financed by

Balance Point

Capital

United Site

Service 270,000 23 states $59M

construction

special events

agricultural;

restroom, trailers,

temporary fencing

Owned by

CALERA

CAPITAL,

financed by GE

Antares

A Loyal

Flush

MA, CT, NY,

NJ, DE and

PA

construction

special events

Septic pumping;

restroom, trailers

Porta

Potty

Direct

across United

States

events, parties &

construction sites;

restroom, trailers

M&A Trend

Increasing demands for portable toilets rentals, which has been fueled by construction

activities’ pickups, is the key driver behind the intensive strategic acquisition activities of

investment firms in the past 2 years. Under the help of investment capital, the large firms

thus are able to acquire more small firms to meet this demand for portable toilet rentals

and as well grab benefit from economy scale.

Recent M&A Transactions:

o April 21, 2014, Balance Point Capital Partners, in conjunction with its capital

partner, Dubin Clark, announced the acquisition of Johnny on the Spot, LLC.

o Aug 13, 2014, GE Antares, a unit of GE Capital, announced it served as

administrative agent on a $265 million senior secured credit facility to support the

acquisition of United Site Services (USS) by Calera Capital,.

o 2013, Northwest Cascade, the home of Honey Bucket, was recapitalized by

Seacoast Capital.

o Apr 24, 2014 – United Site announced the acquisition of S&S Portable Services.

o October 8, 2014, Johnny on the Spot, LLC announces the Acquisition of D.

Lovenberg’s Portable Toilet Rentals, Inc. of Andover, NJ.

o March 21, 2014, Johnny on the Spot announces the Acquisition of Atlantic

Restrooms, Jackson, NJ.

New Technology Progress

Direction of technology progress is to make portable toilet more comfort and

environment friendly. Top companies have been seeing increasing revenue from rentals

of luxury toilet and trailers and use of environment favorable deodorizers.

Full functionalities of firm’s website

o Online quote

o Services and products compares

o Online chat to gain knowledge and advice according to event’s need

o Outdoor events training and guideline for getting permit.

o what other services do these guys provide

o other interesting things

Operating and Pricing

Pricing varies depending on locations:

o Events ( take an example of United Site Service, New York)

$196+tax/unit per week (one week minimum) ($10 more in San Francisco)

Service every 4-5 hours/100 persons

At least one week notice in advance

o Events ( take an example of Honey Bucket)

$103+tax/unit per week (one week minimum) (Berkeley, California)

o Construction site ( take an example of Johnny On the Spot, New York)

$296+tax for first 8 weeks and daily charge at same rate after 8 weeks

Service once a week

One day notice delivery

Portable Sanitation Association International

http://psai.uberflip.com/i/125265/96.

List of the member companies/Advertisement from companies who want to market

products to portable toilet rental companies

Septic Tank Cleaning Sector

Industry growth has been supported by steady demand from government for waste-

holding and drain-cleaning services.

Businesses tend to locate near regions with a high proportion of households that were

built with septic tank systems.

Due to the limit of economy scale, there is no company dominating in this sector.

Market Position ---benefiting from both segments of toilet rental and septic tank cleaning

businesses

This specific sector of market in this industry is located traditionally in the segment of

industrial service (as mentioned above). The companies in this segment provide portable

toilet rentals service to meet demand from work sites of wells. However, due to unusually

fast growth of population fueled by oil development activities in some of those areas,

highly concentred population created tremendous business opportunities for septic tank

service. In addition, growth of population also stimulated housing activities in small cities

around wells and thus provided opportunities for those local companies to gain extra

business from portable toilet rentals.

Revenue, Expense, EBITDA, CAPEX and Return Rate

Revenue

Continuing oil boom in North Dakota

It is true that North Dakota oil boom starting from 2008 has been accompanied with a

period when the oil price stays at high level. However, the lowered oil exploration cost

resulted from new technology has played significant role. While we are not able to know

where the oil price goes, there is a significant buffer for the price to go down before it

freezes new drilling activities in this area. At the same time, while hot money behind high

oil price may leave as economy recovery is getting faster, the stronger economy will still

become a support for price of oil.

Analysis of Source of Revenue (see chart)

All “other clients” actually contributed almost all growth in revenue between 2011 and

2014 (except for 2013, an outlier). This fact reflects that a strong demand in PROJECT

DUTY serving area has been existing, which will be supported by strong population

growth resulting from new drilling activities. None of “other clients” constantly occupies

the list of top 10. This highly diversified distribution avoids firm-specific risk.

While Customer 1, PROJECT DUTY’s biggest client, will also benefit from strong

workforce growth in that area, there is firm-specific risk for this company.

2011 2012 2013 2014 1stH

Total revenue $2.9MM $4,6MM $6.2MM $2.7MM

Customer 1 $2.1MM (72%) $2.1MM (45.5%) >$3.1MM (50%) $1.2MM (44%)

Others $0.8MM $2.5MM $3.1MM $1.5MM

Customer 1’ potential issue and the worst case.

Customer 1 provided constant revenue of $2.1MM or more annually. This may be a result

that most of Customer 1 sales come from its facility in Tioga, Williams County, North

Dakota. However, this company is facing uncertain changes in government policy, the so

called “Man Camp” controversial issue. According to Wikipedia, “the Williams County

Planning and Zoning Commission recommended that the county refrain from both

issuing permits for new workforce housing and allowing existing facilities to expand”.

This may mean that Customer 1 will probably lose business as workers move into other

alternative housing.

Conservative estimate

In this case, the controversy involved with “Man Camps" doesn’t go against Customer 1.

And Demands from PROJECT DUTY’s other small clients are still strong, thanks to its

reputation and local economy. However, limited by market size in Minot area, revenue

will be only able to keep its current level or a moderate growth.

Optimistic estimate

Benefited from Buyer’s input in marketing and sales, or from the strengthened pricing

strategy and optimised routing, PROJECT DUTY successfully increases its revenue from

long distance clients of oil area. PROJECT DUTY should be able to aim at annual 10%

increase in revenue from new clients.

Expense

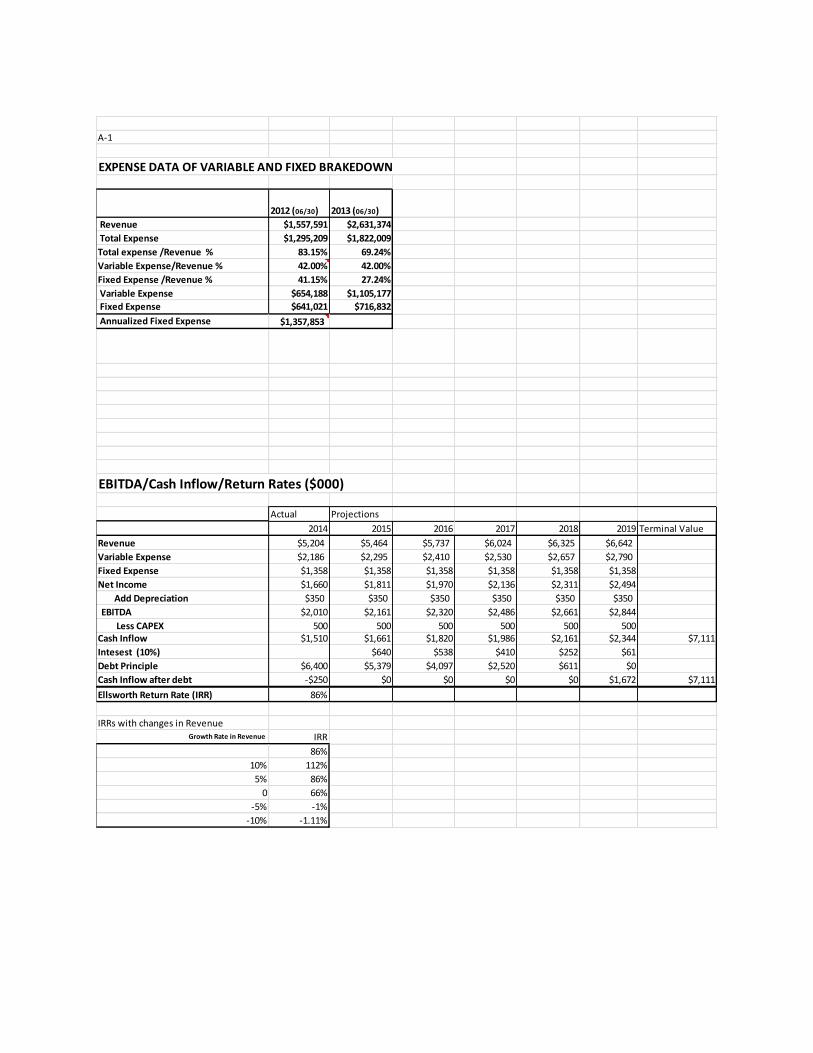

Model (excel file attached) built summarized breakdown of variable expense and fixed

expense, based on data of 2012 and 2013 1st H, which I think, after tests, best

demonstrate the expense distribution at current revenue construction.

Variable expenses include Fuel and oil, equipment repairs and trucking, which are

constantly proportional to revenue. Their percentages of revenue used in model are: 11%,

4%, and 27%.

Fixed expense was calculated by averaging the fixed expenses of 2012 and 2013 and

assumed $350,000 depreciation.

CAPEX

Fixed asset investment in 2011-2014 (in thousands)

2011 2012 2013 2014 1stH

$764 $325 $249 $278

Annualized CAPEX is $478 or $0.5MM.

EBITDA/Cash Inflow/Return Rates

Models (see excel file attached) analysis in this sector is based on the projected $5.2MM

of revenue in 2014 (calculated with data: $2.7MM of 2014 1stH, ratio1stH and 2nd H of

2013)

1. Very conservative case

We assumed that revenue will keep constant on the basis of 2014 projection. In

this case, the debt can be paid off in 5 years and there will be 66% IRR if exit with

2.5X price.

2. The most conservative estimate

We assumed, due to Customer 1’s trouble that the revenue start to decline by 5%

annually after acquisition. In this case, the debt will not be paid off after 5 years

and there will be an IRR of zero if exit with 2.5X price at that point.

3. Optimistic case

We assumed that revenue increase by 5% annually, based on data of 2014

projection. In this case, the debt can be paid off in 4 years and there will be 86%

IRR if exit with 2.5X price.

Uncertain Risks – Oil Production and Customer Concentration

Analysis of oil production activities in Bakken formation

How long oil boom will last depends on two factors: 1. Recoverable amount of oil in oil

resource 2. Price of oil and exploration cost. Data provided by the following research

reports indicate that estimated amount of technically recoverable oil in Bakken formation

of North Dakota increase from 3.0to 4.3 billion barrels of 2008 to 7.4 billion barrels of

2013. An analysis by comparing historical price of oil and chart of production of oil in

Bakken of North Dakota indicate that oil production has increased strongly in period of

2008 to 2013 when the oil price fluctuated in the range of $60-$100 per barrel. It means

the breakeven point for oil production should be below $60 per barrel, which leave a

large buffering space considering that the current price is around $90/barrel.

Source: Wikipedia

Source of Revenue, and Customer 1 and its customer,

According to the revenue source chart, Business from Customer 1 build a base of revenue and

all other PROJECT DUTY’s small customers have contributed most of revenue increase.

However, it is not necessary that PROJECT DUTY can’t afford a decrease in revenue from

Customer 1.

Effort to develop new customers can help make up the loss of business from Customer 1

if there is. If the analysis of oil production in this area is correct, there is reason to think

that this trend will go on because what is behind this trend is the strong population

growth and also effort of PROJECT DUTY to expand into oil field where there is no

physical market size limit.

Customer 1, in fact, has begun to build other type of housing such as a hotel as a response

to critics to its “man camp”. Its impacts to PROJECT DUTY and solutions:

1. No new permits for temporary housing may become a fact in future, but it will not

happen in near future. Existing housing ensures that PROJECT DUTY servicing for

Customer 1’s facility in Tioga will be guaranteed at current level. In fact, PROJECT

DUTY hasn’t been very dependent on increase of Customer 1’s business. Its toilet

business with Customer 1 will not be influenced by any potential negative changes.

2. Even if Customer 1 builds a permanent housing in Tioga, the process of replacement

will take a while. New housing still need septic service before public sewage system

is built. Uncertainty is whether building permanent housing is Customer 1’s long plan

which means a change of its business model.

3. PROJECT DUTY has sufficient time to react to the potential negative changes if

there is, since it will not impact on PROJECT DUTY cash flow in short term, but

possibly on the terminal value.

4. Strongly suggest that PROJECT DUTY utilize its high operating leverage, as

analyzed in my model, by managing to expand into oil field area without considering

too much the distance cost. For PROJECT DUTY, any increase in revenue beyond its

current level, even if margin is much smaller than its service in near location, will

significantly improve its profit. Adjusting pricing strategy may be one of methods.

For example, lower its charge of mileage for distant service or take advantage of the

relationship between Customer 1 and Whiting Petroleum.

A-1

EXPENSE DATA OF VARIABLE AND FIXED BRAKEDOWN

2012 (06/30) 2013 (06/30)

Revenue $1,557,591 $2,631,374

Total Expense $1,295,209 $1,822,009

Total expense /Revenue % 83.15% 69.24%

Variable Expense/Revenue % 42.00% 42.00%

Fixed Expense /Revenue % 41.15% 27.24%

Variable Expense $654,188 $1,105,177

Fixed Expense $641,021 $716,832

Annualized Fixed Expense $1,357,853

EBITDA/Cash Inflow/Return Rates ($000)

Actual Projections

2014 2015 2016 2017 2018 2019 Terminal Value

Revenue $5,204 $5,464 $5,737 $6,024 $6,325 $6,642

Variable Expense $2,186 $2,295 $2,410 $2,530 $2,657 $2,790

Fixed Expense $1,358 $1,358 $1,358 $1,358 $1,358 $1,358

Net Income $1,660 $1,811 $1,970 $2,136 $2,311 $2,494

Add Depreciation $350 $350 $350 $350 $350 $350

EBITDA $2,010 $2,161 $2,320 $2,486 $2,661 $2,844

Less CAPEX 500 500 500 500 500 500Cash Inflow $1,510 $1,661 $1,820 $1,986 $2,161 $2,344 $7,111

Intesest (10%) $640 $538 $410 $252 $61

Debt Principle $6,400 $5,379 $4,097 $2,520 $611 $0

Cash Inflow after debt -$250 $0 $0 $0 $0 $1,672 $7,111

Ellsworth Return Rate (IRR) 86%

IRRs with changes in Revenue Growth Rate in Revenue IRR

86%

10% 112%

5% 86%

0 66%

-5% -1%

-10% -1.11%