carbon markets an international tool for cost-effective ghg mitigation

TRANSCRIPT

Carbon marketsAn international tool for cost-effective GHG

mitigation

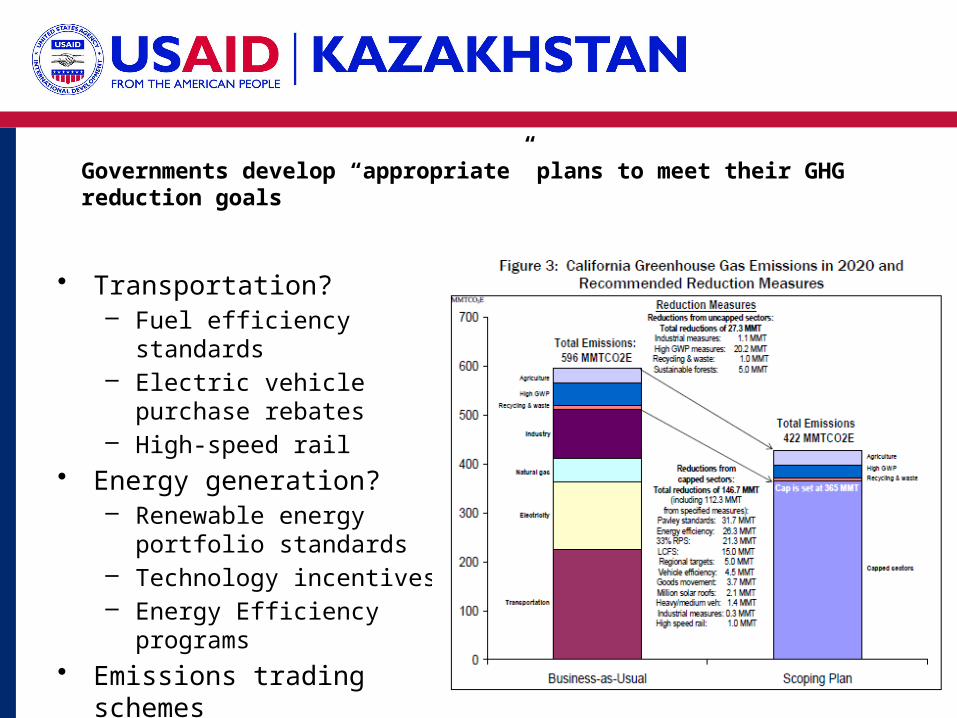

Governments develop “appropriate” plans to meet their GHG reduction goals

• Transportation? – Fuel efficiency standards– Electric vehicle purchase

rebates– High-speed rail

• Energy generation?– Renewable energy portfolio

standards – Technology incentives– Energy Efficiency programs

• Emissions trading schemes• And more…

Market elements are adapted to local conditions

– Coverage and Scope– Cap and allocations– Requirements and systems for monitoring, reporting,

verification and compliance– Trading and stability– Institutional arrangements – Use of offsets and linking

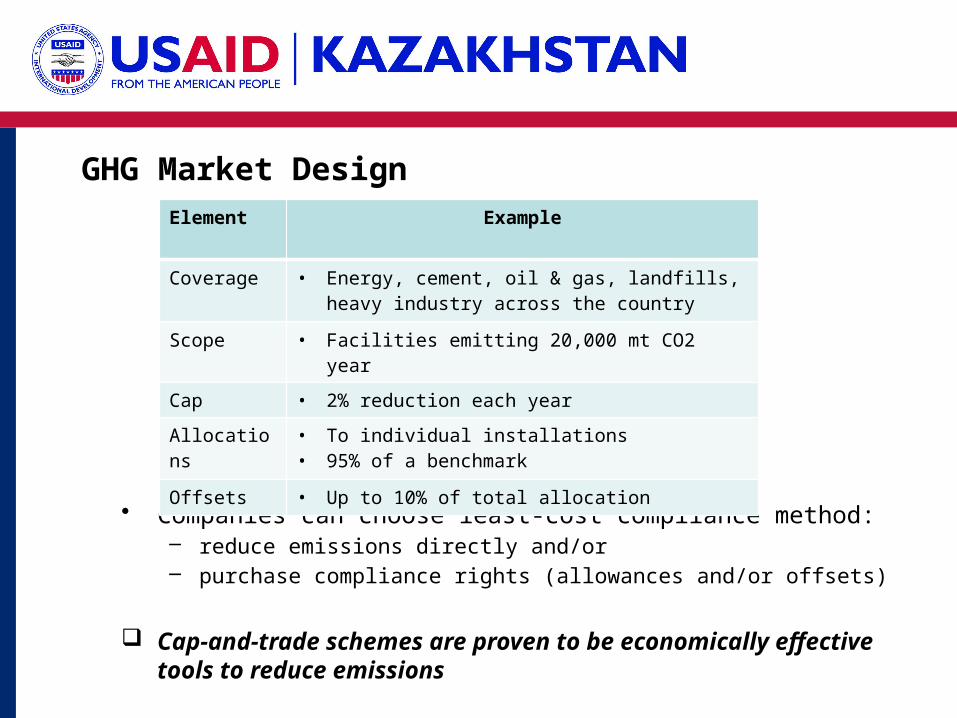

GHG Market Design

• Companies can choose least-cost compliance method:– reduce emissions directly and/or– purchase compliance rights (allowances and/or offsets)

Cap-and-trade schemes are proven to be economically effective tools to reduce emissions

Element Example

Coverage • Energy, cement, oil & gas, landfills, heavy industry across the country

Scope • Facilities emitting 20,000 mt CO2 year

Cap • 2% reduction each year

Allocations • To individual installations• 95% of a benchmark

Offsets • Up to 10% of total allocation

Existing and emerging emissions trading schemes

Source: World Bank, 2013, Mapping Carbon Pricing Initiatives.

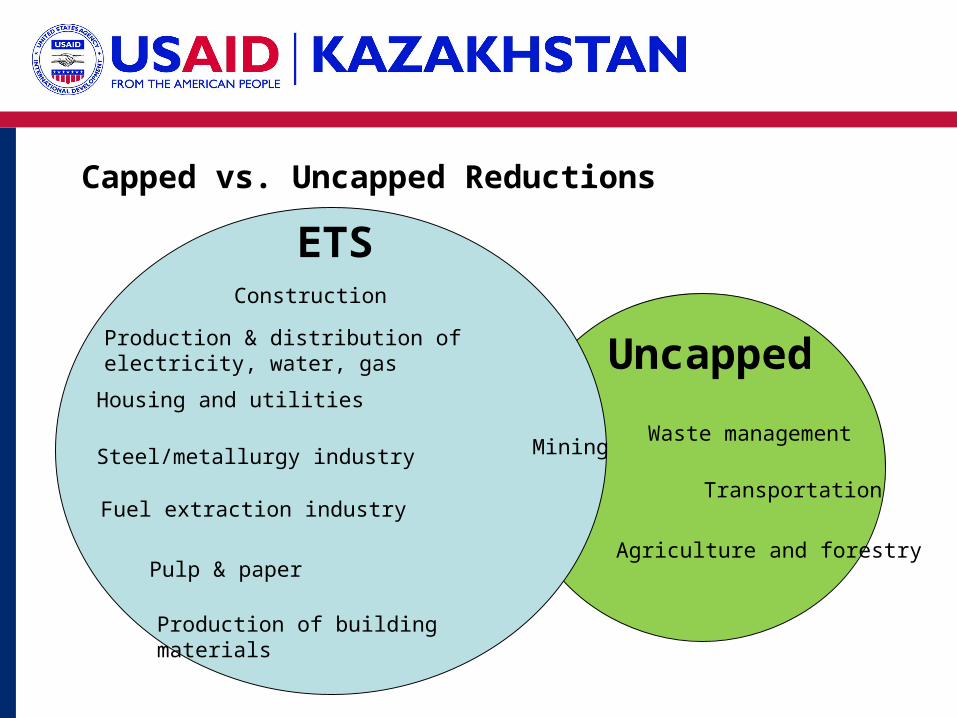

Capped vs. Uncapped Reductions

Housing and utilities

ETSConstruction

Steel/metallurgy industry

Production of building materials

Mining

Pulp & paper

Fuel extraction industry

Production & distribution of electricity, water, gas

Agriculture and forestry

Waste management

Transportation

Uncapped

Two Pathways for GHG Reduction Projects

Capped Sector Projects

• Example: renewable electricity and energy efficiency projects

• Can use streamlined standards and proceduresProjects are given quota allocations based on GHG reductions achieved

Uncapped Sector Projects

• Example: Coal mine methane reductions

• Quantified using carbon offset methodologiesProjects are issuedcarbon offset credits based on GHG reductions achieved

ENVIRONMENTAL MARKETS IN OPERATION

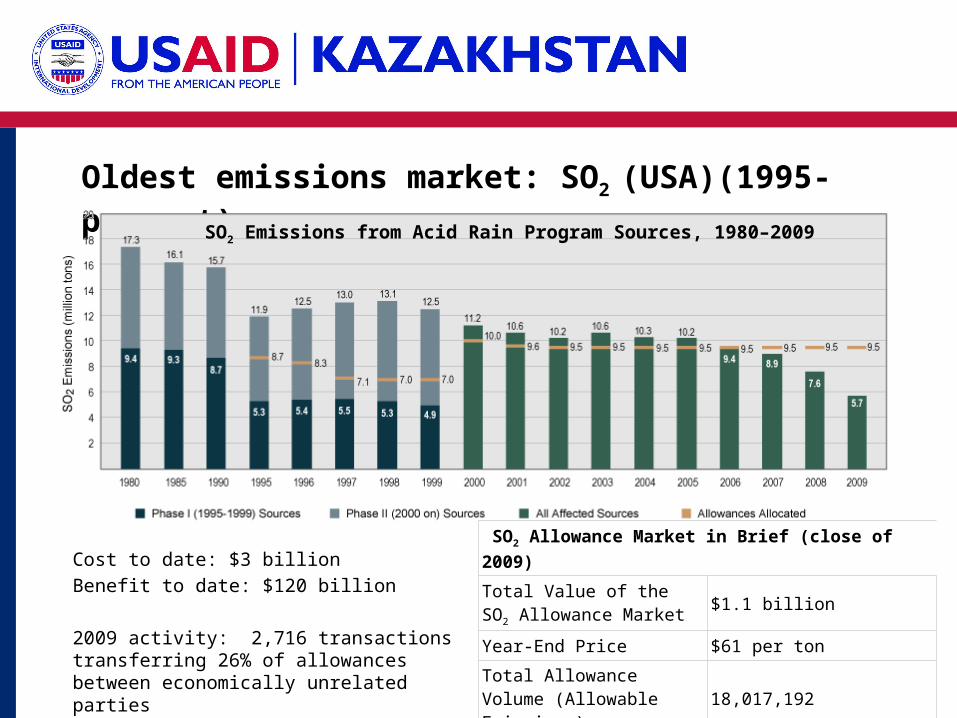

Oldest emissions market: SO2 (USA)(1995-present)

Cost to date: $3 billion

Benefit to date: $120 billion

2009 activity: 2,716 transactions transferring 26% of allowances between economically unrelated parties

SO2 Allowance Market in Brief (close of 2009)

Total Value of the SO2 Allowance Market $1.1 billion

Year-End Price $61 per ton

Total Allowance Volume (Allowable Emissions) 18,017,192

SO2 Emissions from Acid Rain Program Sources, 1980–2009

GHG Market: Kyoto Protocol (1997)

• Countries committed to binding national reduction targets

• Allows use of “Flexibility Mechanisms” to meet reduction targets– Emissions trading– Clean Development Mechanism– Joint Implementation

European Union: Emissions Trading Scheme (ETS)

• First GHG ETS to launch (2005)

• Today 28 member countries participating + Iceland, Liechtenstein, Norway– Cap decreases annually 1.74%

across EU– Has grown as the EU has grown

during the same period– Covers 45% of total emissions– 11,000 installations

EU ETSPhase 1: 2005-2007 (pilot)

Phase 2: 2008-2012 – CO2 emissions from fuel combustion + 5 industrial

sectors– National caps– Mostly free allocation

Phase 3: 2013-2020 – aviation + other activities + N2O (some activities) + PFCs (aluminum)

– Greater harmonization; one EU-wide cap– Increased auctioning of allowances (40% in 2013

with the % increasing each year– Benchmark-based allocations – 300 million allowances reserved for renewable

energy + CCS

EU ETS: Reductions/allocations

– Allocations have tightened over time• Backloading auction of some allowances

– 49% offsets possible across EU• Each country sets own limits within national scheme• CDM units can be converted to offsets, but now only from LDCs

CO2

EU ETS

(2005)

New Zealand (2008)

Economy-wide + forestry

Electric power

RGGI (USA) (2009)

California (Jan 2012)

Economy-wide

Standard-ized offsets

CO2 from Industrial sources + buildings

Tokyo

(April 2012)

Aus-tralia (July 2012)

Carbon Pricing Mech-anism

Link to EU ETS

Economy-wide

(First in Asia)

Kazakhstan

(2013)

China Pilot ETS

(2013)

Voluntary ETS (2012)

carbon tax or offsets

(2014)

Mexico

South Korea (2015)

Learning from the EU ETS

Markets reflect local circumstances

South Africa: one company @ 90% of national industrial emissions so prefer carbon tax

Tokyo – electricity consumption in buildings

New Zealand – include protection of forests

California – 8% limit on offsets to reflect desired level of in-state reductions

One global carbon market?

• Learning by doing• Minimum requirements are necessary to one day link

carbon markets• Provides investment in clean, green technology

Source: World Bank, 2013, Mapping Carbon Pricing Initiatives.