capital structure lecture 8 dr francesca gagliardi 2bus0197 – financial management

TRANSCRIPT

Capital Structure

Lecture 8

Dr Francesca Gagliardi

2BUS0197 – Financial Management

Learning outcomes

By the end of the session students should be able to:

Appreciate the traditional approach to the existence of an optimal capital structure

Understand Modigliani and Miller’s propositions on capital structure

Explain the rational underlying the pecking order theory

Critically discuss whether a company can influence its cost of capital by adopting a particular capital structure

2

Knowledge development

Last week we looked at how a company can determine its average cost of capital (WACC) by calculating the costs of the various sources of finance used and weighting them according to their relative importance

The market value of a company depends on its WACC The lower the WACC, the higher the NPV of future cash flows,

hence a company’s market value

We now need to consider whether the way in which a company’s financing decisions affect its WACC

3

Key questions

Does the mix of debt and equity finance used by a company affect its weighted average cost of capital?

Is there a mix of debt and equity that will minimise the average cost of capital?

A minimum cost of capital will maximise the market value of the firm and hence maximise shareholder wealth

The academic debate on the above questions has been controversial

4

The traditional approach

Simplifying assumptions

No taxes exist

Financing choice is between ordinary shares and perpetual debt

Capital structure changes incur no cost and entail replacing debt with equity or vice versa

All earnings are paid out as dividends

Business risk is constant over time

Earnings and hence dividends are constant

5

Key proposition

An optimal capital structure exists

A company can increase its total value by sensibly using debt finance within its capital structure

The combination of debt and equity finance that minimises a company’s overall cost of capital should be selected as this enables shareholder wealth maximisation

6

The traditional approach to capital structure

Ke increases as gearing increases due to rising financial risk and, later, bankruptcy risk

Kd rises at high levels of gearing due to bankruptcy risk

As the company starts to replace expensive equity with cheaper debt, WACC falls

As gearing continues to increase, Ke and Kd increase, offsetting the benefit of cheap debt

Point A: the firm is entirely financed by equity

Point B: minimum WACC

Debt/Equity0

Cost (%) Ke

WACC

Kd

Optimal capitalOptimal capitalstructurestructure

A

B

7

Modigliani and Miller (I): the net income approach (1958)

Capital markets are assumed to be perfect

No risk of bankruptcy so Kd curve is flat

Linear increase in Ke due to increasing financial risk

As the company gears up and replaces equity with debt, the benefit of cheaper debt is exactly balanced by the increasing cost of equity

No optimal capital structure is found

8

Modigliani and Miller (I): the net income approach In their model, beside the assumptions previously discussed,

capital markets are assumed to be perfect

Bankruptcy risk can be ignored as firms in financial distress can always raise additional finance

The key proposition is that a company’s WACC remains unchanged at all levels of gearing, implying that NO optimal capital structure exists for a particular firm

The market value of a company depends on its expected performance and commercial risk

A firm’s market value and its cost of capital are independent of its capital structure

9

Net income approach The Ke line shows a linear

relationship between the cost of equity and financial risk (level of gearing)

Since debt holders do not face bankruptcy risk, Kd is horizontal to illustrate that the cost of debt is independent of the level of gearing

WACC is constant as the benefit of using an increased level of cheaper debt finance is exactly offset by the increasing cost of equity finance

Since WACC is constant, net income is constant too and so is the firm’s market value

WACC

Kd

Cost (%)

Debt/Equity0

Ke

A

10

Implications of M&M proposition I

The WACC of a geared company is identical to the cost of equity the company would have if it were financed entirely by equity

The cost of equity is determined by the risk-free rate of return and the business risk of the company

Cost of equity independent of financial risk (i.e. level of gearing)

11

M&M (I) and arbitrage theory Miller and Modigliani supported their argument of capital structure

irrelevance in determining a firm’s market value and WACC by using arbitrage theory

Arbitrage proof using companies A and B:

A B

Net income 1000 1000

Interest at 5% Nil 150

Earnings 1000 850

Divide by cost of equity 10% 11%

MV of equity 10 000 7 727

MV of debt Nil 3 000

Total market value 10 000 10 727

WACC 10% 9.3% 12

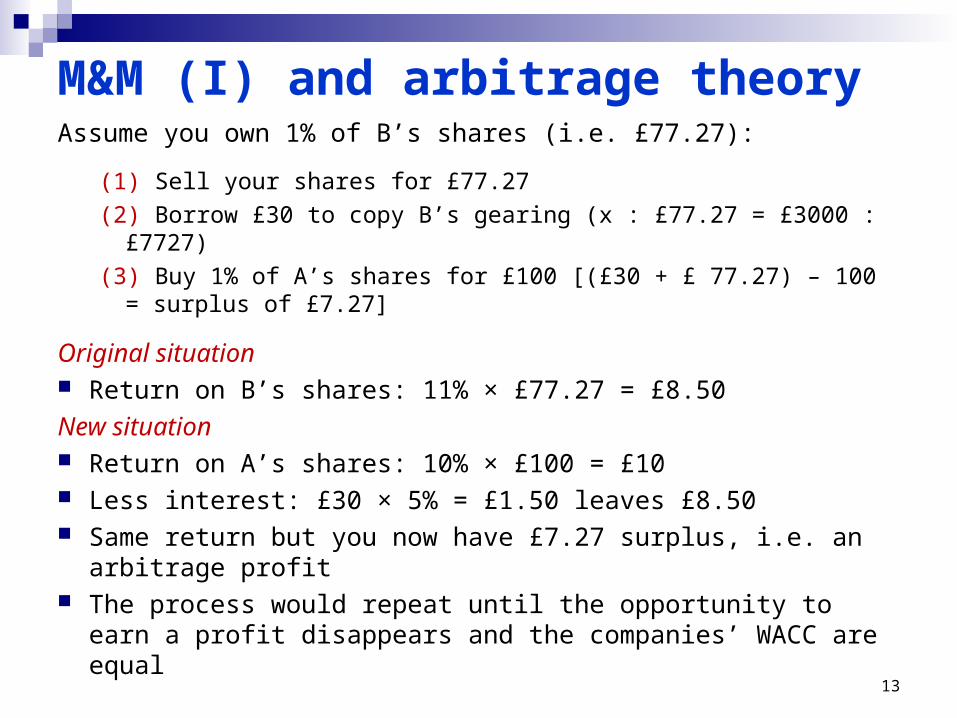

M&M (I) and arbitrage theoryAssume you own 1% of B’s shares (i.e. £77.27):

(1) Sell your shares for £77.27

(2) Borrow £30 to copy B’s gearing (x : £77.27 = £3000 : £7727)

(3) Buy 1% of A’s shares for £100 [(£30 + £ 77.27) – 100 = surplus of £7.27]

Original situation Return on B’s shares: 11% × £77.27 = £8.50

New situation Return on A’s shares: 10% × £100 = £10 Less interest: £30 × 5% = £1.50 leaves £8.50 Same return but you now have £7.27 surplus, i.e. an arbitrage

profit The process would repeat until the opportunity to earn a profit

disappears and the companies’ WACC are equal 13

Modigliani and Miller (II): corporate tax (1963) Miller and Modigliani adjusted their first model to reflect

the existence of corporate tax and the tax deductibility of interest payments

Gearing up by replacing equity with debt gives the benefit of a tax shield, increasing the value of company

This implies that an optimal capital structure does exist: this is 100% debt finance

Kd curve falls from before-tax to after-tax level, so WACC curve slopes downwards

14

Modigliani and Miller (II)

0 Debt/Equity

WACC

Ke

Kd

Cost (%)

Kd(1 –CT)

15

Modigliani and Miller (II)

The tax advantage enjoyed by debt finance over equity finance means that WACC decreases as gearing increases

Hence, the optimal capital structure is one that uses as much debt finance as possible (ideally 100%)

16

Debt/Equity0

Ke

WACC

Kd(1 –CT)

Cost (%)

Market imperfections

Since in practice firms do not adopt an all-debt capital structure, this means that there are market imperfections which undermine the tax advantages of debt finance

These factors are: Bankruptcy costs

Agency costs

Tax exhaustion

17

Bankruptcy costs

By assuming perfect capital markets, Modigliani and Miller’s second proposition ignores bankruptcy costs

In reality at high levels of gearing there is a default risk on interest payments, hence a bankruptcy risk

Hence, at high levels of gearing shareholders require a higher rate of return to compensate them from facing bankruptcy risk

Combining the tax shield advantage of increasing gearing with the bankruptcy costs associated to high gearing, an optimal capital structure emerges

18

Modigliani and Miller incorporating bankruptcy risk

19

Market value with tax benefit

Market value of all-equity firm

Market value with tax and bankruptcy costs

0

Firm’s market value

Optimal capitalOptimal capitalstructurestructure

Debt/Equity

X Y

A

B

C

D

Agency costs With high gearing levels shareholders have a lower stake in the

company and have fewer funds at risk if the company fails

Shareholders will prefer the company to invest in high-risk high-returns projects since they will enjoy the benefit of the higher returns

If those projects were undertaken, providers of debt finance would not share the higher returns (their returns are not related to firm’s performance). They would only be exposed to a higher risk

Debt financiers will take steps to prevent the company from starting high-risk projects (e.g. restrictive covenants, increased management monitoring)

The above agency costs will reduce the tax shields benefits associated with increasing gearing levels

20

Tax exhaustion

Many companies have insufficient profits from which to derive all available tax benefits as they increase their gearing level

This will prevent them from enjoying the tax shield benefits associated with high gearing, but still leave them liable to incur bankruptcy costs and agency costs

21

Pecking order theory Donaldson (1961): companies have a well-defined order

of preference with respect to the sources of finance available to them

First preference is internal finance or retained earnings

Next, bank borrowings and corporate bonds

Finally, issue of new equity

The order of preferences is based on issue costs and the ease with which financing sources are accessed

Myers (1984) suggested that the pecking order is explained by asymmetric information between firms and capital markets

22

Recap on existence of optimal capital structure (OCS)

Traditional approach: OCS exists

Modigliani and Miller I: no OCS is found

Modigliani and Miller II: OCS is 100% debt

Market imperfections: OCS exists

In practice, rather than one optimal capital structure existing for each firm, a range of optimal capital structures may exist

23

A practical view

Theoretical WACC

WACC in practice

OCS0

A range of optimal capital structures

Debt/Equity

Cost (%)

24

Summary

Today we discussed the main theoretical approaches to the existence of an optimal capital structure

and

We evaluated the extent to which they seem to be relevant in practice

25

ReadingsTextbook Watson, D. and Head, A. (2009). Corporate Finance. Principles &

Practice, 5th Ed, FT Prentice Hall, Chapter 9

Research papers Bradley, M., Jarrell, G. A., Kim, E. H. (1984). On the Existence of an

Optimal Capital Structure: Theory and Evidence, Journal of Finance, vol. 39, 3, pp. 857-878

Modigliani, F., Miller, M. (1958). The Cost of Capital, Corporation Finance and the Theory of Investment, American Economic Review, vol. 48, pp. 261-96

Modigliani, F., Miller, M. (1963). Taxes and the Cost of Capital: A Correction, American Economic Review, vol. 53, pp. 433-43

26

Your coursework is due by 9pm on Friday 2nd April

27