capital punishment for bankers? expectations and · pdf filecapital punishment for bankers?...

TRANSCRIPT

Capital punishment for bankers? Expectations and realities Restoring trust in the financial industry, ICMA Asset Management and Investors Council Meeting & Seminar, Zurich, 8 April 2014

Daniel Zuberbühler

Daniel Zuberbühler 1

Overview

1. Introduction 2. Personal sanctions against top bankers

2.1. Switzerland: Report of Parliamentary Oversight Commission on UBS-crisis

2.2 UK Parliamentary Commission on Banking Standards

2.3 Germany: § 54a: Criminal provision in Banking Law

3. Sanctions against banks as enterprises

3.1 Criminal liability of banks

3.2 Monetary sanctions arms race against large financial institutions

4. Prudential alternatives to personal or monetary sanctions 4.1 Much more common equity / capital punishment

4.2 Organisational simplification / reduction of complexity

Daniel Zuberbühler 2

1. Introduction

Disclaimer: no death penalty for bankers • Fall-back into dark middle ages

• Own goal for supervisors: search for culprits will extend to them

• Financial crisis: nobody looks good ! restraint in judgement

Call for sanctions understandable after mega-crisis • Hold culprits accountable ! enhance responsibility of successors

• Bankers are ideal targets, because overpaid and discredited • „Paid too much for doing the wrong things“

• General loss of trust in banks as consequence of crisis • But hypocritical reproach of criminal behaviour in Switzerland for

business-model with foreign tax evaders

23.03.14 23:19Occupy_Wall_Street_March_2012_foreclosure_banner.jpg 800×531 Pixel

Seite 1 von 1http://medien.neopresse.com/Occupy_Wall_Street_March_2012_foreclosure_banner.jpg

Daniel Zuberbühler 4

2. Personal sanctions against top bankers

„Voluntary“ resignations of top managers & board members after mega-losses or even state bail-out • Market pressure (shareholders / customer reactions)

• Call for resignation by media and politicians • Hint from supervisory authority, without formal enforcement • Take-over by other bank

Only lower employees formally dismissed or criminally prosecuted ! unsatisfactory and unjust

Politicians try to hold top bankers accountable for past or at least future failures

Daniel Zuberbühler 6

2.1 Switzerland: GPK-Report on UBS, 30.5.10

Parliamentary oversight on Government and Administration: only behaviour of federal authorities examined • Motions and recommendations primarily addressed to authorities

• FINMA: what did UBS top management know about QIA-violations? • Industry ban (FINMAG 33) for departed execs.: no retro-activity

Recommendation 19: „GPK holds UBS accountable“ • Independent expert group should examine bank-internal handling by

BoD, GEB and audit firm, in particular • Opportunity of criminal procedures / civil-law actions

• Relief from liability for crisis years by General Assembly

• Severance payments for upper and middle management

• Transparency on dispensation with criminal & civil-law actions against former UBS-Management ! UBS transparency report of 14.10.10

Daniel Zuberbühler 7

Expert opinion by Tobias Straumann: The UBS Crisis in Historical Perspective, 28.9.2010

UBS top managers were no gamblers, but in their self-perception (and external assessments) risk-avers and rather conservatively prudent, but without sense for hidden risks, sound distrust, independent judgement, strong leadership

In historic comparison UBS did not commit unusual mistakes • Subprime: Whenever financial bubbles rise, many market participants are

tempted into ignoring time-honoured banking rules

• US x-border WM: To be expected that Swiss banks would experience difficulties to adapt their traditional wealth management to a dramatically tightened regulatory environment. UBS acted only with particular carelessness, but not fundamentally differently than the other banks

Fundamental question: Future positioning of UBS & CS? Binary choice between internationally oriented business model or retreat into the “Reduit” / Illusion: optimised regulation & supervision

Daniel Zuberbühler 8

Tougher sanctions for managers of banks with formal or factual, implicit state guaranty?

Cantonal bank executives: no personal moral hazard • Tax payers react particularly sensitively & resentfully • Against life experience that managers & politicians would

consciously expose themselves to such a purgatory

Large bank executives do not want a state bail-out • Ideological horror to be nationalised and subject to state

interference with business orientation & salaries ! death penalty • Social contempt dissuasive

Wrong incentive from expectation of customers, counter-parties, shareholders in state safety net! low risk premium • Running systemic risks with minimal capital ! Root treatment:

more capital, resolvability, loss sharing of shareholders and creditors (bail-in)

Daniel Zuberbühler 9

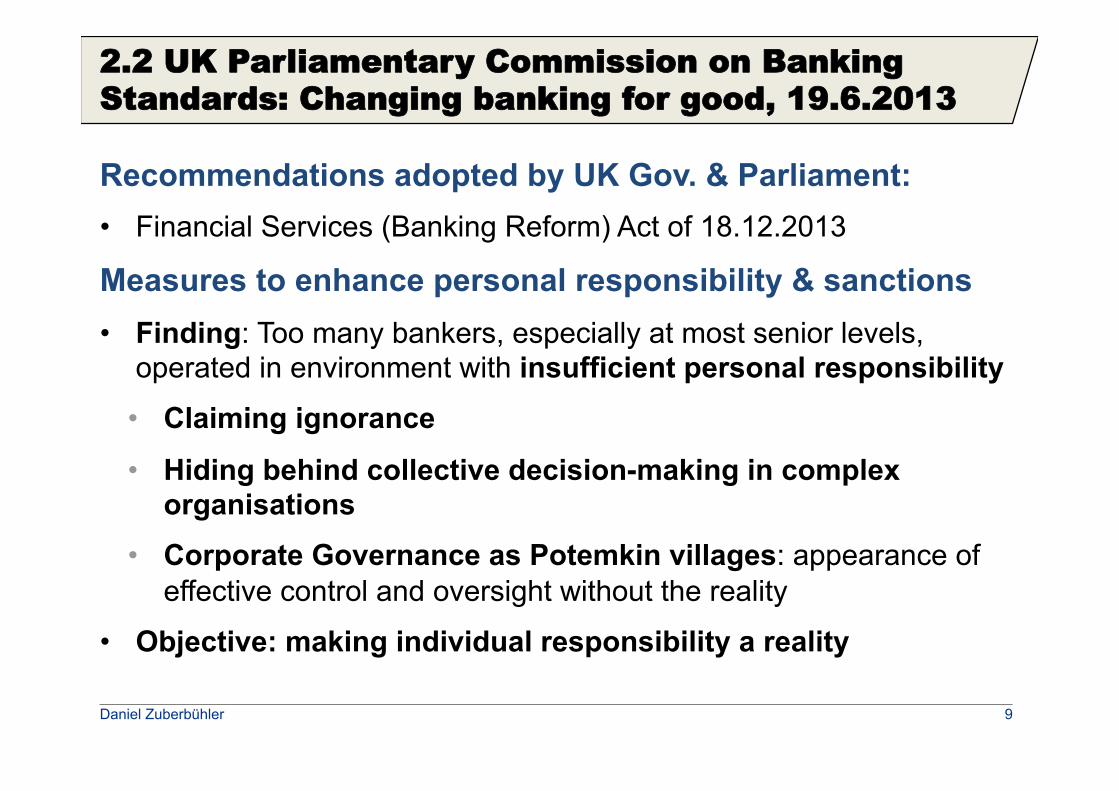

2.2 UK Parliamentary Commission on Banking Standards: Changing banking for good, 19.6.2013

Recommendations adopted by UK Gov. & Parliament: • Financial Services (Banking Reform) Act of 18.12.2013

Measures to enhance personal responsibility & sanctions • Finding: Too many bankers, especially at most senior levels,

operated in environment with insufficient personal responsibility • Claiming ignorance

• Hiding behind collective decision-making in complex organisations

• Corporate Governance as Potemkin villages: appearance of effective control and oversight without the reality

• Objective: making individual responsibility a reality

Daniel Zuberbühler 10

UK: Senior Persons regime for top bankers

All key responsibilities assigned to a specific, senior individual • Senior Persons: BoD, GEB and some other key functions

• Detailed job description • Handover certificate when relinquishing position: outline how

responsibilities were exercised and highlight critical issues for successor

• Responsibility remains with designated individual, even when delegated or subject to collective decision-making

• Burden of proof reversed for supervisory sanctions: • After successful enforcement against bank: Senior Persons must

demonstrate, that they took all reasonable steps to prevent / mitigate failing

• Reckless misconduct: entire remuneration recoverable

Doubts about fairness of formalised responsibility / bureaucracy

Daniel Zuberbühler 11

Scapegoat idea rejected by EBK before crisis 16.02.14 16:44Bock.jpg 450×360 Pixel

Seite 1 von 1http://4.bp.blogspot.com/-6PEBrVvHWrg/Ufqasu356QI/AAAAAAAAAZQ/Q7beW5FcCwg/s1600/Bock.jpg

Designate a senior for compliance • Resignation in case of violation " Sacrifice financially cushioned " After every accident new sacrificial

lamb on ejector seat # Unsustainable & unfair

Daniel Zuberbühler 12

UK: Licensing regime for other bank employees with potential for serious harm

Objective: facilitate enforcement also against lower sinners • Licensed Persons: bankers, whose behaviour could seriously

harm the bank, its reputation or its customers

• Contractual obligation to set of Banking Standards Rules • Bank responsible for instruction and disciplinary actions

• No prior examination / approval by supervisors ! Bank responsible alone

Single public register for Senior & Licensed Persons • Swiss FIDLEG-project: professional skills examinations & duty to

register for all client advisors in financial sector ! bureaucracy

Daniel Zuberbühler 13

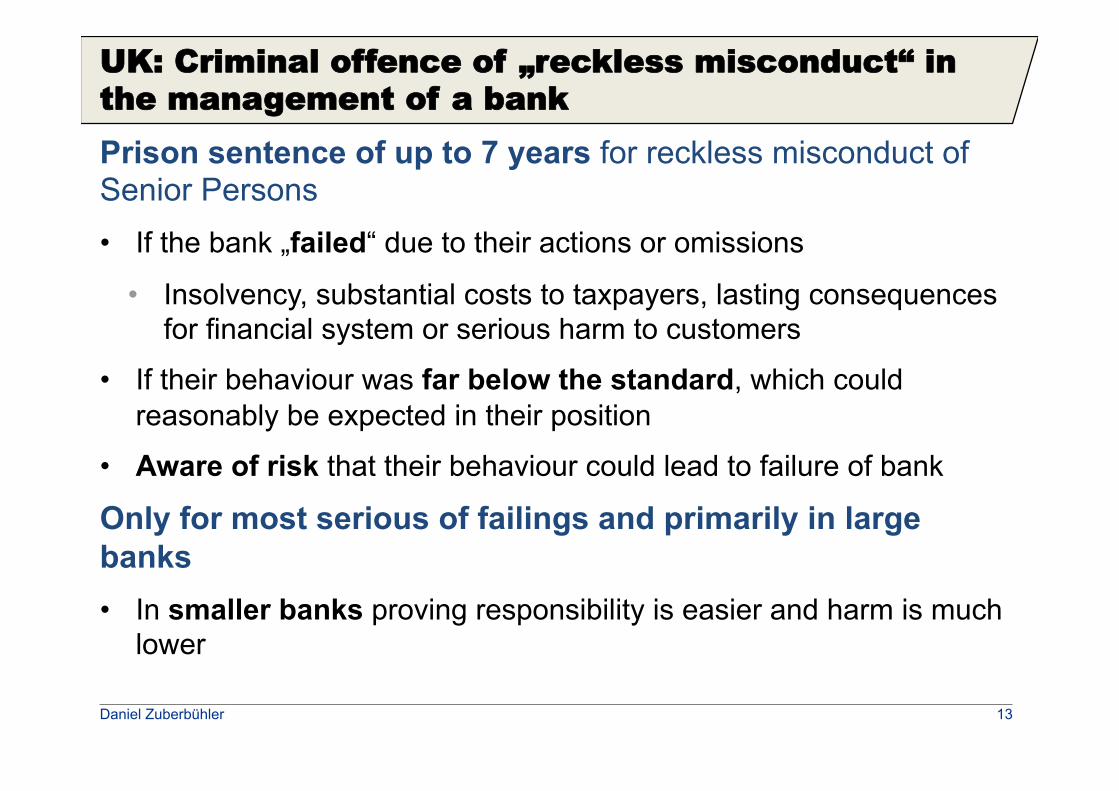

UK: Criminal offence of „reckless misconduct“ in the management of a bank Prison sentence of up to 7 years for reckless misconduct of Senior Persons • If the bank „failed“ due to their actions or omissions

• Insolvency, substantial costs to taxpayers, lasting consequences for financial system or serious harm to customers

• If their behaviour was far below the standard, which could reasonably be expected in their position

• Aware of risk that their behaviour could lead to failure of bank

Only for most serious of failings and primarily in large banks • In smaller banks proving responsibility is easier and harm is much

lower

Daniel Zuberbühler 14

UK: Remuneration for Senior & Licensed Persons: Incentives for better behaviour

Remuneration Code: longer run balance of risks / rewards $ • Deferred compensation: much higher proportion and for much

longer periods of up to 10 years

• Favour long-term performance and soundness of firm ! bail-in bonds / CoCos

• No reliance on narrow measures for profitability: ! RoE • Cancellation of deferred remuneration in light of individual or

wider misconduct or downturn in performance of bank or business area

• Direct taxpayer support: cancellation of deferred remuneration, unvested pension rights and severance payments

• ≈ Lex UBS (Art. 10a BankL): Prohibition of variable compensation / adaptation of remuneration system ! contractual provision

Daniel Zuberbühler 15

2.3 Germany: § 54a criminal offence in Kreditwesengesetz

§ 25c Abs. 4a KWG: Risk management duties of bank executives as part of adequate organisation §54a KWG: Prison sentence of up to 5 years for top managers

• Violation of risk management duties

• Threat to existence for bank or banking group

• Only punishable in case of prior BaFin order to remediate violation and if such an enforceable order is disregarded

• Criticism by German lawyers: against principle of clarity and segregation of powers if BaFin determines punishability

Problem: BaFin-order only feasible, if failings in RM detected • Supervisors did not see risk management failings prior to crisis (incl. UBS)

• More appropriate: order remediation under threat of withdrawal of license / removal of delinquent managers

Daniel Zuberbühler 16

3. Sanctions against banks as enterprises 3.1 Criminal law

Swiss corporate criminal liability (102 StGB): symbolic instead of practical ! at least no overkill More worrying: US criminal indictments against enterprises life-threatening. Reason for • FINMA-rescue of UBS on18.2.09: customer-data passed to DoJ

• US Tax Program of DoJ for other Swiss banks

• Wegelin case: gave up banking activity before court decision, because it would have run out of steam

• Arthur Andersen: acquitted 3 years after indictment

US criminal threat very efficient, but disproportionate and legally highly questionable weapon: death by starvation

18.02.14 01:33I-want-your-money.jpg 1'199×1'608 Pixel

Seite 1 von 1http://www.kjfinancialonline.com/blog/wp-content/uploads/2013/04/I-want-your-money.jpg

18.02.14 01:41The-Drone-Wars-Logo-220.gif 220×220 Pixel

Seite 1 von 1http://3.bp.blogspot.com/-z5tgxB9k5G4/UsvNYqOrsQI/AAAAAAAAAXc/wfBtDwpBB_4/s1600/The-Drone-Wars-Logo-220.gif

Daniel Zuberbühler 18

3.2 Monetary sanctions arms race against large financial institutions – without formal indictment 1

Multi-billion fines against banks for sins committed before or during the financial crisis: • End phase of crisis management: a posteriori redistribution of

crisis-losses from state or investors to banks, combined with civil-law actions for damages

• Crisis winners subsequently become losers:

• Sale of toxic subprime papers and avoiding losses on trading assets before market collapse ! Accusation of defrauding „ignorant“ market participants

• Paying also for sins of insolvent banks taken over at crisis peak

• Fannie Mae & Freddy Mac: Federal Housing Finance Agency sues 18 banks for 200 bn. USD for losses of mortgage GSEs; crisis victim UBS pays 885 m. USD; Credit Suisse pays same amount.

Daniel Zuberbühler 19

3.2 Monetary sanctions arms race against large financial institutions for compliance violations 2

Billions in fines, disgorgements of profits, indemnifications, not only for subprime mortgage securitisations • OFAC sanctions, corruption, money laundering, competition law,

distribution of useless products, rigging of interest rates (LIBOR etc.) and soon also rigging of forex prices

• J.P. Morgan in 2013 paid total of 22 bn. USD for settlement of law suites, but still made a net profit of 18 bn. USD

• of which 920 m. USD to UK and US authorities for control deficiencies in risky derivatives trades of „Whale of London“ with loss of 6.2 bn. USD

• UBS paid for LIBOR-scandal total of 1.4 bn. CHF to US, UK and CH authorities, of which1.2 bn. USD to US authorities; escaped fine of 2.5 bn. € for EU competition law only due to whistleblower rule

• EU Commission in Libor case fined 8 banks with 1.7 bn. € for competition law violations, of which Deutsche Bank with 725 m. €

Daniel Zuberbühler 21

3.2 Monetary sanctions arms race against large financial institutions – process and motives 3

Arms race of supervisors and prosecutors for ever higher monetary sanctions by settlement • Internationally coordinated process: alignment of investigations

and communication of closure of procedure, but • overlapping material & geographic competences lead to

cumulative punishment, esp. in competition among many US authorities ! mark turf & secure part of prey within pack

Motives for arms race • Stated objective: punishment and deterrence against future

misconduct / monetary incentive for preventive measures of top management (get the attention from boards and CEOs)

• Public expectation: „Main Street vs. Wall Street“

Daniel Zuberbühler 22

3.2 Monetary sanctions arms race against large financial institutions – motives of authorities 4

Headline-grabbing fines: WIN-WIN for authorities • Reputation as tough supervisor ! compensate reproach of

earlier laxity or regulatory capture • Promote career of senior officials and prosecutors if

• politically appointed or aspiring for private sector (revolving door)

• Contribution to empty state coffers • Settlement limits burden and procedural risks for

understaffed authorities; no cumbersome search for individual culprits

• Settlement avoids overkill of criminal indictment " But: egoistic motives undermine moral justification

Daniel Zuberbühler 23

3.2 Monetary sanctions arms race against large financial institutions – doubts on efficacy 5

Focus on enterprise weakens individual responsibility • Resolving legacy: convenient for actual management ! blame

predecessors; lessons learned, but if repeated • Suspicion: today‘s ordinary profits will become legacy

tomorrow ! Successors will also exclude them as extraordinary losses / special factors; „adjusted“ results = whitewashing ! Operational risks from breaches of rules & exorbitant sanctions become normality (cost of doing business)

• Justification of bonuses by blending out sanctions as extraordinary factors, even in case of accounting net loss

• Tax deduction as commercially justified expenditure: for fines controversial, but admitted for settlement without admission of guilt

• US excesses at cost of Swiss taxpayers; in addition no corporate income tax paid due to deferred tax assets from crisis losses

Daniel Zuberbühler 24

3.2 Monetary sanctions arms race against large financial institutions – doubts on efficacy 6

• Dose of fines must be increased constantly to achieve effect on firms and public ≈ drug consumption

• Costs borne by shareholders: • Unjust against passive investors without influence on behaviour • Against prudential interest in strong capitalisation to withdraw own

funds from bank or make its shares unattractive investment

Gross violation of proportionality • Guiding principle for sanctions: violations should not pay !

Orientation on realised profit + some risk of loss + costs of procedure and defence + remediation program

• Fines far above: mostly low-profitability activities • Positive example: FINMA disgorgement of profits in UBS-LIBOR

% No competence for FINMA to impose heavy monetary sanctions

Daniel Zuberbühler 25

4. Prudential alternatives to individual or monetary sanctions

No need for tougher sanctions for small / medium-sized banks or lower employees in large banks • Discussion rightly focussed on large, complex and mostly

internationally active banks and their top managers Approaches discussed either ineffectual, bureaucratically burdensome, unjust, legally questionable or simply disproportionate More realistic approach: preventive prudential measures to ensure that 1. Large losses can be absorbed by banks without endangering

creditors or the financial system, and 2. Risk of severe mistakes is reduced by simplifying complex

organisations

Daniel Zuberbühler 26

4.1 Much more CET1 & Capital Punishment instead of fines

Doubling Leverage Ratio to at least 7- 8% of total exposure, with hard common equity ! Review of Swiss Too big to fail-regime in spring 2015 Capital Punishment instead of fines • Supervisory capital surcharge for losses and severe compliance

failures ! Instead of weakening bank by withdrawal of funds , strengthen loss absorption capacity by increasing capital or reducing risky activities

• No penalty or guilt issue: factual proof that bank does not master its risks ! need for higher safety cushion

• FINMA version: capital surcharge of 50% for operational risks from legal and compliance issues of UBS ! correction of inadequate internal model (AMA) = close combat against galloping consumption of risk-weighted assets from internal models

cutting through complexity

Daniel Zuberbühler 28

4.2 Organisational simplification / reduction of complexity

No „culprits“ for failures found among top managers ! complex behemoths no longer manageable or controllable • Too large and complex to be managed by group executive board, to be

overviewed by BoD and to be supervised by regulators • Instead of formalistic or causal-like liability, organisational simplification

and compartmentalisation of group structures • Improved resolvability of G-SIBs requires preventive structural

interventions: ring-fencing systemic functions from risky trading of investment banks; prohibition of proprietary trading (Volcker rule); subsidiarisation of local units by host countries

• Side benefit: business areas and legal entities better overlooked and easier manageable & controllable; investment bank reined in by Basel III and requirement for auto-financing

• Ring-fencing doctrine maybe only temporary fashion ! If experiment fails ! More radical conclusion: break up because simply too big ! hence trial and error in financial market regulation

18.02.14 23:23www_segal_loewe-pferd_b600.jpg 600×384 Pixel

Seite 1 von 1http://www.vsak.ch/members/segal/images/www_segal_loewe-pferd_b600.jpg

18.02.14 23:29tbs-header-image.jpg 990×263 Pixel

Seite 1 von 1http://www.bueso.de/files/images/2013/tbs-header-image.jpg

23.03.14 23:50breakup.jpg 2'918×2'048 Pixel

Seite 1 von 1http://www.addictinginfo.org/wp-content/uploads/2011/11/breakup.jpg

Daniel Zuberbühler Sonnenbergstrasse 3 3013 Berne Switzerland Mobile: +41 78 710 48 74 [email protected]

Full version in German: Banker an den Galgen? Erwartungen und Realitäten, in Jusletter 24. März 2014, http://jusletter.weblaw.ch/_750?current=1