capital debt affordability committee - conduit street · capital debt affordability committee ......

TRANSCRIPT

Capital Debt Affordability Committee Treasurer Nancy K. Kopp, Chair

Louis L. Goldstein Treasury Building 80 Calvert Street, Assembly Room

Annapolis, MD 21401

Agenda

September 2, 2015 2:00 PM

1) Treasurer’s Opening Comments

2) 2015 Legislative Session General Assembly Actions

Department of Legislative Services: Patrick Frank, Manager – 2015 Legislative Session

3) Review of the Size and Condition of Tax Supported Debt: Summary of fiscal year 2015 bond issuances Amount issued in prior five fiscal years Amount outstanding Amount authorized but unissued Current projections for new issuances Debt service projections Status of refunding potential

A) General Obligation Bonds

State Treasurer’s Office: Nikki Griffith, Deputy Director of Debt Management

B) Capital Leases State Treasurer’s Office: Calvin Harding, Lease Administrator

C) GARVEE Bonds Maryland Transportation Authority: Alison Williams, Debt Management Director

D) Maryland Stadium Authority Maryland Stadium Authority: David Raith, Chief Financial Officer

E) Bay Restoration Bonds Maryland Water Quality Financing Administration: Jag Khuman, Director

F) Consolidated Transportation Bonds Maryland Department of Transportation, Office of Finance: David Fleming, Chief Financial Officer

4) Status of Affordability Ratios State Treasurer’s Office: Nikki Griffith, Deputy Director of Debt Management

2015 Legislative Session General Assembly Action

2015 Legislative Session General Assembly Highlights Bonds Authorized by the General Assembly • New General Obligation (GO) Bond Debt Authorized Totals $1,045 Million: The

Capital Debt Affordability Committee (CDAC) limits GO bond debt service to 8% of State revenues and debt outstanding to 4% of revenues. In recent years, debt service expenditures have approached the limit. To keep within the limit, the State may need to adjust GO bond authorizations if the Board of Revenue Estimates (BRE) adjusts out-year revenues downward. Actions taken in the last year reflect this dynamic:

o In October 2014, CDAC recommended limiting GO bond authorizations to

$1,170 million;

o In December 2014, BRE reduced its fiscal 2015 to 2020 revenue estimates. In response, the Spending Affordability Committee (SAC) reduced the debt limit to $1,095 million;

o The State Treasurer estimated that authorizations should not exceed $1,045

million;

o The administration introduced a capital budget totaling just under $995 million; and

o The capital budget bill (House Bill 71/Chapter 495) authorizes $1,045 million in

net GO debt, $1,064 million in new GO debt offset by deauthorizing $19 million in previously authorized GO debt.

• Qualified Zone Academy Bonds (QZABs): House Bill 110 (Chapter 401) authorizes

$4.6 million in QZABs. This is the federal allocation that must be issued by the end of calendar 2015. QZABs support the Aging Schools Program.

• New Academic Revenue Debt Authorization Totals $54.5 Million: CDAC and SAC

recommended that academic revenue bond debt issued in fiscal 2014 be limited to $34.5 million.1 In House Bill 1182 (Chapter 471), the General Assembly increased the authorization by $20.0 million to support a new bioengineering building at the University of Maryland, College Park. The project is also supported by $20.0 million in private donations and $1.9 million in institutional funds. The legislation includes the

1 This $34.5 million provides $17.0 million for facilities renewal projects budgeted within the USM system office; $12.5 million for the New Academic Commons building at Salisbury University; and $5.0 million for campus-wide building system and infrastructure improvements at the University of Maryland, College Park (UMCP).

Department of Legislative Services

2

legislature’s intent that the planned fiscal 2017 and 2018 authorizations be reduced by $10.0 million each, to reflect that the funds are provided in fiscal 2016.

Uses of Bond Authorizations • GO Bonds Support Program Open Space to Mitigate Programmatic Effects of

Depositing Transfer Tax Revenues in the General Fund: Transfer tax revenues support the State’s land conservation programs. The Budget Reconciliation and Financing Act (BRFA) of 2013 (Chapter 425) authorized the transfer of $77.7 million in transfer tax revenues to the general fund in fiscal 2016. In addition, the administration’s BRFA of 2015 (Chapter 489) increased the amount of this transfer by $37.7 million in transfer tax revenues into the general fund for a total of $115.4 million. As enacted, the budget provides $87.2 million for land conservation programs. This includes $38.9 million in GO bonds and $43.4 million in bond sale premiums (details are discussed in the next bullet). Though substantial, this amount is less than the $115.4 million in lost transfer tax revenues.

• Bond Premiums to Support Capital Projects: Since 2001, the State has been generating

substantial bond sale premiums with each GO bond sale to institutional investors. These surplus proceeds are attributable to market conditions. Section 8-132 of the State Finance and Procurement Article require that any premium remaining (after the expenses of the bond sale are paid) is deposited into the Annuity Bond Fund (ABF). The capital budget authorized $48.4 million fiscal 2015 and 2016 bond sale premiums for additional capital projects;2 $18.4 million from the March 2015 bond sale and $30.0 million from July 2015 bond sale. The July bond sale generated a $43.7 million premium, of which $30.0 million supports capital projects and the remaining $13.7 million is deposited into the ABF to support GO bond debt service costs.

Watershed Implementation Plan Is Not Recognized by Spending Plans • Watershed Implementation Plan: The Transportation Infrastructure Investment Act of

2013 (Chapter 429) requires the Governor to include a total of $395 million in the fiscal 2015 to 2019 operating budgets or Capital Improvement Program (CIP) to support the State Highway Administration’s efforts to comply with the Watershed Implementation Plan. In the fiscal 2016 capital budget, the administration included $65 million in GO bonds. The legislation requires an additional $85 million in fiscal 2017, $100 million in fiscal 2018, and $100 million in fiscal 2019. The General Assembly adopted committee narrative expressing the intent that GO bonds or unbudgeted bond premium revenues be used to satisfy the funding commitment for these watershed implementation projects.

2 Projects funded are $21.6 million for State Program Open Space, $0.4 million for local Program Open Space, $9.4 million for the Rural Legacy Program, and $17.0 million for the Maryland Agricultural Land Preservation Program.

Department of Legislative Services

3

The administration does not include fiscal 2017 to 2019 funding for the project in the operating budget forecast, Capital Improvement Plan, or Transportation Trust Fund.

General Obligation Bonds

1

2015 Update on

Maryland General Obligation Bonds

for the

Capital Debt Affordability Committee

September 2, 2015

2

Topics of Discussion

1) FY 2015 and 2016 YTD General Obligation (GO) Bond Issuances

2) Amount of GO Bonds Issued in Prior Five Fiscal Years

3) Outstanding GO Debt and Amounts Authorized but Unissued

4) Current Projections for Future Issuances

5) Summary of Projected Debt Activity

6) Status of Refunding Potential 7) Use of Variable Rate Debt, Derivatives and GICS

3

Fiscal Year 2015 GO Bond Issuances

Series Dates of Sales

($ in millions)

Overall True Interest Cost

(TIC) Tax-Exempt: New Money Competitive

Tax-Exempt: New Money Negotiated

Tax-Exempt: Refunding

Competitive Taxable

Taxable: Federal Tax

Credit

2014 Second Series A 8/5/14 $50.4

2.58% 2014 Second

Series B 8/5/14 $449.6

2014 Second Series C 8/5/14 $649.7 1.88%

2014 QZAB 12/18/14 $4.6 0.00%(a)

2015 First Series A 3/17/15 $518.0 2.64%

2015 First Series B 3/17/15 $365.4 2.14%

Fiscal Year 2015 General Obligation Bond Issues Totaled $2.04 Billion

(a) The 2014 Qualified Zone Academy Bonds (QZABs) are special, federally-authorized taxable bonds where the bondholders receive federal tax credits in lieu of interest payments.

4

Fiscal Year 2016 Year To Date GO Bond Issuances

Series Dates of Sales

($ in millions)

Overall True Interest Cost

(TIC) Tax-Exempt: New Money Competitive

Tax-Exempt: New Money Negotiated

Tax-Exempt: Refunding

Competitive Taxable

Taxable: Federal Tax

Credit

2015 Second Series A 8/3/15 $450.0 2.83%

1.35% 2015 Second Series B 8/3/15 $50.0

Fiscal Year 2016 YTD General Obligation Bond Sales Total $500 Million

5

GO Bonds Issued in Prior Five Fiscal Years (2011 – 2016 YTD)

$6.65 billion in General Obligation Bonds issued since July 1, 2011:

$6.39 billion in tax-exempt bonds (decrease of $943 million from previous 5 years) • $4.40 billion in tax-exempt, new money bonds (69%) • $2.0 billion in tax-exempt, refunding bonds (31%)

$260.3 million in taxable bonds (decrease of $584 million from previous 5 years)

• $213.4 million in taxable bonds (82%) • $46.9 million in special taxable Federal subsidy bonds (18%)

• $40.4 million in taxable, direct subsidy Qualified Zone Academy Bonds (QZABs), last issuance in FY 2015

• $6.5 million in taxable, direct subsidy Qualified Energy Conservation Bonds (QECBs), last issuance in FY 2012

6

Outstanding GO Debt and Amounts Authorized but Unissued

General obligation debt outstanding:

• $8.82 billion was outstanding as of August 3, 2015, the most recent general obligation bond sale

• $8.68 billion was outstanding as of June 30, 2015 • Since June 30, 2015:

• $500 million issued • $358 million retired

$2.06 billion of general obligation debt was authorized but unissued as of

August 3, 2015 (which includes the FY 2016 authorization amount of $1.05 billion).

Current Projections for Future Issuances – October 2014 CDAC Report

For planning purposes only, the Committee in October 2014 recommended a $75 million increase in GO Bond authorizations for FY 2017 – 2020. The following authorizations and issuances incorporate those increases:

7

Fiscal Year Authorizations Issuances 2016 $1,170 $1,056 2017 $1,180 $1,125 2018 $1,275 $1,193 2019 $1,315 $1,239 2020 $1,355 $1,285

Events Following the October 2014 CDAC Report

At the December 2014 meeting, the Board of Revenue Estimates voted to reduce FY 2015 and FY 2016 revenue estimates.

In response, STO re-analyzed the debt affordability ratios. The Treasurer sent a letter to the Governor and General Assembly, which was

shared with the CDAC members. The letter noted that the original authorization would now exceed the 8.0% debt service to revenue guideline and that to remain within the guidelines, the FY 2016 authorization would have to be limited to $1,045 million.

The Spending Affordability Committee recommended an authorization amount of $1,095 million.

The Governor’s Proposed Capital Budget included a $995 million GO authorization for FY 2016.

The final authorization amount for FY 2016 approved in the 2015 Legislative Session was $1,045 million. 8

Current Projections for Future Issuances – Following 2015 Legislative Session

The $1,045 million authorization amount for FY 2016 was reduced from the CDAC recommended amount, therefore reducing planned issuance in out years. The table below still includes an additional $75 million in FY 2017 – FY 2020 for planning purposes.

9

Fiscal Year Authorizations Issuances 2016 $1,045 $1,018 $500 issued 8/3 2017 $1,180 $1,094 ($ in millions) 2018 $1,275 $1,168 2019 $1,315 $1,221 2020 $1,355 $1,274

Annual authorizations are expected to be issued over a 5 year period, based on historical patterns.

Current Projections for Future Issuances – CDAC Baseline

The table below does not include an additional $75 million in FY 2017 – FY 2020, rather it is based on the CDAC baseline authorization (3% annual growth rate) for planning purposes.

10

Based on the December 2014 assumptions, these authorization levels would result in adherence to the affordability benchmarks.

Fiscal Year Authorizations Issuances

2016 $1,045 $1,018 $500 issued 8/3

2017 $1,105 $1,071 ($ in millions)

2018 $1,200 $1,126

2019 $1,240 $1,164

2020 $1,280 $1,206

Annual authorizations are expected to be issued over a 5 year period, based on historical patterns.

Current Projections for Future Issuances – FY 2016 Capital Budget

The table below is based on the projected authorizations in the Governor’s Proposed FY 2016 Capital Budget.

11

Based on the December 2014 assumptions, these authorization levels would result in adherence to the affordability benchmarks.

Fiscal Year Authorizations Issuances

2016 $1,045 $1,018 $500 issued 8/3

2017 $1,029 $1,047 ($ in millions)

2018 $1,059 $1,063

2019 $1,073 $1,061

2020 $1,025 $1,045

Annual authorizations are expected to be issued over a 5 year period, based on historical patterns.

Fiscal Year

Debt Outstanding Start of Year

New Issues Redeemed

Debt Outstanding End of Year Debt Service

2016 $8,677 $1,018 $735 $8,960 $1,121

2017 $8,960 $1,094 $786 $9,268 $1,188

2018 $9,268 $1,168 $836 $9,600 $1,257

2019 $9,600 $1,221 $853 $9,968 $1,295

2020 $9,968 $1,274 $902 $10,331 $1,362

2021 $10,331 $1,307 $918 $10,719 $1,403

2022 $10,719 $1,333 $962 $11,086 $1,468

2023 $11,086 $1,351 $1,013 $11,418 $1,540

2024 $11,418 $1,380 $1,055 $11,743 $1,600

Summary of Projected Debt Activity with additional $75 million

12 Future Issuances assume a 5.0% interest rate. All dollars in millions All debt matures within 15 years and principal payments begin in year 3. Calculations incorporate the August 3, 2015 GO Bond sale.

For planning purposes only, the additional $75 million in GO Bond authorizations for FY 2017 – 2020 are included in the following debt outstanding and debt service projections.

Fiscal Year

Debt Outstanding Start of Year

New Issues Redeemed

Debt Outstanding End of Year Debt Service

2016 $8,677 $1,018 $735 $8,960 $1,121

2017 $8,960 $1,071 $786 $9,245 $1,188

2018 $9,245 $1,126 $836 $9,535 $1,256

2019 $9,535 $1,164 $853 $9,845 $1,291

2020 $9,845 $1,206 $900 $10,142 $1,355

2021 $10,142 $1,255 $915 $10,482 $1,389

2022 $10,482 $1,300 $955 $10,822 $1,449

2023 $10,822 $1,333 $1,002 $11,149 $1,515

2024 $11,149 $1,380 $1,040 $11,489 $1,572

Summary of Projected Debt Activity CDAC Baseline (3% annual growth)

13 Future Issuances assume a 5.0% interest rate. All dollars in millions All debt matures within 15 years and principal payments begin in year 3. Calculations incorporate the August 3, 2015 GO Bond sale.

The following debt outstanding and debt service is projected for GO Bonds, using CDAC baseline assumptions for authorizations.

Fiscal Year

Debt Outstanding Start of Year

New Issues Redeemed

Debt Outstanding End of Year Debt Service

2016 $8,677 $1,018 $735 $8,960 $1,121

2017 $8,960 $1,047 $786 $9,221 $1,188

2018 $9,221 $1,063 $836 $9,449 $1,255

2019 $9,449 $1,061 $853 $9,657 $1,287

2020 $9,657 $1,045 $899 $9,794 $1,344

2021 $9,794 $1,130 $910 $10,014 $1,367

2022 $10,014 $1,211 $944 $10,277 $1,414

2023 $10,277 $1,280 $981 $10,571 $1,467

2024 $10,571 $1,380 $1,011 $10,939 $1,514

Summary of Projected Debt Activity Governor’s Proposed FY 2016 Capital Budget

14 Future Issuances assume a 5.0% interest rate. All dollars in millions All debt matures within 15 years and principal payments begin in year 3. Calculations incorporate the August 3, 2015 GO Bond sale.

The following debt outstanding and debt service is projected for GO Bonds, using the Governor’s Proposed FY16 Capital Budget assumptions for authorizations.

15

Status of Refunding Potential

An analysis is prepared by the State’s financial advisor before each bond sale to determine the financial feasibility of a refunding.

Benchmarks are 3% net present value savings and an Opportunity Cost Index (OCI) which is greater than 70%. The OCI is a measure of the refunding savings in comparison to projected savings in the future.

The two refunding issues in FY 2015 generated $80.1 million in debt service savings on a net present value (NPV) basis.

The State has been aggressive in pursuing refunding savings, resulting in a debt service savings of $138 million over the past five fiscal years to date.

16

Use of Variable Rate Debt, Bond Insurance, Derivatives, and Guaranteed Investment

Contracts (GICS)

The State is authorized to issue variable interest rate bonds in an amount no more than 15% of the outstanding general obligation indebtedness. The State has not issued any variable rate debt as of August 31, 2015 and has not executed any derivatives. The State did not enter into any new GICs related to the issuance of general obligation bonds in FY 2015.

Because of the State’s strong credit profile, perception in the market and maintenance of its AAA credit rating, there has been no need for bond insurance.

Capital Leases

1

An Update of Tax-Supported Leases

for the 2015 Capital Debt Affordability

Committee

2

Topics of Discussion

Status of • Capital Lease Guidelines • Tax-Supported Leases in the CDAC Analysis • Tax-Supported Energy Leases that are included in the CDAC

Analysis • Tax-Supported Energy Leases that are not included in the

CDAC Analysis • Capital Equipment and Energy Lease Activity in Fiscal Year

2015 • Projections of Future Tax-Supported Lease Financings

Capital Lease Guidelines

• STO on behalf of BPW, determines the size, timing, and method to finance capital assets for State agencies and manages the lease procurement and payment of debt service.

• Capital Facility Lease terms range from 15 – 25 years. • Energy Performance Contract (EPC) Leases for energy conservation

projects at State facilities are limited to a 15 year term and require the ESCO to post a bond to guarantee the energy savings.

– DGS in cooperation with STO monitors whether the guarantee continues to cover debt service on an annual basis.

– If the guarantee lapses or falls below the annual debt service amount, the lease is included in tax-supported debt ratios.

• Capital Equipment Lease terms are limited to 3, 5 or 10 years. • Equipment is required to:

– Have a useful life at least as long as the financing term and the cost should be a material amount;

– Be re-possessable and easily identifiable.

3

4

Tax-Supported Leases in the CDAC Analysis

The following table summarizes the current tax-supported leases for FY 2015 included in the 2015 CDAC Affordability Analysis.

*Maryland Stadium Authority reports the Stadium Authority Capital leases in their debt.

FY 2015 Tax-Supported Lease Financings Outstanding

State Agency Equipment and Facilities Financed

Principal Amount

Outstanding as of 6/30/15

Debt Service for FY 2015

State Treasurer’s Office on behalf of State Agencies

Capital Equipment Leases Various communications, computers and other equipment

$12,024,552* $5,173,409*

State Treasurer’s Office on behalf of State Agencies

Energy Performance Projects 4,442,882* 2,991,938*

Department of Transportation Headquarters Office Building 16,690,000 2,792,175 MAA Shuttle Buses - BWI 2,500,000 1,410,800

Department of General Services Hilton Street Facility 670,000 240,924 Prince George’s County Justice Center 16,853,163 1,515,793

Transportation Authority State office parking facility 17,845,000 1,524,255 Lottery Ocean Downs and Perryville 8,555,000 8,679,574 Department of Health and Mental Hygiene

Public Health Lab 158,200,000 13,988,313

Total Tax-Supported Leases $237,780,597 $38,317,181

5

Tax-Supported Energy Leases included in the CDAC Analysis

Energy lease project Debt Service for FY 2015

Debt Outstanding as of 6/30/2015

UMS – Baltimore Campus (UMBC) $643,600 $615,987

DGS - State Office Complex 908,233 1,285,631

DHMH - Rosewood Center 383,326 546,283

DHMH - Rosewood Center 156,934 294,729

St. Mary's College of Maryland 205,295 927,858

Veterans Affairs 56,638 461,491

DHMH – Springfield Hospital 637,912 310,903

Total $2,991,938 $4,442,882

The following table summarizes the current tax-supported Energy leases in the 2015 CDAC Analysis for FY 2015.

6

Tax-Supported Energy Leases that are not included in the CDAC Analysis

The following table summarizes the current tax-supported Energy leases not included in the 2015 CDAC Analysis for FY 2015.

* The listing does not include the Maryland Stadium Authority projects.

Energy lease project * Debt Service for FY 2015 Debt Outstanding as of

6/30/2015

DGS – District Court & Multi – Service Centers

$388,320 $549,837

Maryland School for the Deaf 291,257 412,919

DPSCS – Hagerstown Prison 488,395 1,997,033

DHMH- Deer’s Head Hospital 255,946 928,292

Spring Grove Hospital 1,896,641 12,486,789

Spring Grove Hospital (Modification) 138,649 1,004,452

Department of Agriculture 194,960 1,429,662

DGS - Multi-Service Centers 1,588,714 12,425,270

University of Baltimore 649,125 5,338,303

UMCP 1,836,990 14,806,969

UMCES (Horn Point Lab) 148,783 1,190,846

State Police 483,258 3,902,785

Workforce Technology 169,101 1,327,398

DPSCS – Jessup 1,713,906 8,769,717

Maryland Aviation Administration 1,600,404 14,551,728

State Highway Administration 1,828,852 16,974,807

Maryland Transit Administration 493,823 4,583,501

Maryland Port Administration 1,006,742 9,759,979

Total $15,173,866 $112,440,287

7

Capital Equipment and Energy Lease Activity in Fiscal Year 2015

Equipment • Provides financing of capital equipment to state agencies. • Capital Equipment lease contracts financed $3.8 million during Fiscal Year 2015.

Summary of the Lease Terms for Equipment

Financed in Fiscal Year 2015

3-yr leases $1,628,706 5-yr leases 2,172,468

Total $3,801,174

Energy • Provides financing for energy conservation projects for State agencies. • Lease payments are made from the participating agencies’ annual utility appropriations using savings achieved through the

implementation of energy performance contracts. • No Energy lease financings were closed in Fiscal Year 2015.

Summary of the Lease Terms for Energy Projects

Financed in Fiscal Year 2015

Energy lease $0 Total $0

8

Projections of Future Tax-Supported Lease Financings

in the CDAC Analysis

Types of Financing Period CDAC projections as of June 2015* Equipment Leases (1) Fiscal Years 2016 – 2020 (1) $20 million for FY 2016, $10

million for FY 2017, and $5 million in FY 2018 – 2020.

Energy Leases (2) Fiscal Years 2016 - 2020 $13.0 million for FY 2016, $24 million for FY 2017 and $0 through FY 2020.

Other Capital Leases (3) Fiscal Years 2016 - 2020 $33.0 million in FY 2018.

(1) Fiscal Year 2016- 2018 based on agency survey’s received May 2015. (2) DGS estimates that approximately $13.0 million in energy projects will be financed in FY 2016.

Maryland Environmental Services estimates that approximately $24 million in energy projects will be financed in FY 2017. All of the projected Energy Lease financings include projects that will have surety bond guarantees that equal or exceed the debt service payments through out the term of the lease; therefore, these projects are not included in the CDAC Affordability Analysis.

(3) MDOT and MEDCO expect to issue $33 million in Lease Revenue bonds for the State Center parking garage in FY 2018.

* Preliminary, subject to change.

GARVEE Bonds

1

Grant Anticipation Revenue Vehicles (“GARVEE”) Bonds

Purpose

Grant Anticipation Revenue Vehicles (“GARVEE”) Bonds are authorized by State statute

to leverage federal aid to finance the cost of transportation facilities. GARVEEs were used as a

part of the funding plan for the Intercounty Connector (“ICC”) project, in addition to various

other debt instruments and cash. The use of GARVEEs for the ICC allowed the project to be

constructed sooner than otherwise would have been possible and with less reliance on the State’s

available funds.

Security

GARVEE bonds are secured by a pledge of federal transportation funds received by the

State which approximate $465.8 million annually. In addition, there is a subordinate pledge of

certain State Transportation Trust Fund (“TTF”) tax sources. The GARVEEs were also

structured to include debt service reserve funds for additional security.

Limitations to Debt Issuance

Statute limits the total amount that can be issued for GARVEEs to an aggregate principal

amount of $750.0 million, with a maximum maturity of 12 years. Under State law, the proceeds

could only be used for the ICC. Legislation enacted by the 2005 General Assembly specified that

GARVEE bonds be considered tax-supported debt.

Current Status:

Debt Outstanding as of June 30, 2015: $349,440,000

Ratings

GARVEEs are currently rated AAA by Standard and Poor’s, Aa1 by Moody’s Investors

Service and AA by Fitch Ratings.

Use of Variable Rate Debt, Bond Insurance, Derivatives and Guaranteed Investment

Contracts

The GARVEE bonds are fixed rate bonds, and were issued without bond insurance due to

the subordinate pledge of the TTF and the availability of debt service reserve funds. The

Authority has not used derivatives or guaranteed investment contracts.

Trends in GARVEE Debt A total of $750.0 million in GARVEE bonds have been issued by the Maryland

Transportation Authority. The first issuance occurred in May 2007 and totaled $325.0 million

with a true interest cost of 3.99%. In December 2008, the Authority sold the remaining $425.0

million of GARVEE bonds with a true interest cost of 4.31%. GARVEE debt outstanding and

required debt service for the past five fiscal years and projections until the debt is repaid are

shown in Graph 4.1. The final GARVEE bond matures on March 1, 2020 and no further

issuances are projected, except in the event of a refunding opportunity.

2

CDAC 2015

MARYLAND TRANSPORATION AUTHORITY Refunding of the Parking Lease Revenue Bonds (Calvert Street

Parking Garage Project) Series 2005

Background The Maryland Transportation Authority (Authority) issued $23,760,000 of Parking Lease Revenue Bonds in July 2005 to finance the construction of the Calvert Street Parking Garage. The Department of General Services (DGS) operates and maintains the garage. In June 2015, Davenport & Company, the Authority’s financial advisory firm, issued a Request for Proposal to determine if a direct bank loan would be the most efficient way to refund the Series 2005 Bonds for debt service savings. A bid by TD Bank, N.A. was deemed to be very competitive and in the best interests of the State. The direct bank loan was done on an expedited basis with lower issuance costs and at a very attractive interest rate. The Refunding Bonds were sold on July 10, 2015, and the Series 2005 Bonds were redeemed on August 17, 2015.

Refunding Results

Refunding Bonds issued on August 5, 2015: $18,011,000 True Interest Cost (TIC): 2.62% Par Amount of Series 2005 Bonds redeemed: $17,845,000 Average Coupon of Series 2005 Bonds: 4.25% NPV Savings: $2.3 Million Percentage Savings: 13% of refunded bonds Final Maturity: July 1, 2032 Pledged Revenue: Rental payments are due from DGS for the use of the garage, which are subject to annual appropriation, and serve as a pass-through to the bond trustee to pay debt service to bondholders. Structure: The Refunding Bonds are fixed rate bonds with serial principal payments, and no credit enhancement or reserve funds due to the State’s excellent credit rating. Ratings: Unrated

Maryland Stadium Authority

Maryland Stadium Authority Briefing

Capital Debt Affordability Committee

September 2, 2015

Maryland Stadium Authority

Debt Issued over the past five years

Fiscal

Year

Amount Purpose

2011 $6,630,000 Refunding of the Ocean City Bonds

2012 $105,450,000 $11.1 million - Revenue Bond for Warehouse and Oriole

Park Improvements

$94.35 million - Series 2011 Refunding Bonds (Terminate

Swap with AIG for Series 1998A and 1999)

2013 $26,990,000 $14.1million – Series 2012 Hippodrome Performing Arts

Center Refunding Bonds

$12.9 million - Series 2012 Montgomery County

Conference Center Refunding Bonds

2014 $8,635,000 Refund the Series 2010 Revenue Bond for Oriole Park

Improvements

2015 $9,535,000 Refund the Series 2011 Revenue Bond for Oriole Park

Improvements, reduce the outstanding balance refunded

by $500,000 by negotiating a lower debt service reserve

Maryland Stadium Authority

Amount of Outstanding Debt and Revenues

Fis

cal

Yea

r

Amount

Outstanding

Tax

Supported

Bonds and

Equipment

Revenue

Bond

Energy

(not tax

supported

debt)

Debt Service

for Tax

Supported

and

Equipment

Revenues

(Lottery/

Camden Yards

Operating

Revenue and $2

ticket charge)

2013 $219,601,249 $193,005,129 $19,435,000 $7,161,120 $34,488,483 $24,602,696

2014 $185,442,082 $168,862,603 $10,010,000 $6,569,479 $32,760,702 $23,440,000

2015 $168,421,865 $145,021,979 $17,455,000 $5,944,886 $31,447,251 $21,851,391

2016 $146,291,738 $125,181,285 $15,825,000 $5,285,453 $26,394,035 $21,837,615

2017 $124,627,623 $105,883,444 $14,155,000 $4,589,179 $25,034,455 $21,893,973

2018 $102,100,220 $85,806,273 $12,440,000 $3,853,947 $24,956,432 $21,817,415

2019 $79,034,063 $65,281,548 $10,675,000 $3,077,515 $24,496,590 $21,359,802

2020 $55,027,509 $43,910,000 $8,860,000 $2,257,509 $24,396,585 $21,258,143

2021 $44,306,417 $35,920,000 $6,995,000 $1,391,417 $10,328,763 $7,193,770

2022 $33,076,576 $27,520,000 $5,080,000 $476,576 $10,342,102 $7,201,477

2023 $23,385,000 $20,275,000 $3,110,000 $0 $8,766,383 $7,211,633

2024 $13,700,000 $12,615,000 $1,085,000 $0 $8,775,074 $7,215,824

2025 $6,080,000 $6,080,000 $0 $0 $7,434,296 $7,434,296

Maryland Stadium Authority

Fixed Rate Debt Ratings

Series S&P Moody’s Fitch

2004 AA+ Aa2 AA

2011 AA+ Aa2 AA

2012 HPAC AA+ Aa2 AA

2012 MCCC AA+ Aa2 AA

Maryland Stadium Authority Maryland Stadium Authority

Summary of Swaps and Variable Rate Demand Bonds

as of June 30, 2015, 2015

Sports Facilities Lease Revenue Refudning Bonds

Football Stadium Issue

Series Name Series 2007

Tax Status Tax-Exempt

Dated Date 2/8/2007

Original Issue Par 73,500,000

Current Outstanding 51,385,000

Maturity 3/1/2008 – 2026

Remarketing Agent Goldman Sachs & Co.

Current Remarketing Rate 5 Basis Points

Liquidity/LOC Provider SBPA: Sumitumo

LOC Expiration 12/15/2019

Current LOC Fee 36 Basis Points

Current Reset Frequency 7-Day

Date of Last Reset 8/19/2014

Reset Rate 0.06%

Hedges Synthetic Fixed Rate (MSA paid Fixed Amounts = 5.69% - 5.8%,

receives SIFMA)

Counterparty Barclays

Maryland Stadium Authority

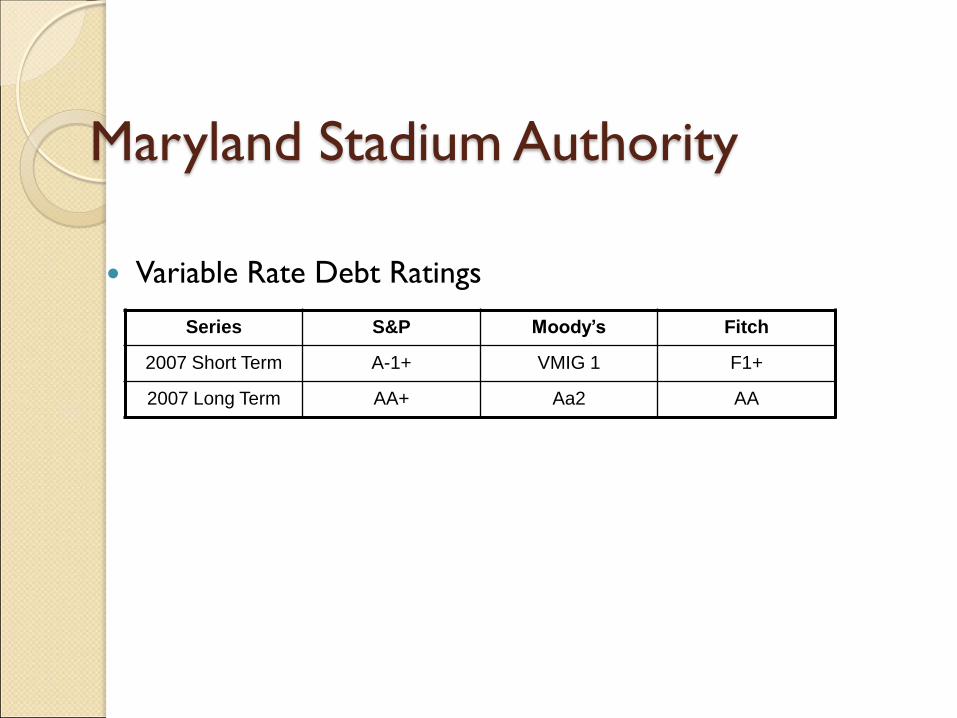

Variable Rate Debt Ratings

Series S&P Moody’s Fitch

2007 Short Term A-1+ VMIG 1 F1+

2007 Long Term AA+ Aa2 AA

Maryland Stadium Authority Current projections for new issuances

◦ FY 2016

Issue $320 million in Baltimore City Public School Revenue Bonds

Proceeds to be used for Year 1 projects

2-3 new schools

5-7 renovated schools

Revenue bond secured by the funds received from:

Lottery

Baltimore City Insurance Subsidy

Baltimore City Bottle Tax, Table Games and Facility Rental

Baltimore City Public Schools

◦ FY 2017

Issue $270 million in Baltimore City Public School Revenue Bonds

Proceeds to be used for the balance of the Year 1 projects ($70 million) and the Architect and Pre-construction of the Year 2 projects ($200 million)

Structured the same way as the first series, unless we don’t receive a AA blended credit

Maryland Stadium Authority

Baltimore City Public Schools Construction and Revitalization Program

Revenue Bond, Series 2015

◦ Financing Plan Approved by MSA board 9/1

◦ Submitted to budget committees for a 45 day review and comment period on or

about 9/2

◦ Presentation for an indicative rating with Moody’s in early September 2015

Seeking a AA credit rating on the blended security of all three (3) revenue

sources

◦ Full rating presentation late September or early October 2015

◦ Board of Public Works approval 10/21

◦ Negotiated sale on or about 11/15 Par Amount of $320 million

Project premium of between $40 million and $50 million

Tax-exempt and CRA

30 year debt

5% coupon

Average annual debt service is $21 million

Bay Restoration Bonds

Department of the Environment

Bay Restoration Fund (BRF) Capital Debt Affordability Committee Briefing

September 2, 2015

Jag Khuman, Director Maryland Water Quality Financing Administration

1800 Washington Boulevard Baltimore, MD 21230

410-537-3119

www.mde.maryland.gov/wqfa

FY Amount ($ Million) Primary Purpose 2008 50.00 Provide grants for the Enhanced 2009 - Nutrient Removal (ENR) 2010 - upgrades at the 67 major Waste 2011 - Water Treatment Plants (Estimated 2012 - Total ENR Capital Cost $1.25 billion) 2013 - 2014 100.00 2015 - Page 2

Bay Restoration Fund

Debt Issued in Prior Fiscal Years

Series 2008 Series 2014 Debt Issued: $50,000,000 $100,000,000 Issue Date: 4/29/2008 5/14/2014 Ratings: Aa2 (Moody’s) Aa2 (Moody’s) AA (S&P) True Interest Cost: 4.03% 2.55% Interest: Fixed Rate Fixed Rate Final Bond Maturity: 3/1/2023 3/1/2029 Security: BRF (WWTP) Fee BRF (WWTP) Fee Debt Service Reserve: None None Optional Redemption: After 3/1/2018 After 3/1/2024 Refunding Potential: Low Savings Low Savings Page 3

Bay Restoration Fund

Existing Bonds/Refunding Potential

BRF Current Outstanding Debt & Annual Debt Service

($ Million)

Page 4

Fiscal Year Ending Outstanding Debt Annual Debt Service

2008 50.000 0.000

2009 46.825 4.655

2010 44.185 4.710

2011 41.560 4.616

2012 38.820 4.614

2013 35.995 4.617

2014 133.055 4.614

2015 129.980 8.248

2016 121.615 14.330

2017 112.880 14.302

2018 103.750 14.261

2019 94.205 14.219

2020 84.110 14.328

2021 73.515 14.330

2022 62.395 14.327

2023 50.725 14.326

2024 43.100 9.717

2025 35.095 9.716

2026 26.770 9.635

2027 18.195 9.469

2028 9.275 9.557

2029 0.000 9.600

2030 0.000 0.000

Debt Authorized through FY 2015: $530,000,000 Debt Issued through FY 2015: $150,000,000 Future Authorized Debt Issuance: $380,000,000 Projected Future Debt Issuance: $280,000,000 Assumptions for future debt issuance

• Wt. Avg. Interest Rate of 4.50% per year • Annual Level Debt Service • Maximum 15-Year Bond Term • Final Debt Service Payment by FY 2030

Page 5

Bay Restoration Fund

Total Debt Authorized and Amount Unissued

Projected Debt Issuance, Debt Service Payments & Annual Revenue ($ Millions)

Page 6

* Actual revenue through FY 2014 BRF fee increase in FY 2013

Fiscal Year New Issues

Debt Outstanding

at 6/30

Debt Service

for FY

Revenue

(Cash) *

2008 50.000 50.000 0.000 55.068

2009 0.000 46.825 4.655 53.356

2010 0.000 44.185 4.710 54.818

2011 0.000 41.560 4.616 54.598

2012 0.000 38.820 4.614 54.552

2013 0.000 35.995 4.617 92.767

2014 100.000 133.055 4.614 108.466

2015 0.000 129.980 8.248 111.785

2016 180.000 ** 301.615 14.330 112.903

2017 100.000 392.880 22.402 114.032

2018 0.000 373.260 37.351 115.172

2019 0.000 346.286 43.776 116.324

2020 0.000 317.978 43.885 117.487

** Bond Sale November 2015

Projected Debt Issuance, Debt Service Payments & Annual Revenue ($ Million)

Fiscal Year New Issues

Debt Outstanding

at 6/30

Debt Service

for FY

Revenue

(Cash) *

2021 0.000 288.350 43.887 118.662

2022 0.000 257.340 43.884 119.849

2023 0.000 224.886 43.883 121.047

2024 0.000 195.541 39.274 122.257

2025 0.000 164.839 39.273 123.480

2026 0.000 132.795 39.192 124.715

2027 0.000 99.434 39.026 125.962

2028 0.000 64.612 39.114 127.222

2029 0.000 28.270 39.157 128.494

2030 0.000 0.000 29.557 129.779

Page 7

Continued….

* Actual revenue through FY 2014 BRF fee increase in FY 2013

Bay Restoration Fund

Page 8

0.000

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$ M

illi

on

FY

New Debt Issuance & Debt Outstanding

New Debt Issuance Debt Outstanding

Consolidated Transportation Bonds

Presented by

David Fleming

Chief Financial Officer

Office of Finance

September 2, 2015

Maryland Department of Transportation

Structure: Fixed rate

Interest only first 2 years

As required by statute Maximum maturity of 15 years

Level debt service payments

Additional Bonds Test: Pledged taxes at least 2.0x maximum annual debt service

Net revenue at least 2.0x maximum annual debt service

-1-

Management Practice: Pledged Taxes at least 2.5x maximum annual Debt Service

Net Revenue at least 2.5x maximum annual Debt Service

Fiscal Year 2014 Actual: Pledged taxes coverage 5.9x Net revenue coverage 3.2x

Fiscal Year 2015 Estimated : Pledged taxes coverage 5.9x Net revenue coverage 3.4x

-2-

Amount issued in prior 5 fiscal years: $1.007 billion new construction $421 million refunding

-3-

Series Sale Date ($ in millions) New Money Refunding

True Interest Cost (TIC)

Series 2015 Second Issue 6/3/2015 $136.00 2.75%

Series 2015 Refunding 6/3/2015 $259.72 1.85%

Series 2015 2/11/2015 $265.54 2.59%

Series 2014 6/11/2014 $100.00 2.66%

Series 2013 Second Issue 11/20/2013 $225.00 2.90%

Series 2013 2/13/2013 $165.00 2.45%

Series 2012 5/23/2012 $115.00 2.36%

Series 2011 Refunding 9/28/2011 $161.44 1.39%

Amount outstanding: FY15 - $2.02 billion Legislative debt ceiling increased to $4.5 billion effective June 1, 2013

Amount authorized but unissued: FY15 - $2.53 billion authorized FY15 - $510 million unissued

Maryland Department of Transportation

Consolidated Transportation Bonds

-4-

Status of refunding potential Refunding analysis is periodically completed by the

department’s financial advisor Benchmarks are 3% net present value savings and an

Opportunity Cost Index of at least 70% Refunded $301 million bonds in June 2015 for a net present

value savings of $21 million

Variable rate debt, swaps and bond insurance None

Bond Insurance Not needed because of MDOT’s stable credit profile

-5-

Preliminary projections for new issuances

Debt Debt

Outstanding Outstanding

at Beginning New at End

Fiscal Year of Year Issues Redeemed of Year

2016E $2,020 $655 $174 $2,501

2017E $2,501 $795 $207 $3,089

2018E $3,089 $675 $222 $3,542

2019E $3,542 $535 $195 $3,882

2020E $3,882 $420 $182 $4,120

2021E $4,120 $410 $235 $4,295

2022E $4,295 $480 $280 $4,495

2023E $4,495 $315 $316 $4,494

2024E $4,494 $300 $299 $4,495

2025E $4,495 $330 $333 $4,492

(E = based on July 2015 Estimate)

-6-

Debt service preliminary projections for the next 10 years

($ in millions)

-7-

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

DS Projected New Issues 6 33 74 114 151 207 268 319 371 421

DS Current Outstanding 258 288 292 243 204 212 206 199 133 119

Total Debt Service 264 321 366 357 355 419 474 518 504 540

0

100

200

300

400

500

600

Rating Agency Updates: As of June 2015

Standard & Poor’s – AAA

Moody’s – Aa1

Fitch – AA+

-8-

Status of Affordability Ratios

1

2015 Preliminary Affordability Analysis for the

Capital Debt Affordability Committee

September 2, 2015

2

Topics of Discussion

1. Authorization and Issuance Assumptions

2. Debt Outstanding Ratios

3. Assumptions

4. Debt Service Ratios

General Obligation Bonds Authorization History

• Last October, the Committee recommended $1,170 million as a prudent authorization amount for FY 2016.

• In December 2014, the Board of Revenue Estimates reduced estimated revenues for FY 2016.

• The Treasurer then sent a letter to the Governor and General Assembly, which was shared with CDAC members, because there wasn’t time for a CDAC meeting before the scheduled SAC meeting. The Treasurer noted that the original authorization would result in exceeding the debt affordability guidelines and that to remain within guidelines the FY 2016 authorization would have to be limited to $1,045 million.

• The Spending Affordability Committee recommended an authorization of $1,095 million.

• The Governor’s Proposed FY 2016 Capital Budget included an authorization of $995 million.

• At the conclusion of the 2015 Legislative Session an authorization of $1,045 million was approved.

3

General Obligation Bonds New Authorization Comparison

• The 2014 CDAC authorization column in the table on page 5 reflects the $75 million increased planning assumption for fiscal years 2017 through 2020 that the committee adopted for its report in October 2014.

• The second column in the table on page 5 represents the CDAC baseline authorizations of 3% annual growth without the $75 million increase in out-year planning.

• The Governor’s Proposed FY 2016 Capital Budget authorization assumptions are shown in the final column in the table on page 5.

4

General Obligation Bonds New Authorization Comparison

($ in millions)

Fiscal Year

CDAC Authorization

With $75 million

CDAC Baseline Authorization

(3% annual growth)

Governor’s Proposed Capital

Budget 2017 1,180 1,105 1,029

2018 1,275 1,200 1,059

2019 1,315 1,240 1,073

2020 1,355 1,280 1,025

2021 1,320 1,320 1,320

2022 1,360 1,360 1,360

2023 1,400 1,400 1,400

2024 1,440 1,440 1,440

2025 1,480 1,480 1,480

5

Tax-Supported Debt Issuance Assumption

6

2014 CDAC with $75 million increase

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

GO $1,018 $1,094 $1,168 $1,221 $1,274

MDOT $655 $795 $675 $535 $420

Bay Bonds $180 $100 $0 $0 $0

Capital Leases $20 $10 $38 $5 $5

Total $1,873 $1,999 $1,881 $1,761 $1,699

The table above reflects the assumed issuances based upon historical issuance patterns, the $1,045 million authorized by the General Assembly for FY 2016 and the additional $75 million authorization the CDAC approved through FY 2020 for planning purposes.

Tax-Supported Debt Issuance Assumption

7

CDAC Baseline (3% annual growth) without additional $75 million

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

GO $1,018 $1,071 $1,126 $1,164 $1,206

MDOT $655 $795 $675 $535 $420

Bay Bonds $180 $100 $0 $0 $0

Capital Leases $20 $10 $38 $5 $5

Total $1,873 $1,976 $1,839 $1,704 $1,631

The table above reflects the assumed issuances based upon historical issuance patterns, the $1,045 million authorized by the General Assembly for FY 2016 and the CDAC baseline of 3% annual growth in authorizations (without additional $75 million for out-year planning).

Tax-Supported Debt Issuance Assumption

8

Governor’s Proposed FY 2016 Capital Budget

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

GO $1,018 $1,047 $1,063 $1,061 $1,045

MDOT $655 $795 $675 $535 $420

Bay Bonds $180 $100 $0 $0 $0

Capital Leases $20 $10 $38 $5 $5

Total $1,873 $1,952 $1,776 $1,601 $1,470

The table above reflects the assumed issuances based upon historical issuance patterns, the $1,045 million authorized by the General Assembly for FY 2016 and the proposed authorizations for FY 2017 – FY 2020 in the Governor’s Proposed FY 2016 Capital Budget.

Preliminary Tax-Supported Debt Outstanding Ratio (2014 CDAC with $75 million)

($ in Millions)

Fiscal Year

Debt Outstanding

Personal Income Ratio (%)

2016 12,399 359,678 3.45% 2017 13,317 376,790 3.53% 2018 13,970 392,982 3.55% 2019 14,530 406,736 3.57% 2020 15,012 420,484 3.57% 2021 15,519 435,621 3.56% 2022 16,030 452,087 3.55% 2023 16,309 469,086 3.48% 2024 16,582 486,724 3.41% 2025 16,804 505,024 3.33% 9

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

Preliminary Tax-Supported Debt Outstanding Ratio (Baseline without $75 million additional increase)

($ in Millions)

Fiscal Year

Debt Outstanding

Personal Income Ratio (%)

2016 12,399 359,678 3.45% 2017 13,294 376,790 3.53% 2018 13,905 392,982 3.54% 2019 14,407 406,736 3.54% 2020 14,823 420,484 3.53% 2021 15,282 435,621 3.51% 2022 15,767 452,087 3.49% 2023 16,039 469,086 3.42% 2024 16,328 486,724 3.35% 2025 16,567 505,024 3.28% 10

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

Preliminary Tax-Supported Debt Outstanding Ratio (Gov. Proposed FY16 CIP)

($ in Millions)

Fiscal Year

Debt Outstanding

Personal Income Ratio (%)

2016 12,399 359,678 3.45% 2017 13,270 376,790 3.52% 2018 13,819 392,982 3.52% 2019 14,219 406,736 3.50% 2020 14,476 420,484 3.44% 2021 14,814 435,621 3.40% 2022 15,221 452,087 3.37% 2023 15,461 469,086 3.30% 2024 15,778 486,724 3.24% 2025 16,053 505,024 3.18% 11

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

12

Tax-Supported Debt Assumptions

General Obligation • Savings: No future refunding issues or use of premium. • Interest Rate: 5.0%

– This assumption is based upon standard municipal bond couponing and the Municipal Market Data (MMD) AAA curve and produces conservative and stable debt service estimates.

– Since FY 1999 the interest rates on State bonds has exceeded 5% only once.

• MDOT Interest Rate: 3.8% in fiscal year 2016; 4.3% in fiscal year 2017; 4.5% in fiscal year 2018 - 2021 and 5.3% in fiscal years 2022 – 2025.

• Bay Bonds Interest Rate: weighted average of 4.5%.

• Capital Lease Interest Rate: from 1.21% to 1.49% with different rates for each expected term.

Preliminary Tax-Supported Debt Service Ratio (2014 CDAC with $75 million)

($ in Millions)

Fiscal Year Debt Service Revenues Ratio (%) 2016 1,549 21,151 7.32% 2017 1,674 22,074 7.59% 2018 1,806 22,807 7.92% 2019 1,841 23,505 7.83% 2020 1,870 24,238 7.71% 2021 1,906 24,575 7.75% 2022 2,024 25,353 7.98% 2023 2,137 26,167 8.17% 2024 2,178 27,000 8.07% 2025 2,259 27,914 8.09%

13

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

These ratios are lower than the Treasurer’s December letter due to lower rates on the 2015 issues and refunding savings.

14

Preliminary Debt Service Ratio 2014 CDAC with $75 million

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

General Obligation Bonds DOT Consolidated Bonds Capital Leases Stadium Authority Bay Restoration Bonds Garvee Bonds Total Tax Supported Debt Service 8.0% Benchmark

15

Preliminary Debt Service Capacity 2014 CDAC with $75 million

250 248 266

224 214

143 92

18 39 69 60 4

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

Total Tax Supported Debt Service Remaining Debt Service Capacity 8.0% Benchmark

Preliminary Tax-Supported Debt Service Ratio (Baseline without increase)

($ in Millions)

Fiscal Year Debt Service Revenues Ratio (%) 2016 1,549 21,151 7.32% 2017 1,675 22,074 7.59% 2018 1,805 22,807 7.91% 2019 1,838 23,506 7.82% 2020 1,862 24,238 7.68% 2021 1,892 24,576 7.70% 2022 2,005 25,354 7.91% 2023 2,112 26,167 8.07% 2024 2,150 27,000 7.96% 2025 2,229 27,914 7.99%

16

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

These ratios are lower than the Treasurer’s December letter due to lower rates on the 2015 issues and refunding savings.

17

Preliminary Debt Service Ratio Baseline Without Increase

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

General Obligation Bonds DOT Consolidated Bonds Capital Leases Stadium Authority Bay Restoration Bonds Garvee Bonds Total Tax Supported Debt Service 8.0% Benchmark

18

Preliminary Debt Service Capacity Baseline Without Increase

250 248 266

224 214

143 92

20 43 77 74 23

10 4

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

Total Tax Supported Debt Service Remaining Debt Service Capacity 8.0% Benchmark

Preliminary Tax-Supported Debt Service Ratio (Governor’s FY16 CIP)

($ in Millions)

Fiscal Year

Debt Service Revenues Ratio (%)

2016 1,549 21,151 7.32% 2017 1,674 22,074 7.59% 2018 1,804 22,807 7.91% 2019 1,834 23,506 7.80% 2020 1,852 24,238 7.64% 2021 1,870 24,576 7.61% 2022 1,970 25,354 7.77% 2023 2,064 26,167 7.89% 2024 2,092 27,000 7.75% 2025 2,167 27,914 7.76% 19

The planning assumptions for authorizations and issuance result in the following projections of tax-supported debt outstanding:

20

Preliminary Debt Service Ratio Governor’s Proposed FY 2016 CIP

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

General Obligation Bonds DOT Consolidated Bonds Capital Leases Stadium Authority Bay Restoration Bonds Garvee Bonds Total Tax Supported Debt Service 8.0% Benchmark

21

Preliminary Debt Service Capacity Governor’s Proposed FY 2016 CIP

250 248 266

224 214

143 92

21 47 87 96 58

29 68 66

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$ in

mill

ions

Total Tax Supported Debt Service Remaining Debt Service Capacity 8.0% Benchmark

CDAC 2015 Recommendation

• At its September 30 meeting, the Capital Debt Affordability Committee will need to vote on a recommended authorization level to support the fiscal year 2017 capital program.

• The committee will also need to adopt planning assumptions for future authorizations. The current CDAC baseline includes an annual 3% growth rate with an additional $75 million in FY 2017 through FY 2020.

22