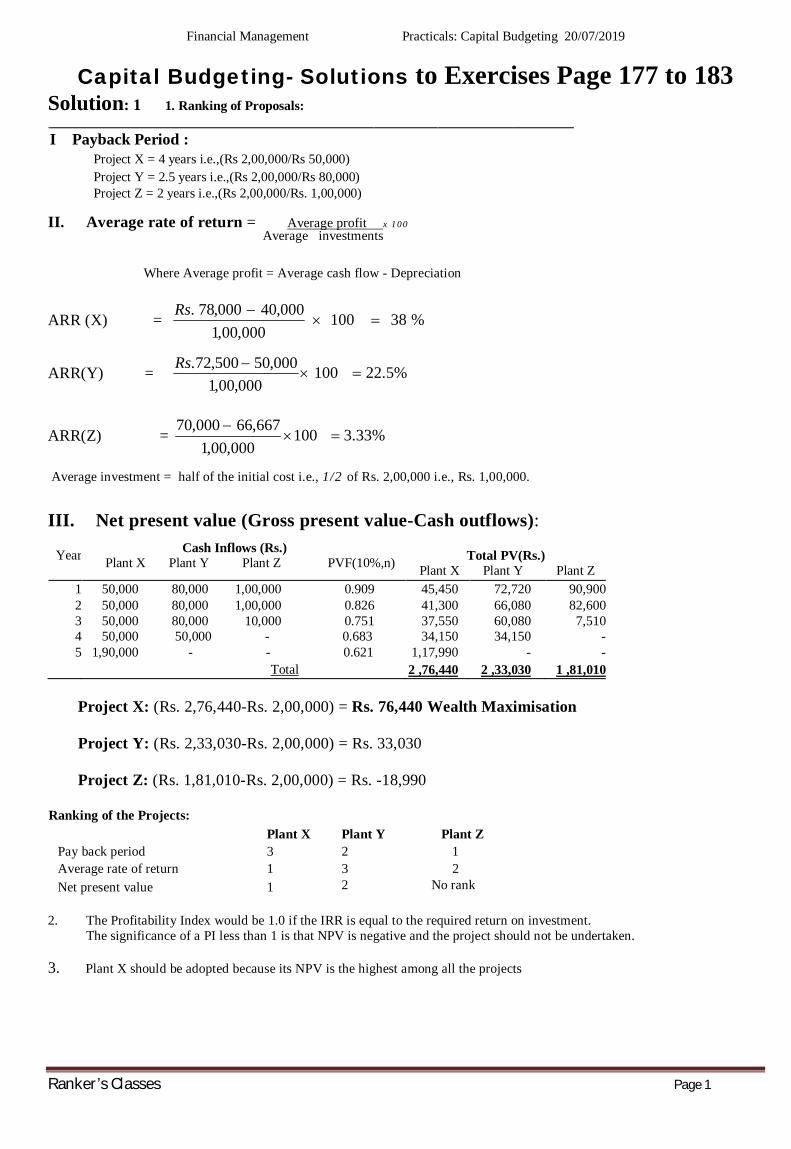

capital budgeting- solutions to exercises page 177 to 183

TRANSCRIPT

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 1

Capital Budgeting- Solutions to Exercises Page 177 to 183 Solution: 1 1. Ranking of Proposals:

I Payback Period : Project X = 4 years i.e.,(Rs 2,00,000/Rs 50,000) Project Y = 2.5 years i.e.,(Rs 2,00,000/Rs 80,000) Project Z = 2 years i.e.,(Rs 2,00,000/Rs. 1,00,000)

II. Average rate of return = Average profit x 100 Average investments

Where Average profit = Average cash flow - Depreciation

ARR (X) = %38100000,00,1

000,40000,78.

Rs

ARR(Y) = %5.22100000,00,1

000,50500,72.

Rs

ARR(Z) = %33.3100000,00,1

667,66000,70

Average investment = half of the initial cost i.e., 1/2 of Rs. 2,00,000 i.e., Rs. 1,00,000.

III. Net present value (Gross present value-Cash outflows):

Year Cash Inflows (Rs.) Plant X Plant Y Plant Z PVF(10%,n) Total PV(Rs.)

Plant X Plant Y Plant Z 1 50,000 80,000 1,00,000 0.909 45,450 72,720 90,9002 50,000 80,000 1,00,000 0.826 41,300 66,080 82,6003 50,000 80,000 10,000 0.751 37,550 60,080 7,5104 50,000 50,000 - 0.683 34,150 34,150 -5 1,90,000 - - 0.621 1,17,990 - -

Total 2 ,76,440 2 ,33,030 1 ,81,010 Project X: (Rs. 2,76,440-Rs. 2,00,000) = Rs. 76,440 Wealth Maximisation Project Y: (Rs. 2,33,030-Rs. 2,00,000) = Rs. 33,030 Project Z: (Rs. 1,81,010-Rs. 2,00,000) = Rs. -18,990

Ranking of the Projects: Plant X Plant Y Plant Z

Pay back period 3 2 1 Average rate of return 1 3 2 Net present value 1 2 No rank

2. The Profitability Index would be 1.0 if the IRR is equal to the required return on investment. The significance of a PI less than 1 is that NPV is negative and the project should not be undertaken. 3. Plant X should be adopted because its NPV is the highest among all the projects

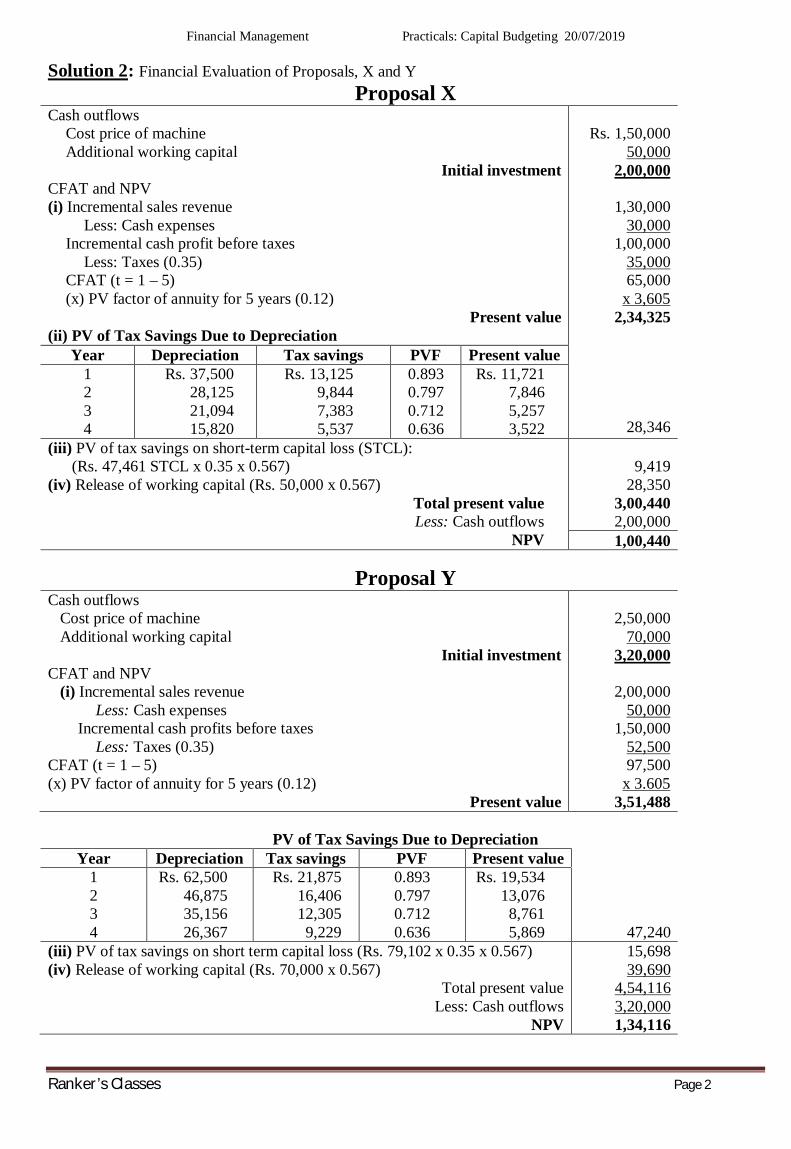

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 2

Solution 2: Financial Evaluation of Proposals, X and Y Proposal X

Cash outflows Cost price of machine Additional working capital

Initial investment CFAT and NPV (i) Incremental sales revenue

Less: Cash expenses Incremental cash profit before taxes

Less: Taxes (0.35) CFAT (t = 1 – 5) (x) PV factor of annuity for 5 years (0.12)

Present value (ii) PV of Tax Savings Due to Depreciation

Rs. 1,50,000

50,000 2,00,000

1,30,000

30,000 1,00,000

35,000 65,000

x 3,605 2,34,325

28,346

Year Depreciation Tax savings PVF Present value 1 2 3 4

Rs. 37,500 28,125 21,094 15,820

Rs. 13,125 9,844 7,383 5,537

0.893 0.797 0.712 0.636

Rs. 11,721 7,846 5,257 3,522

(iii) PV of tax savings on short-term capital loss (STCL): (Rs. 47,461 STCL x 0.35 x 0.567)

(iv) Release of working capital (Rs. 50,000 x 0.567) Total present value Less: Cash outflows

NPV

9,419

28,350 3,00,440 2,00,000 1,00,440

Proposal Y Cash outflows

Cost price of machine Additional working capital

Initial investment CFAT and NPV

(i) Incremental sales revenue Less: Cash expenses

Incremental cash profits before taxes Less: Taxes (0.35)

CFAT (t = 1 – 5) (x) PV factor of annuity for 5 years (0.12)

Present value

2,50,000

70,000 3,20,000

2,00,000

50,000 1,50,000

52,500 97,500

x 3.605 3,51,488

PV of Tax Savings Due to Depreciation

Year Depreciation Tax savings PVF Present value 1 2 3 4

Rs. 62,500 46,875 35,156 26,367

Rs. 21,875 16,406 12,305 9,229

0.893 0.797 0.712 0.636

Rs. 19,534 13,076 8,761 5,869

47,240

(iii) PV of tax savings on short term capital loss (Rs. 79,102 x 0.35 x 0.567) (iv) Release of working capital (Rs. 70,000 x 0.567)

Total present value Less: Cash outflows

NPV

15,698 39,690

4,54,116 3,20,000 1,34,116

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 3

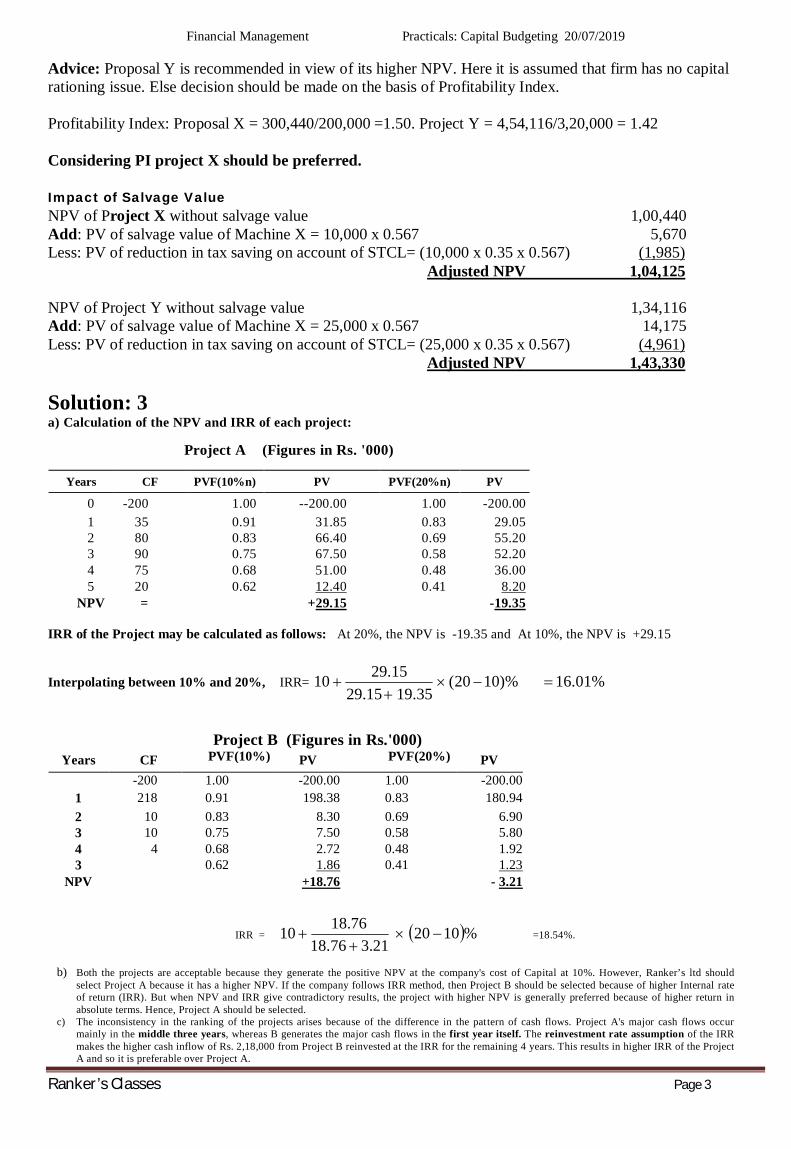

Advice: Proposal Y is recommended in view of its higher NPV. Here it is assumed that firm has no capital rationing issue. Else decision should be made on the basis of Profitability Index. Profitability Index: Proposal X = 300,440/200,000 =1.50. Project Y = 4,54,116/3,20,000 = 1.42 Considering PI project X should be preferred. Impact of Salvage Value NPV of Project X without salvage value 1,00,440 Add: PV of salvage value of Machine X = 10,000 x 0.567 5,670 Less: PV of reduction in tax saving on account of STCL= (10,000 x 0.35 x 0.567) (1,985) Adjusted NPV 1,04,125 NPV of Project Y without salvage value 1,34,116 Add: PV of salvage value of Machine X = 25,000 x 0.567 14,175 Less: PV of reduction in tax saving on account of STCL= (25,000 x 0.35 x 0.567) (4,961) Adjusted NPV 1,43,330 Solution: 3 a) Calculation of the NPV and IRR of each project:

Project A (Figures in Rs. '000)

Years CF PVF(10%n) PV PVF(20%n) PV

0 -200 1.00 --200.00 1.00 -200.00 1 35 0.91 31.85 0.83 29.05 2 80 0.83 66.40 0.69 55.20 3 90 0.75 67.50 0.58 52.20 4 75 0.68 51.00 0.48 36.00 5 20 0.62 12.40 0.41 8.20

NPV = +29.15 -19.35 IRR of the Project may be calculated as follows: At 20%, the NPV is -19.35 and At 10%, the NPV is +29.15

Interpolating between 10% and 20%, IRR= %01.16)%1020(35.1915.29

15.2910

Project B (Figures in Rs.'000)

Years CF PVF(10%)

PV PVF(20%)

PV -200 1.00 -200.00 1.00 -200.00

1 218 0.91 198.38 0.83 180.942 10 0.83 8.30 0.69 6.903 10 0.75 7.50 0.58 5.804 4 0.68 2.72 0.48 1.923 0.62 1.86 0.41 1.23

NPV +18.76 - 3.21

IRR = %102021.376.18

76.1810

=18.54%.

b) Both the projects are acceptable because they generate the positive NPV at the company's cost of Capital at 10%. However, Ranker’s ltd should select Project A because it has a higher NPV. If the company follows IRR method, then Project B should be selected because of higher Internal rate of return (IRR). But when NPV and IRR give contradictory results, the project with higher NPV is generally preferred because of higher return in absolute terms. Hence, Project A should be selected.

c) The inconsistency in the ranking of the projects arises because of the difference in the pattern of cash flows. Project A's major cash flows occur mainly in the middle three years, whereas B generates the major cash flows in the first year itself. The reinvestment rate assumption of the IRR makes the higher cash inflow of Rs. 2,18,000 from Project B reinvested at the IRR for the remaining 4 years. This results in higher IRR of the Project A and so it is preferable over Project A.

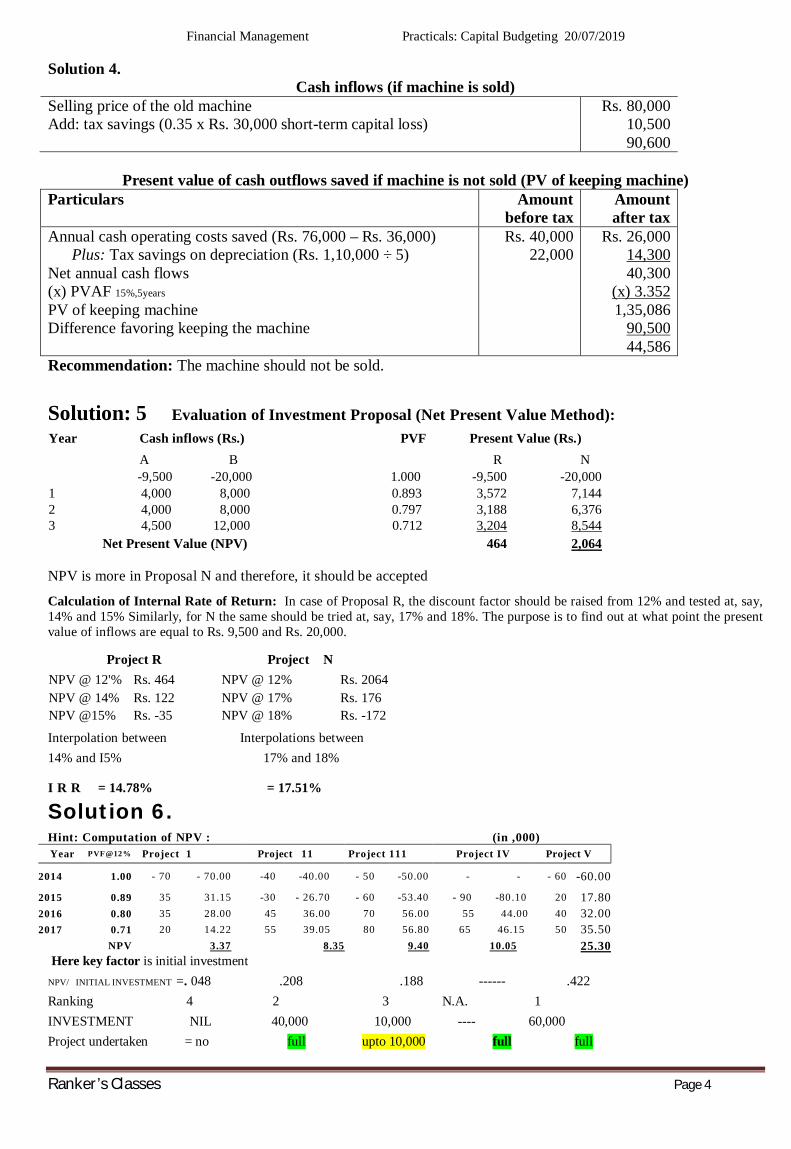

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 4

Solution 4. Cash inflows (if machine is sold)

Selling price of the old machine Add: tax savings (0.35 x Rs. 30,000 short-term capital loss)

Rs. 80,000 10,500 90,600

Present value of cash outflows saved if machine is not sold (PV of keeping machine)

Particulars Amount before tax

Amount after tax

Annual cash operating costs saved (Rs. 76,000 – Rs. 36,000) Plus: Tax savings on depreciation (Rs. 1,10,000 ÷ 5)

Net annual cash flows (x) PVAF 15%,5years PV of keeping machine Difference favoring keeping the machine

Rs. 40,000 22,000

Rs. 26,000 14,300 40,300

(x) 3.352 1,35,086

90,500 44,586

Recommendation: The machine should not be sold.

Solution: 5 Evaluation of Investment Proposal (Net Present Value Method): Year Cash inflows (Rs.) PVF Present Value (Rs.) A B R N -9,500 -20,000 1.000 -9,500 -20,0001 4,000 8,000 0.893 3,572 7,1442 4,000 8,000 0.797 3,188 6,3763 4,500 12,000 0.712 3,204 8,544 Net Present Value (NPV) 464 2,064

NPV is more in Proposal N and therefore, it should be accepted

Calculation of Internal Rate of Return: In case of Proposal R, the discount factor should be raised from 12% and tested at, say, 14% and 15% Similarly, for N the same should be tried at, say, 17% and 18%. The purpose is to find out at what point the present value of inflows are equal to Rs. 9,500 and Rs. 20,000.

Project R Project N NPV @ 12'% Rs. 464 NPV @ 12% Rs. 2064 NPV @ 14% Rs. 122 NPV @ 17% Rs. 176 NPV @15% Rs. -35 NPV @ 18% Rs. -172

Interpolation between Interpolations between 14% and I5% 17% and 18%

I R R = 14.78% = 17.51%

Solution 6. Hint: Computation of NPV : (in ,000) Year PVF@12% Project 1 Project 11 Project 111 Project IV Project V

2014 1.00 - 70 - 70.00 -40 -40.00 - 50 -50.00 - - - 60 -60.00

2015 0.89 35 31.15 -30 - 26.70 - 60 -53.40 - 90 -80 .10 20 17.802016 0.80 35 28.00 45 36.00 70 56.00 55 44.00 40 32.002017 0.71 20 14.22 55 39.05 80 56.80 65 46.15 50 35.50 NPV 3.37 8.35 9.40 10.05 25.30

Here key factor is initial investment NPV/ INITIAL INVESTMENT =. 048 .208 .188 ------ .422 Ranking 4 2 3 N.A. 1 INVESTMENT NIL 40,000 10,000 ---- 60,000 Project undertaken = no full upto 10,000 full full

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 5

Solution 7. (i) Determination of project IRR (Rs crore)

Cash outflow/project cost: Cash inflows (t = 1 – 15 years): Toll revenue

Less: Toll collection expenses, maintenance of the roads, etc (Rs. 200 crore x 0.05) Net cash inflows

Rs. 200

50 10

40

By Trial and Error method r = 18.43 per cent. (ii) Determination of Equity IRR: It may be defined as a rate of discount which discounts future cash inflows available to equity holders in such a way that the PV of these cash inflows is equal to the equity Owners investment. Accordingly, the relevant values are: (a) Equity share capital is Rs. 50 crore and (b) cash inflows available to equity holders are Rs. 14.35 crore as

shown below (Rs. crore)

Net cash inflow of the project Less: Equated installment of the project (Rs. 150 crore / PVIF at 15% for 15 years i.e., 5.847)

Rs. 40 25.65

14.35

Payback period is Rs. 50 crore/Rs. 14.35 crore = 3.484 The PV factor closest to 3.484 (as per PV annuity table corresponding to 15 years) is 3.483, at 28 per cent rate of discount. In other words, 28 per cent is equity IRR.

Note: Depreciation is considered in capital budgeting decisions as it yields tax savings (depreciation per se does not cause cash outflows). Since taxes are to be ignored in the present question, therefore, depreciation is also not taken into account. Solution 8:

Determination of equivalent annual cost of plants X and Y Particulars Year COBT COAT PV factor

at 0.12 Total PV

Plant X Purchase cost Operating costs Tax advantage on depreciation Salvage value

0

1-5 1-5

5

Rs. 5,00,000

2,50,000 --

40,000

Rs. 5,00,000

1,62,5001 (33,2502) (34,7503)

1.000 3.605 3.605 0.567

Rs. 5,00,000

5,85,812 (1,19,866)

(19,703) 9,46,243

3.605 2,62,481

Total cost PVAF at 12%, 5 years

Equivalent annual cost

Plant Y Purchase costs Operating costs Tax advantage on depreciation Overhaul cost

0

1-10 1-8

7

7,00,000 2,20,000

-- 1,00,000

7,00,000

1,43,0004 (30,6255)

65,0006

1.000 5.650 4.968

0.5077

7,00,000 8,07,950

(1,52,145) 32,955

13,88,760

5.650 2,45,798

Total cost PVAF @ 12% for 10 years

Equivalent Annual Cost (EAC) 1. Rs. 2,50,000 (1-tax rate 0.35) = Rs. 1,62,500

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 6

2. [(Rs. 5,00,000 – Rs. 25,000)/5 years] x tax rate, 0.35 = Rs. 33,250 3. Rs. 40,000 – Tax payment on gain i.e., Rs. 15,000 x 0.35 = Rs. 34,750 4. Rs. 2,20,000 (1 – 0.35) = Rs. 1,43,000 5. (Rs. 70,000/8 years) x 0.35 = Rs. 30,625 6. Rs. 1,00,000 x 0.65 = Rs. 65,000 7. PV factor at year-end 6 at 12%

Recommendation: Buy plant Y as its EAC lower. Solution 9.

(i) Determination of NPV and PI for all projects Project Life in

years Year-end

CFAT PV factor at

0.12 corresponding to life of the project

Total PV of CFAT

Initial Investment

NPV PI

Order of

A B C D E

2 5 3 9 10

Rs. 1,87,600 66,000

1,00,000 20,000 66,000

1.690 3.605 2.402 5.328 5.650

Rs. 3,17,044 2,37,930 2,40,200 1,06,560 3,72,900

Rs. 3,00,000 2,00,000 2,00,000 1,00,000 3,00,000

Rs. 17,044 37,930 40,200 6,560

72,900

1.057 1.189 1.200 1.066 1.243

4 3 2 5 1

5 3 2 4 1

(ii) Optimal investment package when capital budget is Rs. 4,00,000 Project Investment NPV

E D

Rs. 3,00,000 1,00,000

Rs. 72,900 6,560

79,460

(iii) Capital budget is Rs. 5,00,000 Project Investment NPV

E C

3,00,000 2,00,000

Rs. 72,900 40,200

1,13,100

(iv) (a) Capital budget is Rs. 4,00,000 Project Investment PI NPV

E C (0.50)

Rs. 3,00,000 1,00,000 (0.50 x Rs. 2,00,000)

1.243 1.200

72,900 20,100 93,000

(b) Capital budget is Rs. 5,00,000 Project Investment PI NPV

E C

Rs. 3,00,000 2,00,000

1.243 1.200

72,900 40,200

1,13,100

Solution 10: (i) Calculation of contribution:

Selling Price (Per unit) Rs. 12 Less: Variable cost (Per unit) 8 Contribution (Per unit) 4 Calculation of NPV Total Contribution (Annual) Rs. 1,60,000 (40,000 units x Rs. 4) Less: Annual Cash Fixed Cost -20,000 Net Cash inflow (Annual) 1,40,000 [ Depreciation and Tax ignored] PVAF(15%, 6 years) 3.784

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 7

Total present value of net cash inflows 5,29,760 Add: Present value of scrap at end of Year 6 (Rs. 20,000 x 0.432) 8,640 Present value of total cash inflows 5,38,400 Less: Initial investment 4,00,000 Net Present Value 1,38,400

(ii) Calculation of minimum volume of sales required to justify[discounted break even] the Project: Let No. of units to be sold be ‘x’. At this level, NPV should be zero. This can be presented as follows: {[( 4x-Rs.20,000)x3.784]+Rs.8,646} =Rs.4,00,000 15.136’x’-75,680 + 8,646 - 4,00,000 = 0 15.136’x’ - 4,67,034 = 0 15.136’x’ = 4,67,034 ‘x’ = 4,67,034/15.136 = 30,856 units

If the firm is expecting as sales of 30,856 units, the project is justified, otherwise not. This can be verified as follows:

Sales (Units) 30,856 Contribution @ Rs. 4 per unit Rs. 1,23,424 Less Fixed Cost 20,000 Net Profit 1,03,424 PVAF(15%,6) 3,784 PV of Annual Inflows Rs. 3,91,356 PV of Scrap 8,640 Total Present Value 3,99,996 Initial Investment 4,00,000

The difference of Rs. 4 is appearing because of approximation. Compute discounted Break even by assuming salvage value of Rs. 40,000 and Tax Rate of 30%

Alternate Solution: 10 Annual Depreciation = 4,00,000-40,000 = 60,000 6 years Let number of units = x. Total contribution = 4 x Annual cash inflow = ( 4x - 20,000-60,000)(1-0.30)+60,000 Or (4x-80,000).7+60,000 Or 2.8 x -56,000+ 60,000 Or 2.8x +4000 PV of annual cash inflow = (2.8x +4000)3.784 = 10.5952x + 15136

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 8

PV of Salvage = 40,000 x 0.432 = 17,280 PV of all inflows =10.5952x + 15136+17,280 = 10.5952 x + 32,416 In case of break even, 10.5952 x + 32,416 = 4,00,000 X = 34,693 Solution to Exercise: 11:

Step 1: Computation of Annual Cash Inflows After Tax (Assume Sales units = X)

No. of Sales Units Selling Price per unit Total Sales [A x B] Less: Variable Cost Contribution [Sales- variable Cost] Cash Fixed cost Depreciation [(Rs. 5,10,000 – Rs. 10,000)/5] Earnings before Tax Less: Tax @ 30% Earnings after tax Add: Depreciation Annual Cash Flow after Tax + Release of Working Capital + Salvage Value Less: Tax on Profit on Sale (30%

of Rs. 5,000) CFAT for the last year

X 100

100 X (30 X)

70X (30,000)

(1,00,000)

70X – 1,30,000 21 X – 39,000 49 X – 91,000

1,00,000 49 X + 9,000

16,458 15,000

(1,500)

49 X + 38,958 Terminal cash flow 29,958

PV OF ANNUAL CASH FLOW for five years = (49 X + 9,000)3.791 = ` = 185.759 X + 34,119 PV OF terminal flow 29,958 x .621 = 18,604 Total PV = 185.759X + 52,723 AT BREAK EVEN 185.759X + 52,723 = 6,10,000 X = 3000 UNITS.

Step 2: Computation of PV of CFAT PV of CFAT = 3.17 (49 X + 9,000) + 0.621 (49 X + 38,958) = 155.33 X + 28,530 + 30,429X + 24,193 = 185.759 X + Rs. 52,723 Step 3: Time Adjusted Break Even Point PV of CFAT = PV of Cash Outflow 185.759 X + Rs. 52,723 = Rs. 6,10,000 (i.e., Cost of Machine + Working Capital)

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 9

X = (Rs. 6,10,000 – Rs. 52,723)/185.759 = 3,000 units Hence, Time Adjusted B.E.P = 3,000 Units Q 12. A company manufacturing and selling domestic appliances wants to take up a diversification project to make and sell a new type of pressure cooker. Estimates relating to the project are given below: Investment Rs. 40 lakhs Method of

depreciation Straight

line Annual sales 10,000 units Tax rate 50% Variable cost/unit Rs. 360 Cost of capital 12% Fixed production, admin. and selling costs p.a. Life of the project Salvage value at the end of project life.

Rs. 10 Lakhs 8 years Nil

PV value of an annuity of Re 1 at 12% p.a.

4.9676

You are required to fix minimum price for the pressure cooker to meet the above requirements. Answer 12 :

Pricing decision on the basis of capital budgeting In this case, we have to find out the sales value of 10,000 units in the reverse order as follows: Investment = Rs. 40 lakhs. Present value of CFAT also will be Rs. 40 lakhs, i.e. yearly cash flow after

tax for 8 years will be: Rs. 40 lakhs/4.9676 = Rs. 8,05,218 Less: Depreciation 40 lakhs/8 = Rs. 5,00,000 PAT = 3,05,218 Tax 50% = 3,05,218 PBT = 6,10,436 Add: Total Cost: Variable cost 10,000 x 360 = 36 lakhs Fixed cost = 10 lakhs Depreciation = 5 lakhs = 51,00,000 Sales value of 10,000 units = 57,10,436 Selling price per unit = Rs. 57,10,436/10,000 units = Rs. 571.04 per unit.

Note: It is assumed that the depreciation of Rs. 5 lakhs per annum is not included in the fixed cost of Rs. 10

lakhs per annum.

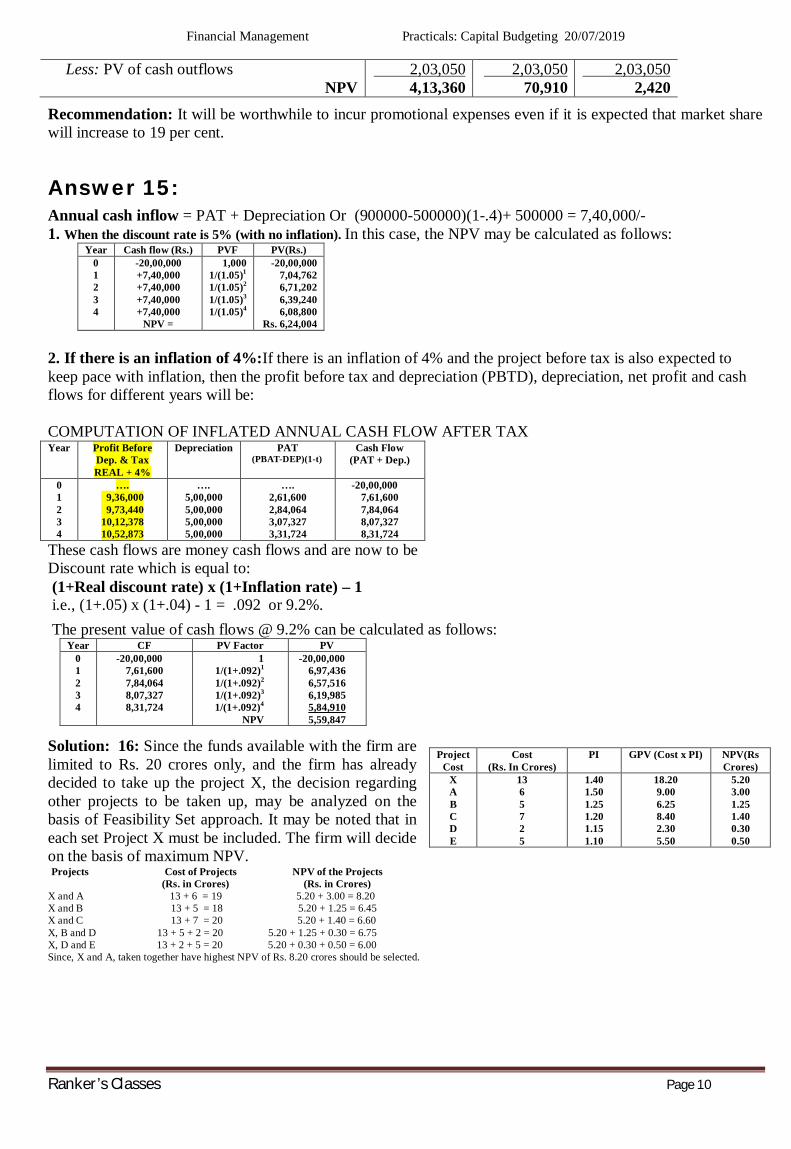

Answer 13: NPV Rs. 2,21,800

Solution 14: Present value of promotional expenses incurred

Year Promotional expenses PV factor Total PV 1 2 3

Rs. 1,00,000 75,000 50,000

1,000 0.870 0.756

Rs. 1,00,000 65,250

37,800 2,03,050

NPV of increased market share (25, 20 and 19 per cent)

Particulars Increased market shares (Years 1 – 3)

25 per cent 20 per cent 19 per cent Incremental sales revenue

Less: Variable costs (0.70) Less: Incremental fixed costs

Incremental profit (x) PV factor annuity (0.15) for 3 years PV of incremental profit

Rs. 10,00,000 7,00,000

30,000 2,70,000

2.283 6,16,410

Rs. 5,00,000 3,50,000

30,000 1,20,000

2.283 2,73,960

Rs. 4,00,000 2,80,000

30,000 90,000

2.283 2,05,470

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 10

Less: PV of cash outflows NPV

2,03,050 4,13,360

2,03,050 70,910

2,03,050 2,420

Recommendation: It will be worthwhile to incur promotional expenses even if it is expected that market share will increase to 19 per cent.

Answer 15:

Annual cash inflow = PAT + Depreciation Or (900000-500000)(1-.4)+ 500000 = 7,40,000/- 1. When the discount rate is 5% (with no inflation). In this case, the NPV may be calculated as follows:

Year Cash flow (Rs.) PVF PV(Rs.) 0 1 2 3 4

-20,00,000 +7,40,000 +7,40,000 +7,40,000 +7,40,000

NPV =

1,000 1/(1.05)1 1/(1.05)2 1/(1.05)3 1/(1.05)4

-20,00,000 7,04,762 6,71,202 6,39,240 6,08,800

Rs. 6,24,004

2. If there is an inflation of 4%:If there is an inflation of 4% and the project before tax is also expected to keep pace with inflation, then the profit before tax and depreciation (PBTD), depreciation, net profit and cash flows for different years will be: COMPUTATION OF INFLATED ANNUAL CASH FLOW AFTER TAX Year Profit Before

Dep. & Tax REAL + 4%

Depreciation PAT (PBAT-DEP)(1-t)

Cash Flow (PAT + Dep.)

0 1 2 3 4

…. 9,36,000 9,73,440 10,12,378 10,52,873

…. 5,00,000 5,00,000 5,00,000 5,00,000

…. 2,61,600 2,84,064 3,07,327 3,31,724

-20,00,000 7,61,600 7,84,064 8,07,327 8,31,724

These cash flows are money cash flows and are now to be Discount rate which is equal to: (1+Real discount rate) x (1+Inflation rate) – 1 i.e., (1+.05) x (1+.04) - 1 = .092 or 9.2%.

The present value of cash flows @ 9.2% can be calculated as follows: Year CF PV Factor PV

0 1 2 3 4

-20,00,000 7,61,600 7,84,064 8,07,327 8,31,724

1 1/(1+.092)1

1/(1+.092)2

1/(1+.092)3

1/(1+.092)4 NPV

-20,00,000 6,97,436 6,57,516 6,19,985 5,84,910 5,59,847

Solution: 16: Since the funds available with the firm are limited to Rs. 20 crores only, and the firm has already decided to take up the project X, the decision regarding other projects to be taken up, may be analyzed on the basis of Feasibility Set approach. It may be noted that in each set Project X must be included. The firm will decide on the basis of maximum NPV. Projects Cost of Projects NPV of the Projects (Rs. in Crores) (Rs. in Crores) X and A 13 + 6 = 19 5.20 + 3.00 = 8.20 X and B 13 + 5 = 18 5.20 + 1.25 = 6.45 X and C 13 + 7 = 20 5.20 + 1.40 = 6.60 X, B and D 13 + 5 + 2 = 20 5.20 + 1.25 + 0.30 = 6.75 X, D and E 13 + 2 + 5 = 20 5.20 + 0.30 + 0.50 = 6.00 Since, X and A, taken together have highest NPV of Rs. 8.20 crores should be selected.

Project Cost

Cost (Rs. In Crores)

PI GPV (Cost x PI) NPV(Rs Crores)

X A B C D E

13 6 5 7 2 5

1.40 1.50 1.25 1.20 1.15 1.10

18.20 9.00 6.25 8.40 2.30 5.50

5.20 3.00 1.25 1.40 0.30 0.50

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 11

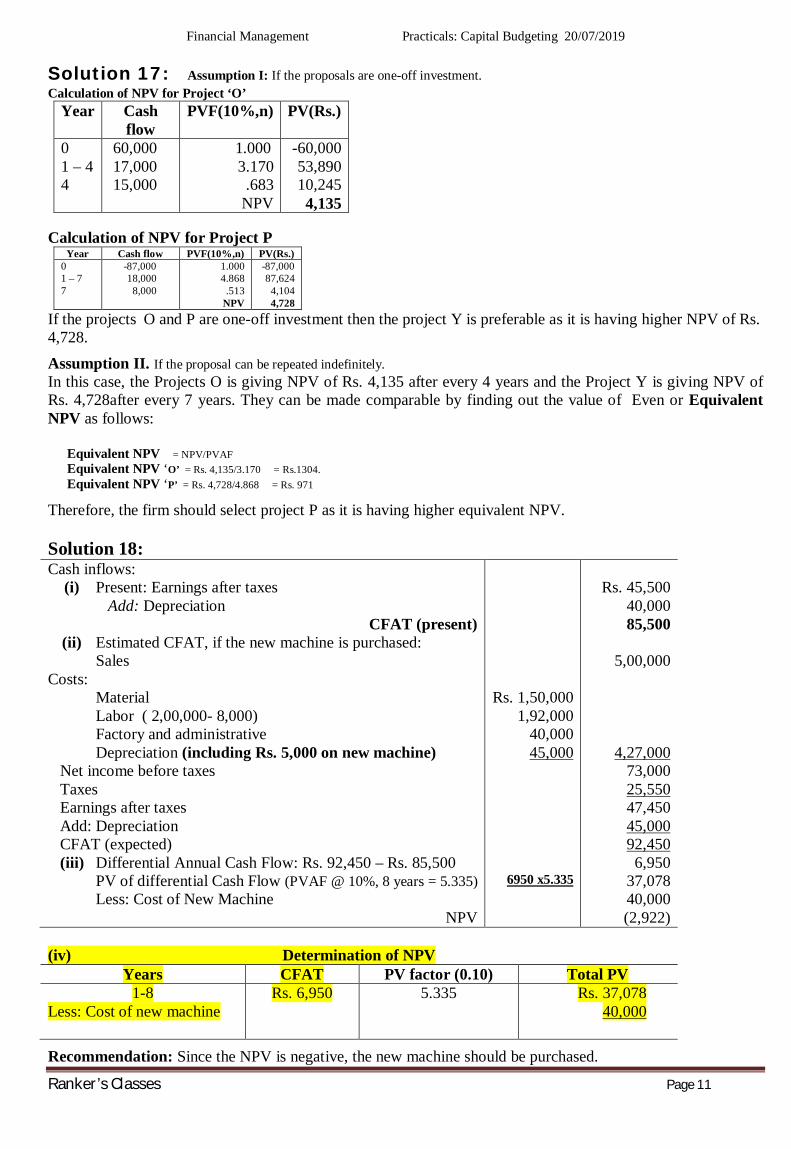

Solution 17: Assumption I: If the proposals are one-off investment. Calculation of NPV for Project ‘O’

Year Cash flow

PVF(10%,n) PV(Rs.)

0 1 – 4 4

60,000 17,000 15,000

1.000 3.170 .683

NPV

-60,000 53,890 10,245 4,135

Calculation of NPV for Project P

Year Cash flow PVF(10%,n) PV(Rs.) 0 1 – 7 7

-87,000 18,000

8,000

1.000 4.868

.513 NPV

-87,000 87,624

4,104 4,728

If the projects O and P are one-off investment then the project Y is preferable as it is having higher NPV of Rs. 4,728.

Assumption II. If the proposal can be repeated indefinitely. In this case, the Projects O is giving NPV of Rs. 4,135 after every 4 years and the Project Y is giving NPV of Rs. 4,728after every 7 years. They can be made comparable by finding out the value of Even or Equivalent NPV as follows:

Equivalent NPV = NPV/PVAF Equivalent NPV ‘O’ = Rs. 4,135/3.170 = Rs.1304. Equivalent NPV ‘P’ = Rs. 4,728/4.868 = Rs. 971

Therefore, the firm should select project P as it is having higher equivalent NPV. Solution 18: Cash inflows:

(i) Present: Earnings after taxes Add: Depreciation

CFAT (present) (ii) Estimated CFAT, if the new machine is purchased:

Sales Costs:

Material Labor ( 2,00,000- 8,000) Factory and administrative Depreciation (including Rs. 5,000 on new machine)

Net income before taxes Taxes Earnings after taxes Add: Depreciation CFAT (expected) (iii) Differential Annual Cash Flow: Rs. 92,450 – Rs. 85,500

PV of differential Cash Flow (PVAF @ 10%, 8 years = 5.335) Less: Cost of New Machine

NPV

Rs. 1,50,000 1,92,000

40,000 45,000

6950 x5.335

Rs. 45,500

40,000 85,500

5,00,000

4,27,000 73,000 25,550 47,450 45,000 92,450 6,950

37,078 40,000 (2,922)

(iv) Determination of NPV

Years CFAT PV factor (0.10) Total PV 1-8

Less: Cost of new machine

Rs. 6,950 5.335 Rs. 37,078 40,000

Recommendation: Since the NPV is negative, the new machine should be purchased.

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 12

Solution: 19 1. Cash outflow at Y0: Cost of new Computer

- Disposal of Office Total

2. Cash inflows (Annual) Saving in Design and Draughtsmanship cost - Operation and Maintenance cost

Cash saving before tax After 40% Tax = 600000 (1 –0.4) =

3. 40% Tax saving on Rs. 36 lacs available at the end of Year 1 4. Sales value of Computer after 6 years

Rs. 36 lacs Rs. 8 lacs Rs. 28 lacs

Rs. In lacs 12.00 6.00 6.00 3.60

14.4

Rs. 90,000 The total cash inflows for the year 1 would be Rs. 18 lacs (i.e., Rs. 14.40 lacs + Rs. 3.60 lacs). Similarly, the total inflow for the last year would be Rs. 4.50 (i.e., Rs. 3.60 lacs + Rs. 90,000).

Calculation of Net Present Value Year Cash flows

(Rs. Lakhs) PVF(12%,n) (Rs. In lacs)

PV Rs.) 0 1 2 3 4 5 6

-28.00 3.60+14.4 =18

3.60 3.60 3.60 3.60

3.60+.90 = 4.50

1.000 0.893 0.797 0.712 0.636 0.567 0.507

-28.00 16.04

2.87 2.56 2.29 2.04 2.28 .115

As the NPV is Positive at Rs. 11,418 the proposal should be accepted.

Solution 20: Incremental cash outflows Purchase price of new machine

Add: Additional working capital Less: Sale value of old machine

Rs. 1,07,500 10,000 25,000 92,500

Determination of CFAT and NPV

Particulars Years 1 2 3 4

Incremental revenue Less: incremental depreciation

Earnings before taxes Less: Taxes (0.35)

Earnings after taxes CFAT (EAT + D)

Add: Recovery of working capital (x) PV factor (0.10)

Present value Total present value (t = 1 – 4)

Less: Incremental cash outflows NPV

Rs. 36,000 20,625 15,375 5,381 9,994

30,619

0.909 27,833

Rs. 36,000 15,469 20,531 7,186

13,345 28,814

0.826

23,800

Rs. 36,000 11,601 24,399 8,540

15,859 27,460

0.751

20,623

Rs. 36,000 8,701

27,299 9,555

17,744 26,445 10,000 0.683

24,892 97,148 92,500 4,648

Recommendation: Since NPV is positive, the company is advised to replace the existing machine.

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 13

Working Notes: (i) Incremental revenues

Particulars

Existing machine New machine Differential (1) – (2)

(1) (2) (3) 1. Annual operating hours 2. Output per hour (units) 3. Total output (units) 4. Selling p[rice per unit (Rs.) 5. Total sales revenue (3 x 4) 6. Less: Expenses Material Labor Consumable stores Repairs and maintenance

Incremental revenue

1,000 15

15,000 3

Rs. 45,000

6,000 11,000 2,000 3,000

23,000

1,000 30

30,000 3

Rs. 90,000

12,000 16,000 1,000 2,000

59,000

--- 15

15,000 3

Rs. 45,000

6,000 5,000 1,000 1,000

36,000

(ii) Incremental depreciation (if machine is purchased) (a)WDV of existing in the beginning of year 3

Initial cost of machined Less: Depreciation charges (years 1 and 2): Year 1 (Rs. 60,000 x 0.25)

2 (Rs. 45,000 x 0.25) (b)Depreciation base of new machine:

WDV of existing machine Add: Cost of new machine Less: Sale value of existing machine

(c)Base for incremental depreciation: (Rs. 1,16,250 – Rs. 33,750)

Rs. 15,000 11,250

Rs. 60,000

26,250 33,750

33,750

1,07,500 (25,000) 1,16,250

82,500

(d) Incremental depreciation (t = 1 – 4) Year WDV Depreciation

1 2 3 4

Rs. 82,500 61,785 46,406 34,805

Rs. 20,625 15,469 11,601 8,701

Note: There will be an additional tax advantage on depreciation of Rs. 26,104 (Rs. 34,805 – Rs. 8,701) in the future years.

Solution 21 : Financial evaluation of whether to replace Machine-R (i) Incremental cash outflows Rs.

Cost of Machine-S Less: Effective sale proceeds of Machine-R (1,00,000 – 30,000) Incremental cash inflows and NPV (for years t = 1 – 5)

Savings in annual operating costs: Annual cash operating costs (R) Annual cash operating costs (S)

(x) PV factor of annuity for 5 years (0.14) Total present value

Less: Incremental cash outflows NPV

2,00,0001,80,000

2,50,000 70,000

1,80,000

20,000 x 3.433 68,660

1,80,000 (1,11,340)

Recommendation: Since NPV is negative, the company is advised not to replace Machine-R.

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 14

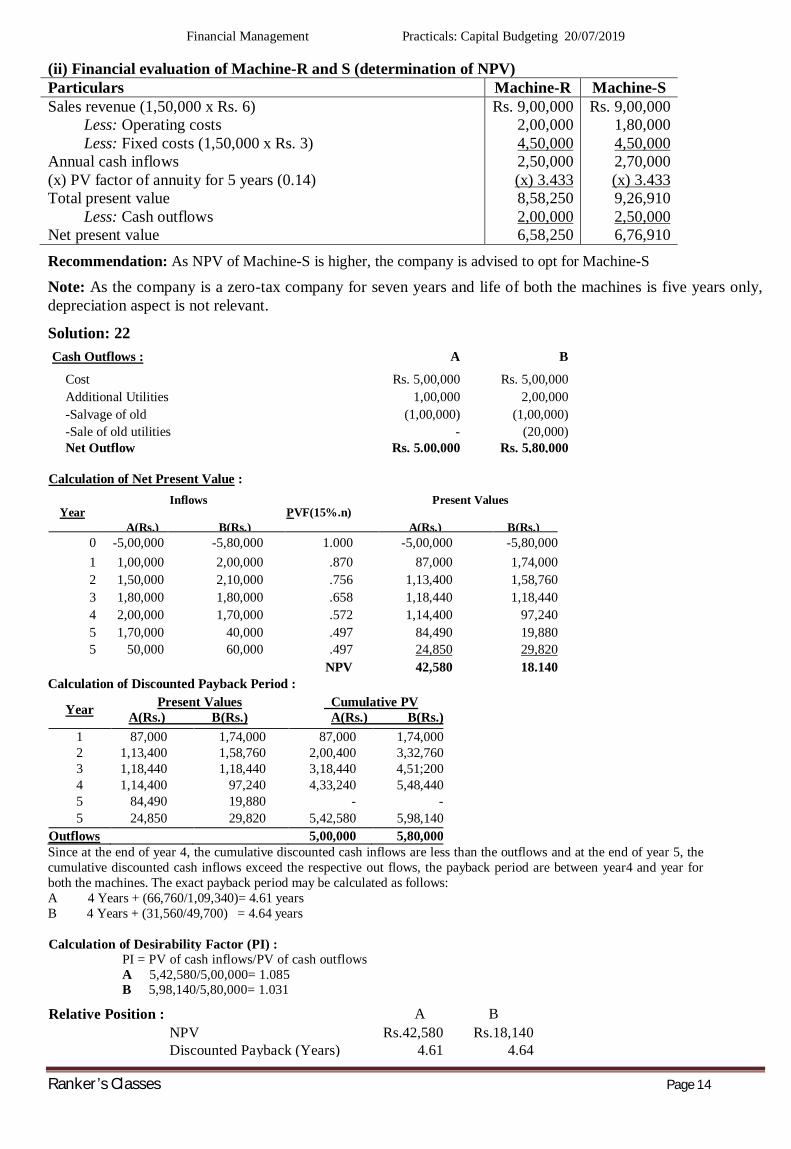

(ii) Financial evaluation of Machine-R and S (determination of NPV) Particulars Machine-R Machine-S Sales revenue (1,50,000 x Rs. 6)

Less: Operating costs Less: Fixed costs (1,50,000 x Rs. 3)

Annual cash inflows (x) PV factor of annuity for 5 years (0.14) Total present value

Less: Cash outflows Net present value

Rs. 9,00,000 2,00,000 4,50,000 2,50,000 (x) 3.433 8,58,250 2,00,000 6,58,250

Rs. 9,00,000 1,80,000 4,50,000 2,70,000 (x) 3.433 9,26,910 2,50,000 6,76,910

Recommendation: As NPV of Machine-S is higher, the company is advised to opt for Machine-S

Note: As the company is a zero-tax company for seven years and life of both the machines is five years only, depreciation aspect is not relevant.

Solution: 22 Cash Outflows : A B

Cost Rs. 5,00,000 Rs. 5,00,000Additional Utilities 1,00,000 2,00,000-Salvage of old (1,00,000) (1,00,000)-Sale of old utilities - (20,000)Net Outflow Rs. 5.00,000 Rs. 5,80,000

Calculation of Net Present Value :

Year Inflows

A(Rs.) B(Rs.)

PVF(15%.n) Present Values

A(Rs.) B(Rs.)

0 -5,00,000 -5,80,000 1.000 -5,00,000 -5,80,0001 1,00,000 2,00,000 .870 87,000 1,74,0002 1,50,000 2,10,000 .756 1,13,400 1,58,7603 1,80,000 1,80,000 .658 1,18,440 1,18,4404 2,00,000 1,70,000 .572 1,14,400 97,2405 1,70,000 40,000 .497 84,490 19,8805 50,000 60,000 .497 24,850 29,820

NPV 42,580 18.140Calculation of Discounted Payback Period :

Year Present Values A(Rs.) B(Rs.)

Cumulative PV A(Rs.) B(Rs.)

1 87,000 1,74,000 87,000 1,74,0002 1,13,400 1,58,760 2,00,400 3,32,7603 1,18,440 1,18,440 3,18,440 4,51;2004 1,14,400 97,240 4,33,240 5,48,4405 84,490 19,880 - -5 24,850 29,820 5,42,580 5,98,140

Outflows 5,00,000 5,80,000Since at the end of year 4, the cumulative discounted cash inflows are less than the outflows and at the end of year 5, the cumulative discounted cash inflows exceed the respective out flows, the payback period are between year4 and year for both the machines. The exact payback period may be calculated as follows: A 4 Years + (66,760/1,09,340)= 4.61 years B 4 Years + (31,560/49,700) = 4.64 years Calculation of Desirability Factor (PI) :

PI = PV of cash inflows/PV of cash outflows A 5,42,580/5,00,000= 1.085 B 5,98,140/5,80,000= 1.031

Relative Position : A B NPV Rs.42,580 Rs.18,140Discounted Payback (Years) 4.61 4.64

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 15

Desirability Factor (PI) 1.085 1.031 Machine A seems to be better as per all the three criteria applied. Therefore, the firm should select machine A.

Solution: 23 Hint: Conclusion: Machine Zen Machine Ben Choice 1.NPV 12.35 13.58 Ben 2.Protitability Index 1.494 1.339 Zen 3.Payback Period 3 years 3 years Indifferent 4.Discounted Payback 3.614 years 3.629 years Zen Because of rising demand of Company's product, Machine Ben should be the choice as it has higher capacity and its NPV is also higher. Solution 24:

Cash outflows Cost of new equipment Add: Shifting expenses Less: Tax benefit Less: Sale proceeds of sold equipment

Incremental cash outflows

Rs. 30,000

10,500

Rs. 3,00,000

19,500 (5,000)

3,14,500 Determination of CFAT and NPV

Particulars Year 1 Year 2 Year 3 Year 4 Cash operating savings

Less: Incremental depreciation Taxable earnings (incremental)

Less: Taxes (0.35) Earnings after taxes (EAT) CFAT (EAT + Depreciation) X PVF (0.15) PV

Total present value Less: Cash outflows

NPV

Rs. 90,000 73,750 16,250 5,687

10,563 84,313 0.870

73,352

Rs. 1,50,000 55,312 94,688 33,141 61,547

1,16,859 0.756

88,345

Rs. 1,50,000 41,484

1,08,516 37,981 70,535

1,12,019 0.658

73,709

Rs. 1,50,000 31,113

1,18,887 41,610 77,277

1,08,390 0.572

61,999 2,97,405 3,14,500 (17,095)

Recommendation: The company should reject the proposal as the NPV is negative.

Working Note: Depreciation base of new equipment:

WDV of existing equipment Add: Cost of new equipment Less: Sale proceeds of existing equipment

Amount of equipment on which depreciation will be charged Less: WDV of existing equipment

Base of incremental depreciation

Rs. 20,000

3,00,000 5,000

3,15,000 20,000 2,95,000

Solution 25 Per annum production per machine = 3,750 units ( i.e. 2500 for six months + 1250 for six months) Total sales per annum =7,500 units Cost saving per annum = 7,500 x 3 = Rs 22,500 Cash flows if new machines are purchased Cash outflow = 60,000 Cash inflows (infinite stream) =22,500 P.V. of cash inflows @ 12% = 22,500 / 0.12

=1,87,500 P.V. of cash outflow = 60,000 N.P.V. of the option = 1,27,500 Hence new machines should be purchased

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 16

Solution 26

Replace Now or at Y0 Replace After three years or at Y3

Cash Flow (Y) Time Amount Cash Flow: Amount

0 3,00,000-60,000 = (2,40,000) 1 1,50,000 2 1,30,000 3 1,20,000 4 1,00,000 5 80,000+20,000 = 1,00,000

0 1 2 3[50,000+40,000- 3lac ]

4 5 6 7 8 [80,000+20,000]

Nil 70,000 60,000

(2,10,000) 1,50,000 1,30,000 1,20,000 1,00,000 1,00,000

PV @ 10 % = 2,24,353 ENPV 2,24,353/3.791 = 59,180

PV @ 10 % = 3,04,322 ENPV 3,04,322/5.335 = 57,043

Machine should be replaced now as it has higher ENPV. Clarification: New machine will be available at same cost and

generate same revenue if replacement takes place after three years.

Solution 27: Statement showing Annualized PV of Cash Outflow in case of Replacement of Existing Machine

Particular

Year

PV factor

at 15%

Replace Now Replace After a Year

Replace After 2 years

Amount PV Amount PV Amount PV .Purchase Price New Machinery Salvage Value of Old Machine Overhaul of Old Machine COAT of New Machine

PV of cash outflow Annuity Factor for 10/11/12 years Annualized PV of Cash Outflow

0 1 2

0

1

5 6 7 8 9 10

1

0.870 0.756

1

0.870

0.497 0.432 0.376 0.327 0.284 0.247

4,00,000 ……….

…….. (80,000)

……

1,00,000

2,00,000

4,00,000

……. ……

(80,000)

……

49,700

65,400

……..

4,00,000 ……

……

……

…..

1,00,000

2,00,000

……….

3,48,000 ………

……

……

…..

43,200

56,800

…….. ……..

4,00,000

……

90,000

……

1,00,000

2,00,000

………

…… 3,02,400

……

78,300

…..

37,600

49,400 4,35,100

5.019

4,48,000 5.234

4,67,700 5.421

86,691 85,594 86,276

Recommendation: Existing Machine should be replaced after a year because it has lowest annualized present value of cash outflow (.e. Rs. 85,594). Solution 28: (b) Statement showing Present Value of cash inflow of new machine when it replaces elderly machine now: Cash inflow of a new machine per year Cumulative present value for 1-3 yrs @ 10% Present value of cash inflow for 3 yrs (80,000 x 2.486) Less: Cash outflow – Purchase cost of new machines 1,50,000

Rs. 80,000

2.486 1,98,880

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 17

Less: Salvage value of old machine 80,000 NPV of cash inflow for 3 years

70,000 1,28,880

Equivalent annual cash inflow of new machine =

Statement Showing Present Value of cash inflow of new machine when it replaces elderly machine next year: Cash inflow of a new machine per year Cumulative P.V. for 1-3 yrs @ 10% P.V. of cash inflow for 3 yrs (80,000 x 2.486) Less: Cash outflow – Purchase cost of new machine 1,50,000 Less: Salvage value of old machine 70,000 N.P.V. of cash inflow for 3 years

Rs. Rs. 80,000

2.486 Rs. 1,98,880

Rs. 80,000 Rs. 1,18,880

Equivalent annual cost inflow of new machine =

Advice: Since the equivalent annual cash inflow of new machine now & next year is more than cash inflow (Rs. 40,000) of an elderly machine, the Co. Y need not wait for the next year to replace the elderly machine since the equivalent annual cash inflow is more than the next years cash inflow.

Solution: 29 The incremental cash flows( both projects have even lives) of the replacement decision may be ascertained as follows:

(i) Initial cash flow: Cost of New machine Rs. 2,50,000 Less Scrap value of old (50,000) Net outflow 2,00,000

(ii) Subsequent cash inflows (Annual): Savings in Operating cost (A) Rs. 60,000 Depreciation on New machine (2,50,000 – 25,000) ÷ 9 25,000 Depreciation on Old machine (90,000 ÷ 9) 10,000 Incremental Depreciation (B) (15,000) Increase in Profit before tax (A – B) 45,000 - Tax@ 50% (22,500) Profit After Tax 22,500 Depreciation added back 15,000 Annual Cash Saving (Benefit) After Tax 37,500

(iii) Terminal cash inflow: Scrap Value of New Rs. 25,000

Calculation of Net Present Value Year Cash flows PV Factor PV (Rs.)

0 1-9 9

Rs. 2,00,000 Rs. 37,500 Rs. 25,000

1.0 PVAF(10%,9) = 5.759

0.424 NPV

Rs. -2,00,000 215963 10,600 26563

The Proposal has Positive NPV, hence machinery should be replaced.

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 18

Solution 30: In this case, the cost of replacement i.e. Rs. 4,000 is to be evaluated against the expected savings in fuel expenses over a period of 5 years as follows:

Year Fuel Bill With 5 %

inflation

Saving @ 10%

PVF(14%,n) PV of Saving

1 2 3 4 5

. 10,500 11,025 11,576 12,155 12,763

1,050 1,103 1,158 1,216 1,276

.877

.769

.675

.592

.519

Total PV of Savings - Cost of replacement

NPV

921 848 781 720 662

3,932

(4,000) ( 68)

Heating System should not be replaced. It is assumed that cool limited will have no additional depreciation advantage. Tax aspect is ignored.

Solution: 31 Since both the options have different life spans; decision should be made on the basis of Equivalent or Annual operating cost. Option I: To repair the existing machine-:

Present value of cash outflows Cost of repairs net of tax [Rs. 13,000 x (1-.4) ] Rs. 7,800 Running cost for 5 years [Rs.22,000(1-.4) x 3.791) 50,041 Total Cost after tax for 5 years 57,841

Equivalent or anuual operating cost (Rs. 57,841/3.791) 15,257 Option II: To Buy a new machine:

Present value of cash outflows Purchase cost new machine Rs. 60,000 -Sale proceeds of old machine 6,000 Rs. 54,000 Annual Running cost [12000(1-.4)] 7,200 Less: Tax benefit on depreciation p.a. - (Rs. 60,000/10) x 40% -2,400 4,800 Net cash outflows for 10 years (Rs. 4,800 x 6.145) 29,496 Total Cost after tax for 10 years 83,496 Equivalent or annual operating cost (Rs. 83,496/6.145) 13,588

Equivalent or annual cash outflows for buying a new machine is less than equivalent outflows on repairing old machine. Therefore, it is advisable that the company should go for buying a new machine. Solution 32. The computation of NPV by using Decision Tree.

Time: 0 Year 1 Expected PV

CFAT x Prob. Rs. 60,000

Rs. 2,00,000 Rs.

3,60,000 6,20,000

3,00,000 NPV = 3,20,000

Rs. 40,000

Rs. 80,000 Rs.

1,40,000 2,60,000

Nil

NPV 2,60,000

Less Cash outflowNPV

Cash outflow

Cash outflow Ni.

0.2 Rs. 2,00,000

0.4 Rs. 2,00,000

0.4 Rs. 2,00,000

0.2 Rs. 3,00,000

0.4 Rs. 5,00,000

0.4 Rs. 9,00,000

Probabilities PV of CFAT

Less: Cash out flowWithout exp.

With expansion

Decisiontree

Less Cash outflow

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 19

Solution 33.

1. (i) = 1.00 lakh components annual requirement to justify for semi-automatic machine. (ii) = 1.50 lakh components annual requirement to justify for semi-automatic machine. 2.

Semi-automatic Automatic Savings in variable Cost 30 – 12 = 18 x 5 lakhs units 90 lakhs Less: fixed costs 18 lakhs Net savings Rs. 72 lakhs

30 – 1- = 20 x 5 lakh units = 100 lakhs

30 lakhs Rs. 70 lakhs

Semi-automatic machine is advised in case of annual requirement of 5 lakh units 3. = 6 lakhs units volume is required to select automatic machine. Solution 34. DO = Rs. 15 i.e. D1 = 15 + 12% = 16.80 (i) If Project is financed by Retained Earnings = Kr = Ke =

= = 0.2133 i.e. 21.33% Cost of Retained earnings: Kr = 21.33% P.V. of annual cash inflow of Rs. 10 lakhs for 3 years At 21% = 10 lakhs x 2.074 = 20.74 lakhs Less: Investment = 20.00 lakhs NPV = 0.74 lakhs

(ii) Flotation cost of 5%

Ke = =

= = 0.2182 i.e., 21.82% P.V. of annual cash inflow of Rs. 10 lakhs for 3 years At 22% = 10 lakhs x 2.0422 = Rs. 20.42 lakhs Less: Investment = Rs. 20.00 lakhs NPV = Rs. 0.42 lakhs

Illustration (on consideration of Risk in Capital Budgeting): A company is considering two mutually exclusive projects X and Y. Project x costs Rs. 30,000 and Project Y Rs. 36,000. You have been given below the net present value probability distribution for each project:

Project X Project Y NPV Estimate (Rs.) Probability NPV Estimate (Rs.) Probability

3,000 6,000 12,000 15,000

0.1 0.4 0.4 0.1

3,000 6,000 12,000 15,000

0.2 0.3 0.3 0.2

(i) Compute the expected net present value of Projects X and Y. (ii) Compute the risk attached to each project i.e., Standard Deviation of each probability distribution. (iii) Which project do you consider more risky and why? (iv) Compute the probability(profitability) index of each project.

Financial Management Practicals: Capital Budgeting 20/07/2019

Ranker’s Classes Page 20

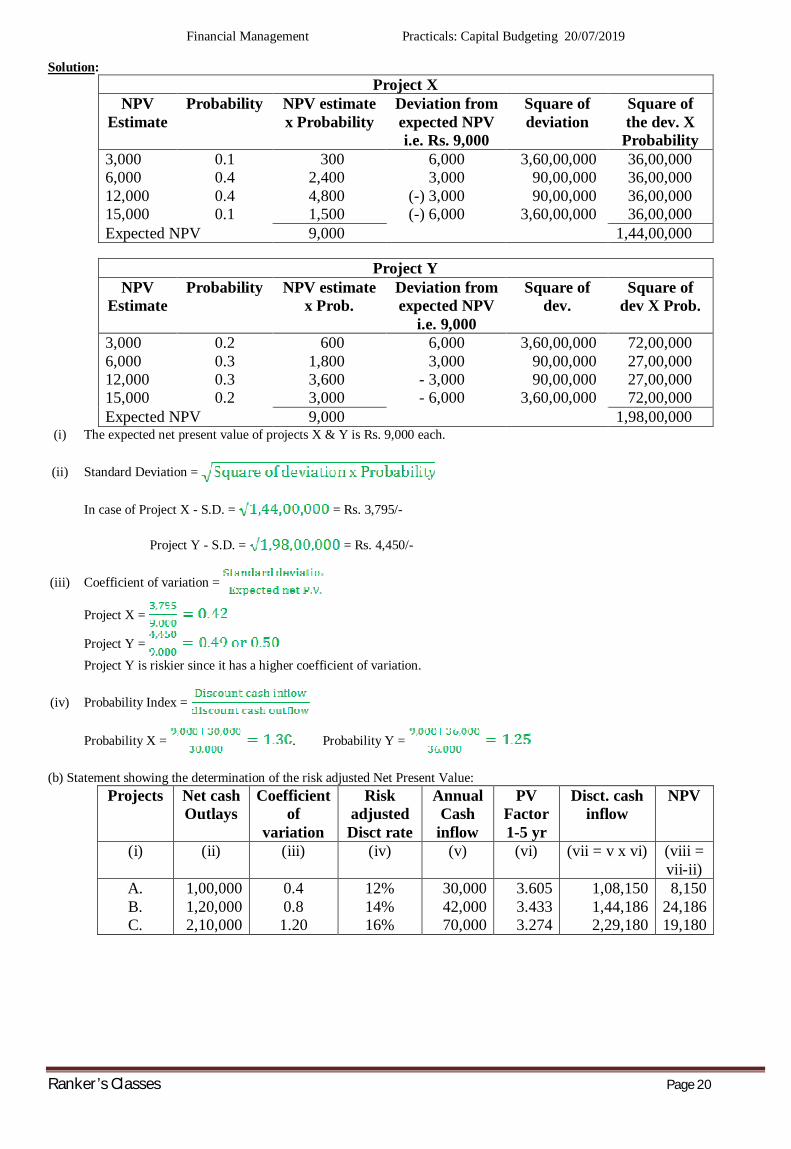

Solution: Project X

NPV Estimate

Probability NPV estimate x Probability

Deviation from expected NPV i.e. Rs. 9,000

Square of deviation

Square of the dev. X

Probability 3,000 6,000 12,000 15,000

0.1 0.4 0.4 0.1

300 2,400 4,800 1,500

6,000 3,000

(-) 3,000 (-) 6,000

3,60,00,000 90,00,000 90,00,000

3,60,00,000

36,00,000 36,00,000 36,00,000 36,00,000

Expected NPV 9,000 1,44,00,000

Project Y NPV

Estimate Probability NPV estimate

x Prob. Deviation from expected NPV

i.e. 9,000

Square of dev.

Square of dev X Prob.

3,000 6,000 12,000 15,000

0.2 0.3 0.3 0.2

600 1,800 3,600 3,000

6,000 3,000

- 3,000 - 6,000

3,60,00,000 90,00,000 90,00,000

3,60,00,000

72,00,000 27,00,000 27,00,000 72,00,000

Expected NPV 9,000 1,98,00,000 (i) The expected net present value of projects X & Y is Rs. 9,000 each.

(ii) Standard Deviation =

In case of Project X - S.D. = = Rs. 3,795/-

Project Y - S.D. = = Rs. 4,450/-

(iii) Coefficient of variation =

Project X =

Project Y = Project Y is riskier since it has a higher coefficient of variation.

(iv) Probability Index =

Probability X = . Probability Y =

(b) Statement showing the determination of the risk adjusted Net Present Value: Projects Net cash

Outlays Coefficient

of variation

Risk adjusted Disct rate

Annual Cash

inflow

PV Factor 1-5 yr

Disct. cash inflow

NPV

(i) (ii) (iii) (iv) (v) (vi) (vii = v x vi) (viii = vii-ii)

A. B. C.

1,00,000 1,20,000 2,10,000

0.4 0.8 1.20

12% 14% 16%

30,000 42,000 70,000

3.605 3.433 3.274

1,08,150 1,44,186 2,29,180

8,150 24,186 19,180