capital budgeting problem

TRANSCRIPT

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-2

Profitability Index (PI) or Benefit-Cost

Ratio (B/C Ratio)

The profitability index/present value index measures the present

value of returns per rupee invested. It is obtained dividing

the present value of future cash inflows (both operating

CFAT and terminal) by the present value ofcapital cash outflows.

The proposal will be worth accepting if the PI exceeds one.

Profitability IndexPresent value cash inflows

Present value of cash outflows=

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-3

Example 8

When PI is greater than, equal to or less than 1, the net present value is

greater than, equal to or less than zero respectively. In other words, the

NPV will be positive when the PI is greater than 1; will be negative when the

PI is less than one. Thus, the NPV and PI approaches give the same results

regarding the investment proposals.

The selection of projects with the PI method can also be done on the basis

of ranking. The highest rank will be given to the project with the highest PI,

followed by others in the same order.

In Example 4 (Table 3) of machine A and B, the PI would be 1.22 for machine

A and 1.27 for machine B:

PI (Machine A) =Rs 69,645

= 1.24Rs 56,125

PI (Machine B) =Rs 71,521

= 1.27Rs 56,125

Since the PI for both the machines is greater than 1, both the machines are

acceptable.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-4

EVALUATION TECHNIQUES

(1) Traditional Techniques

(i) Average rate of return method

(ii) Pay back period method

(2) Discounted Cashflow (DCF)/Time-Adjusted (TA)

Techniques

(i) Net present value method

(ii) Internal rate of return method

(iii) Profitability index

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-5

Average Rate of Return Method

The ARR is obtained dividing annual average profits after

taxes by average investments.

Average investment = 1/2 (Initial cost of machine ± Salvage

value) + Salvage value + net working

capital.

Annual average profits after taxes = Total expected after tax

profits/Number of years

The ARR is unsatisfactory method as it is based on

accounting profits and ignores time value of money.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-6

Example 4

Determine the average rate of return from the following data of twomachines, A and B.

Particulars Machine A Machine B

CostAnnual estimated incomeafter depreciation andincome tax:

Year 12345

Estimated life (years)Estimated salvage value

Rs 56,125

3,3755,3757,3759,375

11,37536,875

53,000

Rs 56,125

11,3759,3757,3755,3753,375

36,8755

3,000

Depreciation has been charged on straight line basis.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-7

Solution

ARR = (Average income/Average investment) × 100.

Average income of Machines A and B =(Rs 36,875/5) = Rs 7,375.

Average investment = Salvage value + 1/2 (Cost of machine ± Salvage

value) = Rs 3,000 + 1/2 (Rs 56,125 ± Rs 3,000) = Rs 29,562.50.

ARR (for machines A and B) = (Rs 7,375/Rs 29,562.50) × 100 = 24.9

per cent.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-8

Pay Back Method

The pay back method measures the number of years required for the CFAT

to pay back the initial capital investment outlay, ignoring interest

payment. It is determined as follows

(i) In the case of annuity CFAT: Initial investment/Annual CFAT.

(ii) In the case of mixed CFAT: It is obtained by cumulating CFAT till the

cumulative CFAT equal the initial investment.

Original/initial Investment (outlay) is the relevant cash outflow for a

proposed project at time zero (t = 0).

Annuity is a stream of equal cash inflows.

Mixed Stream is a series of cash inflows exhibiting any pattern other than

that of an annuity.

Although the pay back method is superior to the ARR method in that

it is based on cash flows, it also ignores time value of money

and disregards the total benefits associated with the investment proposal.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-9

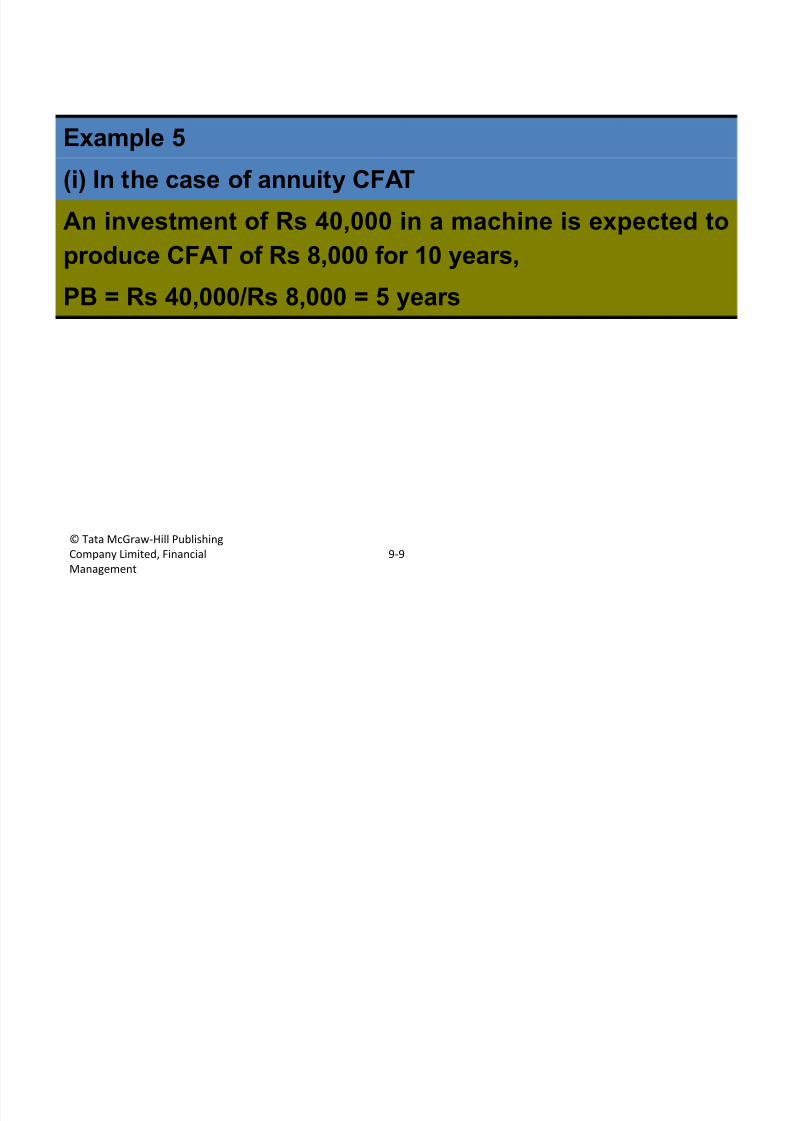

Example 5

(i) In the case of annuity CFAT

An investment of Rs 40,000 in a machine is expected to

produce CFAT of Rs 8,000 for 10 years,

PB = Rs 40,000/Rs 8,000 = 5 years

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-10

(ii) In the case of mixed CFAT

Table 2 presents the calculations of pay back period for Example 4.

Table 2

Year Annual CFAT Cumulative CFAT

A B A B

1

2

3

4

5

Rs 14,000

16,000

18,000

20,000

25,000*

Rs 22,00

0

20,000

18,000

16,000

17,000*

Rs 14,000

30,000

48,000

68,000

93,000

Rs 22,000

42,000

60,000

76,000

93,000

* CFAT in the fifth year includes Rs.3,000 salvage value also.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-11

Discounted Cashflow (DCF)/Time-Adjusted

(TA) Techniques

The DCF methods satisfy all the attributes of a good measure of

appraisal as they consider the total benefits (CFAT) as well as the

timing of benefits.

The present value or the discounted cash flow procedure

recognises that cash flow streams at different time periods differ in

value and can be compared only when they are expressed in terms

of a common denominator, that is, present values. It, thus, takes into

account the time value of money. In this method, all cash flows are

expressed in terms of their present values.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-12

The present value of the cash flows inExample 4 are illustrated in Table 3.

Table 3: Calculations of Present Value of CFAT.

Year Machine A Machine B

CFAT PV

factor

(0.10)

Present

value

CFAT PV

factor

(0.10)

Present

value

1 2 3 4 5 6 7

1

2

3

4

5

Rs 14,000

16,000

18,000

20,000

25,000*

0.909

0.826

0.751

0.683

0.621

Rs 12,726

13,216

13,518

14,660

15,525

69,645

Rs 22,000

20,000

18,000

16,000

17,000*

0.909

0.826

0.751

0.683

0.621

Rs 19,998

16,520

13,518

10,928

10,557

71,521

*includes salvage value.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-13

Net Present Value (NPV) Method

Net Present ValueCFt

(1+k)t=Sn + Wn

(1+k)n

COt

(1+k)t+ -

n

t=1

n

t=1

The NPV may be described as the summation of the present values of

(i) operating CFAT (CF) in each year and (ii) salvages value(S) and

working capital(W) in the terminal year(n) minus the summation

of present values of the cash outflows(CO) in each year. The present value

is computed using cost of capital (k) as a discount rate.

The decision rule for a project under NPV is to accept the project if the NPV

is positive and reject if it is negative. Symbolically,

(i) NPV > zero, accept, (ii) NPV < zero, reject

Zero NPV implies that the firm is indifferent to accepting or rejecting the

project.

The project will be accepted in case the NPV is positive.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-14

Example 6

In Example 4 we would accept the proposals of purchasing machines A and

B as their net present values are positive. The positive NPV of machine A is

Rs 13,520 (Rs 69,645 ± Rs 56,125) and that of B is Rs 15,396 (Rs 71,521 ± Rs

56,125).

In Example 4, if we incorporate cash outflows of Rs 25,000 at the end of the

third year in respect of overhauling of the machine, we shall find the

proposals to purchase either of the machines are unacceptable as their net

present values are negative. The negative NPV of machine A is Rs 6,255 (Rs

68,645 ± Rs 74,900) and of machine B is Rs 3,379 (Rs 71,521 ± Rs 74,900).

As a decision criterion, this method can also be used to make a choice

between mutually exclusive projects. On the basis of the NPV method, the

various proposals would be ranked in order of the net present values. The

project with the highest NPV would be assigned the first

rank, followed by others in the descending order. If, in our example, a

choice is to be made between machine A and machine B on the basis of the

NPV method, machine B having larger NPV (Rs 15,396) would be preferred

to machine A (NPV being Rs 12,520).

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-15

Internal Rate of Return (IRR) Method

The IRR is defined as the discount rate (r) which equates the

aggregate present value of the operating CFTA received each year

and terminal cash flows (working capital recovery and salvage

value) with aggregate present value of cash outflows of an

investment proposal.

The project will be accepted when IRR exceeds the

required rate of return.

Internal Rate of

Return

CFt

(1+r)t=Sn + Wn

(1+r)n

COt

(1+r)t+ -

n

t=1

n

t=1

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-16

The following steps are taken in determining IRR for an annuity.

Determine the pay back period of the proposed investment.

In Table A-4 (present value of an annuity) look for the pay back

period that is equal to or closest to the life of the project.

In the year row, find two PV values or discount factor (DFr) closest to

PB period but one bigger and other smaller than it.

From the top row of the table, note interest rate (r) corresponding to

these PV values (DFr).

IRR for an Annuity

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-17

Determine actual IRR by interpolation. This can be done either directly using

Equation 1 or indirectly by finding present values of annuity (Equation 2).

IRR = r -PB ± DFr

(Equation 1)DFrL - DFrH

Where PB = Pay back period

DFr = Discount factor for interest rate r.

DFrL= Discount factor for lower interest rate

DFrH = Discount factor for higher interest rate.

r = Either of the two interest rates used in the formula

Alternatively, IRR = r -PVco ± PVCFAT

× ̈ r (Equation 2)¨PV

Where PVCO = Present value of cash outlay

PVCFAT = Present value of cash inflows (DFr x annuity)

r = Either of the two interest rates used in the formula

¨ r = Difference in interest rates

¨ PV = Difference in calculated present values of inflows

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-18

Example 7

A project costs Rs 36,000 and is expected to generate cash inflows

of Rs 11,200 annually for 5 years. Calculate the IRR of the project.

Solution

(1) The pay back period is 3.214 (Rs 36,000/Rs 11,200)

(2) According to Table A-2, discount factors closest to 3.214 for 5

years are 3.274 (16 per cent rate of interest) and 3.199 (17 per cent

rate of interest). The actual value of IRR which lies between 16 per

cent and 17 per cent can, now, be determined usingEquations 1 and

2.

Substituting the values in Equation 1 we get: IRR = [(3.274-

3.214)/(3.274-3.199)] = 16.8 per cent.

Alternatively (starting with the higher rate), IRR = 17 ± [(3.214-

3.199)/(3.274-3.199)] = 16.8 per cent.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-19

Instead of using the direct method, we may find the actual IRR by applying

the interpolation formula to the present values of cash inflows and

outflows (Equation 2). Here, again, it is immaterial whether we start with

the lower or the higher rate.

PVCFAT (0.16) = Rs 11,200 × 3.274 = Rs 36,668.8

PVCFAT (0.17) = Rs 11,200 × 3.199 = Rs 35,828.8

IRR = 16 +36,668.8 ± 36,000

× 1 = 16.8 %36,668.8 ± 35,828.8

Alternatively (starting with the

higher rate), IRR = r -

(PVCO ± PVCFAT)× ¨ r

¨ PV

IRR = 17 -36,000 ± 35,828.8

× 1 = 16.8 %840

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-20

Profitability Index (PI) or Benefit-Cost

Ratio (B/C Ratio)

The profitability index/present value index measures the present

value of returns per rupee invested. It is obtained dividing

the present value of future cash inflows (both operating

CFAT and terminal) by the present value ofcapital cash outflows.

The proposal will be worth accepting if the PI exceeds one.

Profitability IndexPresent value cash inflows

Present value of cash outflows=

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-21

Example 8

When PI is greater than, equal to or less than 1, the net present value is

greater than, equal to or less than zero respectively. In other words, the

NPV will be positive when the PI is greater than 1; will be negative when the

PI is less than one. Thus, the NPV and PI approaches give the same results

regarding the investment proposals.

The selection of projects with the PI method can also be done on the basis

of ranking. The highest rank will be given to the project with the highest PI,

followed by others in the same order.

In Example 4 (Table 3) of machine A and B, the PI would be 1.22 for machine

A and 1.27 for machine B:

PI (Machine A) =Rs 69,645

= 1.24Rs 56,125

PI (Machine B) =Rs 71,521

= 1.27Rs 56,125

Since the PI for both the machines is greater than 1, both the machines are

acceptable.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-22

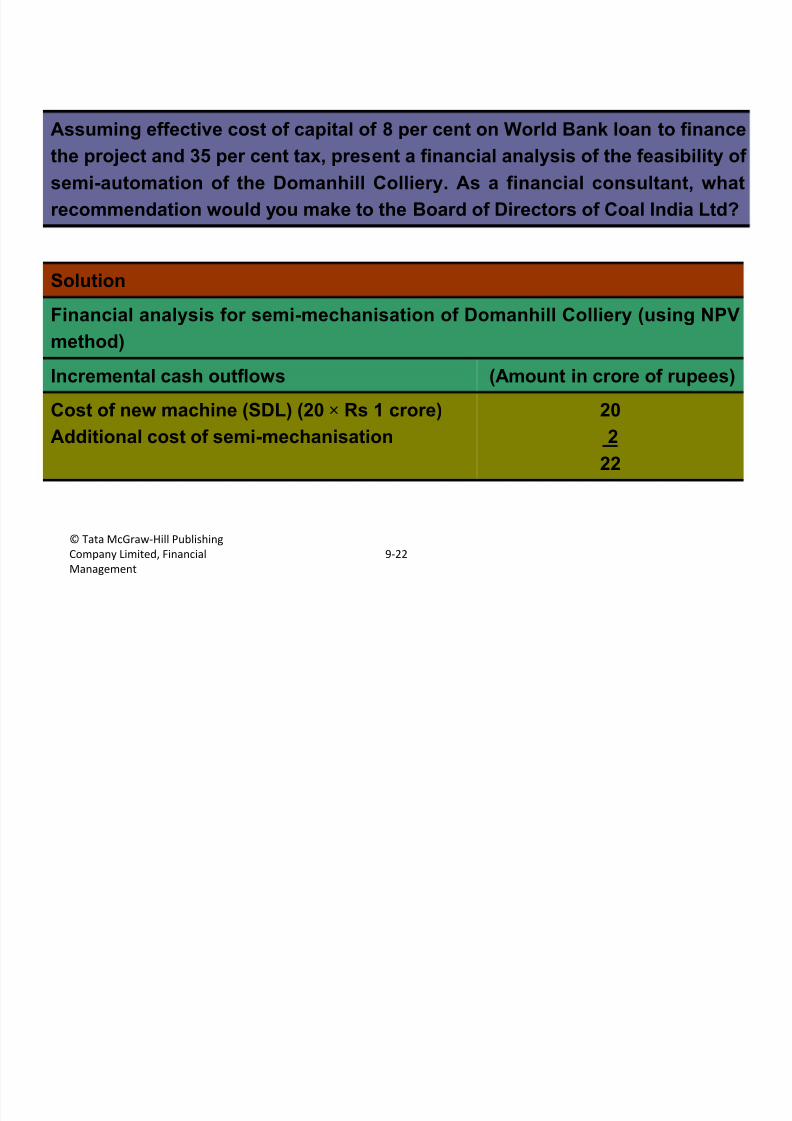

Assuming effective cost of capital of 8 per cent on World Bank loan to finance

the project and 35 per cent tax, present a financial analysis of the feasibility of

semi-automation of the Domanhill Colliery. As a financial consultant, what

recommendation would you make to the Board of Directors of Coal India Ltd?

Solution

Financial analysis for semi-mechanisation of Domanhill Colliery (using NPV

method)

Incremental cash outflows (Amount in crore of rupees)

Cost of new machine (SDL) (20 × Rs 1 crore)

Additional cost of semi-mechanisation

20

2

22

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-23

Nature

Capital Budgeting is the process of evaluating and selecting

long-term investments that are consistent with the goal of

shareholders (owners) wealth maximisation.

Capital Expenditure is an outlay of funds that is expected to

produce benefits over a period of time exceeding one year.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-24

Such decisions are of paramount importance as they affect the

profitability of a firm, and are the major determinants of its efficiency

and competing power. While an opportune investment decision can

yield spectacular returns, an ill-advised/incorrect decision can

endanger the very survival of a firm.

Capital expenditure decisions are beset with a number of difficulties.

The two major difficulties are:

(1) The benefits from long-term investments are received in some

future period which is uncertain. Therefore, an element of risk is

involved in forecasting future sales revenues as well as the

associated costs of production and sales.

(2) It is not often possible to calculate in strict quantitative terms all

the benefits or the costs relating to a specific investment

decision.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-25

Capital budgeting decisions are of two

types

Such types of decisions are subject to less risk as the potential

cash saving can be estimated better from the past production

and cost data.

It is more difficult to estimate revenues and costs of a newproduct line.

(1) Investment Decisions Affecting Revenues

(2) Investment Decisions Reducing Costs

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-26

Capital Budgeting Process

Capital Budgeting Process includes four distinct but interrelated steps used to evaluate

and select long-term proposals: proposal generation, evaluation, selection and follow

up.

Accept-reject Decision

Accept reject decision/approval is the evaluation of capital expenditure

proposal to determine whether they meet the minimum acceptance

criterion.

Mutually Exclusive Project Decisions

Mutually exclusive projects (decisions) are projects that compete with oneanother; the acceptance of one eliminates the others from further consideration.

Capital Rationing Decision

Capital rationing is the financial situation in which a firm has only fixedamount to allocate among competing capital expenditures.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-27

Cash Flows Vs. Accounting Profit

The capital outlays and revenue benefits associated with such

decisions are measured in terms of cash flows after taxes. The cash

flow approach for measuring benefits is theoretically superior to the

accounting profit approach as it

(i) Avoids the ambiguities of the accounting profits concept,

(ii) Measures the total benefits and

(iii) Takes into account the time value of money.

The major difference between the cash flow and the accounting profit

approaches relates to the treatment of depreciation. While the

accounting approach considers depreciation in cost computation, it

is recognised, on the contrary, as a source of cash to the extent of tax

advantagein the cash flow approach.

© Tata McGraw-Hill Publishing

Company Limited, Financial

Management

9-28

Treatment of Depreciation

For taxation purposes, depreciation is charged (on the basis of written

down value method) on a block of assets and not on an individual asset. A

block of assets is a group of assets (say, of plant and machinery)

in respect of which the same rate of depreciation is prescribed by the

Income-Tax Act.

Depreciation is charged on the year-end balance of the block which is

equal to the opening balance plus purchases made during the year (in the

block considered) minus sale proceeds of the assets during the year.

In case the entire block of assets is sold during the year (the block ceases

to exist at year-end), no depreciation is charged at the year-end. If the sale

proceeds of the block sold is higher than the opening balance, the

difference represents short-term capital gain which is subject to tax.

Where the sale proceeds are less than the opening balance, the firm

is entitled to tax shield on short-term capital loss. The adjustment related

to the payment of taxes/tax shield is made in terminal cash inflows of the

project.