capital budgeting full clear

TRANSCRIPT

1

A SUMMER INTERNSHIP

CAPITAL BUDGTING

INDIAN OIL CORPORATION LIMITED

PUNJAB TECHNICAL

K.C COLLEGE OF ENGINEERING $ IT ,

NAWANSHAHR,PUNJAB.

IN PARTIAL FULFILMENT OF TWO

MASTER OF BUSINESS ADMINISTRATION

UNDER THE GUIDANCE OMR.PANKAJ KUMAR MEEN

(CHARTERED ACCOUNTANT)

SUBMITTED TO:-(H.O.D)

MR.SACHIN VERMA

A SUMMER INTERNSHIP PROJECT REPORT

ON

CAPITAL BUDGTING

AT

INDIAN OIL CORPORATION LIMITED

PUNJAB TECHNICAL UNIVERSITY

K.C COLLEGE OF ENGINEERING $ IT ,

NAWANSHAHR,PUNJAB.

AL FULFILMENT OF TWO YEAR FULL TIME COURSE

MASTER OF BUSINESS ADMINISTRATION

(FINANCE)

UNDER THE GUIDANCE OF SUBMITTED BYMR.PANKAJ KUMAR MEENA AKHILESH KUMAR

T) ROLL NO 1315536

PROJECT REPORT

INDIAN OIL CORPORATION LIMITED

YEAR FULL TIME

SUBMITTED BYKUMAR

ROLL NO 1315536

2

PREFACE

In today‘s era of globalization and competition, coping up with technological advancement, which is undergoing evolution at a very fast rate, holds the key to the survival and growth of any organization. Installing technology, well-equipped facilities or going for modification in the existing ones are the means to attain better performance efficiency and hence further the value addition. Indian Oil, the largest commercial enterprise of India (by sales turnover) is India‘s sole representative in Fortunes prestigious listing of world‘s 500 largest corporations, ranked 135th for the year 2007. To maintain strategic edge in the market place, Indian Oil has given importance to capital budgeting because capital investment decisions often represent the most important decisions taken by an organization, and they are extremely important, they sometimes also pose difficulties. The evaluation of projects should be performed by a group of experts who have no axe to grind. It is necessary to ensure that an impartial group scrutinizes projects and that objectivity is maintained in the evaluation process. A company in practice should take all care in selecting a method or methods of investment evaluation. The criterion selected should be a true measure of the investment‘s profitability (in terms of cash flows), and it should lead to the net increase in the company‘s wealth (that is, its benefits should exceed its cost adjusted for time value and risk). It should also be seen that the evaluation criteria do not discriminate between the investment proposals. They should be capable of ranking projects correctly in terms of profitability. The NPV method is theoretically the most desirable criterion as it is a true measure of profitability; it generally ranks projects correctly and is consistent with the wealth maximization criterion

3

ACKNOWLEDGEMENT

This training part of MBA programme taught me a lot to understand the key of success in the organization. One of them is teamwork. Teamwork is ability to work together towards a common vision. It is a fuel that allows common people to attain results. Therefore, I would like to thank all management team of Indian Oil Corporation Limited who help me to achieve this result. This project is not an individual effort but a collection of efforts by each & every member associated with it. Working with Barauni Refinery, IOCL has been an educative, interesting and motivating experience. I would hereby like to extend my gratitude to the following people without whose cooperation and help at every stage, successful completion of the project would not have been possible. It is my privilege to express my deep gratitude to Mr. Pankaj Kumar Meena(CA at IOCL) who gave me such a great opportunity & infrastructure to do this project and also for his kind cooperation & help throughout the project. I would like to express my profound gratitude & a sincere thanks to Mr. Anurag Soni (SFM at IOCL), for his valuable time & educative guidance. Their constant support, innovative ideas & practical approach helped me to make the project more objective. I would also take this opportunity to thank my college K.C COLLEGE OF ENGINEERING $ IT ,NAWANSHAHR,PUNJAB. to put the theoretical inputs gathered at the institute to practice. I also feel a sense of gratitude towards Prof. SACHIN VARMA who took personal interest in the progress of this report.

4

ABSTRACT

A project work is a mandatory requirement for the Business Management Programme. This type of study aims at exposing the young prospective executive to the actual business world. This project gives me knowledge about the capital budgeting decisions of the company. Capital Budgeting decisions may be defined as the firm’s decision to invest its current funds most efficiently in the long-term assets in anticipation of an expected flow of benefits over a series of years. It is very effective way to judge a company’s investment decision prospects, as cash is like life-blood for any company. The report initially begins with the company profile, followed by the detailed analysis of company, like businesses of the company, products offered by the company, financials of the company, etc. The report involves a lot of research tounderstand what exactly capital budgeting is, why companies require research and analysis to invest funds in projects , what are the ideal situation for Investment a Company should maintain, etc. .Various tools, including financial tools, are used in this project to calculate and compare the returns.

5

CERTIFICATE

Certified that this project report titled “A study on Capital Budgeting at Indian Oil Corporation Limited” is the bonafide work of AKHILESH KUMAR

(MBA-2013-2015), student of MBA FINANCE, at K.C COLLEGE OF ENGINEERING $ IT.KARYAM ROAD,NAWANSHAHR, PUNJAB ,carried

out the research under my supervision during her internship programme. Certified further, that to the best of my knowledge the work reported herein

does not form part of any other project or dissertation on the basis of which a degree or award was confirmed on an easier occasion on this or any other

candidate.

PANKAJ KUMAR MEENA

6

CONTENTS

PARTICULARS PAGE NO.

1. - INTRODUCTION OF THE COMPANY

A) Introduction of the company 7-18

B) SWOT ANALYSIS 18-20

C) Introduction of Barauni Refinery 21-25

2. INTRODUCTION OF THE TOPIC

A. CAPITAL BUDGUTING 25-26

B. CAPITAL BUDGUTING TECHNICQUE 27

C. FINANCIAL EVALUTION 27-28

D. NET PRESENT VALLUE 28-31

E. INETRNAL RATE OF RETURN 31-37

F. CORPORATE OBJECTIVE 38-40

G. FINANCIAL OBJECTIVE 39-40

H. SUMMERY OF FINANCIAL ANALYSIS 40-42

7

INTRODUCTION 0F THE COMPANY

HISTORY OF INDIAN OIL CORPORATION LTD.

The Indian Oil Corporation Ltd. operates as the largest company in India in

terms of turnover and is the only Indian company to rank 88th in the Fortune

"Global 500" listing. The oil concern is administratively controlled by India's

Ministry of Petroleum and Natural Gas, a government entity that owns just over

90 percent of the firm. Since 1959, this refining, marketing, and international

trading company served the Indian state with the important task of reducing

India's dependence on foreign oil and thus conserving valuable foreign

exchange. That changed in April 2002, however, when the Indian government

deregulated its petroleum industry and ended Indian Oil's monopoly on crude

oil imports. The firm owns and operates seven of the 17 refineries in India,

controlling nearly 40 percent of the country's refining capacity.

8

HISTORY OF OIL INDUSTRY IN INDIA

In 1881, Assam Railway & Trading co. began laying of tracks in Assam

One day, one of the elephants wandered away, to come back with its feet smeared by slimy oil

Backtracking led to the discovery of oil in Borbhil, near present day Digboi

A Canadian driller, Willey Leove hollered at native boys, “Dig boy dig” Digboi became the birth place of India�s oil industry

In 1890s, crude oil distillated at Margherita, 16 km away from Digboi, in cast iron pans, called „Stills�

Digboi Refinery of Assam Oil Company (AOC) commissioned at its present location in 1901 with 500 bbl/day capacity

AOC nationalised and its Refining and Marketing functions merged with IOC in October, 1981

Digboi refinery is one of the oldest refinery in the world that is still working At the time of independence, India�s oil industry was fully controlled by international oil cartel

In 1956, Industrial Policy Resolution was passed, which laid the foundation of national oil industry

The resolution stated – “Oil is of vast importance in the world today. A country that does not produce its own oil is in a weak position. From the point of view of defence, the absence of oil is a fatal weakness”.

Exploration & production was put into Schedule – „A�, meaning thereby that only state would operate in this field

Soon thereafter, ONGC was formed for oil exploration and drilling

9

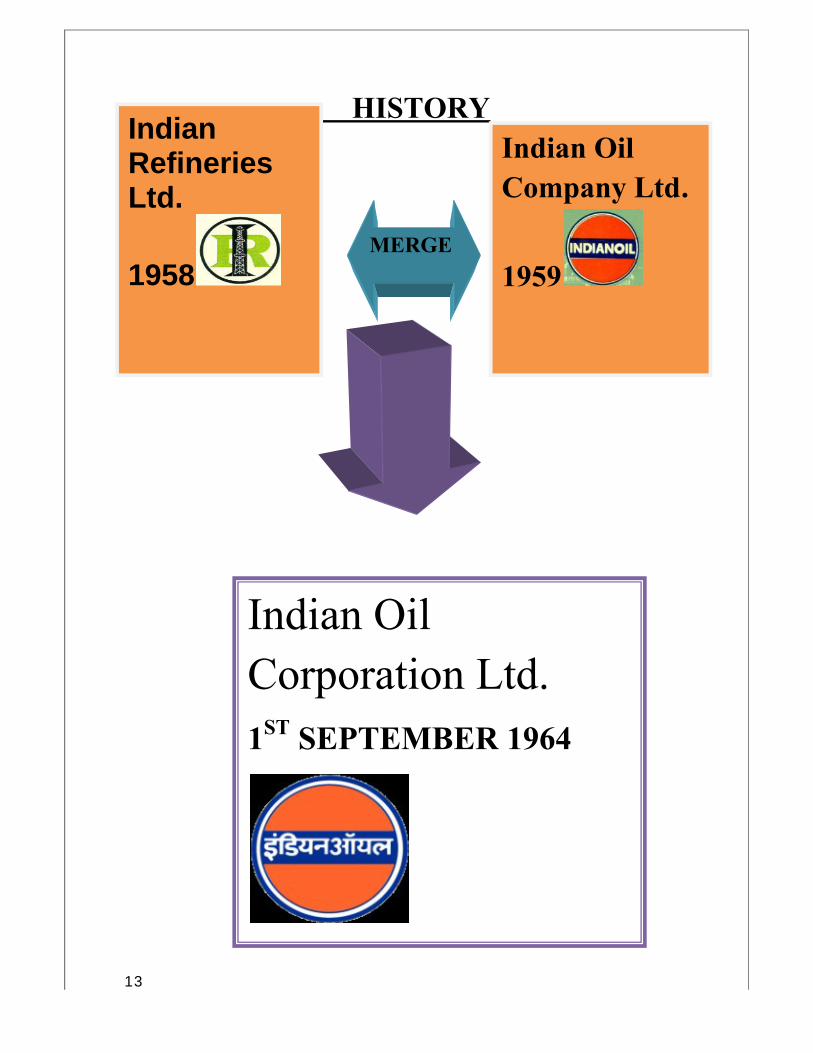

Indian Oil Refineries were formed in 1958 for refining and manufacturing of petroleum products, with Shri Feroze Gandhi as its Chairman

This was followed by the formation of Indian Oil Co. in 1959, for marketing and distribution of petroleum products

In 1960, Indian Oil Co. signed a historic agreement with soviet Union for import of 1.5 MMT of SKO, HSD, and ATF over a period of 4 years on „ rupee payment basis�. This initiated the end of to the monopoly of foreign oil companies

On 1st September 1964, as a step towards achieving improved efficiency, Indian Refineries and Indian Oil Co. were merged. Indian Oil Corporation Ltd. (IOC) was born.

10

INDIAN OIL CORPORATION LTD.

Indian Oil Corporation Ltd. (Indian Oil) was formed in 1964 through the

merger of Indian Oil Company Ltd. (Estd. 1959) and Indian Refineries Ltd. (Estd.

1958).

At Indian Oil, corporate social responsibility (CSR) has been the cornerstone

of success right from inception in the year 1964. The Corporation’s objectives in

this key performance area are enshrined in its Mission statement: "…to help

enrich the quality of life of the community and preserve ecological balance and

heritage through a strong environment conscience”

.From a fledgling company with a net worth of just Rs. 45.18 crore and sales

of 1.38 million tonnes valued at Rs. 78 crore in the year 1965, Indian Oil has

since grown over 3000 times.

Indian Oil Corporation Ltd. (Indian Oil) is India's largest commercial

enterprise, with a sales turnover of Rs. 2,47,479 crore (US $ 61.70 billion) and

profits of Rs. 6,963 crore (US $ 1.74 billion) for the year 2007-08.

Indian Oil is also the highest ranked Indian company in the prestigious

Fortune 'Global 500' listing, having moved up 19 places to the 116th position in

2008. It is also the 18th largest petroleum company in the world.

Indian Oil has ambitious investment plans of Rs. 43,250 crore in the next five

years. By 2011-12, the Indian Oil Group, with 80 MMTPA refining capacity in

its fold, would be playing a key role in realising India’s bid to emerge as an

export-oriented hub for finished products.

PRODUCTS

Indian Oil is not only the largest commercial enterprise in the country it is the

flagship corporate of the Indian Nation. Besides having a dominant market

share, Indian Oil is widely recognized as India’s dominant energy brand and

11

customers perceive Indian Oil as a reliable symbol for high quality products and

services.

Benchmarking Quality, Quantity and Service to world-class standards is a

philosophy that Indian Oil adheres to so as to ensure that customers get a truly

global experience in India.

Indian Oil is a heritage and iconic brand at one level and a contemporary, global

brand at another level. While quality, reliability and service remains the core

benefits to the customers.

Auto gas

Indian Oil Aviation Service

Bitumen

High Speed Diesel

Bulk / Industrial Fuel

Indene Gas

SERVO Lubricants & Greases

Marine Fuels & Lubricants

MS / Gasoline

Petrochemicals

12

Special Products

Superior Kerosene Oil

Crude Oil

13

HISTORYIndian Refineries Ltd.

1958

Indian Oil Company Ltd.

1959MERGE

Indian Oil Corporation Ltd.1ST SEPTEMBER 1964

14

CORPORATE STRUCTURE

CORPORATEDIVISIONS

BOARD

Finance including

International Trade / Information Systems / Optimization / Corporate Affairs

Human Resource including Corporate Communications

Planning & Business Development

Refineries (including AOD�s Digboi Refinery)

Pipelines

Marketing (including AOD�s Marketing)

R&D

15

REFINERIES DIVISION

REFINERIES HQ , NEW DELHI

TECHNICAL

PROJECTS

MATERIALS

HR Finance S & EP

M & I

REFINERIES DIGBOIGUWAHATIBARAUNIGUJARATHALDIAMATHURAPANIPATBONGAIGAON

16

MISSION OBJECTIVES AND OBLIGATIONS OF THE COMPANY

MISSION

To achieve international standards of excellence in all aspects of energy and diversified business with focus on customer delight through value of products and services, and cost reduction

To maximise creation of wealth, value and satisfaction for the stakeholders

To attain leadership in developing, adopting and assimilating state-of-the-art technology for competitive advantage

To provide technology and services through sustained Research and Development

To foster a culture of participation and innovation for employee growth and contribution

To cultivate high standards of business ethics and Total Quality Management for a strong corporate identity and brand equity

To help enrich the quality of life of the community and preserve ecological balance and heritage through a strong environment conscience.

OBJECTIVES

To serve the national interests in the oil and related sectors in accordance and consistent with Government policies.

To ensure and maintain continuous and smooth supplies of petroleum products by way of crude refining, transportation and marketing activities and to provide appropriate assistance to the consumer to conserve and use petroleum products efficiently.

To earn a reasonable rate of interest on investment. To work towards the achievement of self-sufficiency in the

field of oil refining by setting up adequate capacity and to build up expertise in laying of crude oil petroleum product pipelines.

To create a strong research and development base in the field of oil refining and stimulate the development of new

17

product formulations with a view to minimise/eliminate their imports and to have next generation products.

To maximise utilisation of the existing facilities in order to improve efficiency and increase productivity.

OBLIGATIONS

Towards customers and dealers To provide prompt, courteous and efficient service and

quality products at fair and reasonable prices

Towards suppliers To ensure prompt dealings with integrity, impartiality and

courtesy and promote ancillary industries.

Towards employees Develop their capability and advancement through

appropriate training and career planning. Fair dealings with recognised representatives of employees

in pursuance of healthy trade union practice and sound personnel policies.

18

VALUES

Care – Stands for

Concern Empathy Understanding Cooperation Empowerment

Innovation –Stands for

Creativity Ability to learn Flexibility Change

Passion - Stands for

Commitment Dedication Pride Inspiration Ownership Zeal & Zest

Trust - Stands for

Delivered Promises Reliability Dependability Integrity Truthfulness Transparency

19

SWOT ANALYSIS

STRENGTHS

HIGH FOREIGN EXCHANGE DEBT.

IOCL has managed to significantly cut its borrowing cost due to high share of foreign

exchange debt. Its share of foreign exchange borrowings is increasing with foreign exchange

loans crossing 50% of its total debt compared to 42% at the end of the last financial year.

HIGHEST MARKET SHARE

As India's flagship national oil company, Indian Oil accounts for 56% petroleum products

market share, 42% national refining capacity and 67% downstream pipeline throughput

capacity.

FOREIGN SUBSIDIARIES AND JOINT VENTURES

Indian Oil is strengthening its existing overseas marketing ventures. The Corporation has

launched eleven joint ventures (listed separately) in partnership with some of the most

respected corporate from India and abroad .

WEAKNESSES

STRINGENT CORPORATE POLICIES

The decisions relating to administration are taken at the corporate

level. Even minor proposals are to be referred to the top management.

This leads to a delay in decision-making.

LACK OF MARKETING EFFORTS

20

Among the public sector oil companies, Indian Oil Corporation is the

only one to follow a weak marketing strategy. It in only in the recent

years that the company has started to market its products. However,

still the efforts seem to be weak when compared with the competitors

like BPCL and HPCL.

PROMOTION POLICY

The employees are promoted mainly on the basis of experience and

not on the efforts and initiatives displayed by the employee in his

work. This results in demotivation and lack of interest for their work

on the part of the hardworking employees, who then tend to shift jobs

to satisfy their need for self-esteem.

OPPORTUNITIES

Exploration and Production

Indian Oil is metamorphosing from a pure sectoral company with

dominance in downstream in India to a vertically integrated,

transnational energy behemoth. The Corporation is making

investments in E&P and import/marketing ventures for oil and gas in

India and abroad, and is implementing a master plan to emerge as a

major player in petrochemicals by integrating its core refining

business with petrochemical activities.

THREATS

Entry of Big Private players

The opening up of the oil sector for private players poses a threat even

for this well-established company.

21

INTRODUCTION TO BARAUNI REFINERY

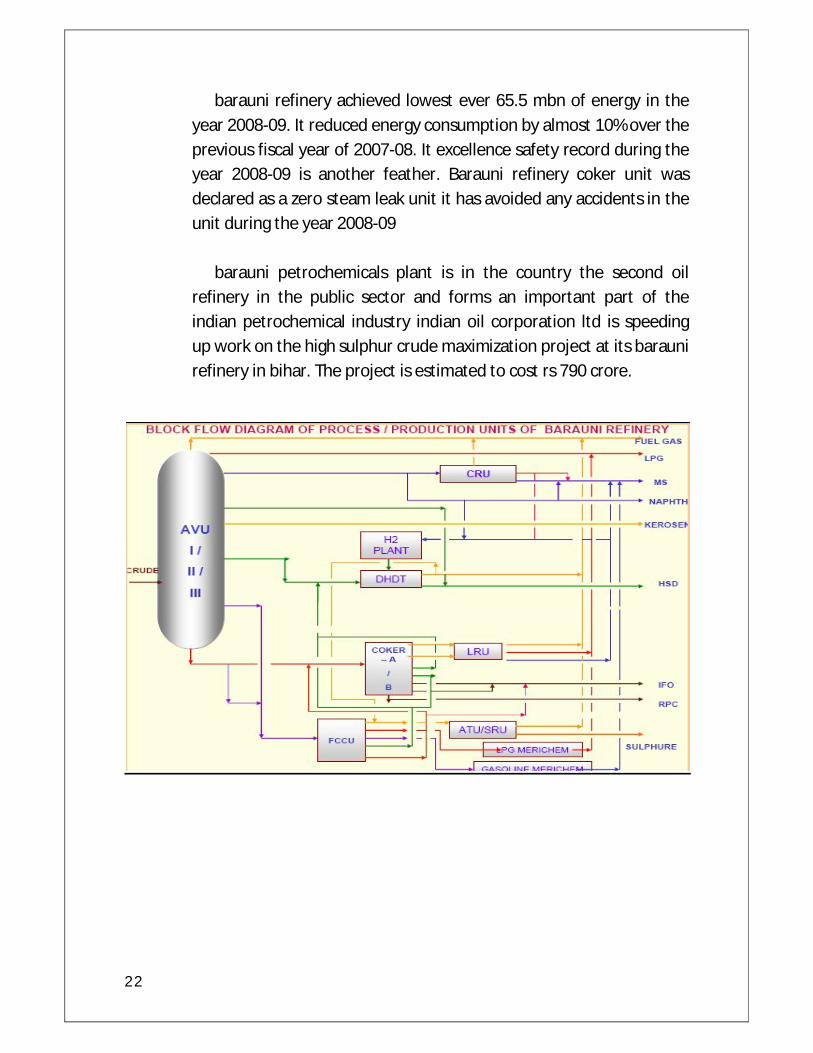

The barauni refinery in eastern india was commissioned in 1964 with a capacity of 2.0 mmtpa. The refining capacity was increased to 3.0 mmtpa by 1969 andfluidised catalytic cracker) and hydrotreater facilities for diesel quality improvement have been added. With the commissioning of the 6.0 mmtpa haldia-barauni crude oil pipeline, the refinery now received imported crude for processing. A cru (catalytic reformer unit) was also added to the refinery in 1997 for production of unleaded motor spirit. Projects are also planned for meeting future fuel quality requirements. Barauni refinery supplies distillate products beside eastern india to northern india through a product pipeline to kanpur in uttar pradesh.

The year 2008-09 saw barauni refinery achieve the highest ever-crude

throughput of 5.94 mmt, beating the previous best of 5.63 mmt, which

was achieved in 2007-08, along with sustaining the distillate yield of

more than 85% (i.e. 85.7%) year after year

22

barauni refinery achieved lowest ever 65.5 mbn of energy in the year 2008-09. It reduced energy consumption by almost 10% over the previous fiscal year of 2007-08. It excellence safety record during the year 2008-09 is another feather. Barauni refinery coker unit was declared as a zero steam leak unit it has avoided any accidents in the unit during the year 2008-09

barauni petrochemicals plant is in the country the second oil refinery in the public sector and forms an important part of the indian petrochemical industry indian oil corporation ltd is speeding up work on the high sulphur crude maximization project at its barauni refinery in bihar. The project is estimated to cost rs 790 crore.

23

FINANCIAL MISSIONS: To provide high quality financial staff support for

decision-making and control to all levels of management—corporate, divisional, unit and location to enable the achievement of overall corporate objectives and goals.

To play a lead role in scanning the domestic and international financial environment, the formulation and implementation of all financial policies and plans for different time spans consistent with and conducive to the business plans for expansion, diversification, productivity etc.

To inculcate financial awareness, cost benefit attitudes and system orientation in the entire organization.

FINANCE DIVISION

1: MAIN ACCOUNTS

For assets management, they prepare the master of assets, which includes name, cost centre and other details for capitalization of assets. Further, receiving debit, credit notes and reconciliation also form a part of this section.

2: PURCHASE

Accounting of cash purchases made by the materials department.

Arrangement for insurance of transit risk.

Maintenance of books of accounts.

Sales tax matters. 3: WORKS

Mainly deals with payment or running contracts. Its considers only plants maintenance, roads, painting, welding, water etc.

4: PAYROLL

Rules for pay and allowance are prescribed by head office from time to time. The eligibility for special type of allowance such as special allowances, shift allowance etc. is determined by personnel department

24

5: STORES AND MODVAT

Under this scheme, a manufacturer can take credit of excise duty paid on raw materials and components used by him. The normal excise duty rate is 16%. However it depends upon the Tariff class under which the product is classified.

6: TA/LTC/MEDICAL

This section also deals encashment of LTC and medical payment.

7: MISCELLANEOUS SECTION

Accounting of cash imp rest and advances for company expenses;

Passing of bills of miscellaneous nature

Miscellaneous recoveries from outsiders 8: PRODUCTION ACCOUNTING

Crude oil quantity and value accounting for the receipts, consumption and stock.

Accounting of consumptions of own fuel/products.

Valuation of closing stocks i.e. Raw Material, ISD, Finished Goods

Preparation of Cost Sheet and Cost Audit Performa

Monitoring of Revenue Budget, Preparation of Revenue Budget.

9: CASH / BANK

No fixed limit is established by the organization for making payments. The organization has special current accounts with State Bank of India. These accounts are the sources of payments.

10&11: PROJECT (WORKS) & PROJECT (PURCHASE)

12: PF & ADVANCES

25

EXECUTIVE SUMMARY

Fortune 500 88thposition IN 2012-2013

Indian Oil_ Indian Oil is India's flagship national oil company with business interests straddling the entire hydrocarbon value chain – from refining, pipeline Barauni Refinery – In harmony with nature- Rs. 5005cr

Other IOCL refineries (such as Gujarat Refinery, Bongaigaon Refinery) are also

in initial stage of adopting this modification. 10 OF INDIA'S 22 REFINERIES CAPACITY 65.7 MMPTA

MARKETING 49% SHARE

REFINING 31% SHARE

PIPELINE 71% SHARE

13thTPM National ConferenceKAIZEN THEME:

Improvement in efficacy of Steam distribution system for reduction in Energy Loss by Converting existing Condensing cum Extraction Turbine into Back Pressure Turbine.

BARAUNI REFINERYINDIAN OIL CORPORATION LIMITED

Estd Year-1964 Location,Bihar (India)

26

INTRODUCTION OF THE TOPIC

CAPITAL BUDGETING

Capital budgeting refers to the process we use to make decisions concerning investments in the long-term assets of the firm. The general idea is that the capital, or long-term funds, raised by the firms are used to invest in assets that will enable the firm to generate revenues several years into the future. Often the funds raised to invest in such assets are not unrestricted, or infinitely available; thus the firm must budget how these funds are invested.

IMPORTANCE OF CAPITAL BUDGETING

A bad decision can have a significant effect on the firm’s future operations. In addition, the timing of the decisions is important. Many capital budgeting projects take years to implement. If firms do not plan accordingly, they might find that the timing of the capital budgeting decision is too late, thus costly with respect to competition. Decisions that are made too early can also be problematic because capital budgeting projects generally are very large investments, thus early decisions might generate unnecessary costs for the firm. Indian oil has given importance for capital budgeting because capital investment decisions often represent the most important decisions taken by an organization, and they are extremely important, they sometime also pose difficulties.

27

Capital Budgeting Techniques

o Replacement decision—a decision concerning whether an existing asset should replaced by a newer version of the same machine or even a different type of machine that does the same thing as the existing machine. Such replacements are generally made to maintain existing levels of operations, although profitability might change due to changes in expenses (that is, the new machine might be either more expensive or cheaper to operate than the existing machine). o Expansion decision—a decision concerning whether the firm should increase operations by adding new products, additional machines, and so forth. Such decisions would expand operations. o Independent project—the acceptance of an independent project does not affect the acceptance of any other project—that is, the project does not affect other projects. For example, if you have a large sum of money in the bank that you would like to spend on yourself

FINANCIAL EVALUATIONAfter determination of cash flow as per methodology enumerated above, the next logical step is to financially evaluate the proposal. The evaluation shall be carried out through following two methods: (a) Internal Rate of Return (ROI/ROE) (b) Net Present Value (NPV) [62] Both the above methods fully recognize the timing of cash flows through the process of discounted cash flows.

TECHNIQUES

In this section, the basic techniques that are used to make capital budgeting decisions are described. To illustrate the techniques, let’s assume a firm is considering investing in a project that has the following cash flows:Year Expected After-Tax

(t) Net Cash Flows, t CF

0 $(5,000)1 8002 9003 15004 12005 3200

28

$(5,000) represents the net cost, or initial investment, that is required to purchase the asset—the parentheses indicate that the cash flow is negative. If the firm’s required rate of return is 12 percent, the cash flow time line for the asset is: 0 CF.

PAYBACK PERIODThe number of years, including the fraction of the year, it takes to recapture the initial investment. The following table shows the payback for this project:

Year Expected After-Tax Cumulative CF

(t) Net Cash Flows, t CF

0 $(5,000) (5,000)1 800 (4200)2 900 ( 3300)3 1500 (1800)4 1200 (600)5 3200 2600

This table shows that the payback period is between four years and five years. The actual payback is:Payback period= (Number of years before recovery of original investment)

+ ( Amount of investment/total cash flow during payback year)

=4 + $600/$3200=4.19 years.

As the computation shows, it takes a little more than four years for the firm to recapture its original investment for this project. The acceptance rule for payback can be stated as follows: Accept the project if Payback, PB < some number of years set by the firm This project would be acceptable if the firm wants to recapture its investments’ costs within five years, but it would not be acceptable if the firm wants to recapture the costs within three years.

NET PRESENT VALUE (NPV)—To determine the NPV of a project, you need to compute the present value of all

the future cash flows associated with the project, sum them up, and then subtract (or add a negative amount to) the initial investment of the project. The resulting value represents the amount by which the firm’s value will increase, on a present value basis, if the firm invests in the project. For example, if the

29

NPV of a project is $1,000, then the value of the firm should increase by $1,000 today. Thus, a project is acceptable if its NPV is positive. If a project has a

positive NPV, then it generates a return that is greater than the cost of the funds that are used to purchase the project.

(a) The present value of a future sum of money can be found by discounting it to the present point in time or Year ‗O‘ at the required rate of return/ discount rate. Required rate of return shall not be less than cost of capital. (b) Under this method, the present value of each years‘ net cash flow is calculated, starting from the year ‗0‘ till complete project life i.e. 15 years. This discounting rate adopted shall be the Hurdle Rate. (c) If the project has a positive Net Present Value, the project is considered to be commercially viable.

According to the acceptance criterion, the project in our example should be purchased. Remember that if the firm accepts a project with a positive NPV its value should increase, and vice versa. Therefore, if the project had a negative NPV it would not be acceptable because such a project would decrease the value of the firm. The easiest way to compute the NPV for a project is to use the cash flow register on your Capital Budgeting calculator. Refer to the instructions that came with your calculator to determine how to use the CF register. If you have a Texas Instruments BAII PLUS, you can use the steps given in the ―Time Value of Money� section of the notes. The inputs should be CF0 = –5,000, CF1 = 800, CF2 = 900, CF3 = 1,500, CF4 = 1,200, CF5 = 3,200, and I = 12. Press the NPV key (or CPT, then the NPV key) to find NPV = 77.82. You can also use a spreadsheet to compute NPV. Using Excel, you could set up the spreadsheet as follows:

30

To solve for the present value of the future cash flows, put the cursor in cell D3 and click on the ―Financial� function named NPV. In the box that appears input the following cell locations

The range B3:B7 contains the values of the cash flows for Year 1 through Year 5 because the NPV function programmed into the spreadsheet computes the present value of the future cash flows only. When you click ―OK� you will see the result of the computation, which is $5,077.82, appear in cell D3. But, because this result represents the present value of the future cash flows, you need to add CF0 to the result to include the amount of the initial investment. In this case, the computation is completed in cell D4, where CF0 is added to the

31

result of the NPV computation that appears in cell D3. Cell D4 should now show the correct answer for the NPV, which is $77.82

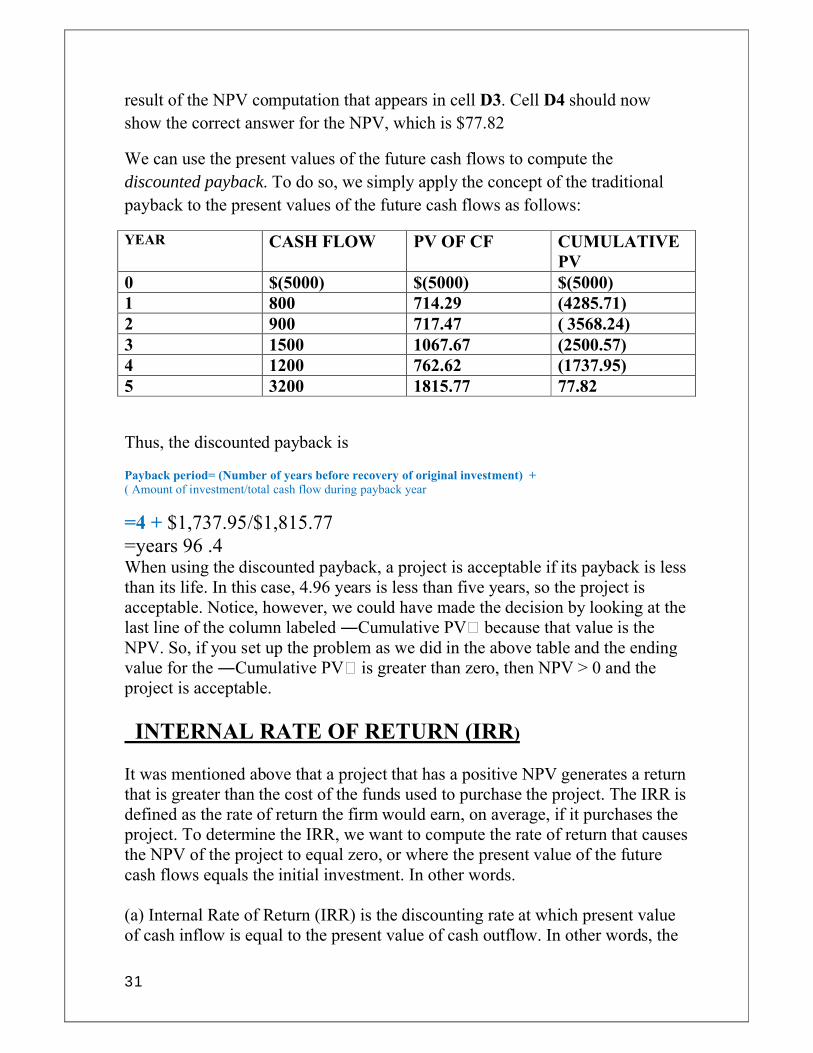

We can use the present values of the future cash flows to compute the discounted payback. To do so, we simply apply the concept of the traditional payback to the present values of the future cash flows as follows:

YEAR CASH FLOW PV OF CF CUMULATIVE PV

0 $(5000) $(5000) $(5000)1 800 714.29 (4285.71)2 900 717.47 ( 3568.24)3 1500 1067.67 (2500.57)4 1200 762.62 (1737.95)5 3200 1815.77 77.82

Thus, the discounted payback is

Payback period= (Number of years before recovery of original investment) + ( Amount of investment/total cash flow during payback year

=4 + $1,737.95/$1,815.77 =years 96 .4When using the discounted payback, a project is acceptable if its payback is less than its life. In this case, 4.96 years is less than five years, so the project is acceptable. Notice, however, we could have made the decision by looking at the last line of the column labeled ―Cumulative PV� because that value is the NPV. So, if you set up the problem as we did in the above table and the ending value for the ―Cumulative PV� is greater than zero, then NPV > 0 and the project is acceptable.

INTERNAL RATE OF RETURN (IRR)

It was mentioned above that a project that has a positive NPV generates a return that is greater than the cost of the funds used to purchase the project. The IRR is defined as the rate of return the firm would earn, on average, if it purchases the project. To determine the IRR, we want to compute the rate of return that causes the NPV of the project to equal zero, or where the present value of the future cash flows equals the initial investment. In other words.

(a) Internal Rate of Return (IRR) is the discounting rate at which present value of cash inflow is equal to the present value of cash outflow. In other words, the

32

discount rate that yields a ZERO Net Present Value is called Internal Rate of Return. (b) IRR shall be computed for all capital investment proposals and indicated in the Capital Investment Proposals.

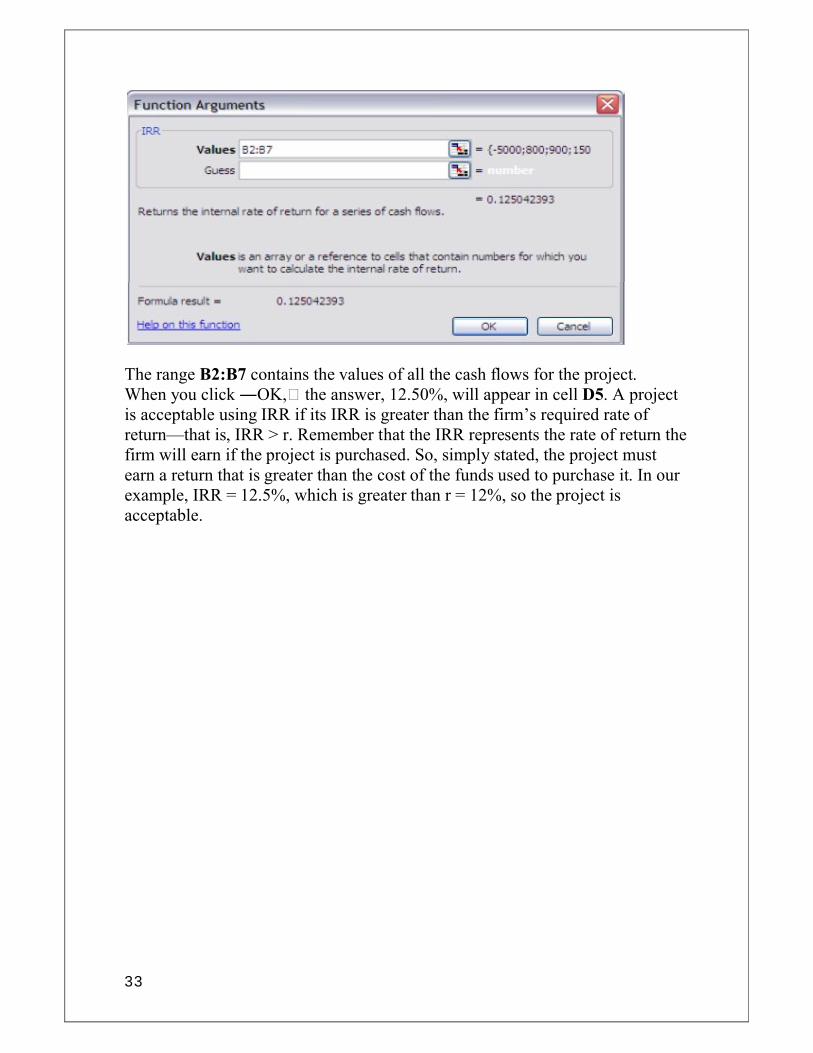

It is not easy to solve for the IRR without a calculator because you have to use a trial-and-error method—that is, plug in various values for IRR until the right side of the equation equals the left side of the equation. With a financial calculator, however, it is very easy to solve for IRR. Follow the same steps you would to compute the NPV, but press the IRR key (or CPT and then the IRR key) instead of the NPV key. You should find that IRR= 12.5%. Using a spreadsheet to compute the IRR for the project, set up the problem as before

To solve for the internal rate of return for this project, put the cursor in cell D5 and click on the ―Financial� function named IRR. In the box that appears input the following cell locations:

33

The range B2:B7 contains the values of all the cash flows for the project. When you click ―OK,� the answer, 12.50%, will appear in cell D5. A project is acceptable using IRR if its IRR is greater than the firm’s required rate of return—that is, IRR > r. Remember that the IRR represents the rate of return the firm will earn if the project is purchased. So, simply stated, the project must earn a return that is greater than the cost of the funds used to purchase it. In our example, IRR = 12.5%, which is greater than r = 12%, so the project is acceptable.

34

35

36

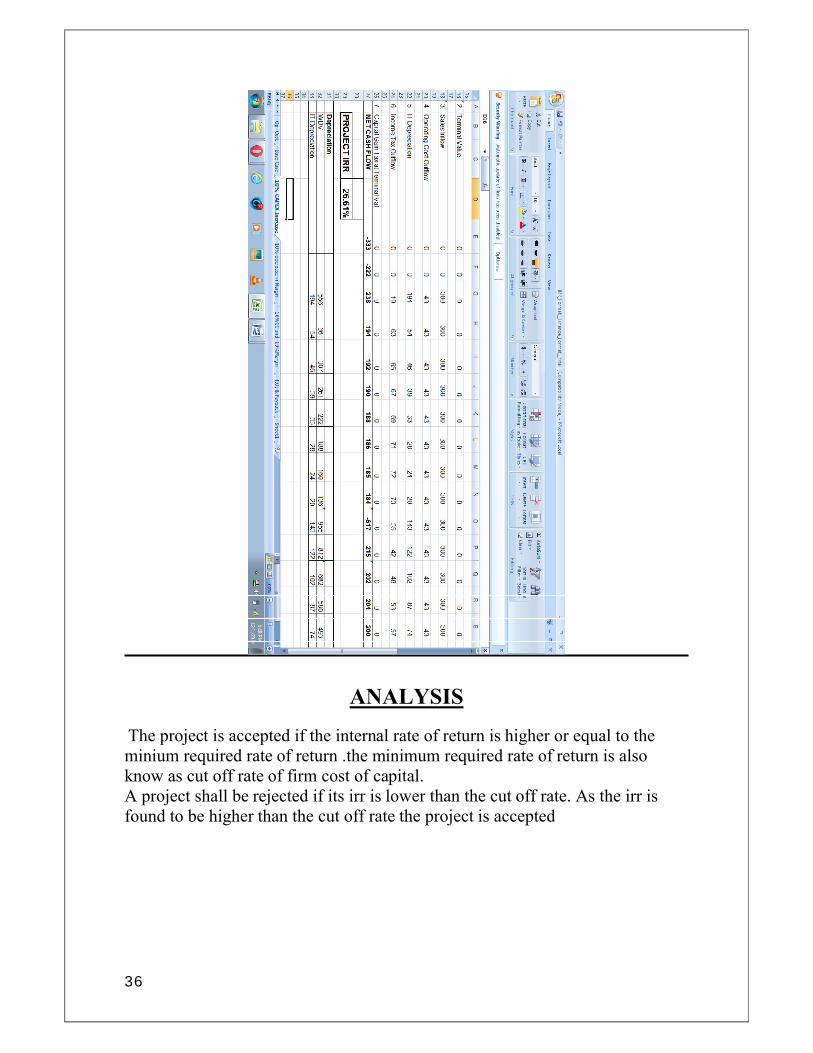

ANALYSIS

The project is accepted if the internal rate of return is higher or equal to the minium required rate of return .the minimum required rate of return is also know as cut off rate of firm cost of capital. A project shall be rejected if its irr is lower than the cut off rate. As the irr is found to be higher than the cut off rate the project is accepted

37

COMPARISON OF THE NPV AND IRR METHODS

Summarizing what we have discussed to this point, we know that a project is acceptable if its NPV is greater than zero. If a project has an NPV greater than zero, then it generates a return that is greater than the cost of the funds used to purchase the project. We also know that a project is acceptable if its IRR is greater than the firm’s required rate of return. When a project has an IRR greater than the required rate of return, then it generates a return that is greater than the cost of the funds used to purchase the project. As you can see by the italicized phrases, accepting a project using the NPV technique provides the same benefit as accepting a project using the IRR technique. As a result, both the NPV technique and the IRR technique should always give the same accept/reject decision—that is, if a project is acceptable using the NPV method, it also is acceptable using the IRR method, and vice versa. As we will discover shortly, however, when comparing two or more projects, the two techniques do not always agree as to which project is best.

For debt-financed projects, Debt Service Coverage Ratio (DSCR) is also to be calculated, so as to ascertain the debt serving capability of the project. DSCR is calculated as under: Profit after tax+ Depreciation + Interest on long term loan Interest on long term loan + Loan Repayment installment Break-ever analysis is a tool to ascertain the level of sales required to meet the funds requirement (fixed + variable). This can be used as a sensitive analysis tool and can be computed as under: Total fixed cost

Break Even Units = (BEU)/( Unit Selling Price – Unit Variable cost )BEUs are minimum sales units at which, project is just meeting its funds requirement and there is no loss or gain.

The computed IRR shall be compared with Benchmark IRR (hurdle rates). Hurdle rates shall be calculated based on Weighted Average Long Term Cost of Capital (WACC) along with project specific risk premium. Hurdle rates shall be revised annually after approval of competent authority.

38

CORPORATE OBJECTIVES

To serve the national interests in the Oil and related sectors in accordance and

consistent with Government policies.

To ensure and maintain continuous and smooth supplies of petroleum products

by way of crude refining, transportation and marketing activities and to provide

appropriate assistance to the consumer to conserve and use petroleum products

efficiently.

To earn a reasonable rate of interest on investment.

To work towards the achievement of self-sufficiency in the filed of Oil refining

by setting up adequate capacity and to build up expertise in laying of crude and

petroleum product pipelines.

To create a strong research and development base in the field of Oil refining

and stimulate the development of new product formulations with a view to

minimize/eliminate their imports and to have next generation products.

To maximize utilization of the existing facilities in order to improve efficiency

and increase productivity.

To optimize utilization of its refining capacity and maximize distillate yield

from refining of crude to minimize foreign exchange outgo.

To minimize fuel consumption in refineries and stock losses in marketing

operations to effect energy conservation.

To further enhance distribution network for providing assured service to

customers throughout the country through expansion of reseller network as per

Marketing Plan/Government approval.

39

To avail of all viable opportunities, both national and global, arising out of the

liberalization policies being pursued by the Government of India.

To achieve higher growth through integration, mergers, acquisitions and

diversification by harnessing new business opportunities

FINANCIAL OBJECTIVES

To ensure adequate return on the capital employed and maintain a reasonable

annual Dividend on its equity capital.

To ensure maximum economy in expenditure.

To manage and operate the facilities in an efficient manner so as to generate

adequate internal resources to meet revenue cost and requirements for project

investment, without budgetary support.

To develop long-term corporate plans to provide for adequate growth of the

activities of the corporation.

To endeavor to reduce the cost of production of petroleum products by means

of systematic cost control measures.

To endeavor to complete all planned projects within the stipulated time and cost

estimates.

40

41

SUMMARY OF FINANCIAL ANALYSIS For the purpose of financial analysis of capital investment proposals, cash flow estimates shall be prepared for the full project life. These cash flow estimates along with calculation of ROI/ROE, NPV, DSCR & Break Even analysis shall be attached to the proposal. While considering the base case, capacity utilization shall not be more than 90% (2nd year onwards) through out the project life cycle for all projects. A statement of assumptions made for Financial Analysis shall be enclosed. In summary it may be stated that the more sophisticated and mathematical methods of investment appraisal, particularly NPV and IRR can have extremely useful applications so long as they are used appropriately. Divisions while using these methods shall have an appreciation of limitations of these methods. Though these methods do reckon time value of money, but results of these methods largely depend on the accurate forecasting of the future cash flow. Therefore, it is important that utmost care is exercised in correctly estimating the future cash flows.

BIBLIOGRAPHY

INTERNET GOOGLE WWW.IOCL.IN WWW.GOOGLE.COM I. M. Pandey – Financial Management Khan And Jain –Financial Management iocl.in investopedia.com

42

43

44