canvaas_media india report

TRANSCRIPT

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 1/30

!"#!$%&$&'()"*+,&-+(.!/0&

12345&6787&

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 2/30

INDIA : SOCIO-ECONOMIC!SummaryIndia has the world’s second largest population at over 1.17billion, of which over 70% live in rural areas. At the sametime the five largest cities in India account for 50% of thecountry’s wealth (1).

The average household size is 4.8 with 5.2% with 31% of population aged under 14. GDP per capita is US$2,932 and

the average income is US$1,040.

India has the most affordable Big Mac index rating in theworld at US$ 1.22 (2) but as a majority Hindu country withthe third largest Muslim population in the world, neither beef or pork are served in any of McDonald’s 123 outlets acrossthe country and the price of a Chicken Maharaja Mac isused as a substitute (3).

India has the world’s second largest agricultural sector andis the largest producer of fruit, milk, coconuts, cashews, tea,ginger and black pepper. At the same time seven Indianfirms were listed among the top 15 technology outsourcingcompanies in the world (4).

India has 22 official languages,reflecting a linguistic, genetic andcultural diversity second only to thatfound in the African continent (4).

Hindi is spoken by 43% of Indians and

another 27 to 43% can understand or speak the language. Other significantlanguages include Bengali, Kannada,Telugu, Marathi, Tamil and Malayalam.English is recognised as the secondofficial language.

Mumbai is 7th in the world''s top 10bi l l ionaire ci t ies – home to 20

bil l ionaires, according to Forbesmagazine

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 3/30

INDIA: SOCIO-ECONOMIC!

Source: World Gazetteer

/239:;<&4=>:;&?@&ABACD2>BE&

F3:9=BEG&

6787&:;>H2<:&

&FH=DD=BE;G&

!"#$%&'()#*$(+(,(-+.,(/# !0"1#

2"#345+)#*345+)/# !2"6#

0"#7(89(5:,4#*;(,8(.(<(/# 6"=#

="#;:5<(.(#*>4-.#7489(5/# 6"!#

6"#?+488()#*@(&)5#A(B%/# ="C#

C"##DEB4,('(B#*F8B+,(#G,(B4-+/# ="!#

H#"#F+&4B4'(B#*I%J(,(./# 0"K#

1"##G%84#*$(+(,(-+.,(/# 0"=#

K"##L%,(.#*I%J(,(./# 0"0#

!M"#;(8N%,#*OP(,#G,(B4-+/# 0"2#

Source: National Geographic

/239:;<&4=>:;&?@&3:9=BE&

!"#;:5<(.(#

2"#345+)#

0"#$%&'()#

="#?+488()#

6"#;(8N%,#

C"#DEB4,('(B#

H#"#7(89(5:,4#

1"#G%84#

K"#F+&4B('(B#

!M"#?:)&'(.:,4#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 4/30

INDIA : SOCIO-ECONOMIC!

Source: US Census Bureau, International Database (March 2010)

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 5/30

INDIA: SOCIO-ECONOMIC!*BA&87&2IC:E<&!EJ=2E&4=>:;&

!"#345+)#

2"#7(89(5:,4#

0"##I,4(.4,#$%&'()#

="#?+488()#

6"#DEB4,('(B#

C"#;:5<(.(#

H#"#;:Q+)#

1"#G%84#

K"#R()N%,#

!M"#F+&4B4'(B#

Based on lifestyle and ownership of

consumer durables.Source: Nielsen UMAR 2009

Based on quantifiable growth

factors.Source: Ernst & Young 2009

Based on 300 indicators on a 10

year timescale.Source: Confederation of IndianIndustry & Institute of Competitiveness 2010

*BA&87&!EJ=2E&4=>:;&=E&

<:3H;&BK&J:L:DBAH:E<&

!"#345+)#

2"#$%&'()#

0"#?+488()#

="#7(89(5:,4#

6"#DEB4,('(B#

C"#;:5<(.(#

H"#G%84#

1"#F+&4B('(B#

K"#?+(8B)9(,+#

!M"#L%,(.#

*BA&87&?:;<&4=>:;&<B&D=L:&=E&&

!"#A4S#345+)#

2"#$%&'()#

0"#?+488()#

="#7(89(5:,4#

6"#;:5<(.(#

C"#DEB4,('(B#

H"#F+&4B('(B#

1"#G%84#

K"#I%,9(:8#

!M"#I:(#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 6/30

INDIA : SOCIO-ECONOMIC!TransportWith good physical connectivity a key driver for economicgrowth in a land of vast distances and over a billion people,India has seen rise in demand for transport infrastructure andservices by around 10% a year since the early 90s (5).

Transport in India contributes to around 4.5% of the nation’s

GDP, with road transportation contributing 90% of the country’spassenger traffic and 65 percent of its freight

Public transport is the primary mode of transport for most of the population, and India's public transport systems are amongthe most heavily utilised in the world. The fully air-conditionedDelhi Metro has carried over a billion customers since itsopening in 2002 (6).

Car ownership has doubled to 1% over the last ten years andis set to double again by 2016 making India one of the fastestgrowing markets in the world (7).

M:;<;:DD=E9&423;&677N&&& O2D:;&

#$(,%T#F5.:# 2!2U6C1#

$(,%T#>(9:8V# !0=UHC1#

@(.(#W8B)Q(# !!!U26C#

$(,%T#LS)X# !!MUMH!#

DE%8B()#)!M# !MCUMK6#

DE%8B()#L(8.,:# K!U=H1#

Source: Society of Indian Automobile Manufacturers

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 7/30

INDIA: RETAIL!SummaryAt US$400 billion and with an annual growth rate of 30%the Indian retail market is ranked as the most attractiveemerging market for investment in the retail sector by ATKearney's 2009 Global Retail Development Index.

Consumer spending has risen 75% in the past four yearsalone, with sales of listed retailers increasing by 12% in the

September 2009 quarter compared with the same period in2008. The organised retail sector currently accounts for around 5% of the Indian retail market (8).

According to Nielsen’s ShopperTrend India Report 2009,traditional grocery stores continue to dominate the Indianretail scene and are frequented more often with only 39%of grocery buyers visiting a Supermarket/Hypermarket atleast once in four weeks and 97% visiting a traditional

store over the same period.Source: IMAGES Retail 2010

*BA&3:<2=D:3;&

G(8.(5::8#V4.()5#

L+:NN4,Y-#L.:N#

V45)(8Q4#V4.()5#

FB).E(#7),5(#V4.()5#

LN48Q4,Y-#V4.()5#

Z(8B&(,<#9,:%N#

@,48.#Z.B#*@(.(#I,:%N/#

7+(,T#V4.()5#

?([\##?:]44#3(E#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 8/30

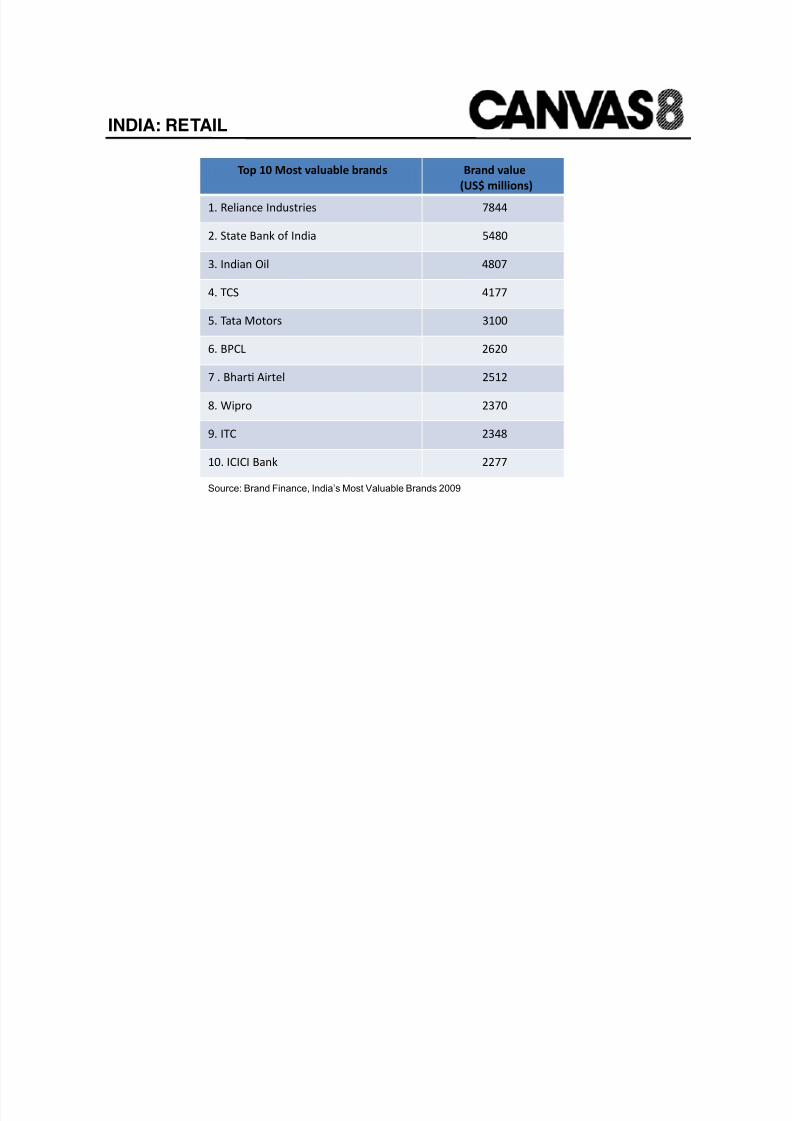

INDIA: RETAIL!*BA&87&1B;<&L2DC2?D:&?32EJ;& M32EJ&L2DC:&

&F)OP&H=DD=BE;G&

!"#V45)(8Q4#W8B%-.,)4-# H1==#

2"#L.(.4#7(8<#:[#W8B)(# 6=1M#

0"#W8B)(8#^)5# =1MH#

="#@?L# =!HH#

6"#@(.(#$:.:,-# 0!MM#

C"#7G?Z# 2C2M#

H#"#7+(,T#F),.45# 26!2#

1"#>)N,:# 20HM#

K"#W@?# 20=1#

!M"#W?W?W#7(8<# 22HH#

Source: Brand Finance, India’s Most Valuable Brands 2009

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 9/30

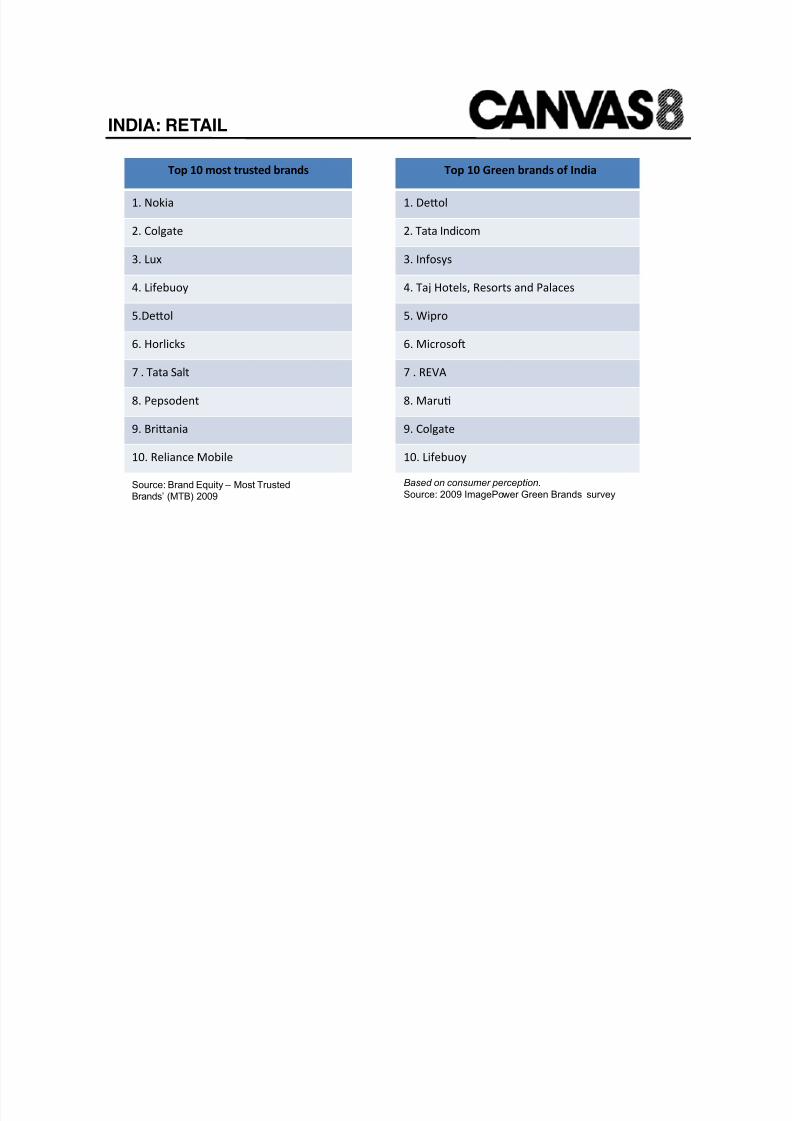

INDIA: RETAIL!

Source: Brand Equity – Most TrustedBrands’ (MTB) 2009

*BA&87&HB;<&<3C;<:J&?32EJ;&

!"#A:<)(#

2"#?:59(.4#

0"#Z%_#

="#Z)[4'%:E#

6"34P:5#

C"#D:,5)Q<-#

H#"#@(.(#L(5.#

1"#G4N-:B48.#

K"#7,)P(8)(#

!M"#V45)(8Q4#$:')54#

Based on consumer perception.

Source: 2009 ImagePower Green Brands survey

*BA&87&Q3::E&?32EJ;&BK&!EJ=2&&

!"#34P:5#

2"#@(.(#W8B)Q:&#

0"#W8[:-E-#

="#@(J#D:.45-U#V4-:,.-#(8B#G(5(Q4-#

6"#>)N,:#

C"#$)Q,:-:X#

H#"#V`aF#

1"#$(,%T#

K"#?:59(.4#

!M"#Z)[4'%:E#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 10/30

Source: WATBlog.com

Online retailThe online retail industry currently stands at US$0.23 billion,but is estimated to grow 30% yearly. The most purchasedproducts online are electronic goods and clothes, butreplicating the success of online retail in the developed worldis stymied by a lack of broadband internet.

Although India is poised to have the third largest amount of

Internet users by 2013, according to KPMG's BusinessPerformance service, the short-term future of online retailingin India is as a complimentary service rather than a corecontributor to sales.

20% of online Indians have bought online within the past oneyear. 65% of these have bought a travel product. The launchof IRCTC (Indian Railway’s ecommerce arm to power the saleof railway tickets has encouraged a whole new demographic

to shop online (9).

With major retailers like Tata Group finally setting up shoponline alongside established players like eBay and Rediff,online retailing is finally establishing a presence in India.

*BA&BED=E:&3:<2=D:3;&?@&A29:&L=:R&&

FM2;:J&BE&4C?:;<2<&2EJ&$D:S2&J2<2G&

`'(E")8#

b5)N<(,."Q:&#

W8c'4(&"Q:&#

L+:NN)89",4B)]"Q:&#

A((N.:5"Q:&#

L+:NN)89")8B)(T&4-"Q:&#

W8B)(N5(d(")8#

D:&4-+:N!1"Q:&#

b%.%,4'(d((,"Q:&&

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 11/30

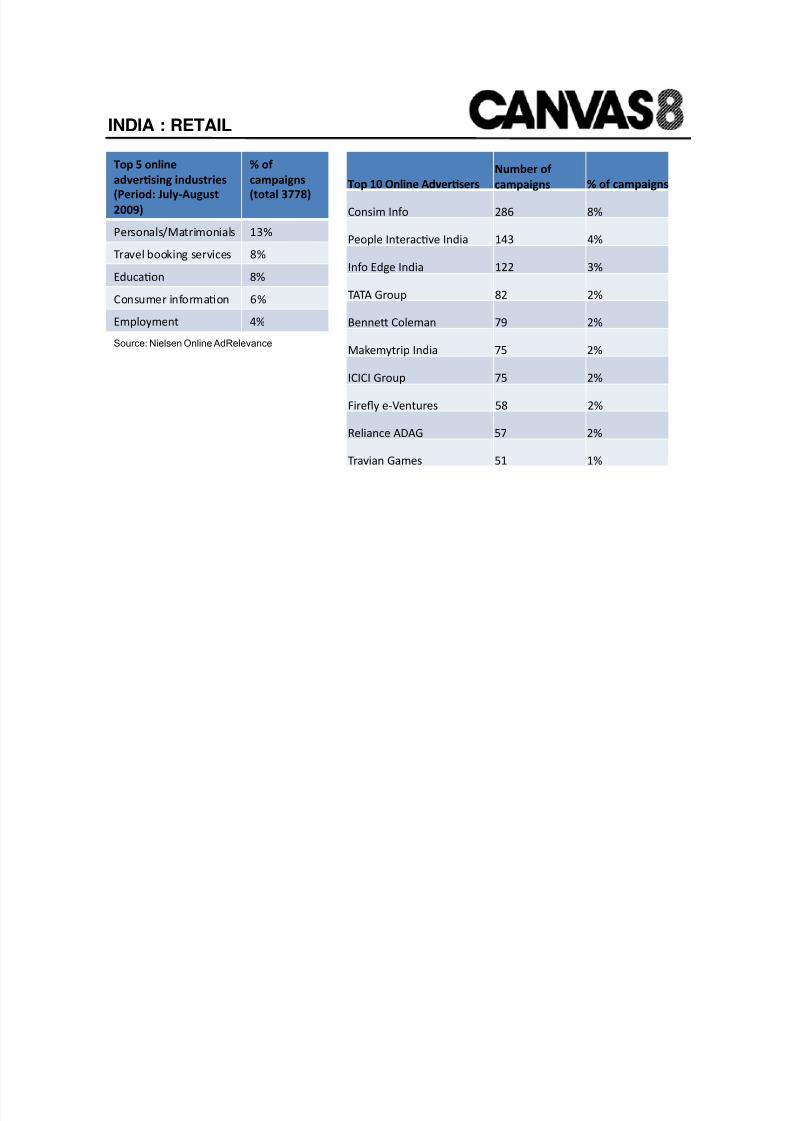

INDIA : RETAIL!*BA&87&(ED=E:&$JL:3>;:3;&

"CH?:3&BK&

42HA2=9E;& T&BK&42HA2=9E;&

?:8-)&#W8[:# 21C# 1e#

G4:N54#W8.4,(QTf4#W8B)(# !=0# =e#

W8[:#`B94#W8B)(# !22# 0e#

@F@F#I,:%N# 12# 2e#

74884P#?:54&(8# HK# 2e#

$(<4&E.,)N#W8B)(# H6# 2e#

W?W?W#I,:%N# H6# 2e#

b),4gE#4ha48.%,4-# 61# 2e#

V45)(8Q4#F3FI# 6H# 2e#

@,(f)(8#I(&4-# 6!# !e#

Source: Nielsen Online AdRelevance

*BA&U&BED=E:&

2JL:3>;=E9&=EJC;<3=:;&F-:3=BJ%&VCD@W$C9C;<&

677NG&

T&BK&

42HA2=9E;&F<B<2D&XYYZG&

G4,-:8(5-i$(.,)&:8)(5-# !0e#

@,(f45#'::<)89#-4,f)Q4-## 1e#

`B%Q(T:8# 1e#

?:8-%&4,#)8[:,&(T:8## Ce#

`&N5:E&48.# =e#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 12/30

INDIA : RETAIL!

Source: goindia.about.com

AlcoholThe Indian market for alcohol totalled US$14 billion last year, and isprojected to grow at 10% a year - more than in China, the U.S. andEurope combined, according to an estimate by KPMG India.

Hard liquor is far more popular than beer and wine, with spiritsaccounting for about 70% of the market, dominated by a $7.5 billionIndian whiskey market - the biggest in the world.

Imports account for only a tiny fraction of alcohol consumed, butwith drivers for alcohol consumption including sizable population, agrowing middle class and a growing economy, only the huge taxeson imported whiskey, prevent it from winning more market share.

Wine is only about 2% of the total alcohol market, but it is the fastestgrowing especially amongst women, for whom drinking wine is amark of urban sophistication. The wine market has grown from

virtually non-existent 10 years ago to $253 million last year, and it isexpected to more than double to $630 million by 2013 (10).

*BA&!EJ=2E&?::3&?32EJ;&

;)89c-+4,#

D(ES(,B-#

V:E(5#?+(554894#

;(5E(8)#75(Q<#Z('45#

;)89Y-#

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 13/30

INDIA : MEDIA!SummaryOverall Media & Entertainment (M&E) is one of the fastest growing industries in the country.According to a 2010 report jointly published by the Federation of Indian Chambers of Commerce andIndustry (FICCI) and KPMG, the TV industry showed good growth in 2009, while Print grewmoderately and Films and Radio experienced negative growth.

Nonetheless, with the majority of the population below the age of 35, and increasing disposable

income in Indian households, the average spend on media and entertainment is likely to grow inIndia, according to the 2009 edition of PricewaterhouseCoopers’ (PwC) Indian Entertainment andMedia Outlook.

The FICCI/KPMG report projects growth at compounded annual growth rate of 13% per annumthrough 2014 to reach INR 1.1 trillion (US$20.09 billion).

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 14/30

INDIA : MEDIA!Projected growth for M&E industry over the next 5 years:

Source: FICCI/KPMG 2010

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 15/30

INDIA : MEDIA!TelevisionThe FICCI/KPMG study predicts the television industry currently valued at about US$ 4.63 billion, willexpand by 14.5% between 2009 and 2013. According to the PwC report, the television advertisingindustry is expected to account for a share of 41.0% of the advertising industry in 2013, up from thepresent share of 39.0%.

Over the next few years, factors driving the industry will include the advent of 3G networks enabling

mobile content-streaming and the growth of digital distribution platforms such as TV-on-demand fromfirms such as Sun Direct, Bhatia Airtel and Big TV, who have all increased their marketing budgets by20-25% in the fiscal year 2010 (11).

The ‘Avatar effect’ will also see television manufacturers gearing up to introduce new 3D TV sets intothe market in the second quarter of 2010. The world's most lucrative cricket event, the Indian Premier League, is also set to become the first sports body to telecast a match live in 3D.

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 16/30

INDIA : MEDIA!FilmThe Indian film industry remains the largest in the world in terms of ticket sales and number of filmsproduced per year. The FICCI/KPMG study values the Indian film industry at US$ 2.11 billion andprojects its growth at 9.1% till 2013.

Despite this 2009 saw domestic film industry revenues down by 14% from 2008, due to lack of infrastructure, idiosyncratic Bollywood production values including shoddy home-grown scripts and the

onset of competition from Hollywood films, now widely dubbed into regional languages.

On the flipside, the opening of the film industry to foreign investment coupled with the granting of industry status to this segment has had a favourable impact, leading to many global production unitsentering the country, for example 2009’s Oscar Winning Best Film Slumdog Millionaire.

Meanwhile, non-resident Indian (NRI) filmmakers are looking to India as the country offers a largemarket and a mainstream arts platform. The framework of reference has changed for NRI cinema andfilmmakers are now more geared towards ethnic communities and the diaspora which assures them of

an audience in India, UK and the US (12).

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 17/30

INDIA : MEDIA!*BA&93B;;=E9&MBDD@RBBJ&[DH;&677N&

0#WB):.- V-=MM#&)55):8

Z:f4#F(J#;(5# V-CH#million

FJ('#G,4&#;+)#I+(d('#;+(8)# V-CC million

A4S#j:,< V-C6#&)55):8

F55#.+4#74-.k#b%8#749)8- V-C=#&)55):8

*BA&93B;;=E9&\BDD@RBBJ&[DH;&677N&

2M!2 V-KMM#million

L5%&B:9#$)55):8(),4 V-01Mmillion

D(,,E#G:P4,#(8B#.+4#D(5[h

75::B#G,)8Q4

V-26Mmillion

Ff(.(,#*:N48)89#S<8B/# V-22Mmillion

@4,&)8(.:,#L(5f(T:8 V-!KM#million

Source: ians.inSource: Indian Box Office

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 18/30

INDIA : MEDIA!Print publishingPrint’s slowing down in India: according to a PwC report, the print industry is projected to grow by5.6% over the period 2009-13, touching US$ 4.26 billion in 2013 from the present US$ 3.24 billion in2008.

Newspaper sales in India, China and Japan which stand at 60% in terms of circulation, are thehighest in the world, according to the World Association of Newspapers and News Publishers (WAN-IFRA).

According to the Indian Readership Survey 2009 (13), only nine of the top 25 most read publications(including dailies and periodicals) registered a growth in readership. The combined percentagedecline in readership, for the 16 publications that registered a drop, was 51.89%. Some of the mostread publications also figure in the list that lost the most readers, Dainik Jagran, for instance, lostsome 1.1 million readers.

The combined percentage of readers who read any English daily, grew 0.47% to 3.1, whilst weekliesin all languages, except Malayalam, registered a drop. Every single one of the top 25 English

magazines registered a drop in readership, perhaps attributable to the availability of online versions .

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 19/30

INDIA : MEDIA!*BA&87&E:R;A2A:3;&

FD2E9C29:G&4=34CD2>BE&&

'=34CD2>BE&

FH=DD=BE;G&

#@+4#@)&4-#:[#W8B)(#*`895)-+/## ##0"!6#

##3()8)<#7+(-<(,#*D)8B)/## ##2"66#

3()8)<#R(9,(8#*D)8B)/### 2"!H#

$(5(E(5(#$(8:,(&(#

*$(5(E(5(&/##

!"6!#

@+4#D)8B%#*`895)-+/## !"0C#

`48(B%#*@45%9%/## !"06#

34QQ(8#?+,:8)Q54#*̀ 895)-+/## !"0=#

F8(8B(#7(d(,#G(.,)<(#

*7489(5)/##

!"2H1#

F&(,#OJ(5(#*D)8B)/# !"20#

D)8B%-.(8#@)&4-#*`895)-+/## !"!=#

*BA&87&H292]=E:;&677N&& +:2J:3;5=A&

F!EJ=2E&D2^5;G&

L(,(-#L(5)5##*D)8B)#[:,.8)9+.5E/# CC"0#

#;%&(B(&#*@(&)5#>44<5E/# C="K#

a(8).+(#*$(5(E(5(&#[:,.8)9+.5E/# 6K"H#

W8B)(#@:B(E# *̀ 895)-+#>44<5E/# 6C"0#

;%89%&(&#*@(&)5#>44<5E/# 6="0#

W8B)(#@:B(E#*D)8B)#>44<5E/# 6=#

I,)+#L+:'+(#*D)8B)#[:,.8)9+5E/# 6M#

F8(8B(#a)<(.(8#*@(&)5#>44<5E/# =C"6#

$4,)#L(+45)#*D)8B)#&:8.+5E/# =C"=#

G,(TE:9).(#3(,N(8#*D)8B)#

&:8.+5E/#

=0"C#

Source: Audit Bureau of Circulations Source: Indian Readership Survey 2009

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 20/30

INDIA : MEDIA!"BEW[4>BE& $C<5B3&

##74Q:&)89#W8B)(8# ##G;#a(,&(#

#a)Q.:,)(#(8B#F'B%5# ##L#7(-%#

@+4#3)lQ%5.E#:[#74)89#I::Bk#

^8#@+4#L%'.54#F,.#:[#3+(,&(#

I#3(-#

@+4#Z(-.#L%8-4.# F#L)89+#

b,44[(55k#F&4,)Q(U#b,44#

$(,<4.-U#(8B#.+4#L)8<)89#:[#

.+4#>:,5B#`Q:8:&E#

R#LT95).d#

V(J(#V(f)#a(,&(k#G()8.4,#:[#

?:5:8)(5#W8B)(#

V#?+(S5(#

Z4-#b,(8Q()-#(8B#345+)k#F9,(U#

F5)9(,+#`.#L(,B+(8(#

RmV#Z([:8.#

L)&N5E#b5E# ?#I:N)8(.+#

?:&&)P4Bk#F#L<4NTQ#$(<4-#

G4(Q4#S).+#$(,,)(94#

`#I)5'4,.#

A)84#Z)f4-k#W8#L4(,Q+#:[#.+4#

L(Q,4B#)8#$:B4,8#W8B)(#

>#3(5,E&N54#

M:;<;:DD=E9&?BB^;&&F8ZW6U_X_87G&

F.=4>BEG&

$C<5B3&

@+4#$%-4%&#^[#W88:Q48Q4# ^#G(&%<#

#@+4#I),5#>+:#;)Q<4B#@+4#

D:,84.-Y#A4-.#

L#Z(,--:8#

@+4#G(5(Q4#:[#W55%-):8-# ?#73)f(<(,%8)#

b(89# R#G(P4,-:8#

2#L.(.4-k#@+4#L.:,E#:[#$E#

$(,,)(94#

?#7+(9(.#

@+4#W&&:,.(5-#^[#$45%+(# F#@,)N(.+)#

WU#F54_#?,:--# R#G(P4,-:8#

>(E#.:#I:# O#?+(P4,J44#

345+)#3%,'(,# ;G#L)89+#;44N#@+4#?+(894# A#L%',(&(8)(8#

Source: ians.in

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 21/30

INDIA : MEDIA!MusicThe music industry grew 14% to around INR 8.3 billion in 2009, driven by digital music sales whichaccounted for approximately 88% of total music industry revenue in 2009.

Despite this there remains a huge amount of piracy. A survey carried out last year by Synovate MusicMatters found that more than 80% of young Indians felt that "music is a very important part of my life".More than 40 % listened to music on their mobiles. But only about 10 per cent would contemplatespending money on a download.

In May 2009, Bharti Airtel, India’s largest mobile operator, announced that for the first time thecompany's music revenues had exceeded those of Sa Re Ga Ma, the country’s largest music label.An estimated 30 per cent of the music industry’s revenues in India – about US$150 million a year –now comes from sales of “ringback tones” - a bizarre product where a snippet of a track isdownloaded to a mobile and played to the caller rather than a “ring ring” tone before the call isanswered. (14).

With TV music channels giving less space to music programming in place of game shows and reality

shows, independent bands are increasingly looking to promote their videos by making them availableonline (15).

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 22/30

INDIA : MEDIA!*BA&;BE9;&&F8N_X_6787G&

OBE9&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&.=DH&

V(+)&(8#W-+n#;(#3+(9(#

V4#

>455#3:84#F''(#

@%#I(8B)# Z:f4#L4_#F%,#3+:<+(#

@(,:8#7+(,)#D()#j4#V((.#

L(J(8#

L(B)E((8#

FJ8(')#D(S((E4)8#74<,(,(#

7(+4)8##

L+((N).#

^#R(84&(8# @%&#$)5:#@:+#L(+#

#$4,)#F(-+(:8#;)# V)9+.#j(((#>,:89#

>(n.#A4#R:#7)J#7:E((# L(B)E((8#

FJ8('44#`+-((-#;:# 3:#3)5:8#;4#;+4)#

$4)8#

F(:#L4484#L4#Z(9#;4# $)P(5#f-#$)P(5#

W#3:8.#;8:S#>+(.#@:#3:# D:%-4[%55#

*BA&87&[DH&;BCEJ<324^&;BE9;&KB3&677N&

OBE9&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&.=DH&

?+:,#'(d(,)# Z:f4#F(J#;(5#

$(-(<(55)# 345+)hC#

D(%54#D(%54# V('#A4#7(8(#3)#R:B)#

R()#D:# L5%&B:9#$)55):8(),4#

3+(8.48(8# ;(&)84E#

I%d(,)-+# I+(J)8)#

L(N8:8#L4#7+(,4#A()8(# Z%Q<#'E#?+(8Q4#

>(<4#ON#L)B# >(<4#ON#L)B#

@%J+#$4)8#V('#3)<+.# V('#A4#7(8(#3)#R:B)#

@4,(#D:84#Z(9(#D::8# FJ('#G,4&#;)#I+(d('#

Based on critical acclaim & sales figuresSource: Planet Bollywood (2010)

Based on radio play .Source: Radio Mirch

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 23/30

INDIA : MEDIA!GamingGaming is the biggest media and entertainment growth area, albeit from a small base of users. Whileall three sectors: mobile gaming, PC gaming and console gaming have together shown a 22% growthin 2009, it is expected to grow at a CAGR of 32 % in the next 5 years to reach INR 32 billion by 2014,according to the FIICI/KPMG study.

Console gaming (including hardware) contributes the biggest percentage of gaming revenue, at over 62% of the total, largely attributable to rising incomes in urban centres, creation of localised content for

the market like Yuvraj Singh International Cricket, Hanuman and Kabaddi for PS2 and awarenessstemming from organised retail regarding the launch of newer products such as the Nintendo Wii,

The major players in console gaming target a wider consumer base rather than focusing on the 6-25demographic, but growth is stymied by high customs on legitimate console hardware and softwarewhich makes console gaming an expensive proposition.

In the future, 3G services and increasing broadband penetration will provide high speed networksdriving growth in mobile and online PC gamers respectively. At the same time, console gaming

companies are moving from a product to a services oriented model enabling users to not only playgames off the console but also watch movies, upload photos and so on.

In addition, branded movie and cricket based games will benefit from an ‘interactive TV’ medium rather than attempting to push users to play on mobiles and pc.

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 24/30

INDIA : TECHNOLOGY!RadioThe cheapest and oldest form of entertainment, radio reaches 99% of the population and is likely to seemany dynamic changes over the next few years.

According to the 2009 PwC study, the radio industry is forecast to grow at a compound annual growth rate(CAGR) of 18% over 2009-13, reaching US$ 391.15 million in 2013 from the present US$ 170.87 million in2008 - more than double its present size.

In terms of its advertising, it is projected that the radio advertising industry will be able to increase its sharefrom 3.8% to 5.2% between 2009 and 2013. (16)

Online habits According to the JuxtConsult’s India Online study 2009, there are currently 47million internet users in India(39 million urban, 8 million rural). This has fallen by 6% from the previous year due to a lapse in‘occasional’ cybercafe users.

There has been a 10% growth in people using the internet once a month, classed as ‘regular’ users and a15% growth in daily internet users.

25% of computer users still do not use the internet, held back by affordability and language, with less than2% of all Indian’s preferring to read in English. 80% of online Indians are aged 19-35, with the office beingthe most common site of access.

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 25/30

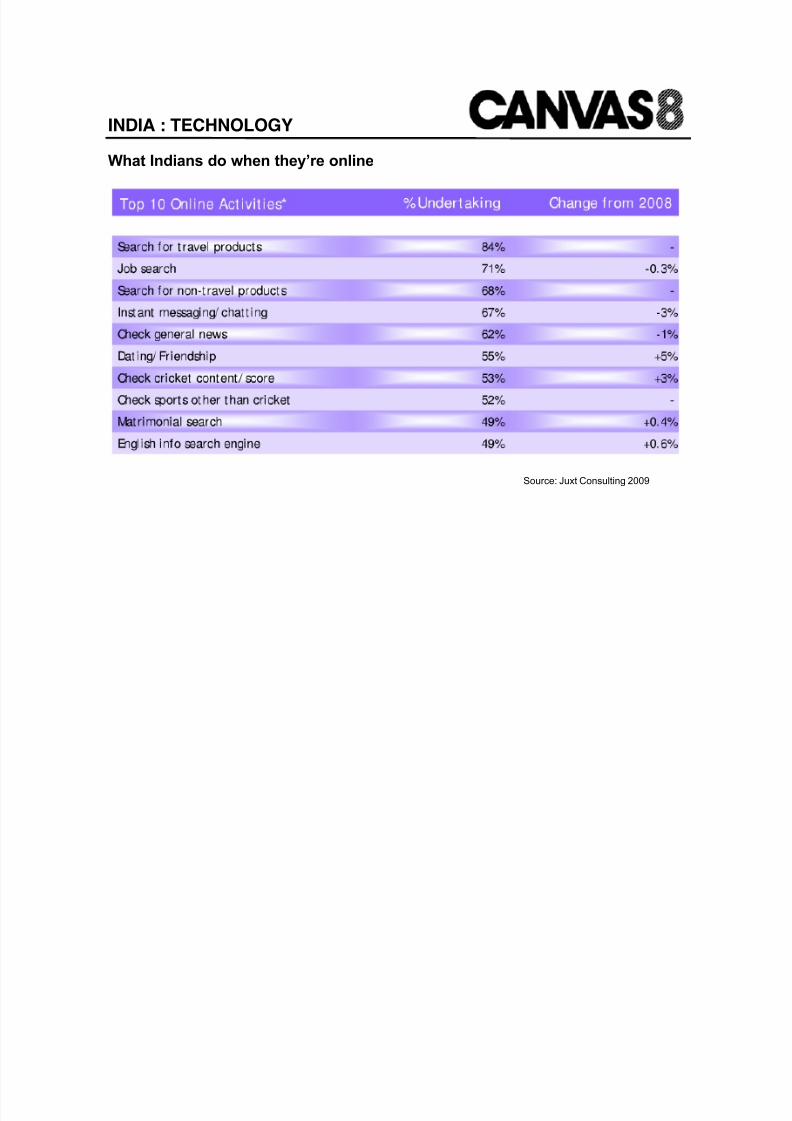

INDIA : TECHNOLOGY!What Indians do when they’re online

Source: Juxt Consulting 2009

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 26/30

INDIA : TECHNOLOGY!Social networkingOrkut was the most popular social network in Indiauntil late last year, and Facebook is only narrowlydominating now, mostly among the older generations – having been considered elitist on first launch.

Mobile and mobile internet is a major factor in Indiansocial networking. Given Orkut’s hold over the Indian

market, it is surprising that they took until June 2009to release a mobile version of the site. Another keyfeature geared to emerging markets is the ‘light’version, with fewer features and images displayed toallow it to run at a lower bandwidth.

Facebook took a little longer to catch up withFacebook Lite (Aug 2009), most recently announcinga ‘Zero’ text-only version at the Mobile World

Congress in February 2010. Facebook use grew229% in 2009, and the site was (bizarrely) nominatedby Forbes India as ‘Person of the Year 2010’.

*BA&&U&;B4=2D&E:<RB3^=E9&;=<:;&

b(Q4'::<#

^,<%.#

@S)P4,#

Z)8<4BW8#

W')':#

Source: Alexa

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 27/30

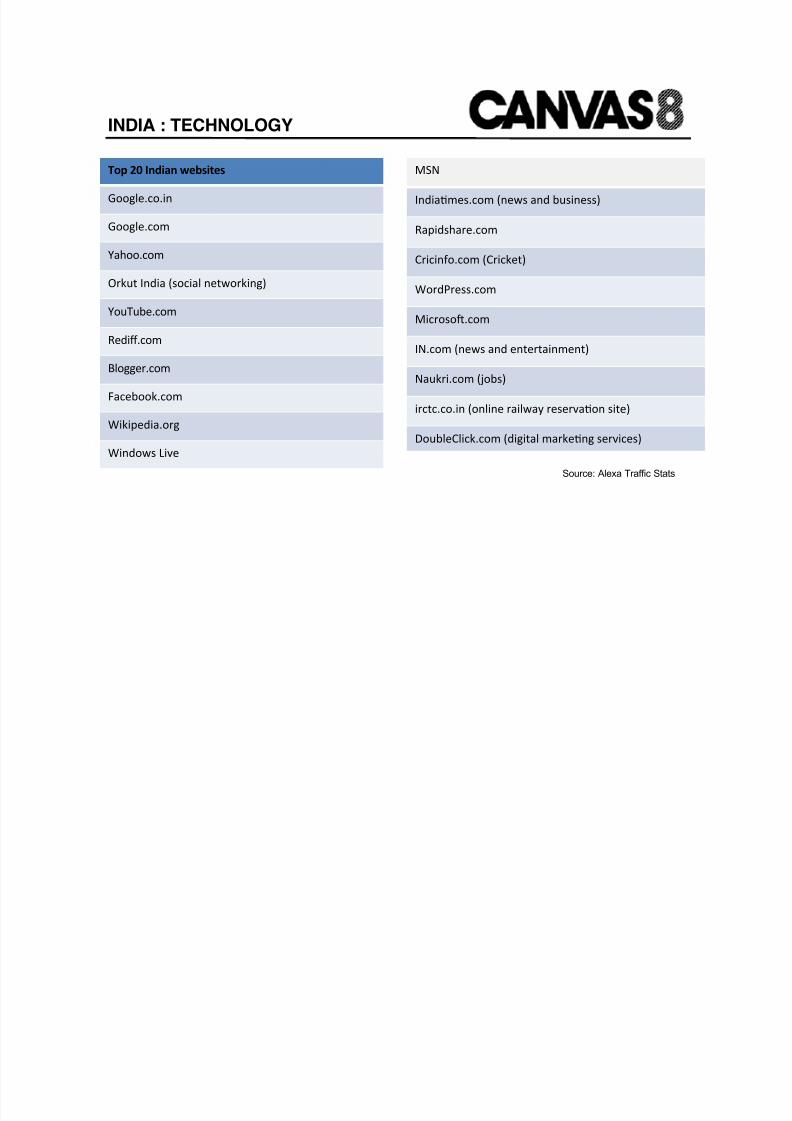

INDIA : TECHNOLOGY!*BA&67&!EJ=2E&R:?;=<:;&

I::954"Q:")8#

I::954"Q:&#

j(+::"Q:&#

^,<%.#W8B)(#*-:Q)(5#84.S:,<)89/#

j:%@%'4"Q:&#

V4B)]"Q:&#

75:994,"Q:&#

b(Q4'::<"Q:&#

>)<)N4B)(":,9#

>)8B:S-#Z)f4#

$LA#

W8B)(T&4-"Q:&#*84S-#(8B#'%-)84--/#

V(N)B-+(,4"Q:&#

?,)Q)8[:"Q:&#*?,)Q<4./#

>:,BG,4--"Q:&#

$)Q,:-:X"Q:&#

WA"Q:&#*84S-#(8B#48.4,.()8&48./#

A(%<,)"Q:&#*J:'-/#

),Q.Q"Q:")8#*:85)84#,()5S(E#,4-4,f(T:8#-).4/#

3:%'54?5)Q<"Q:&#*B)9).(5#&(,<4T89#-4,f)Q4-/#

Source: Alexa Traffic Stats

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 28/30

INDIA : TECHNOLOGY!MobileIndia is the world's second-biggest mobile phone market with morethan 525 million mobile users and adds more cellphone connectionson a monthly basis than anywhere else in the world.

Price wars will increase affordability in the rural market, and aswireless infrastructure reaches further into Indian villages, growthwill continue to increase to a projected billion users in 2015. (17).

Bharti Aitel, Reliance and Vodafone are three major providers of mobile services and Nokia is the preferred handset provider with amarket share of 54% (18).

With 65 times more mobile connections than broadband Internetlinks, Indian firms have invented ways, via simple sms messaging,to wire money to temples, pay for groceries, find jobs and send andreceive e-mail messages - on humble phones with no data

connection (19).

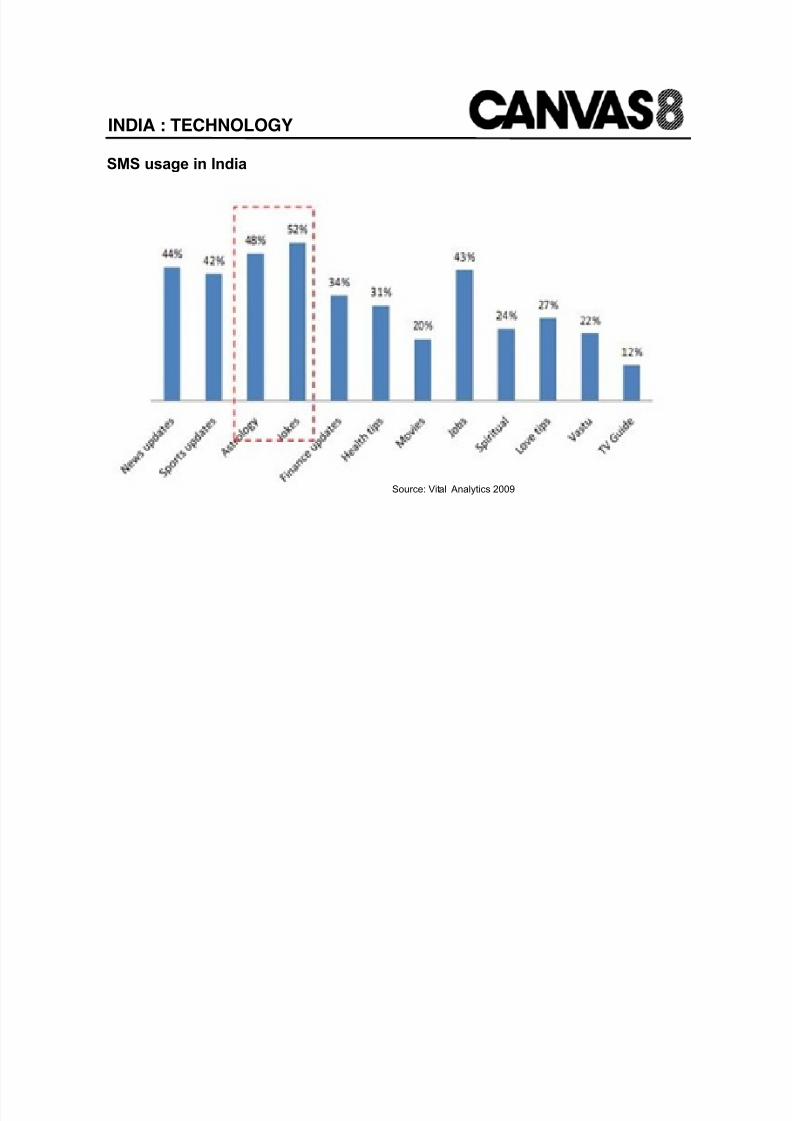

According to Vital Analytics, on average each Indian sends 29 SMS’every month. SMS is used as value-added services (VAS),marketing tool and to spam. Of all the services available, receiving jokes is the most popular in India.

*BA&U&HB?=D:&?32EJ;&=E&!EJ=2&

A:<)(#

L(&-%89#$:')54#G+:84-#

ZI#$:')54#G+:84-#

L:8E#`,)Q--:8#

$:.:,:5(#

Based on brand trust , consumer

preference and recall.Source: Brand Equity – Most TrustedBrands’ (MTB) 2009

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 29/30

8/8/2019 Canvaas_media India Report

http://slidepdf.com/reader/full/canvaasmedia-india-report 30/30

INDIA : SOURCES!

(1)! www.unhabitat.org (2)! www.economist.com (3)! www.mcdonaldsinindia.com (4)! http://lcweb2.loc.gov (5)! http://web.worldbank.org (6)! www.hindu.com (7)! www.bbc.co.uk (8)! www.ibef.org (9)! www.business-standard.com (10)!www.time.com (11)!www.ibef.org (12)!www.ibef.org (13)!http://contentsutra.com

(14)!http://technology.timesonline.co.uk

(15)!www.ibef.org (16)!www.ibef.org (17)! http://economictimes.indiatimes.com (18)!www.pluggd.in (19)!www.nytimes.com

Sources