canto annual meeting, punta cana, dom. rep., june 20, 2006 analysis of the caribbean submarine...

TRANSCRIPT

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Analysis of the Caribbean Analysis of the Caribbean Submarine Cable MarketSubmarine Cable Market

Presented by:Presented by:

Michael RuddyMichael Ruddy

Managing DirectorManaging Director

Terabit ConsultingTerabit Consulting

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Global Submarine Cable Global Submarine Cable Market DynamicsMarket Dynamics

3

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cable Capital: 1995Cable Capital: 1995

4

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cable Capital: 2000Cable Capital: 2000

5

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

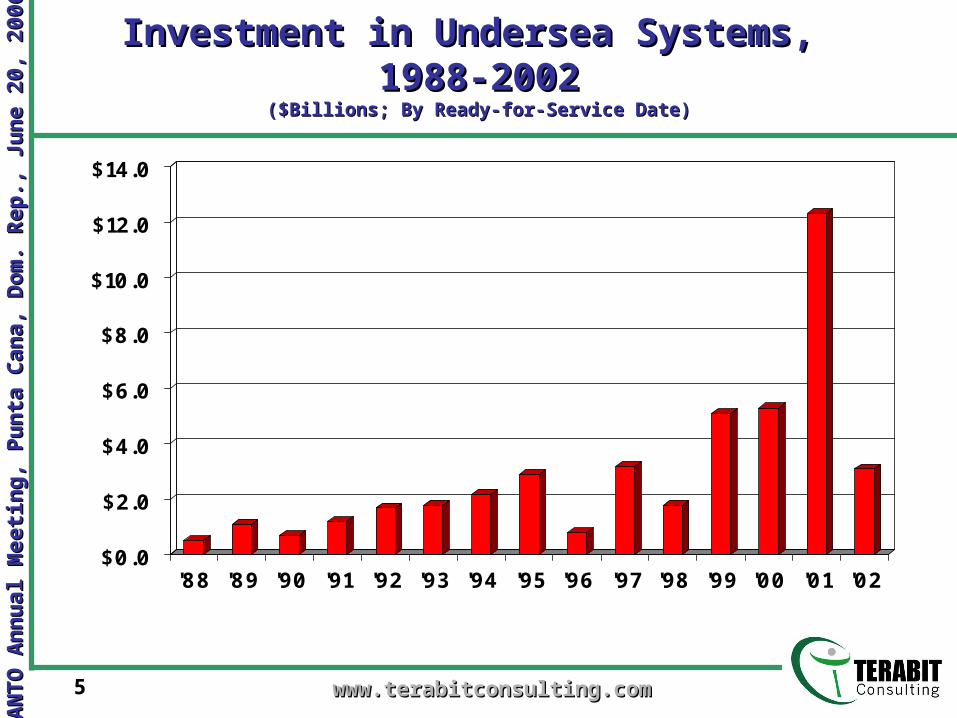

Investment in Undersea Systems, Investment in Undersea Systems, 1988-20021988-2002

($Billions; By Ready-for-Service Date)($Billions; By Ready-for-Service Date)

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

'88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02

6

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Economics after the Bubble BurstEconomics after the Bubble Burst

Bankruptcy, June 2001 360atlantic sold to Columbia VenturesBankruptcy, June 2001 360atlantic sold to Columbia Ventures

Bankruptcy, January 2002 Purchase by Singapore Bankruptcy, January 2002 Purchase by Singapore TechnologiesTechnologies

Bankruptcy, April 2002 Sale to Reliance GroupBankruptcy, April 2002 Sale to Reliance Group

Sale of assets to ReachSale of assets to Reach Reach (Telstra, PCCW) written Reach (Telstra, PCCW) written downdown

Bankruptcy, July 2002Bankruptcy, July 2002

Bankruptcy, November 2002Bankruptcy, November 2002 Sale to China Netcom Sale to China Netcom

7

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Post-2002: A Badly-Beaten MarketPost-2002: A Badly-Beaten Market

Market fell from $10+ billion per Market fell from $10+ billion per year to only a few hundred millionyear to only a few hundred million

Investors in south Asia and east Asia Investors in south Asia and east Asia stepped in to purchase global stepped in to purchase global networks at pennies on the dollarnetworks at pennies on the dollar

Cable operators’ new cost bases led Cable operators’ new cost bases led to unsustainable price erosionto unsustainable price erosion

8

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cable Capital: 2005Cable Capital: 2005

Asia: New Sphere of Influence

9

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

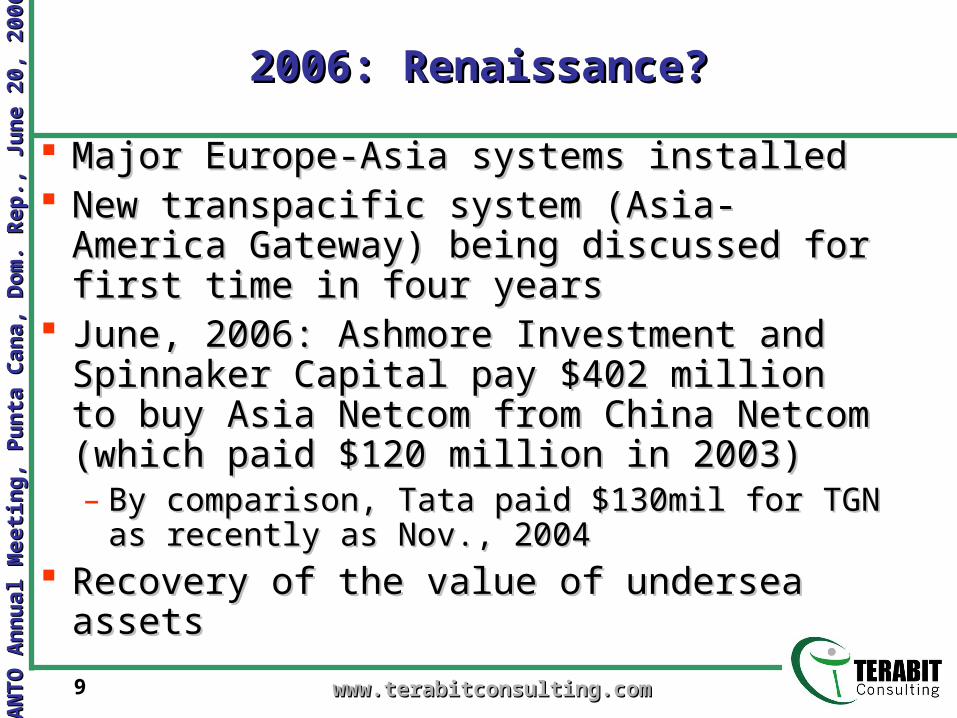

2006: Renaissance?2006: Renaissance?

Major Europe-Asia systems installedMajor Europe-Asia systems installed New transpacific system (Asia-America New transpacific system (Asia-America

Gateway) being discussed for first time Gateway) being discussed for first time in four yearsin four years

June, 2006: Ashmore Investment and June, 2006: Ashmore Investment and Spinnaker Capital pay $402 million to Spinnaker Capital pay $402 million to buy Asia Netcom from China Netcom buy Asia Netcom from China Netcom (which paid $120 million in 2003)(which paid $120 million in 2003)– By comparison, Tata paid $130mil for TGN By comparison, Tata paid $130mil for TGN

as recently as Nov., 2004as recently as Nov., 2004 Recovery of the value of undersea Recovery of the value of undersea

assetsassets

10

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Caribbean Submarine Cable Caribbean Submarine Cable Market DynamicsMarket Dynamics

11

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

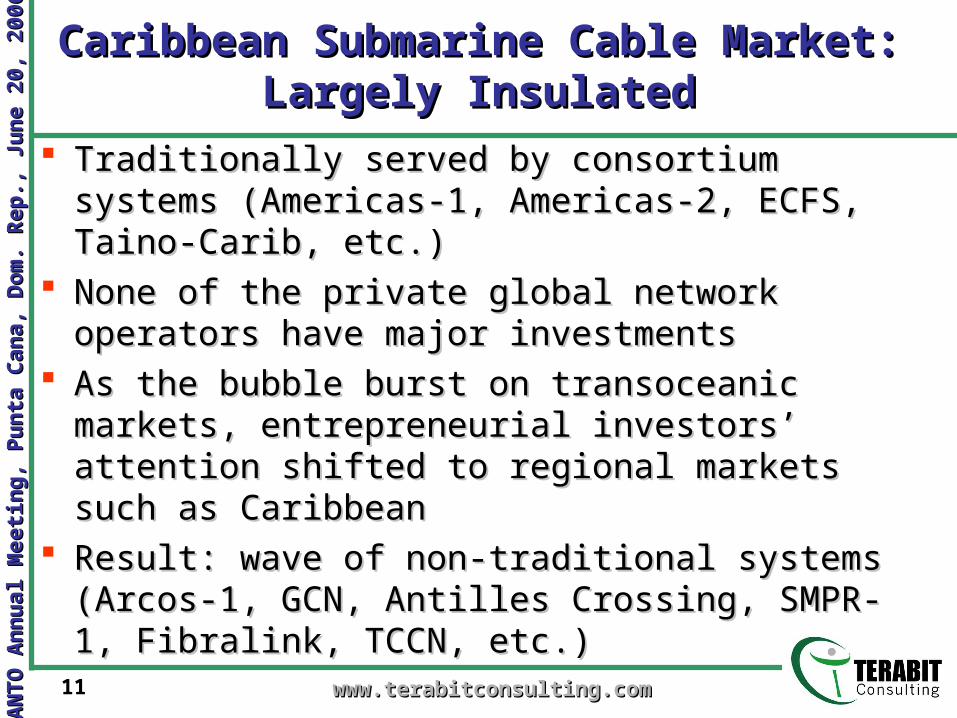

Caribbean Submarine Cable Caribbean Submarine Cable Market: Largely InsulatedMarket: Largely Insulated

Traditionally served by consortium Traditionally served by consortium systems (Americas-1, Americas-2, ECFS, systems (Americas-1, Americas-2, ECFS, Taino-Carib, etc.)Taino-Carib, etc.)

None of the private global network None of the private global network operators have major investmentsoperators have major investments

As the bubble burst on transoceanic As the bubble burst on transoceanic markets, entrepreneurial investors’ markets, entrepreneurial investors’ attention shifted to regional markets such attention shifted to regional markets such as Caribbeanas Caribbean

Result: wave of non-traditional systems Result: wave of non-traditional systems (Arcos-1, GCN, Antilles Crossing, SMPR-1, (Arcos-1, GCN, Antilles Crossing, SMPR-1, Fibralink, TCCN, etc.)Fibralink, TCCN, etc.)

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Analysis of Individual Analysis of Individual Submarine MarketsSubmarine Markets

13

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

MethodologyMethodology

Terabit Model of International Demand = Terabit Model of International Demand = dozens of specific variables used to dozens of specific variables used to forecast PSTN voice, voice-over-IP, forecast PSTN voice, voice-over-IP, private line, and Internetprivate line, and Internet

Impossible to paint the entire region with Impossible to paint the entire region with one brushstrokeone brushstroke– examines the specific dynamics of each market examines the specific dynamics of each market

and the opportunities that they present and the opportunities that they present submarine cable operatorssubmarine cable operators

Most important = sheer numbers (or Most important = sheer numbers (or potential) at the end-user level, and potential) at the end-user level, and competition at the carrier levelcompetition at the carrier level

BroadbandBroadband

14

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Analysis of Individual MarketsAnalysis of Individual Markets

Puerto RicoPuerto Rico Dominican RepublicDominican Republic JamaicaJamaica Trinidad and TobagoTrinidad and Tobago HaitiHaiti French DOMFrench DOM BarbadosBarbados BahamasBahamas CubaCuba ECTEL countriesECTEL countries

15

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Puerto Rico:Puerto Rico: Demand for Int’l. Demand for Int’l.

CapacityCapacity

High competition: fully-liberalized market High competition: fully-liberalized market with 6 mobile operators, 20 ISPs with 6 mobile operators, 20 ISPs

Over 1 million Internet usersOver 1 million Internet users Several cable modem providers: Liberty Several cable modem providers: Liberty

had 35,000 broadband subscribers as of had 35,000 broadband subscribers as of YE05 and doubled its access speed; other YE05 and doubled its access speed; other providers include Choice Cable TV and providers include Choice Cable TV and OneLinkOneLink

DSL has been offered by PRT/Verizon since DSL has been offered by PRT/Verizon since 2001; estimated 80k-100k subscribers2001; estimated 80k-100k subscribers

16

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Puerto Rico:Puerto Rico: Supply of Int’l. Capacity Supply of Int’l. Capacity

Americas-II Americas-II (2000), (2000), EmergiaEmergia (2001) and (2001) and Arcos-1Arcos-1 (2001) to US, Caribbean, and (2001) to US, Caribbean, and South AmericaSouth America

Taino-CaribTaino-Carib (1992) to Virgin Islands; (1992) to Virgin Islands; Antillas-1 Antillas-1 (1997) to Dominican Republic; (1997) to Dominican Republic; SMPR-1SMPR-1 to Saint Maarten (2005); to Saint Maarten (2005); Global Global Caribbean NetworkCaribbean Network (2006) to (2006) to Guadeloupe and Virgin IslandsGuadeloupe and Virgin Islands

Planned: Planned: TCCNTCCN to US, Mexico, Caribbean, to US, Mexico, Caribbean, and South Americaand South America

17

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Puerto Rico:Puerto Rico: Submarine Cable Submarine Cable

OutlookOutlook

North American design capacity > 2 TbpsNorth American design capacity > 2 Tbps On a supply-vs.-demand basis, Puerto Rico On a supply-vs.-demand basis, Puerto Rico

is relatively well-offis relatively well-off However, high level of competition However, high level of competition

(proliferation of operators and ISPs) (proliferation of operators and ISPs) necessitates multiple sources of necessitates multiple sources of intercontinental capacity intercontinental capacity

18

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Dominican Republic:Dominican Republic: Demand for Int’l. Demand for Int’l.

CapacityCapacity

Verizon Dominicana estimated to have 88% of Verizon Dominicana estimated to have 88% of fixed-line market, 84% of Internet market, and fixed-line market, 84% of Internet market, and 64% of mobile market64% of mobile market

Mobile market served by Verizon, Orange Mobile market served by Verizon, Orange (France Telecom), Tricom, Centennial(France Telecom), Tricom, Centennial

Indotel approved sale of Verizon Domicana to Indotel approved sale of Verizon Domicana to America Movil of Mexico (Carlos Slim) in May of America Movil of Mexico (Carlos Slim) in May of 20062006

23 fixed + mobile licenses issued as of 2006, 23 fixed + mobile licenses issued as of 2006, according to Indotelaccording to Indotel

Increasing penetration of DSLIncreasing penetration of DSL

19

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Dominican Republic:Dominican Republic: Supply of Int’l. Capacity Supply of Int’l. Capacity

Antillas-1 Antillas-1 (1997) to Puerto Rico(1997) to Puerto Rico Arcos-1Arcos-1 (2001) to US, Caribbean, Central (2001) to US, Caribbean, Central

America, and South AmericaAmerica, and South America Columbus Communications’ Columbus Communications’ FibralinkFibralink

system to Jamaica was activated in April, system to Jamaica was activated in April, 20062006

Planned: Planned: TCCNTCCN to US, Mexico, Caribbean, to US, Mexico, Caribbean, and South Americaand South America

20

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Dominican Republic:Dominican Republic: Submarine Cable Submarine Cable

OutlookOutlook

Arcos-1 design capacity = 960 Gbps: Arcos-1 design capacity = 960 Gbps: theoretically, enough intercontinental theoretically, enough intercontinental capacitycapacity

In the short-term, any new systems will In the short-term, any new systems will likely require the participation of (or likely require the participation of (or commitments from) America Movilcommitments from) America Movil

In the long-term, higher market share on In the long-term, higher market share on the part of competitors will necessitate the part of competitors will necessitate alternative international infrastructurealternative international infrastructure

21

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Jamaica:Jamaica: Demand for Int’l. Demand for Int’l.

CapacityCapacity Competition was first introduced in 2000; C&W Competition was first introduced in 2000; C&W

monopoly ended in 2003monopoly ended in 2003 According to the Office of Utilities Regulation, According to the Office of Utilities Regulation,

licenses have been issued to 35 domestic carriers, licenses have been issued to 35 domestic carriers, 68 international carriers, and 83 ISPs68 international carriers, and 83 ISPs

C&W remains dominant in fixed-line market C&W remains dominant in fixed-line market Digicel was awarded the first competitive mobile Digicel was awarded the first competitive mobile

license in 2001 and has since gone head-to-head license in 2001 and has since gone head-to-head with C&W in Jamaica and throughout the regionwith C&W in Jamaica and throughout the region

C&W ADSL = leading broadband offering, but C&W ADSL = leading broadband offering, but “the size of the broadband market is small.” – “the size of the broadband market is small.” – C&W, March 2006C&W, March 2006

OUR is expected to rule soon on the unbundling of OUR is expected to rule soon on the unbundling of C&W’s local loop C&W’s local loop

Over 2 million mobile subs; target of 40% Internet Over 2 million mobile subs; target of 40% Internet penetration by 2011penetration by 2011

22

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Jamaica:Jamaica: Supply of Int’l. Capacity Supply of Int’l. Capacity

Existing capacity limited: Existing capacity limited: TCS-1TCS-1 was was removed from service in 2003; only other removed from service in 2003; only other link until this year was link until this year was Cayman-Jamaica Cayman-Jamaica Fibre System (1997)Fibre System (1997)

Columbus Communications’ Columbus Communications’ FibralinkFibralink system to Dominican Republic was activated system to Dominican Republic was activated in April, 2006; connected North America via in April, 2006; connected North America via Arcos (Columbus owns New World Network)Arcos (Columbus owns New World Network)

Planned: Planned: TCCNTCCN to US, Mexico, Caribbean, to US, Mexico, Caribbean, and South America (and South America (DigicelDigicel’s submarine ’s submarine cable license was not granted)cable license was not granted)

23

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Jamaica:Jamaica: Submarine Cable Submarine Cable

OutlookOutlook

It is expected that unbundling and the It is expected that unbundling and the proliferation of competitive licenses will have proliferation of competitive licenses will have a strong impact on international demanda strong impact on international demand

In January of 2005, submarine cable licenses In January of 2005, submarine cable licenses were awarded to Fibralink and TCCNwere awarded to Fibralink and TCCN

Design capacity of Fibralink is 320 GbpsDesign capacity of Fibralink is 320 Gbps Jamaica is arguably the Caribbean’s leading Jamaica is arguably the Caribbean’s leading

candidate for additional submarine candidate for additional submarine deploymentdeployment

24

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Trinidad and Tobago Trinidad and Tobago Demand for Int’l. CapacityDemand for Int’l. Capacity

TSTT = 51% gov’t. holding / 49% C&WTSTT = 51% gov’t. holding / 49% C&W 323k fixed lines (25% teledensity)323k fixed lines (25% teledensity) C&W/Bmobile = mobile service since 1991C&W/Bmobile = mobile service since 1991 Digicel, Laqtel receive licenses (2005)Digicel, Laqtel receive licenses (2005) 2-for-1 promotion causes chaos (12/05)2-for-1 promotion causes chaos (12/05) Mobile penetration > 50% (650k + subs)Mobile penetration > 50% (650k + subs) Internet: 160k users, 9 major ISPsInternet: 160k users, 9 major ISPs 5k DSL (TTST), 2k cable modem subs 5k DSL (TTST), 2k cable modem subs

(CCTT), 2k B/B fixed wireless (Carib Link, (CCTT), 2k B/B fixed wireless (Carib Link, Lisa Communications), GPRS, WiFiLisa Communications), GPRS, WiFi

25

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Trinidad and Tobago Trinidad and Tobago Submarine Cable OutlookSubmarine Cable Outlook

Americas-1 Americas-1 (1.7 Gbps, 1994)(1.7 Gbps, 1994) ECFSECFS (2.5 Gbps, 1995) (2.5 Gbps, 1995) Americas-2Americas-2 (40 Gbps, 2000) (40 Gbps, 2000) Groupe LoretGroupe Loret, , Antilles CrossingAntilles Crossing, and , and

TCCNTCCN are among the planned systems are among the planned systems The most important market in the The most important market in the

southeastern Caribbeansoutheastern Caribbean Any new system to the southeast will be Any new system to the southeast will be

required to capture a share of Trinidadian required to capture a share of Trinidadian traffic in order to be viabletraffic in order to be viable

26

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Haiti:Haiti: Submarine Cable Submarine Cable

OutlookOutlook Teleco maintains fixed-line monopolyTeleco maintains fixed-line monopoly Comcel and Haitel dominate mobile market, but Comcel and Haitel dominate mobile market, but

Digicel launched a GSM network in May of 2006Digicel launched a GSM network in May of 2006 55thth-largest mobile market in Caribbean-largest mobile market in Caribbean Economic restraints and political turmoil have Economic restraints and political turmoil have

posed a major obstacle to telecommunications posed a major obstacle to telecommunications development (80% of country lives in poverty)development (80% of country lives in poverty)

Market has been neglected by undersea operatorsMarket has been neglected by undersea operators BSDNiBSDNi (2006) has a node in Port-au-Prince (2006) has a node in Port-au-Prince Planned: Planned: TCCNTCCN Telecommunications and submarine capacity Telecommunications and submarine capacity

market locked in chicken-and-the-egg cycle market locked in chicken-and-the-egg cycle

27

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Martinique/Guadeloupe Martinique/Guadeloupe Submarine Cable OutlookSubmarine Cable Outlook

Markets fully liberalized with EU in 1998Markets fully liberalized with EU in 1998 Fixed-line market: France Télécom, XTS, OutremerFixed-line market: France Télécom, XTS, Outremer Mobile market: Orange, Bouygues, OutremerMobile market: Orange, Bouygues, Outremer Internet: 1/3 penetration rate; ISPs include FT, Internet: 1/3 penetration rate; ISPs include FT,

Outremer, Mediaserv, NetCaraibes, XTS, MTVCOutremer, Mediaserv, NetCaraibes, XTS, MTVC Broadband: about 20k DSL subs; cable modem Broadband: about 20k DSL subs; cable modem

service; fixed-wirelessservice; fixed-wireless Capacity: Capacity: Americas-2Americas-2 (40 Gbps, 2000) to (40 Gbps, 2000) to

Martinique, Martinique, ECFSECFS to Martinique and Guadeloupe to Martinique and Guadeloupe GCNGCN: Conseil R: Conseil Régionalégional awarded “public services awarded “public services

delegation” BOT contract to Groupe Loret for delegation” BOT contract to Groupe Loret for undersea cable development = Guadeloupe undersea cable development = Guadeloupe NumNumériqueérique

28

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Barbados Barbados Submarine Cable OutlookSubmarine Cable Outlook

C&W = dominant operator, 137k fixed linesC&W = dominant operator, 137k fixed lines 2005 – Movement in mobile sector: Digicel acquires 2005 – Movement in mobile sector: Digicel acquires

Cingular, Laqtel bids for Sunbeach; Market > 200k Cingular, Laqtel bids for Sunbeach; Market > 200k lineslines

Telebarbados building up fixed line business (2006)Telebarbados building up fixed line business (2006) Internet: 160k users, 6 major ISPs; 11k DSL (C&W, Internet: 160k users, 6 major ISPs; 11k DSL (C&W,

Sunbeach), GPRSSunbeach), GPRS Until this year, Until this year, ECFSECFS was only source of undersea was only source of undersea

capacitycapacity Sept.Sept., 2004: Submarine cable licenses awarded to , 2004: Submarine cable licenses awarded to

Antilles CrossingAntilles Crossing and and EC-1 (Island FibreEC-1 (Island Fibre; now ; now Southern CaribbeanSouthern Caribbean))

29

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Bahamas:Bahamas: Demand for Int’l. Demand for Int’l.

CapacityCapacity Telecom sector not liberalized – BTC controls fixed Telecom sector not liberalized – BTC controls fixed

line and mobile marketsline and mobile markets 150k Internet users; however, BTC ADSL 150k Internet users; however, BTC ADSL

deployment stood at only 11,109 subs as of YE04 deployment stood at only 11,109 subs as of YE04 and growth has been sluggishand growth has been sluggish

Most viable telecom/Internet competition is Cable Most viable telecom/Internet competition is Cable Bahamas, which has offered Internet access since Bahamas, which has offered Internet access since 2000 2000

Both BTC and Cable Bahamas have invested heavily Both BTC and Cable Bahamas have invested heavily in undersea infrastructurein undersea infrastructure

BTC signed a $60 million contract with Tyco in BTC signed a $60 million contract with Tyco in September of 2005 for the construction of the September of 2005 for the construction of the Bahamas Domestic Submarine Network (BDSNi) Bahamas Domestic Submarine Network (BDSNi)

Cable Bahamas’ Caribbean Crossings subsidiary Cable Bahamas’ Caribbean Crossings subsidiary owns BICS and Fibralink Jamaica owns BICS and Fibralink Jamaica

30

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Bahamas:Bahamas: Submarine Cable Submarine Cable

OutlookOutlook

Bahamas-II Bahamas-II (1997), (1997), Arcos-1Arcos-1 (2001), and (2001), and BICS (2001)BICS (2001) to US and Caribbean to US and Caribbean

BSDNiBSDNi (2006) to Haiti (2006) to Haiti Planned: Planned: TCCNTCCN to US, Mexico, Caribbean, to US, Mexico, Caribbean,

and South Americaand South America The privatization of BTC may invigorate The privatization of BTC may invigorate

telecom sector; until then, competition and telecom sector; until then, competition and demand will be limited demand will be limited

Total design capacity to North America = Total design capacity to North America = approximately 1 Gbpsapproximately 1 Gbps

31

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cuba: Cuba: Demand for Int’l. Demand for Int’l.

CapacityCapacity Restrictions on Internet access imposed in Restrictions on Internet access imposed in

2004 limit subscriptions to foreigners, 2004 limit subscriptions to foreigners, academics, and top-level bureaucratsacademics, and top-level bureaucrats

Internet is also available at Internet cafes, but Internet is also available at Internet cafes, but access costs US$6/hr. (avg. salary = access costs US$6/hr. (avg. salary = US$15/mo.)US$15/mo.)

Gov’t. argues that the island’s limited Gov’t. argues that the island’s limited bandwidth necessitates “prioritization” of bandwidth necessitates “prioritization” of Internet users in order to ensure that sectors Internet users in order to ensure that sectors such as education and health are able to get such as education and health are able to get on-lineon-line

Because of black market, Cuban Internet Because of black market, Cuban Internet usage population is estimated at 200k to 500kusage population is estimated at 200k to 500k

32

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cuba: Cuba: Supply of Int’l. CapacitySupply of Int’l. Capacity

Primary links are via satellite between the Primary links are via satellite between the Caribe Earth Station in Havana and Caribe Earth Station in Havana and Canada and ItalyCanada and Italy

Since 1994, AT&T has operated a WWII-Since 1994, AT&T has operated a WWII-era copper submarine cable with a few era copper submarine cable with a few hundred circuitshundred circuits

Florida-based QuestNet proposed Projecto Florida-based QuestNet proposed Projecto Unidad undersea cable to Florida in 1999Unidad undersea cable to Florida in 1999

Blue Telecommunications, which had been Blue Telecommunications, which had been bidding for a stake in BTC, proposed Cuba-bidding for a stake in BTC, proposed Cuba-Bahamas cable in 2003Bahamas cable in 2003

Arcos expansion?Arcos expansion?

33

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Cuba: Cuba: Submarine Cable OutlookSubmarine Cable Outlook

Demand for capacity is restrained by the Demand for capacity is restrained by the United States’ embargo and by Cuba’s United States’ embargo and by Cuba’s information security laws information security laws

High potential: largest population in High potential: largest population in Caribbean (11 million) and fixed-line market Caribbean (11 million) and fixed-line market is third-largest in Caribbean, after Puerto is third-largest in Caribbean, after Puerto Rico and Dominican Republic (800k lines)Rico and Dominican Republic (800k lines)

Although there are several schemes to Although there are several schemes to provide undersea capacity to the island, provide undersea capacity to the island, there are unlikely to be any new systems there are unlikely to be any new systems deployed before the end of the Bush deployed before the end of the Bush administration administration

34

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

ECTEL States: ECTEL States: Demand for Int’l. Demand for Int’l.

CapacityCapacity Dominica, Grenada, Saint Kitts and Nevis, Dominica, Grenada, Saint Kitts and Nevis,

Saint Lucia, and Saint Vincent and The Saint Lucia, and Saint Vincent and The Grenadines Grenadines

The World Bank is working with ECTEL to The World Bank is working with ECTEL to promote connectivity to the regionpromote connectivity to the region– Terabit and partner firm Axiom of Paris Terabit and partner firm Axiom of Paris

recently completed feasibility analysis of an recently completed feasibility analysis of an eastern Caribbean cableeastern Caribbean cable

– Conclusion: the region needs at least one Conclusion: the region needs at least one alternative to ECFSalternative to ECFS

– New system must capture some of the market New system must capture some of the market from Trinidad and Barbadosfrom Trinidad and Barbados

Southern Caribbean closed tender process Southern Caribbean closed tender process in April: €20-30 mil systemin April: €20-30 mil system

35

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

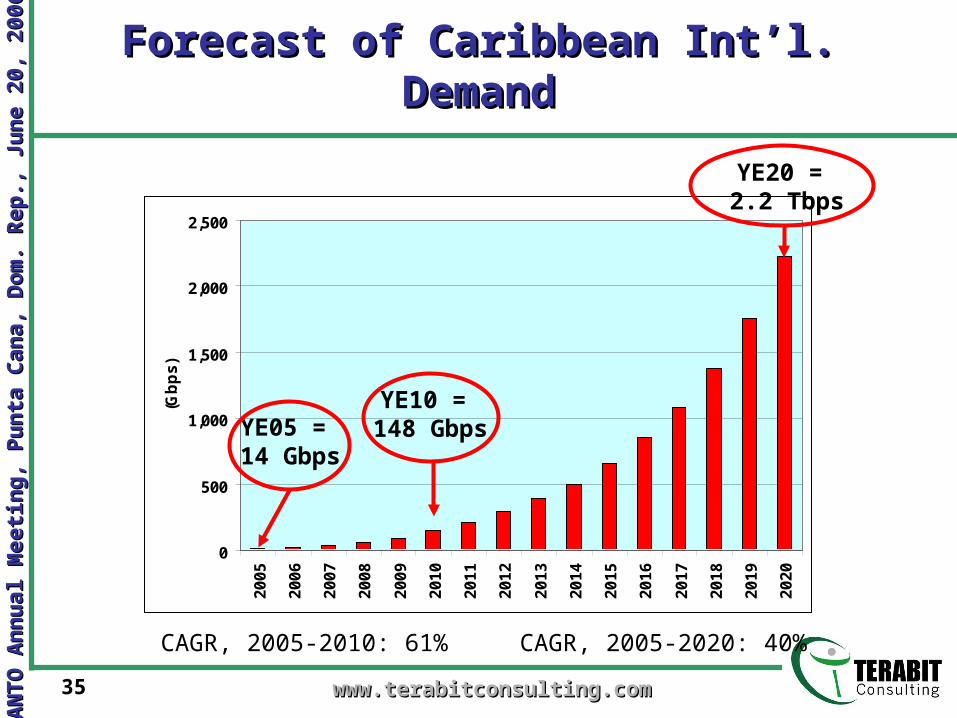

Forecast of Caribbean Int’l. Forecast of Caribbean Int’l. DemandDemand

0

500

1,000

1,500

2,000

2,500

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

(Gb

ps

)

CAGR, 2005-2010: 61% CAGR, 2005-2020: 40%

YE05 = 14 Gbps

YE10 = 148 Gbps

YE20 = 2.2 Tbps

36

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

ConclusionsConclusions

The Caribbean market has largely been insulated from The Caribbean market has largely been insulated from the trends in the global submarine cable market the trends in the global submarine cable market

With the exception of Arcos and TCCN, undersea With the exception of Arcos and TCCN, undersea systems have targeted individual markets and nichessystems have targeted individual markets and niches

Demand forecast: YE2010=148 Gbps; 2020=2.2 TbpsDemand forecast: YE2010=148 Gbps; 2020=2.2 Tbps Beyond systems that are already under development, Beyond systems that are already under development,

the most attractive markets for additional investment the most attractive markets for additional investment are are JamaicaJamaica, , Puerto RicoPuerto Rico, and , and CubaCuba– Near-term: Near-term: BahamasBahamas, once privatization and liberalization take , once privatization and liberalization take

place; place; TrinidadTrinidad; and ; and Dominican RepublicDominican Republic– Long-term: Long-term: Haiti, Haiti, eastern markets (eastern markets (ECTELECTEL//BarbadosBarbados) and ) and

French DOMFrench DOM Strategy: cable developers must partner with operatorsStrategy: cable developers must partner with operators

37

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

CA

NTO

An

nu

al M

eeti

ng

, P

un

ta C

an

a,

Dom

. R

ep

., J

un

e 2

0,

20

06

www.terabitconsulting.comwww.terabitconsulting.com

Thank You!Thank You!

Michael RuddyMichael RuddyTerabit Consulting, Inc.Terabit Consulting, Inc.

First Street CenterFirst Street Center245 First Street, 18245 First Street, 18thth Floor Floor

Cambridge, Massachusetts 02142 USACambridge, Massachusetts 02142 USATel.: +1 (617) 444-8605Tel.: +1 (617) 444-8605Fax: +1 (617) 444-8405Fax: +1 (617) 444-8405

Email: [email protected]: [email protected]://www.terabitconsulting.comhttp://www.terabitconsulting.com