can the financial sector deliver?

TRANSCRIPT

1

INDIA’S ECONOMIC AMBITIONS:

Can the Financial Sector Deliver?

Ratna SahayMonetary & Capital Markets Department

International Monetary Fund

FICCI

March 12th, 2019, New Delhi

Outline

• India’s Financial System: Taking Stock

• Recent Reforms: What Has Been Done?

• Strengthening the Financial System: What Next?

2

“The world’s second-most-populous country has been

flirting with a Lehman moment”

–The Economist (November 2018)

3

India’s Financial System: Taking Stock

4

Economic Backdrop

5

183.5

136.2

90

100

110

120

130

140

150

160

170

180

190

2010 2011 2012 2013 2014 2015 2016 2017 2018

G-20 Peers Range India G-20 Peers Median 1/

Real Growth: India and G20 Peers(Index, Seasonally Adjusted, 2010-Q1=100)

Sources: Haver Analytics and IMF Staff CalculationsIndia's G-20 peers are Brazil, Russia, China, South Africa, Indonesia and Turkey

7.2 7.3

21.2

13.4

0

5

10

15

20

25

2010-13 2014-17

Avg. GDP growth Poverty Rate

India: GDP growth and poverty rate(In percent)

Sources: Haver Analytics and World Bank Group, Poverty and Equity Data Portal.Note: Poverty rate is based on the international poverty line (2011 PPP, $1.9 per person per day).

2011

2015

Economic Backdrop

6

70.1

69.8

69.7

69.8

69.9

70.0

70.1

2010-2013 2014-2017

Gross Debt (% of GDP)

Source: Haver Analytics

-3.4

-1.2

-7.9-7.2

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

2010-2013 2014-2017

External Current Account and Fiscal Balance

Current Account Balance (% of GDP) Fiscal Balance

Source: World Economic Outlook

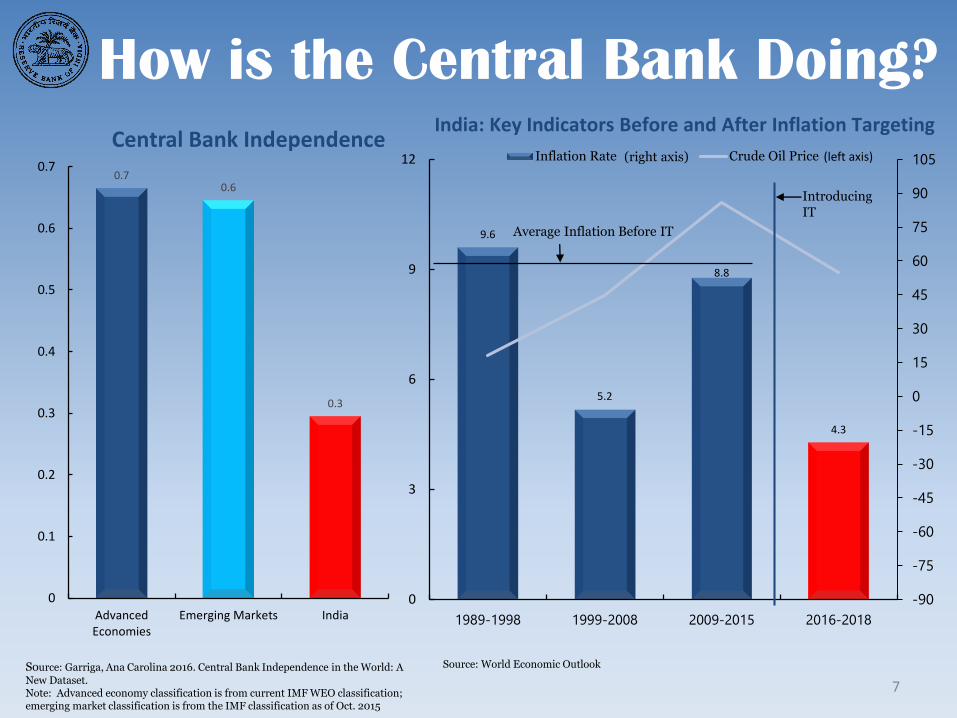

How is the Central Bank Doing?

7

0.70.6

0.3

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

AdvancedEconomies

Emerging Markets India

Central Bank Independence

Source: Garriga, Ana Carolina 2016. Central Bank Independence in the World: A

New Dataset. Note: Advanced economy classification is from current IMF WEO classification; emerging market classification is from the IMF classification as of Oct. 2015

9.6

5.2

8.8

4.3

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

90

105

0

3

6

9

12

1989-1998 1999-2008 2009-2015 2016-2018

Inflation Rate Crude Oil Price

India: Key Indicators Before and After Inflation Targeting

Source: World Economic Outlook

Introducing IT

Average Inflation Before IT

(right axis) (left axis)

How is the Central Bank Doing?

8

3.31

5.65

-0.14

4.84

9.60

-2

0

2

4

6

8

10

12

14

Inflation and Consensus Forecasts(Percent, year-on-year)

Headline Core-Core Food Consensus Expectations (1 year ahead) HH Expectations (1 year ahead)

Source: India IMF Article IV Staff Report, 2018

Are Financial Markets Competitive?

9

Countries Dominated by State-Owned Banks

BhutanChina

India

Belarus

LibyaEgypt Algeria Costa Rica

Turkmenistan

So

urc

e: B

art

h, C

ap

rio

& L

evin

e (2

00

6)

Are Financial Markets Competitive?

10

100

55

32

12

55

10

0

20

40

60

80

100

120

UnitedStates

Korea Brazil India IndiaPrivateSectorBanks

IndiaPublicSectorBanks

Productivity of Bank Employees(Number of transactions/hour)

5.0%

4.0%

3.4%

2.4%

0%

1%

2%

3%

4%

5%

6%

India Thailand China Singapore

Intermediation Costs(lending-deposit spread)

So

urc

e: B

art

h, C

ap

rio

& L

evin

e (2

00

6)

So

urce

: McK

insey

Stu

dy

(20

01)

Source: Report of the Committee of Financial Sector Reforms, GOI (2008)

Are Financial Markets Deep?

11

50

100

150

200

250

300

50

100

150

200

250

300

Au

g-1

0

Jul-

11

Jun

-12

May-1

3

Ap

r-14

Mar-

15

Feb

-16

Jan

-17

Dec-

17

No

v-1

8

Brazil China Russia India (SENSEX)

Stock Market Indices(June 1, 2009 = 100)

Source: Bloomberg Financial Markets L.P.

Are Financial Markets Deep?

12

3.7

22.1 22.5

0

5

10

15

20

25

30

Pensions Life Insurance

Long term Institutional Investors(2012, Percent of GDP)

India U.S.

Source: Mercer, OECD, Allianz Global Investors, IMF Staff estimates

43.046.0

68.6

81.1

108.8

142.3

-

20

40

60

80

100

120

140

160

Indonesia Brazil India Korea SouthAfrica

UnitedStates

Equity Market Value-to-GDP Ratio (2018)

Source: Bloomberg, Haver Analytics

Are Financial Markets Deep?

13

38.749.7

59.7

136.2147.7

155.8

192.2

0

50

100

150

200

250

Indonesia India Brazil UnitedKingdom

South Africa China United States

Domestic Credit to Private Sector 2017(Percent of GDP)

Source: World Development Indicators

Does the Financial Sector Serve the Population?

14

Growth of Aadhaar Accounts, 2012-2017 Growth of Bank Accounts, 2014-2017

Does the Financial Sector Serve the Population?

15

Financial Inclusion and Gender Gap

Source: IMF staff calculations based on the 2017 Global Findex.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

share of adults with an account (men)

shar

e o

f ad

ult

s w

ith

an

acc

ou

nt

(wo

men

)

Philippines

Georgia

Turkey

Mongolia

Argentina

Bangladesh

Jordan

Pakistan

UAE

Lao PDR

Denmark

Myanmar

Namibia

Bolivia

Sri Lanka

Nigeria

South Sudan

India

Is There a Tradeoff Between Financial Inclusion

and Financial Stability?

16

Financial Inclusion and Financial Stability

Source: “Financial Inclusion: Can It Meet Multiple Macroeconomic Goals?” Ratna Sahay et al. SDN 15/17 IMF September 2015

Are Banks Sound Enough to Finance the

Real Economy?

17Source: Reserve Bank of India, and IMF Staff estimates.

-10

-5

0

5

10

15

20

25

30

-10

-5

0

5

10

15

20

25

30

Mar-16Mar-17Mar-18 Sep-18 Mar-16Mar-17Mar-18 Sep-18 Mar-16Mar-17Mar-18 Sep-18

Public sector banks Private banks Foreign banks

Credit growth (yoy change)

NPA ratio

Non-Performing Assets and Credit Growth(In percent)

Are Banks Sound Enough to Finance

the Real Economy?

18

Return on Assets(Percent)

0.4

-0.3-0.2

1.61.6

1.5

1.8

1.4

1.7

-0.5

0.0

0.5

1.0

1.5

2.0

Mar-15 Mar-16 Mar-17

Public sector banks Private sector banks

Foreign banks Aggregate

8.79.1 9.5

12.8 13.2 13.4

15.315.9

17.1

0

3

6

9

12

15

18

Mar-15 Mar-16 Mar-17

Public sector banks Private sector banks

Foreign banks Aggregate

Regulatory Tier 1 Capital Adequacy Ratio(Percent)

Source: Reserve Bank of India, and IMF Staff estimates.

Are Corporates Sound Enough to Contribute to Growth?

19

Indian corporate leverage is among the highest across emerging markets…

BRAARG

RUS IND

TUR

IDNKORCHN

THA

MEXCOL

ZAFPOL

HUN

KAZ

PHL

VIE

PER

CRO

CZE

EGY

ROM

NIG

MYS

0

20

40

60

80

100

120

140

160

180

0 20 40 60 80 100 120 140 160 180

Corporate Leverage, Selected EMs(Debt-to-Equity Ratio, top quartile)

2014

20

15

Source: IMF, Corporate Vulnerability Utility.

Are Corporates Sound Enough to Contribute to Growth?

20

… with leverage particularly high across the largest corporates, and debt-at-risk levels edging up.

0

40

80

120

160

0

10

20

30

40

50

FY

2015

FY

2016

FY

2017*

FY

2015

FY

2016

FY

2017* .

Debt-at-Risk Leverage

Corporate Sector Vulnerabilities(In percent)

Top 50 firms All other firms

Sources: CapitalIQ; and IMF staff estimates.Note: Based on a sample of 1,826 firms. 2017 estimates reflect each firm's latest available quarter. Topfirms determined based on latest total assets. Leverage is median debt-to-equity ratio in each group(no firms with negative equity). Debt-at-risk is the share of debt of firms with ICR less than 1.

Are Corporates Sound Enough to Contribute to Growth?

21

Corporates are exposed to external shocks through external commercial borrowings...

1/ Other local securities include commercial paper (CP) and syndicated loans.

11.6 11.5 12.3 12.7 12.7 11.3 11.1

70.9 69.8 69.3 66.8 65.7 64.0 64.5

17.6 18.7 18.4 20.4 21.6 24.7 24.4

0

10

20

30

40

50

60

70

80

90

100

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

Outstanding Corporate Debt in India 1/

(In percent of total corporate funding)

ECBs Bank Credit Local bonds & CPs

Are Corporates Sound Enough to Contribute to Growth?

22

… but dependence on external foreign-currency funding has declined considerably

0

2

4

6

8

10

12

14

FY20

05

FY20

06

FY20

07

FY20

08

FY20

09

FY20

10

FY20

11

FY20

12

FY20

13

FY20

14

FY20

15

FY20

16

FY20

17

Overseas Borrowing of Indian Corporates(In billions of U.S. Dollars)

Rupee-Denominated Bonds (RDB; external) External Commercial Borrowing (ECB; in foreign currency)

Sources: Reserve Bank of India; IMF, Financial Soundness Indicators; IMF, Corporate Vulnerability Utility; and IMF staff estimates

Can the Non-Bank Sector Pick Up the Slack?

23

23.6

30.7

3.13.8

20.0

22.0

6.05.0

0

5

10

15

20

25

30

35

NBFC-D NBFC-ND-SI NBFC-D NBFC-ND-SI

CAR NPAs

Mar-12 Mar-17

NBFCs Financial Soundness Indicators(Percent)

Scheduled commercial

banks, 81Rural banks and cooperatives, 9

Non-banking financial

companies, 12

Insurance companies, 18

Pension and mutual funds, 15

Financial System Structure (In percent of GDP, March 2017)

Sources: India Article IV IMF Staff Report (2017)

60%

11%

13%

9%

7%

(Share of total)

Sources: Bloomberg; Reserve Bank of India; Insurance Regulatory and Development Authority of India and Securities Exchange Board of India

Can the Non-Bank Sector Pick Up the Slack?

24

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00

United States

China

South Korea

Brazil

India

Indonesia

South Africa

Issuance of Non-Financial Corporates (% of GDP)

2018 2013

16.3

11.3

-

5.0

10.0

15.0

20.0

25.0

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Mar-

17

Sep

-17

Mar-

18

Sep

-18

Contribution to growth (bank) Contribution to growth (NBFC) NBFC loans and advances (y/y change) Bank non-food credit (y/y change)

Sources: RBI and staff estimates.

Credit Growth(Annual percent change)

Challenges in the Non-Bank Sector

25

63.7

45.9

58.0

49.9 49.2

26.0

15.3 13.9

8.1

17.0 17.1

19.1

20.3

0

10

20

30

40

50

60

70

Co

nst

ruct

ion

Meta

ls

Text

iles

Gem

s &

Jew

elr

y

Pap

er

Infr

ast

ruct

ure

Ch

em

icals

Cem

en

t

Au

to &

Tra

nsp

ort

En

gin

eeri

ng

Oth

ers

Fo

od

Pro

cess

ing

Bev &

To

bacc

o

Corporate Sector Debt-at-Risk(In percent of sectoral debt, 2016)

Sources: CapitalIQ; and IMF staff estimates.Note: Debt-at-risk is debt of firms with interest coverage ratio—multiple of earnings before interest, taxes, depreciation and amortization (EBITDA) relative to interest expenses—below one.

All sectors

Infrastructure38.8

Retail loans14.2

Industries11.7

Transport6.4

Commercial real estate

5.4

Others23.4

NBFCs Loans by Sector(Percent, March 2017)

Sources: Bloomberg; Reserve Bank of India; Insurance Regulatory and Development Authority of India and Securities Exchange Board of India

Challenges in the Non-Bank Sector

26

Network plot of the financial system (March 2018)

44.8 44.4 45.9 43.0 46.0

28.3 28.0 25.5 26.9 22.3

5.2 4.9 5.0 6.8 9.1

21.6 22.7 23.6 23.2 22.6

0

10

20

30

40

50

60

70

80

90

100

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

NBFC: Sources of Funding(percent of total borrowing)

Debentures Bank borrowings

Commercial paper Other

Sources: RBI and staff calculations.Source: India FSSA IMF Report, 2017Note: PSBs: Public sector banks, UCBs: Urban commercial banks, HFCs: Housing Finance companies, NBFCs: Non-bank financial corporations, AFIs: All India Financial Institutions, PFs: Private Pension Funds, AMC-MFS: Asset management companies and mutual funds, FBs: Foreign banks, PVBs: Private banks, Insurance cos: Insurance companies

Macroeconomic fundamentals improving slowly.

Credibility of RBI has increased.

27

Most banks are well capitalized, the insurance and security markets are well supervised.

India’s Financial System: Key Takeaways

The PSBs dominate banking sector, are inefficient, NPAs are large, governance is poor. Sovereign-bank nexus is large.

Financial sector increasingly reaching the underserved, helped by technological innovations.

Financial markets are deepening. Pension sector is underdeveloped.

Corporate sector is highly leveraged, high debt-at-risk, impacting banks’ and non-banks’ balance sheets.

Interconnections amongst banks and between banks and non-banks are high. Non-bank sector, though small is rising rapidly, creating vulnerabilities for the financial system.

Recent Reforms: What Has Been Done?

28

29

Recent Reforms: What Has Been Done?

2010Creation of

Financial Stability and Development Committee lead to better interagency

cooperation.

2015Introduction of

Inflation Targeting Framework in the RBI.

2015Started Asset Quality

Review of 36 commercial banks (including all PSBs) covering 93% of all

loans.

2016Insolvency and

Bankruptcy Code introduced to deal with insolvency of companies

and individuals.

2016-18Recognition of NPAs: NPAs increased from 9.6% to 11.6% in one year as restructured loans were moved to

NPA category.

2017The new Prompt Corrective Action framework became effective in April 2017. By

December 2017, RBI instructed 11 PSBs (out of 21), representing 40% of NPAs, to put several large

corporate accounts to time-bound resolution process’s.

Amendment of IBC in June 2018 prioritizes a speedy sale of assets

under liquidation.

2017-18Recapitalization plan for PSBs (1.3

percent of GDP): announced in October 2017, first tranche of

recapitalizations Feb.-March 2018.

2018Introduction of Banking Reforms

Roadmap. Indradhanush Plan and Banking Board Bureau (BBB)

to improve governance and operations in PSBs—quality of

Board members, infuse new talent from private sector, etc.

Recapitalization to be contingent on strengthening governance.

Strengthening the Financial System:

What Next?

30

Amend RBI Act to provide full regulatory and supervisory powers over the PSBs.

In addition to IBC, enhance out of court restructuring of corporates, speedy/time limits, with penalties for non-cooperative creditors. Remove impediments to voluntary settlement processes and develop distressed debt markets.

31

Recapitalization of PSBs should attract fresh capital. Provision of fresh capital based on meaningful restructuring of PSBs. Exit of weak banks. Outright privatization?

Strengthening the Financial System: What Next?

In additional to stock problem (NPAs), address flow problem by enhancing risk-management of banks and financial strength of corporates.

BBB should be further empowered to appoint and remove senior management of PSBs.

Monitor risks migrating to non-bank sector. Improve prudential framework for balance sheet risk management of NBFCs. Enforce stricter standards of corporate governance.

Introduce Special Resolution Regime for financial institutions, per international standards.

Review Statutory Liquidity Ratio (SLR) and Priority Sector Lending (PSL).

Reform ELA (emergency liquidity assistance from the RBI) to clarify eligibility, collateral standards, penalty rates. Government to give guarantee if solvency in doubt.

Strengthen FSDC—systemic risk monitoring, crisis preparedness and response.

Thank You!

32