c2 course test 4

TRANSCRIPT

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 1/16

CMC2CT10(N) – CT4 Questions

CC210 – C2 CT (4)

CIMA

CERTIFICATE IN BUSINESS ACCOUNTING

PAPER C2

FUNDAMENTALS OF FINANCIAL ACCOUNTING

COURSE TEST 4

QUESTION PAPER

Answer all questions

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 2/16

2 CMC2CT10(N) – CT4 Questions

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 3/16

CMC2CT10(N) – CT4 Questions 3

You must attempt all questions.Each correct answer will score two marks. No deduction will be made for wrong answers.

An answer sheet is provided on the last page of this test. You must indicate your answer in the box provided.

No workings should be submitted on the answer sheet

1 P Limited’s balance sheet as at 31 October 2008 included:$

50c ordinary share capital 300,000 $1 6% preference share capital 100,000 Share premium 60,000 Retained profit 105,300

565,300

No new shares have been issued during the year. On 1 April 2008 the company paid an interim dividend

of 2c per share on the ordinary shares and half of the annual preference dividend. A final dividend of 3cper share on the ordinary shares and the remainder of the preference dividend had been proposed as at31 October 2008.

The total dividend for the year ended 31 October 2008 should be $

2 Shearer & Co sell three products – Basic, Super and Luxury. The inventory records at the year end showthe following:

Basic$ per unit

Super$ per unit

Luxury$ per unit

Original cost 6 9 18Estimated selling price 9 12 15

Selling and distribution costs 1 4 5

Units Units UnitsUnits in inventory 200 250 150

The value of inventory at the year end should be $

3 The double entry to record a discount granted by a supplier is

A Debit payables, credit discounts allowed

B Debit payables, credit discounts receivedC Debit discounts received, credit payables

D Debit payables, credit purchases

4 A company's bank statement shows an overdraft of $3,204 at 31 March 2008. The statement includesbank charges of $46 which have not yet been recorded in the company's cash book. The statement doesnot include cheques for $780 paid to suppliers, nor an amount of $370 received from a receivable; both ofthese amounts appear in the bank statement for April 2008.

If the company prepares a balance sheet at 31 March 2008, the figure for the bank overdraft should be

$

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 4/16

4 CMC2CT10(N) – CT4 Questions

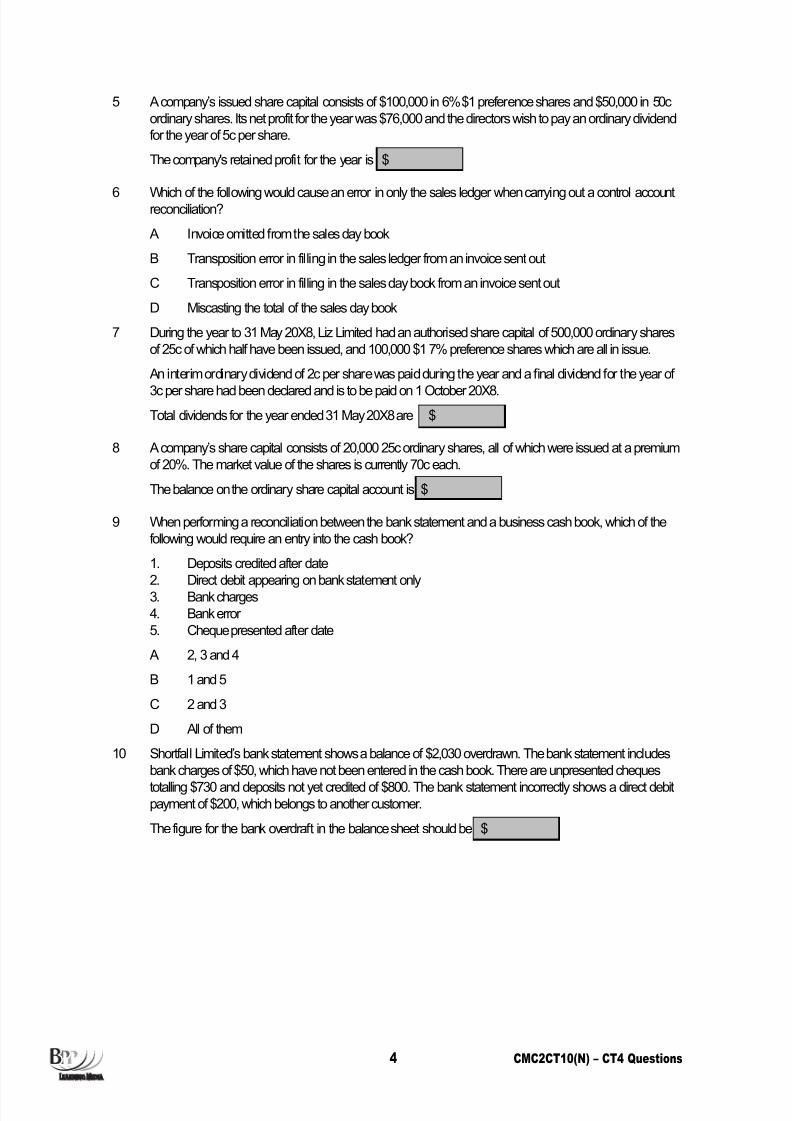

5 A company’s issued share capital consists of $100,000 in 6% $1 preference shares and $50,000 in 50cordinary shares. Its net profit for the year was $76,000 and the directors wish to pay an ordinary dividendfor the year of 5c per share.

The company's retained profit for the year is $

6 Which of the following would cause an error in only the sales ledger when carrying out a control accountreconciliation?

A Invoice omitted from the sales day book

B Transposition error in filling in the sales ledger from an invoice sent out

C Transposition error in filling in the sales day book from an invoice sent out

D Miscasting the total of the sales day book

7 During the year to 31 May 20X8, Liz Limited had an authorised share capital of 500,000 ordinary sharesof 25c of which half have been issued, and 100,000 $1 7% preference shares which are all in issue.

An interim ordinary dividend of 2c per share was paid during the year and a final dividend for the year of

3c per share had been declared and is to be paid on 1 October 20X8.Total dividends for the year ended 31 May 20X8 are $

8 A company’s share capital consists of 20,000 25c ordinary shares, all of which were issued at a premiumof 20%. The market value of the shares is currently 70c each.

The balance on the ordinary share capital account is $

9 When performing a reconciliation between the bank statement and a business cash book, which of thefollowing would require an entry into the cash book?

1. Deposits credited after date2. Direct debit appearing on bank statement only3. Bank charges4. Bank error5. Cheque presented after date

A 2, 3 and 4

B 1 and 5

C 2 and 3

D All of them

10 Shortfall Limited’s bank statement shows a balance of $2,030 overdrawn. The bank statement includesbank charges of $50, which have not been entered in the cash book. There are unpresented cheques

totalling $730 and deposits not yet credited of $800. The bank statement incorrectly shows a direct debitpayment of $200, which belongs to another customer.

The figure for the bank overdraft in the balance sheet should be $

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 5/16

CMC2CT10(N) – CT4 Questions 5

11 A sales ledger reconciliation was prepared by the bookkeeper of Corduroy and Co as at 31 March 2007but one heading was illegible.

Sales Ledger Control Account

$ $

31.3.07 Balance b/f 25,320 Sales day book overcast 1,000

Amended balance c/f 24,320

25,320 25,320

$Total per sales ledger listing 23,890Credit listed as debit (280)Other difference 710

24,320

Assuming the reconciliation has been prepared correctly, the “other difference” is most likely to be:

A Contra settlement omitted from the memorandum ledgers.

B Invoice omitted from the sales day book.

C Balance omitted from the sales ledger listing.

D Debit side overcast when individual customer account balanced off.

12 At 1 April 20X8 the share capital and share premium account of a company were as follows:

$

Share capital – 300,000 ordinaryshares of 25c each 75,000

Share premium account 200,000

During the year ended 31 March 20X9 the following events took place:1. On 1 October 20X8 the company made a rights issue of one share for every five held, at $1.20

per share.

2. On 1 January 20X9 the company made a bonus issue of one share for every three in issue at thattime using the share premium account to do so.

The correct balance on the share capital account is $

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 6/16

6 CMC2CT10(N) – CT4 Questions

FUNDAMENTALS OF FINANCIAL ACCOUNTING – COURSE

TEST 4

Answer SheetName: .......................................................................... Date:..........................................................................

Student number: ....................................................

1

2

3

4

5

6

7

8

9

10

11

12

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 7/16

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 8/16

BPP House, Aldine Place, London W12 8AA

Tel: 0845 0751 100 (for orders within the UK)

Tel: +44 (0)20 8740 2211

Fax: +44 (0)20 8740 1184

www.bpp.com/learningmedia

®

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 9/16

CMC2CT10(N) – CT4 Solutions

CC210 – C2 CT (4)

CIMA

CERTIFICATE IN BUSINESS ACCOUNTING

PAPER C2

FUNDAMENTALS OF FINANCIAL ACCOUNTING

COURSE TEST 4

SOLUTIONS

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 10/16

2 CMC2CT10(N) – CT4 Solutions

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 11/16

CMC2CT10(N) – CT4 Solutions 3

SOLUTIONS TO COURSE TEST 4

1 $36,000

2 $4,700

3 B

4 $3,614

5 $65,000

6 B

7 $19,500

8 $5,000

9 C

10 $1,760

11 C

12 $120,000

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 12/16

4 CMC2CT10(N) – CT4 Solutions

WORKINGS

1 $36,000$

Ordinary (5c x 600,000) 30,000

Preference (6% x 100,000) 6,00036,000

2 $4,700Cost Net realisable

valueLower of cost &

NRVUnits Value

$ $ $ $ $Basic 6 8 6 200 1,200Super 9 8 8 250 2,000Luxury 18 10 10 150 1,500

4,700

3 B

4 $3,614$

Bank balance per bank statement (3,204) ODUnpresented cheques (780)Outstanding lodgements 370∴ per balance sheet (3,614)

5 $65,000

$76,000- ($100,000× 6%) - ($50,000/$0.50× 5c)

6 B The sales ledger is updated from the original invoice. Errors in the sales day book will thereforenot affect the sales ledger. A, C and D are all errors in the sales day book.

7 Ordinary: 250,000 x 5c = 12,500Preference: 100,000 x 7% = 7,000

19,500

8 20,000 x 25c = $5,000

9 C

10 $1,760Balance per bank statement (2,030)Less unpresented cheques (730) Add outstanding lodgements 800 Add bank error 200

(1,760)

11 C A: A contra settlement would reduce the total on the sales ledger.

B: An invoice omitted from the sales daybook would not affect the sales ledger.

D: If the debt side of the customer's account was overcast, his balance would be too high andwould need to be reduced.

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 13/16

CMC2CT10(N) – CT4 Solutions 5

12 $Opening balance = 75,000

Rights issue$0.25

$75,000 x 1/5 x $0.25 = 15,000

Bonus issue ($0.25

$90,000 ) x 1/3 x $0.25 = 30,000

120,000

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 14/16

6 CMC2CT10(N) – CT4 Solutions

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 15/16

8/16/2019 C2 Course Test 4

http://slidepdf.com/reader/full/c2-course-test-4 16/16

BPP House, Aldine Place, London W12 8AA

Tel: 0845 0751 100 (for orders within the UK)

Tel: +44 (0)20 8740 2211

Fax: +44 (0)20 8740 1184

www.bpp.com/learningmedia

®