c o r p o r a t e p r o f i l e - century peak metals€¦ · century peak metals holdings...

TRANSCRIPT

Century Peak Metals Holdings Corporation (“CPMHC”, the “Company”, the “Parent Company”, or the “Issuer”), formerly Fil-Hispano Corporation, was registered with the Philippine Securities and Exchange Commission (“SEC”) on December 30, 2003. On February 15, 2008, the SEC approved the change in the Company’s corporate name to Century Peak Metals Holdings Corporation.

On April 14, 2008, the SEC approved the amendment of the Company’s articles of incorporation. Its primary purpose was changed to include promoting, operating, managing, holding, acquiring or investing in corporations or entities that are engaged in mining activities or mining-related activities. The Company further expanded its primary purpose by including investing in real estate development and energy. Its amended articles of incorporation was approved by the SEC on March 18, 2010.

The Company listed its common shares of stock with the Philippine Stock Exchange (“PSE”) on October 6, 2009.

The registered office address of the Parent Company is at Units 1403 and 1404 Equitable Bank Tower Condominium, 8751 Paseo de Roxas, Makati City.

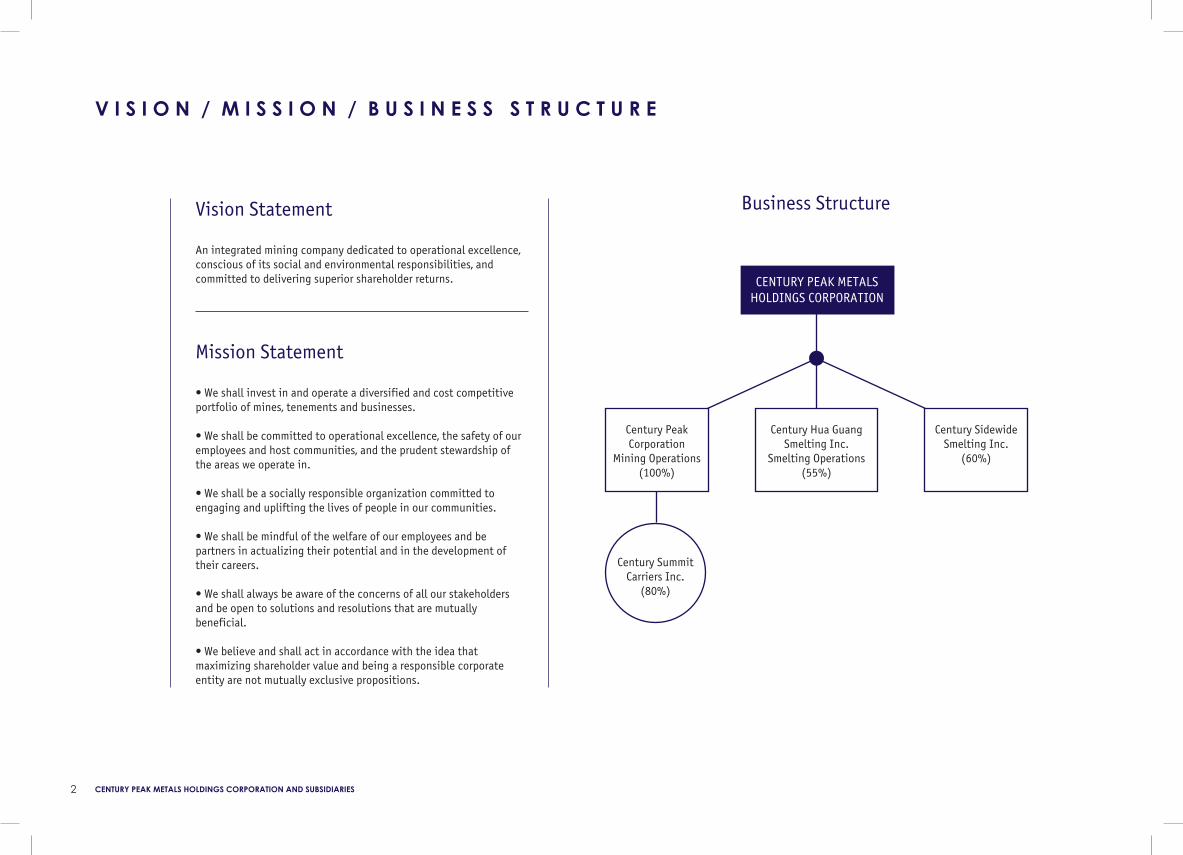

The Company has four subsidiaries, the wholly-owned subsidiary Century Peak Corporation (“CPC”), 55%-owned subsidiary Century Hua Guang Smelting Incorporated (“CHGSI”), 60%-owned subsidiary Century Sidewide Smelting Incorporated (“CSSI”) and 80%-owned subsidiary, through CPC, Century Summit Carrier, Inc. (“CSCI”).

C O R P O R A T E P R O F I L E

1ANNUAL REPORT 2011

The splendid shores of Dinagat Island

V I S I O N / M I S S I O N / B U S I N E S S S T R U C T U R E

Business Structure

2 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

Vision Statement

An integrated mining company dedicated to operational excellence, conscious of its social and environmental responsibilities, and committed to delivering superior shareholder returns.

Mission Statement

• We shall invest in and operate a diversified and cost competitive portfolio of mines, tenements and businesses.

• We shall be committed to operational excellence, the safety of our employees and host communities, and the prudent stewardship of the areas we operate in.

• We shall be a socially responsible organization committed to engaging and uplifting the lives of people in our communities.

• We shall be mindful of the welfare of our employees and be partners in actualizing their potential and in the development of their careers.

• We shall always be aware of the concerns of all our stakeholders and be open to solutions and resolutions that are mutually beneficial.

• We believe and shall act in accordance with the idea that maximizing shareholder value and being a responsible corporate entity are not mutually exclusive propositions.

CENTURY PEAK METALSHOLDINGS CORPORATION

Century Hua GuangSmelting Inc.

Smelting Operations(55%)

Century SidewideSmelting Inc.

(60%)

Century Peak Corporation

Mining Operations(100%)

Century SummitCarriers Inc.

(80%)

Dear Shareholders and Friends,

The year 2011 saw much volatility in commodity prices specifically base metals such as nickel, chromite, copper and others. Veering on the side of prudence, your management decided to continue its mining production, stock piling nickel ore without committing sales. It was therefore a deliberate strategy to stock pile our nickel ore until such time that prices would stabilize and increase in value.

In the second half of 2011, in line with the expansion plans for the Dinagat mining operations your company purchased capital extensive mining equipment composed of excavators, bull dozers, and a fleet of dump trucks. The mine site development for the Casiguran Nickel Mining Project was in full swing during this period with the construction of infrastructures such as road networks, office buildings, housing units, causeway/pier and stockyards.

In order to augment the capacity of operations to meet shipping requirements, your company acquired two (2) units of self-propelled Landing Craft Transport/Tank (LCT), each with a rated Gross Tonnage of 2,099. Owing to the fact that, the weather condition limits the mining operation only from March to October, we thought of providing chartering services to other customers as well. In view of this, we established Century Summit Carriers Inc. (CSCI) which is 80% owned by Century Peak Corporation. CPC or its contractors will enter into chartering agreement for the use of the LCTs.

Simultaneous to the activities at Dinagat Island, is the site preparation for the Ferro-Nickel Smelting Plant located at the Leyte Industrial Development Estate (LIDE) in Leyte. Several plant equipment and machineries were

already delivered at the site, the bulk of which is yet to be delivered. Meantime, we focused all our resources to expedite the production of the mining operations in Dinagat Island.

Conscientious of the environmental impact of mining, the company constructed a nursery at a nearby location in the mine site. Your company, in line with the Environmental Management Plan, shall endeavour to plant trees and vegetation endemic to the disturbed area to ensure growth. Mitigating measures outlined in the Environmental Protection and Enhancement Program (EPEP) shall be implemented and closely monitored and reviewed to ensure compliance.

In all the activities stated above, the community always play a major role. Locals are given priority in employment and under the Social Development and Management Program assures the community assistance in terms of funding, education and training in order to alleviate the social and economic conditions of the people residing in the vicinity of the mining operation.

Looking forward, your company plans to commence mining operations in 2012 on two locations at the Dinagat Island. The Casiguran Nickel Mining Project mentioned earlier is one and the second project is the Esperanza Nickel Mining Project which is at Sitio Bel-at, Barangay Esperanza in Loreto. The company will be contracting third party operators to conduct the actual mine production.

Very truly yours,

Wilfredo D. Keng

C H A I R M A N ‘ S M E S S A G E

3ANNUAL REPORT 2011

4 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

development was the laying out of the drainage system, canals and settling ponds/dams. Stockyards to be utilized as temporary storage area for mined ore material prior to shipment were constructed. A causeway/pier designed to accommodate Landing Craft Tank (LCT) was constructed near the Marayag camp site.

Exploration continued at the northern portion of the property. During the year a total of 3048 samples were recovered out the 895 number of auger drillholes, totalling 2980.7 meters and samples’ assay result showed an average grade of 0.67%Ni, 35.64 %Fe, and 2.08%Cr. The said activity was actually designed to test the continuity and lateral extent of Ni laterite with Fe-Cr deposits.

Other Mineral PropertiesIn addition to the Casiguran Nickel Project, CPC’s mineral rights in Libjo (Albor) in Dinagat Islands covered by MPSA 283-2009-XIII which was approved on June 19, 2009 proved to be very promising. The resource base of the project as based on the report by Dr. Carlo A. Arcilla done particularly in Parcel 2 on April 2010 estimated that the low nickel high iron laterite Limonite volume to be at 3.579 million MT at 0.995% Nickel and 48.109% Iron. At 1.0% Nickel cut-off additional 2.339 million MT limonite ore grading 1.209% Nickel and 39.665% Iron and 1.225 million MT saprolite ore grading 1.308% Nickel and 13.806% Iron. A Declaration of the Mining Project Feasibility (DMPF) report, together with the Environmental Protection and Enhancement Program (EPEP) and Final Mine Rehabilitation and Decommissioning Plan (FMRDP) was prepared during the second semester of 2011 for review and evaluation by January 2012.

R E V I E W O F O P E R A T I O N S

Century Peak Corporation (“CPC”), a 100% owned subsidiary of Century Peak Metals Holdings Corporation, was formed on March 30, 2006 for the purpose of investing in and engaging in the business of development, operation and mining of any mineral resources in the Philippines. CPC was granted exclusive rights to mine in a number of locations in Southern Philippines, particularly in the Dinagat Islands.

The Casiguran Nickel ProjectThe Casiguran Nickel Mining Project covered by a Mineral Production Agreement (MPSA) denominated as MPSA 010-092-X covering an area of about 1,198 hectares is located at Brgy Panamaon in Loreto in the province of Dinagat Island (the “Casiguran Property”).

Based on the report prepared by Dr. Carlo Arcilla entitled “Geologic Resource Evaluation of the Century Peak Corporation Casiguran Mine Prospect” released on April 2010, the project has a combined indicated and measured resource of about 9,897,000 with a grade of 1.02% Nickel (at 0.8% nickel cut-off), subject to mining plans and metal recovery parameters. These could represent about 100,000 metric tons of pure nickel and 3.5 million tons of iron. Dr. Arcilla is an accredited Competent Person in accordance with the definition of the Philippine Mineral Reporting Code (PMRC).

Construction and development of the mine site was the focus of all activities during the year 2011. A network of access/haul roads were developed, interconnecting the major facilities, such are: pit area, stockyards, causeway/pier, and the camp site. Concurrent to the road

Century Peak Corporation

a

b

c

(a) A fleet of 30-tonner dump trucks waiting to be dispatched

(b) An excavator preparing the area for mining

(c) A shipload of lateritic nickel ore

5ANNUAL REPORT 2011

The CRAU property, denominated as APSA 086-XIII whose Operating Agreement was assigned to CPC through a Memorandum of Agreement (MOA) with Maharlika Dragon Mining Corp (“MDMC”). Under the MOA, MDMC assigned all its rights, interest and title as an operator of the CRAU Property under the Operating Agreement dated May 5, 2007. The CRAU Property chromite-nickel prospect is located in Acoje in Loreto in Dinagat Island adjacent to CPC’s Casiguran Nickel Project. The Application for Mineral Production Sharing Agreement (APSA) is still under final evaluation by the MGB Central Office.(The CRAU property had been actively mined for sandy and lumpy chromite ore found in lenses in dark/black dunite) However, its prospect as a nickel mine in addition to Chromite has only been recently highlighted under the Geologic Resource Evaluation of CPC’s Casiguran Property dated April 2010 conducted by Dr. Arcilla.

The Company’s Ferro-Nickel smelting plant project through its subsidiary Century Hua Guang Smelting Inc. (CHGSI), has started plant site preparation in the area located inside the Leyte Industrial Development Estate (LIDE). Access road and drainage system were laid out. Installation of the 6” diameter water pipeline from the LIDE Management Corporation’s 4-million gallon tank to the plant site was completed and passed hydro testing procedure. Initial shipment of the plant equipment & medicineries arrived from China on July 2011 and amongst those are parts of the Blast Furnaces including accessories.

Century Hua Guang Smelting Inc.

Environmental ManagementThe year in review, CPC in its desire to adhere to sustainable development through responsible mining, has developed a drainage system that would mitigate soil erosion even before the mining operation starts. Canals were constructed along roadways with settling ponds at strategic locations to trap silt. Downstream, series of settling ponds are constructed to allow the silt to settle and prevent it from flowing into the natural waterways. The canals and settling ponds are maintained periodically to be effective at all times. Moreover, the roadways are crowned so that surface water runoffs flow towards the canals.

In line with Company’s commitment to support the three-year National Greening Program (NGP) of the government pursuant to Executive Order no. 26 issued on February 24, 2011, was enjoined to implement the NGP to help regain the country’s depleting forest cover and ensure sufficient supply for the future. Under this program, mining companies are required to either plant the trees or donate seedlings to People Organizations (PO) of choice for the PO to plant the seedlings outside of the mining area. CPC chose to construct its own nursery and gathered seedlings of trees endemic to the locality, such are: 2,600 seedlings of magkono, 400 seedlings of pine tree, and 180 seedlings of madre de cacao. A total of 500 seedlings of which 120 seedlings of magkono, 200 seedlings of pine tree, and 180 seedlings of madre de cacao were planted during the year

a

b

(a) Nursery of plants endemic to the island of Dinagat

(b) Forest tree planting project for the National Greening Program

6 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

C O R P O R A T E S O C I A L R E S P O N S I B I L I T Y

Social DevelopmentIn 2011, CPC embarked on several socio economic activities that cater to the upliftment of the current social and economic conditions of the people in the community. Aside from providing direct employment to 101 people residents of the area, the Company extends financial support to the different projects of the Barangay, the school, and the various religious congregations. Barangay projects are funded through the Social Development and Management Program (SDMP) which is updated yearly to conform to the immediate needs of the community. The Community Technical Working Group (CTWG) determines the programs/projects and activities to be included in the SDMP which are most beneficial to the people. SDMP also allocates fund to help maintain the local school facilities and in 2011 a flag pole was constructed. The Roman Catholic church in Brgy. Pamanaon was also a recipient when CPC shouldered the cost of material in the construction of the church’s sanitary facilities.

c

d

(c) CPC personnel socializing with the residents of Brgy. Panamaon

(d) In support of the local parish

7ANNUAL REPORT 2011

The management of Century Peak Metals Holdings Corporation and Subsidiaries is responsible for all information and representations contained in the consolidated financial statements for the periods ended December 31, 2011 and 2010. The consolidated financial statements have been prepared in conformity with Philippine Financial Reporting Standards and reflect amounts that are based on the best estimates and informed judgment of management with appropriate consideration to materiality.

In this regard, management maintains a system of accounting and reporting which provides for the necessary internal controls to ensure that transactions are properly authorized and recorded, assets are safeguarded against unauthorized use or disposition, and liabilities are recognized.

The Board of Directors reviews the consolidated financial statements before such statements are approved and submitted to the stockholders of the Company.

Manabat San Agustin & Co., CPAs, the independent auditor appointed by the stockholders, have audited the financial statements of the Company in accordance with Philippine Standards on Auditing and have expressed their opinion on the fairness of presentation upon completion of such audit, in the report to the stockholders.

Mr. Wilfredo D. Keng

President and Chief Executive Officer

Mr. Enrico M. Trinidad

Chief Finance Officer

S T A T E M E N T O F M A N A G E M E N T R E S P O N S I B I L I T Y

8 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

R E P O R T O F I N D E P E N D E N T A U D I T O R S

9ANNUAL REPORT 2011

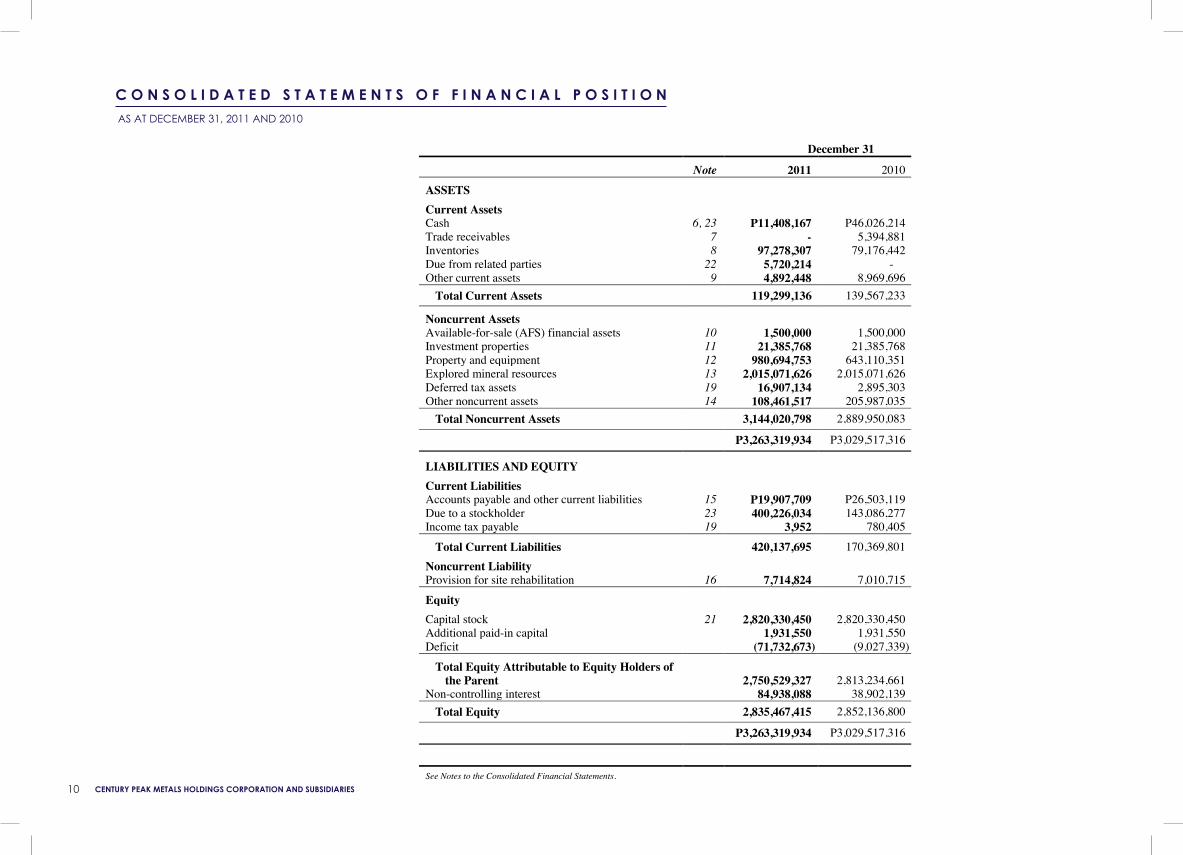

C O N S O L I D A T E D S T A T E M E N T S O F F I N A N C I A L P O S I T I O NAS AT DECEMBER 31, 2011 AND 2010

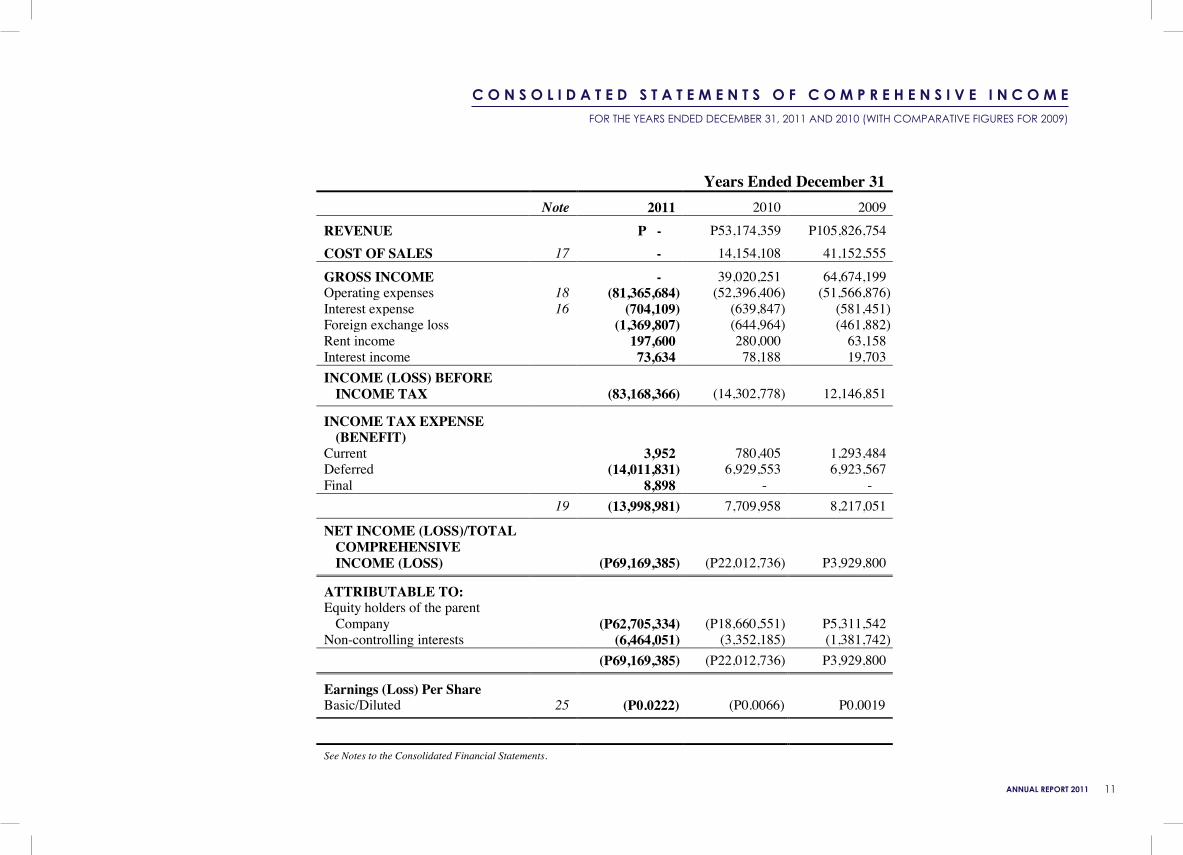

C O N S O L I D A T E D S T A T E M E N T S O F C O M P R E H E N S I V E I N C O M EFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

December 31

Note 2011 2010

ASSETSCurrent AssetsCash 6, 23 P11,408,167 P46,026,214Trade receivables 7 - 5,394,881Inventories 8 97,278,307 79,176,442Due from related parties 22 5,720,214 -Other current assets 9 4,892,448 8,969,696

Total Current Assets 119,299,136 139,567,233

Noncurrent AssetsAvailable-for-sale (AFS) financial assets 10 1,500,000 1,500,000Investment properties 11 21,385,768 21,385,768Property and equipment 12 980,694,753 643,110,351Explored mineral resources 13 2,015,071,626 2,015,071,626Deferred tax assets 19 16,907,134 2,895,303Other noncurrent assets 14 108,461,517 205,987,035

Total Noncurrent Assets 3,144,020,798 2,889,950,083

P3,263,319,934 P3,029,517,316

LIABILITIES AND EQUITYCurrent LiabilitiesAccounts payable and other current liabilities 15 P19,907,709 P26,503,119Due to a stockholder 23 400,226,034 143,086,277Income tax payable 19 3,952 780,405

Total Current Liabilities 420,137,695 170,369,801Noncurrent LiabilityProvision for site rehabilitation 16 7,714,824 7,010,715

EquityCapital stock 21 2,820,330,450 2,820,330,450Additional paid-in capital 1,931,550 1,931,550Deficit (71,732,673) (9,027,339)

Total Equity Attributable to Equity Holders of the Parent 2,750,529,327 2,813,234,661

Non-controlling interest 84,938,088 38,902,139Total Equity 2,835,467,415 2,852,136,800

P3,263,319,934 P3,029,517,316

See Notes to the Consolidated Financial Statements.

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

December 31

Note 2011 2010

ASSETSCurrent AssetsCash 6, 23 P11,408,167 P46,026,214Trade receivables 7 - 5,394,881Inventories 8 97,278,307 79,176,442Due from related parties 22 5,720,214 -Other current assets 9 4,892,448 8,969,696

Total Current Assets 119,299,136 139,567,233

Noncurrent AssetsAvailable-for-sale (AFS) financial assets 10 1,500,000 1,500,000Investment properties 11 21,385,768 21,385,768Property and equipment 12 980,694,753 643,110,351Explored mineral resources 13 2,015,071,626 2,015,071,626Deferred tax assets 19 16,907,134 2,895,303Other noncurrent assets 14 108,461,517 205,987,035

Total Noncurrent Assets 3,144,020,798 2,889,950,083

P3,263,319,934 P3,029,517,316

LIABILITIES AND EQUITYCurrent LiabilitiesAccounts payable and other current liabilities 15 P19,907,709 P26,503,119Due to a stockholder 23 400,226,034 143,086,277Income tax payable 19 3,952 780,405

Total Current Liabilities 420,137,695 170,369,801Noncurrent LiabilityProvision for site rehabilitation 16 7,714,824 7,010,715

EquityCapital stock 21 2,820,330,450 2,820,330,450Additional paid-in capital 1,931,550 1,931,550Deficit (71,732,673) (9,027,339)

Total Equity Attributable to Equity Holders of the Parent 2,750,529,327 2,813,234,661

Non-controlling interest 84,938,088 38,902,139Total Equity 2,835,467,415 2,852,136,800

P3,263,319,934 P3,029,517,316

See Notes to the Consolidated Financial Statements.10 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

C O N S O L I D A T E D S T A T E M E N T S O F F I N A N C I A L P O S I T I O NAS AT DECEMBER 31, 2011 AND 2010

C O N S O L I D A T E D S T A T E M E N T S O F C O M P R E H E N S I V E I N C O M EFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

Years Ended December 31Note 2011 2010 2009

REVENUE P - P53,174,359 P105,826,754COST OF SALES 17 - 14,154,108 41,152,555

GROSS INCOME - 39,020,251 64,674,199Operating expenses 18 (81,365,684) (52,396,406) (51,566,876)Interest expense 16 (704,109) (639,847) (581,451)Foreign exchange loss (1,369,807) (644,964) (461,882)Rent income 197,600 280,000 63,158Interest income 73,634 78,188 19,703INCOME (LOSS) BEFORE

INCOME TAX (83,168,366) (14,302,778) 12,146,851

INCOME TAX EXPENSE (BENEFIT)

Current 3,952 780,405 1,293,484Deferred (14,011,831) 6,929,553 6,923,567Final 8,898 - -

19 (13,998,981) 7,709,958 8,217,051

NET INCOME (LOSS)/TOTAL COMPREHENSIVE INCOME (LOSS) (P69,169,385) (P22,012,736) P3,929,800

ATTRIBUTABLE TO:Equity holders of the parent

Company (P62,705,334) (P18,660,551) P5,311,542Non-controlling interests (6,464,051) (3,352,185) (1,381,742)

(P69,169,385) (P22,012,736) P3,929,800

Earnings (Loss) Per ShareBasic/Diluted 25 (P0.0222) (P0.0066) P0.0019

See Notes to the Consolidated Financial Statements.

11ANNUAL REPORT 2011

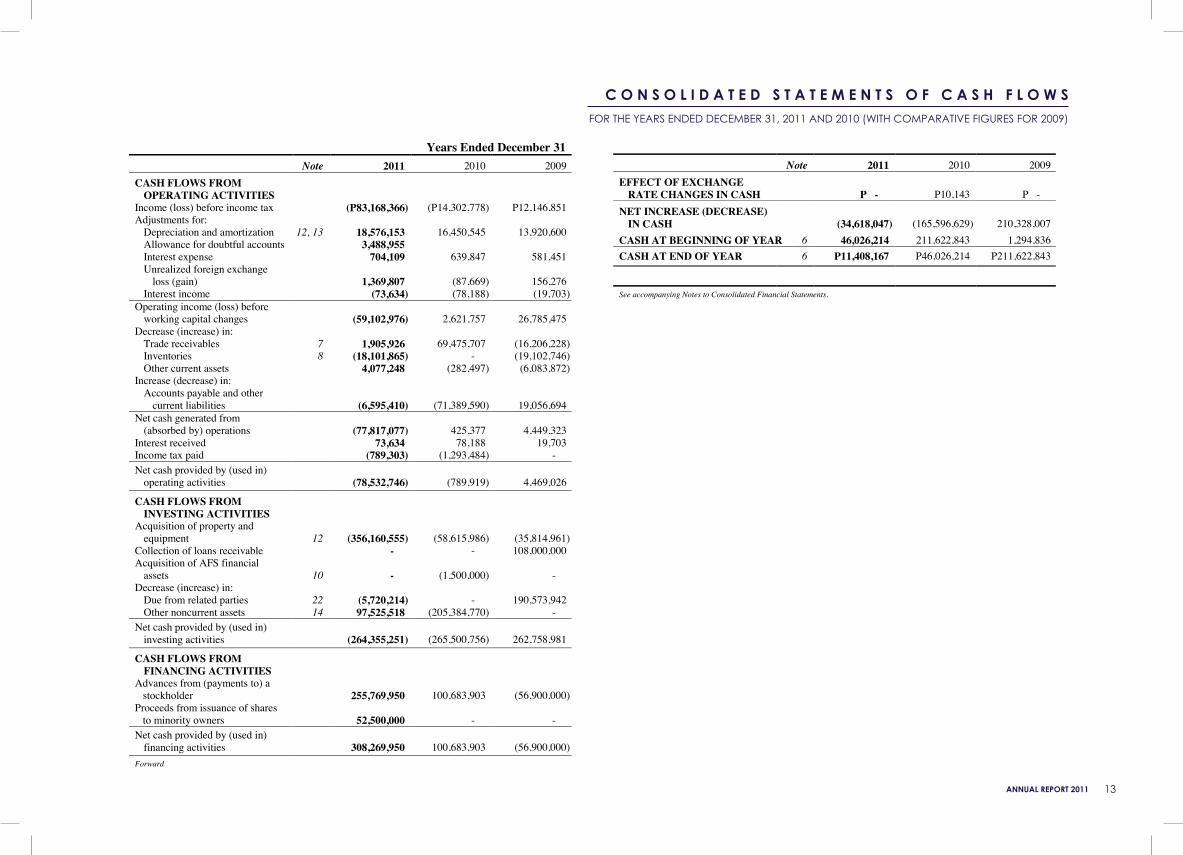

C O N S O L I D A T E D S T A T E M E N T S O F C A S H F L O W SFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

C O N S O L I D A T E D S T A T E M E N T S O F C H A N G E S I N E Q U I T YFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES(Formerly Fil-Hispano Corporation)

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITYFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010

Attributable to Equity Holders of the ParentAdditional

Capital Stock Paid-in Retained Minority(Note 21) Capital Earnings Total Interests Total Equity

Balance at January 1, 2011 P2,820,330,450 P1,931,550 (P9,027,339) P2,813,234,661 P38,902,139 P2,852,136,800Net loss/total comprehensive loss for the year - - (62,705,334) (62,705,334) (6,464,051) (69,169,385)

Transactions with owners, recorded directly in equity

Subscription on newly incorporated entities - - - - 52,500,000 52,500,000Balance at December 31, 2011 P2,820,330,450 P1,931,550 (P71,732,673) P2,750,529,327 P84,938,088 P2,835,467,415

Balance at January 1, 2010 P2,820,330,450 P1,931,550 P9,633,212 P2,831,895,212 P42,254,324 P2,874,149,536Net loss/total comprehensive loss for the year - - (18,660,551) (18,660,551) (3,352,185) (22,012,736)Balance at December 31, 2010 P2,820,330,450 P1,931,550 (P9,027,339) P2,813,234,661 P38,902,139 P2,852,136,800

Balance at January 1, 2009 P2,820,330,450 P1,931,550 P4,321,670 P2,826,583,670 P43,636,066 P2,870,219,736Net income (loss)/total comprehensive income

(loss) for the year - - 5,311,542 5,311,542 (1,381,742) 3,929,800Balance at December 31, 2009 P2,820,330,450 P1,931,550 P9,633,212 P2,831,895,212 P42,254,324 P2,874,149,536

See Notes to the Consolidated Financial Statements.

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended December 31Note 2011 2010 2009

CASH FLOWS FROM OPERATING ACTIVITIES

Income (loss) before income tax (P83,168,366) (P14,302,778) P12,146,851Adjustments for:

Depreciation and amortization 12, 13 18,576,153 16,450,545 13,920,600Allowance for doubtful accounts 3,488,955Interest expense 704,109 639,847 581,451Unrealized foreign exchange

loss (gain) 1,369,807 (87,669) 156,276Interest income (73,634) (78,188) (19,703)

Operating income (loss) before working capital changes (59,102,976) 2,621,757 26,785,475

Decrease (increase) in:Trade receivables 7 1,905,926 69,475,707 (16,206,228)Inventories 8 (18,101,865) - (19,102,746)Other current assets 4,077,248 (282,497) (6,083,872)

Increase (decrease) in:Accounts payable and other

current liabilities (6,595,410) (71,389,590) 19,056,694Net cash generated from

(absorbed by) operations (77,817,077) 425,377 4,449,323Interest received 73,634 78,188 19,703Income tax paid (789,303) (1,293,484) -Net cash provided by (used in)

operating activities (78,532,746) (789,919) 4,469,026

CASH FLOWS FROM INVESTING ACTIVITIES

Acquisition of property and equipment 12 (356,160,555) (58,615,986) (35,814,961)

Collection of loans receivable - - 108,000,000Acquisition of AFS financial

assets 10 - (1,500,000) -Decrease (increase) in:

Due from related parties 22 (5,720,214) - 190,573,942Other noncurrent assets 14 97,525,518 (205,384,770) -

Net cash provided by (used in) investing activities (264,355,251) (265,500,756) 262,758,981

CASH FLOWS FROM FINANCING ACTIVITIES

Advances from (payments to) a stockholder 255,769,950 100,683,903 (56,900,000)

Proceeds from issuance of sharesto minority owners 52,500,000 - -

Net cash provided by (used in) financing activities 308,269,950 100,683,903 (56,900,000)

Forward

12 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

C O N S O L I D A T E D S T A T E M E N T S O F C A S H F L O W SFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

C O N S O L I D A T E D S T A T E M E N T S O F C H A N G E S I N E Q U I T YFOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (WITH COMPARATIVE FIGURES FOR 2009)

CAN’T FIT PDF FILE HERE. WILL BE TOO SMALL IF RESIZED. NEEDS WORD FILE

CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended December 31Note 2011 2010 2009

CASH FLOWS FROM OPERATING ACTIVITIES

Income (loss) before income tax (P83,168,366) (P14,302,778) P12,146,851Adjustments for:

Depreciation and amortization 12, 13 18,576,153 16,450,545 13,920,600Allowance for doubtful accounts 3,488,955Interest expense 704,109 639,847 581,451Unrealized foreign exchange

loss (gain) 1,369,807 (87,669) 156,276Interest income (73,634) (78,188) (19,703)

Operating income (loss) before working capital changes (59,102,976) 2,621,757 26,785,475

Decrease (increase) in:Trade receivables 7 1,905,926 69,475,707 (16,206,228)Inventories 8 (18,101,865) - (19,102,746)Other current assets 4,077,248 (282,497) (6,083,872)

Increase (decrease) in:Accounts payable and other

current liabilities (6,595,410) (71,389,590) 19,056,694Net cash generated from

(absorbed by) operations (77,817,077) 425,377 4,449,323Interest received 73,634 78,188 19,703Income tax paid (789,303) (1,293,484) -Net cash provided by (used in)

operating activities (78,532,746) (789,919) 4,469,026

CASH FLOWS FROM INVESTING ACTIVITIES

Acquisition of property and equipment 12 (356,160,555) (58,615,986) (35,814,961)

Collection of loans receivable - - 108,000,000Acquisition of AFS financial

assets 10 - (1,500,000) -Decrease (increase) in:

Due from related parties 22 (5,720,214) - 190,573,942Other noncurrent assets 14 97,525,518 (205,384,770) -

Net cash provided by (used in) investing activities (264,355,251) (265,500,756) 262,758,981

CASH FLOWS FROM FINANCING ACTIVITIES

Advances from (payments to) a stockholder 255,769,950 100,683,903 (56,900,000)

Proceeds from issuance of sharesto minority owners 52,500,000 - -

Net cash provided by (used in) financing activities 308,269,950 100,683,903 (56,900,000)

Forward

Note 2011 2010 2009EFFECT OF EXCHANGE

RATE CHANGES IN CASH P - P10,143 P -NET INCREASE (DECREASE)

IN CASH (34,618,047) (165,596,629) 210,328,007CASH AT BEGINNING OF YEAR 6 46,026,214 211,622,843 1,294,836CASH AT END OF YEAR 6 P11,408,167 P46,026,214 P211,622,843

See accompanying Notes to Consolidated Financial Statements.

13ANNUAL REPORT 2011

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

CENTURY PEAK METALS HOLDINGS CORPORATIONAND SUBSIDIARIES

(Formerly Fil-Hispano Corporation)NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Corporate Information

Century Peak Metals Holdings Corporation (“CPMHC or the Parent Company”),formerly Fil-Hispano Corporation, was registered with the Philippine Securities and Exchange Commission (SEC) on December 30, 2003. On February 15, 2008, the SEC approved the change in the Parent Company’s corporate name to Century Peak Metals Holdings Corporation.

On April 14, 2008, the SEC approved the amendment of the Parent Company’s Articles of Incorporation changing its primary purpose to include promoting, operating, managing, holding, acquiring or investing in corporations or entities that are engaged in mining activities or mining-related activities. The Parent Company further expanded its primary purpose by including investing in real estate development and energy. The amended articles of incorporation were approved by the SEC on March 18, 2010.

The Parent Company listed its common shares of stock with the Philippine Stock Exchange on October 6, 2009.

On May 27, 2010, SEC approved the amendment of the Parent Company’s articles of incorporation changing the registered principal office to Units 1403 and 1404 Equitable Bank Tower Condominium, 8751 Paseo de Roxas, Makati City.

The consolidated financial statements include the separate financial statements of the Parent Company, its wholly-owned subsidiary, Century Peak Corporation (CPC), its 55%-owned subsidiary, Century Hua Guang Smelting Incorporated (CHGSI) and its 60%-owned subsidiary, Century Sidewide Smelting Incorporated (CSSI) (collectively referred to as the “Group”).

During the year, the Group has incorporated two entities, namely Century Sidewide Smelting, Inc. (“CSSI”) and Century Summit Carrier, Inc. (“CSCI”). CSCI is 80%-owned by Century Peak Corporation and is indirectly owned by the Parent Company.

The Parent Company has entered into a partnership with Sidewide Resources (H.K.) Limited, a subsidiary of Chaoyang Saiwai Mining Co., Ltd of P. R. China., a group that owns an iron powder processing plant, electric furnace smelting plant, and primarily does mineral ore trading. It is the Parent Company’s plan to set up electric furnaces in the future to enhance the production of its nickel pig iron at the LIDE. From this newly formed partnership, CSSI is incorporated.

CSSI is incorporated in the Philippines. Its SEC Registration Certificate was issued on September 6, 2011. The primary purpose of CSSI is to invest in the business of operating and mining mineral resources (mineral ores). It’s activities also involve prospecting, exploring, milling, smelting and preparing market of mineral ores.

- 2 -

CSCI, which is 80%-owned by CPC is registered in the SEC and its Certificate of Registration was issued on September 29, 2011. It is engaged in operating barges, steamships, motorboats and other kind of water crafts for the transportation of cargoes and passengers within the waters and territorial jurisdiction of the Philippines and in high seas. CSCI may also act as agent of domestic steam or other ships.

On December 8, 2011 CSCI was registered with the Maritime Industry Authority (“Marina”) with Certificate NO. DSO-2006-003-095 (2011) under Marina Circular 2006-003, which is valid until December 7, 2014.

Mineral Rights of CPCThe table below summarizes CPC’s mineral rights:

Tenement DesignationArea Covered

(hectares) LocationMPSA-010-92-X 1,198 Casiguran, Loreto, Dinagat IslandsMPSA-283-2009-XIII-SMR 3,188 Libjo (Albor), Dinagat IslandsEPA-IVB-139 5,136 Ihawig, Puerto Princesa, PalawanAPSA-086-XIII 660 Acoje, Loreto, Dinagat Islands

CPC acquired Mineral Production Sharing Agreement (MPSA) No. 010-92-X covering its Mineral Right in Loreto, Province of Dinagat Islands, otherwise known as the Casiguran Nickel Project, by virtue of a Deed of Assignment executed with Casiguran Mining Corporation on May 29, 2006, which was approved by the Department of Environment and Natural Resources (DENR) on December 11, 2006.

In addition to the MPSA over the Casiguran Nickel Project, CPC’s mineral right in Libjo (Albor), Dinagat Islands is covered by MPSA-283-2009-XIII-SMR, which was approved on June 19, 2009.

Furthermore, CPC also has an existing Exploration Permit Application (EPA) designated as EPA-IVB-139 covering its property in Ihawig, Puerto Princesa, Palawan. Moreover, CPC entered into a Memorandum of Agreement (“MOA”) with Maharlika Dragon Mining Corp (“MDMC”) assigning to CPC the Operating Agreement executed by and among MDMC, as the operator and Heirs of C.B. Gupana (owners of 52.5%) and CRAU Mineral Resources Corporation (with an interest of 47.5%) of the adjacent CRAU Property chromite-nickel prospect. Under the MOA, MDMC assigned all its rights, interest and title as an operator of the CRAU Property under the Operating Agreement dated May 5, 2007 to CPC. The operating agreement which is covered by an Application for Mineral Production Sharing Agreement identified as APSA-086-XIII was registered with the MGB. The application is under evaluation by the MGB Central Office.

The CRAU Property is covered by APSA-086-XIII as well as by Environmental Compliance Certificate (ECC) No. 008-345-301C. The Application for Mineral Production Sharing Agreement (APSA) is still under final evaluation by the MGB Central Office.

CPC also entered into a Joint Operating Agreement with Philippine Mining DevelopmentCorporation (PMDC) subject of its winning bid as operating partner to undertake the exploration, development and mining operations of PMDC’s Pinamungahan Limestone Property, covering an area of 4,795 hectares located in Toledo and Pinamungahan, Cebu.

14 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

- 2 -

CSCI, which is 80%-owned by CPC is registered in the SEC and its Certificate of Registration was issued on September 29, 2011. It is engaged in operating barges, steamships, motorboats and other kind of water crafts for the transportation of cargoes and passengers within the waters and territorial jurisdiction of the Philippines and in high seas. CSCI may also act as agent of domestic steam or other ships.

On December 8, 2011 CSCI was registered with the Maritime Industry Authority (“Marina”) with Certificate NO. DSO-2006-003-095 (2011) under Marina Circular 2006-003, which is valid until December 7, 2014.

Mineral Rights of CPCThe table below summarizes CPC’s mineral rights:

Tenement DesignationArea Covered

(hectares) LocationMPSA-010-92-X 1,198 Casiguran, Loreto, Dinagat IslandsMPSA-283-2009-XIII-SMR 3,188 Libjo (Albor), Dinagat IslandsEPA-IVB-139 5,136 Ihawig, Puerto Princesa, PalawanAPSA-086-XIII 660 Acoje, Loreto, Dinagat Islands

CPC acquired Mineral Production Sharing Agreement (MPSA) No. 010-92-X covering its Mineral Right in Loreto, Province of Dinagat Islands, otherwise known as the Casiguran Nickel Project, by virtue of a Deed of Assignment executed with Casiguran Mining Corporation on May 29, 2006, which was approved by the Department of Environment and Natural Resources (DENR) on December 11, 2006.

In addition to the MPSA over the Casiguran Nickel Project, CPC’s mineral right in Libjo (Albor), Dinagat Islands is covered by MPSA-283-2009-XIII-SMR, which was approved on June 19, 2009.

Furthermore, CPC also has an existing Exploration Permit Application (EPA) designated as EPA-IVB-139 covering its property in Ihawig, Puerto Princesa, Palawan. Moreover, CPC entered into a Memorandum of Agreement (“MOA”) with Maharlika Dragon Mining Corp (“MDMC”) assigning to CPC the Operating Agreement executed by and among MDMC, as the operator and Heirs of C.B. Gupana (owners of 52.5%) and CRAU Mineral Resources Corporation (with an interest of 47.5%) of the adjacent CRAU Property chromite-nickel prospect. Under the MOA, MDMC assigned all its rights, interest and title as an operator of the CRAU Property under the Operating Agreement dated May 5, 2007 to CPC. The operating agreement which is covered by an Application for Mineral Production Sharing Agreement identified as APSA-086-XIII was registered with the MGB. The application is under evaluation by the MGB Central Office.

The CRAU Property is covered by APSA-086-XIII as well as by Environmental Compliance Certificate (ECC) No. 008-345-301C. The Application for Mineral Production Sharing Agreement (APSA) is still under final evaluation by the MGB Central Office.

CPC also entered into a Joint Operating Agreement with Philippine Mining DevelopmentCorporation (PMDC) subject of its winning bid as operating partner to undertake the exploration, development and mining operations of PMDC’s Pinamungahan Limestone Property, covering an area of 4,795 hectares located in Toledo and Pinamungahan, Cebu.

- 3 -

Mining Operations of CPCCPC has continuing exploration work in its properties in the Province of Dinagat Islands and has recently signed Contractor’s Service Agreements with three (3) different independent contractors to conduct mining and nickel ore extraction in its Casiguran mine and its Rapid City Parcel II mine. CPC plans to market and export a minimum of 1,000,000 metric tons of nickel ore this 2012. At the same time, nickel ores will continue to be stockpiled in anticipation for the forthcoming operation of the smelter located at the Leyte Industrial Development Estate (LIDE).

Management believes that significantly more value will be added to the Groups’ raw ore, and therefore shareholder interests will be maximized, by smelting it and selling it asnickel pig iron.

Moreover, last April 2010, CPC released two Geologic Resource Evaluation Reports, an update to its Casiguran Mine Prospect, Dinagat Island covered by its MPSA 010-92-Xand a new Resource Evaluation Report for its Rapid City Parcel II Prospect covered by its MPSA 283-2009-XIII-SMR, both prepared by Dr. Carlo A. Arcilla, an Accredited Competent Person in accordance with the definition of the Philippine Mineral Reporting Code (PMRC).

Based on the reports, the Casiguran Mine Prospect has a combined indicated and measured resource of 9,897,000 DMT with a grade of 1.02% Nickel (at 0.8% nickel cut-off). In addition, new data from the Rapid City Parcel II Prospect reveal a combined indicated and measured resource of 9,067,000 DMT with a grade of 1.07% Nickel (at 0.8% Nickel cut-off). These could represent to 100,000 metric tons of pure nickel and 3.5 million tons of iron in its Casiguran property, and 90,000 tons of pure nickel and 3.8 million tons of iron in their Rapid City property, subject to mining plans and metal recovery parameters.

The management looks forward to continue developing and exploring these mineral properties either on its own or with joint venture partners. Moreover, management plans to increase CPC’s capitalization within the year 2012.

The Smelting Plant ProjectLocated at the Leyte Industrial Development Estate (LIDE), the Company’s smelting plant project, through its subsidiary CHGSI, will be constructed in three phases. It is important to note that CHGSI was issued its Environmental Compliance Certificate (ECC) for its Ferro-Nickel smelting plant project last April 16, 2010. With the issuance of the aforementioned ECC, CHGSI shall now commence with the project implementation of its smelting plant at the LIDE.

Earthwork activities are being undertaken for the smelting plant project. Filipino and Chinese engineers are collaborating to prepare the site to receive the equipment which is sourced from the People’s Republic of China (“China”). The Company’s partners at CHGSI are prepared to provide both technological and financial assistance, in addition to having shown interest in the off take of the output of the smelting plant.

CHGSI has signed a Memorandum of Agreement (“MOA”) with Mr. Liu ShenJie, the owner of patents and patents applications for “A Smelting Process of Ferro-Nickel with Nickel Oxide Ore Free of Crystal Water in a Blast Furnace” & “A Smelting Process of Ferro-Nickel with Oxide Ore Containing Crystal Water in a Blast Furnace” (collectively known as the “Patents”). With the signing of the MOA, CHGSI was granted an exclusive license over the Patents for its Philippine operations.

- 4 -

CHGSI has in July 2010 received notices of issuance of letters patent by the Philippine Intellectual Property Office, in favor of the Patentee Liu Shenjie, for his inventions. The letters patent grants unto its owner/s the exclusive right throughout the Philippines to make, use, sell or import the invention and where the invention includes a process, including the product obtained directly or indirectly from such process.

The project is in its pre-operating phase and therefore expenses for construction are not matched by any revenues. The first phase of the smelter project, which is targeted to be operational within 2012, is expected to produce approximately 100,000 tons of nickel pig iron, which is in high demand in China. The total project cost is approximately P1billion, to which will be added working capital requirements of about P200 million. These financial requirements are expected to be financed by a combination of debt and equity.

At the initial pre-operating stage, the smelter project is expected to employ 230 persons, at both managerial and production levels. CHGSI expects to employ additional manpower requirements depending on the smelter’s capacity.

CHGSI has received its Amended Environmental Compliance Certificate (ECC), with Reference Code 1003-0011 issued by the Environmental Management Bureau (EMB), Central Office, to include the installation of a Coking Coal Plant to be located at the LIDE in Isabel, Leyte.

CHGSI application for Mineral Processing Permit (MPP) for its Smelting Plant is under evaluation with the MGB Regional Office, Region 8 for endorsement to DENR Central Office.

Approval of Consolidated Financial StatementsThe accompanying consolidated financial statements as at and for the years ended December 31, 2011 and 2010 were authorized for issuance by the Board of Directors (BOD) on April 13, 2012.

2. Basis of Preparation

Statement of ComplianceThe accompanying consolidated financial statements have been prepared in accordance with Philippine Financial Reporting Standards (PFRS).

Basis of Measurement The consolidated financial statements of the Group have been prepared on a historical cost basis.

Functional and Presentation Currency The consolidated financial statements are presented in Philippine peso, which is the Parent Company’s functional currency. Each entity in the Group determines its own functional currency. The functional currency of the subsidiaries is also the Philippine peso. All values are rounded to the nearest peso, unless otherwise indicated.

- 3 -

Mining Operations of CPCCPC has continuing exploration work in its properties in the Province of Dinagat Islands and has recently signed Contractor’s Service Agreements with three (3) different independent contractors to conduct mining and nickel ore extraction in its Casiguran mine and its Rapid City Parcel II mine. CPC plans to market and export a minimum of 1,000,000 metric tons of nickel ore this 2012. At the same time, nickel ores will continue to be stockpiled in anticipation for the forthcoming operation of the smelter located at the Leyte Industrial Development Estate (LIDE).

Management believes that significantly more value will be added to the Groups’ raw ore, and therefore shareholder interests will be maximized, by smelting it and selling it asnickel pig iron.

Moreover, last April 2010, CPC released two Geologic Resource Evaluation Reports, an update to its Casiguran Mine Prospect, Dinagat Island covered by its MPSA 010-92-Xand a new Resource Evaluation Report for its Rapid City Parcel II Prospect covered by its MPSA 283-2009-XIII-SMR, both prepared by Dr. Carlo A. Arcilla, an Accredited Competent Person in accordance with the definition of the Philippine Mineral Reporting Code (PMRC).

Based on the reports, the Casiguran Mine Prospect has a combined indicated and measured resource of 9,897,000 DMT with a grade of 1.02% Nickel (at 0.8% nickel cut-off). In addition, new data from the Rapid City Parcel II Prospect reveal a combined indicated and measured resource of 9,067,000 DMT with a grade of 1.07% Nickel (at 0.8% Nickel cut-off). These could represent to 100,000 metric tons of pure nickel and 3.5 million tons of iron in its Casiguran property, and 90,000 tons of pure nickel and 3.8 million tons of iron in their Rapid City property, subject to mining plans and metal recovery parameters.

The management looks forward to continue developing and exploring these mineral properties either on its own or with joint venture partners. Moreover, management plans to increase CPC’s capitalization within the year 2012.

The Smelting Plant ProjectLocated at the Leyte Industrial Development Estate (LIDE), the Company’s smelting plant project, through its subsidiary CHGSI, will be constructed in three phases. It is important to note that CHGSI was issued its Environmental Compliance Certificate (ECC) for its Ferro-Nickel smelting plant project last April 16, 2010. With the issuance of the aforementioned ECC, CHGSI shall now commence with the project implementation of its smelting plant at the LIDE.

Earthwork activities are being undertaken for the smelting plant project. Filipino and Chinese engineers are collaborating to prepare the site to receive the equipment which is sourced from the People’s Republic of China (“China”). The Company’s partners at CHGSI are prepared to provide both technological and financial assistance, in addition to having shown interest in the off take of the output of the smelting plant.

CHGSI has signed a Memorandum of Agreement (“MOA”) with Mr. Liu ShenJie, the owner of patents and patents applications for “A Smelting Process of Ferro-Nickel with Nickel Oxide Ore Free of Crystal Water in a Blast Furnace” & “A Smelting Process of Ferro-Nickel with Oxide Ore Containing Crystal Water in a Blast Furnace” (collectively known as the “Patents”). With the signing of the MOA, CHGSI was granted an exclusive license over the Patents for its Philippine operations.

15ANNUAL REPORT 2011

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

- 4 -

CHGSI has in July 2010 received notices of issuance of letters patent by the Philippine Intellectual Property Office, in favor of the Patentee Liu Shenjie, for his inventions. The letters patent grants unto its owner/s the exclusive right throughout the Philippines to make, use, sell or import the invention and where the invention includes a process, including the product obtained directly or indirectly from such process.

The project is in its pre-operating phase and therefore expenses for construction are not matched by any revenues. The first phase of the smelter project, which is targeted to be operational within 2012, is expected to produce approximately 100,000 tons of nickel pig iron, which is in high demand in China. The total project cost is approximately P1billion, to which will be added working capital requirements of about P200 million. These financial requirements are expected to be financed by a combination of debt and equity.

At the initial pre-operating stage, the smelter project is expected to employ 230 persons, at both managerial and production levels. CHGSI expects to employ additional manpower requirements depending on the smelter’s capacity.

CHGSI has received its Amended Environmental Compliance Certificate (ECC), with Reference Code 1003-0011 issued by the Environmental Management Bureau (EMB), Central Office, to include the installation of a Coking Coal Plant to be located at the LIDE in Isabel, Leyte.

CHGSI application for Mineral Processing Permit (MPP) for its Smelting Plant is under evaluation with the MGB Regional Office, Region 8 for endorsement to DENR Central Office.

Approval of Consolidated Financial StatementsThe accompanying consolidated financial statements as at and for the years ended December 31, 2011 and 2010 were authorized for issuance by the Board of Directors (BOD) on April 13, 2012.

2. Basis of Preparation

Statement of ComplianceThe accompanying consolidated financial statements have been prepared in accordance with Philippine Financial Reporting Standards (PFRS).

Basis of Measurement The consolidated financial statements of the Group have been prepared on a historical cost basis.

Functional and Presentation Currency The consolidated financial statements are presented in Philippine peso, which is the Parent Company’s functional currency. Each entity in the Group determines its own functional currency. The functional currency of the subsidiaries is also the Philippine peso. All values are rounded to the nearest peso, unless otherwise indicated.

- 5 -

Use of Estimates and JudgmentsThe preparation of the consolidated financial statements in conformity with PFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements are disclosed in Note 5 to theconsolidated financial statements.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

3. Changes in Accounting Policies

The accounting policies set out below have been applied consistently to all years presented in these consolidated financial statements, and have been applied consistently by the Group, except for the changes in accounting policies as explained below.

Adoption of New or Revised Standards, Amendments to Standards and InterpretationsThe Financial Reporting Standards Council approved the adoption of a number of new or revised standards, amendments to standards, and interpretations [based on International Financial Reporting Interpretations Committee (IFRIC) Interpretations] as part of PFRSs.

The Group has adopted the following PFRSs starting January 1, 2011 and accordingly, changed its accounting policies in the following areas:

Revised PAS 24, Related Party Disclosures (2009), amends the definition of a related party and modifies certain related party disclosure requirements for government-related entities. The revised standard is effective for annual periods beginning on or after January 1, 2011.

Improvements to PFRSs 2010, contain 11 amendments to six standards and to one interpretation. The amendments are generally effective for annual periods beginning on or after January 1, 2011. The following are the said improvements or amendments to PFRSs, none of which has a significant effect on the consolidated financial statements of the Group:

• PFRS 3, Business Combinations. The amendments: (i) clarify that contingent consideration arising in a business combination previously accounted for in accordance with PFRS 3 (2004) that remains outstanding at the adoption date of PFRS 3 (2008) continues to be accounted for in accordance with PFRS 3 (2004); (ii) limit the accounting policy choice to measure non-controlling interests upon initial recognition at fair value or at the non-controlling interest’s proportionate share of the acquiree’s identifiable net assets to instruments that give rise to a present ownership interest and that currently entitle the holder to a share of net assets in the event of liquidation; and (iii) expand the current guidance on the attribution of the market-based measure of an acquirer’s share-based payment awards issued in exchange for acquiree awards between consideration transferred and post-combination compensation cost when an acquirer is obliged to replace the acquiree’s existing awards to encompass voluntarily replaced unexpired acquiree awards. The amendments are effective for annual periods beginning on or after July 1, 2010.

- 5 -

Use of Estimates and JudgmentsThe preparation of the consolidated financial statements in conformity with PFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements are disclosed in Note 5 to theconsolidated financial statements.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

3. Changes in Accounting Policies

The accounting policies set out below have been applied consistently to all years presented in these consolidated financial statements, and have been applied consistently by the Group, except for the changes in accounting policies as explained below.

Adoption of New or Revised Standards, Amendments to Standards and InterpretationsThe Financial Reporting Standards Council approved the adoption of a number of new or revised standards, amendments to standards, and interpretations [based on International Financial Reporting Interpretations Committee (IFRIC) Interpretations] as part of PFRSs.

The Group has adopted the following PFRSs starting January 1, 2011 and accordingly, changed its accounting policies in the following areas:

Revised PAS 24, Related Party Disclosures (2009), amends the definition of a related party and modifies certain related party disclosure requirements for government-related entities. The revised standard is effective for annual periods beginning on or after January 1, 2011.

Improvements to PFRSs 2010, contain 11 amendments to six standards and to one interpretation. The amendments are generally effective for annual periods beginning on or after January 1, 2011. The following are the said improvements or amendments to PFRSs, none of which has a significant effect on the consolidated financial statements of the Group:

• PFRS 3, Business Combinations. The amendments: (i) clarify that contingent consideration arising in a business combination previously accounted for in accordance with PFRS 3 (2004) that remains outstanding at the adoption date of PFRS 3 (2008) continues to be accounted for in accordance with PFRS 3 (2004); (ii) limit the accounting policy choice to measure non-controlling interests upon initial recognition at fair value or at the non-controlling interest’s proportionate share of the acquiree’s identifiable net assets to instruments that give rise to a present ownership interest and that currently entitle the holder to a share of net assets in the event of liquidation; and (iii) expand the current guidance on the attribution of the market-based measure of an acquirer’s share-based payment awards issued in exchange for acquiree awards between consideration transferred and post-combination compensation cost when an acquirer is obliged to replace the acquiree’s existing awards to encompass voluntarily replaced unexpired acquiree awards. The amendments are effective for annual periods beginning on or after July 1, 2010.

16 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

- 6 -

• PAS 27, Consolidated and Separate Financial Statements. The amendments clarify that the consequential amendments to PAS 21, The Effects of Changes in Foreign Exchange Rates, PAS 28, Investments in Associates and PAS 31, Interests in Joint Ventures resulting from PAS 27 (2008) should be applied prospectively, with the exception of amendments resulting from renumbering. The amendments are effective for annual periods beginning on or after July 1, 2010.

• PFRS 7, Financial Instruments: Disclosures. The amendments add an explicit statement that qualitative disclosure should be made in the context of the quantitative disclosures to better enable users to evaluate an entity’s exposure to risks arising from financial instruments. In addition, the IASB amended and removed existing disclosure requirements. The amendments are effective for annual periods beginning on or after January 1, 2011.

• PAS 1, Presentation of Financial Statements. The amendments clarify that disaggregation of changes in each component of equity arising from transactions recognized in other comprehensive income is also required to be presented, but may be presented either in the statement of changes in equity or in the notes. The amendments are effective for annual periods beginning on or after January 1, 2011.

New or Revised Standards, Amendments to Standards and Interpretations Not Yet Adopted

A number of new standards, amendments to standards and interpretations are effective for annual periods beginning after January 1, 2011, and have not been applied in preparing these consolidated financial statements. None of these is expected to have a significant effect on the consolidated financial statements of the Group, except for PFRS 9, Financial Instruments, which becomes mandatory for the Group’s 2015 consolidated financial statements and could change the classification and measurement of financial assets. The Group does not plan to adopt this standard early and the extent of the impact has not been determined.

The Group will adopt the following new or revised standards, amendments to standards and interpretations in the respective effective dates:

To be Adopted on January 1, 2012

Disclosures - Transfers of Financial Assets (Amendments to PFRS 7), require additional disclosures about transfers of financial assets. The amendments require disclosure of information that enables users of financial statements to understand the relationship between transferred financial assets that are not derecognized in their entirety and the associated liabilities; and to evaluate the nature of, and risks associated with, the entity’s continuing involvement in derecognized financial assets. Entities are required to apply the amendments for annual periods beginning on or after July 1, 2011. Earlier application is permitted. Entities are not required to provide the disclosures for any period that begins prior to July 1, 2011.

- 7 -

Deferred Tax: Recovery of Underlying Assets (Amendments to PAS 12) introduces an exception to the current measurement principles of deferred tax assets and liabilities arising from investment property measured using the fair value model in accordance with PAS 40, Investment Property. The exception also applies to investment properties acquired in a business combination accounted for in accordance with PFRS 3, Business Combinations provided the acquirer subsequently measure these assets applying the fair value model. The amendments integrated the guidance of Philippine Interpretation SIC-21, Income Taxes - Recovery of Revalued Non-Depreciable Assets into PAS, 12 Income Taxes, and as a result Philippine Interpretation SIC-21 has been withdrawn. The effective date of the amendments is for periods beginning on or after January 1, 2012 and is applied retrospectively. Early application is permitted.

To be Adopted on January 1, 2013

Presentation of Items of Other Comprehensive Income (Amendments to PAS 1). The amendments:

• require that an entity present separately the items of other comprehensive income that would be reclassified to profit or loss in the future if certain conditions are met from those that would never be reclassified to profit or loss;

• do not change the existing option to present profit or loss and other comprehensive income in two statements; and

• change the title of the statement of comprehensive income to the statement of profit or loss and other comprehensive income. However, an entity is still allowed to use other titles.

The amendments do not address which items are presented in other comprehensive income or which items need to be reclassified. The requirements of other PFRSs continue to apply in this regard.

PFRS 10, Consolidated Financial Statements

PFRS 10 introduces a new approach to determining which investees should be consolidated and provides a single model to be applied in the control analysis for all investees.

An investor controls an investee when:

• it is exposed or has rights to variable returns from its involvement with that investee;

• it has the ability to affect those returns through its power over that investee; and• there is a link between power and returns.

Control is re-assessed as facts and circumstances change.

PFRS 10 supersedes PAS 27 (2008) and Philippine Interpretation SIC-12, Consolidation - Special Purpose Entities.

- 6 -

• PAS 27, Consolidated and Separate Financial Statements. The amendments clarify that the consequential amendments to PAS 21, The Effects of Changes in Foreign Exchange Rates, PAS 28, Investments in Associates and PAS 31, Interests in Joint Ventures resulting from PAS 27 (2008) should be applied prospectively, with the exception of amendments resulting from renumbering. The amendments are effective for annual periods beginning on or after July 1, 2010.

• PFRS 7, Financial Instruments: Disclosures. The amendments add an explicit statement that qualitative disclosure should be made in the context of the quantitative disclosures to better enable users to evaluate an entity’s exposure to risks arising from financial instruments. In addition, the IASB amended and removed existing disclosure requirements. The amendments are effective for annual periods beginning on or after January 1, 2011.

• PAS 1, Presentation of Financial Statements. The amendments clarify that disaggregation of changes in each component of equity arising from transactions recognized in other comprehensive income is also required to be presented, but may be presented either in the statement of changes in equity or in the notes. The amendments are effective for annual periods beginning on or after January 1, 2011.

New or Revised Standards, Amendments to Standards and Interpretations Not Yet Adopted

A number of new standards, amendments to standards and interpretations are effective for annual periods beginning after January 1, 2011, and have not been applied in preparing these consolidated financial statements. None of these is expected to have a significant effect on the consolidated financial statements of the Group, except for PFRS 9, Financial Instruments, which becomes mandatory for the Group’s 2015 consolidated financial statements and could change the classification and measurement of financial assets. The Group does not plan to adopt this standard early and the extent of the impact has not been determined.

The Group will adopt the following new or revised standards, amendments to standards and interpretations in the respective effective dates:

To be Adopted on January 1, 2012

Disclosures - Transfers of Financial Assets (Amendments to PFRS 7), require additional disclosures about transfers of financial assets. The amendments require disclosure of information that enables users of financial statements to understand the relationship between transferred financial assets that are not derecognized in their entirety and the associated liabilities; and to evaluate the nature of, and risks associated with, the entity’s continuing involvement in derecognized financial assets. Entities are required to apply the amendments for annual periods beginning on or after July 1, 2011. Earlier application is permitted. Entities are not required to provide the disclosures for any period that begins prior to July 1, 2011.

17ANNUAL REPORT 2011

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

- 7 -

Deferred Tax: Recovery of Underlying Assets (Amendments to PAS 12) introduces an exception to the current measurement principles of deferred tax assets and liabilities arising from investment property measured using the fair value model in accordance with PAS 40, Investment Property. The exception also applies to investment properties acquired in a business combination accounted for in accordance with PFRS 3, Business Combinations provided the acquirer subsequently measure these assets applying the fair value model. The amendments integrated the guidance of Philippine Interpretation SIC-21, Income Taxes - Recovery of Revalued Non-Depreciable Assets into PAS, 12 Income Taxes, and as a result Philippine Interpretation SIC-21 has been withdrawn. The effective date of the amendments is for periods beginning on or after January 1, 2012 and is applied retrospectively. Early application is permitted.

To be Adopted on January 1, 2013

Presentation of Items of Other Comprehensive Income (Amendments to PAS 1). The amendments:

• require that an entity present separately the items of other comprehensive income that would be reclassified to profit or loss in the future if certain conditions are met from those that would never be reclassified to profit or loss;

• do not change the existing option to present profit or loss and other comprehensive income in two statements; and

• change the title of the statement of comprehensive income to the statement of profit or loss and other comprehensive income. However, an entity is still allowed to use other titles.

The amendments do not address which items are presented in other comprehensive income or which items need to be reclassified. The requirements of other PFRSs continue to apply in this regard.

PFRS 10, Consolidated Financial Statements

PFRS 10 introduces a new approach to determining which investees should be consolidated and provides a single model to be applied in the control analysis for all investees.

An investor controls an investee when:

• it is exposed or has rights to variable returns from its involvement with that investee;

• it has the ability to affect those returns through its power over that investee; and• there is a link between power and returns.

Control is re-assessed as facts and circumstances change.

PFRS 10 supersedes PAS 27 (2008) and Philippine Interpretation SIC-12, Consolidation - Special Purpose Entities.

- 8 -

PFRS 12, Disclosure of Interests in Other Entities

PFRS 12 contains the disclosure requirements for entities that have interests in subsidiaries, joint arrangements (i.e. joint operations or joint ventures), associates and/or unconsolidated structured entities, aiming to provide information to enable users to evaluate:

• the nature of, and risks associated with, an entity’s interests in other entities; and• the effects of those interests on the entity’s financial position, financial

performance and cash flows.

PFRS 13, Fair Value Measurement

PFRS 13 replaces the fair value measurement guidance contained in individual PFRSs with a single source of fair value measurement guidance. It defines fair value, establishes a framework for measuring fair value and sets out disclosure requirements for fair value measurements. It explains how to measure fair value when it is required or permitted by other PFRSs. It does not introduce new requirements to measure assets or liabilities at fair value, nor does it eliminate the practicability exceptions to fair value measurements that currently exist in certain standards.

PAS 27, Separate Financial Statements (2011)

PAS 27 (2011) supersedes PAS 27 (2008). PAS 27 (2011) carries forward the existing accounting and disclosure requirements for separate financial statements, with some minor clarifications.

To be Adopted on January 1, 2015

PFRS 9, Financial Instruments (2009)

Standard Issued in November 2009 [PFRS 9 (2009)]PFRS 9 (2009) is the first standard issued as part of a wider project to replace PAS 39. PFRS 9 (2009) retains but simplifies the mixed measurement model and establishes two primary measurement categories for financial assets: amortized cost and fair value. The basis of classification depends on the entity’s business model and the contractual cash flow characteristics of the financial asset. The guidance in PAS 39 on impairment of financial assets and hedge accounting continues to apply.

Standard Issued in October 2010 [PFRS 9 (2010)]PFRS 9 (2010) adds the requirements related to the classification and measurement of financial liabilities, and derecognition of financial assets and liabilities to the version issued in November 2009.

It also includes those paragraphs of PAS 39 dealing with how to measure fair value and accounting for derivatives embedded in a contract that contains a host that is not a financial asset, as well as the requirements of Philippine Interpretation IFRIC 9,Reassessment of Embedded Derivatives.

Under prevailing circumstances, the adoption of the above new or revised standards, amendments to standards and interpretations in 2012, 2013 and 2015 is not expected to have any material effect on the consolidated financial statements. Additional disclosures required by the new or revised standards, amendments to standards and interpretations will be included in the consolidated financial statements, where applicable.

- 9 -

4. Summary of Significant Accounting Policies

Basis of ConsolidationSubsidiaries Subsidiaries are entities controlled by the Group. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. The accounting policies of subsidiaries have been consistent and aligned with the policies adopted by the Group.

Transactions Eliminated on ConsolidationIntra-group balances and transactions, and any unrealized income and expense arising from intra-group transactions, are eliminated in preparing the consolidated financial statements.

Non-controlling interestNon-controlling interest represents the portion of profit and loss and net assets not held by the Group in CHGSI and are presented separately in the consolidated statement of comprehensive income and within equity in the consolidated statements of financial position, separately from equity attributable to equity holders of the Parent Company.

Financial InstrumentsDate of Recognition. Financial instruments are recognized in the consolidated statementsof financial position when it becomes a party to the contractual provisions of the instrument. Regular way purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace are recognized on the settlement date.

Initial Recognition of Financial Instruments. Financial instruments are recognized initially at fair value of the consideration given (in the case of an asset) or received (in the case of a liability). Except for financial instruments at fair value through profit or loss (FVPL), the initial measurement of financial assets includes transactions costs.

Determination of Fair Value. The fair value of financial instruments traded in active markets is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and ask prices are not available, the price of the most recent transaction provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction. For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques and comparison to similar instruments for which market observable prices exist.

Categories of Financial Instruments. The Group classifies its financial assets into the following categories: financial assets at FVPL, held-to-maturity (HTM) investments, available-for-sale (AFS) financial assets, and loans and receivables. The Group classifies its financial liabilities into financial liabilities at FVPL and other financial liabilities. The classification depends on the purpose for which the investments were acquired and the liabilities incurred and whether they are quoted in an active market. Management determines the classification of its financial instruments at initial recognition and, where allowed and appropriate, re-evaluates such designation at every reporting date.

As of December 31, 2011 and 2010, the Group has no financial assets at FVPL, HTM investments and financial liabilities at FVPL.

- 8 -

PFRS 12, Disclosure of Interests in Other Entities

PFRS 12 contains the disclosure requirements for entities that have interests in subsidiaries, joint arrangements (i.e. joint operations or joint ventures), associates and/or unconsolidated structured entities, aiming to provide information to enable users to evaluate:

• the nature of, and risks associated with, an entity’s interests in other entities; and• the effects of those interests on the entity’s financial position, financial

performance and cash flows.

PFRS 13, Fair Value Measurement

PFRS 13 replaces the fair value measurement guidance contained in individual PFRSs with a single source of fair value measurement guidance. It defines fair value, establishes a framework for measuring fair value and sets out disclosure requirements for fair value measurements. It explains how to measure fair value when it is required or permitted by other PFRSs. It does not introduce new requirements to measure assets or liabilities at fair value, nor does it eliminate the practicability exceptions to fair value measurements that currently exist in certain standards.

PAS 27, Separate Financial Statements (2011)

PAS 27 (2011) supersedes PAS 27 (2008). PAS 27 (2011) carries forward the existing accounting and disclosure requirements for separate financial statements, with some minor clarifications.

To be Adopted on January 1, 2015

PFRS 9, Financial Instruments (2009)

Standard Issued in November 2009 [PFRS 9 (2009)]PFRS 9 (2009) is the first standard issued as part of a wider project to replace PAS 39. PFRS 9 (2009) retains but simplifies the mixed measurement model and establishes two primary measurement categories for financial assets: amortized cost and fair value. The basis of classification depends on the entity’s business model and the contractual cash flow characteristics of the financial asset. The guidance in PAS 39 on impairment of financial assets and hedge accounting continues to apply.

Standard Issued in October 2010 [PFRS 9 (2010)]PFRS 9 (2010) adds the requirements related to the classification and measurement of financial liabilities, and derecognition of financial assets and liabilities to the version issued in November 2009.

It also includes those paragraphs of PAS 39 dealing with how to measure fair value and accounting for derivatives embedded in a contract that contains a host that is not a financial asset, as well as the requirements of Philippine Interpretation IFRIC 9,Reassessment of Embedded Derivatives.

Under prevailing circumstances, the adoption of the above new or revised standards, amendments to standards and interpretations in 2012, 2013 and 2015 is not expected to have any material effect on the consolidated financial statements. Additional disclosures required by the new or revised standards, amendments to standards and interpretations will be included in the consolidated financial statements, where applicable.

18 CENTURY PEAK METALS HOLDINGS CORPORATION AND SUBSIDIARIES

N O T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S

- 9 -

4. Summary of Significant Accounting Policies

Basis of ConsolidationSubsidiaries Subsidiaries are entities controlled by the Group. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. The accounting policies of subsidiaries have been consistent and aligned with the policies adopted by the Group.

Transactions Eliminated on ConsolidationIntra-group balances and transactions, and any unrealized income and expense arising from intra-group transactions, are eliminated in preparing the consolidated financial statements.

Non-controlling interestNon-controlling interest represents the portion of profit and loss and net assets not held by the Group in CHGSI and are presented separately in the consolidated statement of comprehensive income and within equity in the consolidated statements of financial position, separately from equity attributable to equity holders of the Parent Company.

Financial InstrumentsDate of Recognition. Financial instruments are recognized in the consolidated statementsof financial position when it becomes a party to the contractual provisions of the instrument. Regular way purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace are recognized on the settlement date.

Initial Recognition of Financial Instruments. Financial instruments are recognized initially at fair value of the consideration given (in the case of an asset) or received (in the case of a liability). Except for financial instruments at fair value through profit or loss (FVPL), the initial measurement of financial assets includes transactions costs.

Determination of Fair Value. The fair value of financial instruments traded in active markets is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and ask prices are not available, the price of the most recent transaction provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction. For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques and comparison to similar instruments for which market observable prices exist.