c a l & e a s t ern eu op r sia ce n t r al & e a s t e rn...

TRANSCRIPT

Prices:Euro zone: EUR 10.00Poland: PLN 35.00 (incl. Tax)Czech Republic: CZK 257.00Ukraine: UAH 10.00Slovakia: EUR 10.00Russia: USD 15.00United Kingdom: GBP 3.50Romania: RON 39.00USA: USD 15.00

Covering: Baltics, Belarus, Bulgaria, Croatia, Czech Republic, Hungary, Kazakhstan,Montenegro, Poland, Romania, Russia - CIS, Serbia, Slovakia and Ukraine

RETAILGUIDE

Volume 21, Number 1, November 2015

Central & Eastern Europe Russia - CIS

Euro zone: EUR 10.00Poland: PLN 35.00 (incl. Tax)Czech Republic: CZK 257.00Ukraine: UAH 10.00Slovakia: EUR 10.00Russia: USD 15.00United Kingdom: GBP 3.50Romania: RON 39.00

Investment cover final print 2.indd 1 05/11/15 09:58

8th Annual

InterContinental Hotel, Warsaw, Poland28th January 2016

www.RetailAwards.eu

PARTNERS FOR 2016

CEE RETAILAWARDS

#CEERetailAwardsFor further information contact:

Craig Smith/ +48 604 144 769 / [email protected] Kaliszewska/ +48 601 382 667 / [email protected]

Premier Partners:

Auditor:

Venue Partner: Car Rental Partner: PR Solution Partners:

Supporting Partners: Media Partner:

Energy Software Partner:

REAL ESTATESoftware & Services

Warsaw, Poland

JURY MEMBERS:

Rafał ChrapkowiczPako Lorente Sp. z o.o.President

Krzysztof ApostolidisFabryka Biznesu Sp. z o.o. - investor of SUKCESJAPresident of Board

Laurence PaquetImmochan PolandCEO

Matteo MarzottoPercassi

Dieter KnittelDeutsche Pfandbriefbank AGDirector Europe, Real Estate Finance International

Joanna JóźwiakH&M Hennes and Mauritz Sp. z o.o.Expansion Manager CEE

Markus PinggeraDeichmannHead of Expansion and Law CSEE

Marek SkoczylasMedia Saturn Holding PolandHead of Real Estate Poland

Krzysztof BocianowskiLPP S.ALeasing and Expansion Director

Waldemar MadajczykGuess PolandExecutive Board member

Arne BongenaarActeeum GroupManaging Director

Adrian J. HeymansECC Real EstateCEO

Ilona Gryszko-RedoAlshaya PolandHead of Property CEE

Wojciech SztubaTPA HorwathManaging Director

Petr ŽahourH&M Hennes & Mauritz CZLease Manager

Andrzej CzarneckiEURO-net Sp. z o.o.Development Director

Kasia VolkmanTK MAXX,Head of Acquisitions & Real Estate, Poland/Austria

Marko SchönebeckHunkemöller DeutschlandReal Estate Manager

Paweł OskrędaSmykProperty Director

Philippe BeurtheretImmochan HungaryGeneral Manager

Anton SemenenkoRapa GroupHead of Retail Businesses, Member of the Board of Directors

Artur KazienkoKAZAR FootwearOwner

Dorota WiaderekGO Sport Polska Sp. z o.o.General Director

Serdar ErsoyDefacto RetailChief Growth O� cer (CGO)

Karolina Bykowska“GINO ROSSI S.A” ; “SIMPLE”Investment & Development Manager

Alexandra von der GrünAdidas AGDirector Real Estate Western Europe

Paweł Korobacz“YES Biżuteria”Expansion & Organisation Director

Nevena KosticRetail SEE Group d.o.oOwner / Director

Mihai DuicaH&MLease Manager Romania & Hungary

Ivana WinbladhUK Trade & InvestmentRegional Lead for Retail

Vijay GoelLondon Chamber of Commerce Asian Business Association (ABA)Chairman

Christoph GesslerC&A Buying GmbH & Co. KGHead of Global Real Estate

Ronan MartinCarrefour PolskaExpansion and Shopping Centers Director, Vice President of the Board

Małgorzata GabryśOTCF S.A.”4F”Director Expansion & Investment

Harald AichbergerC&ALeiter Expansion/Immobilien Österre-ich/CEE/SEE

Award Sponsors:

Public Relations

Luxury Spirit Partner: Cocktail Partners:

Central & Eastern Europe Russia - CIS

z-gate investment2.indd 1 05/11/15 10:03

8th Annual

InterContinental Hotel, Warsaw, Poland28th January 2016

www.RetailAwards.euPARTNERS FOR 2016

#CEERetailAwardsFor further information contact:

Craig Smith/ +48 604 144 769 / [email protected] Kaliszewska/ +48 601 382 667 / [email protected]

CEE RETAILAWARDS

Premier Partners:

Award Sponsors:

Auditor:

Venue Partner: Car Rental Partner: PR Solution Partners:

Supporting Partners: Media Partner: Energy Software Partner:

REAL ESTATESoftware & Services

Public Relations

Luxury Spirit Partner: Cocktail Partners:

Warsaw, Poland

JURY MEMBERS:

Rafał ChrapkowiczPako Lorente Sp. z o.o.President

Krzysztof ApostolidisFabryka Biznesu Sp. z o.o. - investor of SUKCESJAPresident of Board

Laurence PaquetImmochan PolandCEO

Matteo MarzottoPercassi

Dieter KnittelDeutsche Pfandbriefbank AGDirector Europe, Real Estate Finance International

Joanna JóźwiakH&M Hennes and Mauritz Sp. z o.o.Expansion Manager CEE

Markus PinggeraDeichmannHead of Expansion and Law CSEE

Marek SkoczylasMedia Saturn Holding PolandHead of Real Estate Poland

Krzysztof BocianowskiLPP S.ALeasing and Expansion Director

Waldemar MadajczykGuess PolandExecutive Board member

Arne BongenaarActeeum GroupManaging Director

Adrian J. HeymansECC Real EstateCEO

Ilona Gryszko-RedoAlshaya PolandHead of Property CEE

Wojciech SztubaTPA HorwathManaging Director

Petr ŽahourH&M Hennes & Mauritz CZLease Manager

Andrzej CzarneckiEURO-net Sp. z o.o.Development Director

Kasia VolkmanTK MAXX,Head of Acquisitions & Real Estate, Poland/Austria

Marko SchönebeckHunkemöller DeutschlandReal Estate Manager

Paweł OskrędaSmykProperty Director

Philippe BeurtheretImmochan HungaryGeneral Manager

Anton SemenenkoRapa GroupHead of Retail Businesses, Member of the Board of Directors

Artur KazienkoKAZAR FootwearOwner

Dorota WiaderekGO Sport Polska Sp. z o.o.General Director

Serdar ErsoyDefacto RetailChief Growth O� cer (CGO)

Karolina Bykowska“GINO ROSSI S.A” ; “SIMPLE”Investment & Development Manager

Alexandra von der GrünAdidas AGDirector Real Estate Western Europe

Paweł Korobacz“YES Biżuteria”Expansion & Organisation Director

Nevena KosticRetail SEE Group d.o.oOwner / Director

Mihai DuicaH&MLease Manager Romania & Hungary

Ivana WinbladhUK Trade & InvestmentRegional Lead for Retail

Vijay GoelLondon Chamber of Commerce Asian Business Association (ABA)Chairman

Christoph GesslerC&A Buying GmbH & Co. KGHead of Global Real Estate

Ronan MartinCarrefour PolskaExpansion and Shopping Centers Director, Vice President of the Board

Małgorzata GabryśOTCF S.A.”4F”Director Expansion & Investment

Harald AichbergerC&ALeiter Expansion/Immobilien Österre-ich/CEE/SEE

FORUM GDANSKFood meets fashion

OPENING 2017

For leasing inquires please contact: Małgorzata Słowik, [email protected] Anna Piotrowska, [email protected] tel. +48 22 22 22 800

FORUM GDAŃSK

Diverse food offer

Over 25 food court and full-service restaurant units with unique terrace seating overlooking the historic old town of Gdańsk.

Program: • 62.000 sqm GLA, 220 units including flagship stores, largest multiplex cinema and inner-city supermarket• Largest public transport hub• New central square of Gdansk• Combination of individual buildings, streets and squares• The Gdansk Historic Heritage Centre and new Tourist Information office within the project • 1.100 parking spaces

4

6

8

12

18

28

32

3620

22

26

Editorial

Regional quotes

Regional Investment

SEE Overview

Regional

Regional CEE Retail Awards

CEE Investment & Green Building Awards

Poland OverviewNEE Overview

NEE Overview

NEE Overview

Growing investor interest in CEE retail

The CEE investment market is on the up with

a huge amount of money looking for a home.

This is particularly benefi ting the retail sector with

CBRE recording a 99 percent increase on 2014 with

€2,153 million in deals as of the end of the third

quarter. However, these fi gures can be misleading

as retail investment tends to grab the headlines, of-

ten due to the large lots sizes and some analysts ar-

gue that appetite for retail assets is not signifi cantly

higher than other commercial sectors.

Poland’s retail sector grows in the agglomerations, with new trends on the rise

While Q3 brought about just a modest sprinkling of

new completions, Poland’s retail sector has continued

to be defi ned by strong growth in the major agglomera-

tions, while at the same time continuing to ride a wave of

redevelopments, refurbishments and expansions of exist-

ing retail stock.

Limited supply prevents overheating

Although retail delivery has been limited, new supply

is expected to resume in 2016-2017, with the delivery of

schemes under construction. New retailers are competing

for space in the best-performing shopping centres, and

high-street locations in Prague, although there are limited

locations for new development.

page 8 page 54

page 36

Growing investor interest in CEE retail

Turkish fashion brands expanding

across South Eastern Europe

Expo Real Overview

Retail excellence honoured at the 7th annual EuropaProperty

CEE Retail Awards Gala

Region’s top real estate fi rms recognised at EuropaProperty’s

5th annual CEE Investment & Green Building Awards

Poland’s retail sector grows in the agglomerations,

with new trends on the rise

Professional of the Year: Bogoljub Karić

on Dana Holdings and his BK Group

Demanding market dynamics

creating survival of the fi ttest mentality

Large scale pipeline developments mark the Baltics retail landscape

72

40

42

44

48

52

54

64

58

68

60

70

74

78

Russia quotes

Tri-City Overview

Poland Retail

Poland Warsaw

Poland Investment

Hungary Overview

Czech Rep. Overview

Bulgaria Overview

Slovakia Overview

Croatia Overview

Romania Overview

Serbia Overview

Russia Overview

Ukraine Overview

2015

18-20 November

MAPIC 2015

The International Real Property Market

Palais des Festivals, Cannes, France

www.mapic.com

25-26 November

EEA Real Estate Forum & Project Awards

Fairmont Grand Hotel,

Kiev, Ukraine

www.eeaawards.com

2016

28 January

8th Annual EuropaProperty CEE Retail Awards

InterContinental, Warsaw, Poland

www.retailawards.eu

1- 4 March

22nd International Fair for Industrial

Automation AUTOMATICON

EXPOCENTRE XXI, Warsaw, Poland

www.automaticon.pl

15-18 March

MIPIM

Palais des Festivals, Cannes, France

www.mipim.com

30-31 March

2nd Annual EuropaProperty

NEE Real Estate Awards

Crowne Plaza Minsk Hotel, Minsk, Belarus

www.neeawards.com

11-13 April

International Property Show

World Trade Centre, Dubai

www.internationalpropertyshow.ae

21 April

11th Annual EuropaProperty

SEE Real Estate Awards & Forum

Radisson Blu Hotel, Bucharest, Romania

www.seerealestateawards.com

25-29 April

Hannover Messe

Hannover, Germany

www.hannovermesse.de

26 May

CEE Energy Awards

InterContinental, Warsaw, Poland

www.ceeenergyawards.com

6-7 June

The 11th Annual CEE GRI

Prague, Czech Republic

www.globalrealestate.org

16 June

4th Annual EuropaProperty

CEE Manufacturing Awards

InterContinental, Warsaw, Poland

www.manufacturingawards.eu

20-22 June

IX SEE Real Estate

Belgrade Exhibition & Conference

Belgrade, Serbia

www.rebec.rs

Positive retail fundamentals for Romania

The Romanian retail market is again attracting

developers and retailers with economic growth and

a strong rise in consumption recorded for the fi rst

half of the year. Cushman & Wakefi eld research indi-

cates that retail sales rose by 4.2 percent year-on-year

for May. This is seen as an incentive for retailers to

pursue more ambitious expansion plans in both Bu-

charest and regional cities such as Timisoara, Craiova

and Brasov, which can still support an increase in

shopping centre stock.

page 60

Tri-City: Baltic Boomtown

Commercial potential of PKP S.A. real estate

Construction of new retail in Warsaw gaining momentum

Good perspectives remain for retail investment

Limited space to meet retail demand

Limited supply prevents overheating

Bulgaria’s outlook never looked brighter

Retail development in regional cities

Development in regional cities

Positive retail fundamentals for Romania

Need for new development to meet retail demand

Retail demand slowing, but a gradual recovery forecast

Multi opens Forum Lviv, its fi rst shopping centre in Ukraine

Real EstateEvent Calendar

Editorial

The quality of CEE shopping centres is seen as improving as

“fourth or fi fth generation” centres are delivered across the

region. Prime stock is now regarded as close to the standard

of centres found in Western Europe when it comes to design, as in

many cases they are developed by pan-European developers.

However, CEE shopping centres also lag behind Western Europe

in terms of tenant mix, as the top schemes are still missing some

brands that are present in Western Europe. In addition, some niche

products are lacking, as is the provision of quality food and gastron-

omy outlets. Retailers are also pursuing cautious expansion policies

by entering markets through franchises rather than direct entry.

This also applies to the more established Polish and Czech markets.

At the moment it is unlikely that the markets will become over-

heated as was the case in some countries. The under-performance

and failure of some schemes has been analysed and pipeline is now

more correlated to the local retail and economic environment, in

order to avoid failures.

Developers are conducting detailed research in relation to loca-

tion, income spread in the area and wider macro-economic factors.

Timing is seen as a central issue in the schedule of construction, and

in this way a number of established retail developers have planned

projects that have been on hold for several years, while the devel-

opers and their advisers wait for the most advantageous date for

the start of construction. This calculation obviously brings together

a number of issues such as predicting average income, and there-

fore spending power, and the sourcing of anchor tenants in the

three-year development time. These issues facing developers have

also extended to the political and legal sphere in some markets as

legislation directly aff ecting the retail sector has been introduced at

very short notice with no clear indication of the long term implica-

tions for the retail industry.

Obviously this more rational approach from developers is infl u-

enced by lenders who are conducting their own detailed economic

research and have been imposing stricter lending conditions. This

often involves a higher equity contribution from developers and

a better quality of pre-lets.

From a positive perspective, established European retail develop-

ers and more optimistic investor/developers are increasingly devel-

oping more niche shopping centres and projects in smaller second-

ary cities as the markets in some capital cities are seen as close to

saturation. Research has indicated that these projects will only be

sustainable if a centre is delivered with an appropriate size and ten-

ant mix. This has not always been the case in recent years.

Developers are implementing these practices in less established

markets where very limited retail development has resulted in

a shortage of supply to meet the demands of retailers looking to

enter the market, although debt fi nance is still more expensive and

diffi cult to source.

Investors are increasingly looking to the development option as

there is a limited stock of retail product in CEE and buyers tend to

keep hold of their purchase once an acquisition has been concluded.

Gary J. Morrell

Central & Eastern Europe

Russia-CIS

RETAIL GUIDE

Volume 21, Number 1,

November 2015

Publishing House

Premier Media Sp. z o.o.

Al. Jerozolimskie 81

ORCO Tower, fl oor 13, offi ce 13.01

00-001 Warsaw, Poland

Publisher

Craig Smith

+48 604 144 769

Sales & Marketing Director

Anna Kaliszewska

+48 601 382 667

Editorial Director

Winston Norman

+48 506 535 293

Editor

Gary J. Morrell

+36 703 199 068

Journalists

Gary J. Morrell

Winston Norman

Elie Issa

Alex Webber

Yuri Drazdow

Key Account Manager

Sylwia Gajda

+48 501 091 751

Marketing Department

+48 (22) 586 30 29

+48 (22) 586 30 29

Poland Country Manager

Anna Kaliszewska

+48 601 382 667

Hungary Country Manager

Gary J. Morrell

+36 1 217 34 25

+36 703 199 068

Romania Country Manager

Mihaela Mazilescu

+40 21 781 25 93

+40 722 517 680

Russia CIS Regional Manager

Mikhail Barkovskiy

+ 48 (22) 586 30 10

Ukraine Country Manager

Irena Lisowska

+ 48 (22) 586 30 10

Administration

+ 48 (22) 586 30 10

Subscription

+48 (22) 586 30 28

Graphic

UUUUNNNNDDDDEEERRR CCOOONNNNNSTTTRRRUUUUCCCCTTTTIIIOOOONNNNN,,OOOPPPPEEEENNNNIIIINNNNGGGG 2222QQQQQQQ 2222222220000000000111111117777777777

WARSAW’S TWOBRIGHTEST STARS

PLANNED OPENING1H 2018

Globe Trade Centre S.A., phone: +48 22 60 60 700, e-mail: [email protected]

6 Retail Guide 2015

Regional Quotes

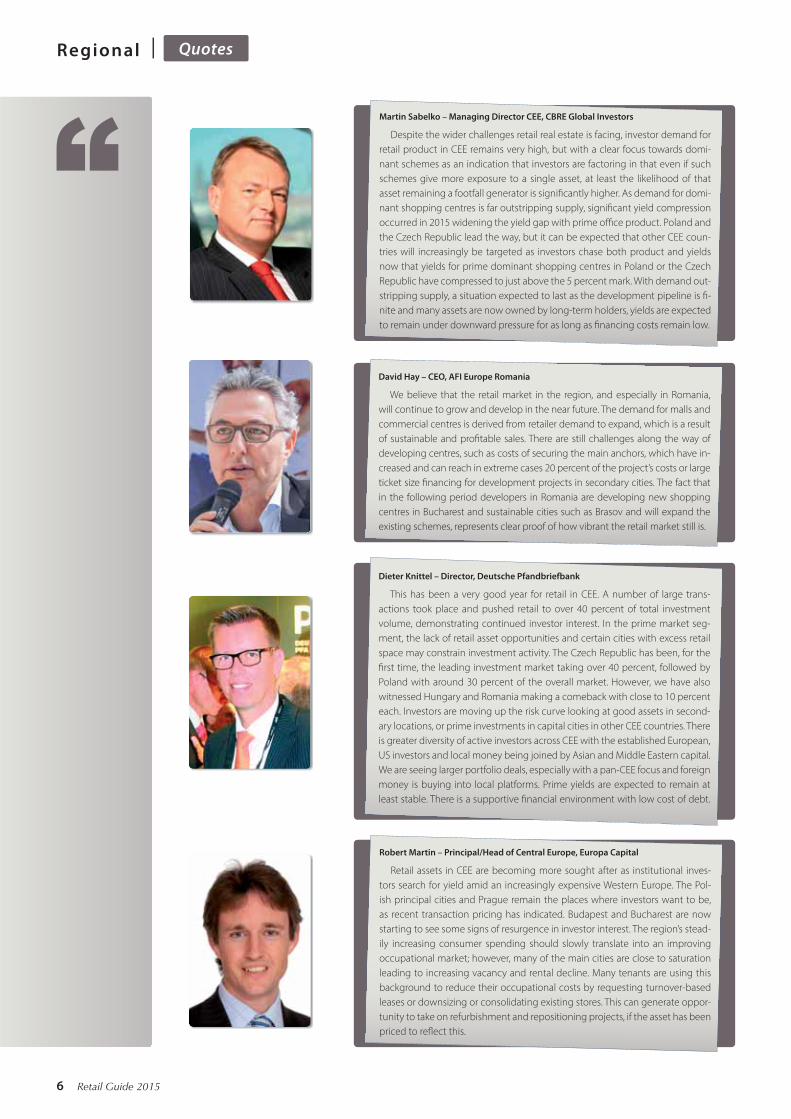

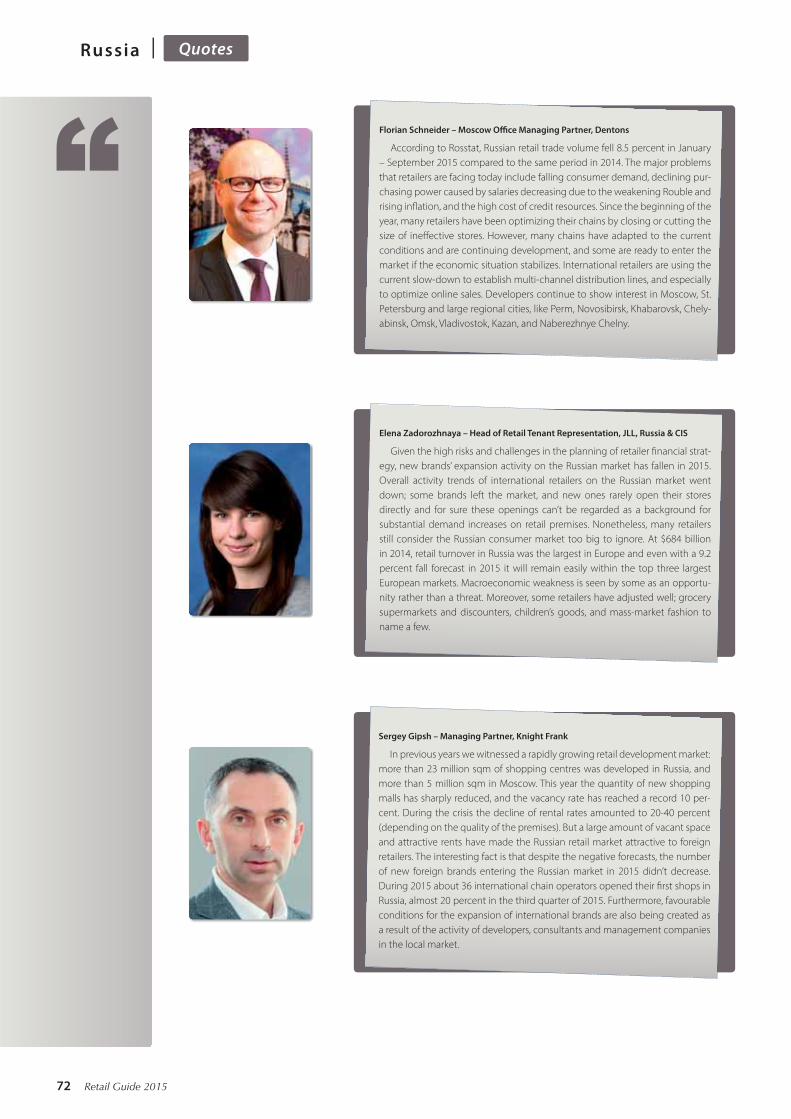

Martin Sabelko – Managing Director CEE, CBRE Global Investors

Despite the wider challenges retail real estate is facing, investor demand for

retail product in CEE remains very high, but with a clear focus towards domi-

nant schemes as an indication that investors are factoring in that even if such

schemes give more exposure to a single asset, at least the likelihood of that

asset remaining a footfall generator is signifi cantly higher. As demand for domi-

nant shopping centres is far outstripping supply, signifi cant yield compression

occurred in 2015 widening the yield gap with prime offi ce product. Poland and

the Czech Republic lead the way, but it can be expected that other CEE coun-

tries will increasingly be targeted as investors chase both product and yields

now that yields for prime dominant shopping centres in Poland or the Czech

Republic have compressed to just above the 5 percent mark. With demand out-

stripping supply, a situation expected to last as the development pipeline is fi -

nite and many assets are now owned by long-term holders, yields are expected

to remain under downward pressure for as long as fi nancing costs remain low.

Dieter Knittel – Director, Deutsche Pfandbriefbank

This has been a very good year for retail in CEE. A number of large trans-

actions took place and pushed retail to over 40 percent of total investment

volume, demonstrating continued investor interest. In the prime market seg-

ment, the lack of retail asset opportunities and certain cities with excess retail

space may constrain investment activity. The Czech Republic has been, for the

fi rst time, the leading investment market taking over 40 percent, followed by

Poland with around 30 percent of the overall market. However, we have also

witnessed Hungary and Romania making a comeback with close to 10 percent

each. Investors are moving up the risk curve looking at good assets in second-

ary locations, or prime investments in capital cities in other CEE countries. There

is greater diversity of active investors across CEE with the established European,

US investors and local money being joined by Asian and Middle Eastern capital.

We are seeing larger portfolio deals, especially with a pan-CEE focus and foreign

money is buying into local platforms. Prime yields are expected to remain at

least stable. There is a supportive fi nancial environment with low cost of debt.

David Hay – CEO, AFI Europe Romania

We believe that the retail market in the region, and especially in Romania,

will continue to grow and develop in the near future. The demand for malls and

commercial centres is derived from retailer demand to expand, which is a result

of sustainable and profi table sales. There are still challenges along the way of

developing centres, such as costs of securing the main anchors, which have in-

creased and can reach in extreme cases 20 percent of the project’s costs or large

ticket size fi nancing for development projects in secondary cities. The fact that

in the following period developers in Romania are developing new shopping

centres in Bucharest and sustainable cities such as Brasov and will expand the

existing schemes, represents clear proof of how vibrant the retail market still is.

Robert Martin – Principal/Head of Central Europe, Europa Capital

Retail assets in CEE are becoming more sought after as institutional inves-

tors search for yield amid an increasingly expensive Western Europe. The Pol-

ish principal cities and Prague remain the places where investors want to be,

as recent transaction pricing has indicated. Budapest and Bucharest are now

starting to see some signs of resurgence in investor interest. The region’s stead-

ily increasing consumer spending should slowly translate into an improving

occupational market; however, many of the main cities are close to saturation

leading to increasing vacancy and rental decline. Many tenants are using this

background to reduce their occupational costs by requesting turnover-based

leases or downsizing or consolidating existing stores. This can generate oppor-

tunity to take on refurbishment and repositioning projects, if the asset has been

priced to refl ect this.

Regional Quotes

Martin Erbe – Head of International Real Estate Finance, Helaba

The Polish retail market will continue to boom. Poland ranks fi rst in Europe

with annual sales growth of around 6.3 percent, vacancy is at a low level (espe-

cially when compared to some offi ce market vacancies), interest from tenants

and investors remains high and developers are planning and completing new

schemes of all sizes. The big advantage for all parties in retail compared to of-

fi ce is the wide variety of product – big shopping centre vs. small retail unit,

Capital vs. small town, new vs. old established centre, high vs. low yields. But as

some markets have already reached the saturation level (or perhaps beyond)

banks will become cautious fi nancing new centre developments in these re-

gions. Certainly more welcome to banks are extensions of shopper-proven lo-

cations with a track record and existing infrastructure.

Ronan Martin – Expansion and Shopping Centres Director,

Vice President of the Board, Carrefour

The Polish retail market is very competitive. It not only struggles with the cur-

rent price defl ation, but also declines in customer loyalty. Each year it becomes

more saturated in each format and faces the rising importance of e-commerce.

In this fi eld only those investors and retailers who can respond faster to custom-

er expectations and changes in their behaviour will succeed. Carrefour, thanks

to its multi-format approach and the strategy aimed at extension, remodeling

and re-commercialization of assets, is able to off er tenants and customers new

and modern retail space. The investors need to focus on innovations as well.

That’s why Carrefour invests not only in modern marketing, events and ani-

mations, but also in digitalization, sensory marketing and initiatives aimed at

increasing the shopping experience and bringing comfort to the consumers’

shopping trip.

Artur Kazienko – Owner, Kazar

Kazar decided to spread its wings internationally due to the limitation of

available premium shopping malls on the Polish market. Consequently, we are

now successfully running franchise stores In Romania, Hungary and UAE. After

much market research, and due to well-established cooperation with landlords

who are successfully running CEE projects, we are a trendsetter which is fi ll-

ing a niche market with regard to quality, styles and price. Markets we have

decided to focus on are Germany, Austria, the Czech Republic, Slovakia, and

the Baltic States, where our fi rst store will open in the Riga Alfa Mall this No-

vember. Further, the fi rst Kazar cooperative store in the UK will open in March

2016 in Westfi eld. Currently we are in negotiations with a strong retail group

from Ukraine, as all through the current situation the purchasing power in our

operating sector is growing.

Arpad Torok – CEO, Trigranit

The CEE retail sector has witnessed relatively calm months in 2015 with only

a few new developments, and the projects in the pipeline predict a similarly

quiet period over the next months. Only three shopping centres opened up

so far in 2015 in the secondary Polish cities adding 81,300 sqm GLA to the pol-

ish retail stock. Apart from these new developments, the extension of three

shopping centres and the refurbishment of one other centre was carried out in

Poland, while no new openings happened in Hungary or in the Czech Republic.

Also in Slovakia the fi rst opening took place in October with the opening of

the Forum Poprad Shopping Centre in Poprad. The presence and activity of

private equity funds brings forward the market with buying retail assets, like the

sale of MOM Park Shopping Centre and Offi ce Park or the Focus Park in Rybnik.

Although Warsaw had no shopping centre development this year, in the next

2-3 years signifi cant growth is expected in modern shopping centre schemes.

Retail Guide 2015 7

8 Retail Guide 2015

Regional Investment

CEE investment acti vity is on track for a record level in 2015

Gary J. Morrell

Growing investor interest in CEE retail

The CEE investment market is on the

up with a huge amount of money

looking for a home. This is particularly

benefi ting the retail sector with CBRE

recording a 99 percent increase on

2014 with €2,153 million in deals as of

the end of the third quarter. However,

these fi gures can be misleading as retail

investment tends to grab the headlines,

often due to the large lots sizes and

some analysts argue that appetite for

retail assets is not signifi cantly higher

than other commercial sectors. Further,

there is a limited supply of available

retail product as investors tend to

hold on to their assets, and this acts as

a barrier to market liquidity.

T he largest single transaction in the

fi rst half year in CEE was the pur-

chase of the Palladium shopping

centre in Prague by Union Invest from Han-

nover Leasing for €570 million. Palladium

opened in 2014 and consists of 40,000 sqm

of retail and 19,000 sqm of offi ce stock.

The development is a landmark building

that was built onto the façade of a former

military barracks in central Prague. A loan

facility for the transaction was provided by

Bayern LB and Helaba banks.

“With several large deals that originated

in 2013 closing in the next few months and

further assets coming to the market later

this year we currently register over €1 bil-

lion of shopping centre investments for

2015,” commented Katarina Brydone, As-

sociate Director of Capital Markets at CBRE

in the Czech Republic, who advised Union

Investment on the deal.

In another deal that refl ects the strong

investor demand for shopping centres

with a strong track record, Atrium Euro-

pean Real Estate acquired a 75 percent

interest in the 38,000 sqm Arkady Pankrac

shopping centre in Prague from Unibail/

Rodamco for around €168 million. The cen-

tre was completed in 2008.

Following these transactions the Czech

Republic currently leads in terms of invest-

ment volume with 43 percent of CEE as

a whole, followed by Poland with 28 per-

cent, Romania with 11 percent, Hungary

10 Retail Guide 2015

with 10 percent, Slovakia with 2 percent,

and the SEE countries recording a 6 per-

cent share, according to JLL.

JLL predict that CEE investment activity

is on track for a record level of investment

activity in 2015. “With the fi nal quarter of

the year often representing one of the bus-

iest periods for our investment teams, and

looking at the pipeline of deals that are in

advanced stages, we predict that the CEE

regional volume could reach the €8 billion

mark by the year end. Should the latter

happen, it would put 2015 at the highest

level since the economic downturn and

third highest in the past 12 years,” said

Kevin Turpin, Head of CEE Research at JLL.

To date retail investment volume stands

at around €661 million for Poland, which is

Atrium purchased a 75 percent interest in Arkady Pankrac

Regional Investment

already surpassing fi gures for 2014, when

total retail investment volume was €570

million, according to JLL. There are also

several retail investment transactions at

advanced stages of negotiation, which indi-

cates that the record €1,307 billion recorded

in retail investment volume for 2013 could

be surpassed. The latest deal is the purchase

of Centrum Riviera in Gdynia by Union In-

vestment for around €300 million. Poland

benefi ts from its sizeable supply of retail

assets in the several major secondary cities.

With prime retail yields at an estimated

7 percent for Hungary and 7.75 percent

for Romania these markets provide a pre-

mium on Prague and Warsaw with yields of

5.25 and 5.50 respectively.

In one of the biggest transactions in

Hungary in recent years a group of inves-

tors led by Morgan Stanley Real Estate in

partnership with the Hungarian developer

and investor, WING and the Austrian retail

manager and investor, CC Real purchased

a Budapest portfolio consisting of the

31,500 sqm MOM Park shopping centre

and the adjacent 19,000 sqm offi ce build-

ing in Buda, and two additional offi ce cen-

tres from a fund managed by AEW Europe.

“The Morgan Stanley/AEW deal will

open investors’ minds to Hungary once

MOM Park in Budapest, bought by Morgan Stanley lead group of investors

again. While the occupational fundamentals have been there

for a while, investors have struggled to answer the question

as to who to exit to. However, the weight of a player such as

Morgan Stanley will surely open eyes to what the market has

to off er,” said Mike Edwards, Head of Capital Markets Markets

Hungary and CEE Valuation at Cushman & Wakefi eld, who ad-

vised the purchasers on the deal.

The transaction is the largest retail sale in Hungary since the

50 percent disposal of the Allee shopping center in Budapest

for around €100 million. However, the question remains as to

what further retail assets could become available as owners

of the six best performing shopping centres are holding onto

their assets, and the three major pipeline projects are currently

on-hold.

The investment market in Romania has been dominated by

NEPI and Globalworth Real Estate in recent years, who have

been prolifi c investors and developers. In what has been de-

scribed as “the largest ever transaction in Bucharest of a single

asset” NEPI purchased the 38,000 sqm Promenada Mall from

Raiff eisen Evolution (RE) for €148 million. The latest delivery in

Bucharest is the fully let 70,000 sqm Mega Mall by the Austrian

Real4you group, and NEPI has invested €165 million in the pro-

ject.

In the biggest recent transaction in Serbia, NEPI purchased

the Kragujevac Plaza from Plaza Centres for a reported €38.5

million. Nemanja Savcic, Country Manager at NEPI Serbia, de-

scribes the strategy of the investor as to enter the market in

major and secondary cities through the acquisition of retail

assets. “If there are no existing opportunities then we will fi nd

suitable locations and develop our own centres. There are no

obvious exit strategies and we are here for the long term,” he

said.

In Belgrade there is only 100,000 sqm of traditional shop-

ping centre space in a city of 1.65 million people and if one of

the three major shopping centres becomes available it would

be snapped up by investors with the yield premium and from

a demand perspective there are waiting lists in existing centres

as retailers are waiting to enter the market.

Mike Edwards – Head of Capital

Markets, Hungary & CEE Valuation,

Cushman & Wakefi eld

Investors are willing to spend mon-

ey in Hungary and in the Morgan

Stanley/AEG deal Morgan Stanley

brought in WING and CC Real as

experienced retail centre operators.

The challenge for Hungary is the lack

of strong sustainable shopping cen-

tres in regional cities as is the case

for Poland. Retail fundamentals are

improving in Hungary but there is

a lack of liquidity after two of the six major centres have been traded

over the past two years, although we have had a lot of approaches

for retail from investors. There is currently a high interest in CEE retail

and this is not limited to specialist retail investors.

The best place for your business!Come to Christmasworld and meet international innovation

drivers for large-scale and contract decorations. Here you’ll find industry specialists with optimal concept lighting

systems tailored to your requirements. Be inspired by the

best the market has to offer at this global stage for festive

decorations.

Order your tickets now: christmasworld.messefrankfurt.com/tickets

Seasonal Decoration at its best 29. 1 – 2. 2. 2016

Founded by industry specialists, ibc are a modern, forward-thinking software

consultancy, focused on helping clients improve the use of information

technology to meet their real estate management needs.

Real Estate Technology and Professional Services include:

Energy Management, Metering and Certifi cation

Lease, Property and Asset Management

Facilities Management, Room/Space Booking and Utilisation

Energy Management and BREEAM/BREEAM-in-Use Assessments

Process Engineering and Solution Architecture

Software Implementation and Data Migration

Business Intelligence, and more...

Visit www.ibc-eu.com or contact our international offi ces today to learn more.

UK & South Africa

John Collison

+44 (0)7711 305 776

Essential Business Tools for

the Real Estate Fast Lane

© Copyright International Business Contracts Ltd. 2015 - Registered Company No.: 6672180

Cental Eastern Europe

Martin Earl

+48 (0)502 052 958

Middle East

Marcel Ros

+971 50 26 91 995

14 Retail Guide 2015

SEE Overview

Turkish fashion brands expanding across South Eastern Europe

S outh East Europe (SEE) has always

been an important bridge in trade

between East and West and in recent

years we have seen a rise in international

brands expanding in the region from both

sides of the continent.

In 2015 Retail SEE Group published on

its business portal retailsee.com over 1,000

news articles on the expansion of interna-

tional brands across the SEE region, and we

can see that Western high street fashion

retailers that have established themselves

in the market are now facing rising com-

petition from the expansion of high street

fashion brands from Turkey.

Turkey has already positioned itself as

one of the leading clothing manufacturers

in the world. By combining the nations tex-

tile production skills with Western fashion

design, well planned marketing strategies

and competitive pricing policies Turkish

fashion brands are on the rise towards

global fashion retail expansion.

According to company statements of

several Turkish fashion brands that have

been actively expanding in South East Eu-

rope, the SEE region presents a strategic

starting point for their further expansion

into Western Europe.

Looking back on the main news head-

lines here is a selection of Retail SEE Group’s

top fi ve Turkish fashion brands that are on

the rise in the SEE region:

LC WAIKIKI

LC Waikiki, one of the fastest growing

Turkish fashion retailers, has pinpointed

the SEE region as their “Gateway to West-

ern Europe”.

In August 2015 they enhanced their

strong presence in the region by entering

the Serbian market with their fi rst store

opening in Belgrade. According to com-

pany representatives, LC Waikiki intends to

pursue further expansion in Belgrade and

nationwide next year. Serbia is an addition

to their existing retail network in the SEE

region, which includes Albania, Bosnia and

Herzegovina, Bulgaria, Macedonia, Kosovo

and Romania.

The brand was established in 1985 and

today operates approximately 540 stores

across 25 countries. Developed under the

motto “everybody deserves to dress well”,

the brand off ers modern, good quality and

competitively priced clothing, shoes, bags

and accessories for all family members of

all ages within stores above 1,000 sqm in

size.

Over the next eight years the retailer has

announced that they aim to reach a total

of 1,500 stores, seeking to become one of

Europe’s top three clothing retailers.

KOTON

Koton, one of the leading Turkish fash-

ion retailers, has recently expanded its

retail presence in SEE by opening its fi rst

store in Croatia, located within the newly

developed Mall of Split.

Established in 1988 in Istanbul, Koton

has more than 377 stores in 25 countries

worldwide. Within the South East Europe

region, Koton currently operates stores

in Albania, Bosnia and Herzegovina, Bul-

garia, Kosovo, Macedonia, Romania and

Serbia.

Its stores in the region range between

1,200 to 2,000 sqm, positioned on main pe-

destrian high streets and in modern shop-

ping centres. The brand off ers a wide range

of fashion apparel, footwear, bags and ac-

cessories for men, women, teenagers and

children at an aff ordable prices. The chain

is known for its good quality, modern and

reasonably priced garments, which refl ect

the latest fashion trends.

Contributed by

Nevena Kostic

Director,

Retail SEE Group

The typical retail store size ranges be-

tween 80 to 220 sqm, and the company

expands directly and through franchise

partners. Established in 2005, Jeordie’s also

has four stores in Turkey and one store in

Kazakhstan, with future plans to continue

expanding on a global scale.

COLIN’S

Colin’s, a Turkish fashion retailer owned

by Eroglu Holding, has been actively ex-

panding on the Romanian market this

year, opening new stores and announcing

plans to reach 25 units in the country by

2016. Within the SEE region, Colin’s is also

present in Albania, Bulgaria, Serbia and is

seeking to enter Bosnia and Herzegovina,

Croatia, Montenegro and Slovenia both di-

rectly and through franchise partners.

The label’s core product range is den-

im, while the accompanying assortment

consists of fashion apparel, bags and ac-

cessories for both men and women. The

company produces high quality, innova-

tive, modern and aff ordable garments, tar-

geting consumers aged 18 to 28. The store

sizes range between 250 and 400 sqm,

while primary locations of interest include

shopping malls, outlet centres and retail

parks in major cities.

Colin’s is a fast growing fashion brand

established in 1983 in Istanbul and today

has more than 600 stores in 38 countries

worldwide.

SEE Overview

Ingo Nissen – Managing Director,

Sonae Sierra Romania

In Romania, where we are focused in the

region, recent outlooks refl ect a rising trend

on overall consumption. This increase in

business volume is also accompanied by

increased desire for more leisure and new

experiences, which become dominant in

purchase decision making. So when think-

ing of tomorrow’s shopping centre we see

a development towards an integrated shop-

ping and leisure experience rather than just

purchasing. This evolution emerges from

new consumer desires, representing a set of

opportunities that fuel new shop and leisure

off ers. This change turns the shopping centre

into a “social venue”, where visitors purchase

goods, services, leisure, but above all of them:

a priceless social experience. So we head to a

shift from the simple physical purchase into

a comprehensive integration of the physical,

digital and enjoyable moment when off ering

shopping experiences.

TUDORS

Tudors, men’s shirts and accessories

brand, owned by the Turkish company

Ayaydin Tekstil Turz. Tic. Ltd, signed a re-

gional partnership in mid 2014 with Ser-

bian retail company BJN d.o.o to expand

the brand in Serbia, Montenegro, Romania,

Bulgaria, Croatia, Slovenia, Hungary, Slova-

kia and the Czech Republic.

In 2015, BJN has been actively expand-

ing the Tudors retail network to six stores

in Serbia and two stores in Montenegro,

while seeking new locations and franchise

partners for the brand in the before men-

tioned countries.

The average size of its stores is about 50

sqm, which are located on main pedestrian

high streets and within modern shopping

centres. The brand off ers modern, well-

tailored shirts, t-shirts, knitwear as well as

complementary accessories such as ties,

cuffl inks, bow-ties and belts, catering to

men of all ages and occupational groups.

According to company representatives,

its competitive advantage lies in its quality

of products manufactured in Turkey, prod-

uct design that follows the latest fashion

trends and aff ordable pricing policy with

an average price of €16 per item.

Tudors was established in 2011 and to-

day has 145 stores in Turkey and 20 stores

in Germany, Poland, Iraq, the United Arab

Emirates, Macedonia, Serbia, Romania,

Bosnia and Herzegovina.

In the past two years alone Tudors has

opened 80 stores with a mission to con-

tinue its rapid international expansion in

order to become in the near future the

number one retail brand of men’s shirts

worldwide.

JEORDIE’S

Jeordie’s, a men’s fashion brand owned

by Meba Textile from Istanbul, has been ex-

panding in the SEE region since 2011. To-

day the company operates 9 stores in Croa-

tia and 8 stores in Bosnia and Herzegovina,

whilst it is preparing to enter Romania, Ser-

bia and the Czech Republic next year.

The brand off ers modern formal and

casual fashion, accessories and perfumes

for men of an age group between 16 and

above. According to company representa-

tives, their competitive advantage lies in

their designs that follow the latest men’s

fashion trends, quality of materials and af-

fordable pricing policy.

Retail Guide 2015 15

16 Retail Guide 2015

Regional Briefs

ICSC’s Baltic States Annual Conference places retail “At the Heart of the Communities”

M ore than 150 retail real estate

professionals converged in Tal-

linn, Estonia for the 9th ICSC

Baltic States Retail Real Estate Annual

Conference. The conference theme “Des-

tination Retail: At the Heart of the Com-

munity” attracted local and international

expert speakers who discussed the current

economic outlook for the region as well as

how shopping centres are at the heart of

investment, city regeneration, the commu-

nity and most importantly in the hearts of

consumers. Andrew Phipps, EMEA Head of

Retail Research, at CBRE shared his insight

into the expansion potential of food & bev-

erage in shopping centres and explored

how shoppers interact with food & bev-

erage in diff erent retail formats before in-

troducing a panel discussion with Valerija

Lieje, Partner at Behrens M&A Internation-

Jonathan Hallett – CEE Region Leader,

Cushman & Wakefi eld

The top retail schemes are still miss-

ing some brands that can be seen

in Western Europe, especially in the

gastronomy, premium food and af-

fordable luxury segments. However,

in terms of the overall quality of the

retail experience, the region’s shop-

ping centres are not far behind their

Western European counterparts.

Western Europe has much more development in niche markets

such as transport retail or large theme park style shopping cen-

tres. However, CEE is catching up very quickly and is now subject

to similar trends as Western Europe. Poland, with large but less

affl uent cities, has a diff erent landscape to the Czech Republic

with less high streets, fewer retail parks and retail boxes, although

it has around the same saturation of shopping centres. Hungary

has a much lower shopping centre stock, mostly due to the more

diffi cult macro-economic environment and thanks to the Buda-

pest eff ect.

Dominika Jedrak – Director,

Research and Consultancy Services

Shopping centres in the Czech Republic and in Hun-

gary are similar to Polish ones. There are traditional

shopping centres as well as specialized schemes, retail

parks and mix-use schemes, which connect retail, of-

fi ce and hotel features. Apart from local retail chains,

there are also the same brands as in Poland. Then best

examples are: Zara, H&M, Deichman, Marks&Spencer

and Sephora. The main diff erence between shopping

centres in Warsaw and in Budapest is their localization.

In the capital of Hungary, due to the lack of vacant land, the retail schemes are

located mainly on the outskirts of the city. In Prague, shopping centres are slightly

smaller than in Warsaw, the maximum number of tenants slightly exceeds 200.

Their off er (fashion, shoes and accessories) is no diff erent than in Polish cities but

entertainment & leisure sector is better developed. Apart from cinemas and fi tness

clubs, there are also ice rinks, swimming pools, spa & wellness centres as well as

children day care. What is interesting, in some Prague shopping centres, the super-

market anchor off er is very well developed. Apart from typical shopping centres in

Prague, there are also projects with a luxury off er located mainly in the city centre.

Compared with Poland, retail parks are far more popular in the Czech Republic.

al, Normunds Labrencis, Country Manager

- Latvia at SIA Forum Cinemas and Vladimir

Janevski, General Manager Baltics at Pre-

mier Restaurants Latvia SIA (DL for McDon-

ald’s Baltics) who analysed the F&B and

entertainment sectors in the Baltics. The

keynote presentation, by Shannon Quilty,

CSM, Partner at Senteo and former Head of

Retail Property Management at JLL Russia,

addressed how to develop relationships

with the local communities by touching

on what is currently done and crucially,

what can be done better. She insisted on

the importance of creating value, design

experience and memories for customers

to transform a rational decision into an

emotional one and a one off engagement

into a long-lasting relationship. Marije

Braam-Mesken, Senior Associate, Head of

EMEA Retail Strategy & Research at CBRE

Global Investors also presented “The New

Customer” and showed how they are in-

fl uencing and changing shopping centres‘

portfolios. “After analysing four types of

customers, we have come to the conclu-

sion that predictable patterns of consumer

spending no longer apply. Instead we see

new types of consumers in our shopping

centres that are defying their usual gender,

age and income categories,” Marije said.

Mike Morrissey, Executive Vice President of

ICSC said: “Our Baltic States Annual Confer-

ence is an important event for the region.

It’s great to see so many delegates in at-

tendance to hear from a diverse range of

speakers from across the world.”

Warehouse networkwww.raktarkereso.info

www.warehousesinfo.hu

Hungarywww.depozitinfo.ro

www.warehouseinfo.rowww.magazynyinfo.pl

www.warehouseinfo.pl

wwwww.w ofo ficerentiinfnfo.o.o.o cococ mmm wwwwww.greeenenbubuili dinginfofofofo.e.euuuu

RomaniaPoland

Now opening of

The Polish member of theFirst professional Warehouse Search Network of CEE

logistic centers / industrial parks warehouses for rent / logistic providers

In partnership with

INVESTMENTGUIDE

Volume 20, Number 1, October 2015

Central & Eastern Europe Russia - CIS

Prices:Euro zone: EUR 10.00Poland: PLN 35.00 (incl. Tax)Czech Republic: CZK 257.00Ukraine: UAH 10.00Slovakia: EUR 10.00Russia: USD 15.00United Kingdom: GBP 3.50Romania: RON 39.00USA: USD 15.00

Covering: Baltics, Belarus, Bulgaria, Croatia, Czech Republic, Hungary, Kazakhstan,Montenegro, Poland, Romania, Russia - CIS, Serbia, Slovakia and Ukraine

INTERNATIONAL MEDIA PARTNER

Interview with Ikea Russia, general director Amin Michaely.Ikea Russia is expanding the most successful chain of retail centres in Russia with over 14 shopping centres, 275 million visitors a year, 2 million sqm retail space, 3,000 stores,

with. For retailers who are in Russia already:and support. Being the largest shopping operator in Russia, we invest our money, time and expertise into creating day-out destinations and providing constantly growing footfall. We are committed to the Russian market. We have a long-term investment strategy for improving existing centres and building new shopping centres in order to remain the reliable and caring partner for retailers. “ For retailers who are not working in Russia: “If you plan to grow your business, come to Russia - the biggest country in the world with a population over 146 million people. Russia has huge potential for economic development and now is the right time to prepare your entry in order to take advantage of the growing market when the economy starts recovering. We are here to help: we offer a captivating retail environment, and deep un-derstanding of local market and international business expertise”

EXPO REAL 2015 UNDERLINES CONFIDENCE IN THE SECTOR with a record number of EuropaProperty Investment Guides, 6000+ distributed at the expo and surrounding hotels: • Interest in the European property market remains high

• 37,857 participants from 74 countries A busy three-day trade fair, a full schedule of meetings, all the real-estate decision-makers gathered together in one place, and business talks at every stand: Between October 5 and 7, 2015, EXPO REAL in Munich was once again the No. 1 meeting point for the property sector. “We already knew that sentiment was good at the moment. But what we have seen here at EXPO REAL in the feedback from the participants is fantastic,” enthused Klaus Dittrich, Chairman & CEO of Messe München. “This trade fair is the place to discuss the burning issues of the day in the property sector: themes such as affordable housing (even more topical in view of the migration situation), digitalization, demographics and changing yield expectations resulting from strong rises in purchase prices.” These points were also right at the top of the agenda for Dr. Barbara Hendricks, German Federal Minister for the Environment, Nature Conservation, Building and Nuclear Safety: “We are facing the biggest housing challenge for decades: How can we create more affordable housing in Germany? We are currently putting together an extensive package of measures to mobilize all state and private-sector options. EXPO REAL is an excellent forum for this.”

Armin Michaely, IKEA Russia

Helaba Bank section, Sunday afternoon Octoberfest

Marcin Juszczyk, Capital Park

Brian Jenkins, Multi Corporation

Romania Investment Panel

Richard Wilkinson, Erste Group Immorent

Main entrance to EXPOREAL

AFI Romania, Emma Toma, Tal Roma

Arpad Torok, Trigranit Corporation

City of Warsaw stand

Michael Sternicki, Aareal Bank Brian Patterson, White Star Real Estate

Warsaw Stand cocktails, another successful year

Robert Dobrzycki, Panattoni Europe

Craig Maguire, Cushman & Wakefi eld

Craig Smith Publisher EuropaProperty Investment Guide

Aleksandar Opsenica, REBECS

Philip Dunne, Prologis Europe Aleksandra Dawidczyk, Sharman ChurchJason Sharman, CEO, Sharman Church

James Turner, Balmain AM

Anna Wiosna, Hochtief Polska

Pawel Kuglarz, Wolf Theiss

P3 annual stand cocktails and once again with over 100 VIP guests attending from the CEE region

George Mula, Integrated Finance Group Petr Suchanek, Hard Rock Hotels

Aleksandra Dawidczyk, Sharman Church

Jason Sharman, CEO, Sharman Church

Jeroen van der Toolen, CEO, Ghelamco

Southeastern Europe investment/development panel

Peter Oberlechner, Wolf Theiss

Ciprian Glodeanu, Wolf theiss

Romania & Transylvania region are attacting new investors every year - 3rd year at Expo Real

Daniel Bienias MD Poland, CBREJeroen van der Toolen CEO, Ghelamco

Czech Republic investment discussion panel

Ian Worboys, CEO, P3

Aneta Rogowicz-Gala, Cushman & Wakefi eld Tom Listowski, Cushman & Wakefi eld

Georg Blaschke, Helaba Bank

Martin Erbe, Helaba Bank

Thomas Staats Deutsche HypoRobert Bodzenta, Inter-BUD

Mark Richards, MACE Group

Martin Sabelko, CBRE Global Investors

Mo Barzegar, CEO, Logicor

Thomas Staats, Deutsche Hypo

Beata Latoszek, Deutsche Hypo

Charles Kingston, Publisher REFIRE

Artur Tomczyk, CEO Poland, SPIE Peter Michael Perwas, Gateway Capital Partners

Maja Biesiekierska, Prelios Real Estate Advisors

Andrea Boeri, Prelios Real Estate Advisors

Patrick Delcol, BNP Paribas

Piotr Gozdziewicz BNP Paribas

Marcel Sedlak, HB Reavis Group

ICSC Europe: Advisory board handover to new chairman

Alexander Otto, CEO, ECE to Josip Kardun, CEO, Atrium Group

Prologis - Women in Real Estate Forum

20 Retail Guide 201520 Retail Guide 2015

Professional of the Year: Bogoljub Karić on Dana Holdings and his BK Group

Ben Jones

How long has Dana Holdings been oper-

ating in Belarus and other countries?

Dana Holdings has been operating in

Europe, the Balkans, Russia, the former So-

viet Union and the Middle East countries

for over 40 years. We have completed such

high-tech projects as the main treasury of

the Central Bank in Moscow, and such stra-

tegic developments as an airport complex

with customs, a hotel and the required in-

frastructure for severe winter conditions of

-50C degrees Celsius in Anadyr, the east-

ernmost town in Russia. We have devel-

oped over 5 million sqm in total in all these

countries.

How is the Dana Mall development pro-

gressing?

To date, a number of new shopping

centres have been built in diff erent parts

of Minsk, including Dana Mall, the largest

shopping centre in the country, developed

by our company. Dana Mall is at the fi nal

stage of construction, and the opening is

planned for the beginning of next year. We

have signed agreements with a range of

international and local brands, and the oc-

cupancy rate has reached 90 percent.

How are the wider geopolitical events af-

fecting business in Belarus? What is your

outlook on the potential for Belarus to

maintain/attract increased foreign in-

vestment in the retail and construction

sectors?

Belarus is a country with an exceptional

strategic location between Eastern and

talking about the Minsk World project in

Minsk, with an area of over three million

sqm. It will attract a lot of business people

and capital, and increase foreign invest-

ment, thus making Belarus the leading

country in the economy of the region.

The Minsk World mixed-use complex in

the centre of Minsk, occupying over 400

hectares. The complex off ers residential,

commercial and offi ce space and delivers

social infrastructure and everything need-

ed within the “city-within-a-city” concept.

We have received tremendous support

from the government of Belarus for my

idea of creating the International Financial

Center based on the successful develop-

ment of the International Financial Centers

in Dubai, Hong Kong, and Singapore.

We have been successfully operating in

Belarus for seven years and have signed

agreements for the development of fi ve

million sqm. By the end of this year we’ll

have completed one million sqm. We also

have a development pipeline of construc-

tion projects internationally that extends

NEE Overview

From the humble origins of a small family workshop, Bogoljub Karić has grown his

BK Group into a multibillion-dollar corporation. With interests ranging from telecoms

and media, through banking and fi nance to engineering and construction, the group

is active right across the Central and Eastern Europe markets. Dana Holdings has

completed more than 1,000 real estate projects across the CEE region developing

more than fi ve million sqm of commercial space and employing over 30,000 people.

Western Europe. It’s situated at the cross-

roads of all important trade routes from

Europe to Russia and off ers excellent op-

portunities in this respect. In addition, it is

easy to do business in Belarus and its abso-

lutely safe. Belarus has great potential for

attracting foreign investment, where there

are signifi cant tax incentives for investors.

Belarus has a strategic location between

East and West and is a founder member of

the Eurasian Union. Belarus is a member

of this free economic zone and the market

of Belarus extends to the markets of Rus-

sia, Kazakhstan and Armenia with a total

population of 484 million people. Ac-

cording to statistics from the World Bank,

released last week, Doing Business 2016,

Belarus ranks as the 44th best country in

the world to do business, which is an im-

provement from 57th last year. Belarus also

boasts a highly qualifi ed workforce and is

one of the safest counties in the world. In

the sphere of offi ce and retail real estate

Belarus has huge potential for the devel-

opment of new shopping centres and at-

tracting international brands.

Professional of the Year is one of the many

awards you have received. What is the

achievement you are most proud of so far?

Last year this international award was

given to the CEO of Amazon Europe, this

year the panel has chosen me, which is an

honour and highly appreciated. As for the

biggest achievement this year, we signed

an investment agreement for the develop-

ment of the largest project in Europe. I’m

Bogoljub Karić

Minsk City

NEE Overview

Retail Guide 2015 21

to 9 million sqm. This places our group as

one of the largest developers in Europe.

What are Dana’s longer-term delivery

plans?

As for our plans, we are focusing on the

“city-within-a-city” concept having its own

infrastructure and everything required for

living, working, leisure and entertainment

in one place. We are planning to implement

a similar project of over two million sqm

called Tesla City in Belgrade. We are also go-

ing to develop the Venice mixed-use com-

plex of over the million sqm in Moscow,

which is part of our development pipeline.

What about new developments? Will

there be more space coming online in

2016 than in 2015? What kind of stand-

ard might we be talking about here?

Could you give me any examples of a new

retail project?

This month we have launched the fi rst

stage of the Minsk World complex, so a 40

percent construction increase is planned

for our company in 2016. As part of the

Minsk World complex, which I have just

mentioned, we are planning to build

a large shopping centre and leisure centre,

which is a regional category killer and will

generate huge interest from international

brands. We are also planning to build busi-

ness-class real estate with over 400 villas in

the diplomatic quarter.

Apart from Belarus and construction,

what are the key emerging markets and

sectors for Dana Holdings and or BK

Group?

Besides Belarus and the construction

sector, our group of companies – BK Group

– covers the trade sector, telecommunica-

tions and electronic media, banking and

fi nance, the mass media (TV, radio, press

and online media), science and education

(BK University in Moscow and Belgrade –

the fi rst private universities), and charity

work (BK Foundation). We also founded

the fi rst non-governmental Association of

Manufacturers and Entrepreneurs in the

former Yugoslavia, which currently has

tens of thousands of members from all Bal-

kan countries.

What proportion of the wider BK Group

portfolio is accounted for by real estate

interests generally and Dana in particu-

lar? Is this likely to change in the future?

To date, our main activity is related to

the construction sector, especially in the

former Soviet Union countries. Our ac-

tivities in the Balkans are more varied, for

example, our company launched the fi rst

mobile telecommunications in the Bal-

kans, as well as the fi rst private TV broad-

cast and the university. However, our core

business will always remain in the con-

struction sector.

What synergies and effi ciencies are pos-

sible between Dana Holdings and the

wider activities of BK Group?

A wider range of activities and risk diver-

sifi cation can only be useful for the compa-

ny in general. For example, students of our

universities in Moscow and Belgrade are

provided with practical training, and the

best students are employed by our com-

panies. We have earned public recognition

and trust thanks to our charitable and me-

dia activities in the Balkans.

Civil society and social engagement,

through initiatives like the BK Founda-

tion and BK University, are important as-

pects of the group’s activities…

Of course, my daughter Danica personally

heads the BK Foundation, which helps pri-

marily children and refugees, provides edu-

cational grants to talented students and pro-

motes cultural values by handing out awards

to outstanding international scientists. BK

Universities in Moscow and Belgrade enrols

hundreds of students every year and a lot of

them are now successful, well-known and

leading sportspeople, managers, and pro-

fessors. Our DNA is comes from our desire

to build, enhance and improve, not only in

construction, but also in the social, cultural

and professional spheres. We are proud that

our foundation has touched and bettered

the lives of people all around the globe, and

continue to do so every day.

22 Retail Guide 2015

NEE Overview

Palazzo Mall

Demanding market dynamicscreating survival of the fi ttest mentality

Yuri Drazdow

An increase in the number of new retail

projects arriving on the commercial

estate market as well as economic

problems in Belarus owing to the

instability in neighbouring Russia and

Ukraine means that many developers

should re-evaluate their expectations.

Demand for high quality retail is still

growing, but clients now have many

more options to choose from.

“The ongoing trend of prices

dropping in all areas of com-

mercial real estate will con-

tinue, but well-planned and designed

projects still have a great chance of suc-

cess, and could generate a healthy profi t,”

commented Denis Chetverikov, Director

of Research and Advisory Department of

Colliers International in Minsk.

Retail rates fell by 20-25 percent with

increased vacancy. As a result, tenants

have the opportunity to rent a better area,

which previously they could only dream of.

The fortunate are those property owners

that have managed to build a stable cus-

tomer base and retained their existing cus-

tomers even in the current economic crisis.

One of the most crucial characteristics of

a development is that is based in a good

location. If the location is good then the

chances of generating business is also very

high. It is all about the “location, location,

location”.

“As an example, we can talk about

a third generation shopping centre Crown

on Kalvaryiskaya Street or the modern

shopping centre The Castle. Vacancy is ex-

tremely low, and rates remain high. How-

ever, many of the popular brands in those

centres are operated by the owners them-

selves. There are also examples where

developers do not attract the popular

brands, but the objects are still successful.

For example, the shopping centre Galileo

where at least periodically and observed

rotation of tenants, customers are always

off ered some new items. The shopping

centre Magnet on Dzerzhinsky Avenue,

which opened at the peak of the crisis in

the fi rst months of work fi lled with tenants

24 Retail Guide 2015

On the subject of foreign brands that

opened or are in the midst of expansions,

experts note the opening of a Sony Cen-

tre, a new sporting goods supermarket

network, Sportsmaster, Ralf Ringer, O’STIN

and Galamart, as well the geographical

expansion of the major clothing store LC

Waikiki and the expansion of the cinema

operator Silver Screen.

The most vibrant market in Minsk’s retail

segment is fast food. This market is growing

both by number of outlets as well as new

brands on the market. In recent months

Burger King opened its fi rst store in Minsk

followed by Baskin Robbins in Vitebsk. KFC

restaurants are about to start operations

in autumn. The current leader McDonalds

has increased its number of restaurants in

Minsk and plans to open new outlets in the

various regions around Belarus.

Classic catering has also been develop-

ing quite steadily. Various high end restau-

rants have opened such as The View locat-

ed on the 28th fl oor of the business centre

Royal Plaza. Coff eeshop Revolution has

fi nally come to Minsk, and as it happens

within the last six months Minsk has seen

the opening of ten new coff ee shop outlets

for coff ee lovers, and there are a few more

that are in the process of opening.

“I would like to refute the statements

that cafes and restaurants are being sold

out in large quantities in Minsk. The num-

ber of venues on off er has increased in-

deed. The catering market in particular

has grown signifi cantly over the last two

years. Therefore, the percentage of sales

has also increased as well,” a market expert

concluded.

NEE Overview

A good locati on is crucial

Developers of shopping centres are having a hard ti me

for more than 90 percent,” Denis Chetverik-

ov said.

It is expected that in the near future

Minsk’s market of large retail properties

will change signifi cantly. In the next few

months new shopping centres are to be

commissioned in Minsk, these are Gal-

lery with a gross leasable area (GLA) of

more 36,000 sqm, MOMO (GLA more than

30,000 sqm) Green City (GLA more than

40,000 sqm) and Dana Mall (GLA more

than 50,000 sqm). However, despite such

new developments potential tenants are

reluctant to step into the retail market and

current shop owners have halted their ex-

pansion plans. As a result, there could be

another round of decline in rental rates

which is due to the signifi cant excess of

supply over demand.

“Developers of shopping centres are

having a hard time. Almost all the projects

have moved into combined determination

of rental rates, in particular, the percentage

of turnover. In Belarus, at the same there

are a number of major projects for which,

even with a stable situation on the market

it would be diffi cult to fi ll vacancies and

acquire tenants. Almost all international

retailers have suspended development in

the neighbouring countries, and if they

do develop then they do it very carefully,”

noted the expert, further stating that “For

them the question of entering other mar-

kets such as Belarus is on the agenda, but

certainly not as a priority.”

Never the less, there are others who are

of a diff erent opinion. The Polish retailer

LPP SA, are one of the few companies that

are actually considering entering the retail

market at such a time. This particular group

owns fi ve diff erent brands (Reserved,

Cropp, House, Mohito and Sinsay) and they

have more than 1,500 stores, mainly in

Europe. The company’s turnover, for 2014

amounted to almost around €1.2 billion.

“Negotiations are under way with the

brands that represent the major perfume

companies, home appliances and house-

hold goods. There are intentions from

a large DIY company to also start opera-

tions in Belarus,” commented Denis Chet-

verikov, he further elaborated “It is good to

see that none of the brands already repre-

sented in Belarus have left our market.”

Furthermore, Belarusian domestic brands

are not hesitating to move forward and

are continuing to grow, utilizing the de-

preciation of rental rates. Developed and

well-known national brands such as Elam

opened a new store in the Expobel shop-

ping centre, in addition to Conte Elegant,

a textile company which opened a pilot

company store of the same name, at Gali-

leo shopping centre.

Gain exposure among21,400+ participants at MIPIM,

380+ international journalists

prestigious Awards Ceremony

ENTRY DEADLINE:27 NOVEMBER 2015

GAIN THE RECOGNITION THEY DESERVE

AT MIPIMOUSTANDING PROPERTY PROJECTS

PALAIS DES FESTIVALS

15-18 MARCH 2016CANNES, FRANCE

FOR MORE INFORMATIONCONTACT LUCIE CHEN: +33 (0)1 79 71 95 [email protected] VISIT WWW.MIPIMAWARDS.COM

26 Retail Guide 2015

NEE Overview

The recently opened Nodrika

Large scale pipeline developments mark the Baltics retail landscape

Alex Webber

The gentle upward trajectory enjoyed

by the economies of the Baltic States

has been mirrored by a lively retail

sector that continues to steadily expand.

While the number of new projects has

remained relatively modest, those that

are being implemented have proved

to be ambitious in both size and scope,

thereby mirroring a maturing market

that learned painful lessons during the

crisis years – and the news hasn’t just

manifested itself in bricks and mortar,

but also in pipeline developments that

suggest a bright future.

“The retail market has remained buoy-

ant, allowing developers to plan and

announce new large-scale develop-

ments, expansions and refurbishments

in all three Baltic capitals,” said Maksim

Golovko of Colliers International.

Just outside Tallinn, that meant the June

launch of the 15,000 sqm Viimsi Market,

the fi fth shopping centre to appear in what

has been previously described as “Estonia’s

richest parish”. And in spite of misgivings

that the Tallinn district is facing saturation,

stock continues to be added. Of the devel-

opments that have broken ground, with

a footprint of 130,000 sqm and a GLA of

52,000 sqm it is T1 that is perhaps the most

anticipated. Due for completion in Q3 of

2017, the €70 million project will include

space for 200 retail units and will play a key

role in the creation of a new “centre” for the

city – the bold plans include a tram link

running to the airport and an international

rail terminal.

This is not the only development that is

forthcoming: Capfi eld, who already own

six cen-tres in Estonia, plan to extend the

Norde and Lasnamae Centrum, while also

adding to their portfolio with the 2016

opening of the RAE Shopping Center. Set

in one of the fast-est growing residential

areas around Tallinn, and with a wider

catchment area of 400,000 people within

a 30-minute drive, the 20,000 sqm scheme

will be a major retail destination hub po-

sitioned right at the mouth of one of the

major entry points to the Estonian capital.

A similar situation is being played out

in Lithuania. “Investors have continued to

show great interest in successfully operat-

ing shopping centres, and while the supply

of new projects has not been huge, devel-

opers are starting to implement projects

on a larger scale,” said Saulius Vagonis of

Ober-Haus.

In Vilnius that has been demonstrated

by the October opening of phase one of

the Nordika Shopping Valley. The fi rst sig-

nifi cant launch in six years, the €50 mil-

lion complex will eventually tout a GLA

of 40,000 sqm once phase two is fi nished

in Q2 of 2016. Hoping to attract consum-

ers from as far afi eld as Minsk, Nordika is

expected to transform southern Vilnius,

thanks to a tenant base that includes sev-

eral new entrants to the Lithuanian retail

market.

“Nordika Shopping Valley isn’t just for lo-

cal resident, but a destination for families

from other parts of Lithuania as well as

neighbouring countries – we expect for-

eign visitors to make up a signifi cant share

of our buyers,” said Peter Gage-Morris, CEO

of the principal investor. Its completion

makes it the 25th shopping centre to open

in Vilnius, bringing the total GLA in the city

to 439,000 sqm.

Beyond Nordika, vacancy rates have

remained low in Lithuania, more so in

the popular shopping centres, leading to

a slight increase in rents, though mainly

the market has been defi ned by its stabil-

ity. If there has been a trend, it has been

the subtle shake-up of the tenant mix.

“Shopping centres have been actively

adjusting this with international and lo-

cal brands expanding in the market,” said

Dmitrijs Kacalovs of Colliers. “This expan-

sion into the retail market has mostly been

related to clothing and catering services.

For example, McDonald’s, Subway and Cili,

whilst new brands such as Samsung have

also entered the market.”

With no large shopping centres opened

outside the capital, the GLA in Lithuania’s