business tax reform: where are we now? 2-tax reform powerpoint... · active” or “passive”...

TRANSCRIPT

70th Annual University of Chicago Law School Federal Tax Conference | Nov. 3, 2017

Business Tax Reform: Where Are We Now?

0

Rosanne AltshulerDavid HaritonDavid P. Lewis

Nicholas J. DeNovio (Moderator)

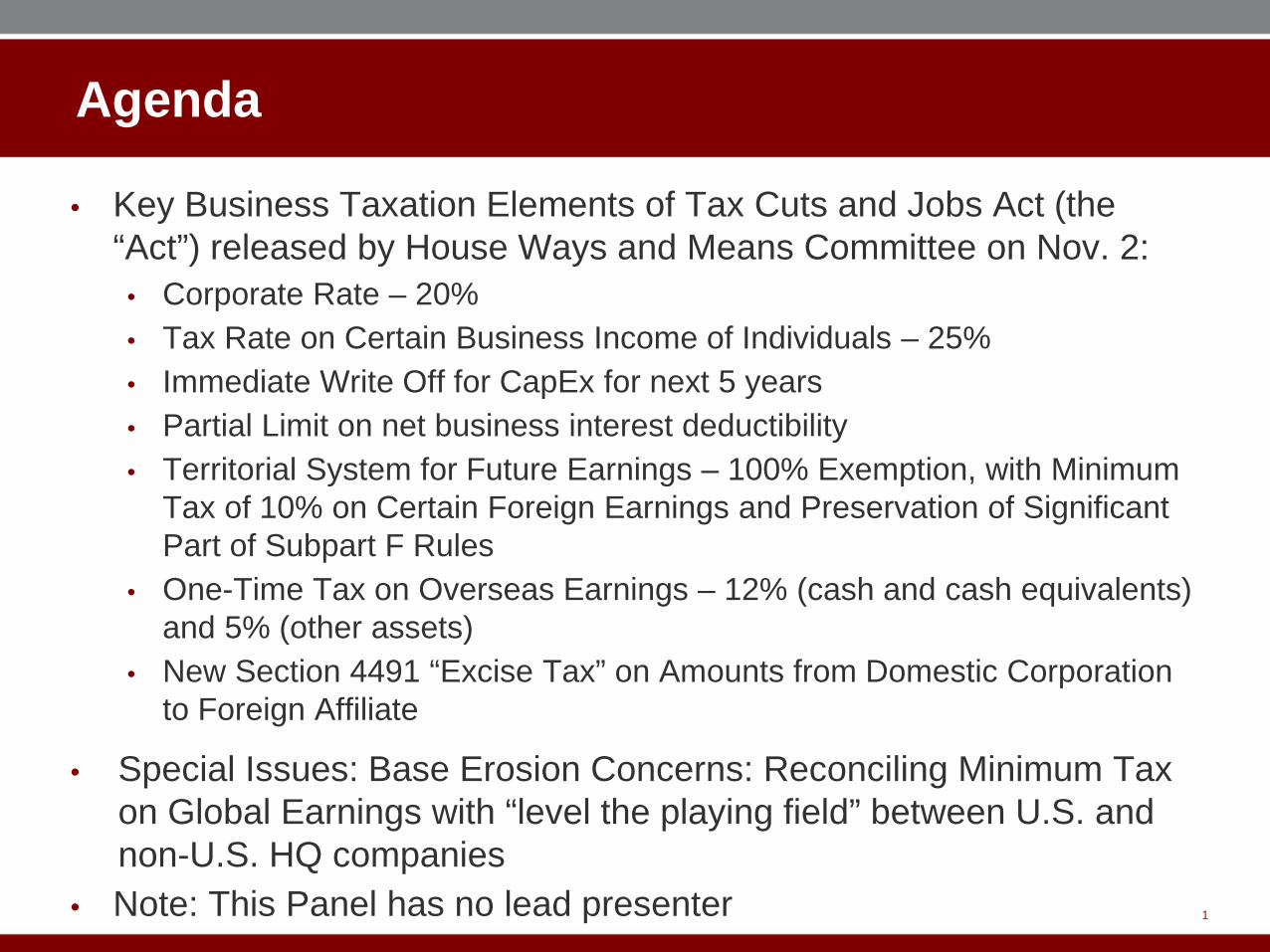

Agenda

• Key Business Taxation Elements of Tax Cuts and Jobs Act (the “Act”) released by House Ways and Means Committee on Nov. 2:

• Corporate Rate – 20%• Tax Rate on Certain Business Income of Individuals – 25%• Immediate Write Off for CapEx for next 5 years• Partial Limit on net business interest deductibility• Territorial System for Future Earnings – 100% Exemption, with Minimum

Tax of 10% on Certain Foreign Earnings and Preservation of Significant Part of Subpart F Rules

• One-Time Tax on Overseas Earnings – 12% (cash and cash equivalents) and 5% (other assets)

• New Section 4491 “Excise Tax” on Amounts from Domestic Corporation to Foreign Affiliate

• Special Issues: Base Erosion Concerns: Reconciling Minimum Tax on Global Earnings with “level the playing field” between U.S. and non-U.S. HQ companies

• Note: This Panel has no lead presenter 1

Need for Tax Reform – Is there one?

• Last major rewrite in 1986. Tinkering since then, including American Jobs Creation Act of 2004 (Sections 199, 965, 409A, etc.) and a series of “temporary extenders” (Sections 954(c)(6); 168(k))

• The drafters of IRC framework on fundamentals of taxation of worldwide income, and FTC, Subpart F, and other key underpinnings (all done either pre-FDR or in Kennedy Administration) would recognize their work in today’s IRC

• The world has changed (but the IRC has not)

• Inversion Debate was an example: Republicans and Democrats looked at same picture but viewed it very differently; companies reacting to a competitive global world? Or not paying their “fair share”

• Prior Reform Efforts: Camp I and II; Enzi; various other proposals; June 2016 House Blueprint and Trump Plan

• September 27 Big Six Framework and the November 2 Act

2

Corporate Rate

• The Act cuts rate from 35% to 20%. Change is immediate and permanent. Issues:

• How to pay for a corporate rate cut? Offsets (domestic and international); Spending cuts; deficits?

• The rate drives many of other terms of package; Revenue Neutral? By IRC Title? Reconciliation and Budget Resolution

• Compare to Blueprint (20%); Trump Plan (15%); Camp II (25%); Obama (28%)

• Average OECD Rate: 23-24%

• Another Stat: Percentage of Corporate Tax/GDP: U.S. (2.2%); OECD (2.8%)

• Debate over how burdensome U.S. tax rate of 35% actually is; Tax Foundation/Citizens for Tax Justice/Tax Policy Center

3

How to defend higher rate on individual and partnership income vs lower corporate rate?

• Should the lower corporate rate be extended to certain kinds of individual or partnership income?

• What is the rationale for such extension?• What kinds of income should get a lower rate?

• business income• investment income• service income or income from your own efforts• disguised wages and wage proxies• should partnership income be distinguished from individual

income?• The Act adds measures to prevent the recharacterization of

personal income into business income.

4

How to defend higher rate on individual and partnership income vs lower corporate rate?

• What are the practical problems with determining and policing the distinctions?• current law’s inbound “effectively connected” income

distinctions• the line between business and investment—equity and

hedge funds, carried interests, etc.• what is “reasonable compensation”? Is it some fixed

percentage of overall income? Is it all income in excess of a designated rate of return on assets invested?

• audit and enforcement

5

Maximum Rate on Business Income of Individual Owners of Pass-Through Entities

• Business income of individuals taxed at 25% rate.• Rate is applicable to passive business income and an applicable percentage

of active business income.• Applicable percentage of active business income is based on “capital

percentage” of active business income.• Generally, capital percentage is 30%, leaving 70% of the individual’s

active business income subject to ordinary individual income tax rates. • Alternatively, an individual may make a binding 5-year election to apply a

formula measuring the capital percentage based on a rate of return (Federal short-term rate plus 7%) multiplied by the business’ capital investments.

• The proportion of business income would be determined by each owner of the pass-through entity separately.

• Special rules prevent recharacterization of actual wages paid as business income.

• Active” or “passive” based on Section 469 principles.

6

Territorial System – Finally, But…

…If I were forming U.S. BigCo today I would form it in…

• What are the problems of the current U.S. International Tax System:1. Rate: 35% on Repatriation2. CFC system designed in manufacturing era, when U.S. had

50% of world GDP, the Cold War prompted concerns about investment in developing countries and U.S. multinationals derived a fraction of income from overseas.

3. The ever-shrinking FTC (see last panel) resulting in double tax.

7

Territorial System for Future Foreign Earnings

• The Act replaces worldwide tax system with a 100% exemption for dividends from foreign subsidiaries (in which the U.S. parent owns at least a 10% stake)

• Eliminates the Lockout Effect

• Section 956 disappears for US corporate shareholders

• Foreign Base Company rules appear to continue in part

• No FTC on distribution including under Section 901, but see discussion below

8

Territorial System for Future Foreign Earnings: A New Era

9

US Parent Company

ForeignSub 2

ForeignSub 1

ForeignSub 3

Credit Support for Parent Debt

Distributionsand

Loans to US Affiliates

Saleof Foreign

Sub

Buyer

Lender

Participation Exemption?

Territorial System: Base Erosion Issues

• Act imposes a minimum tax generally at 10% rate (20% corporate rate x 50% of “foreign high return amount”) of a U.S. multinational AND enacts rules to (in the Framework’s words) “level the playing field” between U.S.-headquartered parent companies and foreign-headquartered parent companies (see Section 4491 later). Opposing statements? How can they possibly be reconciled?

• Policy goal of Minimum Tax? • Revenue offset for Corporate Rate Cut? • Revenue Neutrality on International Provisions (each “Title”)?• Protection of U.S. Tax Base? Probably main reason.

• Act: Under current law, allocation of income by U.S. companies to intangible property in low-tax jurisdictions is an acute source of erosion of the U.S. tax base. The adoption of a dividend-exemption system could, without appropriate safeguards, exacerbate this incentive by allowing profits that have been shifted to be repatriated with minimal U.S. tax consequences.

10

Prior anti-base erosion minimum tax proposals

11

Proposal Chairman Camp H.R. 1 (2014) Senator Enzi S. 2091 (2012) Obama Budgets FY16/17

U.S. rate 25% 35% < 35%

Foreign dividends 95% exemption – CFC or section 902 corporation 95% exemption – CFC or electing section 902 corporation Replaced with minimum tax

Tax base • As in Option C, income of a CFC that is from intangibles and low-taxed becomes a new category of Subpart F income -- Foreign Base Company Intangible Income (“FBCII”)

• FBCII measures a CFC’s low-taxed, foreign intangible income by reference to the excess of (A) the CFC’s gross income > 10% of asset basis (the “Excess”) over (B) a percentage of Subpart F income. The percentage is the Excess/gross income.

• (AGI > 10% QBAI)→(Excess/AGI x other Subpart F income).

• New category of Subpart F income for low-taxed CFC incomemeasured as all gross income less qualified business income (“QBI”) that is in excess of minimum tax

• All low-taxed foreign earnings

Minimum tax • 15% minimum tax on foreign intangible income • Foreign ETR ≤ 50% of U.S. rate (i.e., 17.5%)

• Determined country by country (branches not addressed –remain disregarded)

• QBI is same country income, which requires either employee / officer presence, but does not include intangible income

• 19% minimum tax on foreign earnings, reduced by 85% of the per-country foreign ETR (i.e., minimum tax applies if ETR ≤ 22.4%)

• An allowance for corporate equity (“ACE”) - intended to exempt a return on actual activities abroad from the min tax

Foreign branches • No change in foreign branch income taxation • No change in foreign branch income taxation • Treated as CFC for minimum tax

U.S. incentive • 40% U.S. tax deduction against foreign intangible income earned directly by U.S. corporation or foreign corporation that is included in U.S. shareholder’s gross income as Subpart F income

• The deduction does not apply to property sold or services provided back into U.S. (prevents round tripping – where goods are sold outside the U.S. but ultimately provided to an end-user in the U.S.)

• A 50% deduction (i.e., 17.5% rate) for U.S. corporation’s qualified foreign intangible income (“QFII”): derived from the active conduct of a business in the U.S., provided the U.S. corporation developed the intangible property, or, if acquired, added substantial value to it within the U.S.

• New 20% general business credit for expenses in connection with insourcing U.S. trade or business

• No U.S. deduction for expenses in connection with outsourcing U.S. trade or business

Minimum Tax Proposal:New Code Section 951A Foreign High Return Amount

1. Foreign high returns would be measured as the excess of the U.S. parent’s foreign subsidiaries’ aggregate net income over a routine return (7 percent plus the Federal short-term rate) on the foreign subsidiaries’ aggregate adjusted bases in depreciable tangible property, adjusted downward for interest expense.

2. Treated similarly to Subpart F income. FTC limited to 80%.

12

USP

FS1

FS3 FS5 FS6

Country A Country A Country C Country C

FS2

FS4

Minimum Tax Proposals:Grubert & Altshuler: Fixing the System

1. A country-by-country minimum tax of 15 percent on active income. FTC for foreign tax rate up to the 15 percent threshold. Effective tax rates computed for income in each jurisdiction. No active business exception. Calculation based on straightforward E&P.

2. Same as 1. except calculation allows company to deduct real investment in the country from the minimum tax base. No U.S. minimum tax on the company’s normal return abroad. Only excess return is taxed.

13

USP

Dutch

EU EU EU EU

Country A Country A Country C Country D

DutchMin Tax Base Min Tax Base

Minimum Tax Proposals:Grubert & Altshuler: Fixing the System

1. An overall group (i.e., treat foreign subs as “one CFC”) minimum tax of 15 percent on active income. FTC for the effective foreign tax rate up to the 15 percent threshold. No active business exception. Calculation based on straightforward E&P.

2. Same as 1. except calculation allows company to deduct real investment in the country from the minimum tax base. No U.S. minimum tax on the company’s normal return abroad. Only excess return is taxed.

14

USP

Dutch

EU EU EU EU

Country A Country A Country C Country D

Dutch

Min Tax Base

Minimum Tax: Categories of Income

15

USP

FS1 FS2 FS3 FS4

Classic Foreign Personal Holding

Co. Income*

Foreign Base Company Sales or

Service Income

Active Non-FBC Income

(ETR is 8%)

Active Non-FBC Income

(ETR is 20%)

Which of these categories should be subject to Minimum Tax?

* Presumably subject to regular corporate tax rate as under current law.

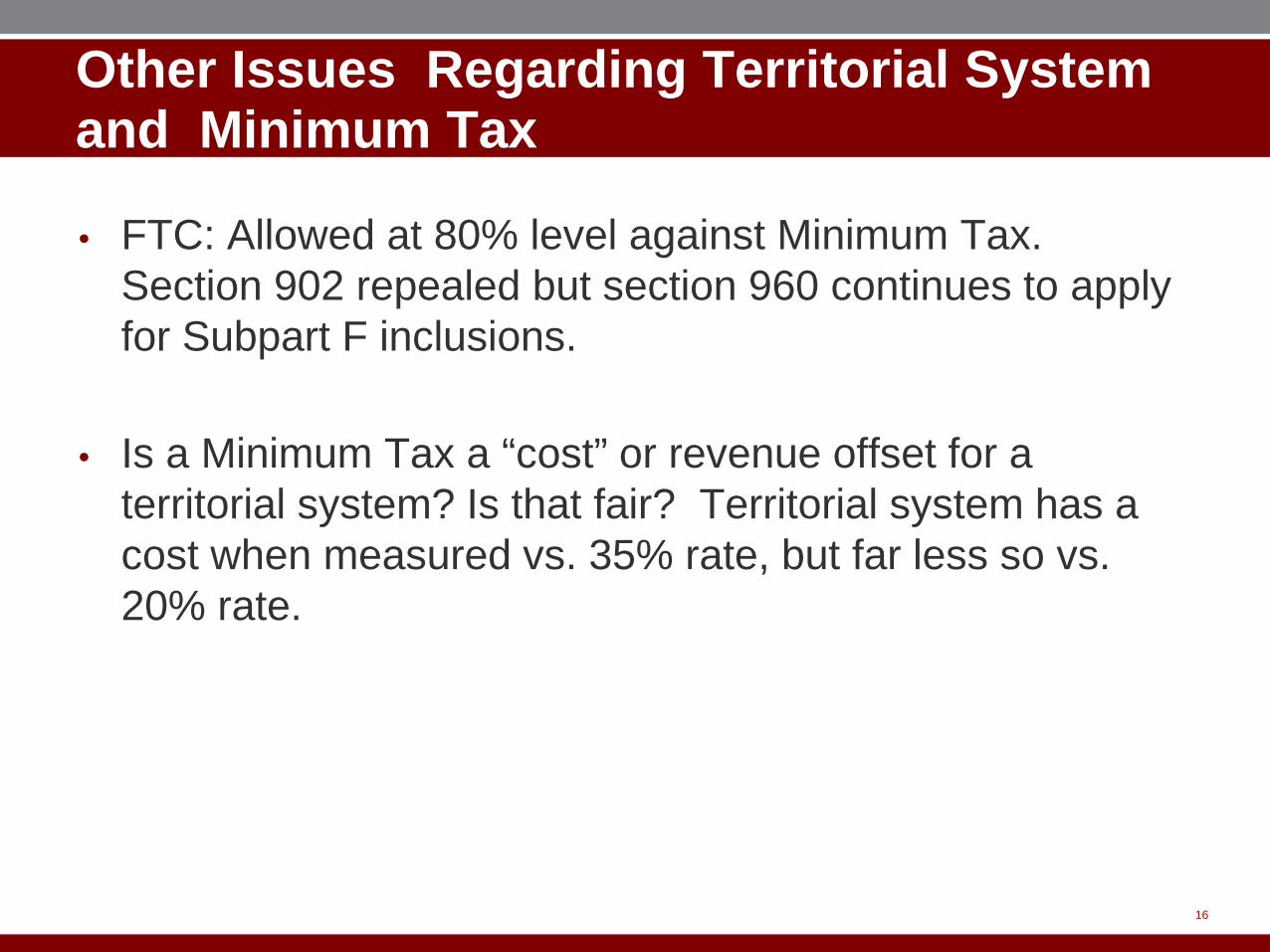

Other Issues Regarding Territorial System and Minimum Tax

• FTC: Allowed at 80% level against Minimum Tax. Section 902 repealed but section 960 continues to apply for Subpart F inclusions.

• Is a Minimum Tax a “cost” or revenue offset for a territorial system? Is that fair? Territorial system has a cost when measured vs. 35% rate, but far less so vs. 20% rate.

16

How can a Minimum Tax on Foreign Profits be Reconciled with “Level the Playing Field”

• Questions we were thinking about on November 1:• To “level the playing field” might mean tilting the field

more in favor of U.S. parented group? A repeal of things like section 956 would help. But a Minimum Tax by definition “unlevels” that field?

• Or it might mean tilting the field against Foreign parented groups with new inbound rules?

• Might they be thinking: Further limits on base erosion? Tightening 163(j)? An inbound Minimum Tax? A gross basis surtax? See Testimony from several experts before Senate Finance Committee on October 3.

• Note the EU approach on its inbound taxation of U.S. tech companies.

17

New Section 4491 Imposition of Tax on Certain Amounts from Domestic Corporations to Foreign Affiliates

18

FP

US Sub FS1Royalty Payment

Manufacturing

Assume US Sub purchases product or makes royalty payments to foreign affiliates.

20% excise tax on payments unless ECI elected

Territorial System: Base Erosion Issues

• How will other countries react to a U.S. Territorial System and an outbound Minimum Tax? Or an inbound Excise Tax?

• Will they enact new withholding taxes on repatriation back to U.S.? Since deferral no longer a likely goal for US tax planning companies may pay more frequent dividends up the ownership chain.

• Will they enact a soak up for Minimum Tax?• Is Minimum Tax a defense against State Aid claim due to

no more ‘stateless income’?• Can U.S. object to EU actions on U.S. multinationals if

U.S. imposing its own inbound Excise Tax?

19

Territorial System – What about Gains?

• Is there any kind of participation exemption on sale of CFC? Prior bills differed.

• Is there a true exemption system without a participation on sale exemption?

• Assume Company #1 captures business advantages with current profits.• Assume Company #2 reinvests revenues in R&D, brand enhancement, etc.• Both U.S. companies sell Foreign Subs. Should U.S. Company #2 pay

regular tax on gain? Is that fair given U.S. Company #1 had the tax benefits of a lower Minimum Tax on accumulated earnings?

20

US Company #1

US Company #2

Foreign sub Foreign sub

Current and accumulated profits

(historic losses)

Territorial System – What about Gains?

When a USP sells a FS, should there be a mandatory type of section 338 election? Deemed sale gain being exempt under a participation regime except the extent attributable to FPHC type property?

21

US Company #1

US Company #2

Foreign sub Foreign sub

Current and accumulated profits

(historic losses)

One Time Tax on Accumulated Overseas E&P

• Act: This is not a repatriation holiday (such as 2005), but rather a one time tax at 12% (cash and cash equivalents) and 5% (other assets) imposed on historic earnings; payable over 8 years.

• Unlocking $2.5 trillion of earnings – will it boost the economy?

22

One Time Tax on Accumulated Overseas E&P

23

USP

FS1 FS2 FS3 FS4

Deficit Positive E&P Excess Cash Third Party Debt

FS1 deficit in E&P appears to offset FS2 positive E&P in calculating tax base. If FS3 has cash or cash equivalents should it somehow

be offset by debt payable by FS4?

Expensing, Major Credits & NOLs

• Policy goal: Encourage investment

• Act: Full and immediate expensing of new investments in depreciable assets made after September 27, 2017, for at least five years; Maintain R&E Credit; envisions repeal of other credits though under review depending on budget limits; Special rules on NOLs

• Blueprint: Full and immediate expensing of tangible and IP; Maintain R&ECredit with modifications; NOL carryforward indefinite (90% limit)

• Camp II: Repeal MACRS; lengthen lives/inflation index; section 197 set at 20 years; NOLs allowed (90% limit)

24

Interest Expense

• Current Law: Gross interest expense is deductible, subject to limits where arguably disguised equity (AHYDO rules; Sections 163(L), 163(j), 385, Litton, Nestle and other classic cases)

• Policy goal? Equalize debt/equity (note Hatch approach of deduction for equity); raise revenue; prevent base erosion; does Congress see societal benefits (is debt good?)

• Framework: deduction for net interest expense (NIE) incurred by C corporations “partially limited”; Committees to consider appropriate treatment of interest paid by non-corporate taxpayers, indicating special rules for non-corporate taxpayers?

• Blueprint: Disallowed NIE deduction; with a reference to “special rules” for financial services companies

• Camp II: No broad limits; Special rules for U.S. Parented groups with CFCs

25

Interest Expense

• What is NIE? Interest equivalents on income and expense side• What are the alternatives to “partially limit” NIE?• Flat Percentage Limit on Deductible Net Interest Expense?

- [50%] of NIE deductible in any given year.- What if NOL? Carry forward of Excess NIE?

• Limit NIE based on overall Group EBITDA? Like Germany.- What of Non-U.S. EBITDA of U.S. Parented Group?

• Policy issues of each alternative?• Why is interest treated differently than, say, electric bill for

Corporate HQ? They are both expenses?• These were the questions on November 1

26

Interest Expense – New Section 163(j)

• Limited to 30% of ATI

• Excess interest expense carried forward

• Special Rules in Section 381 and 382 Transactions• Deductible net interest expense of U.S. corporation in

international group would limited to the extent the U.S. corporation’s share of the group’s global net interest expense exceeds 110% of the U.S. corporation’s share of EBITDA; limit to apply in addition to the general rules.

• Effective 2018

27

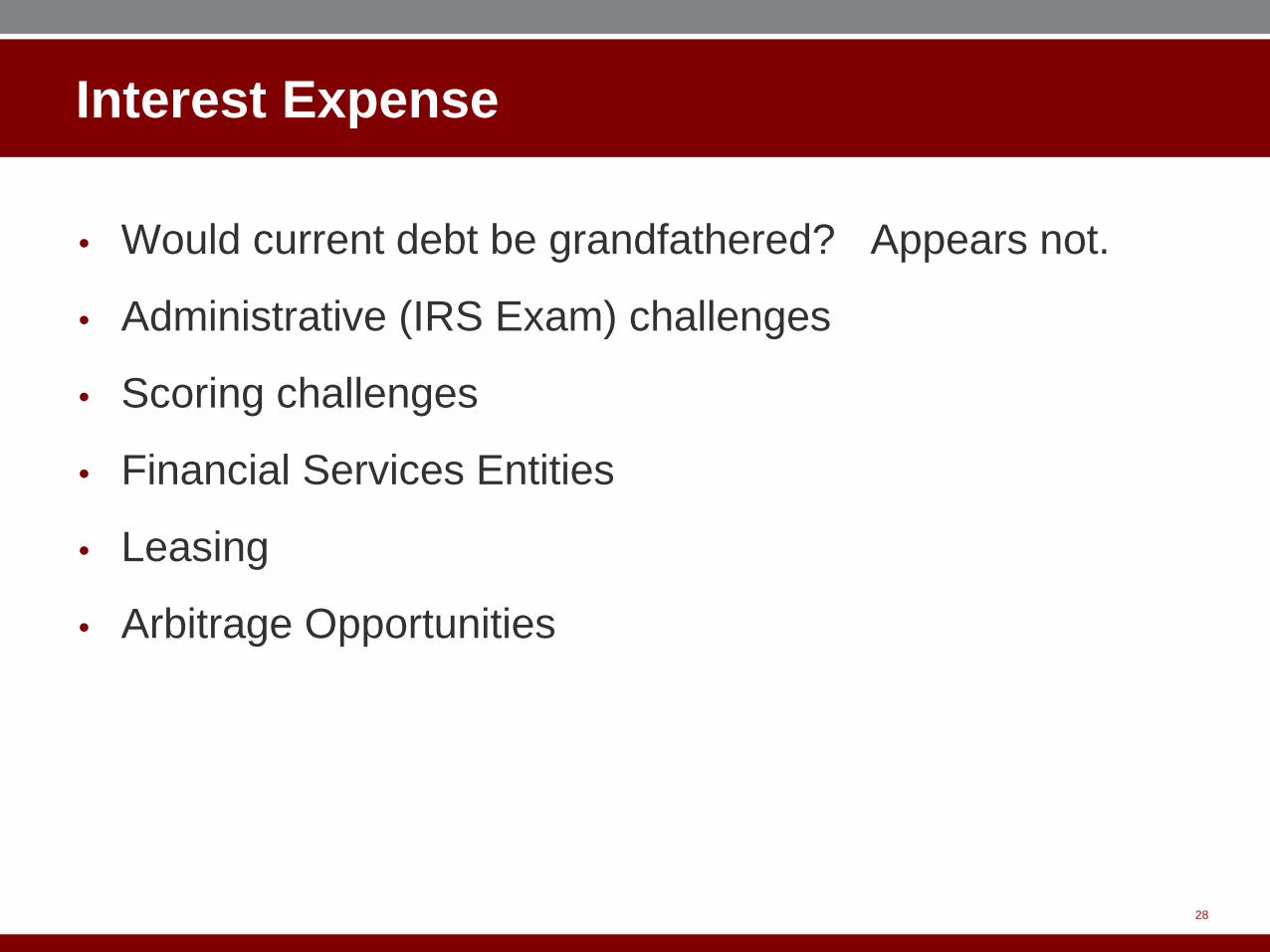

Interest Expense

• Would current debt be grandfathered? Appears not.

• Administrative (IRS Exam) challenges

• Scoring challenges

• Financial Services Entities

• Leasing

• Arbitrage Opportunities

28

Interest Expense

• For a US Parented Group, how should any limit apply taking into account principles such as those embedded in Allocation/Appointment rules of Section 861?

29

Subpart F Income and Foreign High Return Amount Appear to be Included in

EBITDAUSP

FS

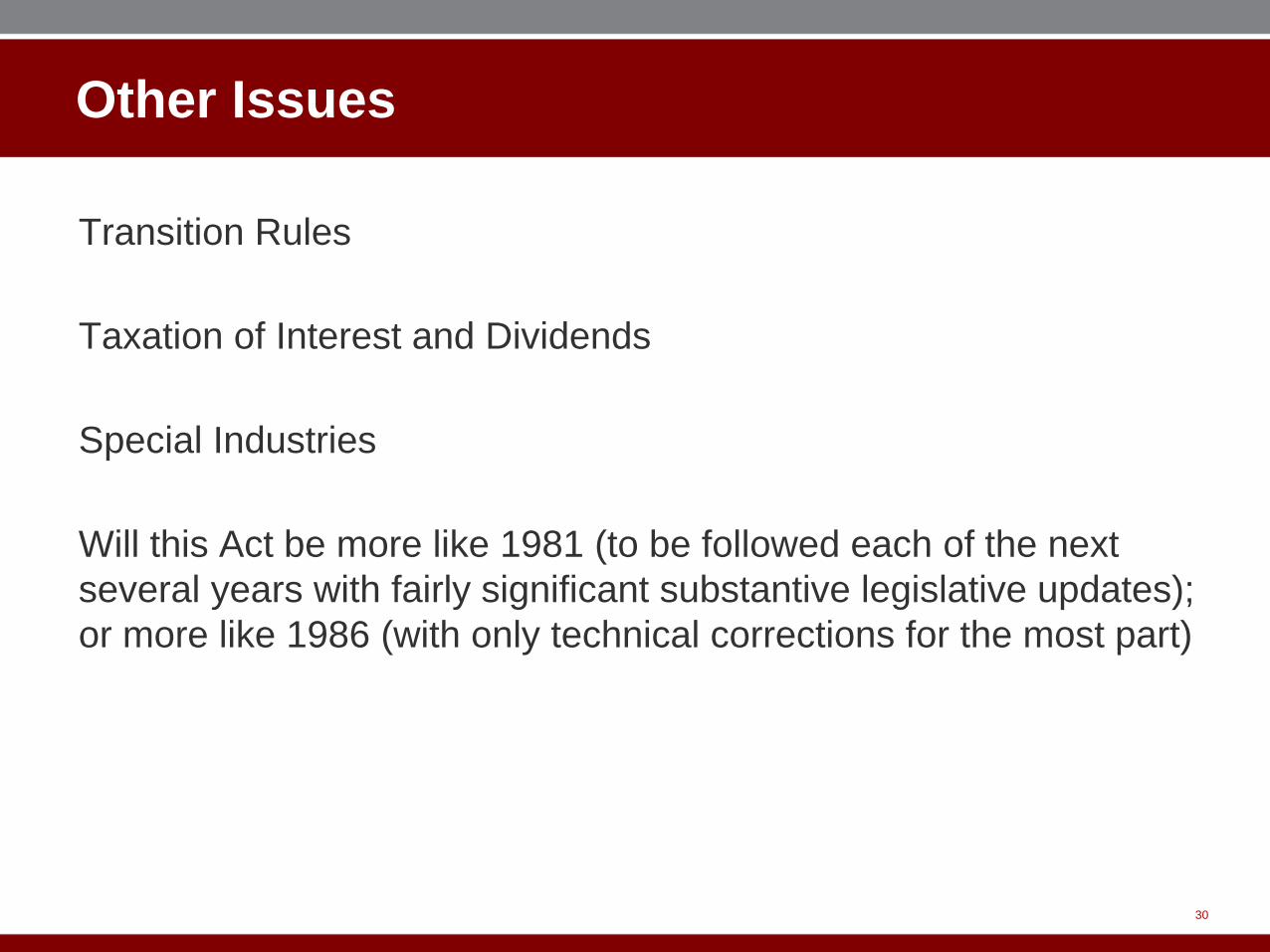

Other Issues

Transition Rules

Taxation of Interest and Dividends

Special Industries

Will this Act be more like 1981 (to be followed each of the next several years with fairly significant substantive legislative updates); or more like 1986 (with only technical corrections for the most part)

30