business strategy and performance measurement · marketing operations. ... • some outsource, some...

TRANSCRIPT

Strategy and PerformanceStrategy and Performance

K Pl tt d D i i O htKen Platts and Dominic Oughton

IfM Briefing Day, Tuesday 15 May 2012

AgendaOverview of the Centre for Strategy and Performance

Approaches to strategic analysisApproaches to strategic analysis

An example of a tool - Make vs Buyp y

Centre for Strategy and PerformanceCentre for Strategy and Performance

Aims of the CentreAims of the Centre• to develop effective research-based

techniques for strategy-making andtechniques for strategy-making and performance measurement system design

• to develop practical tools for industrial• to develop practical tools for industrial managers and consultants

• to interpret and disseminate research• to interpret and disseminate research findings

• to support and provide an industry academic• to support and provide an industry-academic community focused on strategy and performance

• to deliver educational and training materials

St t i D i i M ki

ThemesStrategic Decision MakingBuilding structured approaches that support strategy making

St t M d lli d Vi li tiStrategy Modelling and VisualisationDeveloping visual approaches to support strategy development

Competence Capability and Resource AnalysisCompetence, Capability and Resource AnalysisStudying the way companies create and exploit competences

Performance MeasurementPerformance MeasurementDesigning, developing and implementing performance measurement systems

ServitizationServitizationDeveloping tools to support servitization

Strategy Options for Start-upsgy p pExploring the strategic challenges for start-up companies

Taking a Process View

• Aims to understand ‘how’ operations management activities are carried out, with a view to improving them

i ll ‘hi h’ l l t t f l ti– especially ‘high’ level processes - e.g. strategy formulation, performance measurement design

Output• Processes and tools which will help managers manage their

operations better

Typical output - workbooks

Competing through competences Getting the measure of your businessCreating a winning business formula

Wi i d i i t l ti Make-or-BuyCompetitive ManufacturingWinning decisions -translating business strategy into action plans

St t D l t P dStrategy Development ProcedurePart 1Grouping ProductsGrouping Products

Stakeholder Requirements

Market and Company Constraints

Part 2What are our business

P t 5

Requirements

objectives? Part 5Navigating toward business objectivesCustomer

Requirements

Part 4Can current strategy achieve our

Part 6Again and again

Part 3What is our current strategy?

objectives? and .............

A Procedure

is a sequence of

Steps

involving the use of

Tools

th t li d i t

Techniques

that are applied using correct

Techniques

AnalogyAnalogy

Make vs. Buy Strategy: Example of a tool y gy pand case studies

Dominic Oughton, Principal Industrial Fellow

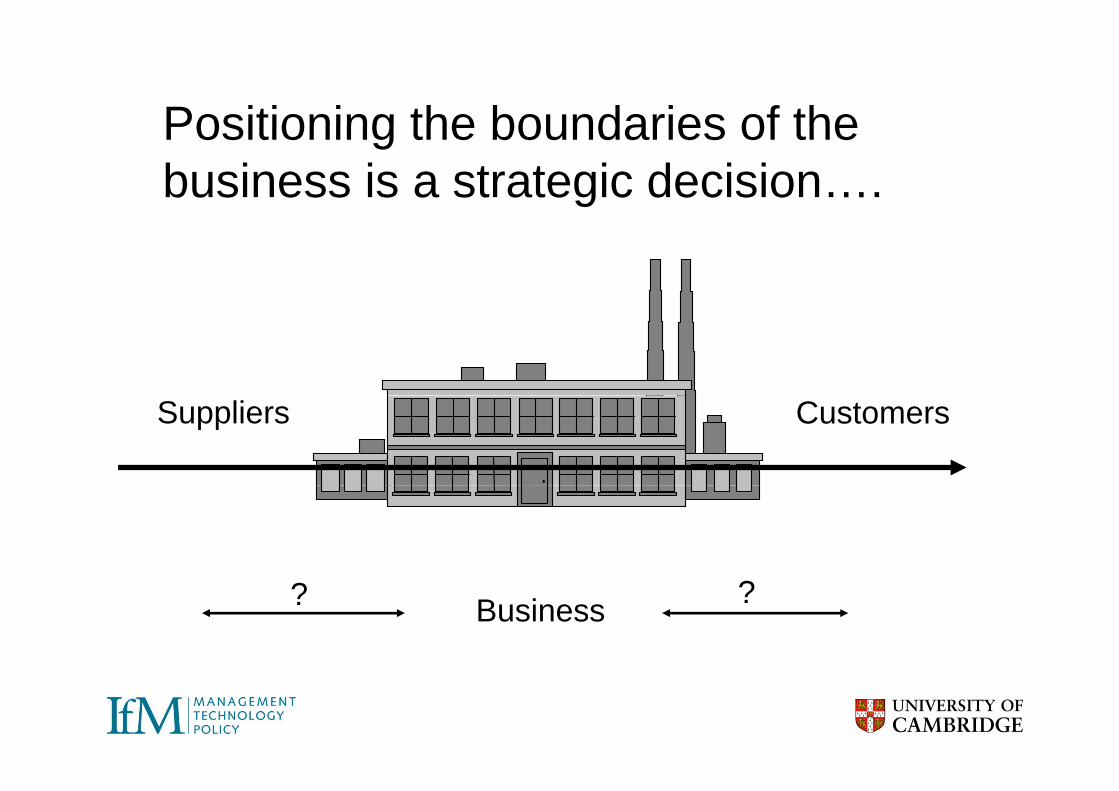

Positioning the boundaries of thePositioning the boundaries of the business is a strategic decision….

Suppliers Customers

? ?Business

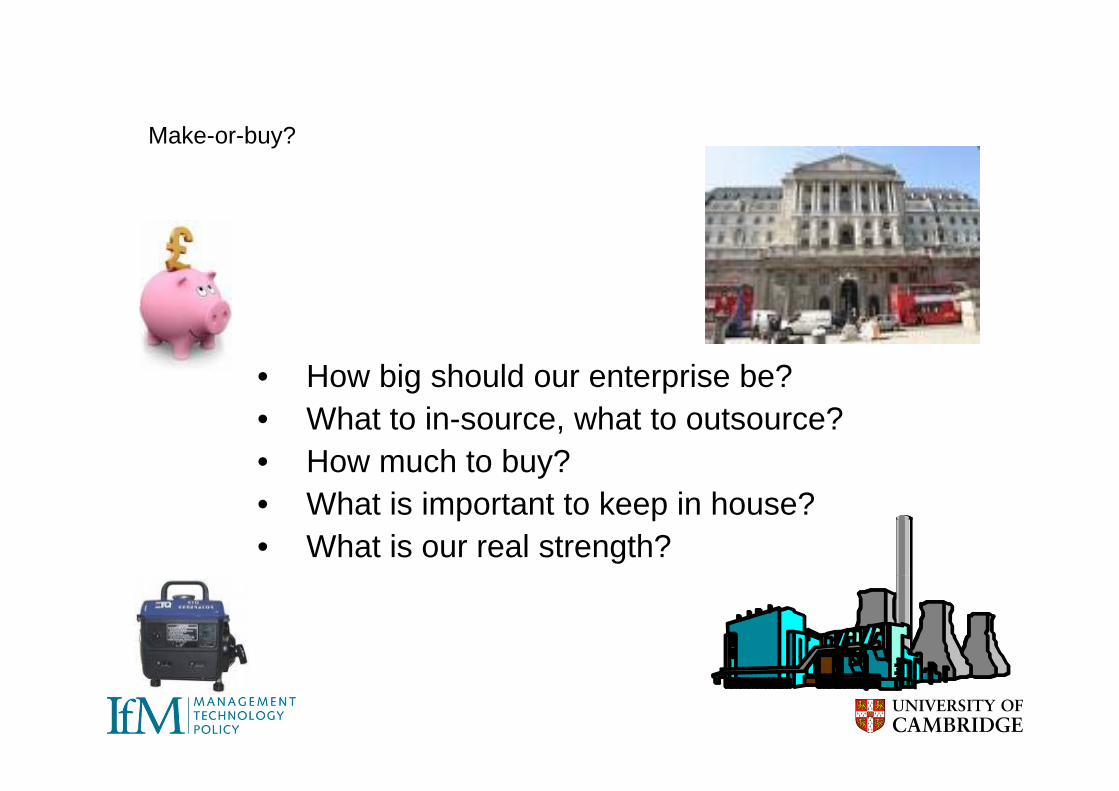

?Make-or-buy?

• How big should our enterprise be?• What to in-source, what to outsource?• How much to buy?• What is important to keep in house?• What is our real strength?

A common conflictA common conflictF iliFamiliar

scene?

Marketing Operations

The Common OutcomeThe Common Outcome

DEFINING MANUFACTURING AS A BROADER VALUE CHAIN

“The full cycle from understanding markets through product

design production distribution and related services within andesign, production, distribution and related services within an

economic and social context”

ServiceDistributionProductionDesignResearch ServiceDistributionProductionDesignResearch

This makes it possible to be in manufacturing without owning a factory!y

CISCO – NETWORK EQUIPMENT

ServiceDistributionProductionDesignResearch

Degree of shading represents relative focus

• Moving to become “lifestyle” brandM i f ti t t ff• Manage information not stuff

• From transaction to interactionM i l it diff ti t• Managing complexity as differentiator

• 100% outsource visionF d i d d• Focus on design and new product introductionO i ti t hi• Open innovation partnerships

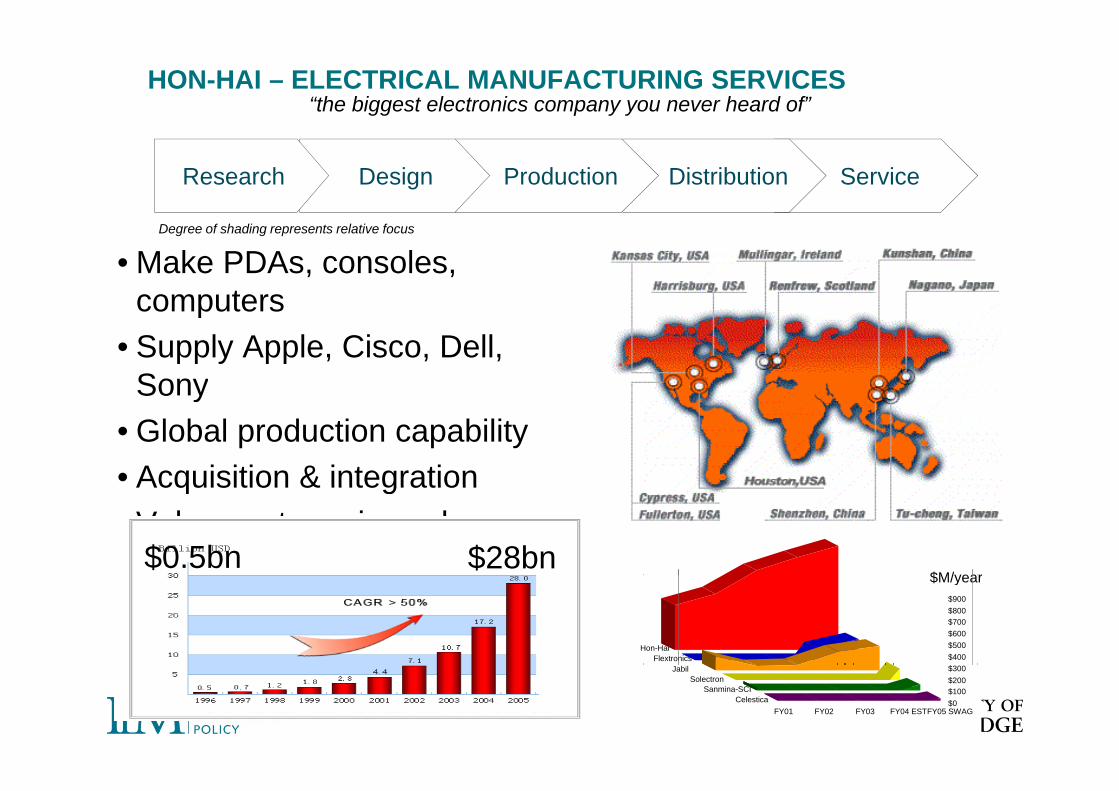

HON-HAI – ELECTRICAL MANUFACTURING SERVICES“the biggest electronics company you never heard of”

ServiceDistributionProductionDesignResearch

• Make PDAs, consoles, computers

Degree of shading represents relative focus

computers• Supply Apple, Cisco, Dell,

SonySo y• Global production capability• Acquisition & integrationAcquisition & integration• Value capture via scale• Moving to design and service $2,000

$M/year$0.5bn $28bnMoving to design and service

-$2,000

-$1,000

$0

$1,000

Hon-Hai Flextronics Jabil Solectron Sanmina-SCI Celestica

Hon-HaiFlextronics

$$400$500$600$700$800$900

$M/year

-$4,000

-$3,000

$ ,Jabil

SolectronSanmina-SCI

Celestica $0$100$200$300

FY01 FY02 FY03 FY04 ESTFY05 SWAG

ZARA - CLOTHES

ServiceDistributionProductionDesignResearch

Degree of shading represents relative focus

• Spanish clothes maker Zara owns all production capability (or has close-knit local partners)local partners)

• Products in own shops change every 2 weeks2 weeks

• Production can be flexed to respond to demandto demand

• Competitors can’t follow!

LLOYDS TSB – FINANCIAL SERVICES

ServiceDistributionProductionDesignResearch

• 2004: The Lloyds TSB Mumbai call centre was opened l i 700 t ff Ll d h t ll t i N tl

Degree of shading represents relative focus

employing 700 staff. Lloyds shuts call centre in Newcastle with the loss of 968 jobs.

• “Lloyds TSB's reputation has been seriously damaged because of customer dissatisfaction with having to deal withbecause of customer dissatisfaction with having to deal with the India call centre, with customers and staff unable to understand each other.”

• 2007: Lloyds TSB, the UK's biggest provider of current y gg paccounts, is bowing to customer demands and moving calls back to the UK from a service centre in India.

• Sally Jones-Evans, managing director, telephone banking f Ll d TSB d th t it h i it li

Norwich Union:of Lloyds TSB, argued that it was changing its policy because of the introduction of an automated voice-recognition answering service

• Rivals suggested the change would cost Lloyds up to £30m

• “We have moved certain calls back to the UK, like household claims," • Indian call centres now deal with things such as changing the address on a policy. • Customer satisfaction levels are roughly • Rivals suggested the change would cost Lloyds up to £30m the same for centres in the UK and in other countries

Thoughts from earlier in the day...

Cisco – Hon Hai – Lloyds – Zara

ServiceDistributionProductionDesignResearch

No single right answer• No single right answer

• Some outsource, some make process-ownership a virtue

• Some offshore, some go close to customer or ‘knowledge’

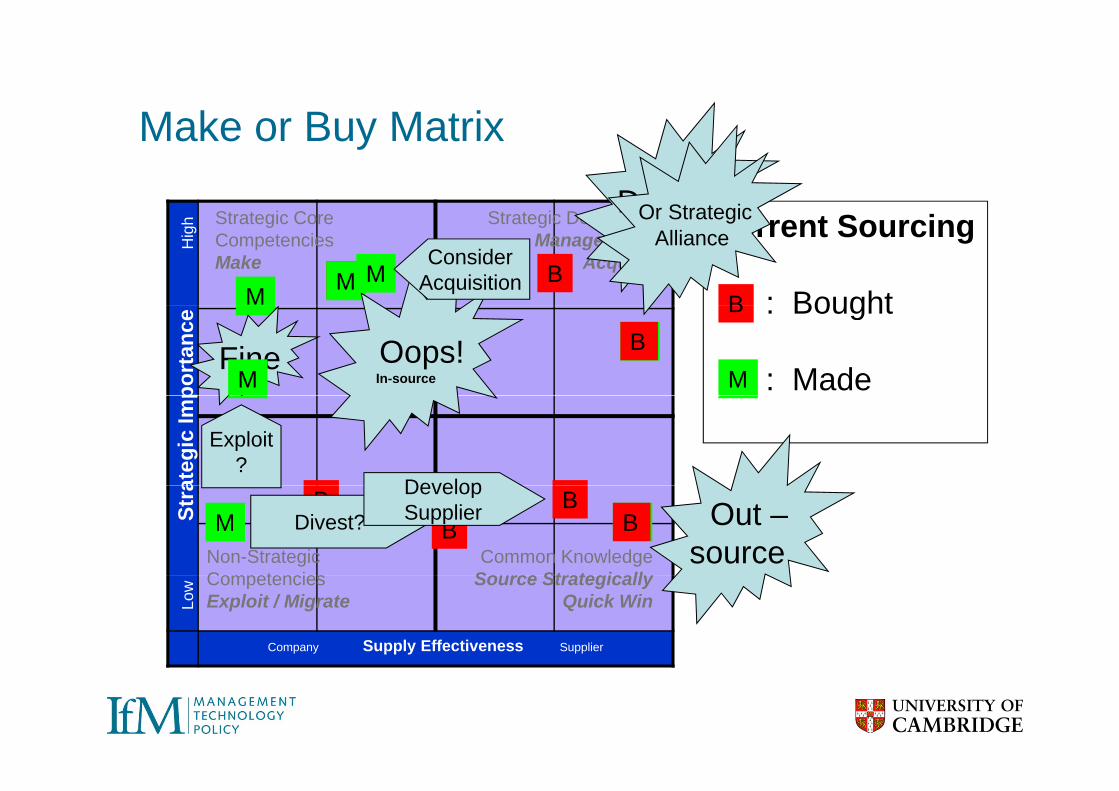

Make or Buy MatrixMake or Buy Matrix

Strategic Core Strategic DeficiencyStrategic Core CompetenciesMake

Strategic DeficiencyManage risk /

Acquire

Hig

hpo

rtan

ceat

egic

Imp

Non-StrategicC t i

Common KnowledgeS St t i ll

Stra

Company Supply Effectiveness Supplier

CompetenciesExploit / Migrate

Source StrategicallyQuick WinLo

w

Make or Buy MatrixMake or Buy Matrix

Strategic Core Strategic Deficiency C t S iStrategic Core CompetenciesMake

Strategic DeficiencyManage risk /

Acquire

Hig

h

M B BB

Current Sourcing

: Bought

port

ance

MM

: Bought

: Made

ateg

ic Im

p

Non-StrategicC t i

Common KnowledgeS St t i ll

Stra

M MB

Company Supply Effectiveness Supplier

CompetenciesExploit / Migrate

Source StrategicallyQuick WinLo

w

Make or Buy Matrix

C t S i

Make or Buy Matrix

Strategic Core Strategic DeficiencyDanger!Or Strategic

B

Current Sourcing

: Bought

Strategic Core CompetenciesMake

Strategic DeficiencyManage risk /

Acquire

Hig

h

M B B

g

M MConsider

Acquisition

Or StrategicAlliance

M

B : Bought

: Madeport

ance

MFine Oops!In-source

BM

ateg

ic Im

p

Exploit?

Develop

Non-StrategicC t i

Common KnowledgeS St t i ll

Stra

M MB B

Divest? Out –source

BB

DevelopSupplier

Company Supply Effectiveness Supplier

CompetenciesExploit / Migrate

Source StrategicallyQuick WinLo

w

Industrial Case Study 1 -Make v Buy in Practice

European Capital GoodsEuropean Capital Goods

Background

• European Capital good manufacturer• Serving global market• Serving global market• Highly-engineered / bespoke core product• Entered related market for “commodity product”

– Full product line offering– Customer service

S t & h l– Same customers & channels• Sourced product for market entry from Chinese manufacturer• 3 years on3 years on

– Number 2 in commodity market– Price pressure– Time for review…

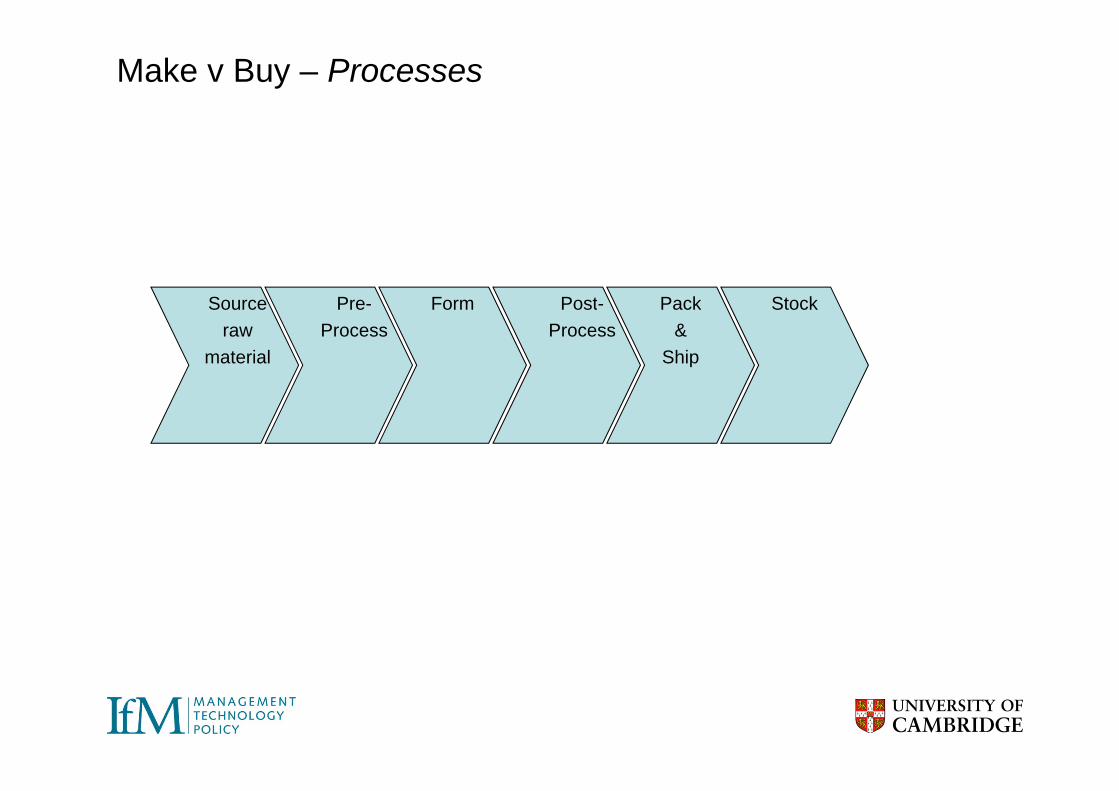

Make v Buy – Processes

Source Form PackPost-Pre- StockSourceraw

material

Form Pack&

Ship

PostProcess

PreProcess

Stock

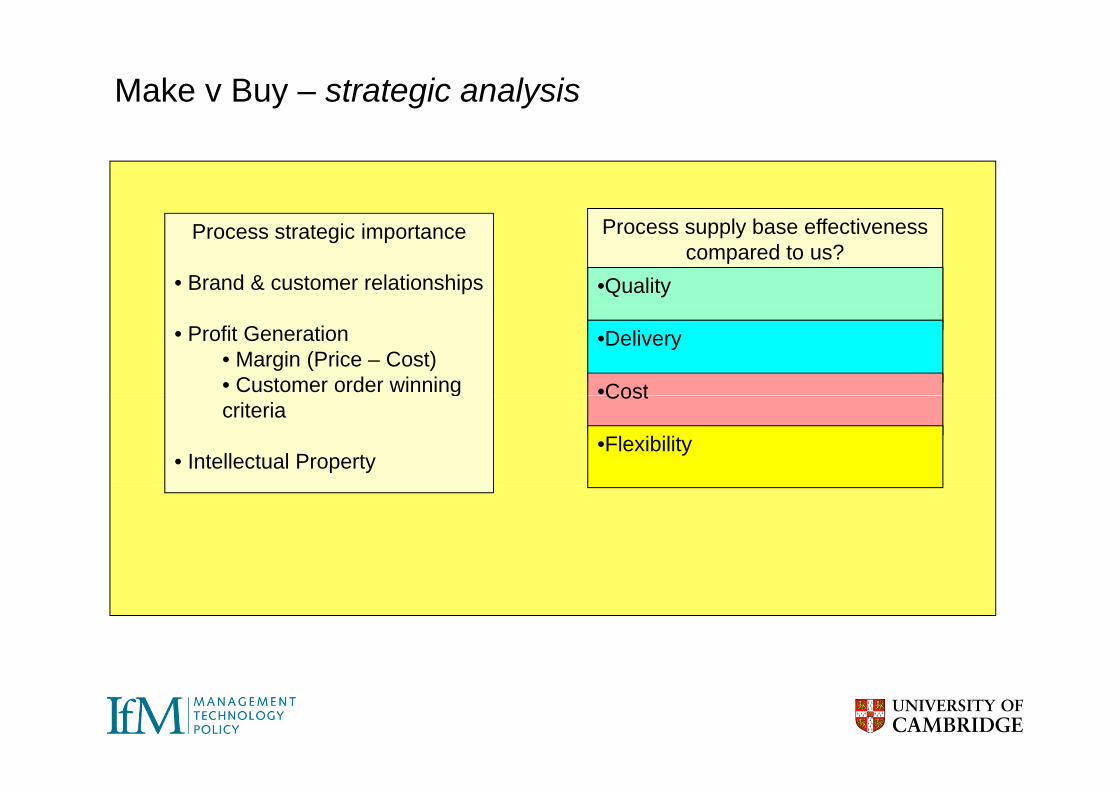

Make v Buy – strategic analysis

Process strategic importance

• Brand & customer relationships

Process supply base effectiveness compared to us?

•Quality

• Profit Generation• Margin (Price – Cost)• Customer order winning

•Delivery

•Costgcriteria

• Intellectual Property

Cost

•Flexibility

Make or Buy Matrix

Strategic Core Strategic Deficiencyh

CompetenciesMake

Manage risk / Acquire

e

Hig

h

Source

mpo

rtanc

eS

trate

gic

Im

FormStock

Pack & Ship

Non-StrategicCompetencies

Common KnowledgeSource Strategicallyow

S

Pre-process

•Company Supply Effectiveness Supplier

pExploit / Migrate

g yQuick WinL Post-process

Outcomes

• In-source:– Raw material sourcing is critical competence– Raw material sourcing is critical competence– Remaining processes are necessary to enable strategic sourcing

• Quality & Delivery benefits from in-sourcing• Network approach to optimisation

– Shipping costs v labour costsB fit f b i l t t– Benefits of being close to customer

• Regional service centre network– China / South America / CIS / MEChina / South America / CIS / ME

• 17% reduction in costs = Euro 3.4 million annual saving

Make-or-Buy Framework

Case Study 2 IMI plc• A dynamic, international business delivering innovative, knowledge-

based engineering and system solutions for global customers

Case Study 2 – IMI plc

based engineering and system solutions for global customers• Focused on strong niche markets• Quoted on the London Stock Exchange• Turnover £1.9bn , recent market cap approximately £1.6bn• 19,000 employees in more than 35 countries

C &• Two core business areas: Fluid Controls & Retail Dispensing

Context

International business expansion requiring linkage between business, customers manufacturing a supply chaincustomers manufacturing a supply chain

Significantly high value of manufacturing output, IMI has manufacturing sites in 2 i25 countries

Considerable part of manufacturing in high cost countries, however major p g g jbusiness expansion in emerging regions

Many activities considered non-coreMany activities considered non core

Significant shift in manufacturing strategy processes

Need for Strategic Manufacturing Decisions Linked With Business Strategy

IMI Identified the need for a structured approach to manufacturing decisions

“We need to be in China”

“We can make it internally much more efficiently”

“Labour in Asia is much cheaper”

more efficiently

“Eastern Europe seems to be better

“Why don’t we

tbe better solution” go to

Mexico?”

Need for a structured approach to manufacturing decisions

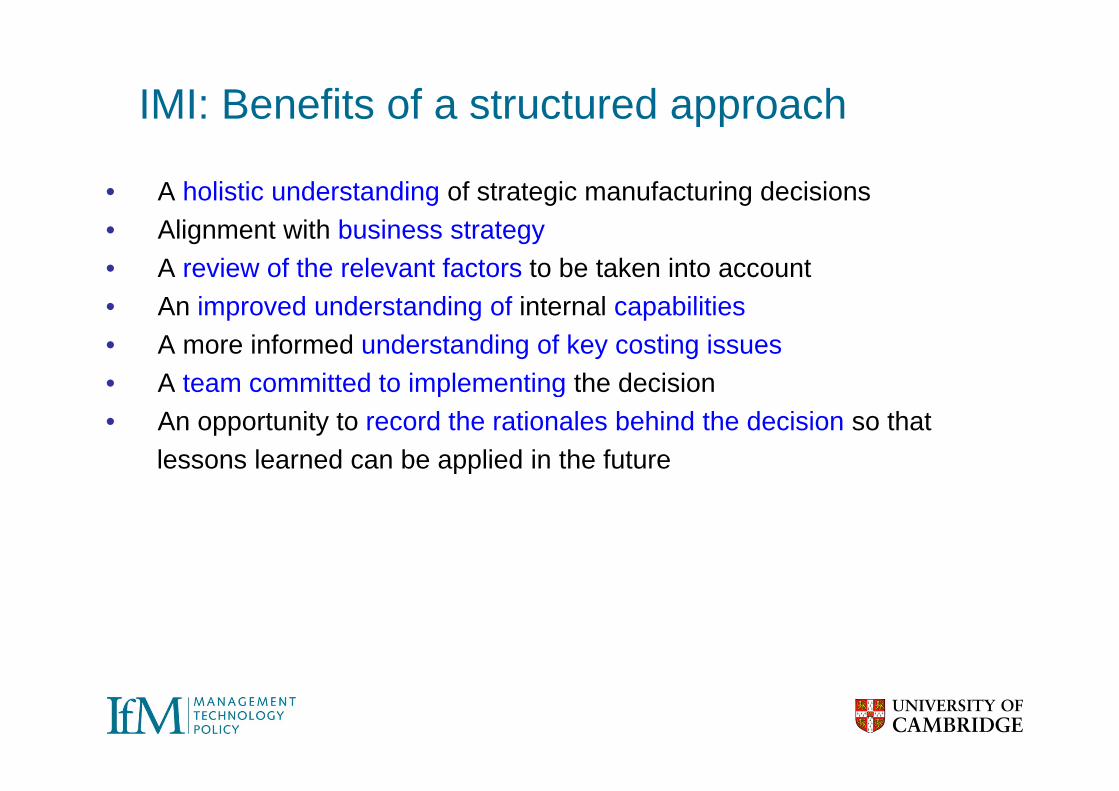

IMI: Benefits of a structured approach

• A holistic understanding of strategic manufacturing decisions

pp

• Alignment with business strategy• A review of the relevant factors to be taken into account• An improved understanding of internal capabilities• An improved understanding of internal capabilities• A more informed understanding of key costing issues• A team committed to implementing the decisionp g• An opportunity to record the rationales behind the decision so that

lessons learned can be applied in the future

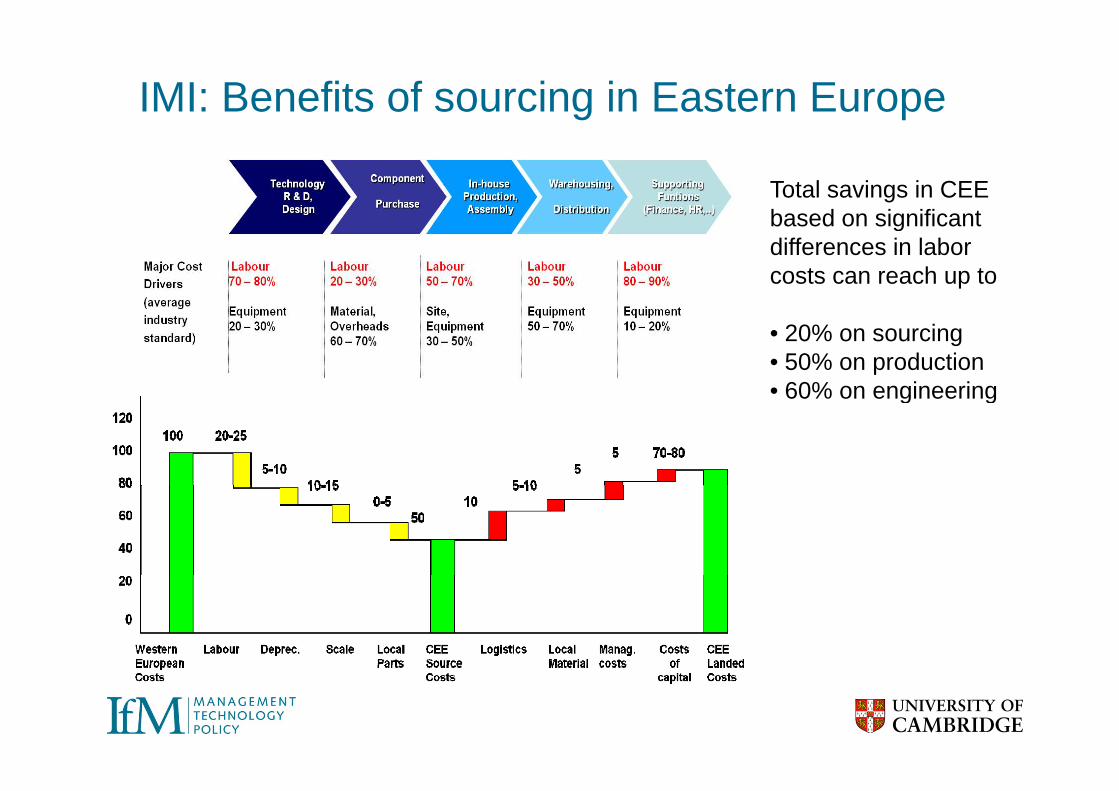

IMI: Benefits of sourcing in Eastern Europe

Total savings in CEE based on significantbased on significant differences in labor costs can reach up to

• 20% on sourcing• 50% on production • 60% on engineering60% on engineering

Industrial Case Study 3 -Make v Buy in Practice

at Novar plcat Novar plc

Setting the scene g

• Huge competitive cost pressure upon European manufacturing base, mainly from the Far East sources with low cost and acceptable quality productsp

• European manufacturing has a high fixed cost base and structure• The global economic market has created new threats and opportunities,

l di t t titi d l ileading to greater competition and lower prices• The cost of labour can be circa 80% cheaper in Far East, in part off-set by

supply chain complexity/constraintspp y p y• New sources of supply identified in Eastern Europe• Need to really understand and challenge why we should ‘make’• Key is to understand the customer needs and then determine the best

way to satisfy them, in some instances the customer will be totally indifferent to who makes the productp

Common Mistakes when OutsourcingCommon Mistakes when Outsourcing

• Underestimating the skills required

• Having a poor understanding of the supplier capabilities

• Overlooking transaction costs

• Decision making by single individuals without input from other areas of the organisationfrom other areas of the organisation

Novar evaluation of IfM ProcessNovar evaluation of IfM Process

• Very good basis to start the detailed evaluation process• Provides a structured approach and greater objectivity• Provides a structured approach and greater objectivity• Cross functional team approach is essential• The methodology is an important element of a bigger• The methodology is an important element of a bigger

picture, it cannot stand however as the only element of the evaluation process.evaluation process.

• A good facilitator is required to process manage and ensure objectivenessj

• The 2 supporting books are very good

Questions?Questions?