business outlook for asean country 2017 outlook for asean country 2017 ... central bank rates, ......

TRANSCRIPT

Business Outlook forASEAN Country 2017Thailand Insurance Symposium 201619 December 2016Bangkok, Thailand

Clarence WongChief Economist Asia

2

Agenda

• What are our top economic concerns?

• What does this mean to ASEAN?

• What will be the key insurance themes forASEAN countries?

What are our topeconomic concerns?

33

4

Top economic risk map that could impact ASEAN

Chinese hardlanding: Credit risksfrom a significantslowdown in theproperty sector are thegreatest downside risk

Chinese hardlanding: Credit risksfrom a significantslowdown in theproperty sector are thegreatest downside risk

Sharp growthslowdown inadvanced marketsdue to fallout fromBrexit, downside risksin emerging marketsand political conflicts

Sharp growthslowdown inadvanced marketsdue to fallout fromBrexit, downside risksin emerging marketsand political conflicts

Recession in the Euroarea: Risks of policy errors,reform complacency,renewed conflicts in Ukraine,geopolitical risks andslowdown in China

Recession in the Euroarea: Risks of policy errors,reform complacency,renewed conflicts in Ukraine,geopolitical risks andslowdown in China

Emerging marketContagion: risks includeFed normalisation, highexternal debts, lowcommodity prices etc

Emerging marketContagion: risks includeFed normalisation, highexternal debts, lowcommodity prices etc

15%15%

20%20%

20%20%

15%15%

Source: Swiss Re Economic Research & Consulting

Medium-term inflationrisksMedium-term inflationrisks

15%15%

Oil price collapse – astabilising forceOil price collapse – astabilising force

10%10%

Interest rate risk

Note: Updated on 28/09/2016Source: CEIC

Central bank rates, monthly data

5

Ultra-low monetary policy continues in most advancedmarkets

0

2

4

6

8

10

12

14

16

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

EU United Kingdom United States

• Weak growth anddownside risks arenudging central bankersto keep interest rateslower for longer

• The scale of negativepolicy rates has expanded(Euro Area, Denmark,Japan, Sweden andSwitzerland) to representnearly 25% of global GDP

• Half of the world’ssovereign bonds carrynegative interest rates*

* refers to bonds in the S&P GlobalDeveloped Sovereign Bond Index

6

• The expected recovery in tradehas been slow and unsteady.

• This could reflect changes inthe global value chain, weakerdemand from emerging marketsand low supply of credit.

• Economic growth in recent years hasbeen supported by higher debt, bothfor households and corporations

• Against the backdrop of slowingtrade/economic growth, risinginterest rates, debt servicing willbecome more challenging

• Pace has remained cautious dueto heightened uncertainty overglobal economic outlook.

• Fed tightening will result incapital outflows from Asia andincreased financial volatility.

• China is in the process of goingthrough complex economicadjustments – resulting in slowergrowth.

• Key concerns include policy errors,mis-communication, systemicfinancial risks and conflictingobjectives.

High debt leverageWeak trade activities

Fed lift-off China hard-landing

Strong economic headwinds facing ASEAN

6

ASEAN has maintained ~5% growth since financial crisis…

7

6.1

%

2.7

%

5.1

% 5.6

% 6.6

%

5.6

%

6.1

% 6.6

%

4.7

%

1.8

%

7.9

%

4.9

% 5.9

%

5.0

%

4.5

%

4.5

%

4.5

%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average real GDP growth rate

5.4% 5.3%

Source: Swiss Re Economic Research & Consulting

Fina

ncia

l Cri

sis

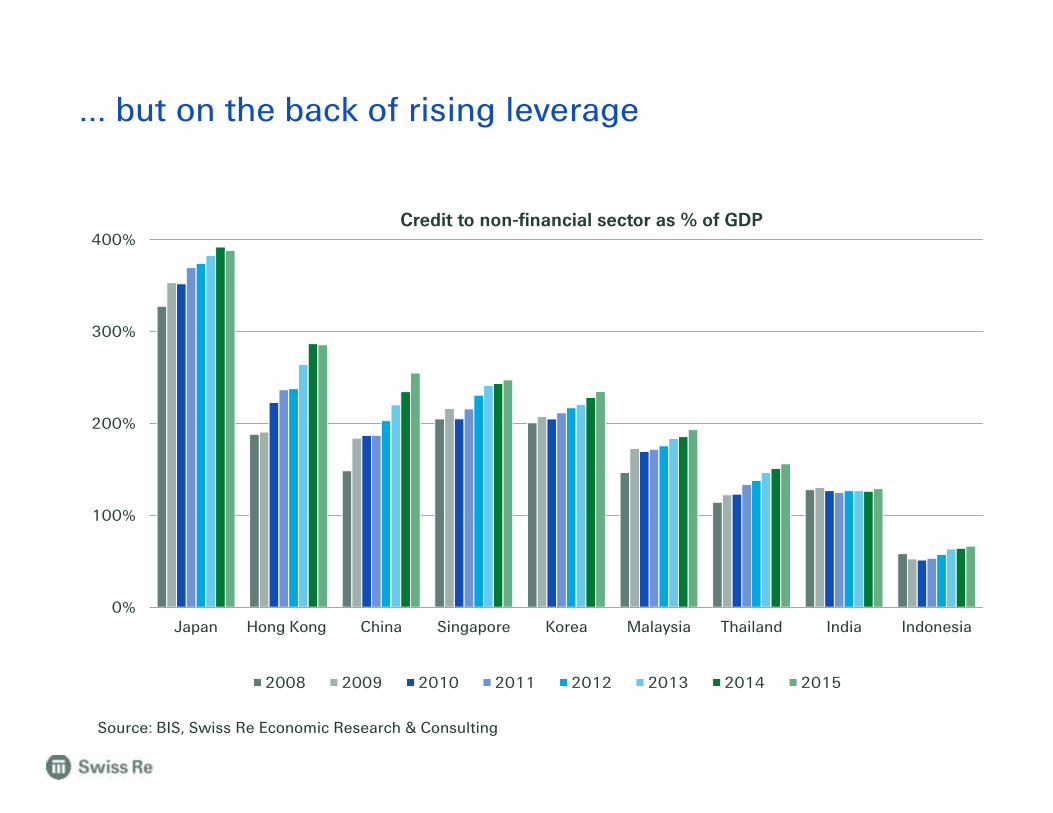

… but on the back of rising leverage

0%

100%

200%

300%

400%

Japan Hong Kong China Singapore Korea Malaysia Thailand India Indonesia

Credit to non-financial sector as % of GDP

2008 2009 2010 2011 2012 2013 2014 2015

Source: BIS, Swiss Re Economic Research & Consulting

Government deficit and leverage have also increasedsince the GFC

9

Source: Oxford Economics, BIS, Swiss Re Economic Research & Consulting

-6%

-4%

-2%

0%

Viet

nam

Mya

nmar

Mal

aysi

a

Indo

nesi

a

Thai

land

Laos

Cam

bodi

a

Phi

lippi

nes

Sing

apor

e

Government deficit as % of GDP

2007 2015

0%

30%

60%

90%

120%

Sing

apor

e

Phi

lippi

nes

Mal

aysi

a

Thai

land

Indo

nesi

a

Government leverage: credit to generalgovernment sector as % of GDP

2007 2015

What does this mean toASEAN?

1010

Interest and coupon payments are rising faster thancorporate and household income

11

Source: Bank for International Settlement

0%

5%

10%

15%

20%

25%

Hong Kong Korea China Japan Malaysia Thailand India Indonesia

Debt service ratios of private non-financial sector

1999 2009 2015

Sensitivity of ASEAN to China – trade channel

12

0

2

4

6

8

10

12

14

16

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

USD million (LHS) Share of total trade (%, RHS)

Note: *includes Indonesia, Malaysia, Philippines, Singapore and ThailandSource: CEIC

ASEAN-5 China trade exposure*

Sensitivity of ASEAN to China – trade and other channels

13

Channels of Spillovers from a Slowdown in China

Note: AUS = Australia; IND = India; IDN = Indonesia, JPN = Japan; KOR = Korea; MYS =Malaysia; NZL = New Zealand; PHL = the Philippines; SGP = Singapore; THA = Thailand;TWN = Taiwan Province of China; VNM = Vietnam.Source: IMF

China has more impact

on ASEAN exports than

the US and EU (except

for the Philippines) – a

1ppt rise in growth in

China will result in 1.5-

2.5 ppt increase in

ASEAN exports …

… but ASEAN is still

relatively less exposed to

China compared to other

Asian countries

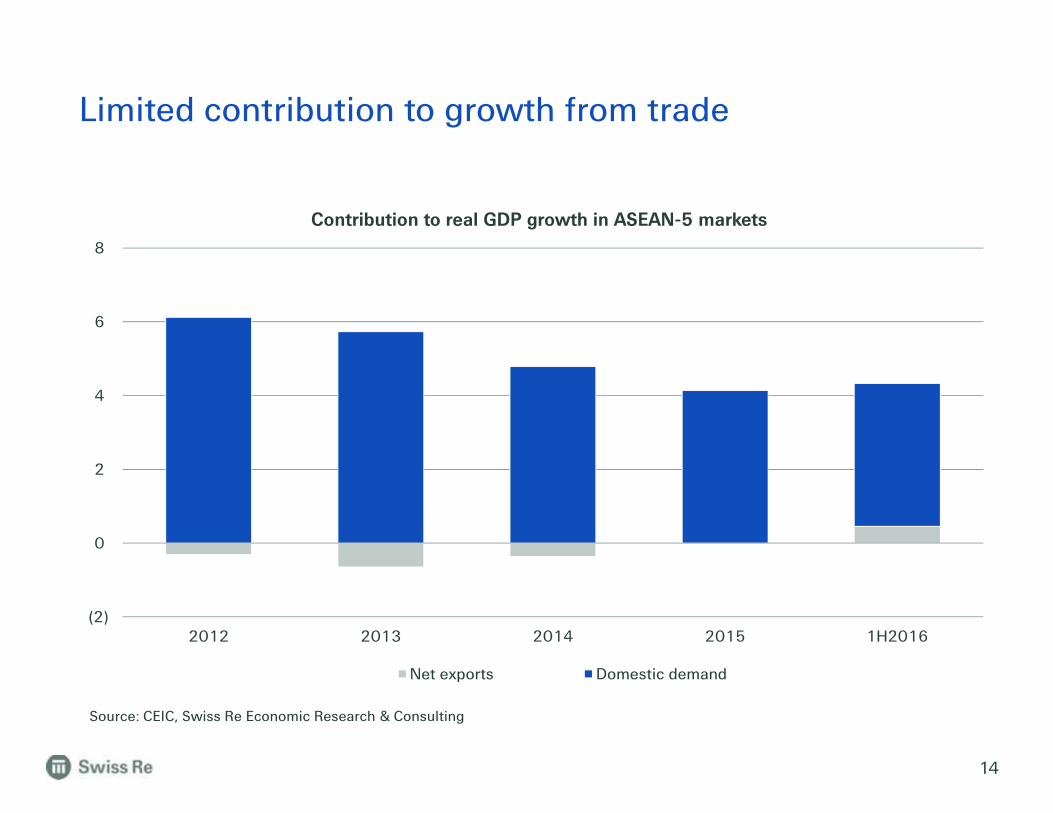

Limited contribution to growth from trade

14

(2)

0

2

4

6

8

2012 2013 2014 2015 1H2016

Contribution to real GDP growth in ASEAN-5 markets

Net exports Domestic demand

Source: CEIC, Swiss Re Economic Research & Consulting

20

40

60

80

100

120

140

Jan-

20

13

Jul-2

01

3

Jan-

20

14

Jul-2

01

4

Jan-

20

15

Jul-2

01

5

Jan-

20

16

Jul-2

01

6

Crude oil, copper and USD indices(1 Jan 2013=100)

Copper (LME) Crude oil (WTI)

USD trade weighted index

Elevated financial volatility coincides with falling crude oil,commodity prices and USD strength

15

50

100

150

200

250

300

Jan-

20

13

Jul-2

01

3

Jan-

20

14

Jul-2

01

4

Jan-

20

15

Jul-2

01

5

Jan-

20

16

Jul-2

01

6

Bond and stock volatility indices(1 Jan 2013 = 100)

US treasury volatility index (MOVE)

S&P volatility index (VIX)

Source: Bloomberg, CEIC, Swiss Re Economic Research & Consulting

16

What will be the keyinsurance themes forASEAN countries?

16

Insurance having gone through phases of development inAsia

17

0

120

240

360

480Nonlife premiums (USD b)

Life & health premiums (USD b)

Phase 1: monopolistic market structure,entry barriers, price/product regulations

Phase 2: liberalisation, deregulationand globalisation

Phase 3: economic/income growth,solvency reforms, personal lines

Source: Swiss Re Economic Research & Consulting

ASEAN FrameworkAgreement on Servicessigned in 1995

Asia financial crisis

India opened insurancesector to private and foreigncompanies

International insurersentering EM Asia markets

Global financial crisis

China entered WTO inDec 2001

-20%

0%

20%

40%

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Nonlife premiums real growth

Life & health premiums real growth

China

India

South Africa

Angola

Nigeria

Morocco

Ghana

Cote d Ivoire

Kenya

Mozambique

Ethiopia

0%

1%

2%

3%

4%

0.45 4.5 45GDP per capita in 1000 USD

Asia Middle East Africa

Non-life insurance penetration(premiums as a % of GDP) South Korea

Taiwan

Japan

Hong KongMalaysia

Philippines

IndonesiaVietnamBrunei

Thailand

CambodiaBangladesh

Source: Swiss Re Economic Research & Consulting. 18

Many emerging Asian markets have low insurancepenetration but are poised to achieve fast growth

Early movers Middle market Growers Slow growth

Singapore

log scaleIncome growthIncome growth

Pene

trat

ion

grow

thPe

netr

atio

n gr

owth

Fundamentals remain strong – middle income class andurbanisation

0

5

9

14

18

China India Indonesia MiddleEast

& Africa

LatinAmerica

OtherEmergingmarkets

USD trillion

Urbanisation-led infrastructure spending isexpected to be the highest in China during

2013-2023 (USD trillion)

Commercial floor space constructionWater & waste-water managementEnergy sectorTransportation

0%

20%

40%

60%

80%

100%

2009 2020 2030

The number of middle-income households isexpected to rapidly increase in Asia Pacific,

especially in India and China

North America EuropeCentral & South America Asia PacificSub-Saharan Africa Middle East & North Africa

Source: OECD, McKinsey Institute

One-Belt-One-Road

20

0

2

4

6

8

10

12

14

16

Japa

n

Sou

th K

orea

Sin

gapo

re

Hon

g K

ong

Chi

na

Thai

land

Aus

tral

ia

Vie

tnam

Indo

nesi

a

Wor

ld

Mal

aysi

a

Indi

a

Phi

lippi

nes

Old age support ratio(population aged 15-64 over population aged

65+)

2011 2030 2050

Demographic changes and healthcare needs

Source: WHO World Health Statistics, United Nations Population Division

Government funding and out-of-pocketexpenditure are the main financing

channels for healthcare expenditure

0%

20%

40%

60%

80%

100%

Government fund Social fund Private insurance

out-of-pocket other private fund

Technologies will have an impact on the whole of societyand thus shift risk pools and create new opportunities.

World's largest transportation company owns no vehicles -

Largest accommodation provider owns no real estate -

Largest phone company owns no telco infra -

World's most valuable retailer has no inventory -

Most popular media owner creates no content -

Fastest growing banks have no actual money -

World's largest movie house owns no cinemas -

Largest software vendors don't write the apps -

What will be the insurance headline?

Source: Tech Crunch, The Battle Is For The Customer Interface, Insurance and the Connected World, Strategy Meets Action

23

Digital Technology Adaption CurveIm

pact

of d

igita

lisat

ion

Point on digitalisation journey

Energy

Health Care

Logistics

Automotive

Consumer Packaged Goods

Telecom, Insurance and Banking

Retail

Media

Several majordisruptions haveoccurred

Disruptive moves (e.g. by pure onlineplayers) have affected these industries, butthe final outcome is still to be determined

Effect of digitalisation is still unknown anddisruptive changes remain to be seen; theseindustries are very similar in their overall levelof digitalisation

Data protection and privacy

Non-traditional players areentering across the valuechain

Are consumers comfortablewith insurers access toinformation on usage/behavior

Source: BCG, How to jump start a digital transformation, 2015

In ASEAN, mortality protection gap increased by an annualaverage of 9% over the past decade to USD 3.5 trillion

24

Note: mortality protection gap is defined as the difference between the protection needed (10x of average annual salary) and theprotection in place (including net financial assets/savings and relevant life insurance) to maintain dependents in living standardsfollowing the death of the primary breadwinner.Source: Swiss Re Economic Research & Consulting

0%

6%

12%

18%

50%

150%

250%

350%Vi

etna

m

Thai

land

Mal

aysi

a

Sing

apor

e

Phi

lippi

nes

Indo

nesi

a

ASE

AN

Mortality protection gap in 2014 (USD bn), LHS Avg annual increase in mortality protection gap (2004-2014), RHS

Uninsured Nat Cat losses have been particularly large inThailand, Indonesia, Philippines and Myanmar

25

Source: Swiss Re Economic Research & Consulting

(40) (30) (20) (10) - 10 20 30 40

Singapore

Laos

Cambodia

Malaysia

Vietnam

Myanmar

Philippines

Indonesia

Thailand

Accumulative nat cat losses, USD bn (2004-2015)

Insured losses Uninsured losses

Uninsured Nat Cat losses Insured Nat Cat losses

26

ASEAN Economic Community – ASEAN in 2030

1. AEC stands for ASEAN Economic Community2. Consuming class refers to those with income exceeding the level at which they can begin to make significant discretionary purchases.Source: Southeast Asia at the crossroads: Three path to prosperity, Nov 2014, Mckinsey&Company.

USD 7 trillion ininfrastructureinvestmentopportunities

USD 7 trillion ininfrastructureinvestmentopportunities

“Consumingclass” 2

doubling to163 mnhouseholds

“Consumingclass” 2

doubling to163 mnhouseholds

Urbanisation:More than 90 mnpeople areexpected to moveto cities

Urbanisation:More than 90 mnpeople areexpected to moveto cities

AEC 1 couldcreate USD280bn to USD615bn in annualeconomic value

AEC 1 couldcreate USD280bn to USD615bn in annualeconomic value

Concluding remarks

27

• Growth in ASEAN is increasingly constrained by 1) weak trade outlook; 2)limited room for further debt accumulation; and 3) already low interest rates

• Regional markets will nonetheless continue to pursue fiscal expansion tosupport growth

• Longer–term, structural and economic reforms are key to success

• Regardless of when the Fed actually lifts off, the impact is already felt inASEAN

• The next phase of growth – deleveraging but not a financial crisis

• What these mean to the insurance industry?

28

Legal notice

29

©2016 Swiss Re. All rights reserved. You are not permitted to create any modificationsor derivative works of this presentation or to use it for commercial or other public purposeswithout the prior written permission of Swiss Re.

The information and opinions contained in the presentation are provided as at the date ofthe presentation and are subject to change without notice. Although the information usedwas taken from reliable sources, Swiss Re does not accept any responsibility for the accuracyor comprehensiveness of the details given. All liability for the accuracy and completenessthereof or for any damage or loss resulting from the use of the information contained in thispresentation is expressly excluded. Under no circumstances shall Swiss Re or its Groupcompanies be liable for any financial or consequential loss relating to this presentation.