business manager training may 2010 financial … versions/year_end_presentation...business manager...

TRANSCRIPT

BUSINESS MANAGER TRAININGMay 2010

Financial ServicesPolicies and Procedures

Lynne DavisAssistant Director, ASU Financial Services

General & Auxiliary Accounting

Presentation Objectives

• Knowledge of various entities/policies/standards governing financial transactions.

• Understanding what constitutes public funds/monies at ASU, and the importance of public purpose.

• Familiarity with the financial responsibilities of ASU business administrators.

Agency/Org Set up for Non-

Sponsored Accounts

• ORGS (ORGANIZATIONS):

• XXX 1XXX-Tempe Campus

• XXX 4XXX -Downtown Phoenix Campus

• XXX 5XXX-West Campus

• XXX 7XXX-Polytechnic Campus

Agency/Org Set up

AGENCIES:

• XX1 XXXX - State General Operating

• XX2 XXXX - Auxiliary

• ___ XXXX - Sponsored (Agency Code is ALPHA)

• XX4 XXXX - Summer Session

• XX5 XXXX - Designated

• XX6 XXXX - Plant

• XX7 XXXX - Agency

• XX8 XXXX - Endowment, Student Loan

• XX9 XXXX - Restricted

Types of Accounts

• State appropriations. Can not transfer appropriations among campuses.

– Current year personal services , ERE, and operating expenses.

– Unencumbered appropriations at year-end do not roll into the next fiscal year. They are used to help fund university-wide initiatives.

• Local Accounts -

– Auxiliaries

• Self Supporting (Residential Life, Bookstore, ICA)

– Restricted

• Gifts

• Scholarship Accounts – Student Financial Assistance Office

• Technology & Research Initiatives Fund (TRIF)

– Designated

• Sales/Services

• Departmental tuition/fees

Types of Accounts (cont.)

• Sponsored projects/Grants and Contracts

– Comply with all ASU Policies and Procedures

– Granting agency can be more restrictive

• Plant Funds

– Renovation projects on state accounts must be less than $50,000.

– Locally funded renovation projects over $25,000 typically are established as plant project accounts.

• Agency Funds

– YV7 Accounts

– Revenues and expenses belong to organization other than ASU

– ASU does have fiduciary responsibility so all ASU policies and procedures are followed.

• Endowments

– ASU Endowments – oversight is by Financial Services

– ASU Foundation Endowments – oversight is by ASU Foundation

Who are users of ASU’s Financial Statements?

• State legislature• Arizona Board of Regents• ASU departments• Bond rating agencies• Accreditation agencies • Arizona tax payers Parents or others paying for

tuition • Granting agencies • Gift donors • Other universities (for trend comparisons)

What users of ASU’s Financial Statements Might Want to Know

• Is ASU financially healthy? (page 14)

• How did ASU use the revenues it received? (page 10, and page 30, Note I)

• Is ASU better off financially at the end of the fiscal year than it was at the beginning? (page 16)

• Which revenue categories are showing growth? (pages 8-9)

Page references are from the ASU 2009 Financial Report.

Should users ‘trust’ ASU’s Financial Report?

• YES.

• The ASU Financial Report is an accumulation of all ASU departmental accounts – so departments must ensure the validity of their accounts!

• Any ASU departmental transaction can traced to lines on the financial statements

• Before the Financial Report is issued –– Signed certification

• President Michael Crow• Executive VP/Treasurer/CFO Morgan Olsen• Sr. Associate VP for Finance & Deputy Treasurer Joanne Wamsley

– They have (personally) reviewed the financial report– Report does not contain (material) untrue statements or omissions– Statements present the financial condition of results of operation

– Audit letter issued by State of Arizona Office of the Auditor General (pages 4 and 5)• Generally accepted accounting principles• Governmental Accounting Standards Board• Accrual accounting to appropriately allocate revenues and expenses to correct accounting period

Page references are from the ASU 2009 Financial Report.

You might be an accountant if:

• You had no idea that GAP is a clothing

store……..

Generally accepted accounting principles (GAAP)

• Rules, procedures and conventions guiding accounting and reporting practices.

• Uniform and consistent accounting standards ensure that ASU’s financial statements are fairly and consistently presented.

• Accounting and financial reporting standards for all state and local entities, including public colleges and universities are set by the Governmental Accounting Standards Board (GASB).

• ASU’s related organizations (ASUF, Alumni Association etc.) follow standards set by the Financial Accounting Standards Board (FASB).

Why is GAAP Important?

• CONSISTENCY. “Levels the playing field.” Ensures all organizations would record material transactions in the same manner. Also ensures activity is presented the same way across all accounting periods.

• RELEVANCE. Information in the financial statements should be appropriate to assist a person evaluating the statements to make educated guesses regarding the financial state of the organization.

• RELIABILITY. Information presented is reliable and verifiable by an independent party.– Organization is presenting a clear picture of what really happened during the period being reported.

• COMPARABILITY. Allows for comparison of financial statements to similar organizations.– Allows for a benchmark to show how an organization is doing compared to peers.

• Individual (departmental) instances of non compliance can lead to an increase in audit scope, which can delay the issuance of the Financial Report.

• If ever received, a negative audit opinion could potentially impact – state appropriations– enrollment numbers – level of oversight by State or ABOR– bond ratings for debt the University issues– ability to receive governmental grants – the ability to solicit gifts

Accrual Accounting

• Accrual accounting is the matching of revenues and expenses.

• Estimates are something used to record activity within the period.

• Related revenues and expenses should be recorded in the same period.

• If expenses are incurred in advance of the revenues being earned – the expenses should be deferred at year-end.

• If the revenue is earned but not all the expenses recorded, then outstanding expenses should be recorded (accrued) before the end of the fiscal year.

• Financial Services coordinates the year-end journal entries, including accruals, for the University.

• Accruals are reversed in the next accounting period so the activity is not recorded twice.

(State) Policy Making Entities Include

• STATE OF ARIZONA– State Statutes– General Accounting Office Policy Manual

• ARIZONA BOARD OF REGENTS (ABOR)– Policy Manual

• ASU ADMINISTRATION– Provost/Vice Presidents’ Offices– Policies and Procedures Manuals*– Accounting standards through Financial Services

• COLLEGES/DEPARTMENTS

*Note: Policy manuals are subject to updates/revisions and should be checked for current information.

State of Arizona – Laws and Policies• Misuse of public funds.

• Documentation of public purpose served.

• Gifting/Loaning of public funds.– No documented public purpose– Deficits in ASU accounts if funding is in ASU Foundation accounts– Employee overpayments

• Prepayments. – Standard industry practice (subscriptions, airline tickets)– Clear (documented) economic benefit - $

Must have preapproval from Purchasing & Financial Service (form)

• Travel policies.

• Prohibits unfair competition with private enterprise.

• Prohibits student support to be paid for with state general fund appropriations.

State of Arizona Code of Conduct

Covers State of Arizona employees whose responsibilities include the administration of public monies.

• Integrity

• Competence

• Professional Conduct

• Conflict of Interest

State of Arizona Code of ConductFor Employees Engaged in Accounting, Financial and Budgeting Activities

The Chief Financial Officers of the Agencies of the State of Arizona are financial and accounting professionals committed to promoting the highest standards of personal ethics, competence and professional conduct. Therefore, we embrace the following moral, ethical, legal and professional standards as the minimal values to be exhibited by those in Arizona Government engaged in

accounting, financial and budgeting activities.

www.gao.az.gov

Misuse of Public MoniesArizona Revised Statutes § 35-301 (also FIN 124)

ARS § 35-302. Public money defined

Arizona Board of Regents Website

www.abor.asu.edu

ABOR Policy 3-412Technology and Research Initiative Fund

The TRIF will be used to support projects and initiatives that meet one or more of the following criteria:

• Promote university research, development and technology transfer related to the knowledge based global economy;

• Expand access to baccalaureate or post-baccalaureate education for time-bound and place-bound students;

• Implement final recommendations from the Governor's Task Force on Higher Education and/or the Arizona Partnership for the New Economy.

• Develop programs that will prepare students to contribute in high technology industries located in Arizona.

TRIF is generated from part of a 0.6% education sales tax approved by Arizona voters in November 2000 as part of an economic development strategy for the State.

Primary Use for TRIF at ASU is the Biodesign Institute. » Fiscal 2009, ASU received $23.7 million in TRIF revenues.

ABOR Policy 4-105Special Class Fees and Deposits

• Special class fees and deposits must be imposed only for expenses that are necessary for the successful completion of course objectives.

1. Off Campus Field Trips or Specialized Equipment/Facilities Use.– Group travel costs such as gas and mileage reimbursements. Food only in remote areas.

2. Private Instruction.– One on one study with an instructor in special areas of study, such as music performance.

3. Expendable Materials.– Specialized in nature and not readily available– Significant cost savings to students by departments purchasing in large quantities.– Materials that must conform to certain specifications and be identical for all students.– Expensive materials that could not economically be normally purchased

4. Technology Expense Fees.– Course-specific, beyond normally expected services, as defined by each University.

5. Selected Personnel Expenses.– Models hired for art classes for clinical practice classes. Musical accompanists for music and dance

classes for classes requiring them.– Supervisory instruction (including travel costs) for in-context training classes such as on-site student

teaching; social work practicum (field experience); and nursing clinical experience.6. Deposits.

– For expensive equipment or apparatus that is temporarily entrusted to student’s care.– Deposit must be fully refundable upon return of equipment which in satisfactory condition

ABOR Directive Regarding Fiscal Responsibility

The Arizona Board of Regents have indicated a desire for stringent personnel actions for those that intentionally or flagrantly misuse or mismanage financial transactions, or do not follow financial policies and procedures.

Sanctions for the violator’s supervisor, or others with oversight responsibilities are possible.

State of Arizona - Auditors Scope• The State of Arizona Office of the Auditor General performs the annual financial audit

of ASU.– Preliminary work is typically May through June– Final work is typically September – mid November

• Items which formerly were ‘points for discussion’ have been raised to management letter comments.

• Increased the time span of audits as more comprehensive reviews are required by auditing standards.

• Advantage – ASU’s official system of record for financial transactions.– Auditors will ask for original source documents for all transactions in their audit

sample.– Put as much information as possible in Advantage document and description fields

• IMPACT ON ASU AREAS – THE BETTER DOCUMENTED YOUR TRANSACTIONS ARE THE FASTER WE CAN RESOLVE AUDITOR QUESTIONS.

Auditors’ Responsibility

• Auditors express an opinion on the financial statements.• Must obtain reasonable assurance that the financial statements are

free from misstatement.• Assess the accounting principles used for estimates and preparation

of the statements.• Conformity with GAAP.• Report on internal control.• Report on compliance with certain laws, regulations, contracts and

grants.

Note: The audit sample size is relatively small, so if ‘problems’ are identified in the sample, the scope of the audit size can be significantly impacted.

Point of Contact for Auditors

• Entrance conference is held with Financial Services.

• Downloads of all individual transactions are provided to the auditors.

• Auditors provide a list of sample transactions to Financial Services, or Human Resources.

• Draft financial statements are prepared by F/S and audited by the Auditor General’s Office.

• Departments are typically not directly contacted by the Auditor General’s staff, however for FY10 for the payroll sample, the AG’s Office is going to each department included in the payroll sample in order to review the departments payroll reconciliation and leave reporting procedures.

ASU Financial Services serves as the bridge

between the State of Arizona’s Office of the

Auditor General staff and ASU departments for the

annual financial audit.

Financial Services Contact Information

• Current Financial Services website (www.asu.edu/fs/)

• Accountant as shown on Advantage Reports

• Financial Services contact numbers –

phone 480.965.3601

fax 480.965.2683

ASU Policies and Procedures Manuals

Public Funds (Public Monies) at ASU

• Once deposited in an ASU account monies becomes public funds. This includes all ASU revenues. Examples are gifts, program fees revenues, sales and services revenues from external customers, indirect cost recoveries.

• Gifts to ASU can not be returned to the donor without the approval of the ASU Office of General Counsel.

• ASU public funds can not be deposited at the ASU Foundation - or transferred to ASU Foundation accounts.

FIN 129: ENSURING FINANCIAL INTEGRITY

FIN 203: ORG MGR RESPONSIBILIES

1. Authorize appropriate account signers2. All transactions on account are appropriate. There is sufficient indication of the public purpose served.3. Has primary and ultimate responsibility for sound internal controls in regards to account(s)4. Monitor adherence by their staff to university policies and procedures5. Control spending so deficits do not occur6. Determine timely funding sources for any agency/org deficits.7. Do not allow accounts to be in deficit if funding is available at related organizations (ASU Fdn)8. Adhere to Financial Services Policies & Procedures9. Designate another person as org manager if transferring to another position on campus or leaving ASU10. Review monthly Advantage reports to determine that all charges are appropriate. The monthly expense review

should also include the use of Dashboard Reports or other resources as necessary to verify salary/wage expenses for each employee.

11. Contact Financial Services accountant, or Grants and Contracts accountant, if clarification is needed.

12. Ensure any lobbying related expenses has appropriate approval 13. Ensure capital expenses are appropriate/needed14. Awareness of conflict of interest policy; university policy & ARS 38-501 to 51115. Signature stamps are not appropriate on documents obligating the University to expend funds.16. Restrict personal use of university resources. If it does occur immediate reimbursement is required.17. Contact Financial Services for guidance on sales tax issues related to departmental sales of goods/services.18. Contact Financial Services to close accounts which are no longer needed.19. Ensure ASU Foundation accounts are used appropriately.20. Makes all payments to nonresident aliens through ASU account, not financially affiliated organization.21. Obtains fingerprint checks from appropriate faculty or staff.22. Ensure all vendors are allowable per U.S. Dept. of Treasury Specially Designated Nationals List23. All federal funds are to be deposited with Sponsored Projects, (with the exception of federal financial aid)

FIN 210: BUSINESS MGR RESPONSIBILITES

FIN 112: ACCOUNTING ASSISTANCE

• For questions not answered by FIN, or if there are specific financial transactions concerns, departmental personnel should contact:

• Their college/department business manager

• Provost or vice president’s office financial administrator

• Financial Services accountant or higher level position within Financial Services

• If needed/appropriate, Financial Services will ask for the opinion of Morgan Olsen – Executive Vice President, Treasurer and CFO

University Revenues

• FIN 300 – Deposits of University Funds.• University funds can only be deposited into ASU accounts associated

with approved bank accounts.• Timely depositing.• Gifts to ASU (including gifts-in-kind) must be processed through the

ASU Foundation into ASU departmental accounts. ASUF issues official gift receipts.

• FIN 303 – Requires GIK transactions with donor provided appraisal of >$1M to be provided to the Sr Assoc VP Finance before it is recorded.

• FIN 308-01 – Overall Revenue Coding Structure.• Cash handling requirements.• Timely invoicing of revenues due. External/Internal.• Matching of revenues to expenses.• Year End Accruals/Deferrals. Revenue earned in a fiscal year must be

recorded in that fiscal year.

Every transaction must be supported!

FIN 119: PUBLIC PURPOSE SERVED

• In order to fulfill ASU’s fiduciary requirements, Financial Services requires that the public purpose be clearly documented on each payment transaction (including travel documents).

• Each document processed must have public purpose documented, unless it is readily apparent by the nature of the item.

(Each financial transaction should be able to stand alone during an audit, or contain the correct references. Appropriate documentation is essential.)

Expenses• Public Purpose Served – benefit to ASU (FIN 119)

• Appropriate supporting documentation.

• Even if we can do it, should we? Headlines test.

• Prohibited Transactions (FIN 401-03).

• Misuse of Public Monies (FIN 124).

• Payment for Services. Contract signed by someone with authority? PUR 202 – Contract Signature Authority.

• Personal Use of University Resources (FIN 117)

Don’t – but if you do, reimburse ASU immediately.

• Fiscal Year-End Closing (FIN 105)

FIN 401-02: PROVOST/VICE PRESIDENT/VICE PROVOST APPROVALS

Including:• Holiday celebrations• Live plant purchases• Employee awards > $100• Employee reimbursement > $1,000• Warehouse club memberships• Financial Services discretion

Any transaction requiring VP office approval should first have dean’s office/director approval.

• Gifts are prohibited.

• Awards are based on performance and/or objective criteria

• A public purpose is served in making the award

– Nonmonetary

• < $100 per person – No additional approval/reporting

• > $100 per person – Needs VP approval, must be reported to Human Resources

– Monetary/Cash Equivalents

• > $25 - must be paid through Human Resources

• > $1,000 – pre-award VP level approval

FIN 420-04: AWARDS VS. GIFTS

FIN 401-03: PROHIBITED TRANSACTIONS INCLUDE:

• Use of 12 or 15 Passenger Vans• Alcoholic Beverages• Bus and Light Rail Passes for

Personal Use• Direct Vendor Billings > $5,000

when PO is required• Fines and Penalties• Flowers, unless for official

University event - limited• Gifts, Contributions, Donations,

Advances, or Loans• Graduation Caps and Gowns• Internet Reimbursements• Legal Fees, unless approved by

General Counsel’s Office• Lost Key Charges

• Parking Decals for employees/ students (multi-campus duty assignment exception for 2nd

decal)• Payments Benefiting External

Organizations with no direct benefit to ASU

• Postage Stamps• Prepayments – form for exceptions

• Purchases from ASU Individuals• Refunds to Donors• Transfers of ASU revenues to off-

campus bank accts or other organizations.

• University Club Dues• Vendor Invoices > Two Fiscal

Years

Prohibited Transactions on State Accounts(may be allowable on local accounts)

• Awards, both students and faculty/staff.• Bottled water.• Student support payments (scholarships).• Food/Meals for employees unless in travel status.• Holiday celebrations.• Interviewee expenses.• Flowers. (In very limited circumstances flowers are allowed

on local accounts. Must have Financial Services pre-approval before purchasing with University funds.)

• Moving expenses.• Remodeling projects > $50,000.

Reference FIN 111: Charges to State Operating Agency/Orgs

Financial Information Sources

• Advantage Web Reports (updated nightly).

• Budget Position Control dashboard.

• Payroll Reconciliation Dashboards.

• MyReports.

• Data warehouse queries.

• Monthly Advantage Reports (available from Control D).

• Financial Services does periodic reporting that requires assistance from departments.

• Cash basis deficits

• ABOR updates (new)

• Quarterly budgeted accounts status

• Year-end audited financial reports

Colleges/DepartmentsPolicies & Procedures

• Can not conflict with higher level policies and procedures (State statutes, ABOR/ASU).

• Are more restrictive than university policy.

• At discretion of each college/department.

• Enforcement is at college/department level.

Closing Comments• Don’t depend on someone else to ‘catch’ a questionable transaction.

– Accounts Payable does not conduct a full ‘audit’ of each transaction.

• If you approve a document (on-line or hard copy) you are authorizing the payment.

– If you don’t want to be associated with the transaction should it become ‘public’, then don’t approve the document.

• Exceptions to policy can be given if the facts warrant it. But exceptions must be in writing from someone authorized to do so.

• Financial Services must be given full facts in order to accurately answer a policy question.

• When in doubt, ask.

• Any questions?

The End!

Accounting for Payroll Transactions

FY 2010

What’s New

• Change in AZ Withholding Taxes

– All employees are required to complete the

Employee’s Arizona Withholding Percentage

Form (A-4) to comply with a change in AZ

income tax withholdings.

– Change will be effective on the July 2, 2010 pay

check.

What’s New

• Withholdings had previously been calculated as

a percentage of federal income tax withheld.

The new mandate is to withhold AZ state

income tax based on a percentage of gross

taxable wages.

• Deadline to submit the form is June 15th.

Employees that do not submit a form by June

15th will have their AZ withholding set up at

2.7%.

What’s New

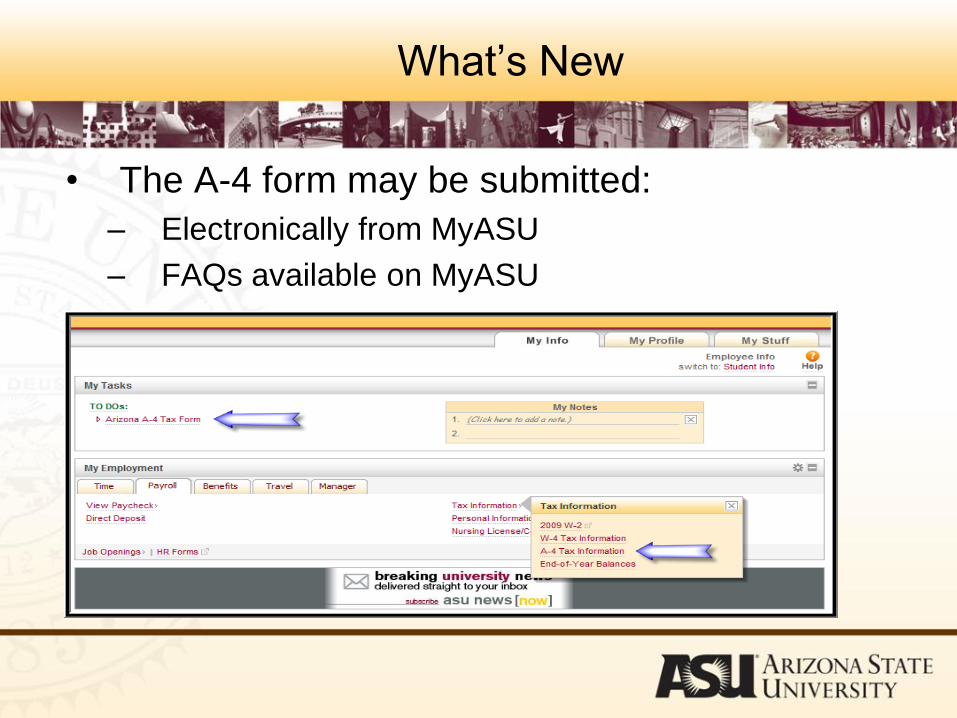

• The A-4 form may be submitted:

– Electronically from MyASU

– FAQs available on MyASU

What’s New

• The A-4 form may be submitted:

– Using a paper form. The form can be found

at www.asu.edu/hr/forms

• A-4 (USE ONLY FOR WAGES

PAID AFTER JUNE 30, 2010)

What’s New

• The new Hiring Incentives to Restore Employment

Act (HIRE) Act is a $17.5 billion jobs bill that allows

ASU and other employers to qualify for two new tax

benefits for hiring new employees who have been

unemployed for 60 days or more.

• Please help us take advantage of this opportunity by

making sure new employees hired between Feb. 3,

2010 and Jan. 1, 2011 fill out the 2010 HIRE Act

Employee Affidavit and return it by fax to payroll at

480.993.0554.

What’s New –ERE Rates

What’s New –ERE Rates

• Non-Benefits Eligible Rate- Originally included

employees in Benefit Programs OTH. Effective

for FY 2011 employees in the LMT Benefits

Program will also be charged at the Non-

Benefits Eligible rate. If an employee has

multiple jobs with one job in Benefit Program of

OTH or LMT and an additional job in another

Benefit Program, the employee will be

considered benefits eligible and charged ERE

based upon the Employee Class.

What’s New –Coding of RA/TA Tuition

Remission

• Tuition remission charges on flat rate accounts were

originally charged to student support, 7700.10 and

7700.11. Charges on these codes were exempt from

IDC and ASC.

• A change has been made retroactive to July 1, 2009 to

re-code flat rate tuition remission charges to employee

related expenses, 7200.48 and 7200.49.

• Codes 7200.48 and 7200.49 have been exempted from

IDC on Sponsored Accounts.

What’s New –Coding of RA/TA Tuition

Remission

• The recoded transactions on non-sponsored accounts

will be manually credited for the related ASC. The ASC

exemption for non-sponsored accounts will be effective

for FY 2010 and FY 2011.

• The re-coding was necessary to correctly record these

charges as an employee related expenses for the

Annual Financial Report.

Tracking Payroll Expenses in Advantage

• Payroll transactions interfaced to Advantage

are posted as summarized transactions.

Gross Pay Expenses

Gross Pay is posted to Advantage every Friday.

ERE Expenses

ERE Encumbrances on Sponsored

Accounts

• ERE encumbrances are calculated using

the most recent on-cycle pay period.

• First a ERE percentage is calculated using

the most recent on-cycle gross pay

amount divided by the sum of the most

recent ERE and tuition remission

expenses.

ERE Encumbrances on Sponsored

Accounts

• This percentage is then applied against

the current pay period’s gross pay

encumbrance.

ERE Encumbrances on Sponsored

Accounts

• Gross Pay = $5,000

• ERE Expense = $1,600

• Tuition Remission =$685

• Gross Pay

Encumbrance=$4,000

ERE Percentage Calculation

• (ERE + Tuition)/Gross Pay = ERE

Encumbrance Percentage

• (1,600 + 685)/ 5,000= 45.7%

ERE Encumbrance

• Gross Pay Encumbrance x ERE

Percentage = New ERE

Encumbrance

• $4,000 x 45.7% = $1,828

ERE Encumbrances on Sponsored

Accounts

Payroll Expense Redistributions

• Payroll Expense Redistributions are used for the

following:

– Workstudy (system generated)

– Tuition Remission (system generated)

– Transfer gross pay, recode earnings codes and

recode close date (submitted by departments)

• The JV document number will begin with

P3 for all Payroll Expense Redistribution

Entries

Payroll Expense Redistributions

• The PeopleSoft Payroll Expense Redistribution

Transaction Number is referenced in the

Comment field which is also the JV Document

Description.

• Each Payroll Expense Redistribution

Transaction will create a separate JV.

• In PeopleSoft navigate to ASU

CUSTOMIZATION-ASU HCM CUSTOM—

POSITION MANAGEMENT—VIEW

REDISTRIBUTIONS

Workstudy

System

Generated

Tuition Remission

System Generated

Payroll Transfer

Submitted by

Department

Payroll Distribution Dates

Gross Pay and ERE Expense Detail

• MyReports HR Expenditures Query

– http://www.asu.edu/it/eds/welcome.html

Use the MyReports HR Expenditures Query to view detail Gross Pay and

ERE Expenses

Choose the Query Salaries, Wages and ERE Query

1. Click on the PROCESS button

2. Two filter boxes will pop up one after the other, enter your account

number. USE UPPER CASE LETTERS

Once the query has run, create a new Pivot Table to view Gross Pay

and ERE by pay period.

Drag and Drop the Fields you want in your Pivot table. In this example we

used Pay Period End Date, Name, Account Number, Transaction Number,

Expenditure Code and Amount.

Gross Pay and ERE Detail

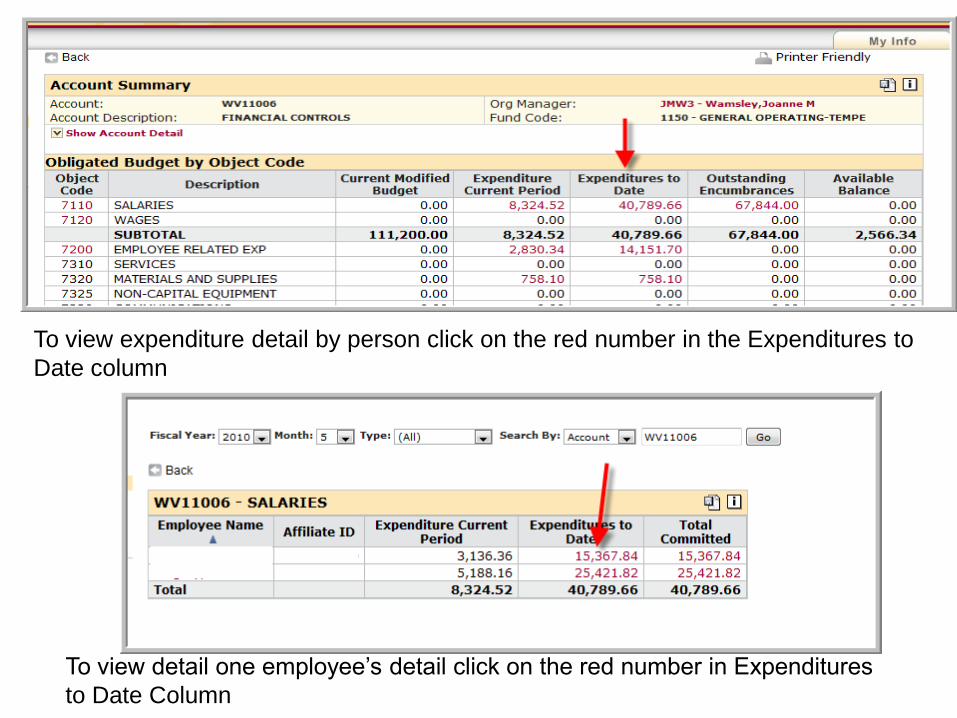

• Dashboard Financial (Super Report)

– http://www.asu.edu/dashboard/

Go to the ASU Dashboard website on click on Financial Super Report

Choose your search criteria and click on the GO button

To view expenditure detail by person click on the red number in the Expenditures to

Date column

To view detail one employee’s detail click on the red number in Expenditures

to Date Column

This screen will show you the expenses for the current pay period and prior

pay period for the selected employee.

Gross Pay Encumbrance Detail

• PeopleSoft

– Navigate to ASU Customizations-ASU HCM Custom-ASU

Position Management-Commit Acctg Cross Ref

Enter the Account Number

Gross Pay Encumbrance Detail

• MyReports

– http://www.asu.edu/it/eds/welcome.html

Choose the HR Encumbrances Query

1. Click on the Process button

2. Enter Fiscal Year and Account Number in the Filter Boxes

The query results will provide CURRENT encumbrance balances.

Gross Pay Encumbrance Detail

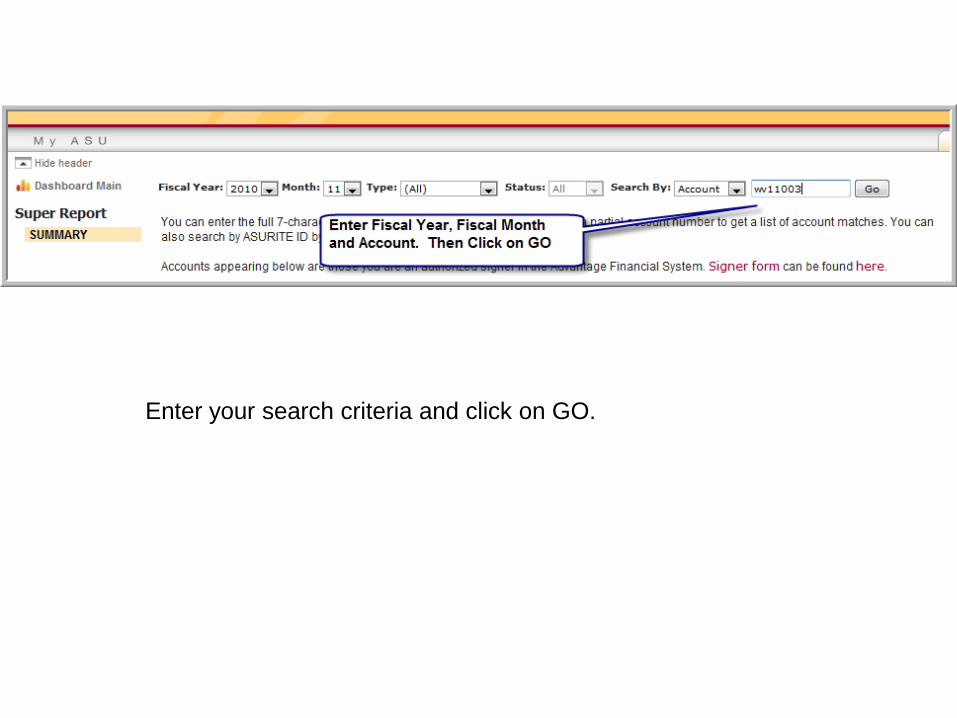

• Dashboard Financial (Super Report)

• http://www.asu.edu/dashboard/

Go to the ASU Dashboard website on click on Financial Super Report

Enter your search criteria and click on GO.

Click on the Object Code to View Encumbrance Detail by person

Encumbrance Detail by Person

Additional Training Classes

Sign up for Training on the LMS Website

• http://www.asu.edu/hr/training/

– Payroll Redistributions

– Payroll Reconciliation

– EPM: Introduction to My Reports

– EPM: Intermediate My Reports

Fi l 2010 Ad t YFiscal 2010 Advantage Year End Close: Who, What, When,End Close: Who, What, When,

Where, and How

May 2010 ASU Financial Services

WHO IS IMPACTED?

• Anyone with oversight or other fiscal responsibility for Advantage accounts should be aware of the fiscal year end close process.

• All fiscal year accounts close at the end of the fiscal year – and begin the new fiscal year with no revenue or expenditure activitybegin the new fiscal year with no revenue or expenditure activity (with the exception of local accounts’ balance forward).

• Multi-year accounts (for example Sponsored Accounts and• Multi-year accounts (for example Sponsored Accounts and Summer Sessions) have roll-over activity from one year to the next, but do not ‘close’ out activity at the end of a fiscal year.

ASU Financial Services

WHAT IS THE DIFFERENCE BETWEEN A FISCAL YEAR ACCOUNT AND A MULTI-

YEAR ACCOUNT?• A fiscal year account records activity specific for a fiscal year. Its revenues and

expenditures are all received or expended in one fiscal year. Examples of fiscal year accounts are state accounts (WV11003) , local accounts (WV51006), and auxiliary accounts (BD21001).auxiliary accounts (BD21001).

• Multi-year accounts record revenues and expenditures for a period of time other than a specific fiscal year. It may be for several years – in the case of

d t t fi l i th fsponsored grant accounts, or a non-fiscal year – in the case of summer sessions accounts. The activity for these accounts includes inception-to-date transactions that show activity since the account was established through the current date – or until its close date.

ASU Financial Services

WHAT IS A FISCAL YEAR?

• A fiscal year is the 12 months that represent a year of activity for that business or organization. Many companies have a fiscal year that is the same as a calendar year (January 1 through December 31). The U it d St t f d l t h fi l f O t b 1United States federal government has a fiscal year of October 1 through September 30. Many educational institutions (including ASU) have a fiscal year of July 1 through June 30.

ASU Financial Services

WHY DOES ASU HAVE A JULY TOWHY DOES ASU HAVE A JULY TO JUNE FISCAL YEAR?

• ASU is an agency of the State of Arizona and therefore has the same fiscal year as the State.

ASU Financial Services

WHY DO WE CLOSE A FISCAL YEAR?

• State budgets are allocated for a fiscal year, and expenses must be reported at the end of the fiscal year.

• The University is required to produce audited financial statements based on a fiscal year (12 months) of activity.

ASU Financial Services

AT JUNE 30TH HAVE ALLAT JUNE 30 HAVE ALL TRANSACTIONS BEEN RECORDED?

YES for deposits - After June 30th no deposits through the Cashier’s Office will be recorded into Advantage accounts for the fiscal year that just ended.

And NO for other Transactions - The Advantage financial system will remain open to record or adjust fiscal year activity approximately through the third week of July We leave Advantage open so that wethrough the third week of July . We leave Advantage open so that we can more accurately record activity that has occurred through June 30 and to make accounting entries to properly account for any major outstanding items.

ASU Financial Services

WHAT HAPPENS IF I RECEIVE REVENUE IN JULY THAT BELONGS TO

THE PREVIOUS FISCAL YEAR?

• Contact your accountant in Financial Services. According to the accounting matching principle revenue should be recorded in the year it g g p p ywas earned. All revenues that were earned in fiscal 2010 but not actually received and deposited by June 30th should be recorded in your account by journal entry. Provide your accountant with the documentation they need in order to record the revenue in yourdocumentation they need in order to record the revenue in your account.

ASU Financial Services

WHAT IS THE MATCHING PRINCIPLE?• All expenses incurred in generating revenues must be recorded in the

in the same fiscal year as the related revenue.

ASU Financial Services

Matching Principle Example

• The English Department holds a conference on June 20. All registration fees have been deposited by June 30. An invoice for the facility rental was received July 7th, one day past the accounts payable d dli Wh t h ld th E li h D t t d ith th i i ?deadline. What should the English Department do with the invoice?

• The English Department should provide their Financial Services’ accountant with the invoice and Financial Services will create a journal entry to accrue the facility rental expense in fiscal 2010 so that allentry to accrue the facility rental expense in fiscal 2010 so that all conference revenues and expenditures are ‘on the books’ in the same fiscal year.

ASU Financial Services

WHAT HAPPENS IF I DON’T RECEIVE ALL MY OUTSTANDING ORDERS BY

JUNE 30TH?Never enter a receiver document in Advantage until the goods have Never enter a receiver document in Advantage until the goods have

been receivedbeen received!

If you have not received orders by June 30th –payment can not be made to the vendor using the ‘old’ fiscal year money.

In order to be a fiscal 2010 expense, goods or services must be received by ASU on or before June 30th.

ASU Financial Services

WHAT DATE DO I USE ON RECEIVERWHAT DATE DO I USE ON RECEIVER DOCUMENTS?

• Use the actual date the order was received. JULY 1st

is the last day to enter a Receiver Document in Advantage for orders received by JUNE 30th.Advantage for orders received by JUNE 30 .

• If you are entering the receiver in July for goods that ere recei ed b J ne 30 ENTER A JUNE 30were received by June 30 – ENTER A JUNE 30

DATE IN THE RECEIPT DATE FIELD. If you leave the date field empty, Advantage will populate the date fi ld ith th t (J l ) d t d th t illfield with the current (July) date and the payment will be processed in fiscal 2011.

ASU Financial Services

WHY IS THE DATE ON THE RECEIVERWHY IS THE DATE ON THE RECEIVER IMPORTANT?

• Arizona law prohibits state agencies from making prepayments for good and services. The receiver document is what tells Advantage it is OK to pay a vendor. Accounts Payable puts invoices on-line as they are received from vendors. Payment is made when both the receiver and invoice are in the system. If a receiver is put on-line before the goods are received –prepayment may occur.

ASU Financial Services

DATES ON OTHERDATES ON OTHER ADVANTAGE DOCUMENTS

• For Advantage transactions (Journal Entries, Expense Transfers, Transfers In and Out, Appropriation Changes, Receivers, Stores Orders, Payment Vouchers and Travel Claims) being processed for FY 2010, use the current date up through June 30 and after June 30 continue to use a date of JUNE 30, 2010 in the document date for all on-line Advantage

fdocuments. If the document date is blank, the document date will default to the current date.

• We currently have two fiscal years open so it is important that h d i d i hyou use the correct date in order to post your transaction to the

correct fiscal year.

PAYMENTS OF ANNUAL SERVICES

• Payment for subscriptions, dues, maintenance agreements, and other services covering a period of time generally should be made in the fiscal year in which service begins. However, if the period of service begins in July, payment may be made in the last quarter of the prior fiscal year.

ASU Financial Services

WHAT HAPPENS TO PURCHASE ORDERS IF THEY ARE NOT CLOSED

BY JUNE 30TH ?• Purchase orders still open at the time of fiscal year close will

automatically roll into the new fiscal year as encumbrances.

• On local accounts, purchase orders which have not closed will remain encumbered at the end of the fiscal year.

• On state accounts all encumbrances for prior year commitment items will remain encumbered at the end of the year. All other encumbrances will drop off state accounts before we close. NON-PRIOR YEAR COMMITMENT ENCUMBRANCES BEGINNON-PRIOR YEAR COMMITMENT ENCUMBRANCES BEGIN TO DROP OFF STATE ACCOUNTS THE NIGHT OF JULY 6th. THEY WILL AUTOMATICALLY RE-ENCUMBER IN FISCAL 2011.

ASU Financial Services

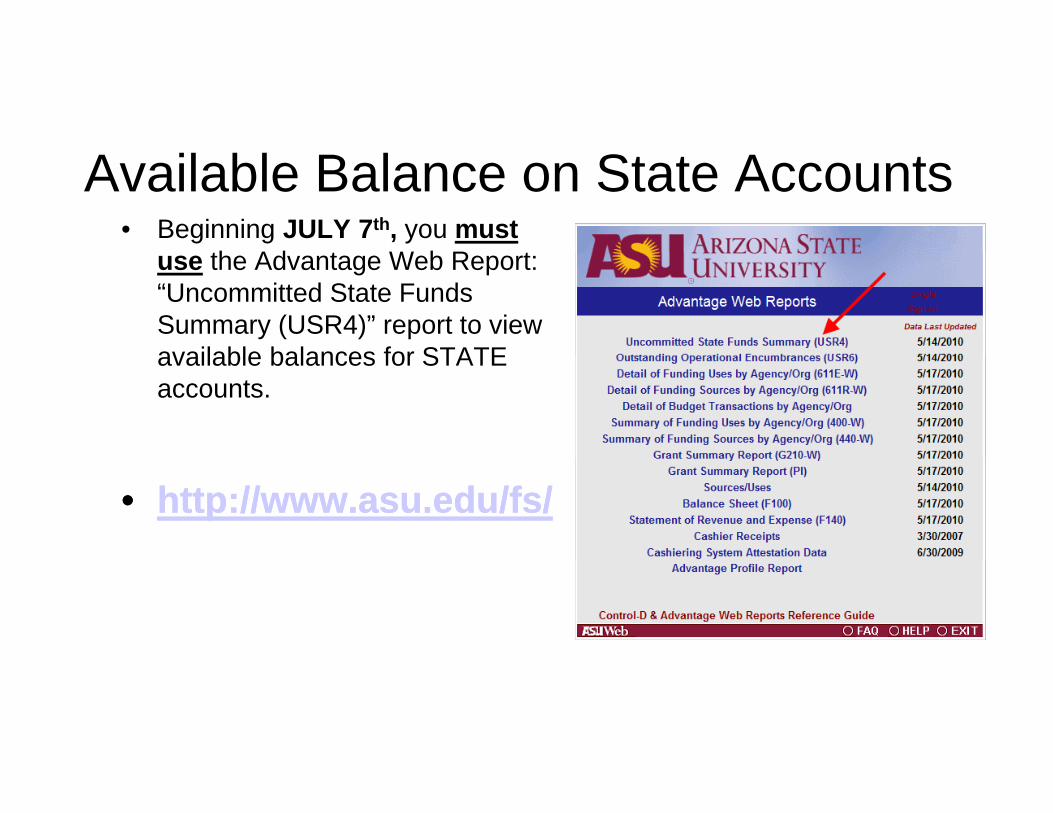

• Beginning JULY 7th, you must th Ad t W b R t

Available Balance on State Accountsuse the Advantage Web Report: “Uncommitted State Funds Summary (USR4)” report to view available balances for STATEavailable balances for STATE accounts.

•• http://www.asu.edu/fs/http://www.asu.edu/fs/

Available Balances on StateAvailable Balances on State Accounts

• As of July 7th the state balances on the Advantage APP2 screen are no longer accurate. Th APP2 ill t i l d b f• The APP2 screen will not include encumbrances for prior year commitments which remain encumbered at year end.y

• The Advantage Web Report “Uncommitted State Funds Summary (USR4)” report is the only report that will give you accurate state balances after Julythat will give you accurate state balances after July 6th, (July 6th is the day that purchase order encumbrances and travel encumbrances disencumber on state accounts)

WHAT ARE PRIOR YEARWHAT ARE PRIOR YEAR COMMITMENTS?

• Prior year commitments apply to state accounts only. They are primarily capital purchases or special projects that remain encumbered at year end and for which appropriation (budget) increases are recorded in the ensuing fiscal year.

ASU Financial Services

PRIOR YEAR COMMITMENTSPRIOR YEAR COMMITMENTS INCLUDE:

• Capital purchases coded to object code 78XX – and related non-capital items on p p j pthe same purchase order (PC external vendors) – $500 minimum for total purchase order.

• Internal ASU Purchase Orders with at least $500 in outstanding balance to the following vendors:

FACMAN– FACMAN– IT – SUNCARD (building security/access projects)– FURNITURE

CARPET– CARPET– ASUWFACMAN (ASU West Facilities Management)– ASUWIT (ASU West Information Technology Services)– BOOKSTORE (capital only)

ASUSTORES (capital only)– ASUSTORES (capital only)– CANON (capital only)– OFFICEMAC (capital only)– COMPUTING (EDP services only, must be coded to 731031)

• Soft encumbrances

ASU Financial Services

• Soft encumbrances

WHAT IS A SOFT ENCUMBRANCE?

• Again for state accounts only – this is a process that allows state accounts to encumber special items for long-term projects subject to approval by Financial Services.

• Departments must make a written request to their accountant indicating the circumstances that qualify their request as a soft encumbrance, include any supporting documentation such as invoices purchaseinclude any supporting documentation such as invoices, purchase order etc.

• Soft encumbrance requests must have appropriate approval by theSoft encumbrance requests must have appropriate approval by the Dean/Director and VP/Provost before being submitted to Financial Services.

ASU Financial Services

• FY2010 will require an additional approval by the Provost or Dr. Olsen.

WHAT HAPPENS TO THE FUNDS LEFTWHAT HAPPENS TO THE FUNDS LEFT IN MY STATE ACCOUNT?

• Balances for accounts within the same vice presidential area and the same campus are combined for a consolidated ending balance for the VP area. Any balances left in the VP area at the end of the fiscal year go to support overall university initiatives.university initiatives.

• Your state account begins the new fiscal year with the new year budget. Any uncommitted balance left in your old year state account will not roll over to the

t P i Y C it t ill ll ith th b d t i thnew year account. Prior Year Commitments will roll over with the budget in the new fiscal year. This entry is made after the original state budget load is completed.

• Every appropriate attempt should be made to expend your state funds by the end of the fiscal year. An expense means the payment has been made – and the funds are no longer available. Encumbrances show the need for funds – but indicates payment will occur in the future.

ASU Financial Services

HOW CAN I MAKE SURE I HAVE SPENT ALL OF MY STATE

APPROPRIATION?• Know what will expense this fiscal year, what will remain encumbered as a prior year

commitment, and what encumbrances will drop off before fiscal year close (and free up available balance).

• Make sure you account for payroll expenses for June 30th.

• If you are aware of operations encumbrances/travel encumbrances that will drop off – you need to act accordingly and have a plan in mind to expend these funds as they becomeneed to act accordingly and have a plan in mind to expend these funds as they become available. It is possible to temporarily overspend your state appropriation - if you are confident of what encumbrances will drop off as the roll over process begins.

• Once the purchase order rollover process begins the night of July 6th – Advantage tables such g g y gas the APP2 no longer reflect all transactions – you must use the web report (Uncommitted State Funds Summary , USR4) to track your state account balance starting July 7th.

ASU Financial Services

WHAT HAPPENS TO TRAVELWHAT HAPPENS TO TRAVEL ENCUMBRANCES AT YEAR-END?

• The night of July 6, 2010, outstanding travel encumbrances will disencumber on STATE accounts in fiscal year 2010 and will re-encumber in fiscal yearin fiscal year 2010 and will re encumber in fiscal year 2011. Once the disencumbrance occurs, the uncommitted balance in state accounts will increase – meaning you have more available funding.meaning you have more available funding.

• Remember to start using the web report Uncommitted State Funds Summary (USR4) Web report on July 7th.

• State accounts do not receive budget increases for travel encumbrances that roll over from the prior year. Expenses related to the rollover encumbrances will go against fiscal 2011 budget.

ASU Financial Services

WHAT IF A TRIP WAS COMPLETED IN JUNE, BUT I MISSED THE TRAVEL CLAIM

DEADLINE?• Contact your accountant in Financial Services. The accountant

MAY be able to process an accrual entry based upon the appropriate supporting documentation.

• (Generally we don’t process accrual entries for less than $500 -so please use some discretion before asking for an accrualso please use some discretion before asking for an accrual entry to be made.)

Feb 2006 ASU Financial Services

Payroll Expenses

• The Pay Period Ended June 27th is scheduled to post to Advantage on July 2nd as a fiscal year 2010 expense.

thJune 30th Payroll Expense

• We must record all payroll expenses from July 1 through June 30th in this fiscal year. The payroll expenses for June 28th through June 30th will be paidexpenses for June 28th through June 30th will be paid on the July 16th pay day. The three days of expenses for June 28th, 29th,and 30th will be recorded in Advantage as a fiscal year 2010 expense. Payroll accruals for June 28th, 29th, and 30th will post to departmental accounts on July 6th.p y

YEAR END CALENDAR

• The Advantage year end calendar is available at Financial Services web site:– http://www.asu.edu/fshttp://www.asu.edu/fs– Click on: Advantage Calendars– Then click on: Fiscal Year End 2010 Calendar

ASU Financial Services

Important Dates to Rememberp• June 21st – Deadline to process a P-Card Transaction for fiscal year 2010• June 30th – Deadline for deposits to Cashiering Services to process as FY10 revenue.• July 1st – Deadline for:

– RC documents (goods received by 6/30/2010)– Vendor Invoices for PC, SC, and PDLVPO– FY10 PVs to Accounts Payable– FY10 Travel Claims to Travel OfficeFY10 Travel Claims to Travel Office

• July 2nd – Deadline for Service Department II Billings• July 6th – Deadline for:

– PC and SC modifications (decreases only)FY10 PO PC SC PD d T l d t di b– FY10 PO, PC, SC, PD, and Travel documents disencumbrance

• July 7th – Begin using the web report Uncommitted State Funds Summary (USR4) to view available balances on state accounts

• July 7th – Deadline to enter FY 10 non-sponsored Payroll Expense• July 7 – Deadline to enter FY 10 non-sponsored Payroll Expense Redistribution Entries in PeopleSoft.

• July 9th – Departmental Deadline for FY10 A1,J1,IX and TV documents• July 16th – FY 10 Year End Close

ASU Financial Services

WHERE DO I GO TO FIND THEWHERE DO I GO TO FIND THE ADVANTAGE WEB REPORTS?

• Go to http://www.asu.edu/fs/– Click on Advantage Web Reports

• A Data Warehouse ID is required to use the web reports. To request a warehouse ID go to:

http://helptech.asu.edu/node/448

ASU Financial Services

Click on “Uncommitted State Funds Summary (USR4)” to track available balance on your state account(s).

ASU Financial Services

Enter your Advantage IDEnter an Account Number: You may use an agency/org or rollup agency/org (1RPXXXX)

ASU Financial Services

ASU Financial Services

Reminders

• In July, please use 06/30/10 date on RC, A1, J1, IX, TV, and PV documents to be processed in FY2010.

• Use the web report Uncommitted State Funds Summary (USR4) beginning July 7th to view available balances on state accounts.

ASU Financial Services

Year End Presentation

• A copy of this presentation is available on Financial Services’ website (Click on “What is Year End”):

http://www asu edu/fs/http://www.asu.edu/fs/

ASU Financial Services

What’s New for FY 2011?• Environmental Impact Fee – assessment to

all airfare expenses. (Rates are being determined )determined.)

• Driver’s License MonitoringDriver’s Authorization Form required to be on file– Driver s Authorization Form – required to be on file with OHR for reimbursements for mileage and car rental. This is in addition to job related use of a vehicle. For more information, see SPP 319 –Driver’s License Monitoring and EHS 119 – Motor Fleet Safety.y

What’s New for FY 2011?• Personal Services related assessmentsPersonal Services related assessments

– Netcom Fee – 1.1% assessed to Personal Services expenses (will not be charged to sponsored accounts)

– Risk Management – increasing from 1.45% to 1 55%1.55%

• Employee Related Expenses (ERE)– ERE Rates – increases in the following categoriesERE Rates increases in the following categories

Employee Category FY 2010 FY 2011Faculty 28.0% 25.5%S ff 3 0% 3 %Staff 34.0% 34.5%RA/TA 7.2% 7.5%

ADVANTAGE YEAR ENDCLOSE JULY 16, 2010

ASU Financial Services

WHO SHOULD I CONTACTWHO SHOULD I CONTACT IF I HAVE ANY QUESTIONS?

C t t Fi i l S i A t tContact your Financial Services Accountant

Tempe, Downtown, & West Campuses:p , , pJoshua Consier 5-2592 Jami Hovet 5-8951Julie Reeves 5-9288 Lynne Davis 5-7889Julie Miller 5 1921 Edalia Kousari 5 7428Julie Miller 5-1921 Edalia Kousari 5-7428Michael Mumpower 5-5072 Marilyn Mulhollan 5-7236Anthony Gallese 5-1922Liala Berger 7-8465

Polytechnic Campus:Polytechnic Campus:David Sittner 7-1044