business combinations. c012 business combinations uthe acquisition of an entire company...

TRANSCRIPT

Business Combinations

C01 2

Business combinations

The acquisition of an entire company Understanding the reporting benefits that

caused firms to favor the pooling method prior to July 1, 2001

Purchase accounting procedures at alternative prices

Pooling of Interests accounting procedures (appendix)

C01 3

Basic issues in combinations

The motivation to combine Pre-acquisition audit confirms value Every deal focuses on market values Asset acquisition versus stock acquisition

(investment)

C01 4

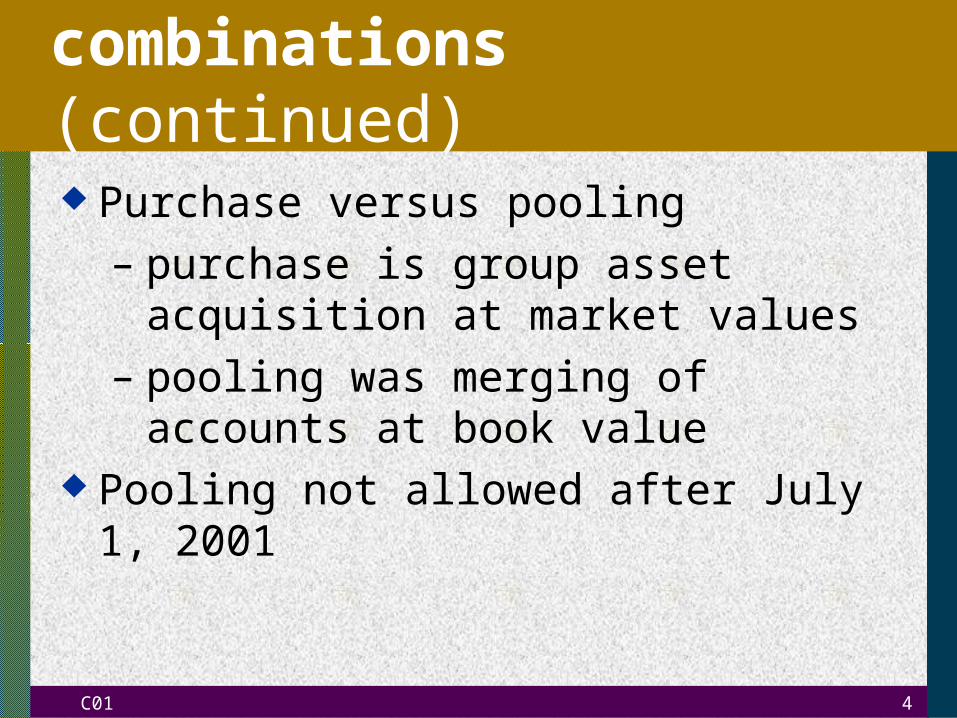

Basic issues in combinations (continued) Purchase versus pooling

– purchase is group asset acquisition at market values

– pooling was merging of accounts at book value

Pooling not allowed after July 1, 2001

C01 5

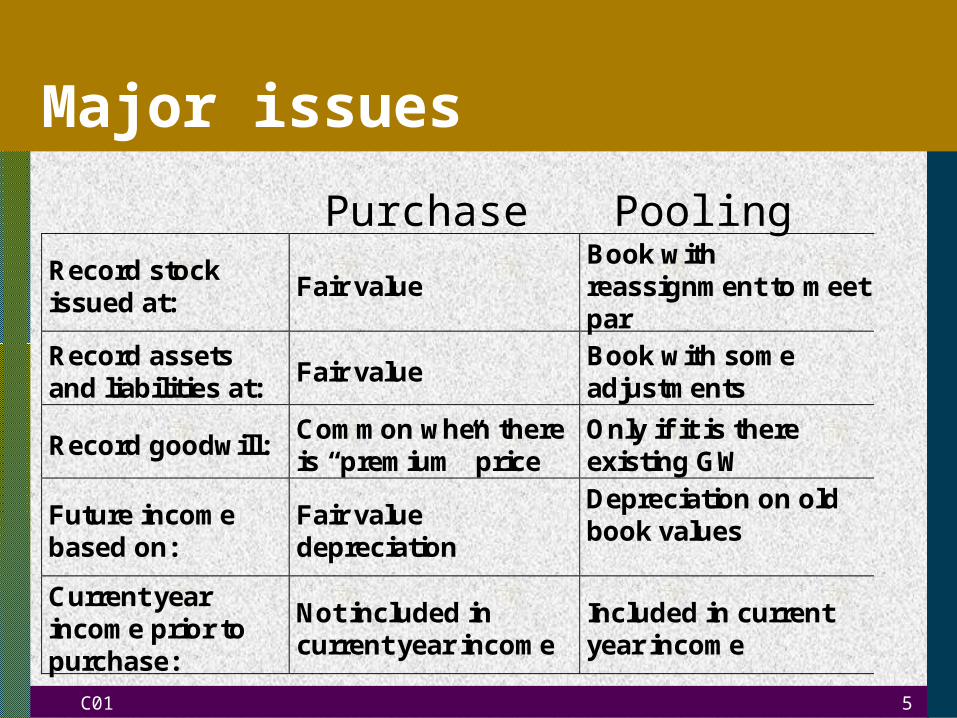

Major issues

Record stockissued at:

Fair valueBook withreassignment to meetpar

Record assetsand liabilities at:

Fair valueBook with someadjustments

Record goodwill:Common when thereis “premium” price

Only if it is thereexisting GW

Future incomebased on:

Fair valuedepreciation

Depreciation on oldbook values

Current yearincome prior topurchase:

Not included incurrent year income

Included in currentyear income

Purchase Pooling

C01 6

Prior period’sincome:

Not in prior yearcomparatives

Included in prioryear comparatives

Acquired firm RE:Not added to issuerbalance

Added to issuerbalance

Change inmethods:

Retroactive to priorperiods

Retroactive tooprior periods

Direct acquisitioncosts:

Add to price Expensed

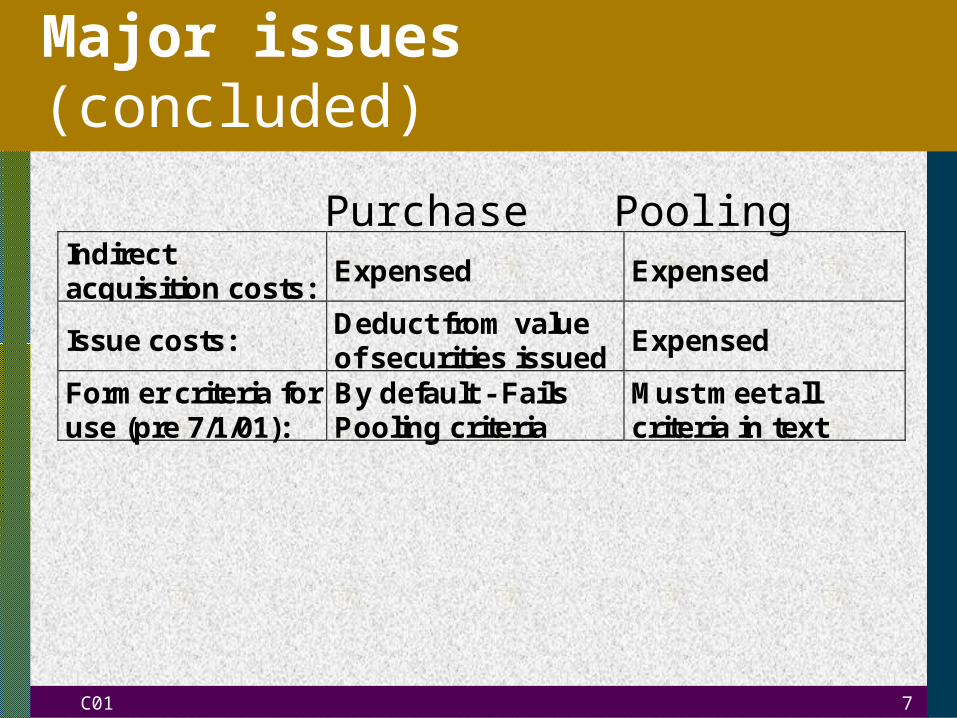

Major issues (continued)

Purchase Pooling

C01 7

Indirectacquisition costs:

Expensed Expensed

Issue costs:Deduct from valueof securities issued

Expensed

Former criteria foruse (pre 7/1/01):

By default - FailsPooling criteria

Must meet allcriteria in text

Major issues (concluded)

Purchase Pooling

C01 8

Purchase price rulesPremium Price - Price high enough to record all accounts at fair value, excess price is goodwill with no amortization, but required impairment testing

Bargain - Priority accounts at fair value, balance of price allocated to non priority accounts.

Extraordinary Gain - Price paid is less than priority accounts, excess of priority accounts over price is extraordinary gain.

C01 9

Priority accounts

All current assets All liabilities Deferred tax assets Pension and other post retirement benefit

plan assets Nonpriority assets that are to be sold

C01 10

Basic purchase example

Assets Liabilities & EquityInventory 120,000 Bonds payable 100,000Land 50,000 Common stock, $5 par 10,000Building 250,000 Retained earnings 310,000Total 420,000 Total 420,000

Fair Values:Inventory (priority) 170,000 Bonds pay (priority) 105,000Land 100,000Building 300,000Patent (unrecorded) 50,000

C01 11

Price zone analysis

1. Calculate the market value net assets:

• Using fair values, net assets = $515,000

C01 12

Price zone analysis (continued)

2. Determine the 3 price zones:• Premium: Over $515,000

all accounts at fair value, goodwill for price over $515,000

• Bargain: $65,000 [priority] to $515,000priority accounts at fair value; balance allocated to nonpriority accounts

• Extraordinary Gain: Below $65,000priority accounts at fair value; other accounts not recorded; extraordinary gain for excess of priority accounts over price paid

C01 13

Purchase entrypremium price: $600,000Inventory (fair value) 170,000Land (fair value) 100,000Building (fair value) 300,000Patent 50,000Goodwill (price over $515,000) 85,000

Bonds payable 100,000Premium on bonds payable (to fair value) 5,000Cash 600,000

Goodwill is not amortized, but could be impairment adjusted at a later date

C01 14

Purchase allocationbargain price: $365,000$65,000 for priority accounts; $300,000 allocated to fixed & identifiable intangible assets

Asset Market Percent Available AmountLand 100,000 22% 300,000 66,000Building 300,000 67% 300,000 201,000Patent 50,000 11% 300,000 33,000

Allocation Table

C01 15

Purchase entrybargain price: $365,000

Inventory (fair value) 170,000Land (allocated) 66,000Building (allocated) 201,000Patent (allocated) 33,000

Bonds payable 100,000Premium on bonds pay (to fair value) 5,000Cash 365,000

C01 16

Purchase entryextraordinary gain: $50,000Price is below $65,000; there is no value to assign to fixed or identifiable intangible assets:

Inventory (fair value) 170,000Land (no value available) 0Building (no value available) 0Patent (no value available) 0Extraordinary gain 15,000

Bonds payable 100,000Prem on bonds pay (to fair value) 5,000Cash 50,000

C01 17

Goodwill impairment

Test: Goodwill is impaired if estimated value of business unit is less that remaining book value of net assets (including goodwill).

New GW estimate = (estimated value of business unit) – (new estimate of identifiable net assets at fair value)

Impairment Loss = Book value of GW – new estimate.

C01 18

Impairment example

Recorded $100,000 goodwill in purchase three years ago. Now

Net assets at book value = $650,000

Fair value of the business unit = $625,000

Fair value net identifiable assets

(not including goodwill) =$580,000

C01 19

Impairment calculations

Test

Est. value of business unit $625,000Book value ofassets (includinggoodwill) 650,000Excess book $25,000Goodwill is impaired

Adjustment

Est. value of business unit $625,000Fair value ofident. assets,not incl. GW 580,000New GW est. 45,000GW bookvalue 100,000Impair. loss $55,000

C01 20

Purchase: some fine points

Direct acquisition costs are paid to outside parties; include them in the price paid

Indirect acquisition costs are internally incurred; they are expensed

Issue costs are to issue bonds or stock; they are subtracted from the value assigned to the securities

Stocks and bonds issued are always recorded at fair value in a purchase

C01 21

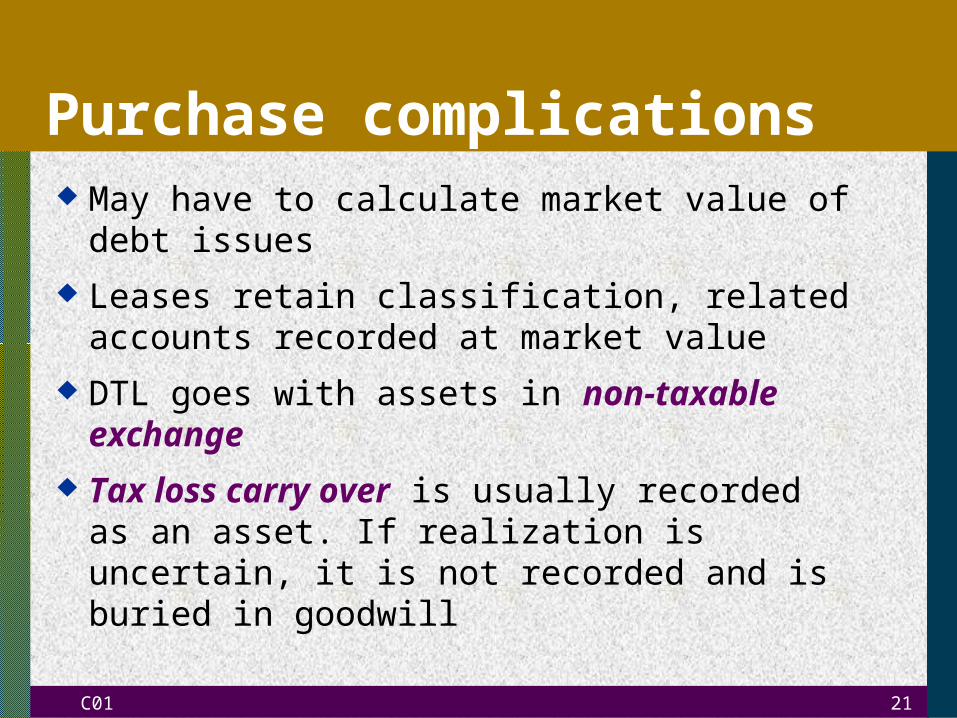

Purchase complications May have to calculate market value of debt

issues

Leases retain classification, related accounts recorded at market value

DTL goes with assets in non-taxable exchange

Tax loss carry over is usually recorded as an asset. If realization is uncertain, it is not recorded and is buried in goodwill

C01 22

Purchase complications (continued) There may be contingent goodwill

payment. Added goodwill is recorded Price guarantees cover decline in value of

securities issued in purchase. If issued, value assigned to securities is adjusted

C01 23

Example of tax-free exchange

The price paid for a company is $480,000 The only asset is a machine with a book value of

300,000 and a market value of $400,000 The tax rate is 40% A $40,000 DTL goes with the Machine The remaining price is $120,000 ($480 - $400 + $40) $120,000 is available for goodwill net of a 40% DTL Goodwill = $120,000 (1.0 - .4) = $200,000

C01 24

Tax-free exchange: journal entry

Machine (fair value) 400,000Goodwill (gross value) 200,000

Deferred Tax Liability* 120,000Cash 480,000

* $40,000 on machine and $80,000 on goodwill

The DTLs are amortized over the same life (and by the same method) as the assets to which they attach

C01 25

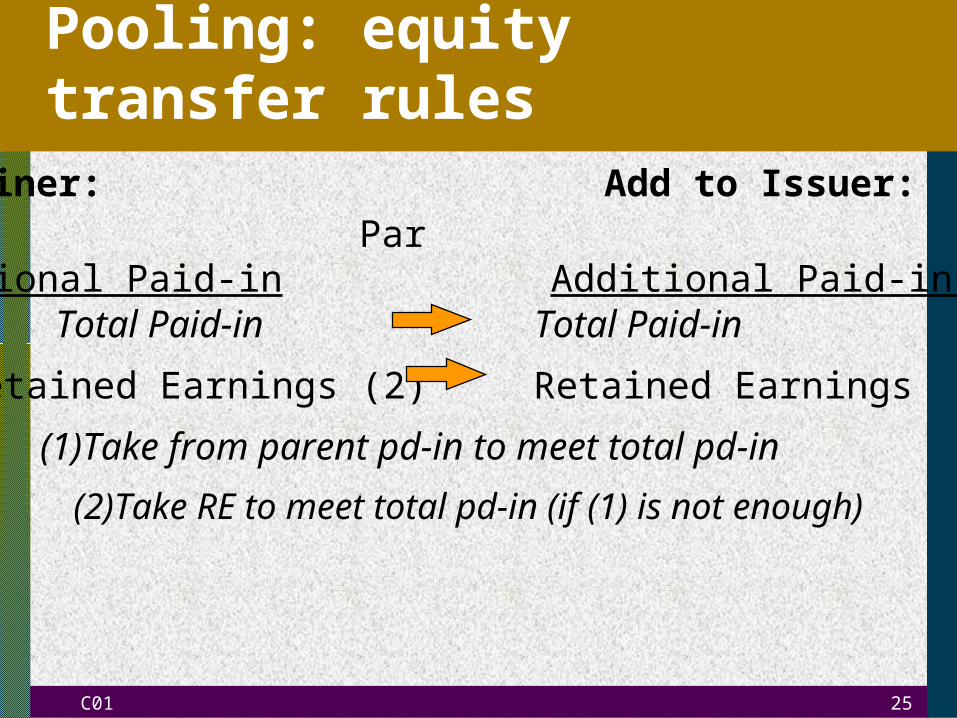

Pooling: equity transfer rules

(2)Take RE to meet total pd-in (if (1) is not enough)

Total Paid-in Total Paid-in

Retained Earnings (2) Retained Earnings

Combiner: Add to Issuer:Par ParAdditional Paid-in Additional Paid-in (1)

(1)Take from parent pd-in to meet total pd-in

C01 26

Pooling example

Assets Liabilities & EquityInventory 120,000 Bonds payable 100,000Land 50,000 C. stock, $5 par 10,000

Paid-in capital in excess of par 100,000

Building 250,000 Retained earnings 210,000Total 420,000 Total 420,000

Market ValuesInventory 170,000 Bonds payable 105,000Land 100,000Building 300,000Estimated goodwill 135,000

C01 27

Pooling analysis

Issuer will issue $50 market value shares to meet the $600,000 market value. $600,000 $50 = 12,000 shares issued.

The deal is based on market values; but they are not recorded!

The assets and liabilities are recorded at book value Pooling transfer rule is used to assign equity amounts Assume the following par values for shares issued:

$.50 $5 $10

C01 28

Equity transfer for $0.50 par

Common Stock 10,000 Common Stock* 6,000

Paid-in Capital Paid-in Capital

in Excess of Par 100,000 in Excess of Par 104,000

Total Paid-in 110,000 Total Paid-in 110,000

R E(adjusted) 210,000 RE 210,000

320,000 320,000

Combiner Add to Issuer

*12,000 shares, par $0.50

C01 29

Journal entry for $0.50 par

Inventory 120,000

Land 50,000

Building 250,000

Bonds payable 100,000

Common stock 6,000

Paid-in capital in excess of par 104,000

Retained earnings 210,000

C01 30

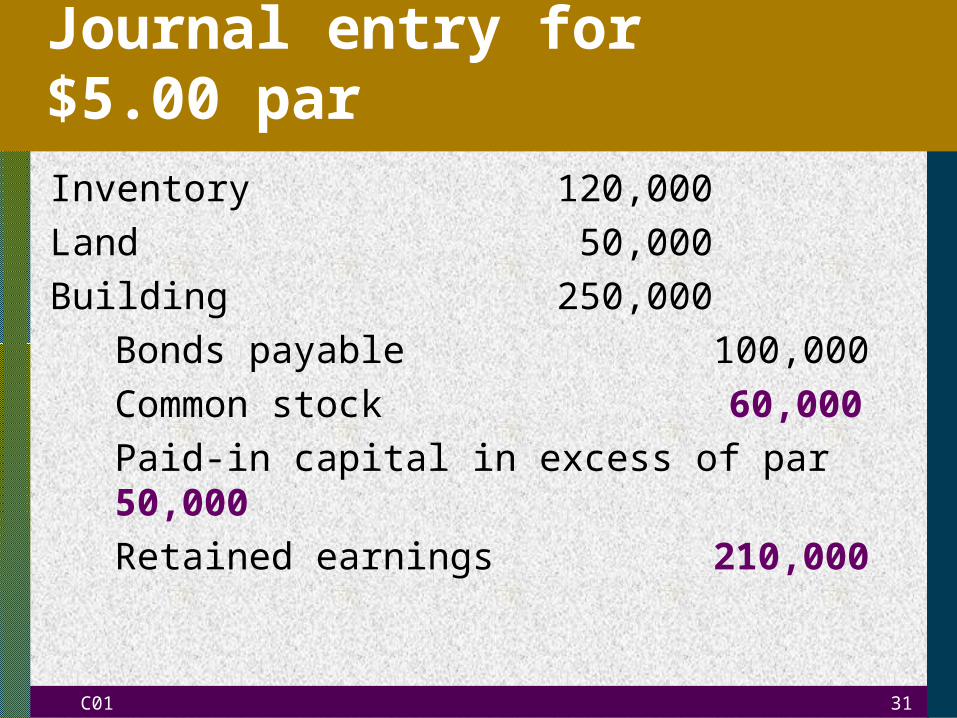

Equity transfer for $5.00 par

Common Stock 10,000 Common Stk* 60,000

Paid-in Capital Paid-in Capital

in Excess of Par 100,000 in Excess of Par 54,000

Total Paid-in 110,000 Total Paid-in 110,000

R E(adjusted) 210,000 RE 210,000

320,000 320,000

Combiner Add to Issuer

*12,000 shares, par $5.00

C01 31

Journal entry for $5.00 par

Inventory 120,000

Land 50,000

Building 250,000

Bonds payable 100,000

Common stock 60,000

Paid-in capital in excess of par 50,000

Retained earnings 210,000

C01 32

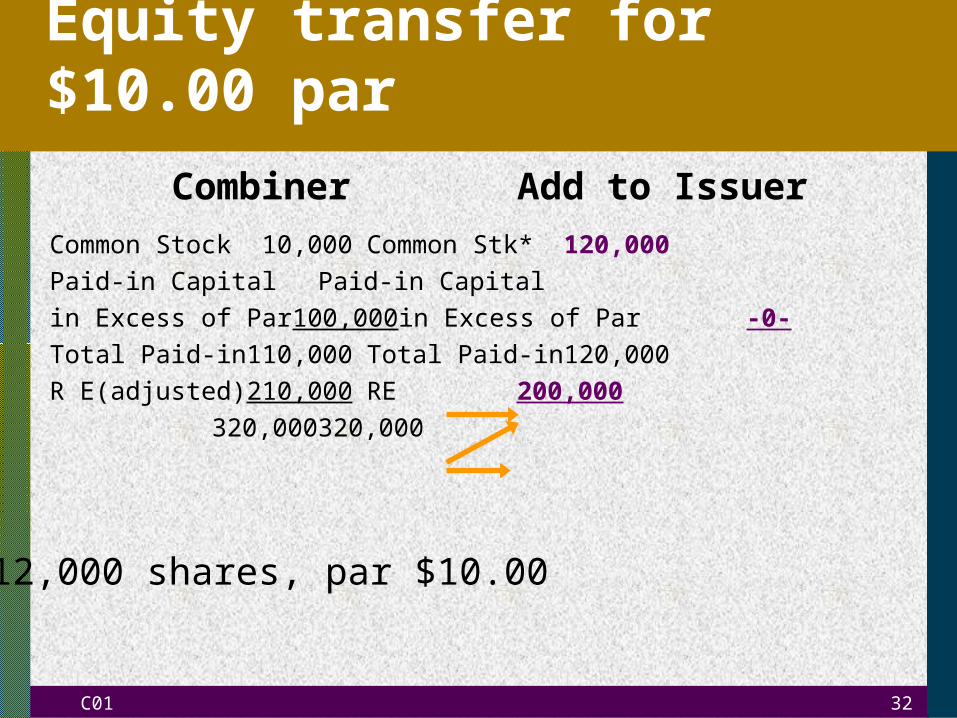

Equity transfer for $10.00 par

Common Stock 10,000 Common Stk* 120,000

Paid-in Capital Paid-in Capital

in Excess of Par 100,000 in Excess of Par -0-

Total Paid-in 110,000 Total Paid-in 120,000

R E(adjusted) 210,000 RE 200,000

320,000 320,000

Combiner Add to Issuer

*12,000 shares, par $10.00

C01 33

Entry for $10.00 par

Inventory 120,000

Land 50,000

Building 250,000

Bonds payable 100,000

Common stock 120,000

Retained earnings 200,000

C01 34

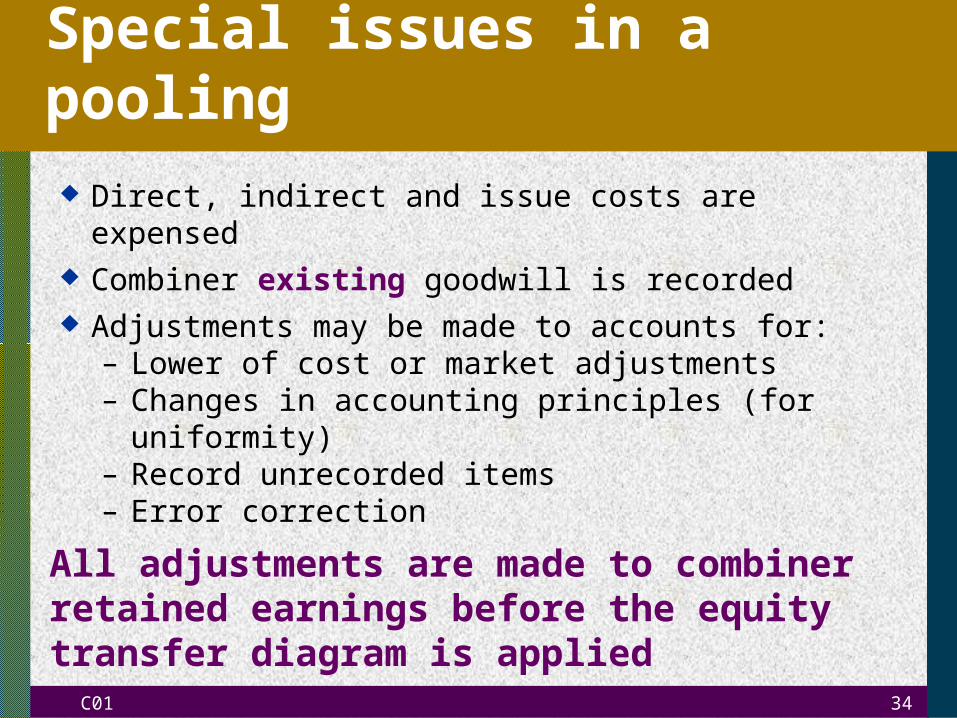

Special issues in a pooling

Direct, indirect and issue costs are expensed Combiner existing goodwill is recorded Adjustments may be made to accounts for:

– Lower of cost or market adjustments– Changes in accounting principles (for uniformity)– Record unrecorded items– Error correction

All adjustments are made to combiner retained earnings before the equity transfer diagram is applied