business and financial literacy for young...

TRANSCRIPT

BUSINESS AND FINANCIAL LITERACY FOR

YOUNG ENTREPRENEURS:

EVIDENCE FROM BOSNIA-HERZEGOVINA

Miriam Bruhn and Bilal Zia (World Bank, DECFP)

Introduction

What are the determinants of firm growth?

Much of the literature has focused on access to capital and external

finance (Banerjee et. al., 2009; De Mel, McKenzie and Woodruff, 2008)

Recent work argues that business management skills are another

important driver of firm growth and a key determinant of productivity

(Bloom, et. al., 2010; Bruhn et. al., 2010)

Academic interest is matched by a policy interest in training

programs that aim to enhance financial and business skills

But we know relatively little about what kinds of programs are

effective and for whom

Related Work and Contribution

Effects of financial literacy on households is limited (Cole, Sampson and Zia, 2010)

Evidence on business training is also scarce, though some studies are now coming through

Karlan and Valdivia (2010); Drexler, Fischer and Schoar (2010); Gineand Mansuri (2011); De Mel, McKenzie and Woodruff (2011).

Our contribution

Study effects of business training for current and prospective entrepreneurs, using a randomized controlled trial

Focus is not on micro-enterprises, but slightly larger firms

Complement survey data with high quality administrative loan data

Study Setting

Collaborate with a financial institution in Bosnia

(Partner) to provide business and literacy financial

training to their clients

Clients have a business loan

Look at young clients, age 18 to 35

Youth unemployment is 58 percent in Bosnia

Promoting creation, survival, and growth of youth-led

enterprises provides one possible solution to unemployment

problem

Business and Financial Training

Provided through a local NGO that has experience with business training for university students

Adapted content for loan clients based on client and loan-officer interviews, pilot training with university students

5 module basic course (2 days, 3 hours per day)

General concepts

Business plan

Marketing

Managing the firm’s finances

Business growth

Extra module on external finance (1 day, 3 hours)

Financing sources, importance of financial responsibility, interest rates, diversification, short term & long term, the devil is in the details

Experimental Design

Took 445 interested clients and randomly divided them into 3 groups

Treatment group 1 is offered 5 module course

Treatment group 2 is offered 5 module course plus external finance module

Control group

Stratified randomization based on Partner’s data and baseline survey data

Gender

Above and below median business and financial literacy score

Sector

Missing baseline profits, then sorted by profits within strata

Implementation Challenges

Low participation rate in the training (39%)

Main reason for not participating was lack of time

96% of participants would recommend training to a friend

Few people attended 6th module (external finance) In the analysis, combine both treatment groups

One third of clients did not have a business at baseline (they had an exploratory business loan)

Examine effect on business creation

For remaining analysis of business outcomes, keep only individuals who had a business at baseline

Baseline Data (Sample Characteristics)

Sample includes all 445 business loan clients

Sample includes the 267 clients who had a business at baseline

Female 0.35 0.35 0.98

Age 28.1 28 0.8

Completed secondary school 0.85 0.80 0.19

Risk averse 0.68 0.71 0.53

Treatment group

average

Control group

average

p-value of difference

(treatment – control)

Avg. employees 2.30 2.10 0.56

Avg. business age (yrs) 4.9 5 0.823

Registered 0.20 0.30 0.09*

Avg. monthly profits (KM, w/o outliers) 841.00 728.00 0.38

Services sector 0.541 0.463 0.23

Farming sector 0.20 0.25 0.3

Treatment Group Control Group p-value of difference

(treatment – control)

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

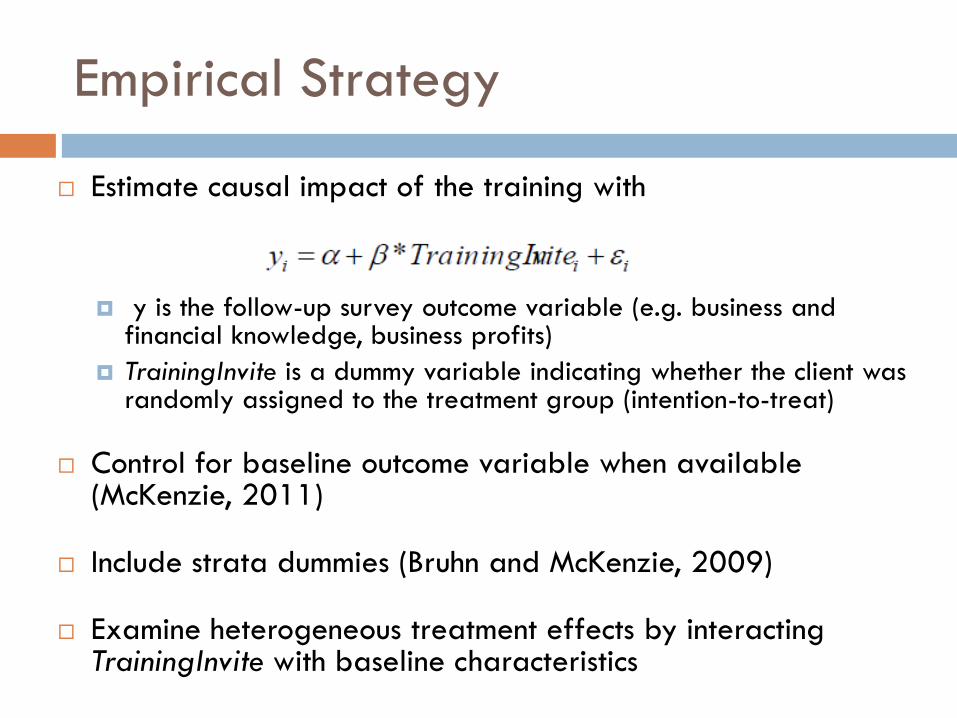

Empirical Strategy

Estimate causal impact of the training with

y is the follow-up survey outcome variable (e.g. business and financial knowledge, business profits)

TrainingInvite is a dummy variable indicating whether the client was randomly assigned to the treatment group (intention-to-treat)

Control for baseline outcome variable when available (McKenzie, 2011)

Include strata dummies (Bruhn and McKenzie, 2009)

Examine heterogeneous treatment effects by interacting TrainingInvite with baseline characteristics

Business and Financial Knowledge Scores

Find no impact of the training on average levels of business and

financial knowledge

But: the training significantly increased business and financial

knowledge among individuals with below median baseline levels of

business and financial knowledge

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

(1) (2)

Treatment -0.002 0.239*

(0.104) (0.131)

Treatment*Above median baseline financial literacy -0.248

(0.181)

R-squared 0.188 0.183

Observations 396 396

Mean of dependent variable in control group 1.129 1.129

Dependent variable: Business and financial knowledge score

Business Creation and Survival

No significant effect on the extensive margin (i.e.

business creation and survival)

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

(1) (2) (3) (4) (5)

Treatment -0.015 0.021 0.03 0.021 0.063

(0.053) (0.079) (0.027) (0.062) (0.099)

Treatment*Above median baseline fin lit -0.063 -0.074

(0.107) (0.128)

Treatment*Had business at baseline -0.004

(0.068)

Had business at baseline 0.645***

(0.055)

R-squared 0.089 0.089 0.409 0.115 0.117

Observations 396 396 396 267 267

Mean of dep. variable in control group 0.439 0.439 0.439 0.611 0.611

Dependent variable: Has business at follow-up

Business Practices

Treatment group is less likely than the control group

to use personal accounts for business

(1) (2) (3) (4)

Treatment -0.218*** -0.278** 0 -0.022

(0.079) (0.137) (0.063) (0.095)

Treatment*Above median baseline fin lit 0.095 0.034

(0.166) (0.129)

R-squared 0.287 0.289 0.146 0.147

Observations 169 169 170 170

Mean of dep. variable in control group 0.655 0.655 0.172 0.172

Dependent variable:

Uses personal

account for

business

Has credit card

for business

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Business Investment

Training led to more investment in the business

(1) (2) (3) (4)

Treatment 0.106** 0.087** 0.165*** 0.156**

(0.044) (0.047) (0.061) (0.077)

Treatment*Above median baseline fin lit 0.029 0.014

(0.079) (0.115)

R-squared 0.19 0.19 0.227 0.227

Observations 169 169 170 170

Mean of dep. variable in control group 0.017 0.017 0.121 0.121

Dependent variable:

Invests savings in

business

Implemented new

production

processes

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Business Performance

Evidence suggests that the treatment increased

profits by about 50% for clients with high baseline

levels of business and financial knowledge

(1) (2) (3) (4)

Treatment -65.828 -1485.965 0.051 -0.102

(837.310) (1,149.150) (0.080) (0.129)

Treatment*Above median baseline fin lit 2675.04+ 0.245+

(1,635.066) (0.162)

R-squared 0.179 0.202 0.084 0.099

Observations 108 108 170 170

Mean of dep. variable in control group 2642.162 2642.162 0.224 0.224

Profits May 2010 Increased profits

Dependent variable:

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Business Growth

The treatment increased sales for clients with high

baseline levels of business and financial knowledge,

no significant effect on employees (slower moving)

(1) (2) (3) (4)

Treatment 0.062 -0.115 -0.011 -0.116

(0.079) (0.127) (0.120) (0.239)

Treatment*Above median baseline fin lit 0.282* 0.169

(0.158) (0.274)

R-squared 0.067 0.087 0.306 0.308

Observations 169 169 170 170

Mean of dep. variable in control group 0.207 0.207 0.681 0.681

Dependent variable:

Increased sales Log employees

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

New Loans

Treatment group is not more likely than the control

group to take out a new loan from Partner (same is

true for loans from any source)

(1) (2) (3) (4)

Treatment 0.002 -0.006 -0.045 -0.118

(0.037) (0.055) (0.074) (0.120)

Treatment*Above median baseline fin lit 0.014 0.118

(0.075) (0.152)

R-squared 0.053 0.054 0.188 0.191

Observations 445 445 170 170

Mean of dep. variable in control group 0.169 0.169 0.759 0.759

Took out loan from

Partner after

training

Currently has

business loan from

any source

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Loan Characteristics

Treatment group clients who took out a new loan from

Partner have longer term loans (more installments) than

their peers in the control group

This is consistent with using loans for investment

(1) (2) (3) (4) (5) (6)

Treatment 0.429 603.03 4.939* 7.866*** -0.117 0.205

(849.055) (1,421.171) (2.865) (2.918) (0.645) (0.581)

Treatment*Above median baseline fin lit -1006.045 -4.886 -0.537

(1,760.976) (5.268) (1.165)

Control for loan amount Yes Yes Yes Yes

R-squared 0.2 0.205 0.537 0.544 0.452 0.453

Observations 80 80 80 80 80 80

Mean of dep. variable in control group 4392 4392 22.68 22.68 20.461 20.461

Dependent variable:

Loan amount Interest rateNumber of

installements

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Loan Default and Refinancing

The training lowered default rates among clients with low

baseline levels of business and financial knowledge

Some evidence that the training led to higher rates of

loan refinancing/restructuring

(1) (2) (3) (4)

Treatment -0.019 -0.048+ 0.034* 0.015

(0.018) (0.032) (0.020) (0.032)

Treatment*Above median baseline fin lit 0.052 0.034

(0.037) (0.040)

Control for loan amount Yes Yes Yes Yes

R-squared 0.041 0.044 0.09 0.091

Observations 3901 3901 3901 3901

Mean of dep. variable in control group 0.06 0.06 0.039 0.039

Dependent variable:

More than 30 days

past due

Refinanced or

restructured

Statistical significance levels: + 15%, * 10%, ** 5%, *** 1%

Summary and Conclusion

The business and financial literacy training had no effect on the extensive margin in our sample(firm creation or survival)

But: Individuals who already had a business tend to use better business practices and make more investments in their business due to the training

Weak evidence suggests that this increased profits and sales (for individuals with above median levels of baseline financial literacy)

Promising result for financial/business literacy advocates