burns affordability index™ (bai)

TRANSCRIPT

1See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

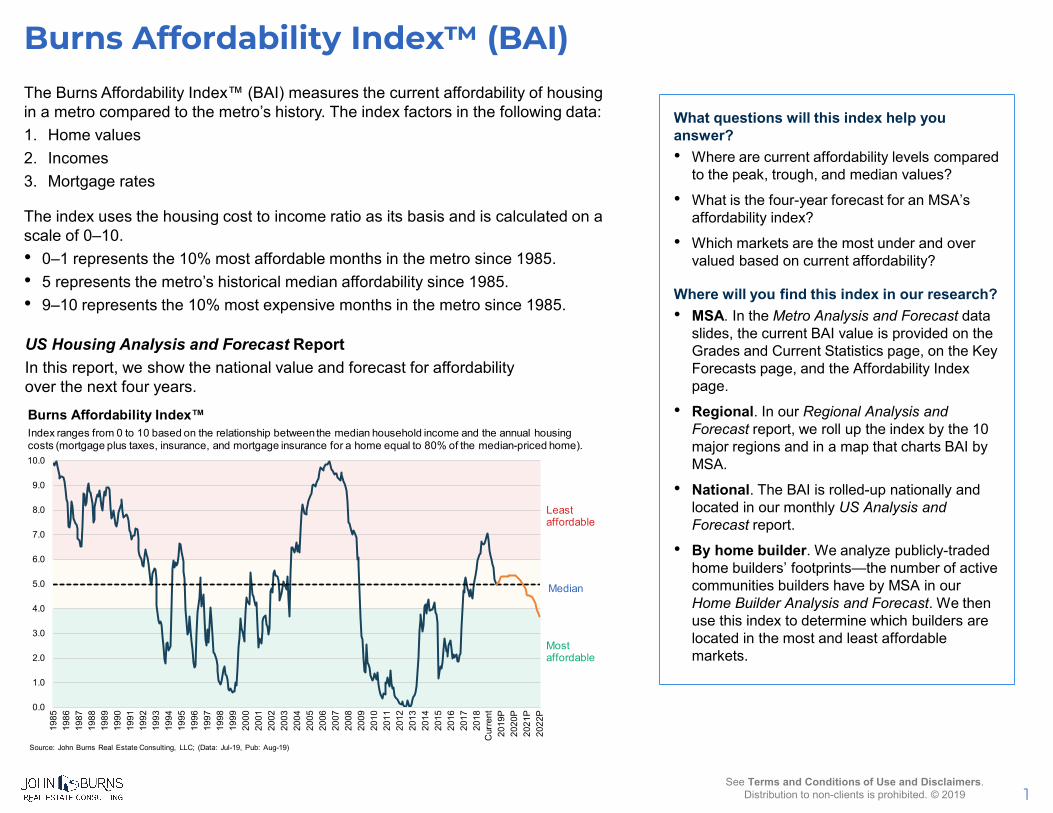

Burns Affordability Index™ (BAI)The Burns Affordability Index™ (BAI) measures the current affordability of housing in a metro compared to the metro’s history. The index factors in the following data:1. Home values2. Incomes3. Mortgage rates

The index uses the housing cost to income ratio as its basis and is calculated on a scale of 0–10. • 0–1 represents the 10% most affordable months in the metro since 1985.• 5 represents the metro’s historical median affordability since 1985.• 9–10 represents the 10% most expensive months in the metro since 1985.

What questions will this index help you answer?• Where are current affordability levels compared

to the peak, trough, and median values?

• What is the four-year forecast for an MSA’saffordability index?

• Which markets are the most under and overvalued based on current affordability?

Where will you find this index in our research?• MSA. In the Metro Analysis and Forecast data

slides, the current BAI value is provided on theGrades and Current Statistics page, on the KeyForecasts page, and the Affordability Indexpage.

• Regional. In our Regional Analysis andForecast report, we roll up the index by the 10major regions and in a map that charts BAI byMSA.

• National. The BAI is rolled-up nationally andlocated in our monthly US Analysis andForecast report.

• By home builder. We analyze publicly-tradedhome builders’ footprints—the number of activecommunities builders have by MSA in ourHome Builder Analysis and Forecast. We thenuse this index to determine which builders arelocated in the most and least affordablemarkets.

US Housing Analysis and Forecast ReportIn this report, we show the national value and forecast for affordability over the next four years.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Cur

rent

2019

P20

20P

2021

P20

22P

Source: John Burns Real Estate Consulting, LLC; (Data: Jul-19, Pub: Aug-19)

Leastaffordable

Burns Affordability Index™Index ranges from 0 to 10 based on the relationship between the median household income and the annual housing costs (mortgage plus taxes, insurance, and mortgage insurance for a home equal to 80% of the median-priced home).

Median

Mostaffordable

2See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

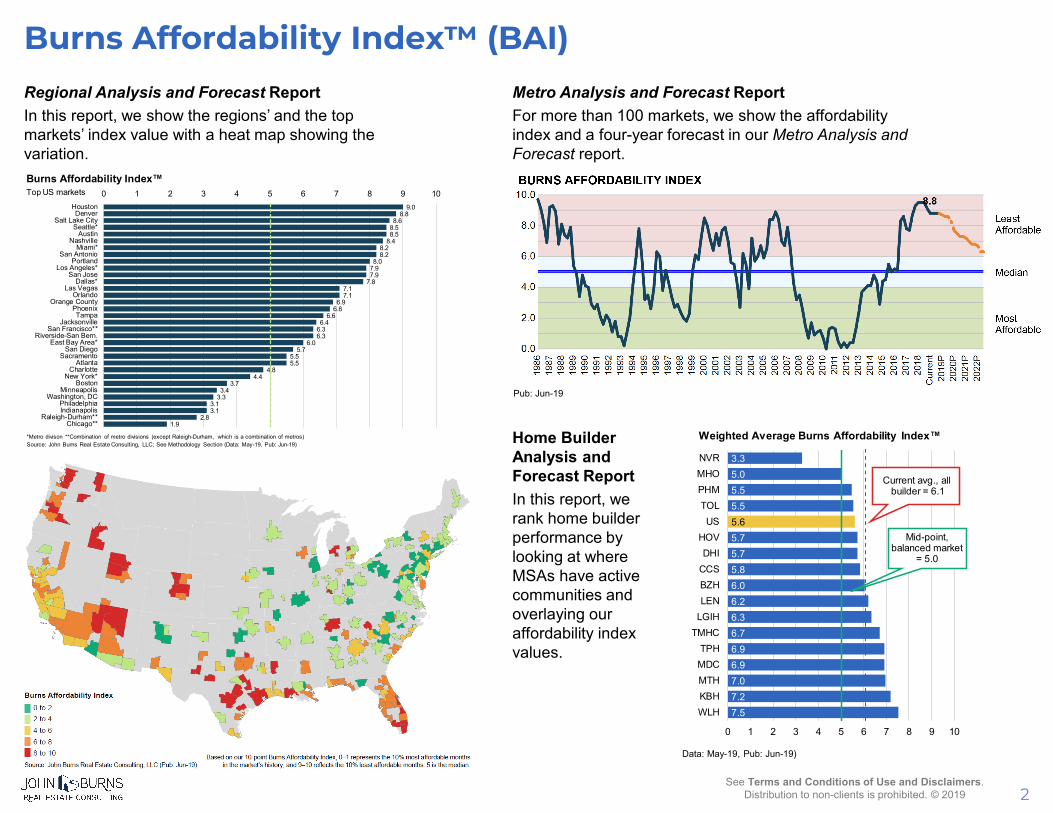

Burns Affordability Index™ (BAI)Regional Analysis and Forecast ReportIn this report, we show the regions’ and the top markets’ index value with a heat map showing the variation.

Metro Analysis and Forecast ReportFor more than 100 markets, we show the affordability index and a four-year forecast in our Metro Analysis and Forecast report.

Home Builder Analysis and Forecast ReportIn this report, we rank home builder performance by looking at where MSAs have active communities and overlaying our affordability index values.

7.57.27.06.96.96.76.36.26.05.85.75.75.65.55.55.03.3

0 1 2 3 4 5 6 7 8 9 10

WLHKBHMTHMDCTPH

TMHCLGIHLENBZHCCSDHI

HOVUS

TOLPHMMHONVR

Weighted Average Burns Affordability Index™

Current avg., allbuilder = 6.1

Mid-point, balanced market

= 5.0

Data: May-19, Pub: Jun-19)

9.08.8

8.68.58.5

8.48.28.2

8.07.97.9

7.87.17.1

6.96.8

6.66.4

6.36.3

6.05.7

5.55.5

4.84.4

3.73.4

3.33.13.1

2.81.9

0 1 2 3 4 5 6 7 8 9 10HoustonDenver

Salt Lake CitySeattle*

AustinNashville

Miami*San Antonio

PortlandLos Angeles*

San JoseDallas*

Las VegasOrlando

Orange CountyPhoenixTampa

JacksonvilleSan Francisco**

Riverside-San Bern.East Bay Area*

San DiegoSacramento

AtlantaCharlotte

New York*Boston

MinneapolisWashington, DC

PhiladelphiaIndianapolis

Raleigh-Durham**Chicago**

Source: John Burns Real Estate Consulting, LLC; See Methodology Section (Data: May-19, Pub: Jun-19)*Metro divison **Combination of metro divisions (except Raleigh-Durham, which is a combination of metros)

Burns Affordability Index™Top US markets

Pub: Jun-19

3See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

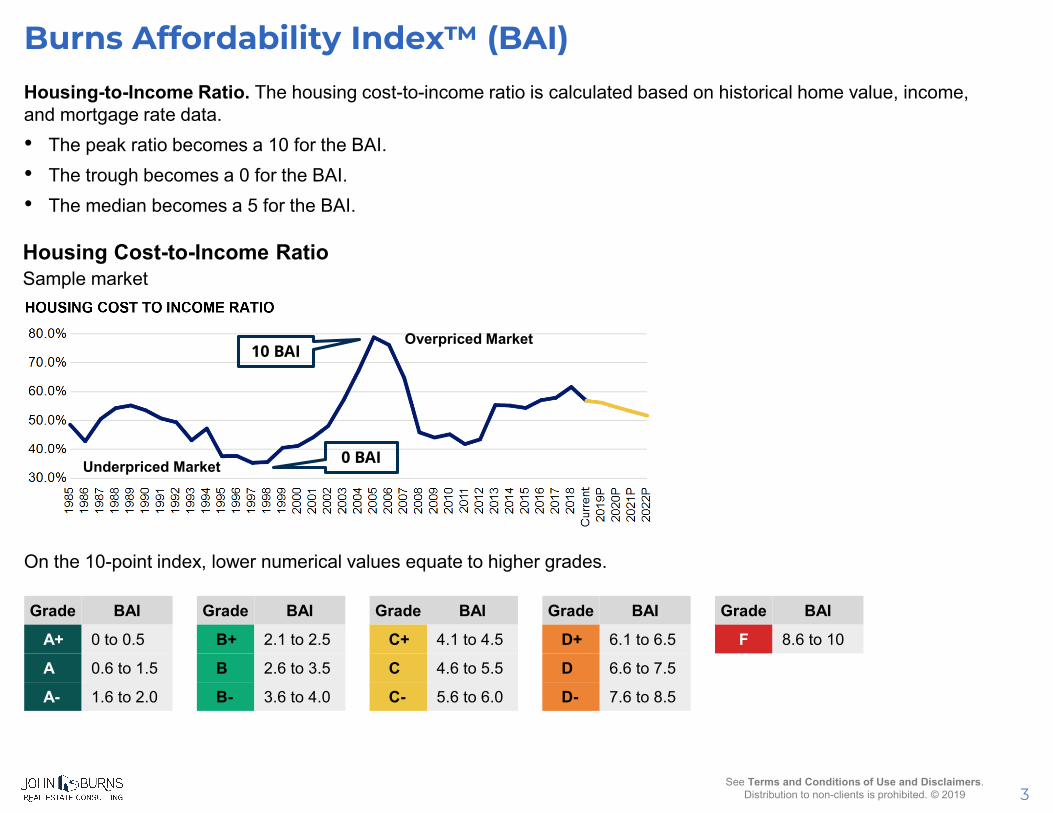

Housing-to-Income Ratio. The housing cost-to-income ratio is calculated based on historical home value, income, and mortgage rate data. • The peak ratio becomes a 10 for the BAI.• The trough becomes a 0 for the BAI.• The median becomes a 5 for the BAI.

10 BAI

0 BAI

Housing Cost-to-Income RatioSample market

Overpriced Market

Underpriced Market

Burns Affordability Index™ (BAI)

Grade BAI

A+ 0 to 0.5

A 0.6 to 1.5

A- 1.6 to 2.0

Grade BAI

B+ 2.1 to 2.5

B 2.6 to 3.5

B- 3.6 to 4.0

Grade BAI

C+ 4.1 to 4.5

C 4.6 to 5.5

C- 5.6 to 6.0

Grade BAI

D+ 6.1 to 6.5

D 6.6 to 7.5

D- 7.6 to 8.5

Grade BAI

F 8.6 to 10

On the 10-point index, lower numerical values equate to higher grades.

4See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

The median housing cost to median income ratio is the annual housing cost of a median-priced home divided by the median household income. Housing cost assumes the purchase of a home at 80% of the market’s median-priced existing home with a 5% down payment and a 30-year, fixed-rate mortgage. Payment includes PITI (principal, interest, taxes and insurance) plus mortgage insurance.

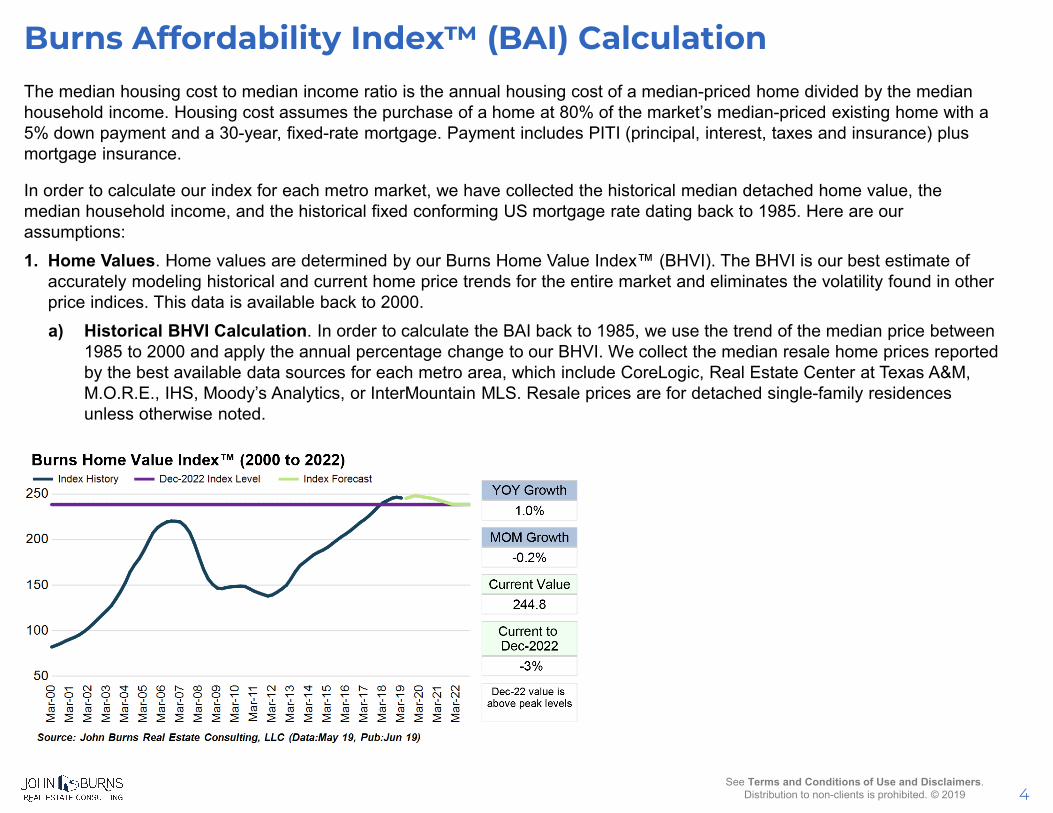

In order to calculate our index for each metro market, we have collected the historical median detached home value, the median household income, and the historical fixed conforming US mortgage rate dating back to 1985. Here are our assumptions:1. Home Values. Home values are determined by our Burns Home Value Index™ (BHVI). The BHVI is our best estimate of

accurately modeling historical and current home price trends for the entire market and eliminates the volatility found in other price indices. This data is available back to 2000.a) Historical BHVI Calculation. In order to calculate the BAI back to 1985, we use the trend of the median price between

1985 to 2000 and apply the annual percentage change to our BHVI. We collect the median resale home prices reported by the best available data sources for each metro area, which include CoreLogic, Real Estate Center at Texas A&M, M.O.R.E., IHS, Moody’s Analytics, or InterMountain MLS. Resale prices are for detached single-family residences unless otherwise noted.

Burns Affordability Index™ (BAI) Calculation

5See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

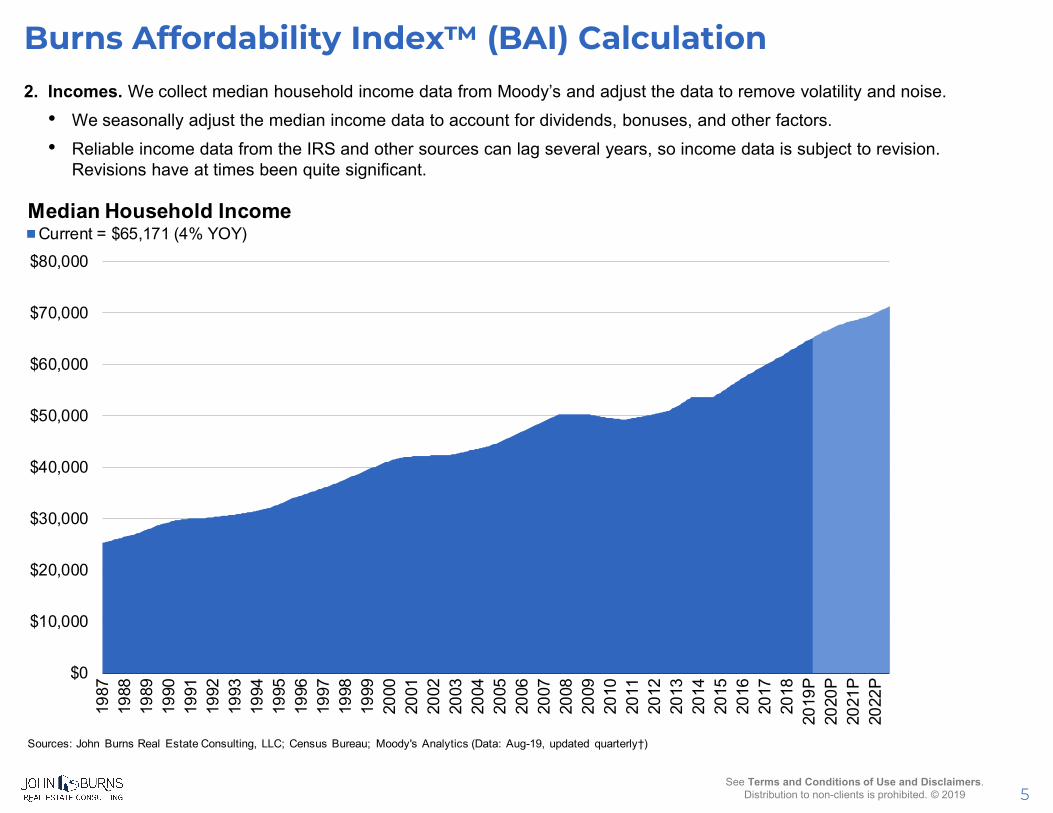

2. Incomes. We collect median household income data from Moody’s and adjust the data to remove volatility and noise. • We seasonally adjust the median income data to account for dividends, bonuses, and other factors. • Reliable income data from the IRS and other sources can lag several years, so income data is subject to revision.

Revisions have at times been quite significant.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

P20

20P

2021

P20

22P

Current = $65,171 (4% YOY)Median Household Income

Sources: John Burns Real Estate Consulting, LLC; Census Bureau; Moody's Analytics (Data: Aug-19, updated quarterly†)

Burns Affordability Index™ (BAI) Calculation

6See Terms and Conditions of Use and Disclaimers.

Distribution to non-clients is prohibited. © 2019

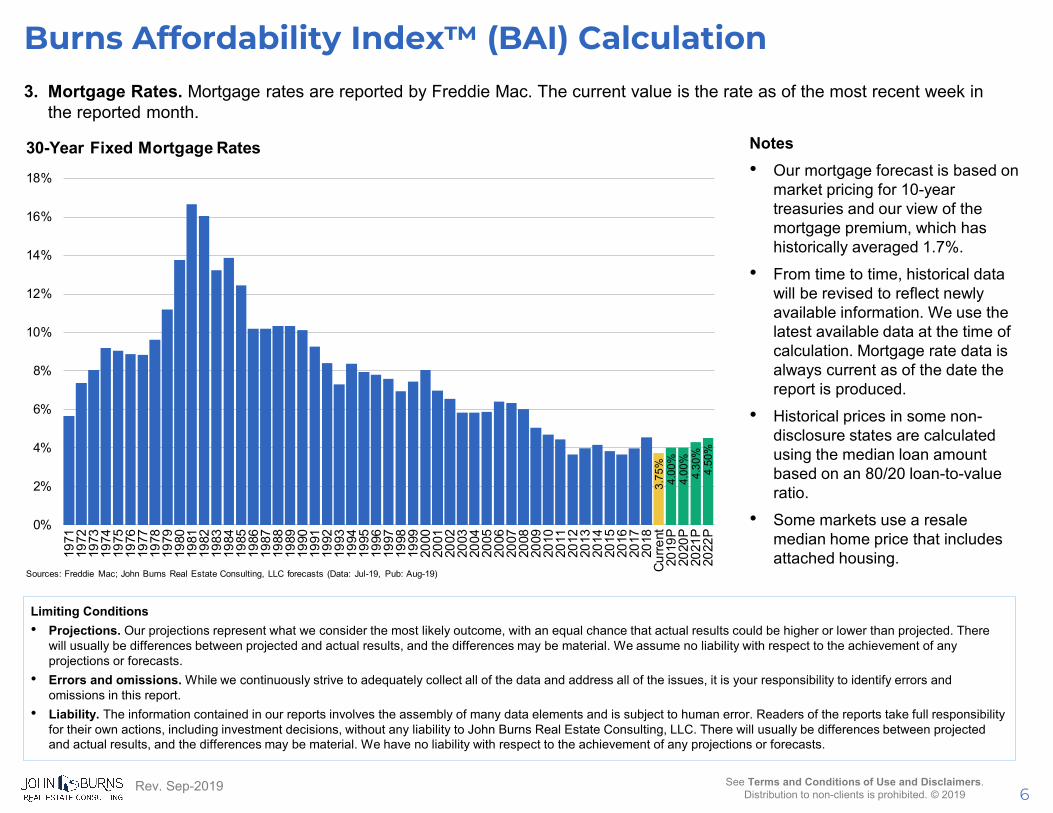

3. Mortgage Rates. Mortgage rates are reported by Freddie Mac. The current value is the rate as of the most recent week in the reported month.

Notes• Our mortgage forecast is based on

market pricing for 10-year treasuries and our view of the mortgage premium, which has historically averaged 1.7%.

• From time to time, historical data will be revised to reflect newly available information. We use the latest available data at the time of calculation. Mortgage rate data is always current as of the date the report is produced.

• Historical prices in some non-disclosure states are calculated using the median loan amount based on an 80/20 loan-to-value ratio.

• Some markets use a resale median home price that includes attached housing.

Limiting Conditions• Projections. Our projections represent what we consider the most likely outcome, with an equal chance that actual results could be higher or lower than projected. There

will usually be differences between projected and actual results, and the differences may be material. We assume no liability with respect to the achievement of any projections or forecasts.

• Errors and omissions. While we continuously strive to adequately collect all of the data and address all of the issues, it is your responsibility to identify errors and omissions in this report.

• Liability. The information contained in our reports involves the assembly of many data elements and is subject to human error. Readers of the reports take full responsibility for their own actions, including investment decisions, without any liability to John Burns Real Estate Consulting, LLC. There will usually be differences between projected and actual results, and the differences may be material. We have no liability with respect to the achievement of any projections or forecasts.

3.75

%4.

00%

4.00

%4.

30%

4.50

%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Cur

rent

2019

P20

20P

2021

P20

22P

Sources: Freddie Mac; John Burns Real Estate Consulting, LLC forecasts (Data: Jul-19, Pub: Aug-19)

30-Year Fixed Mortgage Rates

Burns Affordability Index™ (BAI) Calculation

Rev. Sep-2019