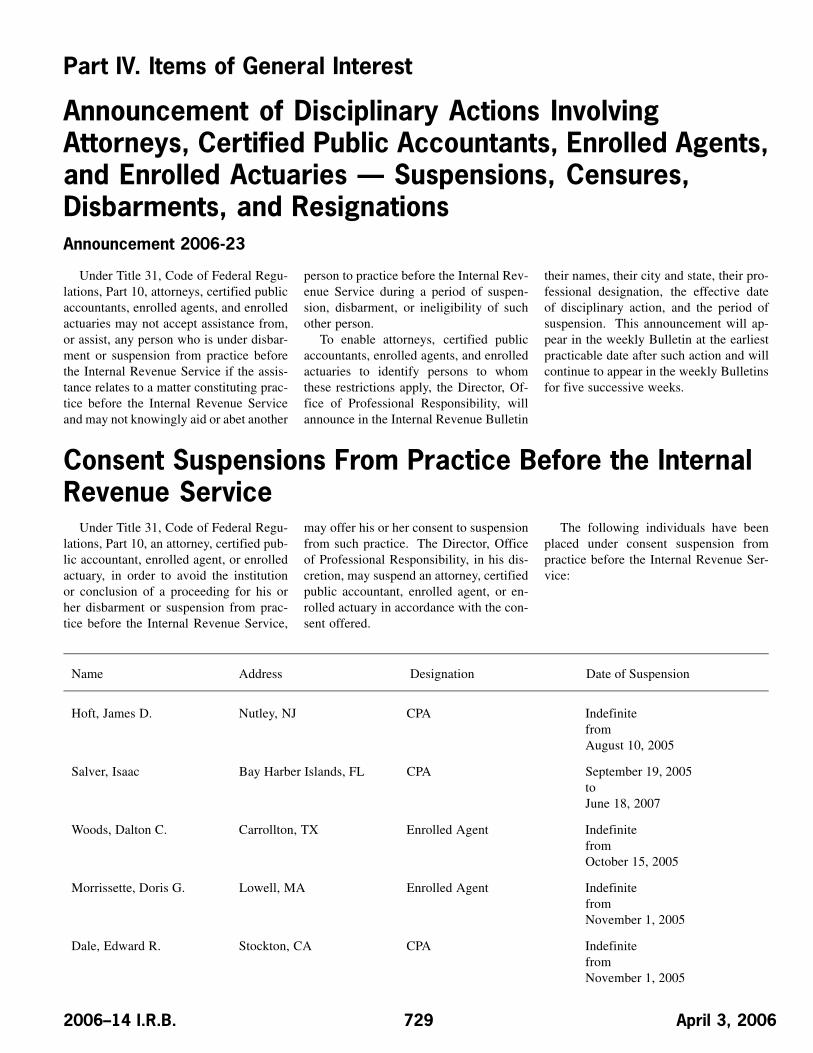

bulletin no. 2006-14 highlights of this issue - irs tax forms

TRANSCRIPT

Bulletin No. 2006-14April 3, 2006

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Ct. D. 2082, page 697.Sale of seized real property by IRS; federal tax delin-quency. The Supreme Court holds that the national interest inproviding a federal forum for federal tax litigation is sufficientlysubstantial to support the exercise of federal-question jurisdic-tion over the disputed issue on removal. Grable & Sons MetalProducts, Inc. v. Darue Engineering & Manufacturing.

Rev. Rul. 2006–16, page 694.Joint and several liability; relief under section 6015. Thisruling discusses the issue of whether a taxpayer is precludedfrom raising a request for relief from joint and several liabilityunder section 6015 by virtue of a previous Chapter 7 bank-ruptcy case in which the Service filed a proof of claim, but thebankruptcy court did not make an actual determination of taxliability.

Rev. Rul. 2006–22, page 687.Federal rates; adjusted federal rates; adjusted federallong-term rate and the long-term exempt rate. For pur-poses of sections 382, 642, 1274, 1288, and other sectionsof the Code, tables set forth the rates for April 2006.

T.D. 9245, page 696.Final regulations under section 6103(j) of the Code incorporateand clarify the phrase “return information reflected on returns”in conformance with the terms of section 6103(j)(5), which pro-vides for limited disclosures of returns and return informationin connection with the census of agriculture.

T.D. 9253, page 689.The Treasury Department and the IRS issued comprehen-sive withholding and reporting regulations (T.D. 8734 andT.D. 8881) that became effective on January 1, 2001. InNotice 2001–4, 2001–1 C.B. 267; Notice 2001–11, 2001–1C.B. 464; and Notice 2001–43, 2001–2 C.B. 72; the TreasuryDepartment and the IRS announced the intention to amendthe final regulations. These final regulations implement certainchanges announced in those notices and other changes. Inaddition, these final regulations provide guidance under sec-tion 411 of the American Jobs Act of 2004. Notice 2001–11and certain sections of Notices 2001–4 and 2001–43 super-seded.

Notice 2006–34, page 705.The Treasury Department and the Service request informationthat will be considered in formulating guidance on the incometax treatment of cross licensing arrangements.

Notice 2006–35, page 708.This notice modifies Announcement 2000–48, 2000–1 C.B.1243, and Notice 2001–43, 2001–2 C.B. 72, by providingthat, generally, a branch of a financial institution may not actas a qualified intermediary (QI) after December 31, 2006, ina country that does not have approved know-your-customer(KYC) rules. Announcement 2000–48 and Notice 2001–43modified.

(Continued on the next page)

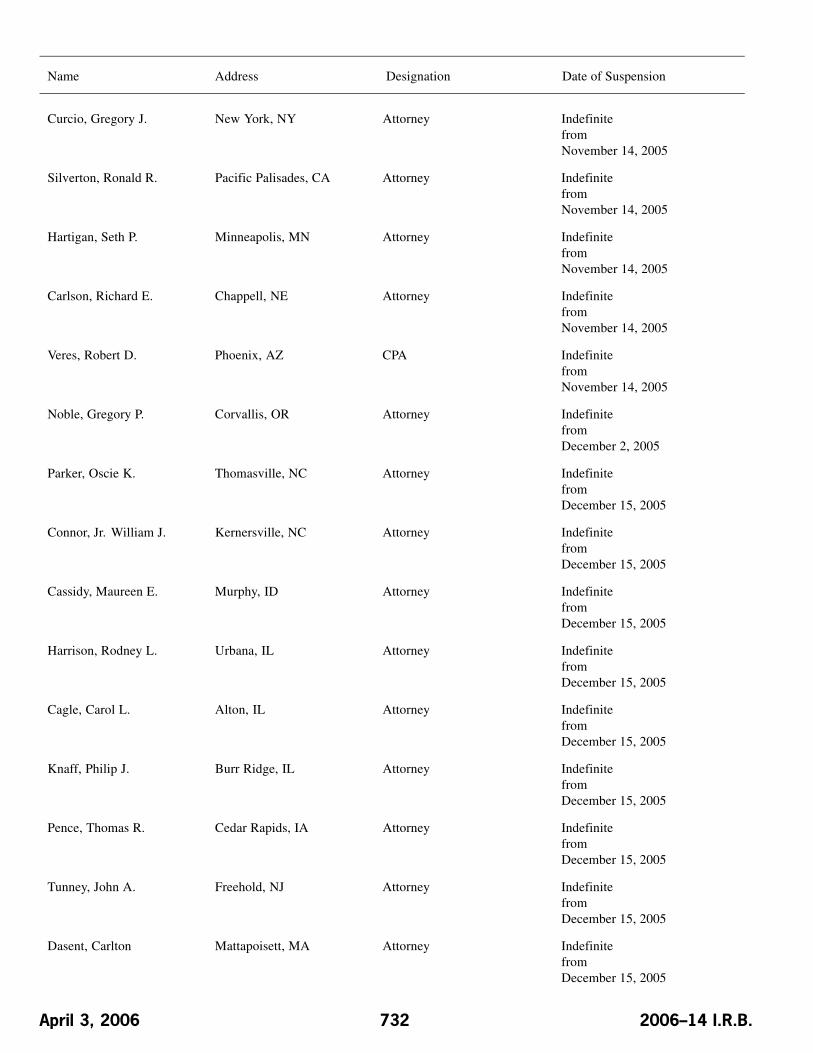

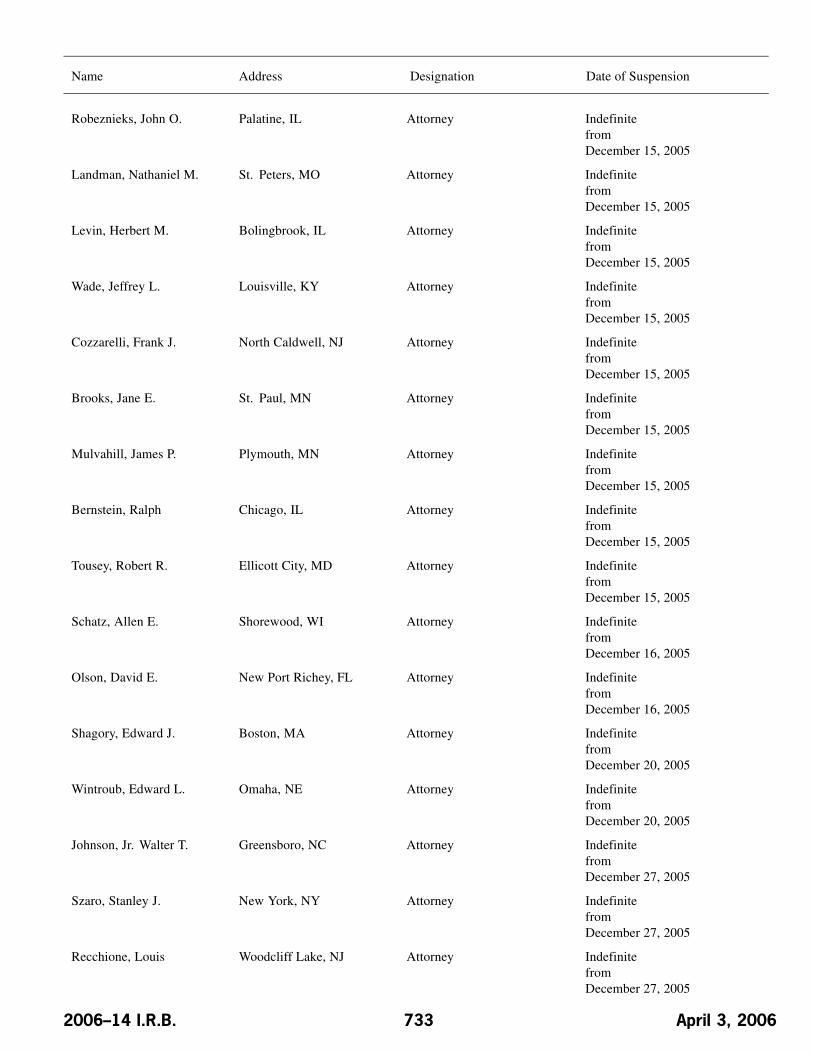

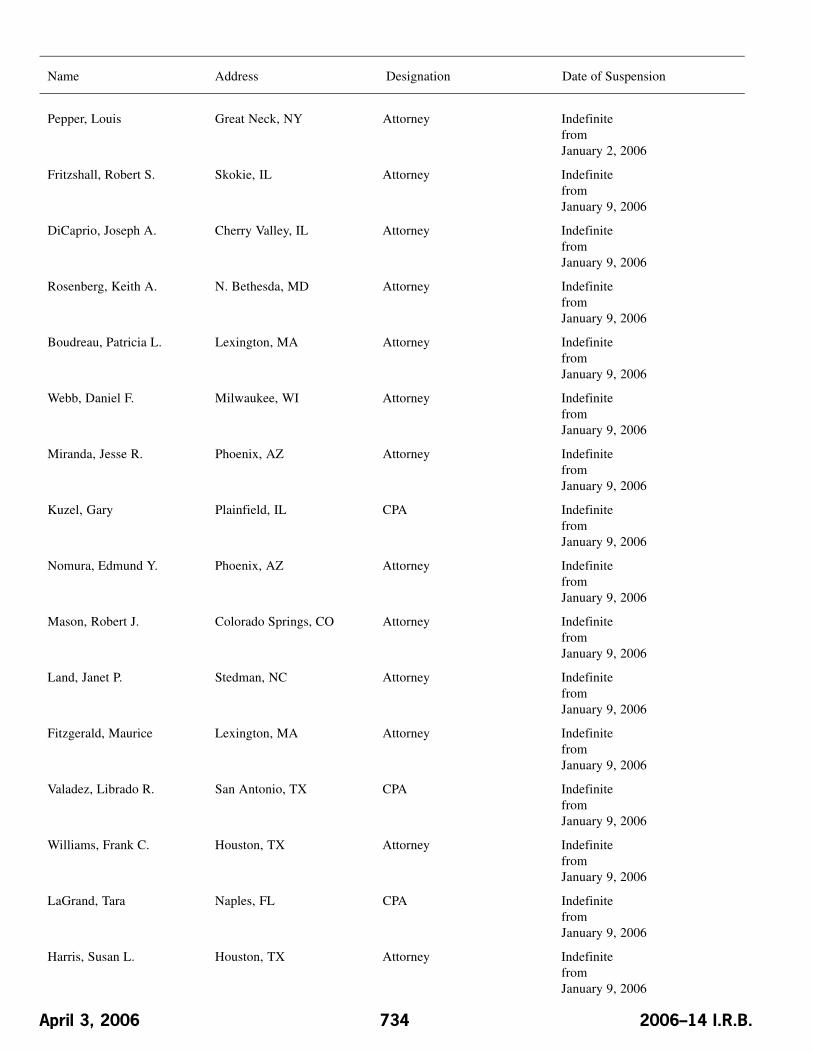

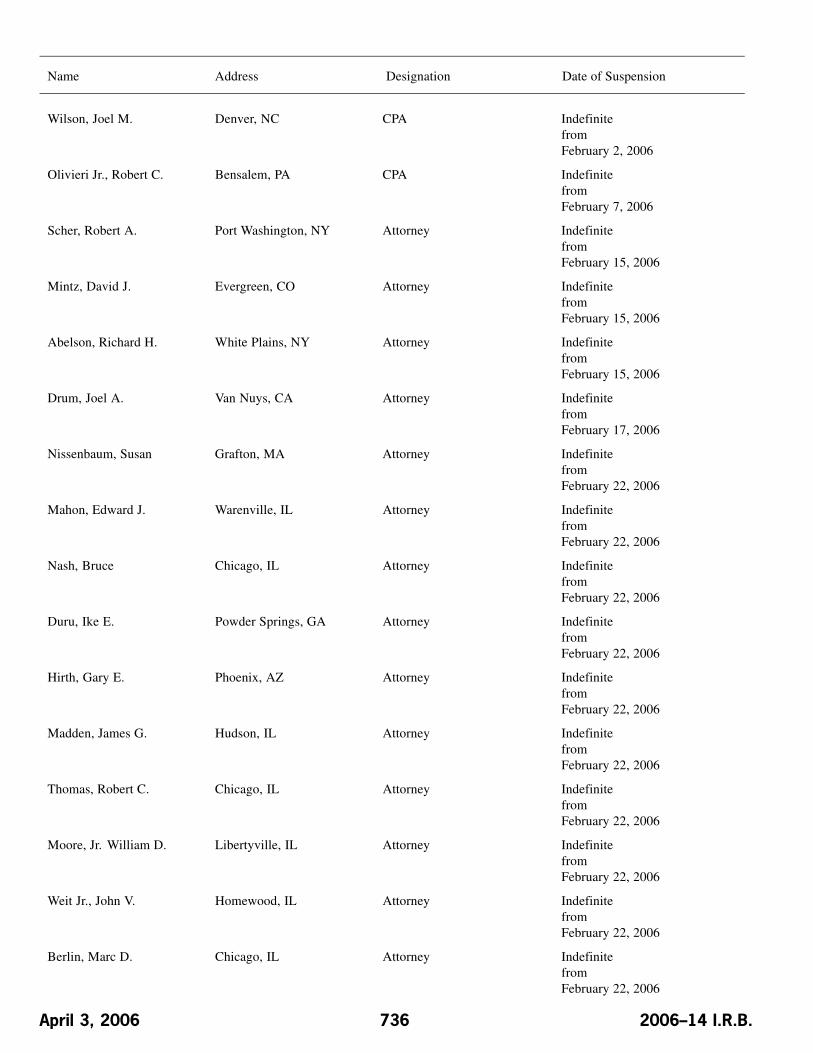

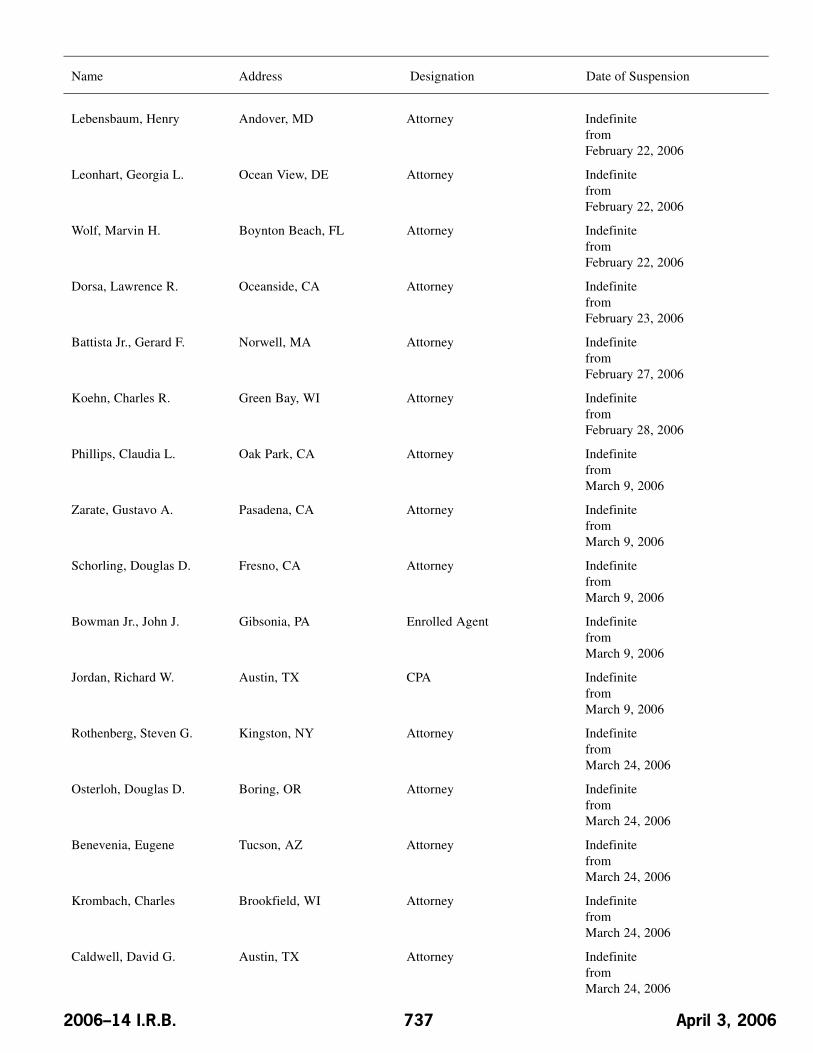

Announcements of Disbarments and Suspensions begin on page 729.Finding Lists begin on page ii.

TAX CONVENTIONS

Announcement 2006–21, page 703.This announcement sets forth a copy of the mutual agreemententered into on February 15, 2006, by the Competent Author-ities of the United States and Spain, regarding the treatmentof limited liability companies (LLCs), S corporations, and otherbusiness entities treated as partnerships or disregarded en-tities for U.S. tax purposes under the U.S.-Spain income taxtreaty and protocol.

ADMINISTRATIVE

Rev. Rul. 2006–16, page 694.Joint and several liability; relief under section 6015. Thisruling discusses the issue of whether a taxpayer is precludedfrom raising a request for relief from joint and several liabilityunder section 6015 by virtue of a previous Chapter 7 bank-ruptcy case in which the Service filed a proof of claim, but thebankruptcy court did not make an actual determination of taxliability.

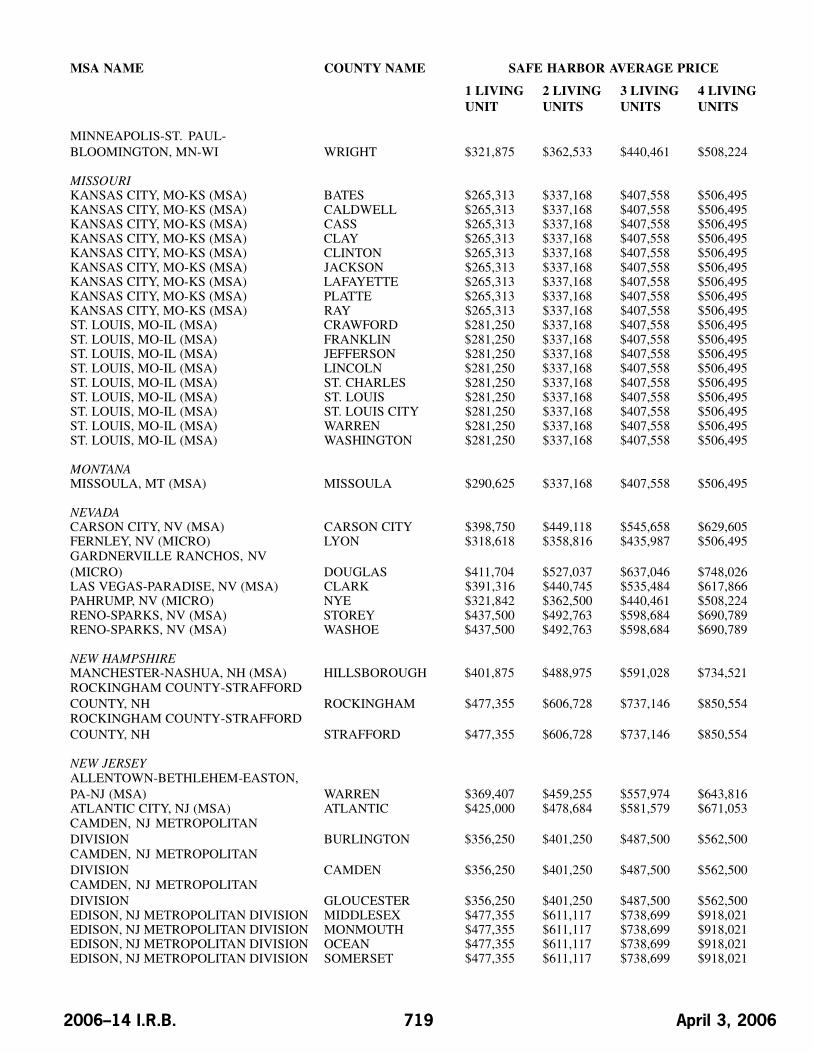

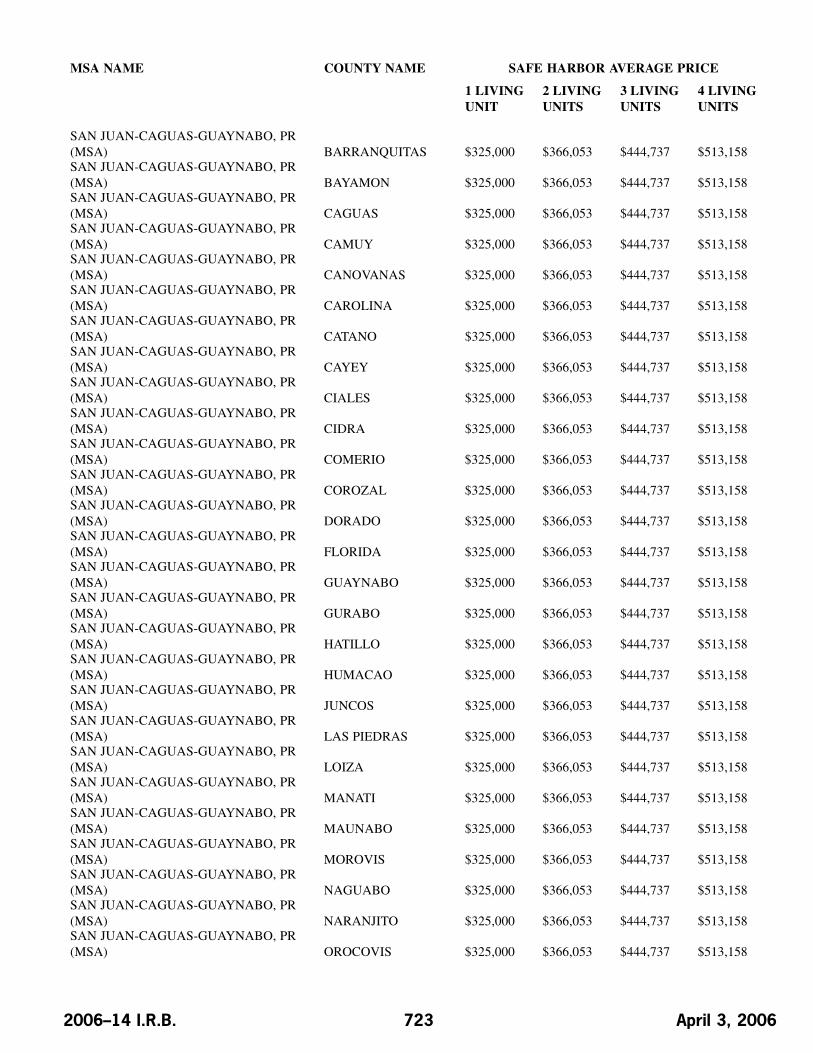

Rev. Proc. 2006–17, page 709.This procedure provides issuers of qualified mortgage bonds(QMBs) and qualified mortgage credit certificates (MCCs) withaverage area purchase price safe-harbors for statistical areasin the United States and with a nationwide average purchaseprice for residences in the United States for purposes of theQMB rules under section 143 of the Code and the MCC rulesunder section 25. Rev. Proc. 2005–15 obsoleted in part.

April 3, 2006 2006–14 I.R.B.

The IRS MissionProvide America’s taxpayers top quality service by helpingthem understand and meet their tax responsibilities and by

applying the tax law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bulletincontents are compiled semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Sec-retary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2006–14 I.R.B. April 3, 2006

Part I. Rulings and Decisions Under the Internal Revenue Codeof 1986Section 42.—Low-IncomeHousing Credit

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 280G.—GoldenParachute Payments

Federal short-term, mid-term, and long-term ratesare set forth for the month of April 2006. See Rev.Rul. 2006-22, page 687.

Section 382.—Limitationon Net Operating LossCarryforwards and CertainBuilt-In Losses FollowingOwnership Change

The adjusted applicable federal long-term rate isset forth for the month of April 2006. See Rev. Rul.2006-22, page 687.

Section 412.—MinimumFunding Standards

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 467.—CertainPayments for the Use ofProperty or Services

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 468.—SpecialRules for Mining and SolidWaste Reclamation andClosing Costs

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 482.—Allocationof Income and DeductionsAmong Taxpayers

Federal short-term, mid-term, and long-term ratesare set forth for the month of April 2006. See Rev.Rul. 2006-22, page 687.

Section 483.—Interest onCertain Deferred Payments

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 642.—SpecialRules for Credits andDeductions

Federal short-term, mid-term, and long-term ratesare set forth for the month of April 2006. See Rev.Rul. 2006-22, page 687.

Section 807.—Rules forCertain Reserves

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 846.—DiscountedUnpaid Losses Defined

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 1274.—Determi-nation of Issue Price in theCase of Certain Debt Instru-ments Issued for Property(Also Sections 42, 280G, 382, 412, 467, 468, 482,483, 642, 807, 846, 1288, 7520, 7872.)

Federal rates; adjusted federal rates;adjusted federal long-term rate and thelong-term exempt rate. For purposes of

sections 382, 642, 1274, 1288, and othersections of the Code, tables set forth therates for April 2006.

Rev. Rul. 2006–22

This revenue ruling provides vari-ous prescribed rates for federal incometax purposes for April 2006 (the currentmonth). Table 1 contains the short-term,mid-term, and long-term applicable fed-eral rates (AFR) for the current monthfor purposes of section 1274(d) of theInternal Revenue Code. Table 2 containsthe short-term, mid-term, and long-termadjusted applicable federal rates (adjustedAFR) for the current month for purposesof section 1288(b). Table 3 sets forth theadjusted federal long-term rate and thelong-term tax-exempt rate described insection 382(f). Table 4 contains the ap-propriate percentages for determining thelow-income housing credit described insection 42(b)(2) for buildings placed inservice during the current month. Finally,Table 5 contains the federal rate for deter-mining the present value of an annuity, aninterest for life or for a term of years, ora remainder or a reversionary interest forpurposes of section 7520.

2006–14 I.R.B. 687 April 3, 2006

REV. RUL. 2006–22 TABLE 1

Applicable Federal Rates (AFR) for April 2006

Period for Compounding

Annual Semiannual Quarterly Monthly

Short-term

AFR 4.77% 4.71% 4.68% 4.66%110% AFR 5.25% 5.18% 5.15% 5.12%120% AFR 5.73% 5.65% 5.61% 5.58%130% AFR 6.21% 6.12% 6.07% 6.04%

Mid-term

AFR 4.72% 4.67% 4.64% 4.63%110% AFR 5.21% 5.14% 5.11% 5.09%120% AFR 5.68% 5.60% 5.56% 5.54%130% AFR 6.16% 6.07% 6.02% 5.99%150% AFR 7.13% 7.01% 6.95% 6.91%175% AFR 8.34% 8.17% 8.09% 8.03%

Long-term

AFR 4.79% 4.73% 4.70% 4.68%110% AFR 5.27% 5.20% 5.17% 5.14%120% AFR 5.76% 5.68% 5.64% 5.61%130% AFR 6.24% 6.15% 6.10% 6.07%

REV. RUL. 2006–22 TABLE 2

Adjusted AFR for April 2006

Period for Compounding

Annual Semiannual Quarterly Monthly

Short-term adjustedAFR

3.33% 3.30% 3.29% 3.28%

Mid-term adjusted AFR 3.58% 3.55% 3.53% 3.52%

Long-term adjustedAFR

4.25% 4.21% 4.19% 4.17%

REV. RUL. 2006–22 TABLE 3

Rates Under Section 382 for April 2006

Adjusted federal long-term rate for the current month 4.25%

Long-term tax-exempt rate for ownership changes during the current month (the highest of the adjustedfederal long-term rates for the current month and the prior two months.) 4.26%

REV. RUL. 2006–22 TABLE 4

Appropriate Percentages Under Section 42(b)(2) for April 2006Appropriate percentage for the 70% present value low-income housing credit 8.11%

Appropriate percentage for the 30% present value low-income housing credit 3.47%

April 3, 2006 688 2006–14 I.R.B.

REV. RUL. 2006–22 TABLE 5

Rate Under Section 7520 for April 2006

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years,or a remainder or reversionary interest 5.6%

Section 1288.—Treatmentof Original Issue Discounton Tax-Exempt Obligations

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof April 2006. See Rev. Rul. 2006-22, page 687.

Section 1441.—Withholdingof Tax on Nonresident Aliens26 CFR 1.1441–1: Requirement for the deductionand withholding of tax on payments to foreign per-sons.

T.D. 9253

DEPARTMENT OFTHE TREASURYInternal Revenue Service26 CFR Parts 1 and 301

Revisions to RegulationsRelating to Withholding of Taxon Certain U.S. Source IncomePaid to Foreign Persons andRevisions of InformationReporting Regulations

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations and removalof temporary regulations.

SUMMARY: This document contains fi-nal regulations relating to the withholdingof tax under sections 1441 and 1442 oncertain U.S. source income paid to foreignpersons and related requirements govern-ing collection, deposit, refunds, and creditsof withheld amounts under sections 1461through 1463. Additionally, this documentcontains final regulations under sections6049 and 6114. These regulations affectpersons making payments of U.S. sourceincome to foreign persons and foreign per-sons claiming benefits under a U.S. in-come tax treaty.

DATES: Effective Date: These regulationsare effective March 14, 2006. The removalof §1.1441–1(e)(4)(vii)(G) is effective asof January 1, 2001.

FOR FURTHER INFORMATIONCONTACT: Ethan Atticks, (202)622–3840 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Paperwork Reduction Act

The collections of information con-tained in this final rule have been previ-ously reviewed and approved by the Officeof Management and Budget in accordancewith the Paperwork Reduction Act of 1995(44 U.S.C. 3507(d)) under control number1545–1484.

An agency may not conduct or sponsor,and a person is not required to respondto, a collection of information unless thecollection of information displays a validcontrol number assigned by the Office ofManagement and Budget.

Books or records relating to a collectionof information must be retained as longas their contents may become material inthe administration of any internal revenuelaw. Generally, tax returns and tax returninformation are confidential, as requiredby 26 U.S.C. 6103.

Background

In Treasury Decision 8734, 1997–2C.B. 109 [62 FR 53387], the Treasury De-partment and the IRS issued comprehen-sive regulations under chapter 3 (sections1441–1464) and subpart B of Part III ofSubchapter A of chapter 61 (sections 6041through 6050T) of the Internal RevenueCode (Code). Those regulations wereamended by T.D. 8804, 1999–1 C.B. 793[63 FR 72183], T.D. 8856, 2000–1 C.B.298 [64 FR 73408], T.D. 8881, 2000–1C.B. 1158 [65 FR 32152], and T.D. 9023,2002–2 C.B. 955 [67 FR 70310] (collec-tively the current regulations). The currentregulations are generally effective as ofJanuary 1, 2001.

In Notice 2001–4, 2001–1 C.B. 267,Notice 2001–11, 2001–1 C.B. 464, andNotice 2001–43, 2001–2 C.B. 72, theTreasury Department and the IRS an-nounced the intention to amend the currentregulations under sections 1441, 6049 and6114 to address the matters discussed inthose notices.

On March 30, 2005, the IRS andTreasury published a notice of proposedrulemaking (REG–125443–01, 2005–16I.R.B. 912) in the Federal Register (70FR 16189) (hereinafter the proposed reg-ulations). The proposed regulations con-tained provisions to implement certainchanges announced in those notices andother changes.

No public hearing regarding the pro-posed regulations was requested or held.However, certain written comments werereceived. After consideration of thecomments, the proposed regulations areadopted as revised by this Treasury deci-sion.

Summary of Comments

These final regulations finalize theprovisions of the proposed regulationswith only two areas of modification. Thecomments received and the modificationsmade in response to those comments aredescribed below.

A. Taxpayer Identification Number (TIN)Requirement for Certain Foreign GrantorTrusts

Section 1.1441–1(e)(4)(vii)(G) pro-vides that a TIN must be stated on awithholding certificate from a person rep-resenting to be a foreign grantor trustwith 5 or fewer grantors. Generally,if no TIN is provided, the withholdingcertificate is considered invalid. See§1.1441–1(e)(2)(ii).

The proposed regulations eliminatedthis TIN requirement for withholdingcertificates provided by such persons toqualified intermediaries (QIs), but retainedit for withholding certificates provided by

2006–14 I.R.B. 689 April 3, 2006

such persons to other withholding agentsif the certificate was executed on or beforeDecember 31, 2003.

Commentators requested that these fi-nal regulations adopt the provisions of theproposed regulations that remove the TINrequirement but with an effective date thatapplies to certificates executed and pro-vided to all withholding agents, not justQIs, on or after January 1, 2001, the effec-tive date of the current regulations. Thecommentators state that the retroactiveeffective date for withholding certificatesprovided to the other withholding agentsis consistent with the IRS and Treasury’srecognition that the TIN requirement inthe current regulations is not serving toenhance enforcement objectives. Further,the commentators state that for adminis-trative reasons the effective dates shouldbe consistent whether or not the withhold-ing certificate is provided to a QI or otherwithholding agent. The IRS and Treasuryagree with this comment. Accordingly,under these final regulations, a withhold-ing certificate executed on or after January1, 2001, and provided to a QI or otherwithholding agent by a person represent-ing to be a foreign grantor trust with fiveor fewer grantors does not need to state aTIN for such certificate to be valid.

B. Reporting of Treaty-based ReturnPositions

Section 301.6114–1(a) provides that,if a taxpayer takes a return position thata tax treaty overrules or modifies anyprovision of the Code and thereby effectsa reduction of any tax at any time, thetaxpayer must disclose that return posi-tion, either on a statement attached to thereturn or on a return filed for the pur-pose of making such disclosure. Whenapplicable, §301.6114–1(d) generally re-quires a taxpayer to attach Form 8833,Treaty-Based Return Position DisclosureUnder Section 6114 or 7701(b), to itsU.S. Federal income tax return. Section301.6114–1(b) states that reporting is re-quired unless it is expressly waived andprovides a nonexclusive list of particularpositions for which reporting is required.Section 301.6114–1(c) then provides a listof specific exceptions from the generalreporting requirements of §301.6114–1(a)and (b).

The proposed regulations provided thatreporting under §301.6114–1(b)(4)(ii) isrequired only for the positions specificallydescribed in paragraphs (b)(4)(ii)(A) and(B), or (C) or (D) of that section. Further,the proposed regulations provided thatreporting under §301.6114–1(b)(4)(ii)(D)is waived for taxpayers that are not indi-viduals or States and that receive amountsof income subject to withholding thatdo not exceed $10,000 in the aggregatefor the taxable year. See Prop. Reg.§301.6114–1(c)(1)(i), and (7).

Commentators suggested that the$10,000 threshold applicable to tax-payers that are not individuals or Statesshould be increased to $500,000, thethreshold amount for reporting under§301.6114–1(b)(4)(ii)(C) (addressing pay-ments to a related foreign person wherebenefits are claimed under a treaty thatcontains a limitation on benefits article).The commentators noted that entities typ-ically have substantially higher levels ofinvestment as compared to individuals andtherefore a higher threshold is warranted.The commentators concluded that theadministrative burden placed on these en-tities by the regulations is not appropriatewhen considering the benefit to the gov-ernment by the disclosure. As a result, thecommentators believed that the exceptionshould be modified.

In addition, the commentators sug-gested that reporting be waived for pensionfunds and certain other persons requiredto report under §301.6114–1(b)(4)(ii)(D),which requires reporting whenever a treatyimposes “any condition” in addition to aperson’s residence in the treaty countryfor entitlement to treaty benefits. Thecommentators stated that because, for ex-ample, an income tax treaty may conditiona pension fund’s entitlement to a reducedrate of taxation on dividends on the pen-sion fund not being engaged in a tradeor business, and because a pension fundrarely will violate such a condition, froma practical standpoint the sole requirementfor entitlement to treaty benefits is theresidence of the pension fund. Therefore,the commentators suggested that requiringthe pension fund to file an income taxreturn and make a treaty based disclosureof its position imposes an unnecessaryadministrative burden. Accordingly, thecommentators believed that it was ap-propriate to interpret the regulations such

that the trade or business requirementdescribed above with respect to pensionfunds is not “any condition” described in§301.6114–1(b)(4)(ii)(D). To clarify thispoint, the commentators requested thatthe final regulations waive reporting forpension funds.

Commentators also requested that§301.6114–1(c)(6), which waives report-ing for amounts required to be reportedunder section 6038A on a Form 5472, “In-formation Return of a 25% Foreign-OwnedU.S. Corporation or a Foreign Corpora-tion Engaged in a U.S. Trade or Business(under sections 6038A and 6038(c) of theInternal Revenue Code),” to the extentpermitted under the form or accompany-ing instructions, be activated by includingsuch permission in the form or instruc-tions.

The IRS and Treasury considered thecomments discussed above, as well as thegeneral bases for requiring reporting undersection 6114. The IRS and Treasury agreethat reporting under section 6114 shouldnot be required in certain circumstanceswhere the payment is properly reportedon Form 1042–S, “Foreign Person’s U.S.Source Income Subject to Withholding,”and the withholding agent is a U.S. per-son, or a foreign person that has enteredinto an agreement that provides for IRSaudit. Thus, in response to the commentsdescribed above, the following amend-ments are made to the waiver provisionsof §301.6114–1(c).

First, rather than activating the excep-tion for amounts required to be reportedunder section 6038A on Form 5472, para-graph (c)(6) of the regulations is revisedto replace this provision regarding Form5472 with a provision waiving reportingfor amounts properly reported on Form1042–S by a withholding agent that is areporting corporation within the meaningof section 6038A(a). Second, a new para-graph (c)(7) is added to provide that re-porting is waived for amounts properly re-ported on Form 1042–S by a withholdingagent that is a U.S. financial institution, aQI, or a withholding foreign partnership(WP) or withholding foreign trust (WT)if the beneficial owner is a direct accountholder of the U.S. financial institution orQI or a direct beneficiary or owner of theWP or WT. Third, a new paragraph (c)(8)is added which replaces the provision inthe proposed regulations (see Prop. Reg.

April 3, 2006 690 2006–14 I.R.B.

§301.6114–1(c)(7)) waiving reporting fortaxpayers that are not individuals or Statesand that receive amounts of income sub-ject to withholding that do not exceed the$10,000 threshold. New paragraph (c)(8)contains a waiver for taxpayers that are notindividuals or States that receive amountsthat have been properly reported on Form1042–S, do not exceed $500,000, and arenot received through an intermediary orflow-through entity.

Notwithstanding the discussion above,the final regulations provide that thewaivers from reporting in paragraph (c)(6),(7) and (8) do not apply to the extent thatreporting is specifically required under theinstructions to Form 8833.

Finally, these final regulationsclarify that reporting under section301.6114–1(b)(4)(ii) is required only forthe positions specifically described inparagraphs (b)(4)(ii)(A) and (B), or (C) or(D).

Effect on Other Documents

Sections (V)(C), (D), and (E) of No-tice 2001–4, 2001–1 C.B. 267, Notice2001–11, 2001–1 C.B. 464, and Sections2 and 3 of Notice 2001–43, 2001–2 C.B.72, are superseded as of March 14, 2006.

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assessmentis not required. It has also been determinedthat section 553(b) of the AdministrativeProcedure Act (5 U.S.C. chapter 5) doesnot apply to these regulations, and, be-cause the regulations do not impose a newcollection of information on small entities,the Regulatory Flexibility Act (5 U.S.C.chapter 6) does not apply. Pursuant to sec-tion 7805(f) of the Code, the proposed reg-ulations preceding these regulations weresubmitted to the Chief Counsel for Advo-cacy of the Small Business Administrationfor comment on their impact on small busi-ness.

Drafting Information

The principal author of these proposedregulations is Ethan Atticks, Office ofAssociate Chief Counsel (International).However, other personnel from the IRS

and Treasury Department participated intheir development.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR parts 1 and 301are amended as follows:

PART 1 — INCOME TAXES

Paragraph 1. The authority citation forpart 1 continues to read, in part, as follows:

Authority: 26 U.S.C. 7805 * * *Par. 2. Section 1.1441–1 is amended as

follows:1. Paragraph (b)(2)(iv)(A) is revised.2. Paragraph (b)(3)(iii)(E) is added.3. Paragraph (c)(30) is added.4. Paragraph (e)(4)(vii)(G) is removed

and paragraph (e)(4)(vii)(H) and (I) are re-designated as paragraph (e)(4)(vii)(G) and(H) respectively.

The revisions and additions read as fol-lows:

§1.1441–1 Requirement for the deductionand withholding of tax on payments toforeign persons.

* * * * *(b) * * *(2) * * *(iv) Payments to a U.S. branch of cer-

tain foreign banks or foreign insurancecompanies—(A) U.S. branch treated as aU.S. person in certain cases. A paymentto a U.S. branch of a foreign person is apayment to a foreign person. However,a U.S. branch described in this para-graph (b)(2)(iv)(A) and a withholdingagent (including another U.S. branch de-scribed in this paragraph (b)(2)(iv)(A))may agree to treat the branch as a U.S.person for purposes of withholding onspecified payments to the U.S. branch.Notwithstanding the preceding sentence,a withholding agent making a paymentto a U.S. branch treated as a U.S. personunder this paragraph (b)(2)(iv)(A) shallnot treat the branch as a U.S. person forpurposes of reporting the payment made tothe branch. Therefore, a payment to suchU.S. branch shall be reported on Form1042–S under §1.1461–1(c). Further, aU.S. branch that is treated as a U.S. personunder this paragraph (b)(2)(iv)(A) shall

not be treated as a U.S. person for pur-poses of the withholding certificate it mayprovide to a withholding agent. There-fore, the U.S. branch must furnish a U.S.branch withholding certificate on FormW–8 as provided in paragraph (e)(3)(v)of this section and not a Form W–9. Anagreement to treat a U.S. branch as a U.S.person must be evidenced by a U.S. branchwithholding certificate described in para-graph (e)(3)(v) of this section furnishedby the U.S. branch to the withholdingagent. A U.S. branch described in thisparagraph (b)(2)(iv)(A) is any U.S. branchof a foreign bank subject to regulatorysupervision by the Federal Reserve Boardor a U.S. branch of a foreign insurancecompany required to file an annual state-ment on a form approved by the NationalAssociation of Insurance Commissionerswith the Insurance Department of a State,a Territory, or the District of Columbia. Inaddition, a financial institution organizedin a possession of the United States willbe treated as a U.S. branch for purposes ofthis paragraph (b)(2)(iv)(A). The InternalRevenue Service (IRS) may approve alist of U.S. branches that may qualify fortreatment as a U.S. person under this para-graph (b)(2)(iv)(A) (see §601.601(d)(2)of this chapter). See §1.6049–5(c)(5)(vi)for the treatment of U.S. branches asU.S. payors if they make a payment thatis subject to reporting under chapter 61of the Internal Revenue Code. Also see§1.6049–5(d)(1)(ii) for the treatment ofU.S. branches as foreign payees underchapter 61 of the Internal Revenue Code.

* * * * *(3) * * *(iii) * * *(E) Certain payments for services. A

payment for services is presumed to bemade to a foreign person if —

(1) The payee is an individual;(2) The withholding agent does not

know, or have reason to know, that thepayee is a U.S. citizen or resident;

(3) The withholding agent does notknow, or have reason to know, that the in-come is (or may be) effectively connectedwith the conduct of a trade or businesswithin the United States; and

(4) All of the services for which thepayment is made were performed by thepayee outside of the United States.

* * * * *

2006–14 I.R.B. 691 April 3, 2006

(c) * * *(30) Possessions of the United States.

For purposes of the regulations underchapters 3 and 61 of the Internal Rev-enue Code, possessions of the UnitedStates means Guam, American Samoa, theNorthern Mariana Islands, Puerto Rico,and the Virgin Islands.

* * * * *Par. 3. Section 1.1441–3 is amended

by revising paragraphs (c)(3) and (e)(2) toread as follows:

§1.1441–3 Determination of amounts tobe withheld.

* * * * *(c) * * *(3) Special rules in the case of dis-

tributions from a regulated investmentcompany—(i) General rule. If the amountof any distributions designated as beingsubject to section 852(b)(3)(C) or 5(A),or 871(k)(1)(C) or (2)(C), exceeds theamount that may be designated underthose sections for the taxable year, then nopenalties will be asserted for any resultingunderwithholding if the designations werebased on a reasonable estimate (madepursuant to the same procedures as de-scribed in paragraph (c)(2)(ii)(A) of thissection) and the adjustments to the amountwithheld are made within the time perioddescribed in paragraph (c)(2)(ii)(B) of thissection. Any adjustment to the amountof tax due and paid to the IRS by thewithholding agent as a result of under-withholding shall not be treated as a distri-bution for purposes of section 562(c) andthe regulations thereunder. Any amountof U.S. tax that a foreign shareholder istreated as having paid on the undistributedcapital gain of a regulated investmentcompany under section 852(b)(3)(D) maybe claimed by the foreign shareholder as acredit or refund under §1.1464–1.

(ii) Reliance by intermediary on rea-sonable estimate. For purposes of de-termining whether a payment is a distri-bution designated as subject to section852(b)(3)(C) or (5)(A), or 871(k)(1)(C)or (2)(C), a withholding agent that is notthe distributing regulated investment com-pany may, absent actual knowledge orreason to know otherwise, rely on the des-ignations that the distributing companyrepresents have been made in accordancewith paragraph (c)(3)(i) of this section.

Failure by the withholding agent to with-hold the required amount due to a failureby the regulated investment company toreasonably estimate the required amountsor to properly communicate the relevantinformation to the withholding agent shallbe imputed to the distributing company.In such a case, the IRS may collect fromthe distributing company any underwith-held amount and subject the company toapplicable interest and penalties as a with-holding agent.

* * * * *(e) * * *(2) Payments in foreign currency. If the

amount subject to withholding tax is paidin a currency other than the U.S. dollar,the amount of withholding under section1441 shall be determined by applying theapplicable rate of withholding to the for-eign currency amount and converting theamount withheld into U.S. dollars on thedate of payment at the spot rate (as definedin §1.988–1(d)(1)) in effect on that date. Awithholding agent making regular or fre-quent payments in foreign currency mayuse a month-end spot rate or a monthly av-erage spot rate. In addition, such a with-holding agent may use the spot rate on thedate the amount of tax is deposited (withinthe meaning of §1.6302–2(a)), providedthat such deposit is made within sevendays of the date of the payment giving riseto the obligation to withhold. A spot rateconvention must be used consistently forall non-dollar amounts withheld and fromyear to year. Such convention cannot bechanged without the consent of the Com-missioner. The U.S. dollar amount so de-termined shall be treated by the beneficialowner as the amount of tax paid on the in-come for purposes of determining the finalU.S. tax liability and, if applicable, claim-ing a refund or credit of tax.

* * * * *Par. 4. In §1.1441–6, paragraph (b)(1)

is revised to read as follows:

§1.1441–6 Claim of reduced withholdingunder an income tax treaty.

* * * * *(b) Reliance on claim of reduced with-

holding under an income tax treaty—(1)In general. The withholding imposed un-der section 1441, 1442, or 1443 on anypayment to a foreign person is eligible forreduction under the terms of an income

tax treaty only to the extent that such pay-ment is treated as derived by a residentof an applicable treaty jurisdiction, suchresident is a beneficial owner, and all otherrequirements for benefits under the treatyare satisfied. See section 894 and the reg-ulations thereunder to determine whethera resident of a treaty country derives theincome. Absent actual knowledge or rea-son to know otherwise, a withholdingagent may rely on a claim that a beneficialowner is entitled to a reduced rate of with-holding based upon an income tax treatyif, prior to the payment, the withholdingagent can reliably associate the paymentwith a beneficial owner withholding cer-tificate, as described in §1.1441–1(e)(2),that contains the information necessaryto support the claim, or, in the case ofa payment of income described in para-graph (c)(2) of this section made outsidethe United States with respect to an off-shore account, documentary evidencedescribed in paragraphs (c)(3), (4), and (5)of this section. See §1.6049–5(e) for thedefinition of payments made outside theUnited States and §1.6049–5(c)(1) for thedefinition of offshore account. For pur-poses of this paragraph (b)(1), a beneficialowner withholding certificate described in§1.1441–1(e)(2)(i) contains informationnecessary to support the claim for a treatybenefit only if it includes the beneficialowner’s taxpayer identifying number (ex-cept as otherwise provided in paragraph(c)(1) of this section and §1.1441–6(g))and the representations that the beneficialowner derives the income under section894 and the regulations thereunder, ifrequired, and meets the limitation on ben-efits provisions of the treaty, if any. Thewithholding certificate must also containany other representations required by thissection and any other information, certifi-cations, or statements as may be requiredby the form or accompanying instruc-tions in addition to, or in place of, theinformation and certifications describedin this section. Absent actual knowledgeor reason to know that the claims areincorrect (and subject to the standardsof knowledge in §1.1441–7(b)), a with-holding agent may rely on the claimsmade on a withholding certificate or ondocumentary evidence. A withholdingagent may also rely on the informationcontained in a withholding statement pro-vided under §§1.1441–1(e)(3)(iv) and

April 3, 2006 692 2006–14 I.R.B.

1.1441–5(c)(3)(iv) and (e)(5)(iv) to deter-mine whether the appropriate statementsregarding section 894 and limitation onbenefits have been provided in connectionwith documentary evidence. The Inter-nal Revenue Service (IRS) may apply theprovisions of §1.1441–1(e)(1)(ii)(B) tonotify the withholding agent that the cer-tificate cannot be relied upon to grantbenefits under an income tax treaty.See §1.1441–1(e)(4)(viii) regarding re-liance on a withholding certificate by awithholding agent. The provisions of§1.1441–1(b)(3)(iv) dealing with a 90-daygrace period shall apply for purposes ofthis section.

* * * * *Par. 5. Section 1.6049–5 is amended as

follows:1. Paragraph (c)(1) is revised.2. Paragraphs (c)(5)(i), (ii), (iii), (iv),

(v) and (vi) are redesignated as paragraphs(c)(5)(i)(A), (B), (C), (D), (E), and (F), re-spectively.

3. A new heading is added to paragraph(c)(5)(i).

4. New paragraph (c)(5)(ii) is added.The revisions and additions read as fol-

lows:

§1.6049–5 Interest and original issuediscount subject to reporting afterDecember 31, 1982.

* * * * *(c) Applicable rules—(1) Documentary

evidence for offshore accounts and forpossessions accounts. A payor may relyon documentary evidence described in thisparagraph (c)(1) instead of a beneficialowner withholding certificate describedin §1.1441–1(e)(2)(i) in the case of apayment made outside the United Statesto an offshore account, in the case of apayment made to a U.S. possessions ac-count or, in the case of broker proceedsdescribed in §1.6045–1(c)(2), in the caseof a sale effected outside the United States(as defined in §1.6045–1(g)(3)(iii)(A)).For purposes of this paragraph (c)(1), anoffshore account means an account main-tained at an office or branch of a U.S. orforeign bank or other financial institutionat any location outside the United States(i.e., other than in any of the fifty Statesor the District of Columbia) and outsideof possessions of the United States. Thus,for example, an account maintained in a

foreign country at a branch of a U.S. bankor of a foreign subsidiary of a U.S. bank isan offshore account. For purposes of thisparagraph (c)(1), a U.S. possessions ac-count means an account maintained at anoffice or branch of a U.S. or foreign bankor other financial institution located withina possession of the United States. For thedefinition of a payment made outside theUnited States, see paragraph (e) of thissection. A payor may rely on documen-tary evidence if the payor has establishedprocedures to obtain, review, and maintaindocumentary evidence sufficient to estab-lish the identity of the payee and the statusof that person as a foreign person (in-cluding, but not limited to, documentaryevidence described in §1.1441–6(c)(3)or (4)); and the payor obtains, reviews,and maintains such documentary evidencein accordance with those procedures. Apayor maintains the documents reviewedby retaining the original, certified copy,or a photocopy (or microfiche or sim-ilar means of record retention) of thedocuments reviewed and noting in itsrecords the date on which and by whomthe document was received and reviewed.Documentary evidence furnished for thepayment of an amount subject to with-holding under chapter 3 of the InternalRevenue Code must contain all of the in-formation that is necessary to complete aForm 1042–S for that payment. A payormay also rely on documentary evidenceassociated with a flow-through withhold-ing certificate for payments treated asmade to foreign partners of a nonwith-holding foreign partnership, as defined in§1.1441–1(c)(28), the foreign beneficia-ries of a foreign simple trust, as definedin §1.1441–1(c)(24), or foreign ownersof a foreign grantor trust, as defined in§1.1441–1(c)(26), even though the part-nership or trust account is maintained inthe United States.

* * * * *(5) * * * (i) Definition. * * *(ii) Reporting by U.S. payors in U.S.

possessions. U.S. payors are not requiredto report on Form 1099 income that isfrom sources within a possession of theUnited States and that is exempt from tax-ation under section 931, 932, or 933, eachof which sections exempts certain incomefrom sources within a possession of theUnited States paid to a bona fide resident of

that possession. For purposes of this para-graph (c)(5)(ii), a U.S. payor may treat thebeneficial owner as a bona fide resident ofthe possession of the United States fromwhich the income is sourced if, prior topayment of the income, the U.S. payor canreliably associate the payment with validdocumentation that supports the claim ofresidence in the possession of the UnitedStates from which the income is sourced.This paragraph (c)(5)(ii) shall not apply ifthe U.S. payor has actual knowledge orreason to know that the documentation isunreliable or incorrect or that the incomedoes not satisfy the requirements for ex-emption under section 931, 932, or 933.For the rules determining whether incomeis from sources within a possession of theUnited States, see section 937(b) and theregulations thereunder.

* * * * *

PART 301 — PROCEDURE ANDADMINISTRATION

Par. 6. The authority citation for part301 continues to read, in part, as follows:

Authority: 26 U.S.C. 7805 * * *Par. 7. Section 301.6114–1 is amended

as follows:1. Paragraphs (c)(1)(i) through

(c)(1)(vii) are redesignated as paragraphs(c)(1)(ii) through (c)(1)(viii), respectively.

2. New paragraph (c)(1)(i) is added.3. Paragraph (c)(6) is revised.4. Paragraphs (c)(7) and (8) are added.The additions and revision read as fol-

lows:

§301.6114–1 Treaty-based returnpositions.

* * * * *(c) * * * (1) * * *(i) For amounts received on or after

January 1, 2001, reporting under para-graph (b)(4)(ii) is waived, unless reportingis specifically required under paragraphs(b)(4)(ii)(A) and (B) of this section, para-graph (b)(4)(ii)(C) of this section, orparagraph (b)(4)(ii)(D) of this section;

* * * * *(6)(i) For taxable years ending after

December 31, 2004, except as providedin paragraph (c)(6)(ii) of this section, re-porting under paragraph (b)(4)(ii) of thissection is waived for amounts receivedby a related party, within the meaning of

2006–14 I.R.B. 693 April 3, 2006

section 6038A(c)(2), from a withhold-ing agent that is a reporting corporation,within the meaning of section 6038A(a),and that are properly reported on Form1042–S.

(ii) Paragraph (c)(6)(i) of this sectiondoes not apply to any amounts for whichreporting is specifically required under theinstructions to Form 8833.

(7)(i) For taxable years ending after De-cember 31, 2004, except as provided inparagraph (c)(7)(iv) of this section, report-ing under paragraph (b)(4)(ii) of this sec-tion is waived for amounts properly re-ported on Form 1042–S (on either a spe-cific payee or pooled basis) by a withhold-ing agent described in paragraph (c)(7)(ii)of this section if the beneficial owner is de-scribed in paragraph (c)(7)(iii) of this sec-tion.

(ii) A withholding agent described inthis paragraph (c)(7)(ii) is a U.S. financialinstitution, as defined in §1.1441–1(c)(5)of this chapter, a qualified intermediary, asdefined in §1.1441–1(e)(5)(ii) of this chap-ter, a withholding foreign partnership, asdefined in §1.1441–5(c)(2)(i) of this chap-ter, or a withholding foreign trust, as de-fined in §1.1441–5(e)(5)(v) of this chapter.

(iii) A beneficial owner described inthis paragraph (c)(7)(iii) of this sectionis a direct account holder of a U.S. fi-nancial institution or qualified intermedi-ary, a direct partner of a withholding for-eign partnership, or a direct beneficiaryor owner of a simple or grantor trust thatis a withholding foreign trust. A bene-ficial owner described in this paragraph(c)(7)(iii) also includes an account holderto which a qualified intermediary has ap-plied section 4A.01 or 4A.02 of the quali-fied intermediary agreement, contained inRevenue Procedure 2000–12, 2000–1 C.B.387 (as amended by Revenue Procedure2003–64, 2003–2 C.B. 306; Revenue Pro-cedure 2004–21, 2004–1 C.B. 702; Rev-enue Procedure 2005–77, 2005–51 I.R.B.1176 (see § 601.601(b)(2) of this chapter)a partner to which a withholding foreignpartnership has applied section 10.01 or10.02 of the withholding foreign partner-ship agreement, and a beneficiary or ownerto which a withholding foreign trust hasapplied section 10.01 or 10.02 of the with-holding foreign trust agreement, containedin Revenue Procedure 2003–64, 2003–2C.B. 306 (as amended by Revenue Proce-dure 2004–21, 2004–1 C.B. 702; Revenue

Procedure 2005–77, 2005–51 I.R.B. 1176(see § 601.601(b)(2) of this chapter).

(iv) Paragraph (c)(7)(i) of this sectiondoes not apply to any amounts for whichreporting is specifically required under theinstructions to Form 8833.

(8)(i) For taxable years ending afterDecember 31, 2004, except as providedin paragraph (c)(8)(ii) of this section, re-porting under paragraph (b)(4)(ii) of thissection is waived for taxpayers that arenot individuals or States and that receiveamounts of income that have been prop-erly reported on Form 1042–S, that donot exceed $500,000 in the aggregate forthe taxable year and that are not receivedthrough an account with an intermediary,as defined in §1.1441–1(c)(13), or withrespect to interest in a flow-through entity,as defined in §1.1441–1(c)(23).

(ii) The exception contained in para-graph (c)(8)(i) of this section does not ap-ply to any amounts for which reporting isspecifically required under the instructionsto Form 8833.

* * * * *

Mark E. Matthews,Deputy Commissioner forServices and Enforcement.

Approved February 27, 2006.

Eric Solomon,Acting Deputy Assistant Secretary

of the Treasury (Tax Policy).

(Filed by the Office of the Federal Register on March 13,2006, 8:45 a.m., and published in the issue of the FederalRegister for March 14, 2006, 71 F.R. 13003)

Section 6015.—Relief FromJoint and Several Liabilityon Joint Return26 CFR 1.6015–1: Relief from joint and several lia-bility on a joint return.

Joint and several liability; relief un-der section 6015. This ruling discussesthe issue of whether a taxpayer is pre-cluded from raising a request for relieffrom joint and several liability under sec-tion 6015 by virtue of a previous Chapter 7bankruptcy case in which the Service fileda proof of claim, but the bankruptcy courtdid not make an actual determination of taxliability.

Rev. Rul. 2006–16

ISSUE

Whether the taxpayer is precluded fromraising a request for relief from joint andseveral liability under section 6015 byvirtue of a previous Chapter 7 bankruptcycase in which the Internal Revenue Service(Service) filed a proof of claim, but thebankruptcy court did not make an actualdetermination of tax liability.

FACTS

Married taxpayers, H and W, sign andtimely file a joint return for Year 1. Dur-ing an audit, the Service determines thatthe joint return substantially understatesthe income attributable to taxpayer W. TheService issues a notice of deficiency, onwhich taxpayers default. In January ofYear 3, the Service assesses against tax-payers income tax deficiencies, for whichthey are jointly and severally liable. Nei-ther taxpayer pays the deficiency assess-ment. In October of Year 3, taxpayersfile a voluntary joint petition for bank-ruptcy under Chapter 7 of Title 11 of theUnited States Code (Bankruptcy Code). InNovember of Year 3, the Service files aproof of claim asserting an unsecured pri-ority claim for the deficiency. Neither tax-payer, nor any other party in interest, ob-jects to the proof of claim, which is not dis-charged and is deemed allowed under sec-tion 502(a) of the Bankruptcy Code. Nei-ther taxpayer requests relief from joint andseveral liability under section 6015 duringthe bankruptcy case. Neither taxpayer re-quests the bankruptcy court to adjudicatethe merits of the tax liability under section505 of the Bankruptcy Code.

After the bankruptcy case is closed, tax-payers H and W separate. Thereafter, H(requesting spouse) files a request for re-lief from joint and several liability undersection 6015. No party in interest files adischargeability proceeding.

LAW

The Bankruptcy Code provides rulesfor debtors to consolidate and resolve theirdebts to various creditors, including theService, in various ways. Section 301of the Bankruptcy Code allows debtorsto commence a bankruptcy case by filinga voluntary petition with the bankruptcy

April 3, 2006 694 2006–14 I.R.B.

court. Once a petition is filed, creditorshave an opportunity to file proofs of claim.11 U.S.C. § 501. A proof of claim assertsthe right of a creditor to payment and caninclude rights that are fixed, contingent,liquidated, or unliquidated. See 11 U.S.C.§ 101(5). A properly filed proof of claimis prima facie evidence of the validity andamount of the claim. Fed. R. Bankr. P.3001(f). The proof of claim is deemed al-lowed, unless a party in interest objects.11 U.S.C. § 502(a). If a party in interestobjects, the bankruptcy court, after noticeand a hearing, determines the validity andamount of the claim as of the date of thepetition and allows the claim in the properamount. 11 U.S.C. § 502(b).

Generally, the bankruptcy court maydetermine the amount or legality of anytax, any fine or penalty relating to a tax,or any addition to tax, whether or not pre-viously assessed and whether or not paid.11 U.S.C. § 505(a)(1). This includes thedetermination of the eligibility of a debtorfor relief from joint and several liabilityunder section 6015 in appropriate cases.See In re French, 242 B.R. 369 (Bankr.N.D. Ohio 1999). The determination ofthe bankruptcy court on the merits of aclaim is a final judgment and, unless ap-pealed, is binding on the parties to a con-tested matter. See Freytag v. Commis-sioner, 110 T.C. 35 (1998). The determi-nation also precludes subsequent litigationby a debtor over the merits of the liabil-ity under principles of res judicata. Seeid. at 40. The Supreme Court in Commis-sioner v. Sunnen explained the rule of resjudicata:

[W]hen a court of competent jurisdic-tion has entered a final judgment on themerits of a cause of action, the partiesto the suit and their privies are there-after bound “not only as to every matterwhich was offered and received to sus-tain or defeat the claim or demand, butas to any other admissible matter whichmight have been offered for that pur-pose.”

333 U.S. 591, 597 (1948) (quotingCromwell v. County of Sac, 94 U.S. 351,352 (1876)).

Although filing a bankruptcy petitioncommences a case, “a bankruptcy case issimply an aggregation of controversies.”See In re Martin Bros. Toolmakers, Inc.,

796 F.2d 1435, 1437 (11th Cir. 1986).In order to bring a controversy before thebankruptcy court, a party generally movesfor relief in a contested matter under Fed-eral Rule of Bankruptcy Procedure 9014or initiates an adversary proceeding un-der Rule 7001. The merits of a tax lia-bility are generally raised in one of twoways. Either the debtor or the Service canseek a determination of a tax liability un-der section 505 of the Bankruptcy Code,or a party in interest can object to a proofof claim listing tax liabilities under section502(a). See In re Taylor, 132 F.3d 256, 262(5th Cir. 1998). Unless a party in interestmoves for relief or initiates a proceeding,the merits of a tax liability are not beforethe bankruptcy court, and the bankruptcycourt does not inquire into the merits of thetax liability or enter a final judgment fixingthe tax liability.

Certain taxes are excepted from dis-charge in a Chapter 7 bankruptcy case.See 11 U.S.C. § 523(a)(1), 727(b). For ex-ample, income tax liabilities for tax yearsending within three years of the bank-ruptcy petition are entitled to priority sta-tus and are excepted from the bankruptcydischarge under sections 523(a)(1)(A) and507(a)(8)(A)(i). These tax liabilities areexcepted from discharge under section523(a)(1)(A) whether or not a claim wasfiled or allowed, and the principles of resjudicata do not apply unless the meritsof the tax liabilities were actually deter-mined. Hambrick v. Commissioner, 118T.C. 348 (2002).

A debtor or creditor may request thebankruptcy court to determine the dis-chargeability of a debt by initiating anadversary proceeding under Federal Ruleof Bankruptcy Procedure 7001. A dis-chargeability proceeding is a proceedingto determine whether a bankruptcy dis-charge includes the discharge of liabilityfor certain debts. A determination of thebankruptcy court in a discharge proceed-ing that is a final judgment on the meritsbars relitigation of dischargeability. SeeFlorida Peach Corp. v. Commissioner,90 T.C. 678, 682 (1988). However, a dis-charge determination generally does notinclude consideration of the merits of thedebt. In re Doerge, 181 B.R. 358, 364(Bankr. S.D. Ill. 1995). There are casesin which bankruptcy courts consider the

merits of a tax liability, including relieffrom joint and several liability, duringthe course of determining whether thetax liability is dischargeable. See, e.g., Inre Brackin, 148 B.R. 953 (Bankr. N.D.Ala. 1992). If the bankruptcy court wereto make a determination on the meritsof the tax liability, that determinationgenerally would preclude the requestingspouse from later raising a request forrelief under section 6015 if the requestingspouse was a debtor in the bankruptcycase and meaningfully participated in thedischargeability proceeding. See section6015(g)(2).

ANALYSIS

Under the facts of this revenue ruling,the Service filed a proof of claim in thebankruptcy case and neither taxpayer, andno other party in interest, filed an objec-tion to the proof of claim under 11 U.S.C§ 502(a) or moved for the bankruptcy courtto determine the liability under 11 U.S.C.§ 505(a). Thus, the merits of the tax liabil-ity were not determined by the bankruptcycourt and the requesting spouse is not pre-cluded from raising a request for relief un-der section 6015 after the bankruptcy caseis closed.

HOLDING

The taxpayer, H, is not precluded fromraising a subsequent request for relief fromjoint and several liability under section6015 by virtue of the prior bankruptcy casefiled by H and W in which the Service fileda proof of claim, but the bankruptcy courtdid not make an actual determination of theliability.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is G. William Beard of the Office of theAssociate Chief Counsel (Procedure andAdministration), Collection, Bankruptcy& Summonses Division. For further in-formation regarding this revenue ruling,contact Branch 2 of Collection, Bank-ruptcy & Summonses at (202) 622–3620(not a toll-free call).

2006–14 I.R.B. 695 April 3, 2006

Section 6103.—Confi-dentiality and Disclosureof Returns and ReturnInformation26 CFR 301.6103(j)(5)–1: Disclosures of return in-formation reflected on returns to officers and employ-ees of the Department of Agriculture for conductingthe census of agriculture.

T.D. 9245

DEPARTMENT OFTHE TREASURYInternal Revenue Service26 CFR Part 301

Disclosure of ReturnInformation to the Departmentof Agriculture

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document contains fi-nal regulations that incorporate and clar-ify the phrase “return information reflectedon returns” in conformance with the termsof section 6103(j)(5) of the Internal Rev-enue Code (Code), which provides for lim-ited disclosures of returns and return infor-mation in connection with the census ofagriculture. These final regulations alsoremove certain items of return informa-tion that the Department of Agriculture nolonger needs for conducting the census ofagriculture.

DATES: Effective Date: These regulationsare effective on February 22, 2006.

FOR FURTHER INFORMATIONCONTACT: Deborah Lambert-Dean at(202) 622–4570 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Background

This document contains amendments to26 CFR part 301 under section 6103(j)of the Code. On June 6, 2003, the Fed-eral Register published a temporary regu-lation (T.D. 9060, 2003–1 C.B. 1116) re-garding disclosure of return informationto the Department of Agriculture (68 FR33857) and a notice of proposed rulemak-ing (NPRM) (REG–103809–03, 2003–1

C.B. 1132) cross-referencing the tempo-rary regulations (68 FR 33887). Therewere no comments submitted in responseto the NPRM. There was no request for apublic hearing, and none took place. Theproposed regulations are adopted and thecorresponding temporary regulations areremoved.

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assessmentis not required. It also has been deter-mined that section 553(b) of the Admin-istrative Procedure Act (5 U.S.C. chapter5) does not apply to these regulations, andbecause the regulations do not impose acollection of information on small entities,the Regulatory Flexibility Act (5 U.S.C.chapter 6) does not apply. Pursuant to sec-tion 7805(f) of the Code, the IRS submit-ted the NPRM preceding this Treasury de-cision to the Chief Counsel for Advocacyof the Small Business Administration forcomment on its impact on small business.

Drafting Information

The principal author of these regula-tions is Deborah Lambert-Dean, Office ofthe Associate Chief Counsel, Procedure& Administration (Disclosure & PrivacyLaw Division).

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 301 isamended as follows:

PART 301— PROCEDURE ANDADMINISTRATION

Paragraph 1. The authority citationfor part 301 is amended by removing theentry for “Section 301.6103(j)(5)–1T andadding an entry in numerical order to readin part as follows:

Authority: 26 U.S.C. 7805 * * *Section 301.6103(j)(5)–1 also issued

under 26 U.S.C. 6103(j)(5). * * *

§301.6103(j)(5)–1T [Removed]

Par. 2. Section 301.6103(j)(5)–1T isremoved.

Par. 3. Section 301.6103(j)(5)–1 isadded to read as follows:

§ 301.6103(j)(5)–1 Disclosures of returninformation reflected on returns to officersand employees of the Department ofAgriculture for conducting the census ofagriculture.

(a) General rule. Pursuant to the provi-sions of section 6103(j)(5) of the InternalRevenue Code and subject to the require-ments of paragraph (c) of this section, offi-cers or employees of the Internal RevenueService will disclose return information re-flected on returns to officers and employ-ees of the Department of Agriculture to theextent, and for such purposes, as may beprovided by paragraph (b) of this section.“Return information reflected on returns”includes, but is not limited to, informationon returns, information derived from pro-cessing such returns, and information de-rived from other sources for the purposesof establishing and maintaining taxpayerinformation relating to returns.

(b) Disclosure of return information re-flected on returns to officers and employ-ees of the Department of Agriculture. (1)Officers or employees of the Internal Rev-enue Service will disclose the followingreturn information reflected on returns de-scribed in this paragraph (b) for individ-uals, partnerships and corporations withagricultural activity, as determined gener-ally by industry code classification or thefiling of returns for such activity, to offi-cers and employees of the Department ofAgriculture for purposes of, but only to theextent necessary in, structuring, preparing,and conducting, as authorized by chapter55 of title 7, United States Code, the cen-sus of agriculture.

(2) From Form 1040 “U.S. IndividualIncome Tax Return”, Form 1041 “U.S. In-come Tax Return for Estates and Trusts”,Form 1065 “U.S. Return of Partnership In-come”, and Form 1065–B “U.S. Return ofIncome for Electing Large Partnerships”(Schedule F)—

(i) Taxpayer identity information (asdefined in section 6103(b)(6) of the Inter-nal Revenue Code);

(ii) Spouse’s Social Security Number;(iii) Annual accounting period;(iv) Principal Business Activity (PBA)

code;(v) Taxable cooperative distributions;

April 3, 2006 696 2006–14 I.R.B.

(vi) Income from custom hire and ma-chine work;

(vii) Gross income;(viii) Master File Tax (MFT) code;(ix) Document Locator Number (DLN);(x) Cycle posted;(xi) Final return indicator;(xii) Part year return indicator; and(xiii) Taxpayer telephone number.(3) From Form 943, “Employer’s An-

nual Federal Tax Return for AgriculturalEmployees”—

(i) Taxpayer identity information;(ii) Annual accounting period;(iii) Total wages subject to Medicare

taxes;(iv) MFT code;(v) DLN;(vi) Cycle posted;(vii) Final return indicator; and(viii) Part year return indicator.(4) From Form 1120 series, “U.S. Cor-

poration Income Tax Return”—(i) Taxpayer identity information;(ii) Annual accounting period;(iii) Gross receipts less returns and al-

lowances;(iv) PBA code;(v) MFT Code;(vi) DLN;(vii) Cycle posted;(viii) Final return indicator;(ix) Part year return indicator; and(x) Consolidated return indicator.(5) From Form 1065 series, “U.S. Re-

turn of Partnership Income” —(i) Taxpayer identity information;(ii) Annual accounting period;(iii) PBA code;(iv) Gross receipts less returns and al-

lowances;(v) Net farm profit (loss);(vi) MFT code;(vii) DLN;(viii) Cycle posted;(ix) Final return indicator; and(x) Part year return indicator.(c) Procedures and Restrictions. (1)

Disclosure of return information reflectedon returns by officers or employees of theInternal Revenue Service as provided byparagraph (b) of this section will be madeonly upon written request designating, byname and title, the officers and employeesof the Department of Agriculture to whomsuch disclosure is authorized, to the Com-missioner of Internal Revenue by the Sec-retary of Agriculture and describing—

(i) The particular return information re-flected on returns for disclosure;

(ii) The taxable period or date to whichsuch return information reflected on re-turns relates; and

(iii) The particular purpose for the re-quested return information reflected on re-turns.

(2) (i) No such officer or employee towhom the Internal Revenue Service dis-closes return information reflected on re-turns pursuant to the provisions of para-graph (b) of this section shall disclose suchinformation to any person, other than thetaxpayer to whom such return informationreflected on returns relates or other offi-cers or employees of the Department ofAgriculture whose duties or responsibili-ties require such disclosure for a purposedescribed in paragraph (b)(1) of this sec-tion, except in a form that cannot be asso-ciated with, or otherwise identify, directlyor indirectly, a particular taxpayer.

(ii) If the Internal Revenue Service de-termines that the Department of Agricul-ture, or any officer or employee thereof,has failed to, or does not, satisfy the re-quirements of section 6103(p)(4) of theInternal Revenue Code or regulations orpublished procedures, the Internal Rev-enue Service may take such actions as aredeemed necessary to ensure that such re-quirements are or will be satisfied, includ-ing suspension of disclosures of return in-formation reflected on returns otherwiseauthorized by section 6103(j)(5) and para-graph (b) of this section, until the InternalRevenue Service determines that such re-quirements have been or will be satisfied.

(d) Effective date. This section is appli-cable on February 22, 2006.

Mark E. Matthews,Deputy Commissioner forServices and Enforcement.

Approved February 11, 2006.

Eric Solomon,Acting Deputy Assistant Secretary

of the Treasury (Tax Policy).

(Filed by the Office of the Federal Register on February 21,2006, 8:45 a.m., and published in the issue of the FederalRegister for February 22, 2006, 71 F.R. 8945)

Section 6335.—Sale ofSeized Property

Ct. D. 2082

SUPREME COURT OF THEUNITED STATES

No. 04-603

GRABLE & SONS METAL PRODUCTS,INC. v. DARUE

ENGINEERING & MANUFACTURING

CERTIORARI TO THEUNITED STATES COURT OF

APPEALS FORTHE SIXTH CIRCUIT

June 13, 2005

Syllabus

The Internal Revenue Service seizedreal property owned by petitioner (here-inafter Grable) to satisfy a federal taxdelinquency, and gave Grable notice bycertified mail before selling the propertyto respondent (hereinafter Darue). Grablesubsequently brought a quiet title action instate court, claiming that Darue’s title wasinvalid because 26 U. S. C. §6335 requiredthe IRS to give Grable notice of the sale bypersonal service, not certified mail. Darueremoved the case to Federal District Courtas presenting a federal question becausethe title claim depended on an interpreta-tion of federal tax law. The District Courtdeclined to remand the case, finding thatit posed a significant federal-law question,and it granted Darue summary judgmenton the merits. The Sixth Circuit affirmed,and this Court granted certiorari on thejurisdictional question.

Held: The national interest in providinga federal forum for federal tax litigation issufficiently substantial to support the ex-ercise of federal-question jurisdiction overthe disputed issue on removal. Pp. 3–11.

(a) Darue was entitled to remove thequiet title action if Grable could havebrought it in federal court originally, as acivil action “arising under the . . . laws. . . of the United States,” 28 U. S. C.§1331. Federal-question jurisdiction isusually invoked by plaintiffs pleading acause of action created by federal law,but this Court has also long recognizedthat such jurisdiction will lie over some

2006–14 I.R.B. 697 April 3, 2006

state-law claims that implicate significantfederal issues, see, e.g., Smith v. KansasCity Title & Trust Co., 255 U. S. 180.Such federal jurisdiction demands notonly a contested federal issue, but a sub-stantial one. And the jurisdiction must beconsistent with congressional judgmentabout the sound division of labor betweenstate and federal courts governing §1331’sapplication. These considerations havekept the Court from adopting a singletest for jurisdiction over federal issuesembedded in state-law claims betweennondiverse parties. Instead, the questionis whether the state-law claim necessarilystated a federal issue, actually disputedand substantial, which a federal forummay entertain without disturbing a con-gressionally approved balance of federaland state judicial responsibilities. Pp. 3–6.

(b) This case warrants federal jurisdic-tion. Grable premised its superior titleclaim on the IRS’s failure to give adequatenotice, as defined by federal law. WhetherGrable received notice is an essential ele-ment of its quiet title claim, and the fed-eral statute’s meaning is actually disputed.The meaning of a federal tax provisionis an important federal-law issue that be-longs in federal court. The Governmenthas a strong interest in promptly collectingdelinquent taxes, and the IRS’s ability tosatisfy its claims from delinquents’ prop-erty requires clear terms of notice to assurebuyers like Darue that the IRS has goodtitle. Finally, because it will be the rarestate title case that raises a federal-law is-sue, federal jurisdiction to resolve genuinedisagreement over federal tax title provi-sions will portend only a microscopic ef-fect on the federal-state division of labor.This conclusion puts the Court in vener-able company, quiet title actions havingbeen the subject of some of the earliestexercises of federal-question jurisdictionover state-law claims. E.g., Hopkins v.Walker, 244 U. S. 486, 490–491. Pp. 6–7.

(c) Merrell Dow Pharmaceuticals Inc.v. Thompson, 478 U. S. 804, is not to thecontrary. There, in finding federal juris-diction unavailable for a state tort claimresting in part on an allegation that the de-fendant drug company had violated a fed-eral branding law, the Court noted thatCongress had not provided a private fed-eral cause of action for such violations.Merrell Dow cannot be read to make afederal cause of action a necessary con-

dition for federal-question jurisdiction. Itdisclaimed the adoption of any bright-linerule and expressly approved the exerciseof jurisdiction in Smith, where there wasno federal cause of action. Accordingly,Merrell Dow should be read in its entiretyas treating the absence of such cause as ev-idence relevant to, but not dispositive of,the “sensitive judgments about congres-sional intent,” required by §1331. Id., at810. In Merrell Dow, the principal sig-nificance of this absence was its bearingon the consequences to the federal system.If the federal labeling standard without acause of action could get a state claim intofederal court, so could any other federalstandards without causes of action. Andthat would mean an enormous number ofcases. A comparable analysis yields a dif-ferent jurisdictional conclusion here, be-cause state quiet title actions rarely involvecontested federal-law issues. Pp. 7–11.

377 F. 3d 592, affirmed.SOUTER, J., delivered the opinion for

a unanimous Court. THOMAS, J., filed aconcurring opinion.

SUPREME COURT OF THEUNITED STATES

No. 04-603

GRABLE & SONS METAL PRODUCTS,INC., PETITIONER v. DARUE

ENGINEERING & MANUFACTURING

ON WRIT OF CERTIORARITO THE UNITED STATES

COURT OF APPEALSFOR THE SIXTH CIRCUIT

June 13, 2005

JUSTICE SOUTER delivered the opin-ion of the Court.

The question is whether want of a fed-eral cause of action to try claims of titleto land obtained at a federal tax sale pre-cludes removal to federal court of a stateaction with non-diverse parties raising adisputed issue of federal title law. We an-swer no, and hold that the national interestin providing a federal forum for federal taxlitigation is sufficiently substantial to sup-port the exercise of federal question juris-diction over the disputed issue on removal,which would not distort any division of la-

bor between the state and federal courts,provided or assumed by Congress.

I

In 1994, the Internal Revenue Serviceseized Michigan real property belongingto petitioner Grable & Sons Metal Prod-ucts, Inc., to satisfy Grable’s federal taxdelinquency. Title 26 U. S. C. §6335 re-quired the IRS to give notice of the seizure,and there is no dispute that Grable receivedactual notice by certified mail before theIRS sold the property to respondent DarueEngineering & Manufacturing. AlthoughGrable also received notice of the sale it-self, it did not exercise its statutory rightto redeem the property within 180 days ofthe sale, §6337(b)(1), and after that periodhad passed, the Government gave Darue aquitclaim deed. §6339.

Five years later, Grable brought a quiettitle action in state court, claiming thatDarue’s record title was invalid becausethe IRS had failed to notify Grable of itsseizure of the property in the exact mannerrequired by §6335(a), which provides thatwritten notice must be “given by the Sec-retary to the owner of the property [or] leftat his usual place of abode or business.”Grable said that the statute required per-sonal service, not service by certified mail.

Darue removed the case to Federal Dis-trict Court as presenting a federal ques-tion, because the claim of title dependedon the interpretation of the notice statutein the federal tax law. The District Courtdeclined to remand the case at Grable’s be-hest after finding that the “claim does posea significant question of federal law,” Tr.17 (Apr. 2, 2001), and ruling that Grable’slack of a federal right of action to enforceits claim against Darue did not bar the ex-ercise of federal jurisdiction. On the mer-its, the court granted summary judgmentto Darue, holding that although §6335 byits terms required personal service, sub-stantial compliance with the statute wasenough. 207 F. Supp. 2d 694 (WD Mich.2002).

The Court of Appeals for the SixthCircuit affirmed. 377 F. 3d 592 (2004).On the jurisdictional question, the panelthought it sufficed that the title claimraised an issue of federal law that had tobe resolved, and implicated a substantialfederal interest (in construing federal taxlaw). The court went on to affirm the

April 3, 2006 698 2006–14 I.R.B.

District Court’s judgment on the merits.We granted certiorari on the jurisdictionalquestion alone,1 543 U. S. (2005) to re-solve a split within the Courts of Appealson whether Merrell Dow PharmaceuticalsInc. v. Thompson, 478 U. S. 804 (1986),always requires a federal cause of actionas a condition for exercising federal-ques-tion jurisdiction.2 We now affirm.

II

Darue was entitled to remove the quiettitle action if Grable could have broughtit in federal district court originally, 28U. S. C. §1441(a), as a civil action “aris-ing under the Constitution, laws, or treatiesof the United States,” §1331. This pro-vision for federal-question jurisdiction isinvoked by and large by plaintiffs plead-ing a cause of action created by federallaw (e.g., claims under 42 U. S. C. §1983).There is, however, another longstanding,if less frequently encountered, variety offederal “arising under” jurisdiction, thisCourt having recognized for nearly 100years that in certain cases federal questionjurisdiction will lie over state-law claimsthat implicate significant federal issues.E.g., Hopkins v. Walker, 244 U. S. 486,490–491 (1917). The doctrine captures thecommonsense notion that a federal courtought to be able to hear claims recognizedunder state law that nonetheless turn onsubstantial questions of federal law, andthus justify resort to the experience, solici-tude, and hope of uniformity that a federalforum offers on federal issues, see ALI,Study of the Division of Jurisdiction Be-tween State and Federal Courts 164–166(1968).

The classic example is Smith v. KansasCity Title & Trust Co., 255 U. S. 180(1921), a suit by a shareholder claimingthat the defendant corporation could notlawfully buy certain bonds of the NationalGovernment because their issuance wasunconstitutional. Although Missouri lawprovided the cause of action, the Court rec-ognized federal-question jurisdiction be-cause the principal issue in the case was thefederal constitutionality of the bond issue.Smith thus held, in a somewhat generousstatement of the scope of the doctrine, thata state-law claim could give rise to fed-

eral-question jurisdiction so long as it “ap-pears from the [complaint] that the right torelief depends upon the construction or ap-plication of [federal law].” Id., at 199.

The Smith statement has been subjectto some trimming to fit earlier and latercases recognizing the vitality of the ba-sic doctrine, but shying away from the ex-pansive view that mere need to apply fed-eral law in a state-law claim will sufficeto open the “arising under” door. As earlyas 1912, this Court had confined federal-question jurisdiction over state-law claimsto those that “really and substantially in-volv[e] a dispute or controversy respect-ing the validity, construction or effect of[federal] law.” Shulthis v. McDougal, 225U. S. 561, 569 (1912). This limitation wasthe ancestor of Justice Cardozo’s later ex-planation that a request to exercise fed-eral-question jurisdiction over a state ac-tion calls for a “common-sense accommo-dation of judgment to [the] kaleidoscopicsituations” that present a federal issue, in“a selective process which picks the sub-stantial causes out of the web and laysthe other ones aside.” Gully v. First Nat.Bank in Meridian, 299 U. S. 109, 117–118(1936). It has in fact become a constantrefrain in such cases that federal jurisdic-tion demands not only a contested federalissue, but a substantial one, indicating a se-rious federal interest in claiming the ad-vantages thought to be inherent in a fed-eral forum. E.g., Chicago v. InternationalCollege of Surgeons, 522 U. S. 156, 164(1997); Merrell Dow, supra, at 814, andn. 12; Franchise Tax Bd. of Cal. v.Construction Laborers Vacation Trust forSouthern Cal., 463 U. S. 1, 28 (1983).

But even when the state action disclosesa contested and substantial federal ques-tion, the exercise of federal jurisdiction issubject to a possible veto. For the federalissue will ultimately qualify for a federalforum only if federal jurisdiction is consis-tent with congressional judgment about thesound division of labor between state andfederal courts governing the application of§1331. Thus, Franchise Tax Bd. explainedthat the appropriateness of a federal forumto hear an embedded issue could be eval-uated only after considering the “welter ofissues regarding the interrelation of federal

and state authority and the proper man-agement of the federal judicial system.”Id., at 8. Because arising-under jurisdic-tion to hear a state-law claim always raisesthe possibility of upsetting the state-fed-eral line drawn (or at least assumed) byCongress, the presence of a disputed fed-eral issue and the ostensible importance ofa federal forum are never necessarily dis-positive; there must always be an assess-ment of any disruptive portent in exercis-ing federal jurisdiction. See also MerrellDow, supra, at 810.