bulgarian pension reform – stages, prerequisites and philosophy phd j. hristoskov

TRANSCRIPT

BULGARIAN PENSION REFORM – STAGES, PREREQUISITES AND

PHILOSOPHY

PhD J. HRISTOSKOV

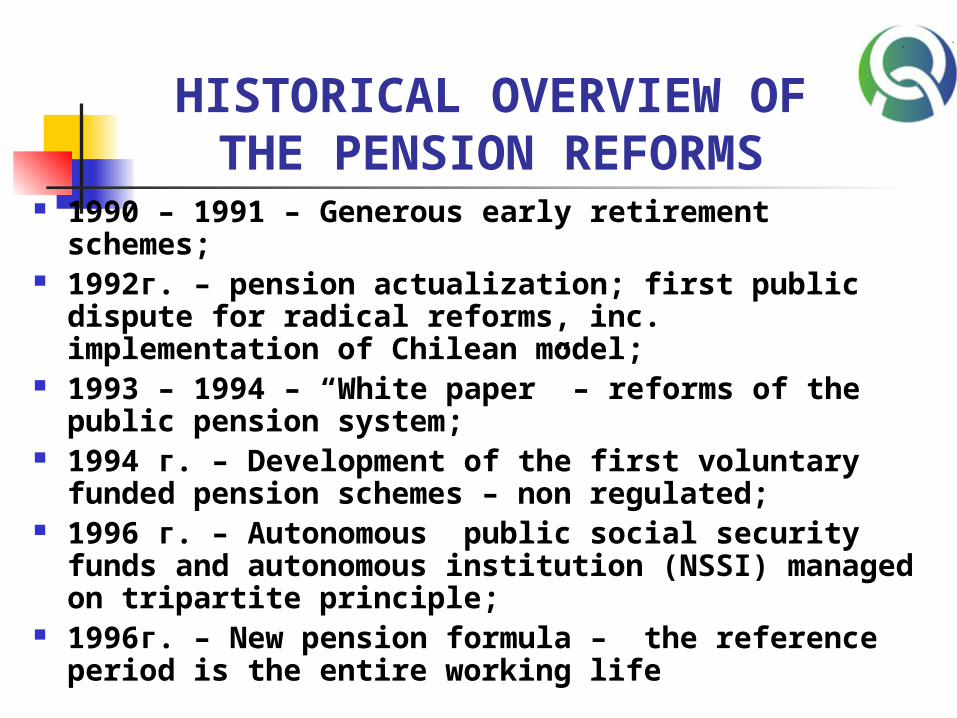

HISTORICAL OVERVIEW OF THE PENSION REFORMS

1990 – 1991 – Generous early retirement schemes;

1992г. – pension actualization; first public dispute for radical reforms, inc. implementation of Chilean model;

1993 – 1994 – “White paper” – reforms of the public pension system;

1994 г. – Development of the first voluntary funded pension schemes – non regulated;

1996 г. – Autonomous public social security funds and autonomous institution (NSSI) managed on tripartite principle;

1996г. – New pension formula – the reference period is the entire working life

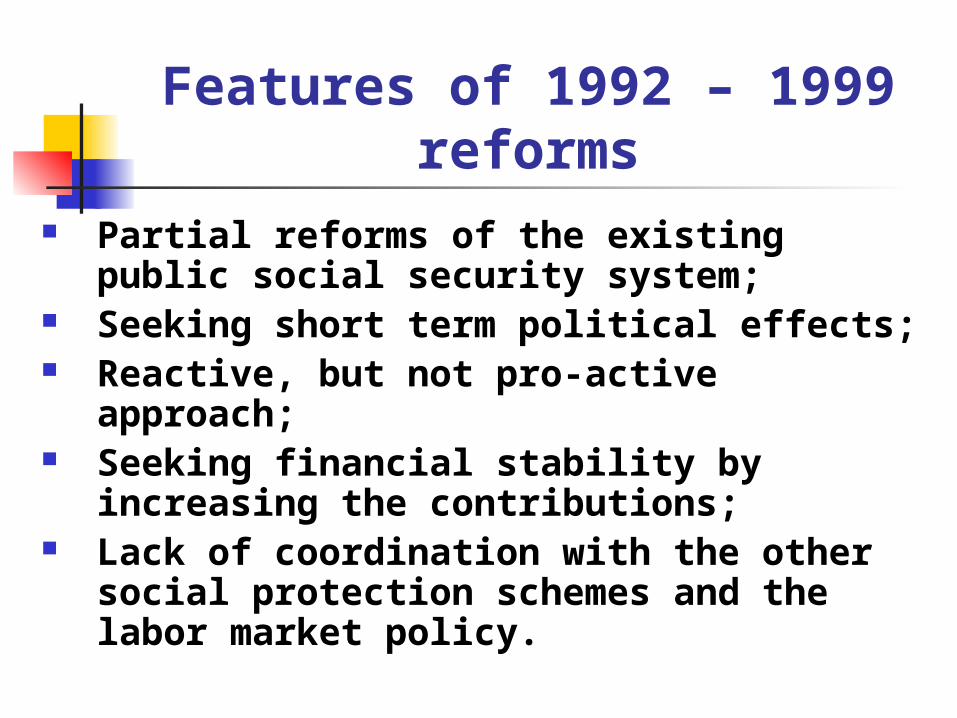

Features of 1992 – 1999 reforms

Partial reforms of the existing public social security system;

Seeking short term political effects; Reactive, but not pro-active

approach; Seeking financial stability by

increasing the contributions; Lack of coordination with the other

social protection schemes and the labor market policy.

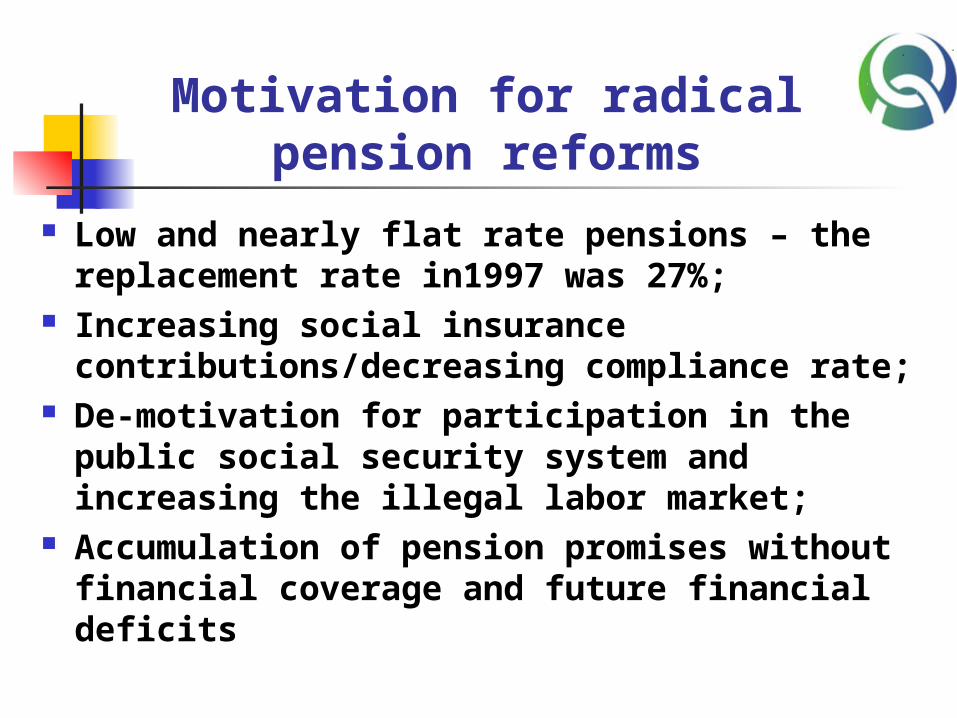

Motivation for radical pension reforms

Low and nearly flat rate pensions – the replacement rate in1997 was 27%;

Increasing social insurance contributions/decreasing compliance rate;

De-motivation for participation in the public social security system and increasing the illegal labor market;

Accumulation of pension promises without financial coverage and future financial deficits

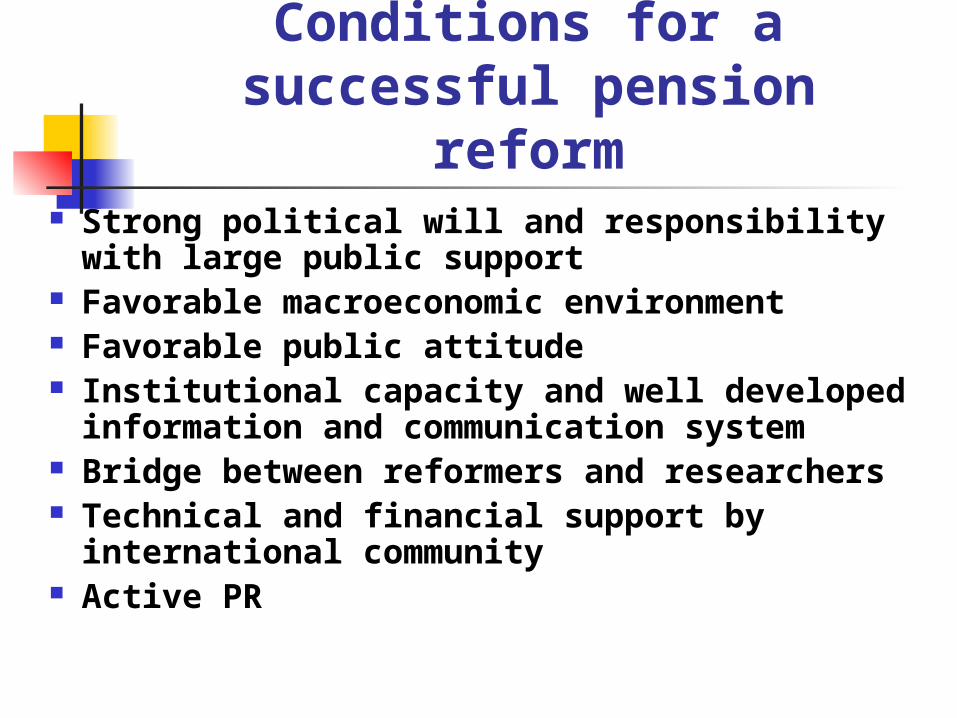

Conditions for a successful pension reform

Strong political will and responsibility with large public support

Favorable macroeconomic environment Favorable public attitude Institutional capacity and well developed

information and communication system Bridge between reformers and

researchers Technical and financial support by

international community Active PR

Philosophy framework of the pension reform

Based on the World Bank conception for multipillar social protection system, considering the national traditions and specificity:

Leading role of the solidarity PAYG system with changes in its parameters;

A new paradigm – building supplementary well regulated privately managed funded pension schemes – both mandatory and voluntary

Content of the parametric reforms in solidarity I-st pillar

Unification: covers all economically active population with incentives for labor mobility;

Supplemented with non-contributive pensions (old age and disability social pensions, personal pensions) – 0 pillar;

Establishment of fund “Pensions” based on contributions and fund “Non-labor pensions” based on state budget transfers;

Gradually shifting the early retirement pensions in special segment of the II-nd pillar;

Stronger qualifying condition for pension access.

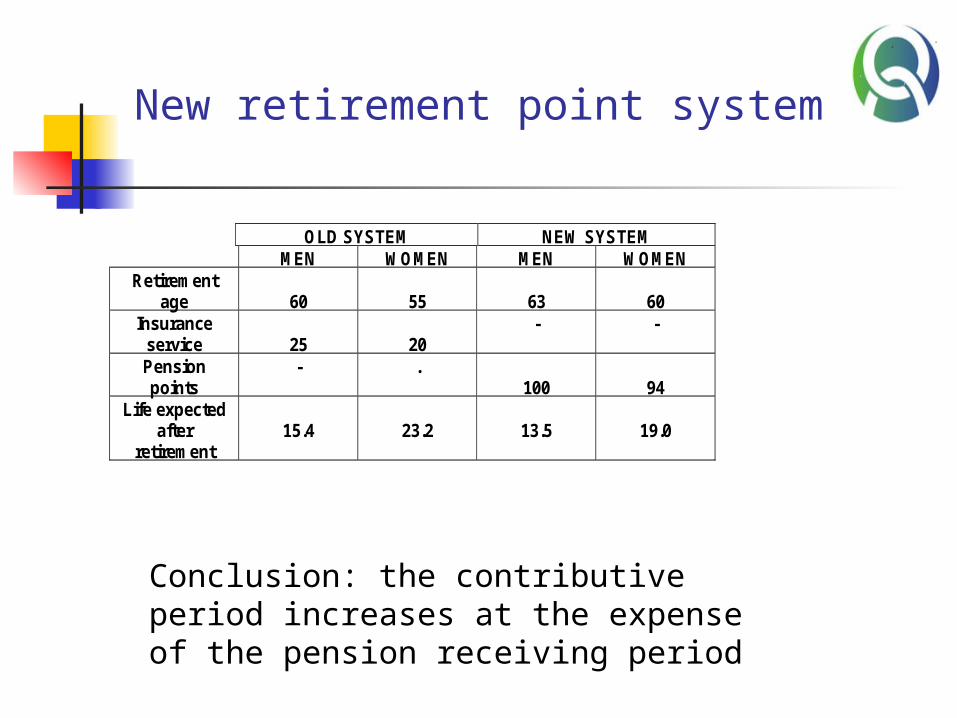

New retirement point system

OLD SYSTEM NEW SYSTEM MEN WOMEN MEN WOMEN

Retirement age

60

55

63

60

Insurance service

25

20

- -

Pension points

- . 100

94

Life expected after

retirement

15.4

23.2

13.5

19.0

Conclusion: the contributive period increases at the expense of the pension receiving period

Essential steps in the systematic part of the

pension reform Development of a mandatory funded II-nd pillar with

two types of pension funds: Occupational pension funds – early retirement pension

plans for those working in higher risk, sponsored by the employer;

Universal (open) pension funds – life time pension schemes for those born after 1959, sponsored by the employer and the employee;

Regulation of the voluntary pension insurance (funded III-rd pillar) based on voluntary contributions from the employers and personal savings. Tax incentives;

Establishment of a strong state regulator – integrated supervision for all non-bank financial institutions;

Codification of the State Public Insurance in one normative act – Social Insurance Code

Good public – private partnership

Adequacy of the reformed pension system

Access to pensions – almost full coverage of the population. Conflict points – high unemployment rate among the population in pre-retirement age;

Replacement rate from the three pillars (final goal of the reform) – 70 – 80%, as follows:

I-st solidarity pillar – 40%; II-d funded pillar – 20%; III-rd funded pillar - 10 – 20%

Current disappointment of the pension levels. Very thrifty pension indexation formula;

Individual accounts, good motivation and personal choice in II-d and II-rd pillar.

Pension adequacyFig. № 7. Replacement rate 2000 - 2008

53,8%53,3%53,0%51,3%49,7%49,6%49,9%48,2%51,1%

0

50

100

150

200

250

300

350

2000 г. 2001 г. 2002 г. 2003 г. 2004 г. 2005 г. 2006 г. 2007 г. 2008 г.

0%

10%

20%

30%

40%

50%

60%

Average pension per pensioner

Average insured income lv

REPLACEMENT RATE

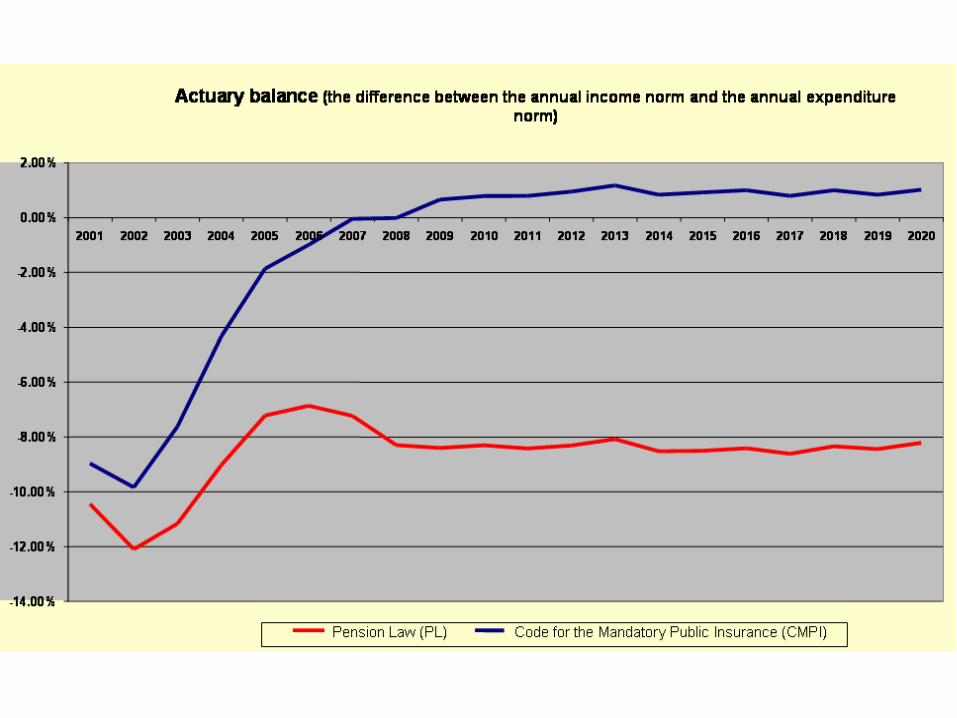

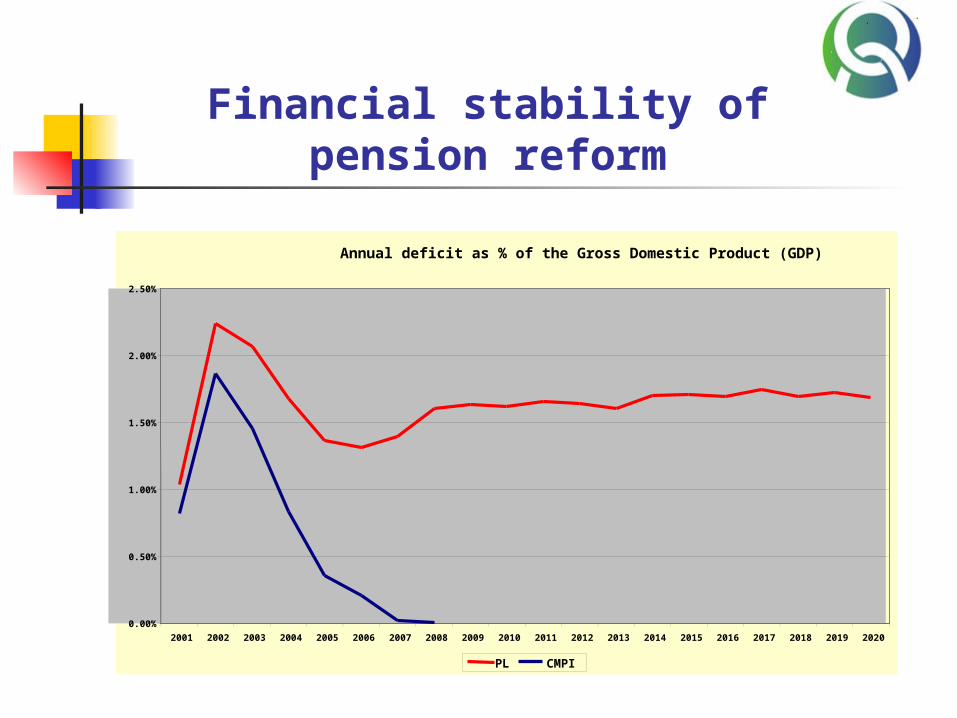

Financial stability of pension reform

Annual deficit as % of the Gross Domestic Product (GDP)

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PL CMPI

Deficit in the public pension system – reasons

Generous retirement regimes High dependency ratio - (0.98) –

aging and emigration Transfers to the occupational and

universal pension funds Incomplete coverage of the

insured persons Compliance problems Political will of decreasing the

contributions

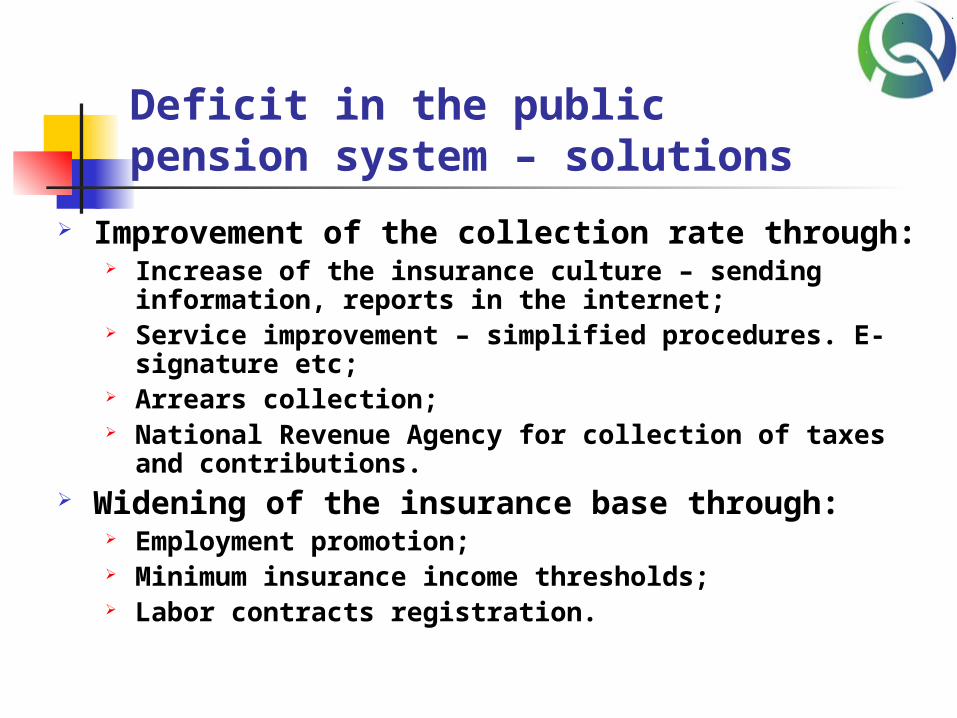

Deficit in the public pension system – solutions

Improvement of the collection rate through: Increase of the insurance culture – sending

information, reports in the internet; Service improvement – simplified procedures. E-

signature etc; Arrears collection; National Revenue Agency for collection of taxes and

contributions. Widening of the insurance base through:

Employment promotion; Minimum insurance income thresholds; Labor contracts registration.

Deficit in the public pension system – other solutions

Increase of the contributions – unacceptable decision

State Budget subsidy – current practice Credits from commercial banks – possible

decision only for the current (cash) deficit Incomes from privatization and other

sources – establishment of a reserve fund to cover the future deficits;

Debt financing – possible decision

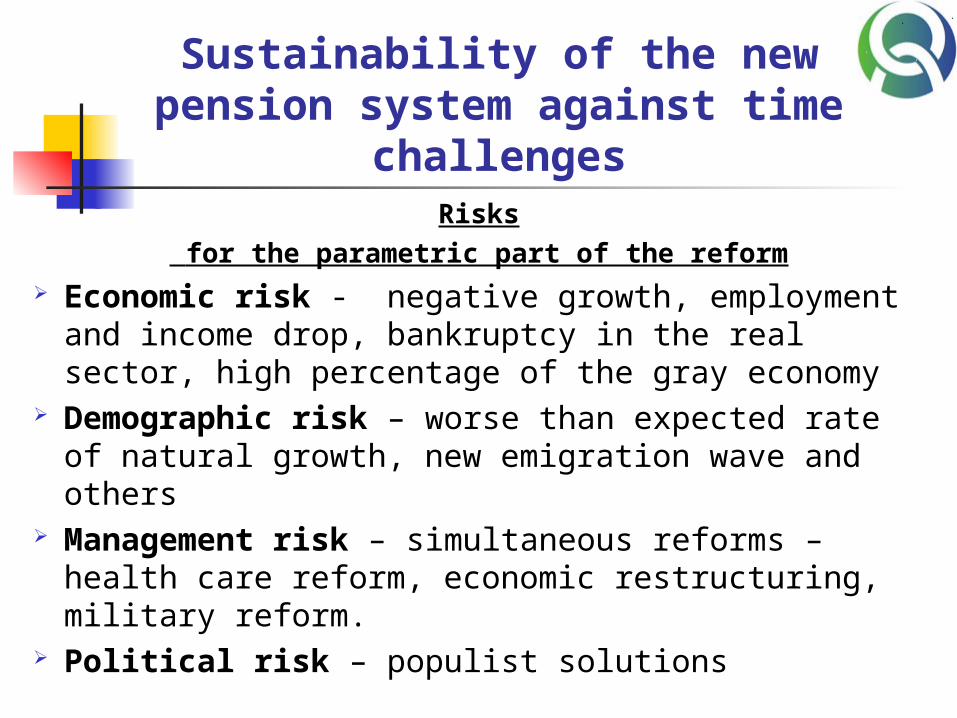

Sustainability of the new pension system against time

challengesRisks

for the parametric part of the reform Economic risk - negative growth, employment and

income drop, bankruptcy in the real sector, high percentage of the gray economy

Demographic risk – worse than expected rate of natural growth, new emigration wave and others

Management risk – simultaneous reforms – health care reform, economic restructuring, military reform.

Political risk – populist solutions

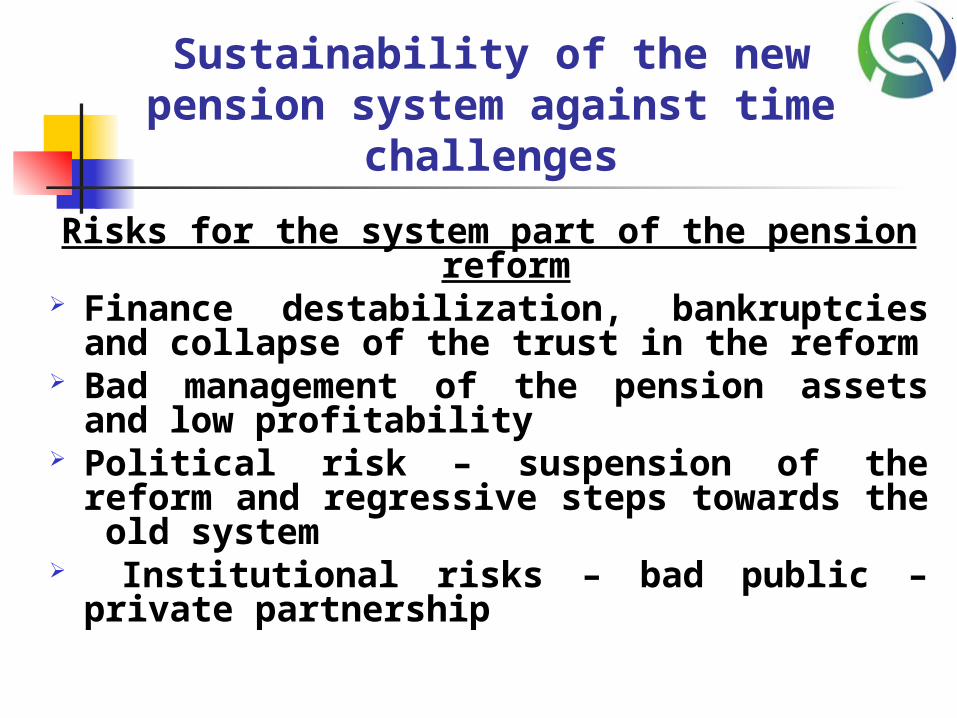

Sustainability of the new pension system against time

challenges

Risks for the system part of the pension reform

Finance destabilization, bankruptcies and collapse of the trust in the reform

Bad management of the pension assets and low profitability

Political risk – suspension of the reform and regressive steps towards the old system

Institutional risks – bad public – private partnership

Alternatives of the current pension model

Two alternative solutions are under discussion in the public space:

Absolute domination of the public PAYG system and restriction of the funded schemes only as a voluntary pension saving plans;

Privatization of the public pension system – the Chilean model

Why we should not rely only on the solidarity PAYG system?

The aging of the population and intensive emigration make the future pensions of present young generation very risky;

Lack of personal choice; Lack of motivation among the young

people to participate in the solidarity system;

Lack of accumulation and capitalization of pension assets.

Why we should not remove the public solidarity PAYG

system? PAYG system has a leading role in most of the

developed countries. It is one of the great achievements of the civilization;

It is almost impossible to reject (or to compensate) the accrued pension rights of the middle and pre-retirement age population;

The transitional costs are very high. The double price issue;

Bilateral and multilateral agreements in the social security area can not be canceled easily. EC - 1408 Regulation;

The social protection of the elderly population can not be exposed to the risk of the emerging capital market.

QUESTIONS