building the lp&i workforce of the future: is your organisation’s dna fit for the future?

TRANSCRIPT

Building the LP&I workforce of the future

Is your organisation’s DNA fit for the future?

2

The zeitgeist of disruption in life, pensions and investments (LP&I) is ongoing, with governments, regulators, economists and customers continuing to challenge and reset thinking and expectations in this long-established industry.

Much has been written about the need for LP&I providers to respond digitally, and many organisations are proactively taking their first tentative steps into the digital world. But Accenture believes that one critical component of this journey is being overlooked – the ‘Workforce of the Future’.

Being digital on the outside means being digital on the inside, and that has to start with the employees, their perspectives and the operating model and culture within which they operate. From now on, leaders must fundamentally change their organisations from within – creating more agile ways of working, sustaining efficiencies and capitalising on critical talent to support future growth.

Is your organisation’s DNA fit for the future?

3

The LP&I industry faces disruption from all sides. Intensifying and unpredictable regulation is a fact of life. Auto-enrolment and pensions reform are re-establishing the company workplace as a key market.

4

The LP&I workforce of the future

New, fierce sources of competition are proliferating – from non-core adjacent competitors (like Hargreaves Lansdown and Nutmeg), to online platforms and data champions (like Amazon and Google). And, already the norm in most other industries, strong digital capabilities are now essential – to meet new expectations from consumers for propositions that cater to every stage of their life journeys, provide a positive working environment for their own employees and enable a consolidated view of products.

These disruptive forces have been discussed at length in the boardroom in the context of providers’ processes and their technology – particularly where digital responses are concerned. But, as yet, few organisations have been able to make the move to digital with any conviction. In most cases, their journey is being blocked by a failure to identify and focus on one critical enabler – the ‘Workforce of the Future’.

Disruption has profound implications for an organisation’s DNA – not just in terms of identifying the types of roles that will be increasingly vital from now on (see Figure 1), but also the operating models and culture that will be best suited to a marketplace in constant flux. Now is the time for LP&I providers to make up for lost time and invest in building a workforce that’s fit for the future – agile, insightful and enabled by digital: a new DNA for a new future.

So what does this mean for your organisation? As a starting point, ask yourself whether your workforce currently thinks, acts and operates in a way that you are confident can address some of the key challenges facing the LP&I industry:

• How can we achieve customer relevance and generate customer lifetime value?

• How should we write risk in a digital world?

• Do we truly understand the impact of new distribution channels on my business?

• Do we know what our customers are saying and thinking, are we listening, and are we brave enough to test responses with them?

• What will tomorrow’s critical talent be and how can we optimally attract, retain and integrate it into today’s world?

• How do we optimise our business and operating models to execute our legacy and new worlds in parallel?

Organisations that shape and develop their workforce to identify answers to these questions will be the progressive LP&I providers of the future. But it’s a journey that calls for a rapid and radical reassessment of how work is done, by whom and where – as well as how the workforce can be changed incrementally over time.

5

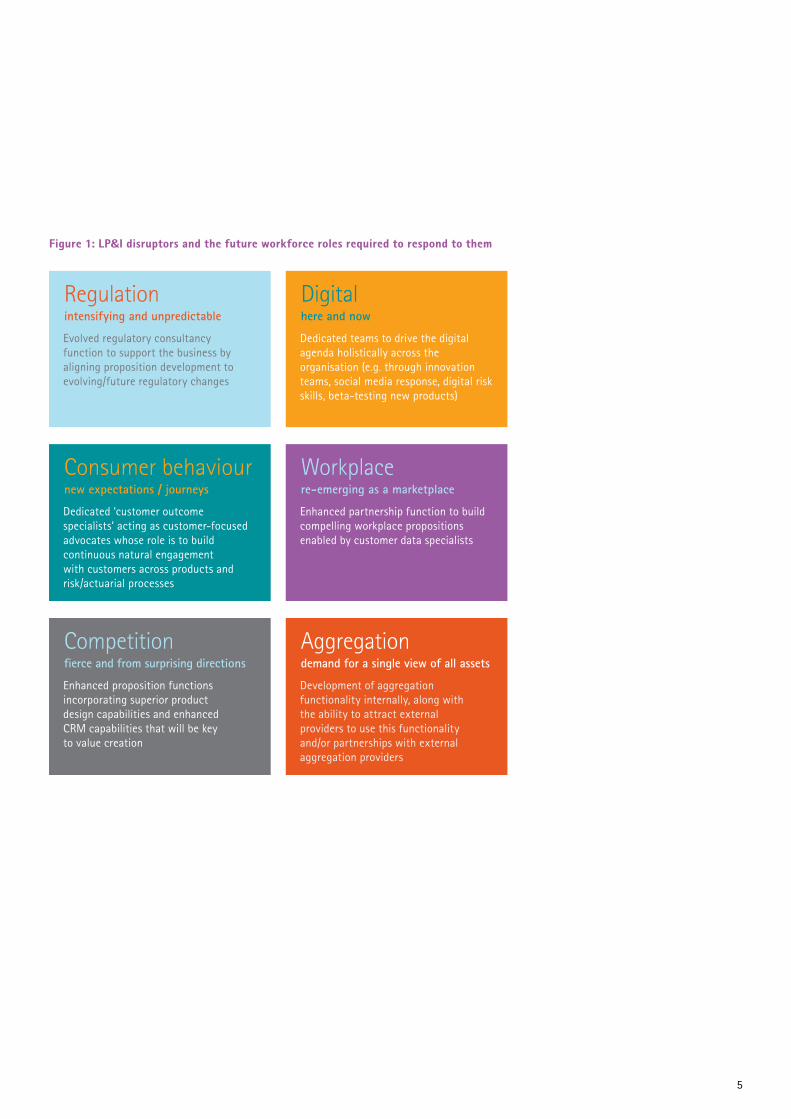

Figure 1: LP&I disruptors and the future workforce roles required to respond to them

Evolved regulatory consultancy function to support the business by aligning proposition development to evolving/future regulatory changes

Regulationintensifying and unpredictable

Dedicated teams to drive the digital agenda holistically across the organisation (e.g. through innovation teams, social media response, digital risk skills, beta-testing new products)

Digitalhere and now

Dedicated ‘customer outcome specialists’ acting as customer-focused advocates whose role is to build continuous natural engagement with customers across products and risk/actuarial processes

Consumer behaviour new expectations / journeys

Enhanced partnership function to build compelling workplace propositions enabled by customer data specialists

Workplace re-emerging as a marketplace

Enhanced proposition functions incorporating superior product design capabilities and enhanced CRM capabilities that will be key to value creation

Competitionfierce and from surprising directions

Development of aggregation functionality internally, along with the ability to attract external providers to use this functionality and/or partnerships with external aggregation providers

Aggregationdemand for a single view of all assets

6

Bring on the alchemists

Disruptive digital players, such as Google, pose a potent threat. With the ability to harness huge volumes of information (up to 37 million data-points per consumer in one recent programme), they have the raw material, and the technology know-how, to accurately predict consumers’ life journeys. From there, it’s a small step to targeting customised propositions at LP&I providers’ core marketplace. There is already speculation about Google and Amazon launching life insurance products in North America.1 And in the UK, we’re seeing movement in this direction with the recent launch of Google Compare for Car Insurance, a price comparison website.

The stark truth is that most LP&I providers do not have access to anything like the same quantity of data-points on consumers. And even if they did, they currently lack the digital capabilities needed to drive value from them. Research for the 2015 Accenture Technology Vision2 surveyed over 220 insurers worldwide: 56 percent of them said managing data is ‘extremely’ or ‘very’ challenging, considering changes in its volume, variety and velocity.

As providers seek to leverage these opportunities, an immediate priority must be creating, developing and harnessing two roles that will be increasingly vital that will be in increasing demand: data scientists to mine every available consumer data-point; harness this big data and use analytics to drive insights from it, and ‘proposition alchemists’ who

can take these insights and combine them with their in-depth business knowledge to differentiate propositions, and make them relevant to individual customers. We’re seeing these roles emerge, but their skills, heritage and placement in the organisational hierarchy vary significantly. Accordingly, many are left disenfranchised and disillusioned, reduced simply to processing poor data for management information (MI) rather than applying analytics to rich blends of internal and external data for product or customer strategy.

We believe these ‘proposition alchemists’ will be critical to the future of LP&I – enabling providers to offer more compelling, outcome-focused and personalised propositions. Alchemy, like insurance, has deep traditional roots that must not be forgotten when designing the future. Individuals and teams that can mix the right components in an organisation and bring them to the right customers at the right points in their journey, will succeed.

These skills, their place in the organisation and the associated governance and operating models, are a long way from the models of today. But they are key to the future. Much like Jung and Dhoni3, today’s alchemists must learn to blend myth (history), magic (innovation), religion (existing customers) and spirituality (capability and culture) and present them to the market and customers through the right channels and media.

Consumer behaviours are changing faster than ever before. Customers are less brand loyal, more price savvy and increasingly comfortable buying through digital channels and/or non-traditional players.

7

The intersection of humans and machines

Robotics process automation (RPA) is fundamentally changing the way all organisations operate. And with recent research4 predicting that 35 percent of UK jobs will be automated in the next 10-20 years, LP&I providers need to move fast to understand how increasing automation will transform the required skill and job mixes in core areas of the business – from claims management and underwriting support to policy processing and credit control. It will also deliver potentially huge cost savings. By creating, in effect, an automated virtual workforce that is not only far more accurate and efficient, but also works 24/7, we know that RPA can result in processing costs being cut by up to 80 percent in as little as three months.

Employees will increasingly be expected to develop working relationships with intelligent machines, and we’ll see these technologies dissolving the boundaries between today’s back-office and tomorrow’s front-office. Automated workflow and administration will drive higher job satisfaction through the eradication of monotonous tasks, freeing up individuals to augment capabilities elsewhere and focus on higher-value work. In our experience, people whose jobs are replaced by RPA have to upskill themselves from being ‘doers’ to becoming ‘developers’. Their jobs evolve into developing processes that instruct robots to follow a procedure – which in some cases is not just a shift in skills but also a significant leap in mindset for someone who has been doing the same job for decades.

By providing workers with more democratised and customised work experiences, together with interactive learning programmes and simpler, more effective ways of engaging with customers, automation enables more connected workforces. Employees enjoy a ‘complete’ relationship with the information they need to do their jobs – whether that’s instant access, via headset, to ‘how to’ videos for the field force, or transmitting data and content back to head-office to get a ‘crowd-sourced’ opinion on solving a problem. Remember too, automation and democratisation make organisations much more attractive to Millennials – critical potential recruits who bring with them vital talents and a whole new set of expectations, but who do not currently see LP&I as an attractive career choice.

As intelligent machines proliferate, change will be experienced at every level of the organisation. For example, the use of propensity modelling will transform the effectiveness of HR by identifying people most likely to respond to a job offer, or focusing retention activity on those most likely to churn. Meanwhile, managers will need to be willing to collapse silos and open up to extended workforces beyond their own walls, establishing digital platforms to create global talent exchanges that address skills shortages (including data scientists and proposition alchemists).

Business and technology leaders in LP&I providers must start to view software intelligence not as a pilot or a one-off project, but as an across-the-board functionality. This will demand a new acceptance by managers of what autonomy means – and how it changes the organisation’s DNA. We’ll see decision-making devolved to proposition alchemists empowered by valuable data, with automation playing a vital role in supporting the rapid creation and delivery of new propositions. This will enable providers to approach work as a ‘live’ experiment, with fluid, iterative, discovery-oriented design of products and processes – a must-have capability in a digital world.

Successful LP&I providers will recognise the benefits of human talent and intelligent technology working together – and they will embrace them both as critical members of the reimagined workforce.

8

No more ‘business as usual’

As a result, the way providers write risk must change immediately. Customers are already starting to look elsewhere, with group-buying websites like boughtbymany.com demonstrating the huge potential for digital disruption in this space.

Most insurers are still tied to a business model based on pooling risk, calculating average pricing and generating gross premium income. But analysts today have a very different take on performance. They’re seeking to break down these reporting and operational walls to get at underlying performance and customer-centricity. And the pooled risk model will come under even more pressure in the future as the Internet of Things, big data, digital channels, and artificial intelligence enable carriers to assess and price risk directly and individually.

In other words, ‘business as usual’ is becoming a thing of the past. The whole core of the industry needs to change by insurers adapting an experimentation mindset in which, unlike today, failure is acceptable so long as its lessons are captured in the organisation’s memory and incorporated in its DNA. This has major impacts for the LP&I

workforce. Leading providers are already thinking about how they can meet these new challenges by creating operating models based on experimentation and building agile, collaborative workforces composed of both people and machines. Test, learn, refine and test again: that’s the goal. But very few providers are ready to work this way and at speeds where actual customer impact can be meaningfully measured.

Social forums provide further opportunities. Providers with the capabilities needed to tap into these communities, and to manage their brand within them, will better understand how to delight their customers and continually evolve in line with their expectations. But gaining access to social forums and interacting with them successfully hinges on the ability to attract and retain the right people. And that, inexorably, comes down to the organisation’s DNA.

The market disrupters we’ve identified have implications far beyond the need for personalisation of propositions. The central tenet of insurance is shifting, with the fundamental concept of risk being reset through increased access to genetic testing, safer ways of living (e.g. driverless cars), real-time access to customer data (via telematics) and rapid medical advances.

9

Changing the DNA

So where and how to get started? We believe five steps stand out as clear priorities:

1. Empower next-generation leaders who want to make this happen – start small by incubating leaders who are not afraid to fail and learn.

2. Establish an evolving ‘two-speed’ operating model – organisational frameworks must support agile, flexible teams, enabled by an experimentation mindset, to adapt continually to changing business needs. But in the medium-term, these new models will likely co-exist with legacy models.

3. Lay foundations for merging front- and back-offices – increased automation pays dividends – both short and long term – through increased productivity and responsiveness. But it must be introduced in a way that ensures man and machine work effectively together.

4. Harness analytics at the next level – social media listening and big data have a vital role to play in informing personalised proposition designs. Having invested hugely post-RDR and to address Solvency II requirements, now’s the time to harness those investments, connecting them with external sources to provide powerful customer-centric strategic insights.

5. Manage critical talent proactively in the context of robotics – having identified the roles most likely to be replaced by machines, along with the key roles and employees that will be critical from now on, proactively establish strategies to reshape a workforce for the future – with data scientists and proposition alchemists at the core.

The organisation of the future is emerging. And as this happens, providers need to reimagine how they are structured, and how they operate. Changes across skills and competencies, management and leadership, and organisational cultures all need to be addressed. But this needs to be a subtle journey, one that allows organisations to navigate their legacy mindset and future worlds in a complementary fashion for several years.

10

Do you have what it takes?

One of the world’s oldest industries is changing faster than ever before, as new expectations from governments, regulators, economists and customers combine with technology innovation to transform the LP&I landscape. From now on, providers with the vision and commitment to shake up their DNA will position themselves for a sustainable and profitable future. The overriding priority? Create an environment that flexes and provides space for people to experiment – and shape a workforce that is agile, works successfully with machines, and is not afraid to fail.

11

Copyright © 2015 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with approximately 319,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$30.0 billion for the fiscal year ended Aug. 31, 2014. Its home page is www.accenture.com.

AuthorsWilliam Pritchett Managing Director, Insurance Head of Accenture UK&I Life & Pensions [email protected] +44 20 7844 5485

Sharad Mistry Senior Principal, Strategy [email protected] +44 77 6997 7559

Chloe Harmer Industry Solutions & Services Manager [email protected] +44 79 1904 2272

Mya Moe Industry Solutions & Services Consultant [email protected] +44 78 8194 3277

15-1012

References1 http://www.lifehealthpro.com/2014/06/23/ will-google-and-amazon-offer-one-click- life-insura?t=life-products

2 http://techtrends.accenture.com/us-en/it- technology-trends-2015.html

3 http://en.wikipedia.org/wiki/Psychology_ and_Alchemy

4 http://www.ft.com/cms/s/0/ba59685a-6821- 11e4-bcd5-00144feabdc0. html#axzz3UeJpZxTq