building deep-rooted empowerment. - muthoot. · building deep-rooted empowerment. ... vision and...

TRANSCRIPT

“Money entering a household through a woman brings more bene f i t s to t he f am i l y a s a who le . ” - Muhammad Yunus

ANNUAL REVIEW 2011-12

Building deep-rooted empowerment.

MUHOOT MAHILA MITRA5TH FLOOR, MUTHOOT TOWERS, ERNAKULAM - 682035. PH: 0484 4161678

www.muthoot.com www.muthoot.com/mmm

4

HIS VISION, ENTERPRISE,SIMPLICITY AND HUMANENESS

WILL FOREVER GUIDE US.

MUTHOOT PAPPACHAN

FOUNDER CHAIRMAN1927-2004

3

4

1. VISION AND MISSION

2. MESSAGE FROM THE MENTOR 01

3. CHIEF OPERATING OFFICER SPEAKS 02

4. MUTHOOT PAPPACHAN GROUP - AN OVERVIEW 03

5. MUTHOOT MAHILA MITRA 05

6. MANAGEMENT TEAM 09

7. HIGHLIGHTS 11

8. CORPORATE SOCIAL RESPONSIBILITY 15

9. CASE STUDY

10. CLIENT GALLERY 32

11. MUTHOOT MAHILA MITRA IN THE NEWS 36

12. FINANCIALS 2011-2012 41

13. RATIO ANALYSIS 43

14. IMPACT ASSESSMENT STUDY

TABLE OF CONTENTS

5

6

Vision To be the most successful microfinance company providing need based financial services to the needy and the un-served, and to contribute to the society and serve all stakeholders alike.

Mission To be among the top 3 microfinance companies in India by 2020, managing the best portfolio with presence in all possible corners of the country.

7

VISION AND MISSION

We are committed to truth, transparency and fair dealing.

Integrity and Quality

We provide sound advice and adopt the finest practices keeping the welfare of our customers in mind. Total customer satisfaction and growth are our objectives. Every member of the Group is responsible for upholding our principles in the workplace. We rigorously adhere to applicable laws, rules, regulations, codes and standards of good business practices.

Social responsibility

We promote sustainable development, responsibility towards the environment and upliftment of local communities in areas we operate. We identify and promote local talent. We believe in respecting the individual and encourage continuous learning.

Our people

We believe that people are our strength. Fostering teamwork, nurturing creativity, encouraging hard work, dedication, commitment and rewarding excellence are key elements of our human resource initiatives.

CORE VALUES

8

MESSAGE FROM THE MENTOR

Technology and Finance hold the key to eradicating poverty. The poor in India do not have adequate access to the formal banking; mainly due to the lack of good retail outlets offering banking services and also because the poor may lack assets that can be used as collaterals while taking loans. Illiteracy is perhaps another overwhelming hindrance.

Muthoot Pappachan Group is a diversified business conglomerate built on years of in-depth experience in financial services sector. It launched the Microfinance division in 2010 to focus on developing commercial relationships with microfinance institutions, networks and investors pan India, in order to expand access to financial services for the unbanked and the under banked.

Our support has helped to empower women by improving their economic welfare, and thereby promote gender equality. We ensure transparency in all activities, with a special focus on customer service. We have been constantly modifying our products and our processes with changing consumer expectations and mindsets, that too, at a truly commendable pace.

However, there are a few things that we take pride in not changing. Our passion for excellence.Our commitment to quality and our devotion towards delighting the customer.

The Microfinance division has been ranked as the second largest Micro-Finance Institution from Kerala in terms of outstanding loan amount. It provides services to more than two lakh clients, which is ever rising. The Company is well placed to comply with all regulatory changes while consolidating its position with increased focus on existing borrowers.

Looking back, FY 2011-12, was an important year for the progress of our Microfinance division. We have been able to double our outreach. The number of branches has increased from 40 in 2010-11 to 80 in 2011-12. The outstanding loan portfolio of the company has simultaneously increased to Rs.178.90 Cr. Our employee strength exclusively for the Microfinance Division has increased from less than 400 at the end of 2010-11 to more than 740 in 2011-12. Ultimately the profit (EBIT) of the company for the financial year 2011-12 was Rs.23.04 Cr as compared to 5.08 Cr in 2010-11. Further we have been able to spread our wings to support more than two lakh clients spread across Kerala, Tamil Nadu and Karnataka.

Muthoot Pappachan Foundation has been involved in various CSR Activities, the most prominent of which was the Skill Development Initiative supported by NABARD. The Skill Development Initiative aims at training women on various income generating projects such as dry flower arrangements, embroidery, basket making etc.

Another initiative by the Group is the Sthree Jyothi-Financial Literacy Training for women. Today the initiative covers three states - Kerala, Tamil Nadu and Karnataka. More than 8,000 women have been trained in Kerala alone and the company intends to spread this initiative to other parts of India.

We are proud of the fact that we have been ensuring strict compliance of the statutory requirements as mandated by the Ministry of Corporate Affairs, Reserve Bank of India and other regulators.

Ours is a young company, both in years and in attitude. We dream big and we are not afraid to try the seemingly impossible. I am sanguine about the rapid growth of the Microfinance division and that we will be ranked among the top three microfinance companies in India, soon.

01

9

Thomas MuthootExecutive Director

CHIEF OPERATING OFFICER SPEAKS :

W ith another successful year the Micro Finance Division of Muthoot Fincorp Limited, Muthoot Mahila Mitra (MMM), has now completed two years of successful and profitable operations. In the past two years Microfinance team has delivered on all objectives with which this business was launched two years ago. True to its stated vision, Microfinance unit has successfully contributed towards financial inclusion of large number of rural masses. In the FY 2011-12, with its network of 80 branches, MMM has increased its outreach to 2,95,000 households. In this financial year, MMM cumulatively disbursed loans worth Rs 380 crore in 3 states covering 22 districts in South. In addition to the credit assistance, Microfinance unit has also extended entrepreneurship & skill development training to more than 13000 clients, organised several medical camps and skill training workshops for the benefit of its clients.I am happy to share that the success of Microfinance has translated into profits of Rs 11.46 crore (PBT) for FY 2011-12 for Microfinance SBU. Overall Microfinance division has delivered on all parameters. Interest income has increased from Rs 8.23 crore in FY 2010-11 to Rs 33.32 crore in FY 2011-12, an increase of 400%. Number of branches has increased from 40 in FY 2010-11 to 80 by 31st March 2012. Portfolio under management has increased from 74 crore as on 31st March 2011 to 179 crore on 31st March 2012. On social performance parameters also MMM has delivered well, an independent impact assessment study done by IntelleCash reveals that around 50% of the clients of MMM have confirmed an increase in profit and sales after availing the MMM loan. Another 30% felt it has helped them to expand and grow their business and 3% of the entrepreneurs who have availed the MMM loan have been able to contribute in job creation thus leading to indirect employment generation. In the recently concluded survey done by MFIN, a leading microfinance industry association, the Micro Finance Division of Muthoot Fincorp Limited has been recognised as the 2nd fastest growing MFI (refer MFIN micro meters). This is a very significant recognition of our performance, especially when our portfolio quality continues to be the best in the industry with PAR 30+ remaining at 0.46% (46 bps).In coming years Muthoot Mahila Mitra operations would grow to newer heights. We plan to expand ouroperation to new locations such as Gujarat, Maharashtra and UP while continuing to focus majority of the operationsin South. Based on the growth and expansion of microfinance business and focusing on its long term vision Muthoot Pappachan Group plans to carve out microfinance business into a separate entity as a subsidiary of the flagship entity Muthoot Fincorp Limited. This subsidiary will work under the NBFC-MFI fold, which is in line with the mandate issued by RBI for Microfinance institution. This restructuring will lead to increase in operational efficiency of microfinance business and help us access cheaper funds by availing benefit of priority sector leading. I am happy to share with all stakeholders that the larger part of this structuring has already started and will be completed by September 2012.From microfinance industry prospective, with government keeping its focus firm on financial inclusion and RBI enabling microfinance industry to carry forward this agenda as reflected in RBI’s recent policies (priority sector guidelines), the scope for microfinance is enormous. Microfinance will continue to be the key component for last mile delivery of financial services to poor. Further boost for microfinance industry will come from Microfinance bill once it is passed in the Parliament and taking the shape of a full fledged Act. This will provide the industry much needed stability and regulatory clarity enabling MFIs to focus single-mindedly on upliftment of the poor. As these developments take place, our microfinance operations, with its robust growth and strong systems,procedures & policies in place, will continue to maintain and build excellent quality microfinance portfolio. This will put us in a good position ready to take the next leap and continue the journey of serving the society, to promote entrepreneurship, enabling financial inclusion to masses while meeting the requirements of needy andunderserved. I am convinced that Microfinance business will help us and our group to achieve its long term goals. “As we look ahead into the next century, leaders will be those who empower others.” – Bill Gates

02

10

Sadaf SayeedChief Operating Officer

MUTHOOT PAPPACHAN GROUP - AN OVERVIEW

The beginnings of the Muthoot Pappachan Group (MPG) can be traced back to Kozhencherry – a small town in Kerala, India. In 1887, Ninan Mathai Muthoot started a retail business which was later diversified into a finance business. In 1939, his sons established the Muthoot Chit Fund Enterprises that provided small and medium loans to farmers and merchants. Within a short span of 10 years, Muthoot Chit Fund Enterprises became a household name. They specialized in gold loans and advances to small enterprises and individuals on quick and easy terms. After a few successful years, Ninan Mathai Muthoot’s younger son, MathewM.Thomas or Muthoot Pappachan, as he is fondly known, branched off and founded the Muthoot Pappachan Group. Under Muthoot Pappachan’s watchful eyes, MPG expanded its financial services and diversified into hospitality, IT infrastructure, automotive,alternative energy and other business.

Today the Group has over 10,000 people serving more than one million loyal customers at offices and establishments across the Nation. Annual turnover is Rs. 20,000 crores (US$4.4 Billion), generated by the loyal customer base of over one million. Muthoot Pappachan Group enjoys a strong reputation in Kerala and Tamil Nadu, and has in recent years expanded its operations and reputation across India. The Group has articulated and built its reputation around its core values: Truth, Integrity and Quality, People and Social Responsibility.

Financial Services contributes to about 65% of the Group’s business. The Group has two Non Banking Finance Companies (NBFCs). Muthoot Fincorp Limited (MFL) which is the flagship Company of the Group and a market leader in the gold loan business; and Muthoot Capital Services Limited (MCSL), a public limited company registered with the Reserve Bank of India and listed on the Bombay Stock Exchange primarily focused on the auto financing segment and distribution of financial products.

Muthoot Housing Finance Company Limited (MHFCL) provides home purchase and construction loans to low income housing customers. MHFCL customers are primarily from the informal sector, who do not have income documents and are therefore excluded from the organized financial network. Set up in 2011, with the intention to cater to the huge demand for housing finance in the low income informal segment, the company offers loans from Rs 3-15 lakhs and in a short period of time has built up a loan portfolio of Rs 27 Cr. The company's home finance products extend the product line-up of the Muthoot Pappachan Group to a full suite of products, aimed at catering to the financial needs of the low income customer.

Muthoot Fincorp LimitedDesignated as a systemically important NBFC, the Company is a mass provider of finance in the form ofgold and other loans. With over 2200 branches spread across the cities, towns and villages of India,the Company serves an average of 40,000 customers a day. Muthoot Fincorp’s long-standing experience,expertise and stronghold in the semi - urban and rural areas have enabled the Company to provide quick, customized finance options and investment products, maximizing returns to the population. The loanproducts of Muthoot Fincorp are uniquely structured to serve people who do not have easy access tomainstream commercial banks.

The microfinance division of Muthoot Fincorp was established in 2010. It’s product Muthoot Mahila Mithra (MMM) provides micro credit facility to aspiring women entrepreneurs from weaker section of the society. Muthoot Mahila Mithra product has been designed after the famous 'Grameen model of microfinance' which is based on the concept of Joint Liability Group (JLG). MMM provides both financial aid and training to encourage and develop the spirit of entrepreneurship. So far, within a short span of a year theMicro Finance division has made a profit of Rs. 11.40 cr. (Before tax) for the FY 2011-2012. While achieving this, more importantly MMM has touched the lives of more than 2,95,000 household.

03

11

MUTHOOT MAHILA MITRA

A Small Step towards a Big Goal

Inspired by the Group’s decade long commitment to the common man and the poorest of poor, Muthoot Mahila Mitra (MMM) was launched in 2010 as the first product of Microfinance Initiative of Muthoot Fincorp Ltd., a Group Company of Muthoot Pappachan Group. MMM had its initial launch in March 2010 from Chullaimedu Branch (Chennai-1), Chennai, Tamilnadu. The division is now operating in three states namely Kerala, Tamilnadu & Karnataka and planning to spread its operation to Gujarat and Maharashtra soon.

Today this initiative serves as a voice and change agent for economically challenged women entrepreneurs. The Group’s goal is to identify talents and nurture entrepreneurs and innovators and through themtransform the lives of hundreds of people from economically and socially challenged backgrounds.

Business Model:

MMM is modelled after the famous Grameen Model of Micro Finance based on the concept of Joint Liability Group (JLG). Each JLG has a minimum of 5 members. Target clients are a group of 5-10 economically active females having regular cash flow through lawful, sustainable and stable economic activity. Members of JLG should be willing to take each other’s responsibility backed by mutual guarantee. MMM focuses on empowerment activities in rural areas and urban slums.

The underwriting norms lay herewith aim to appraise this profile based on cash flows, income stability, repayment capacity, business models and group guarantee. Emphasis has been laid on understanding the borrower’s weekly and monthly income, family income, household and other expenses and thereon the instalment affordability. The underwriting norms ensure that the customer borrows only as much as she can afford to repay every month during the tenure of the loan. Maximum care has been taken to avoid any exposure on an over-leveraged customer and avoid multiple lending as far as possible.

04

12

MICROFINANCE - INTRODUCTION

WHAT IS MICROFINANCE?

Microfinance began as a financial system to provide poor families with very small loans (micro-credit) to help members sustain income-generating activities.

Microfinance is being practiced as a tool to attack poverty the world over. The term “Microfinance” could be defined as “provision of thrift, credit and other financial services and products of very small amounts to the poor in rural, semi urban or urban areas, for enabling them to raise their income levels and improve living standards” (NABARD 99).

Microfinance Institutions (MFIs) are those, which provide thrift, credit and other financial services andproducts of very small amounts mainly to the poor in rural, semi-urban or urban areas for enabling them to raise their income level and improve living standards. Lately, the potential of MFIs as promising institutions to meet the consumption and micro-enterprise demands of the poor has been realized.

WHY MICROFINANCE?

Lack of capital has been identified as the single most important obstacle in helping poor come out of poverty. But providing money as a charity or subsidy has failed to have any appreciable impact. If the poor get money for free, they will not have any accountability for it. They rarely use such money for anyproductive purpose. To some extent it also makes the poor lazy till the money lasts. Besides, a one time capital cannot bring a person out of poverty. Poor need consistent and incremental source of credit and insurance. Charity cannot be sustained for all the poor or for very long. The customer unfriendly procedures and lack of collateral excludes the poor from banks. The provision of financial services is manpower intensive and banks do not have the manpower to support it. The only source available to such people is the local money lender. But the moneylenders charge heavy interest rates ranging from 5% to 10% per month. Microfinance provides the solution. It not only provides the poor with capital on easier terms, but makes him learn to utilize it.

There is huge demand for micro-credit estimated to $200 billion. The role of Microfinance institutions (MFIs) in providing services to the poor and helping them come out of poverty in a sustainable manner is immense.

05

13

THE CLIENTS OF MICROFINANCE

Microfinance clients are often described according to their poverty level – APL (above poverty line), BPL (below poverty line) other people at bottom of pyramid. This can obscure the fact that microfinance clients are a diverse group of people and require diverse products. While women clients make up a majority of clients and in some instances comprise 100 percent of an MFI’s clientele; small percentage of allMicrofinance clients are men also.

These clients operate small businesses, work on small farms, or work for themselves or others in a variety of businesses – fishing, carpentry, vegetable selling, small shops, transportation, rice flour and curry powder making, dairy products, catering unit, soda making units, garments and readymade, provisions store, tender coconut selling unit, laundry unit, mat weaving and cover making unit, the book binding unit, agricultural nursery, bakery and sweet product, tailoring unit, grinding unit, fish vending unit, bag manufacturing, pickle making, coconut products, bricks and hollow bricks units, herbal nursery unit, paddy cultivation, pappadam making unit, agarbatti and candle making unit, rubber cultivation, pineapple cultivation, spices cultivation and selling, soap making unit and much more. Some of these microfinance clients are trulyentrepreneurs - they enjoy creating and running their own businesses. Others become entrepreneurs by necessity when there are few jobs available in the formal sector.

HOW DOES MICROFINANCE HELP THE POOR?

Microfinance plays an important role in fighting the multi-dimensional aspects of poverty. Microfinance increases household income, which leads to attendant benefits: increased food security, the building of assets, and an increased likelihood of educating one’s children.

Microfinance is also a means for self-empowerment. It enables the poor, especially women, to become economic agents of change - they increase income, become business-owners and reduce their vulnerability to external dependence.

WHY IS MONEY LENT ONLY TO WOMEN?

Social development studies have demonstrated that women are much more likely to reinvest income into the household, for the benefit of the entire family.

By providing access to financial services only through women - making women responsible for loans,ensuring repayment through women, providing insurance coverage through women - microfinance programs send a strong message to households as well as to communities.

Many qualitative and quantitative studies have documented how access to financial services has improved the status of women within the family and the community. Women have become more assertive andconfident. In regions where women's mobility is strictly regulated, women have become more visible and are better able to negotiate the public sphere. Women own assets, including land and housing, and play a stronger role in decision making.

06

14

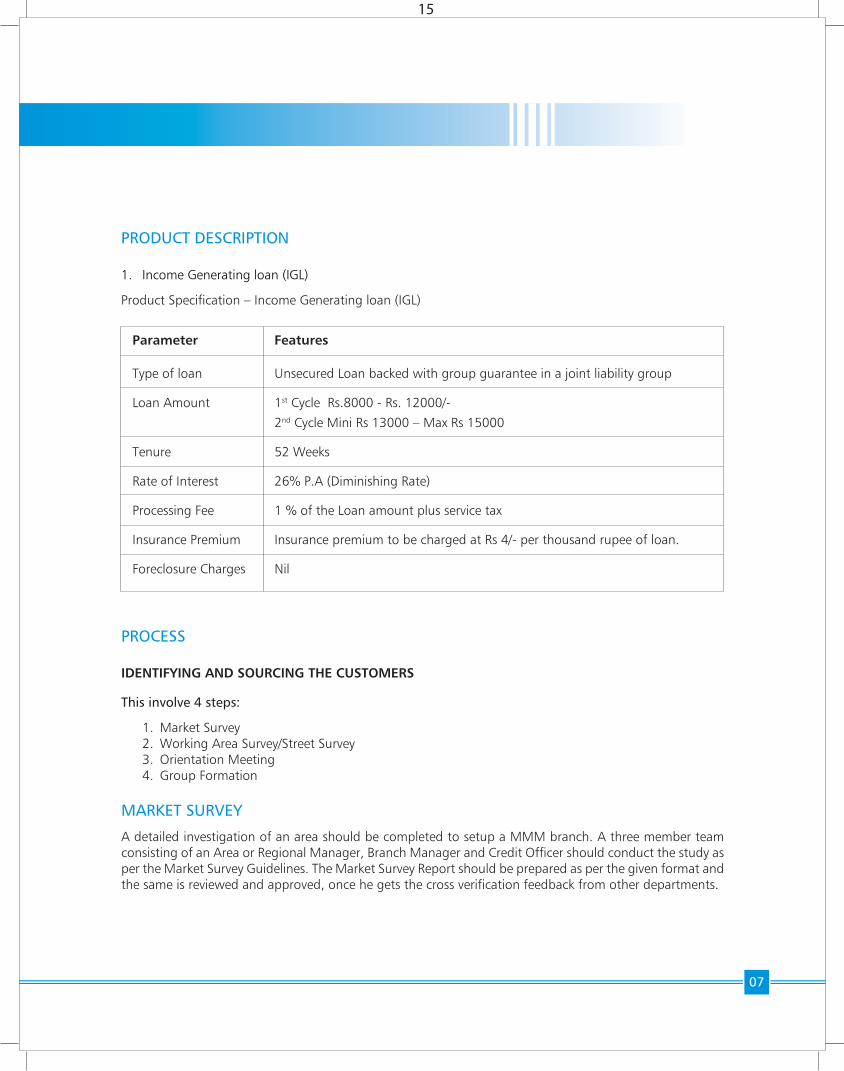

Parameter Features

Type of loan Unsecured Loan backed with group guarantee in a joint liability group

Loan Amount 1st Cycle Rs.8000 - Rs. 12000/-

2nd Cycle Mini Rs 13000 – Max Rs 15000

Tenure 52 Weeks

Rate of Interest 26% P.A (Diminishing Rate)

Processing Fee 1 % of the Loan amount plus service tax

Insurance Premium Insurance premium to be charged at Rs 4/- per thousand rupee of loan.

Foreclosure Charges Nil

PRODUCT DESCRIPTION

1. Income Generating loan (IGL)

Product Specification – Income Generating loan (IGL)

07

PROCESS

IDENTIFYING AND SOURCING THE CUSTOMERS

This involve 4 steps:

1. Market Survey 2. Working Area Survey/Street Survey 3. Orientation Meeting 4. Group Formation

MARKET SURVEY

A detailed investigation of an area should be completed to setup a MMM branch. A three member team consisting of an Area or Regional Manager, Branch Manager and Credit Officer should conduct the study as per the Market Survey Guidelines. The Market Survey Report should be prepared as per the given format and the same is reviewed and approved, once he gets the cross verification feedback from other departments.

15

08

STREET SURVEY/WORKING AREA SURVEYOnce the Market survey has been approved and branch has established working areas for each Relationship Officer he will undertake a street survey. The Street Survey refers to the process of collecting basic information about the families living in a particular street and is an important step in identifying potential customers.

ORIENTATION MEETINGA process of addressing a large number of potential customers of a locality at the same time as a beginning step of group formation. Staff will give a brief description about the company, criteria for providing loans, product description, documents needed and a question answer session to clear the doubts.

GROUP FORMATIONA group is a set of five to ten individual women from similar economic backgrounds or occupations, who know and trust each other and come together to become customers of Muthoot. Women should form these groups independently after the Orientation meeting.

RESIDENCE AND BUSINESS VERIFICATIONCredit Officer will conduct 100% house visit for all groups to ensure that non target customers and groupsare eliminated at this stage itself. The following will be checked:

1. Financial parameters like income limit, repayment capacity, multiple borrowing etc. 2. Qualitative parameters like group size, group criteria, group guarantee, residence check, standard of living etc.

COMPREHENSIVE GROUP TRAINING (CGT)Each applicant should undergo 3 days of comprehensive group training (CGT). The focus of the trainingshould be on developing a sense of group responsibility, terms and conditions of loan, product features, member and group discipline, responsibility of group leader, collecting necessary documents and fixingcenter meeting time and place etc.

GROUP RECOGNITION TEST

On the 4th day of the meeting credit officer should conduct a group recognition test to evaluate the eligibility of the client and also to understand that all client are familiar with each other, there are no agents involved in sourcing and all applicants are willing to take each other’s responsibility for repayment. Once the credit officer is convinced that all the criteria’s have been fulfilled then only a case should be approved for disbursement.

LOAN DISBURSEMENT If all criteria are met the Muthoot Mahila Mitra Loan will be disbursed through the Gold Loan Branches of Muthoot Fincorp Ltd.

COLLECTIONCollections are an integral part of the credit cycle as it helps to maintain the quality of the portfolio and frees up money to lend again. Muthoot strictly follow the code of conduct and best practices issued by MFIN for the collection process.

16

Has 5 years of experience in Banking and Micro Finance Industry. He is a management graduate from Lucknow University, started career with ICICI bank and later joined in

Satin Credit Care Network Ltd, were he handled Microfinance audit for 4 years. Joined Muthoot Mahila Mitra in November 2011.

Has over 8 years experiencein Banking and Financialsector. He is a graduate inMathematics, Post-graduate in Financial Management and a Post graduate diploma holder

in Taxation. He is also a Cost Accountant andassociated with Muthoot Pappachan group for the last 5 years.

Seby Cherian, Sr. Associate Vice President - Accounts

Handled across entire Retail loans sales, credit collections & Customer service with over 20 years experience in Retail Portfolio. Graduate in commerce from University of Madras,

worked with leading banks - ANZ Grindlays / Standard Chartered, HDFC, ING & DCB, withNBFC's - Sundaram Finance & Indiabulls Financial Services Ltd.

Sridhar MA - Head Risk and Fraud Control

Has over 9 years of experience in Banking and Financial service industry. He has worked with organisations such as HDFC Bank, GE Money and Spandana Sphoorty Financial Limited in

Credit and Risk Management functions. He has handson experience in policy making, credit administration, operations and Risk management. He has expertise in retail lending business with core competencies in unsecured small and large loans. He has worked with Spandana Sphoorty Financial Limited as Vice President Audit & credit Risk. He is a Graduate in commerce from Delhi University and MBA in Finance from Guru Gobind Singh Indraprastha University, Delhi. Sadaf has been associated with Muthoot Microfinance, group-lending business from the days of its inception.

MANAGEMENT TEAM

Sadaf Sayeed -Chief Operating Officer

He is hav ing 13 years ofexperience in MFI sector of which 6 years of experienceis in Training and HR, 3 yearsin Audit and 4 years in Operat ions. He is a Post

Graduate in Commerce and has worked with SHARE, Spandana Sphoorty Financial Ltd, Fullerton &Satin Credit Care Network Ltd.

Radhakrishna Eale -Senior Manager Training

Has 5 years of experience in HR and Administration. She is MBA in HR from Kerala Univers i ty . She has been associated with Muthoot Pappachan Group for the last

three and half years. She has worked with Kerala Kaumudi and UST Global-TEN.

Asha Anand,Senior Manager - HR

09

Dileep Kumar Pathak, Manager - Audit

He is having vast 8 years of experience in Retail Banking and Microfinance. Post graduate in Commerce. He has worked with many reputed banks like ICICI, ING Vysya and Fullerton.

He is associated with Muthoot Pappachan group for the last 5 years.

UdeeshUllas, Associate Vice President - Operations

17

10

HUMAN RESOURCES AND TRAININGThe Muthoot Mahila Mitra has a separate HR wing in coordination with the parent company. This is one of the key elements in attracting and retaining the talent. The Human Resource function has developed its capabilities and set up a scalable recruitment process, ongoing refresher trainings, periodical appraisals and other human resources management process, which enables to attract and retain higher calibre employees and encourage them to contribute more than 100% to the Company. The total manpower strength of the Microfinance team on March 31, 2012 was 744. With the help of training team, staff are trained to the policies and guidelines of the organisation. In addition refreshertrainings are conducted to the existing staff regularly for updating the current process and procedures.

ACCOUNTSThe Muthoot Mahila Mitra has a separate Accounts wing for tracking all expenses and payments. This ensures the costs are well within the budgeted figures. Productivity and variances are constantly monitored throughout the period through reports like cost variance analysis. The Real time accounts module with facilities like automatic cheque printing, E-net facility for direct credit help accurate, transparent and error-free transactions. New initiatives like mail/mobile alert for each payments and mobile phone based repayment mechanism are also introduced.

AUDIT AND RISKThe audit and risk division is vigilant about the quality of the portfolio and compliances of rules andregulations are followed in time. Regular audit as well as surprise audit is conducted in branches.The follow up mechanism to the audit report ensures the rectification measures are taken properly.

INFRA AND CENTRAL STORES DEPARTMENTIn order to facilitate the forms and stationary distribution throughout the locations, a central stores department is set up at HO. The request for each stationary is placed through an online ERP module and the despatch is tracked through courier POD in the system itself. In addition this division coordinates all infrastructure requirements for new branches and up keeping of existing branches.

18

4. Total Gross Loan portfolio as on 31.3.2012: Rs. 146,7510396 for IGL and for SW Rs. 32,15,46,157 (Total Rs. 178,90,56,553)

5. Profit before tax for 2011-2012: 11.46 Cr. (PBIT: Rs. 23.04 Cr)

6. Active member in MFIN and KAMFI

7. Tie up with High Mark Credit Bureau for credit information report.

8. 11 crore Term Loan to other Microfinance Institutions.

9. Second Largest MFI in Kerala.

HIGHLIGHTS

1. Interest charge in line with RBI/ Malegam committee report from inception.

2. 80 branch across 4 states in a short span of time

3. DISBURSEMENT HIGHLIGHTS:

11

FROM INCEPTION

TOTALSWIGL

38729270475764176982560472806063174671000295811

AMT (Rs)NOAMT (Rs)NOAMT (Rs)NO

2011-2012

TOTALSWIGL

28990889374122485351139371984692363975000213779

AMT (Rs)NOAMT (Rs)NOAMT (Rs)NO

2010-2011

TOTALSWIGL

9738381101641691631421108213781069600082032

AMT (Rs)NOAMT (Rs)NOAMT (Rs)NO

19

2. OUTSTANDING LOAN PORTFOLIO

MILESTONES

1. BRANCH NETWORK

12

BRANCH NETWORK

0

Mar

-11

Feb-

11

Jan-

11

Mar

-12

Feb-

12

Jan-

12

Dec

-11

Nov

-11

Oct

-11

Sep-

11

Aug

-11

Jul-1

1

Jun-

11

May

-11

Apr

-11

Dec

-10

Nov

-10

Oct

-10

Sep-

10

Aug

-10

Jul-1

0

Jun-

10

May

-10

Apr

-10

2040

60

80

100

120140

160

180

200

74

178.90

Figu

res

In C

ore

40 BRANCHES

MMM Portfolio

2011 - 20122010 - 2011

80 BRANCHES

0102030405060708090

20

3. EMPLOYEE STRENGTH

13

4. OUTSTANDING GROWTH:

April 2011 : Rs. 74,14,60,746 Sept 2011 : Rs. 116,44,63,046 March 2012 : Rs. 178,90,56,553

EMPLOYEE STRENGTH

Dec/11

Apr/11

800700600500400

378

566

744

3002001000

Jun/11

Aug/11

Oct/11

Feb/12

21

14

5. DISBURSEMENT GROWTH FROM INCEPTION (IGL)

April 2011 : 81,06,96,000 (82,032 nos) Sept 2011 : 152,75,47,000 (1,50,818 nos) March 2012 : 317,46,71000 (295,811 nos)

OUTSTANDING GROWTH

DISBURSEMENT GROWTH - IGL

0.00

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

3,000,000,000

3,500,000,000

0

Mar

...

Feb.

..Ja

n...

Dec...

Nov...

Oct...

Sep.

..

Aug...

Jul...

Jun.

..M

a...

Apr...

Mar

...

Feb.

..

Jan.

..

Dec

...

Nov

...

Oct

...

Sep.

..

Aug

...

Jul..

.

Jun.

..

Ma.

..

Apr

...

200,000,000400,000,000600,000,000800,000,000

1,000,000,0001,200,000,0001,400,000,0001,600,000,0001,800,000,0002,000,000,000

741460746

1527547000

3174671000

1164463046

1789056553

810696000

22

15

CORPORATE SOCIAL RESPONSIBILITY:

Corporate social responsibility (CSR, also called corporate responsibility, corporate citizenship, and responsible business) is a concept whereby organizations consider the interests of society by taking responsibility for the impact of their activities on customers, suppliers, employees, shareholders, communities and other stakeholders, as well as the environment. This obligation is seen to extend beyond the statutory obligation to comply with legislation and sees organizations voluntarily taking further steps to improve the quality of life for employees and their families as well as for the local community and society at large.

Benefits for Entrepreneurs

1. Increased self confidence 2. Enhanced knowledge and skill to promote potential revenue generation source.3. Improved communication skills 4. Enhanced cash management with ability to analyse basis of cash flow5. Opportunity to learn new products and expand the business.

A) STHREEJYOTI - EMPOWERING WOMENThis entrepreneurial training programme has been launched under the corporate social responsibility of Muthoot Pappachan group in partnership with Accion India for the women entrepreneurs in Kerala,Karnataka and Tamilnadu states. The objective of this training is to achieve greater competitiveness through the development of the managerial abilities of women entrepreneurs and contribute to the improvement of their quality of life.

23

16

FINANCIAL LITERACY TRAINING :

Courses offered - Stree Jyothi Financial Literacy programme

1. Self management: Women can make very successful enterprises based on the fact that they have the built in capacity to perform multi-task. The training will help women who want to become entrepreneurs - to think of a business idea, build a vision, implement their idea and use available financial resources.

2. Cash management: Cash management is very vital for the short term stability and long term survival of the enterprise. This module provides basic concepts and tools necessary for the management of cash resources.

3. Leadership: This module address some questions like can an average person can be leader, what are the attributes needed, How the leadership style can be used for business promotion etc.

4. Idea to business: This is designed for entrepreneurs who have made the decision to to start a business. This module helps the entrepreneur to overcome hurdles and implement methods and strategies.

5. Business feasibility: This module is designed to support Entrepreneures who have several ideas for starting a business by evaluating the feasibility.

6. Entrepreneurial management: It helps to recognize and evaluate inherent skills and constantly think of ways and means to improve the business.

7. Savings and Investment: Money management is the lifeline of a business venture. This module helps entrepreneurs to assess their initial situation, look for opportunities, take wise decisions and enjoy a positive outcome.

8. Debt management: The objective of this module is to help the entrepreneur to dispel myths about the dangers of debt and get a clear notion of its inherent features, both advantages and disadvantages.

9. Communication and promotion: Communicating effectively with clients, suppliers, financial institutions and marketing provides the stimulus for the growth of the organisation and this training will lay foundation for an area which all entrepreneurs could constantly improve upon for better and results.

24

Total Clients Trained:

17

B) SKILL DEVELOPMENT INITIATIVE (SDI) Supported by NABARD and Accion India:

This aims at providing training for manufacturing different eco friendly Handicraft and Home Decor products. This unique training module will help a multitude of women Entrepreneurs achieve greater competitiveness through the development of their skills and managerial abilities.

Products Trained:

1. Grass bouquet2. Potpuri3. Lilly pot4. Bowls and Balls5. Grass bunch & Hand bunch6. Eco style Banana Fibre Products7. Natural Fibre products8. Jute products 9. Dry flowers.10. Eco Pac Bags11. Paper bags

STATE NO OF CLIENTS MODULES DELIVERED

KERALA 8,757 20,362

TAMIL NADU 3,303 5,494

KARNATAKA 4,783 9,804

TOTAL 16,843 35,660

Clients at work:

25

Skill development training for products include nests made of palm fiber, dryflowers, banana fiber products etc.

Skill Development Trainings:-

18

26

Products made from Palm Fibre, Pineapple Leaf and Banana Fibre are shown.

19

27

20

The Wheel of Fortune……!

As we enter the neighborhood of Ms. Leelamani, there is something which makes her house apart from others, the rhythmic sound of sewing / tailoring machine from the house. For Leelamani in her early forties, sewing was her livelihood for the past twenty years. She catered the neighborhood tailoring orders and piece work of ‘nighty’ (a gown like night wear for ladies) from the big textiles of the Kottayam Town to sustain her living. She recollects that, during that time she felt that she was just a part of a ‘big machine’ which produces clothes. She earned Rs 7/- per ‘nighty’ to the tune of Rs 49/- max per day (seven nighty’s). Followed by four visits to the town for delivering the stitched materials adding the transportation expense to her meagre income. As a single woman living in a rented house, goodwill of the neighbourhood was her only asset.

For the last eleven months she was feeling something different. The wheel of sewing machine continues to rotate, but in a different dimension. Leelamani came to know about the Income Generating Loan

(IGL) of Muthoot Mahila Mithra (MMM) through her friends and attended an orientation by MMMRelationship Officer. During the orientation she came to know about ‘Sthreejyothi’ - the exclusive training wing of MMM for providing entrepreneurial training to the women entrepreneurs. At that time she felt ’Sthreejyothi’ was just another routine exercise before loan disbursal. The sessions on entrepreneurial development by Sthree jyothi team motivated her to explore the available opportunities with existing man power with an entrepreneurial insight.

She invested the MMM loan amount for the procurement of raw materials of nighty (Rs 110/- per piece) and stitched around four to six pieces a day. She sold it to the neighborhood for Rs.160/-, earning Rs.50/- a piece to a tune of Rs 200 to Rs 300 per day. Apart from direct selling, she also ensures the help of two members of the MMM group to sell it among their friends and relatives by sharing a percentage of profit. She was motivated and guided by the MMM team through their periodic visits. Leelamani felt that the periodic sthreejyothi training encourages her do more market analysis and maintaining accounts in a structured way. She opines that the raw material cost can be brought down if the purchases are made in a large scale, and expand her business into next phase. Leelamani evolved from a person who just thought herself as a part of ‘Big Machine’ to an entrepreneur who visualize a ‘Big Industry.’

Place: Sankranti, Kottayam

LOAN NO: SHMT#76.

28

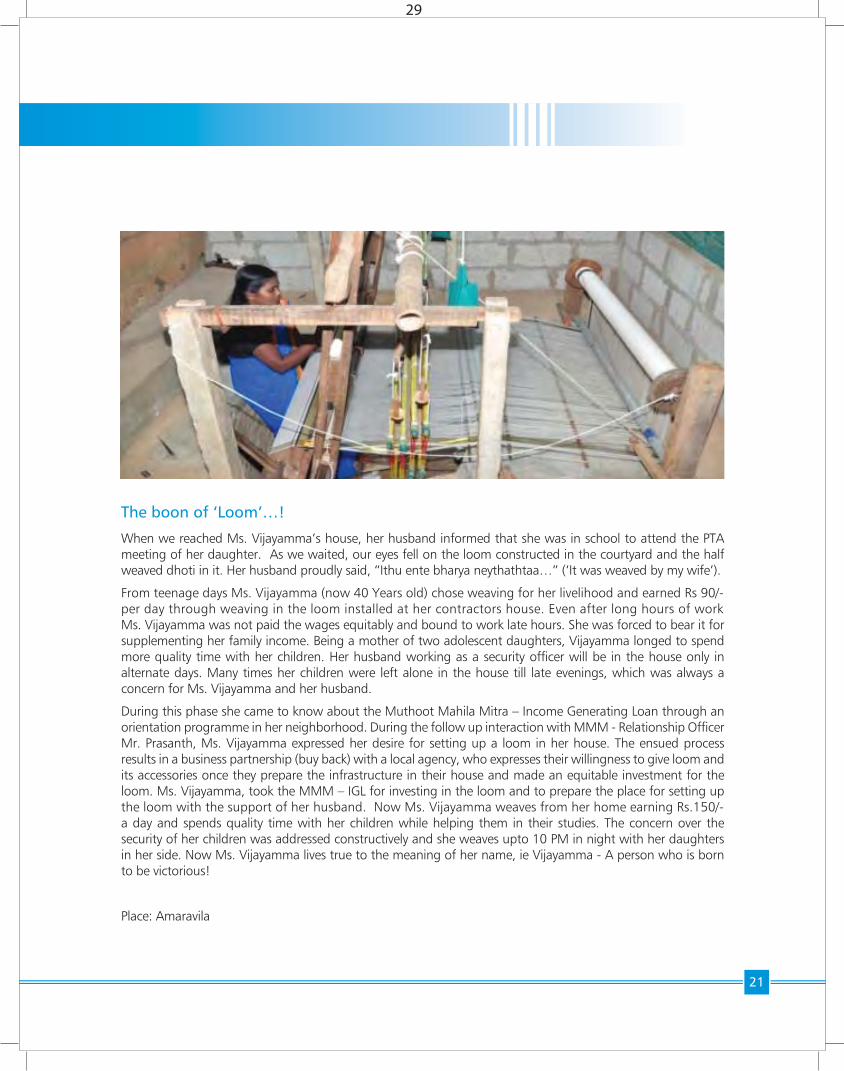

The boon of ‘Loom’…!

When we reached Ms. Vijayamma’s house, her husband informed that she was in school to attend the PTA meeting of her daughter. As we waited, our eyes fell on the loom constructed in the courtyard and the half weaved dhoti in it. Her husband proudly said, “Ithu ente bharya neythathtaa…” (‘It was weaved by my wife’).

From teenage days Ms. Vijayamma (now 40 Years old) chose weaving for her livelihood and earned Rs 90/-per day through weaving in the loom installed at her contractors house. Even after long hours of workMs. Vijayamma was not paid the wages equitably and bound to work late hours. She was forced to bear it for supplementing her family income. Being a mother of two adolescent daughters, Vijayamma longed to spend more quality time with her children. Her husband working as a security officer will be in the house only in alternate days. Many times her children were left alone in the house till late evenings, which was always a concern for Ms. Vijayamma and her husband.

During this phase she came to know about the Muthoot Mahila Mitra – Income Generating Loan through an orientation programme in her neighborhood. During the follow up interaction with MMM - Relationship Officer Mr. Prasanth, Ms. Vijayamma expressed her desire for setting up a loom in her house. The ensued process results in a business partnership (buy back) with a local agency, who expresses their willingness to give loom and its accessories once they prepare the infrastructure in their house and made an equitable investment for the loom. Ms. Vijayamma, took the MMM – IGL for investing in the loom and to prepare the place for setting up the loom with the support of her husband. Now Ms. Vijayamma weaves from her home earning Rs.150/- a day and spends quality time with her children while helping them in their studies. The concern over the security of her children was addressed constructively and she weaves upto 10 PM in night with her daughters in her side. Now Ms. Vijayamma lives true to the meaning of her name, ie Vijayamma - A person who is born to be victorious!

Place: Amaravila

21

29

The ‘Friends’

The roar of jet engines coupled with sea breeze ushers us into a compound located between the famed Shangumugham Beach and Domestic Airport Terminal of Trivandrum. When we step into the compound having two houses, the aroma of homemade sweet stimulated our nostrils. In midst of clattering vessels, five energetic women were engaged in different activities of food processing. The local sweets known as unniyappam, munthirikothu, achappam etc are dished out in periodic succession.In between their hectic activity they eagerly shared their entrepreneurial experiences – The ‘Friends’ experience.

During the orientation on self management in Sthreejyothi training, the five housewives (Ms. Binitha, Ms. Sabeena, Ms. Saifunisa, Ms. Shaheeda, and Ms. Tajumaa) who previously idle their day time, thought of initiating something productively. And it started as a simple initiative of processing rice flour for local dishes to the taste of their neighbours. Following the encouraging responses from the community and family members they diversified to local savories’ too. ‘Friends’ was the name, they given to this entrepreneurial association developed as an offshoot of the Muthoot Mahila Mithra (MMM) Centre in their neighborhood. Their initiatives got support from other big catering service providers, as they give orders for making some dishes. The first exclusive catering service order they executed too has its uniqueness; it was provided for the trainees of NABARD – Skill Development Initiative (SDI) training participants.

“Not like early days… now we learned… how to take orders… things to be considered… maintaining the accounts” quotes Ms. Saifunisaa. Her husband who owns an auto rickshaw helps in transporting the finished products. The ‘Friends’ gratefully acknowledges the timely support of Ms. Ayeshumma, the mother of Ms. Saifanusia for their initiatives. The profit from the catering business was invested in cloth business by the group. The group procures ‘Nighties’ – a night dress for women, at wholesale price from the dealers and retails it among the neighbors’. This enhances the visibility and customer base of ‘Friends’. "We are like the five fingers in our hand and that’s our strength" concludesMs. Binitha. The ‘Friends’ experience gave us insight into the effective team work and family support.

MMM Branch: Trivandrum 1

22

30

C) CSR ACTIVITIES BY MUTHOOT MAHILA MITRA:

Free Medical Camps:

A General health camp was organized by Muthoot Mahila Mitra-Puducherry in association with Sri Lakshmi Narayana Institute of Medical Science & Hospital-Puducherry (SLIMS) to provide basic health care to its customers at Vennila Nagar, Kamarajar Salai and Puducherry on 8th October 2011.

23

Check up and supply of medicines

The camp was inaugurated by Thiru N. Rangasamy, Hon’ble Chief Minister, Pondicherry.

31

Muthoot Mahila Mitra and PSG Hospital, Coimbatore at the Sri Lakshmi Mahal, Kannampalyam,Coimbatore on Sunday 24th July 2011.

The camp was organized to provide free medical services to all clients in Karumathampatty MM branch and over 223 people turned up for the camp; All were treated and some cases referred to PSG. The organization took the responsibility of providing all necessary logistics including Medicines/Drugs, Accommodation, Meals andTransport. The services carried out were Child Clinic, General Clinic, Medical Clinic, BP Check up and Gynaecology.

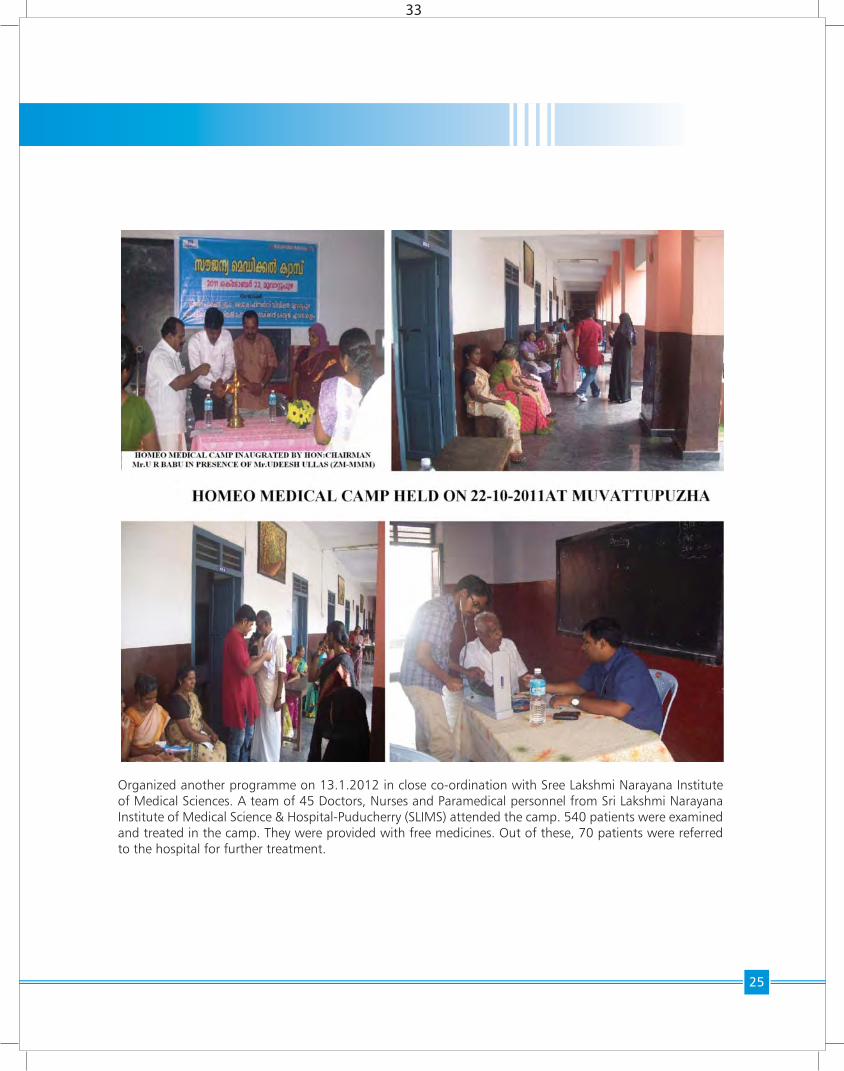

Free Homeo Medical camp at Muvattupuzha, Kerala along with Dr Padiyar MemmorialHomeo Medical College, Ernakulam on 22/10/2011.

Inauguration by Chief Doctor

24

CONSULTATION AND CHECK UP

32

25

Organized another programme on 13.1.2012 in close co-ordination with Sree Lakshmi Narayana Institute of Medical Sciences. A team of 45 Doctors, Nurses and Paramedical personnel from Sri Lakshmi Narayana Institute of Medical Science & Hospital-Puducherry (SLIMS) attended the camp. 540 patients were examined and treated in the camp. They were provided with free medicines. Out of these, 70 patients were referred to the hospital for further treatment.

33

26

Muthoot Fincorp Limited CEO, Mr. Suhas Soman, inaugurates the camp in the presence of Ministers.

Client Interaction Programmes:The first client interaction programme was conducted by Palakkad 2 branch on 27th April 2011. It was a skill training programme in which the resource person has trained our clients about making of Wash Soap, Bath Soap and Pine Oil. In the programme, 39 clients from different centres of Palakkad-2 activelyparticipated and we received good response from all of them.

The second Client Interaction Programme was held at Wadakkancherry, Kerala on 28th April 2011. It was also a skill training programme, in which 36 clients from 9 different centres actively participated.

Conducted another client interaction programme in Kunnamkulam, Kerala on 14th May 2011 at LIWA Towers, Kunnamkulam. It was a skill training, in which given training in "Screen Printing on Sarees & other related works". 41 clients from 14 centres actively participated in the training.

34

Class room sessionsThe trainer addressing the participants

Skill trainingThe participants

27

Conducted a Product Training Programme (Mushroom Cultivation) at North Paravur, Ernakulam house on 23rd July 2011.The one day training programme has covered the different kinds of Mushroom Cultivation and practical demonstration class.

35

28

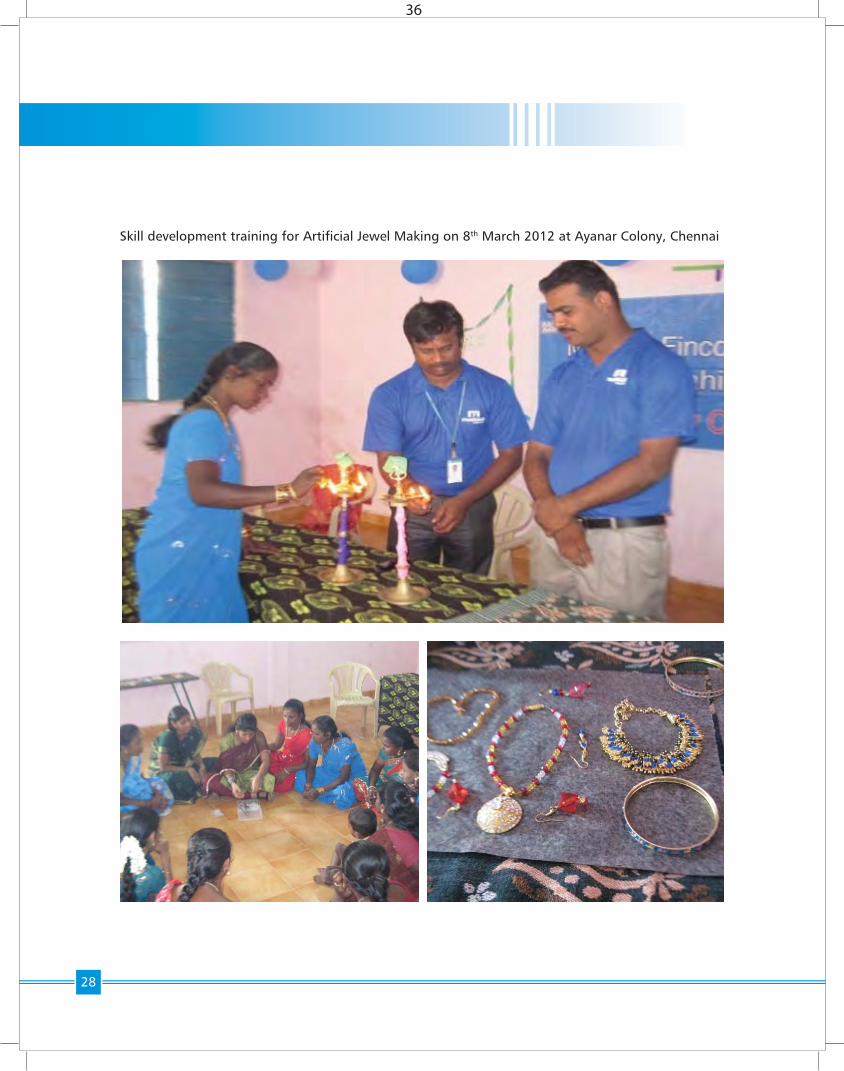

Skill development training for Artificial Jewel Making on 8th March 2012 at Ayanar Colony, Chennai

36

“Now we are also company owners”Ms. Merlin, Member, Producer Group

Initiatives for a Producer Group/Company for Women clients:

Muthoot Pappachan Foundation in Association with Accion India, NABARD and ROPE international has started a series of skill development initiatives training to the women customers. Muthoot Mahila Mitra believes in empowerment of woman through financial autonomy. Thus, evolved the concept of producer group later which will develop into producer company in due course, for which Muthoot Pappachan Group will provide conceptual guidance. The first of such group was formed at Trivandrum on 23.02.2012.

29

37

OUTREACH:

30

State Name Tamilnadu

Branches 22

Clients 61,228

IGL O/s Rs. 43,98,04,752

SW O/s Rs. 9,99,34,979

Total O/s Rs. 53,97,39,731

State Name Kerala

Branches 46

Clients 1,23,005

IGL O/s Rs. 88,46,66,538

SW O/s Rs. 19,00,47,793

Total O/s Rs. 107,47,14,331

State Name Karnataka

Branches 12

Clients 18,464

IGL O/s Rs. 14,30,39,106

SW O/s Rs. 3,15,63,385

Total O/s Rs. 17,46,02,491

38

31

Mar ‘2012Feb ‘2012Jan ‘2012Dec ‘2011Nov ‘2012Oct ‘2012

One of the lowest Delinquency rate in the industry

30 + %Total %Month

Oct ‘2012 0.92% 0.61%

Nov ‘2012 0.79% 0.63%

Dec ‘2011 0.65% 0.50%

Jan ‘2012 0.72% 0.62%

Feb ‘2012 0.74% 0.58%

Mar ‘2012 0.46% 0.45%

Delinqency

Delinquency Trend

0.61%

0.92%0.79%

0.65% 0.72% 0.74%

0.46%TOTAL DPD

0.63%

0.50%0.62% 0.58%

0.45%

30 + DPD

39

PHOTO GALLERY:

32

PandiammalLoan ID - PLHV#1007,

Kuzhalmandam

Soubhagyavathi And Vasantha

Loan ID - KLZM #756/757, Palakkad

Kanchana MohananLoan ID - KHRI # 251,

Kunnamkulam

VijayammaLoan ID - KNNM#166,

Karakkonam

Vijayalakshmai.RLoan ID - UPTT#947, Ansari street, Udumalpettu

AngammalLoan ID - UPTT#3145, Jallipatti, near Udumalpettu

40

CLIENTS AT WORK:

33

41

34

42

35

43

36

MUTHOOT MAHILA MITRA IN THE NEWS:

The Hindu

44

“The skill training for Embroidery and Stitching conducted by

Muthoot at Uruliyan Pettai for ladies were very useful” - DINAKARAN

"Skill training for ladies for stitching /embroidery at Pondicherry on Dec 11, 2011attended by more than 100 ladies” - DINAKARAN

37

45

An article in Outlook Magazine

regarding the unique Swarnavarsham

gold savings product.

“Free medical camp conducted by Muthoot

Micro Finance Division in association with

Lakshmi Narayana Hospital, Pondicherry was

very useful” - DINA MALAR

Picture from free medical camp conducted by Muthoot Micro Finance Division in association with Lakshmi Narayana Hospital, Pondicherry published in TAMIL MURA.

38

46

TESTIMONIALS:

“We were able to double the income using the loan from Mahila Mitra by purchasing new grinding machines”

Vidya from Palakkadu, Kerala (LAN: KHRI # 14)

“This letter is written to say thanks to Muthoot. We got prosperous by taking a loan from Muthoot and utilising the same for purchasing Duck and Goat/Cow. We express our sincere thanks”

Ms. Foumya from Kunnamkulam, Kerala (LAN: KKLM # 77)

39

47

"Due to this loan from Muthoot Mahila Mitra , Murukku business is going well and the unique Swarna-varsham scheme helped us to fulfill the long dream of owning a piece of gold"

Ms. Poonkodi from Mettupalayam (LAN: KMAD #8)

"This all happened only because of the Loan from Muthoot Mahila Mitra and we thank for the timely help”

Ms.Radha from Mettupalayam (LAN: KMAD #10)

40

48

FINANCIALS

41

49

42

50

RATIO ANALYSIS

KARNATAKA BASED MFI

18.04

27.81%

Rs.9392/-

Rs.24.93 Lacs

210

0.58%

21.24 Cr.

31.89%

22.01%

31.57%

7.22%

96.59%

MMM - A COMPARATIVE STUDY WITH OTHER MFIs

TN BASED MFI

10.43

53.30%

Rs.6371/-

Rs.36.90 Lacs

579

1%

18.10 Cr.

63.60%

15.18%

35.05%

22.40%

118.63%

MMM 2012

58.78

52.97%

15.10%

Rs.9800/-

Rs.38.96 Lacs

287

1%

23.04 Cr.

69.15%

7.46%

17.28%

18.06%

152.40%

MMM 2011

86.9

40.30%

17%

Rs. 9120/-

Rs. 25.21 Lacs

276

1%

5.08 Cr.

61.69%

6.88%

14.30%

13%

155%

PARAMETERS

CURRENT RATIO (CA/CL)

FINANCIAL COST /TOTAL COST

SPREAD ( IRR -COF )

LOAN PER BORROWER

LOAN PER EMPLOYEE

BORROWER PER EMPLOYEE

PROVISION FOR DOUBTFUL DEBTS

PBIT

PBIT TO OPERATING INCOME

OPERATING COST RATIO(OP COST EXCLUDINFINANCIAL COST & LOSS PROVISION /AV.OSPORTFOLIO )

TOTAL COST RATIO (TOTAL COST /AV.OSPORTFOLIO )

ROA (PBIT /AVERAGE ASSETS)

OPERATIONAL SELFSUFFICIENCY(OPERATING INCOME/TOTAL COST )

SLNO

1

2

3

4

5

6

7

8

9

10

11

12

13

43

51

CREDIT SHIELD & DEATH CLAIMS SETTLEMENT 2011-2012:

DEATH CASES SETTLED

41

65

3

109

0.07%

SUM ASSURED

4,18,000

6,48,000

29,000

10,95,000

(Reported claims 150 / Total clients 2,13,779)

STATE

KERALA

TAMIL NADU

KARNATAKA

TOTAL

Percentage of claims on active loans

Branch manager handing over the insurance cheque to the nominee of the deceased customer Mugajira Banu (LAN: PNDY # 1136) at Pondicherry.

44

52

2 YEARS AT A GLANCE:

2012

80

295810

202695

22

744

236,39,75,00053,51,13,937TOTAL - 289,90,88,937

178.90 Cr.

99.55 %

295 KG

1768.31

33.32 Cr.

23.04 Cr.

397

13809

2011

40

82032

80991

378

IGL - 810696000SW - 163142110TOTAL - 973838110

74 Cr.

99.82 %

82 KG

782.30

8.24 Cr.

5.08 Cr.

193

4429

NO. OF MMM BRANCHES

NO. OF MMM MEMBERS

ACTIVE MMM CLIENTS

DISTRICTS COVERED

TOTAL STAFF

LOAN DISBURSED (Rs.)

OUTSTANDING (Cr.)

REPAYMENT RATE (%)

GOLD COINS SOLD

BOOK SIZE (Rs. in Millions)

INCOME FROM OPERATIONS (Rs.)

EBIT (Rs.)

PRESENCE IN MFL BRANCHES (Nos)

NO OF CENTERS FORMED

45

53

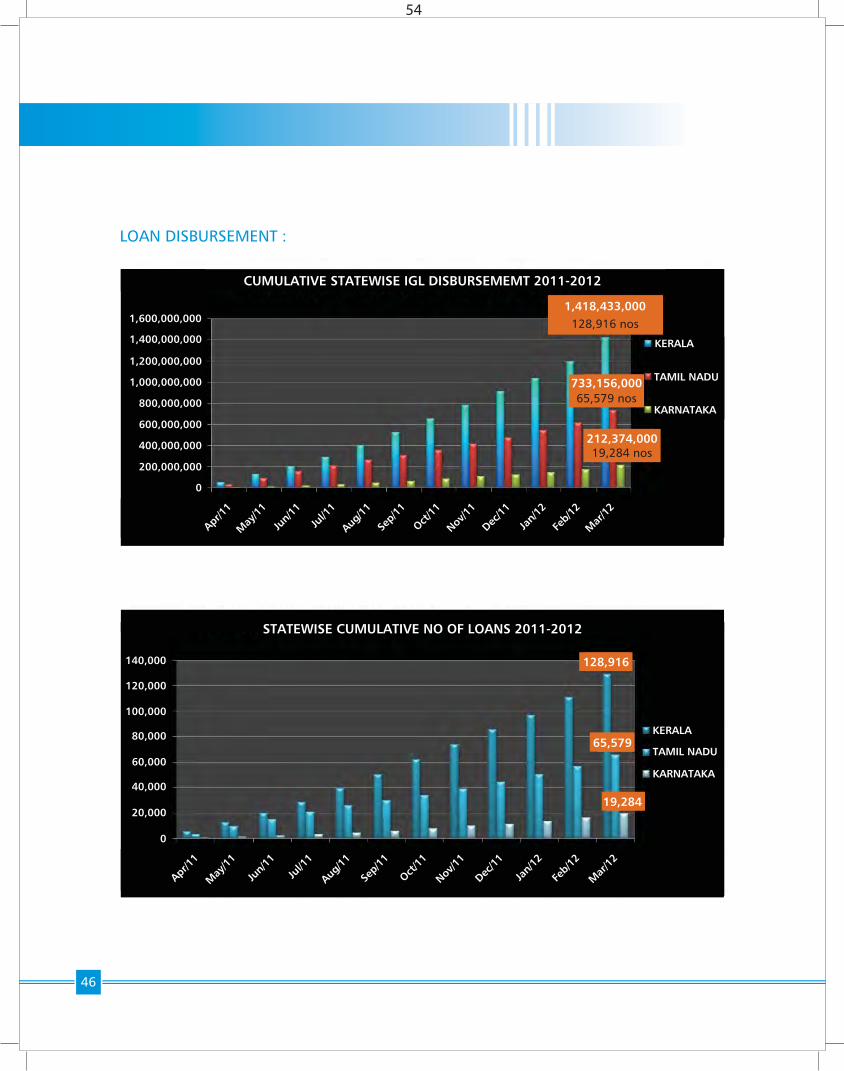

LOAN DISBURSEMENT :

CUMULATIVE STATEWISE IGL DISBURSEMEMT 2011-2012

140,000

0

20,000

40,000

60,000

80,000

100,000

120,000

1,600,000,000

KERALA

KARNATAKA

TAMIL NADU

KERALA

128,916 nos1,418,433,000

KARNATAKA

TAMIL NADU

0

200,000,000

Mar

/12

Feb/1

2

Jan/

12

Dec/1

1

Nov/1

1

Oct/1

1

Sep/1

1

Aug/1

1

Jul/1

1

Jun/

11

May

/11

Apr/11

Mar

/12

Feb/1

2

Jan/

12

Dec/1

1

Nov/1

1

Oct/1

1

Sep/1

1

Aug/1

1

Jul/1

1

Jun/

11

May

/11

Apr/11

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

STATEWISE CUMULATIVE NO OF LOANS 2011-2012

46

65,579 nos733,156,000

19,284 nos212,374,000

128,916

65,579

19,284

54

47

0

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

0

50,000

100,000

150,000

200,000

250,000

Mar/12Feb/12Jan/12Dec/11Nov/11Oct/11Sep/11Aug/11Jul/11Jun/11May/11Apr/11

2,363,975,000213,779 nosCUMULATIVE IGL DISBURSEMEMT 2011-2012

CUMULATIVE LOAN NUMBERS 2011-2012

231,677,000

374,948,000536,774,000

36,498

85,390

140,897

213,779

716,851,000895,068,000

1,299,681,000

1,508,346,000

1,723,150,000

1,978,291,000

89,535,000

1,090,222,000

Mar

/12

Feb/1

2

Jan/

12

Dec/1

1

Nov/1

1

Oct/1

1

Sep/1

1

Aug/1

1

Jul/1

1

Jun/

11

May

/11

Apr/11

55

CUSTOMER ANALYSIS:

48

30%

8%

36%

26%Tiled

Tatched

Sheet

RCC

51 Yrs AND ABOVE

36-50

26-35

18-25

ROOF TYPE

57

34

4 5

AGE WISE SPLIT UP

56

49

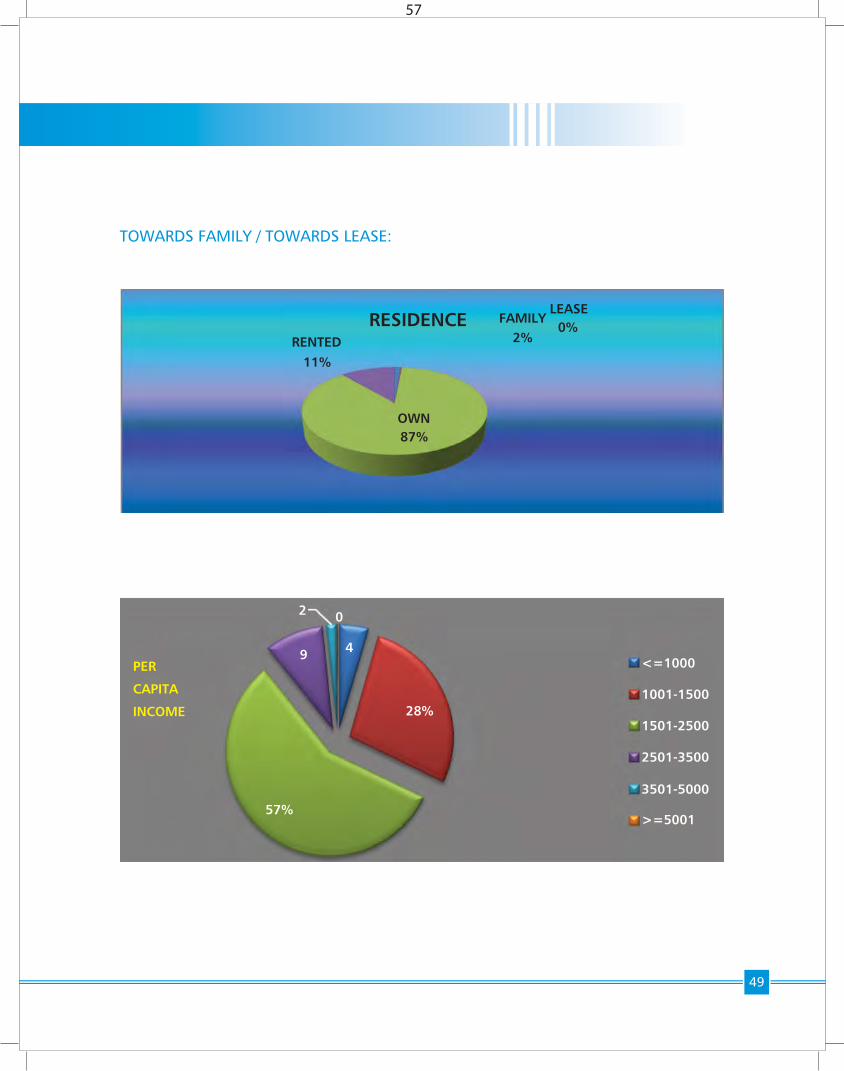

TOWARDS FAMILY / TOWARDS LEASE:

11%

2%0%

87%

9

2 0

4

28%

57%

OWN

RENTED

PER

CAPITA

INCOME

3501-5000

2501-3500

1501-2500

1001-1500

>=5001

<=1000

FAMILYLEASE

RESIDENCE

57

50

YES57%

NO43%

EXPENSES HABITS AS A % OF TOTAL SPENDING

MOBILE PENETRATION

06

13

48

6555444

10

20

30

40

50

60

FOOD

OTHER

CLOTH

TRANSS

PORT

EDUCATIO

N

MED

ICAL

ELEC

TRIC

ITY

ENTT

ERTA

INM

E...

PHONE

RENT

58

51

CLIENT ACTIVITY

NO. OF CENTERS

Trading13%

Agriculture34%

Debt Repayment0%

Consumption0%

FY 2010-2011

14000120001000080006000400020000

FY 2011-2012 13809

4429

Manufacturing2%

Animal Husbandry5%

Trading

Services

Others

Manufacturing

Housing

Debt Repayment

Consumption

Animal Husbandry

Agriculture

Housing0% Others

10%

Services36%

59

Tailor/ Embroidery

Bricks

Beauty Parlor

Building Hardware shop

Cane Works

Handicrafts

Flour Mill

Bakery

Bakery Items

Scrap Business

Fancy Ornaments Prod.

Tea shop and Coolbar

Cloth Carry bag

Stationary Shop

Jewellery

Textile Distributor

Plastic Net & Rope

Textiles

Grocery Shop

Catering

Convenience

Stationary

Vegetable Shop

Flowers & Plants

Purchase-Cow

Cattle Farm

Purchase-Goat

Clothes

Food Items

Farm:Poultry,Eggs,Milk

Stitching

All Rental Services

MAIN CLIENT ACTIVITIES

52

LOAN AMOUNT WISE

<=8000

8001-10000

Loan 10001-1500067584

16

146179

160000140000120000100000800006000040000200000

60

53

Statewise IGL Gross Loan Portfolio

STATEWISE SWARNAVARSHAM GROSS PORTFOLIO

Karnataka142949672

10%

Karnataka31474773

10%

Andhra89434

0%

Andhra88612

0%

T-Nadu439804752

30%

T-Nadu99934979

31%

Kerala884666538

60%

Kerala190047793

59%

Andhra Karnataka T-NaduKerala

Andhra

Karnataka

T-Nadu

Kerala

61

COMPLIANCE WITH RBI GUIDELINES:

ACTIVE PARTICIPATION IN:

1. Micro Finance Institutions network (MFIN)

2. Kerala Association of Microfinance Institutions (KAMFI)

CUSTOMER SERVICE:

1. Grievance redressal mechanism

Muthoot Mahila Mitra is one among the few, who has set up an effective grievances redressal mechanism. Customers can directly call the call center at HO for any assistances or complaints which the number is printed on every Loan card. The concerned officer will be intimated and a follow up call from HO will be followed to get the feedback for the progress for call made by client.

2. MFIN code of conduct

It is strictly directed to comply with the MFIN code of conduct which is displayed in all the branches.The respective officer will monitor the activities for any breach of fair practice and will forward therecommendation to HO for actions.

MUTHOOT MAHILA MITRA COMPLIANCE

100%

100%

100%

100%

100%

100%

100%

100%

RBI GUIDELINES

1. TOTAL INDEBTNESS OF FAMILY = < 50K

2. LOAN PURPOSE - INCOME GENERATING

3. INTEREST CAP 26%

5. COLLATERAL FREE LOAN

7. PROCESSING FEE CAP 1%

8. PROVISIONING NORMS AS PER RBI

9. CODE OF CONDUCT

10. VERNACULAR PRINTED LOAN CARD &LOAN AGREEMENT

54

62

BEST PRACTICES:

55

CUSTOMER CARE NO0484 - 4161678

FINANCIAL LITERACYPROGRAMMES

CENTRALISED TELECALLING WING

LOAN CARDS

TRANSPARENCY - (3 DAYSComprehensive Group Training Before Disbursement)

63

Organisational Structure

ORGANISATIONAL STRUCTURE

The Company’s hierarchy level is defined as follows -

56

IT/MIS HR & Training

Accounts Operations Audit & Risk BD Finance

MD/Directors

COO

ZM

RM

AM

BM

RO Credit Officer

Internal Audit

Policy Risk & Credit Analysis

64

57

STRENGTHS:

1. WIDE BRANCH NETWORK OF MUTHOOT FINCORP LIMITED ACROSS INDIA - MORE THAN 2300 BRANCHES

2. STRONG MANAGEMENT TEAM

3. EFFICIENT WORK FORCE

4. TAILOR MADE PRODUCTS

5. BEST PRACTICES

6. UPDATED USE OF TECHNOLOGY

7. LOWEST OPERATIONAL COST

Employee Speaks:

Ms. Suja (Employee ID: MP 10012611) is working as a Relationship officer in Alapuzha micro finance branch at Central Kerala, which is popularly known as the Venice of East. She joined on 8.12.2010 and since then she is one of the top performer in the branch without compromising on the quality. The discipline,attendance, 100% repayment and the good relationship with the clients are the key factors ensuring the quality of her portfolio. While speaking to her, she said “the service that Muthoot Mahila Mitra is delivering to the needy and unserved of the society that attracted me to join in the company“.

She is leading a happy life with her husbandMr. Abhilash and two children.

65

58

Submitted by:

Submitted to:

Muthoot Fincorp, Kochi, Muthoot Chambers, City BranchOpp: Saritha Theatre, Banerji Road, Kochi

Mumbai ∙ New Delhi ∙ Hyderabad∙ Patna

INTELLECASH Microfinance Network Company Pvt. Ltd. #11 F, Gopala Tower, Rajendra Place, New Delhi – 110008, INDIATel: +91-11-47093361, 45558027, 28, 29 Fax: +91-11-45558026

Website: www.intellecash.com

66

59

The Social Impact Assessment study was conducted by INTELLECASH Microfinance Network Company Pvt. Ltd, Delhi. IntelleCash is a subsidiary of the leading global advisory firm INTELLECAP that works at the intersection of the private sector and development. It provides consulting and investment banking services driven by innovative thought processes, to Business and Development communities globally, helping them bring entrepreneurship solutions to development challenges at the Base of the Pyramid and beyond.

Objectives of the Impact Assessment study:1. To understand the various activities carried out for Muthoot Mahila Mitra members.

2. To measure the knowledge and skills of women group members before and after the intervention.

3. To measure the impact of the interventions on the target client’s managerial abilities, and if it has contributed to an improved quality of life.

4. To understand other stakeholders’ view and perspective on the intervention.

Main findings: Muthoot Mahila Mitra appears to have achieved most of its microfinance programme objectives.

Evidence of the achievements can be seen under income increase and improved quality of life namely health, education and children’s vaccination.

Muthoot’s approach of using CSR activities to complement its Microfinance programme is yielding good results. Its flagship programme “Sthreejyothi” is showing positive results and members perceive the programme as positive. One of the key achievements of the MMM programme is the impact on Decision Making ability of its members. The findings confirm that members have started taking equal position in the family in all major decisions. The results are more pronounced among the trained clients.

Impact of IGL product on the Business is quite good; nearly 50% of the clients confirm that their profit and sales have increased. While 30% felt it has helped them to expand and grow their business.

Though the employment/jobs created by members' enterprises is around 3%, it is considered as very important indicator in social performance management arena.

To view the full report visit our website:www.muthoot.com/mmm

67

OUR BANKS:-

UNION BANK OF INDIA

HDFC BANK

OUR AUDITORS

JVR & ASSOCIATES, ERNAKULAM

ADDRESS:

MUTHOOT MAHILA MITRA

5TH FLOOR

MUTHOOT TOWERS

ERNAKULAM - 682035

PHONE: 0484 4161678

Web site: www.muthoot.com/mmm

60

68

“Money entering a household through a woman brings more bene f i t s to t he f am i l y a s a who le . ” - Muhammad Yunus

ANNUAL REVIEW 2011-12

Building deep-rooted empowerment.

MUHOOT MAHILA MITRA5TH FLOOR, MUTHOOT TOWERS, ERNAKULAM - 682035. PH: 0484 4161678

www.muthoot.com www.muthoot.com/mmm