budget preparation module -...

TRANSCRIPT

BUDGET PREPARATIONMODULE

October 2014

P A R T I C I P A N T B O O K

Public Financial Management

KENYA SCHOOL OF GOVERNMENTNATIONAL TREASURY MINISTRY OF DEVOLUTION AND PLANNINGREPUBLIC OF KENYA REPUBLIC OF KENYA

Public Financial Management

BUDGET PREPARATIONMODUlE

P A R T I C I P A N T B O O K

October 2014

Table of Contents

Foreword .................................................................................................................................... i

Acknowledgements .................................................................................................................... ii

Abbreviations .............................................................................................................................. iii

Introduction ................................................................................................................................... 1

Aims and Objectives of the training ........................................................................................... 1

Public Finance Management Curriculum—Summary ................................................................. 2

Target Participant Group ............................................................................................................ 4

Glossary and Resources ................................................................................................... 4

Timings and Methodology .......................................................................................................... 4

Training Overview—Budget Preparation .................................................................................... 5

Getting Started ............................................................................................................................. 6

History of Budgeting in Kenya ........................................................................................................ 7

County Budget Cycle, Calendar and Conceptual Overview of Budgeting ...................................... 10

1. Key legislation, documents, roles and responsibilities in county budgeting ........................... 11

2. County Budget Cycle and Calendar ......................................................................................... 22

3. Legislative Approval Process ................................................................................................... 28

4. Strategic vs. Operational Phases of budget preparation ........................................................ 36

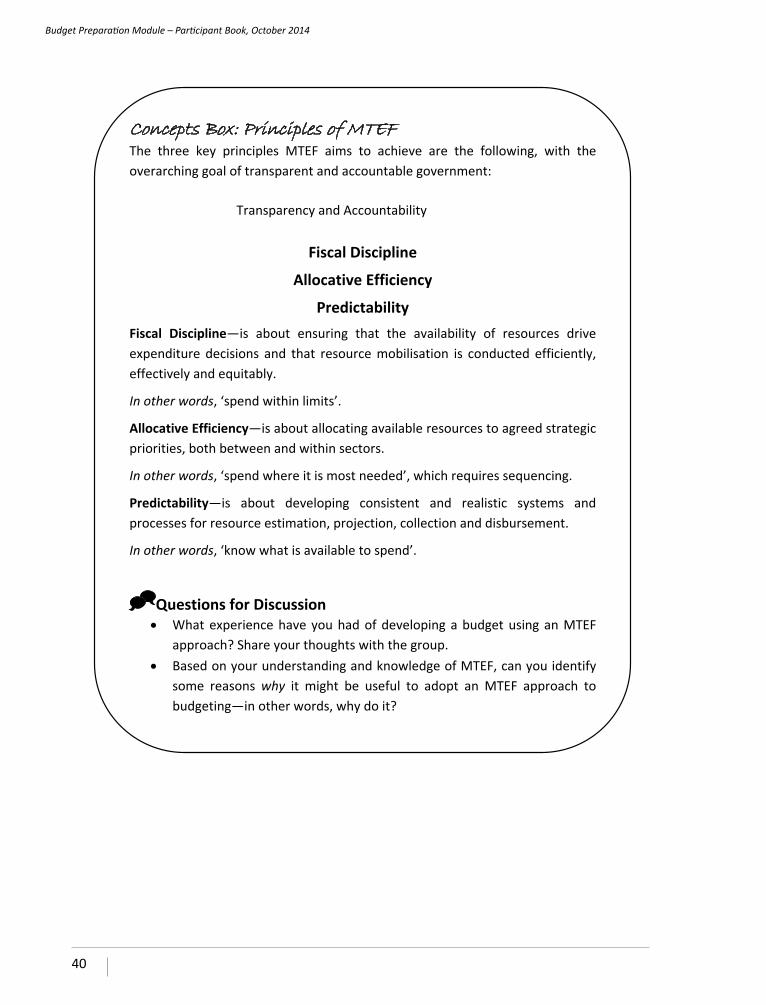

5. Introduction to Medium Term Expenditure Framework ......................................................... 39

6. Introduction to Programme Based Budgeting ........................................................................ 41

7. Introduction to the Chart of Accounts (CoA) .......................................................................... 44

8. Public Participation in Budget Preparation ............................................................................. 46

Strategic Phase of Budgeting ......................................................................................................... 48

1. County Budget Circular ........................................................................................................... 50

2. County Integrated Development Plan .................................................................................... 51

3. County Budget Review and Outlook Paper (C-BROP) ............................................................. 54

4. Sector Working Groups and Resource Allocation ................................................................... 64

5. County Fiscal Strategy Paper (C-FSP) ...................................................................................... 66

Operational Phase of Budgeting .................................................................................................... 68

1. County Budget Circular/Budget call circular (budget estimates) ............................................ 70

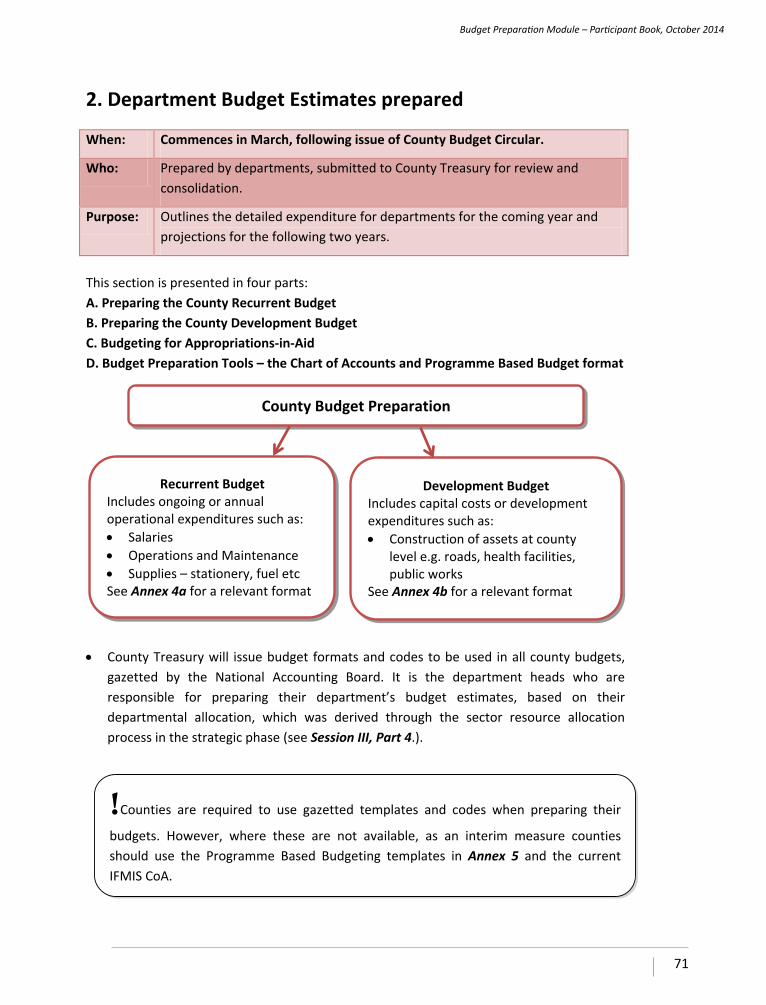

2. Department Budget Estimates prepared ................................................................................ 71

A. Preparing the County Recurrent Budget ............................................................................ 72

B. Preparing the County Development Budget ...................................................................... 73

C. Budgeting for Appropriations-in-Aid (A-in-A) ..................................................................... 74

D. Budget Preparation Tools – The Chart of Accounts and Programme Based Budgeting format .... 75

3. Review, consolidate and submit Budget Estimates .................................................................... 83

Conclusion ..................................................................................................................................... 86

Summary .................................................................................................................................... 86

Assessment & Evaluation ............................................................................................................ 86

Glossary ......................................................................................................................................... 87

Resources ...................................................................................................................................... 89

Assessment .................................................................................................................................... 90

Annexes ......................................................................................................................................... 91

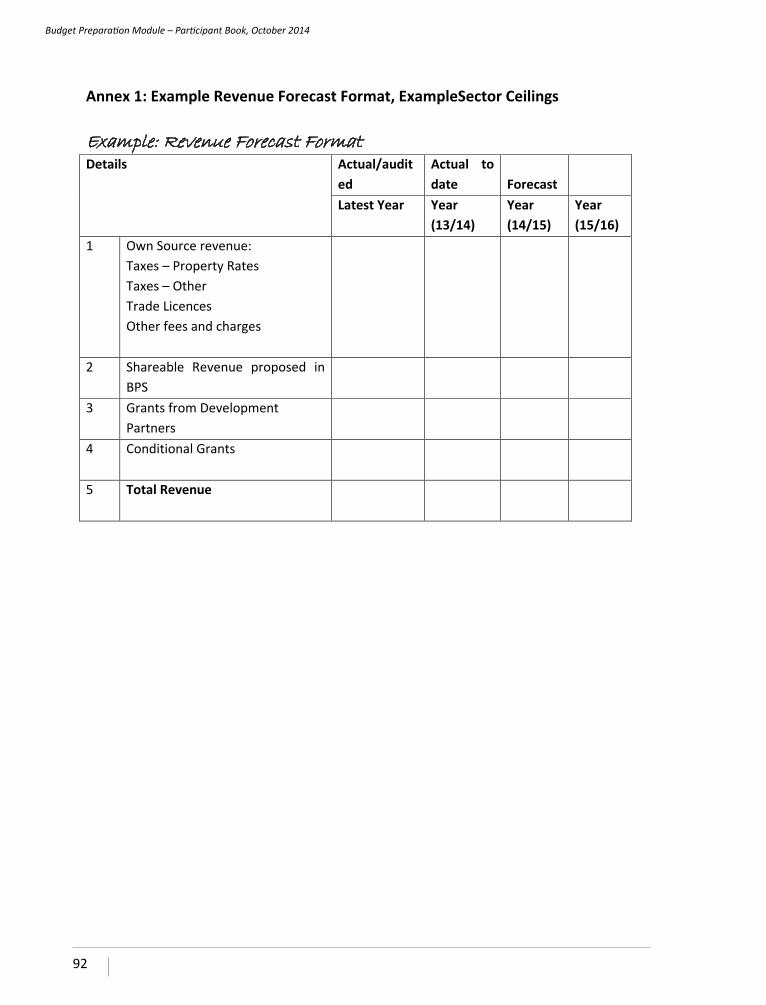

Annex 1: Example Revenue Forecast Format, Example Sector Ceilings ...................................... 92

Annex 2: C-FSP Format ............................................................................................................... 95

Annex 3: Sector Working Group Report Format ......................................................................... 96

Annex 4a: Estimates of Recurrent Expenditure .......................................................................... 99

Annex 4b: Estimates of Development Expenditure .................................................................... 100

Annex 5: FORMAT FOR PRESENTATION OF PROGRAMME BASED BUDGETS (PBB) .................... 101

Annex 6: Departmental/Sectoral Committees ........................................................................... 104

Annex 7: County Integrated Development Plan Chapter Outlines ............................................. 106

Annex 8: Template for costing of programs and activities ......................................................... 110

Foreword

The Fourth Schedule of the Constitution of Kenya assigns the National Government the function of capacity building of counties. This mandate of the National Government

has also been recognised and elaborated in the National Government Capacity Building Framework for County Governments. With regard to county public finance management (PFM) capacity building, this responsibility has been placed on the National Treasury.

In order to effectively deliver on its mandate of building the capacity of county governments in PFM, the National Treasury developed a County PFM Training Curriculum and has in partnership with development partners embarked on the development of a number of County PFM Training Modules. The National Treasury intends to roll out training on PFM and make these modules accessible to all county governments.

In this respect, the National Treasury will partner with the Kenya School of Government (KSG) to roll out the training of county State and public officers using the County PFM Modules as the primary training toolkit. These modules, besides standardizing the County PFM Training, will also ensure that those trained will also have reference material for use in their day-to-day operations.

At the outset, training will be delivered by a pool of staff drawn from the National Treasury. In the medium and long-term, the National Treasury, in partnership with the Kenya School of Government will identify and train a pool of professionals, through scheduled training of trainers. This pool of professionals will then conduct future training of county PFM staff. For this purpose, each module includes a ‘Training of Trainers’ guide in addition, to the participants guide.

This Budget Preparation module, is among the first to be developed and is specifically designed to equip the county officials with the necessary skills and information, to help improve and strengthen their capacity in the preparation of county budgets. The module will be used to train officials drawn from the county executives as well as county legislatures and emphasizes the use of participatory and practical approaches to learning.

I have no doubt that this county PFM Training modules will help to strengthen the capacity of county governments in public finance management and contribute towards enhancing prudent, accountable and transparent management of public resources.

Henry K. Rotich,Cabinet SecretaryNational Treasury

i

Budget Preparation Module – Participant Book, October 2014

Acknowledgements

This Budget Preparation module has been developed through the concerted effort of various institutions and professionals. We wish to express our gratitude to all those

persons and institutions that contributed towards the development of this manual.

In particular, I wish to acknowledge the role of the Budgetary Supply Department and the newly created Intergovernmental Fiscal Relations Department of the National Treasury in coordinating and providing technical guidance in the development of this Module.

Much thanks to the Kenya School of Government (KSG) who provided quality control during the development of the module and for their commitment to include the Budget Preparation module as the main toolkit for county PFM training at the Kenya School of Government.

We are equally grateful to World Bank through its Kenya Accountable Devolution Programme, for its support towards the development of this module. Special thanks to the pool of experts from the World Bank who worked tireless to ensure successful delivery of this module.

Dr. Kamau Thugge, EBSPrincipal SecretaryNational Treasury

ii

Budget Preparation Module – Participant Book, October 2014

Abbreviations

AOs Accounting Officers

BROP Budget Review and Outlook Paper

CA County Assembly

C-BEF County Budget and Economic Forum

CEC County Executive Committee

CEC-MF County Executive Committee Member for Finance

CEC-MP County Executive Committee Member for Planning

CoB Controller of Budget

CoK Constitution of Kenya (2010)

CFPG County Fiscal Planning Group

CRA Commission for Revenue Allocation

CT County Treasury

GDP Gross Domestic Product

IBEC Inter-governmental Budget and Economic Council

MTEF Medium Term Expenditure Framework

NT National Treasury

PBB Programme Based Budgeting

PEM Public Expenditure Management

PFM Public Finance Management

PFMA Public Finance Management Act (2012)

SWGs Sector Working Groups

iii

Budget Preparation Module – Participant Book, October 2014

1

Introduction Aims and Objectives of the training This Budget Preparation training is one component of the Public Finance Management Module. It aims to enhance general understanding of public financial management, and for the technical county staff empower them, the participants, to prepare timely, accurate and effective county budgets which address some key weaknesses encountered through the 2014/15 budget preparation period. The training will achieve this by increasing participants’ understanding of the budget preparation process and its related concepts, as well as the specific ‘how to’ elements of budget preparation. Specific Objectives

By the end of this training, participants should be able to better perform their roles and: • Identify the different elements of the budget cycle and calendar, and plan work

accordingly to ensure that they can comply with deadlines. • Identify areas of challenges and what improvements may be necessary in their own

county’s budget preparation process and explore ways to achieve this. • Clearly explain the different components of the budget preparation process,

including key legislation, players and documents. • Effectively manage the county budget preparation process for a smooth process of

legislative approval. • Identify specific places in budget preparation where public participation is

needed,and explore and incorporate different mechanisms for public participation. • Carry out the tasks associated with the ‘Strategic Phase’ of budgeting, including

revenue forecasting and ceiling setting, through the preparation of C-BROP and C-FSP documents and Sector Working Group Reports.

• Carry out the tasks associated with the ‘Operational Phase’ of budgeting, including the preparation of detailed department budget estimates.

• For the officers, use the Chart of Accounts to code expenditure as part of preparing budget estimates.

• Identify how thecounty budget will incorporate the programme based budget for 2014/15.

!It is important that each county/organization/entity using this manual ensures

modifications are made in the delivery of the training to take account of local dynamics, to meet specific needs in public financial operations and applications in the target unit.

Budget Preparation Module – Participant Book, October 2014

2

Budget Preparation Module – Participant Book, October 2014

Specific training outcomes

As an outcome, it is anticipated that participants will feel more confident in the budget preparation process, as a result of addressing weaknesses identified in the preparation of the 2014/15 budget, and will be motivated to implement what they have learned into their preparation of their county budget for 2014/15. Public Finance Management Curriculum—Summary Component What is covered?

i) Constitutional and Legal Framework for PFM

• Overview of the Constitutional and legal framework for PFM, including the Constitution of Kenya, 2010;PFM Act, 2012; CRA Act, 2011 among others

• Roles and responsibilities of national and county government PFM institutions

• Process/Role of County Assembly in approval and oversight of County Government’s (CG) budget

ii) Budget Preparation

• History of budgeting in Kenya • Budget Cycle, Calendar and Conceptual

Overview • Strategic Phase of budget preparation • Operational Phase of budget preparation

iii) Budget Execution • Cash and Treasury Management: • Revenue Management (Tax, non-tax): sources and modalities for

optimizing capacity for raising revenue • Grants and Donations Management • Expenditure Management, including losses and write-offs • Debt Management • Procurement • County Assets and Liabilities Management • Role of the Controller of Budget

iv) Financial Accounting, Recording and Reporting

• Role of Accounting Officers • Financial Reports: types, content and timelines • Standard Chart of Accounts and relationship with COFOG and GFS • Integrated Financial Management Information System (IFMIS)

!Budget Preparation is the focus of this Participant Book.

3

Budget Preparation Module – Participant Book, October 2014

v) PFM in AGAs and SAGAs / Audit and Risk Management (Autonomous and Semi-Autonomous Government Agencies)

• Internal Audit • External Audit

vi) Inter- and Intra-governmental Fiscal Relations

• Process of Revenue Sharing – Division of Revenue Bill and the County Allocation of Revenue Bill

• IGFR Institutions – IBEC and Joint Technical Committee • Stoppage of Funds • Inter-governmental Reporting • Budget Policy Statement

vii) Monitoring and Evaluation

• Public Expenditure Review (PER) • Public Expenditure Tracking Survey (PETS) • Parliamentary and County Assembly oversight • Performance measurement • PFM and performance contracting • Public participation • Tools for public participation

viii) Leadership and Integrity

• Chapter Six (Constitution of Kenya 2010) • Ethics and Anti-corruption Act provisions • Leadership and Integrity Act provisions • Public Officer and Ethics Act provisions

ix) Gender and Youth in Development

• Understanding gender, youth and persons with disabilities in development

• Government policies on gender, youth and persons with disabilities

• Preferences and Reservations for Women, Youth and Persons with Disabilities on public procurement

• Strategies for gender and youth mainstreaming

4

Budget Preparation Module – Participant Book, October 2014

Target Participant Group This Budget Preparation training is designed for the following target groups:

• County Executive Committee Members for Finance • Chief Officers/Accounting Officers of County Governments • Staff of the department or departments of the County Treasury • Clerks of the County Assemblies • Members of County Assemblies • Staff of city and municipal boards involved in public finance management • Audit committee members • Staff of County Departments and county government entities involved in public

finance

! Note that Sessions I and II of the trainingare targeted at all the above participants.

Session III is largely targeted at County Assembly, County Treasury, and County Executive Committee. Session IV is largely targeted at county departments in preparing their budgets. Glossary and Resources

• There is a Glossary of relevant terms and their meanings included at the end of this Participant Book.

• You will find a list of useful Resources for further information at the end of this Participant Book.

Timings and Methodology This Budget Preparation training has been designed as three (3) day training, but can be extended to four (4) days or more depending on the target audience (i.e. for different levels the time table can be adjusted). A timetable will be provided by your trainer. This training in Budget Preparation aims to be interactive and participatory. In addition to lecture/presentations, the following will be used: • Group and plenary discussions • Group exercises • Brainstorm questions • Example-based questions • Written exercises

5

Budget Preparation Module – Participant Book, October 2014

Training Overview—Budget Preparation Session What is covered?

Getting Started • Welcomes, Introductions • Aims, Objectives • Expectations, Ground Rules • Understanding the emerging challenges in the budget

process

Session I: History of Budgeting in Kenya

• Overview of Key Budgeting Reforms in Kenya • Key legislation in budgeting • Exercise: Impact of Budget Reforms • Questions for Discussion

Session II: Budget Cycle, Calendar and Conceptual Overview

• Overview of key players, documents, responsibilities • Outline of budget cycle, budget calendar, legislative

approval process • Introducing MTEF and Programme Based Budgeting • Introduction to Chart of Accounts • Role of Public Participation in budgeting

Session III: Strategic Phase of Budgeting

• The County Integrated Development Plan • Preparing the C-BROP • Resource Envelope, Ceilings, Medium Term Budget

Strategy • Sector Working Groups and Sectoral Resource Allocation • Preparing the C-FSP

Session IV: Operational Phase of Budgeting

• Preparing Detailed Budget Estimates—recurrent and development budgets

• Preparing budget estimates according to Programme Based Budgeting formats

• Using the CoA to code expenditure.

Module Conclusion • Module Summary • Assessment Exercise • Evaluation

6

Budget Preparation Module – Participant Book, October 2014

Introductory Session

Getting Started Here are some topics your trainer is likely to cover in this session:

• Welcome, Introductionsand ‘Housekeeping’

• Aims and Objectives of the training

• Training Overview and Timetable

• Relevant Documents

• Expectations and Ground Rules

• Understanding the challenges in the budget process

‘Icebreaker’Questions:

Session Objectives: • To create a comfortable and encouraging learning environment. • To provide an overview of the training, including aims and objectives. • To understand participants’ expectations of the training. • To set some agreed ground rules for the training.

Briefly discuss the following with your neighbour: • What are your expectations of this training? • What do you think you can contribute to this training?

Discuss the following quote:

If we all did the things we are capable of, we would astound ourselves.

Thomas Edison,American inventor What do you think this quote is saying? How might it apply to this training?

!In this session you will get to know your trainer/s and the other participants. You will

find out what the training involves and what you are expected to do.

7

Budget Preparation Module – Participant Book, October 2014

Session I History of Budgeting in Kenya

Session Objectives: By the end of this session participants will be able to: • Identify how key budget reforms in Kenya since independence have influenced the

current budgeting process at a national and local level. • Discuss areas for improvement from their own county’s budget for 2013/14 and

identify possible ways ahead for 2014/15 and beyond.

Concepts Box 1: Budgeting in Kenya • Executive Branch, through the Minister for Finance, had total authority over

budget and overall PFM for many years.

• Parliament debated budget proposals each year, but constitutionally could not increase any fiscal measures. Also, the budget could not be rejected, as this would lead to a ‘vote of no confidence’ and hence require new elections.

• Such restrictions led to ineffective legislative budget oversight, and over time the need for a robust PFM system was recognized by government.

• For example, prior to the budget reforms, two separate budgets were prepared for each fiscal year; a recurrent and a development (or capital) budget. As the economy grew and became more complex, the need arose to change how resources were mobilized and allocated.

• Since independence, the budget process has gone through many reforms in an effort to improve PEM for better delivery of services to the citizens (see Table 1).

• In some cases, the need for reform was not locally driven, but came from external sources such as development partners, who had been providing Kenya with financial support.

• In addition, on the revenue side, since 1990 Kenya has carried out a wide-ranging tax modernisation program which has enabled Kenya to sustain a ‘revenue to GDP’ ratio well above the sub-Saharan average. This has been important for reducing dependency on aid to a manageable level.

Source: PFM training curriculum document

8

Budget Preparation Module – Participant Book, October 2014

Table 1: Key Budget Reforms since Independence Budget Reform Period Objective of Reform Success of reform and

impact on today’s budget process?

Programme Review and Forward Budgeting (PRFB)

1970s Achieving a linkage between the development agenda and the budget through a medium-term oriented budget process.

Budget Rationalization Programme(BRP)

1986 Introducing a mechanism of prioritization consistent with available recourses to priority programmes (address resource constraints).

Public Investment Programme (PIP)

1990s Linking the capital budget to future recurrent budgets through a mechanism of prioritizing project implementation.

Kenya Tax Modernization Programme

Since 1990

• Modernize tax policy and administration.

• Shift emphasized on revenue mobilization to consumption.

• Simplify tax administration to lower cost of compliance and enforcement.

• Reduce excessive protection of local producers that was based on import substitution to encourage efficiency, innovation and competitiveness of local goods and services.

• Introduce computer-based enforcement and compliance.

The Medium Term Expenditure Framework Process (MTEF)

2000 Provide a link between policy, planning and budgeting through a coherent multi-year budgeting process.

Programme Based Budgeting

2013 Aims to deepen the MTEF approach by moving decision-making on resource allocation from line item to expected outputs. From line item to program and sub-program and outputs and performance targets.

9

Budget Preparation Module – Participant Book, October 2014

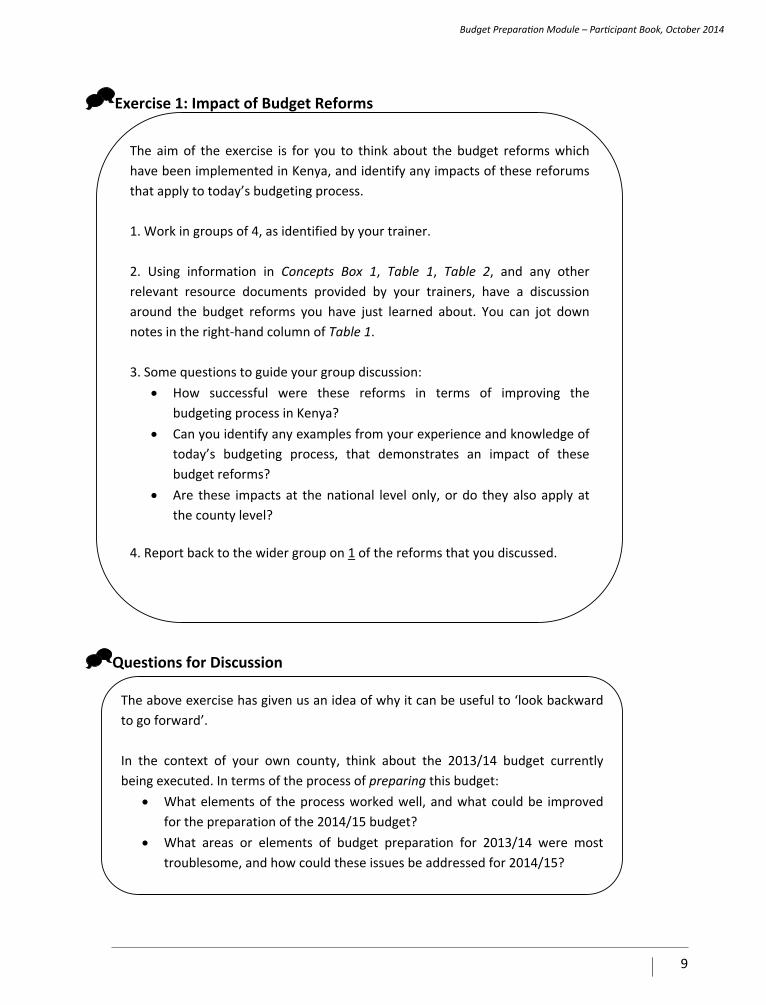

Exercise 1: Impact of Budget Reforms

Questions for Discussion

The above exercise has given us an idea of why it can be useful to ‘look backward to go forward’. In the context of your own county, think about the 2013/14 budget currently being executed. In terms of the process of preparing this budget:

• What elements of the process worked well, and what could be improved for the preparation of the 2014/15 budget?

• What areas or elements of budget preparation for 2013/14 were most troublesome, and how could these issues be addressed for 2014/15?

The aim of the exercise is for you to think about the budget reforms which have been implemented in Kenya, and identify any impacts of these reforums that apply to today’s budgeting process. 1. Work in groups of 4, as identified by your trainer. 2. Using information in Concepts Box 1, Table 1, Table 2, and any other relevant resource documents provided by your trainers, have a discussion around the budget reforms you have just learned about. You can jot down notes in the right-hand column of Table 1. 3. Some questions to guide your group discussion:

• How successful were these reforms in terms of improving the budgeting process in Kenya?

• Can you identify any examples from your experience and knowledge of today’s budgeting process, that demonstrates an impact of these budget reforms?

• Are these impacts at the national level only, or do they also apply at the county level?

4. Report back to the wider group on 1 of the reforms that you discussed.

10

Budget Preparation Module – Participant Book, October 2014

Session II County Budget Cycle, Calendar and Conceptual Overview of Budgeting At the outset, it is important to understand that the county budgeting process fits within a wider Public Expenditure Management (PEM) cycle, as shown in Diagram 1 below: Diagram 1: The PEM Cycle and budget preparation

Source: Adopted from http://blog-pfm.imf.org/pfmblog/2008/08/public-expendit.html

Session Objectives: By the end of this session participants will be able to: • Identify the stages in the county budget cycle and calendar, including key

calendar targets and the legislative approval process. • Demonstrate an understanding of the concepts of MTEF, Programme Based

Budget and the Chart of Accounts. • Explain the importance of public participation in the budget preparation process

and identify key opportunities for public input in this process.

Formulate plans andbudgets

Execute budgets

Account and report

Audit and scrutinise budgets

and reports

• Prepare , present and review:• National development plan• Budget policy statement• Medium-term expenditure

framework• Annual budget

• Release funds • Procure goods, works and

services• Manage the wage bill • Manage debts

• Undertake internal audit• Conduct procurement reviews,

public expenditure reviews, service delivery surveys etc.

• Carry-out external audit• Parliament provides oversight

and scrutiny

• Account for expenditure • Reconcile of accounting records• Generate in-year and end of year

financial and other reports

In this training, we focus on this section of the PEM cycle.

11

Budget Preparation Module – Participant Book, October 2014

1. Key legislation, documents, roles and responsibilities in county budgeting Table 2: Quick Reference—Key legislation for budget preparation

Legislation

Relevant Sections

Constitution of Kenya (2010)

Articles 201, 202, 203 on revenue sharing Article 207 County Revenue Fund Article 209 and Article 210 on tax allocation and taxation Article 212 (County Borrowing) Articles 215–219 (Revenue Allocation) Articles 220,224, 227 (Budgets and Spending) Article 225 (Financial Control) Article 226 Accounts and audits Article 228, Controller Budget Article 229, Auditor-General

Public Finance Management Act (2012)

Sections 25–27 (Responsibilities of the National Treasury with respect to the budget process) Sections 35–45 (NationalGovernment BudgetProcess) Sections 102-116, 117–118 (Responsibilities of county governments with respect to the county budget process, principles of PFM) Sections 147–149 (Roles, responsibilities of Accounting Officers Sections 157–162 Receivers and collectors of revenue Sections 125–137 (The County Government Budget Process) Sections 189–191 (The Process of Sharing Revenue)

County Government Act (2012)

Part VIII – Citizen Participation Section 91 (c) Budget preparation and validation fora

!You will learn more about relevant legislation in the training module:

i) Constitutional and Legal Framework for PFM

12

Budget Preparation Module – Participant Book, October 2014

Tab

le 3

: Qu

ick

Ref

eren

ce—

Key

pla

yer

s in

the

cou

nty

bu

dg

etin

g p

roce

ss (

in a

lpha

beti

cal

ord

er)

Initi

als

Body

Wha

t is t

heir

role

?

Coun

ty L

evel

Inst

itutio

ns

AOs

Acco

untin

g O

ffice

rs

•Le

ad th

e va

rious

Cou

nty

Sect

or W

orki

ng G

roup

s.

•Ar

e de

signa

ted

by th

e CE

C-M

F an

d ar

e ac

coun

tabl

e to

theC

ount

y As

sem

bly

(CA)

for f

inan

cial

man

agem

ent.

•Ar

e re

spon

sible

for a

ccou

ntin

g fo

r mon

eyap

prop

riate

d by

Cou

nty

Asse

mbl

y.

•Ha

ve p

ower

s to

exec

ute

loan

doc

umen

ts, m

anag

e as

sets

and

liab

ilitie

s of C

G an

d re

allo

cate

fund

ssub

ject

to

cert

ain

cond

ition

s.

•En

sure

pub

lic re

sour

ces a

re u

sed

in a

way

that

is la

wfu

l and

aut

horis

ed a

nd in

an

effe

ctiv

e an

d ef

ficie

nt m

anne

r. •

Mus

t ens

ure

prop

er fi

nanc

ial m

anag

emen

tof t

he re

spec

tive

Coun

ty G

over

nmen

t ent

ity.

•Le

ad ro

le in

pre

parin

g an

d su

bmitt

ing

depa

rtm

enta

l bud

gets

and

in th

e bu

dget

pre

para

tion

proc

ess.

•

Appr

oval

of r

e-al

loca

tion

of fu

nds b

etw

een

prog

ram

s, su

bjec

t to

limits

set i

n th

e re

gula

tions

. •

CEC

Fina

nce

coor

dina

tes b

udge

ting

and

PFM

for c

ities

and

urb

an a

reas

.

CA

Coun

ty

Asse

mbl

y

•Ap

prov

es/a

dopt

s key

bud

get d

ocum

ents

, inc

ludi

ng In

tegr

ated

Dev

elop

men

t Pla

n, C

-FSP

, Deb

t Man

agem

ent

Stra

tegy

, and

Bud

get E

stim

ates

. •

Prov

ides

ove

rall

over

sight

ove

r pub

lic fi

nanc

es a

t the

Cou

nty

Gove

rnm

ent l

evel

. •

Ensu

re a

dher

ence

by

CEC

and

CG to

Prin

cipl

es o

f Pub

lic F

inan

ce a

nd th

e fis

cal r

espo

nsib

ility

prin

cipl

es.

•Ap

prov

es th

e es

tabl

ishm

ent o

f oth

er c

ount

y pu

blic

fund

s.

•Ap

prov

es b

udge

t and

reve

nue

allo

catio

n fo

r citi

es a

nd u

rban

are

as.

•O

vers

ight

of a

ccou

ntab

ility

and

com

plia

nce

with

lega

l req

uire

men

ts, e

.g. a

ccou

ntin

g st

anda

rds a

nd o

ther

. •

Appr

oves

and

ove

rsee

s Cou

nty

Asse

mbl

y Bu

dget

. •

Appr

oves

Cou

nty

Debt

Str

ateg

y Pa

per w

hich

sets

bor

row

ing

limits

, det

ails

borr

owin

g ne

eds.

13

Budget Preparation Module – Participant Book, October 2014

Co

unty

As

sem

bly

Cler

k

•Su

bmits

the

budg

et o

f the

Cou

nty

Asse

mbl

y, to

the

Coun

ty A

ssem

bly

for c

onsid

erat

ion

and

appr

oval

by

30Ap

ril

as p

er P

FM A

ct 2

012,

129

(3).

Also

resp

onsib

le fo

r Cou

nty

Asse

mbl

y Bu

dget

. •

May

real

loca

te re

sour

ces w

ithin

Vot

es su

bjec

t to

10%

lim

it.

C-BE

F Co

unty

Bu

dget

and

Ec

onom

ic

Foru

m

A ne

w st

ruct

ure

at c

ount

y le

vel t

o se

rve

asa

cons

ulta

tive

foru

m o

n co

unty

pla

ns a

nd b

udge

ts. I

t inc

lude

s:

•Co

unty

Gov

erno

r as C

hair

•M

embe

rs o

f the

CEC

•

Repr

esen

tativ

es o

f a w

ide

rang

e of

gro

ups a

t cou

nty

leve

l inc

ludi

ng p

rofe

ssio

nals,

bus

ines

s, la

bour

issu

es,

wom

en, p

erso

ns w

ith d

isabi

litie

s,th

e el

derly

and

faith

bas

ed g

roup

s.

•Sp

ecifi

c re

spon

sibili

ties i

nclu

de c

onsu

ltatio

ns fo

r the

pre

para

tion

of: C

ount

y De

velo

pmen

t Pla

ns, C

-BRO

P, C

-FSP

. Se

e PF

MA

(201

2) S

ectio

n 13

7, E

stab

lishm

ent o

f For

um fo

rcon

sulta

tion

by c

ount

ygov

ernm

ents

CEC

Coun

ty

Exec

utiv

e Co

mm

ittee

•Re

spon

sible

for t

he so

cial

-pol

itica

l, po

licie

s, fi

nanc

e an

d ex

ecut

ion

aspe

cts i

n a

coun

ty.

•Co

ordi

nate

s pre

para

tion

of C

IDPS

that

gui

de b

udge

ting,

on

appr

oval

impl

emen

ts b

oth

plan

and

bud

get.

•Ap

prov

es C

-BRO

P an

d C-

FSP

docu

men

ts.

•Re

view

s the

Ann

ual B

udge

t Est

imat

esbe

fore

subm

issio

n to

the

CA fo

r app

rova

l. •

With

the

appr

oval

of C

ount

y As

sem

bly

appr

oves

, is i

n ch

arge

of e

stab

lishm

ent a

nd d

issol

utio

n of

a c

ount

y co

rpor

atio

n •

With

the

appr

oval

of C

ount

y As

sem

bly,

app

rove

s the

est

ablis

hmen

t of a

cou

nty

emer

genc

y fu

nd.

CE

C-M

F Co

unty

Ex

ecut

ive

Com

mitt

ee

Mem

ber f

or

Fina

nce

•Re

spon

sible

for p

ropo

sing

coun

ty P

FM p

olic

ies a

nd m

anag

ing

the

budg

et p

roce

ss o

f the

Cou

nty

Gove

rnm

ent.

See

PFM

A (2

012)

Sec

tions

128

–130

. •

Prop

oses

reve

nue

raisi

ngm

easu

res,

incl

udin

g bo

rrow

ing

subj

ect t

o na

tiona

l gov

ernm

ent g

uara

ntee

. •

Desig

nate

s rec

eive

rs o

f cou

nty

reve

nues

. •

Desig

nate

s cou

nty

acco

untin

g of

ficer

s.

•M

anag

es th

e Co

unty

Rev

enue

Fun

d.

14

Budget Preparation Module – Participant Book, October 2014

•Es

tabl

ishes

the

nece

ssar

y sy

stem

s for

cas

h m

anag

emen

t as p

rovi

ded

in th

e la

w.

•Pr

epar

es a

nd su

bmits

to C

ount

y As

sem

bly

the

Med

ium

Ter

m D

ebt M

anag

emen

t Str

ateg

y.

! The

CEC

-MF

mus

t ens

ure

that

the

budg

et p

roce

ss is

con

duct

ed in

a m

anne

r and

with

in a

tim

efra

me

suffi

cien

t to

perm

it th

e ot

her p

artic

ipan

ts in

the

proc

ess t

o m

eet t

he re

quire

men

ts o

f the

CoK

(201

0) a

nd P

FMA

(201

2), i

nclu

des

ensu

ring

the

C-BR

OP,

C-F

SP a

re p

repa

red

and

subm

itted

to th

e Co

unty

Ass

embl

y on

tim

e.

CE

C-M

P CE

C M

embe

r fo

r Pla

nnin

g

•Su

bmits

the

Inte

grat

ed D

evel

opm

ent P

lan

to th

e CA

for a

ppro

val e

ach

year

.

Ci

tizen

s

•Im

port

ant r

ole

to p

artic

ipat

e in

pub

lic h

earin

gs o

n th

e CI

DP, C

-BRO

P, S

ecto

r Rep

orts

and

Bud

get E

stim

ates

. •

Impo

rtan

t rol

e in

iden

tifyi

ng c

omm

unity

nee

ds a

nd p

riorit

ies,

thro

ugh

the

coun

try

deve

lopm

ent p

lans

pla

nnin

g pr

oces

s.

•Im

port

ant r

ole

in p

rovi

ding

ove

rsig

ht a

nd fe

edba

ck o

n pr

ogra

ms a

nd p

roje

cts a

nd in

par

ticul

ar o

n th

e us

e of

pu

blic

reso

urce

s.

Co

unty

SW

Gs

Coun

ty

Sect

or

Wor

king

G

roup

s

•Co

unty

Dep

artm

ents

are

gro

uped

into

rela

ted

sect

ors,

(bas

ed o

n st

ruct

ure

of C

ount

y Go

vern

men

t), d

epen

ding

on

thei

r man

date

s and

func

tions

. •

Grou

ps m

ust a

gree

on:

o

Sect

oral

obj

ectiv

es, o

utpu

ts a

nd p

riorit

ies,

link

ed to

the

Coun

ty D

evel

opm

ent P

lan.

o

Activ

ities

, inc

ludi

ng th

e re

view

and

dev

elop

men

t of p

rogr

amm

es a

nd su

b-pr

ogra

mm

es, a

nd th

eir c

ostin

g.

oM

ediu

m-t

erm

out

puts

and

targ

ets f

or th

e se

ctor

and

est

imat

e re

sour

ce re

quire

men

ts fo

r the

sect

or.

•Gr

oups

nee

d to

link

shar

ing

of a

vaila

ble

reso

urce

s to

the

criti

cal p

riorit

ies o

f the

sect

or (r

efer

red

to a

s ‘se

ctor

re

sour

ce sh

arin

g pr

oces

s’).

•Th

e Se

ctor

Wor

king

gro

up is

cha

ired

by th

e co

unty

chi

ef o

ffice

rs w

ith a

con

veno

r fro

m th

e Co

unty

Tre

asur

y.

15

Budget Preparation Module – Participant Book, October 2014

CT

Coun

ty

Trea

sury

•Ha

s ove

rall

resp

onsib

ility

for m

anag

ing

the

finan

cial

and

eco

nom

ic a

ffairs

of t

he C

ount

y Go

vern

men

t. •

Prep

ares

and

subm

its th

e C-

FSP

to th

e CE

C fo

r app

rova

l. •

Subm

its C

ount

y De

bt M

anag

emen

t Str

ateg

y to

the

CA.

•Dr

ives

the

MTE

F pr

oces

s, (t

he th

ree-

year

rolli

ng p

lan)

wor

king

clo

sely

with

rele

vant

dep

artm

ents

and

in

stitu

tions

in th

e co

unty

and

the

depa

rtm

ent i

n ch

arge

of e

cono

mic

pla

nnin

g.

•Pr

epar

es A

nnua

l Bud

get E

stim

ates

for t

he C

ount

y Go

vern

men

t (CG

)and

coo

rdin

ates

the

prep

arat

ion

and

impl

emen

tatio

n of

the

CG b

udge

t. •

Enfo

rces

Fisc

al R

espo

nsib

ility

Prin

cipl

es a

t the

CG

leve

l. •

Prep

ares

bud

get,

finan

cial

and

fisc

al re

port

s and

subm

its th

em to

the

CA a

nd a

lso p

ublis

hes a

nd p

ublic

izes

them

. •

Prep

ares

bud

get,

finan

cial

and

fisc

al re

port

s and

subm

its th

em to

the

CA a

nd a

lso p

ublis

hes a

nd p

ublic

izes

them

. •

Coor

dina

tes t

he p

roce

ss o

f fin

alizi

ng th

e bu

dget

, inc

ludi

ng c

onsu

ltatio

n w

ith o

ther

stak

ehol

ders

at t

he c

ount

y.

CFPG

C

ount

y Fi

sal

Plan

ning

G

roup

•In

cha

rge

of e

stim

atio

n of

the

coun

ty re

sour

ce e

nvel

ope.

•

Resp

onsib

le fo

r dev

elop

ing

draf

t C-B

ROP

and

C-FS

P.

•M

embe

rshi

p in

clud

es C

ount

y Tr

easu

ry, t

he d

epar

tmen

t res

pons

ible

for e

cono

mic

pla

nnin

g, a

nd o

ther

rele

vant

th

ink

tank

s on

reve

nue

fore

cast

ing

and

econ

omic

issu

es.

Nat

iona

l Lev

el In

stitu

tions

Co

B Co

ntro

ller o

f Bud

get

•Ro

le is

to o

vers

ee th

e im

plem

enta

tion

of b

udge

ts o

f nat

iona

l and

cou

nty

gove

rnm

ents

by

auth

orisi

ng

with

draw

als f

rom

:The

Con

solid

ated

Fun

d; T

he E

qual

isatio

n Fu

nd; T

he C

ount

y Re

venu

e Fu

nds.

CRA

Com

mis

sion

for

Reve

nue

Allo

catio

n,

(CRA

)

•Re

com

men

ds th

e ba

sis fo

r the

equ

itabl

e sh

arin

g of

reve

nue

betw

een

natio

nal a

nd c

ount

y go

vern

men

ts

and

allo

catio

n am

ong

coun

ty g

over

nmen

ts (A

rtic

le 2

16).

16

Budget Preparation Module – Participant Book, October 2014

•Re

com

men

ds re

venu

e en

hanc

emen

t mea

sure

s for

bot

h le

vels.

•

Prop

oses

revi

sion

of re

venu

e sh

arin

g/al

loca

tion

form

ula.

IBEC

In

ter-

gove

rnm

enta

l Bu

dget

and

Ec

onom

ic C

ounc

il

•IB

EC p

rovi

des a

mea

ns fo

r con

sulta

tionb

etw

een

the

two

tiers

of g

over

nmen

t and

am

ong

CGs o

n a

broa

d ra

nge

of e

cono

mic

and

fina

ncia

l iss

ues,

incl

udin

g:bo

rrow

ing

and

guar

ante

es; b

udge

ts; d

evel

opm

ent

plan

s; c

ash

disb

urse

men

ts; r

egul

atio

ns to

PFM

Act

, 201

2; d

ivisi

on o

f rev

enue

.

NT

N

atio

nal T

reas

ury

•

Has o

vera

ll re

spon

sibili

ty fo

r mac

roec

onom

ic m

anag

emen

t, na

tiona

l eco

nom

ic p

olic

y.

•Re

spon

sible

for o

vera

ll re

venu

e m

obili

zatio

n an

d de

bt g

uara

ntee

s to

coun

ty g

over

nmen

ts.

•Pr

epar

es a

nnua

l bud

get e

stim

ates

of r

even

ues a

nd e

xpen

ditu

res o

f the

NG

and

coor

dina

tes t

he

prep

arat

ion

and

impl

emen

tatio

n of

the

NG

budg

et.

•Pr

epar

es th

e Bu

dget

Pol

icy

Stat

emen

tand

the

Budg

et R

evie

w a

nd O

utlo

ok p

aper

for t

he N

atio

nal

Gove

rnm

ent.

•En

forc

esfis

cal r

espo

nsib

ility

prin

cipl

es a

t nat

iona

l lev

el.

•Pr

epar

es th

e pr

e-an

d-po

st b

udge

t rep

orts

.

N-B

AC

Nat

iona

l Ass

embl

y Bu

dget

and

Ap

prop

riatio

n Co

mm

ittee

•Re

view

s and

app

rove

s the

BPS

that

sets

pol

icie

s and

gui

des b

udge

ting,

ver

tical

shar

ing

of th

e na

tiona

lly

Raise

d Re

venu

es, c

ount

ies n

ot to

pre

judi

ce se

t eco

nom

ic p

olic

ies.

•

Prov

ides

gen

eral

dire

ctio

n on

bud

geta

ry m

atte

rs.

•M

onito

rs a

dher

ence

to P

FM p

rinci

ples

and

acc

ount

abili

ty b

y pa

rliam

ent,

the

Judi

ciar

y an

d N

atio

nal

Gove

rnm

ent a

nd o

ther

pub

lic e

ntiti

es.

•Re

view

s mon

ey b

ills i

nclu

ding

the

Annu

al D

ivisi

on o

f Rev

enue

, ens

ures

adh

eren

ce to

PFM

Fin

anci

al

prin

cipa

ls in

the

Cons

titut

ion

and

adhe

renc

e to

app

rove

d Fi

scal

fram

ewor

k.

•Re

view

s Ann

ual B

udge

t est

imat

es o

f exp

endi

ture

and

reve

nue

and

intr

oduc

es th

e an

nual

an

dSup

plem

enta

ry A

ppro

pria

tions

.

17

Budget Preparation Module – Participant Book, October 2014

PBO

Pa

rliam

enta

ry

Budg

et O

ffic

e •

Prov

ides

pro

fess

iona

l adv

ice

on b

udge

ting

and

over

all P

FM, f

inan

ce a

nd e

cono

mic

info

rmat

ion

to

parli

amen

t (its

adv

ice

on re

venu

es a

ffect

s ove

rall

reso

urce

env

elop

e).

•Pr

ovid

es a

naly

sis o

n al

l bill

s tha

t hav

e an

eco

nom

ic a

nd fi

nanc

ial i

mpa

ct.

•Re

view

s and

adv

ices

rele

vant

com

mitt

ees o

f par

liam

ent o

nleg

islat

ivep

ropo

sals

for D

ivisi

on o

f Rev

enue

an

d Co

unty

Allo

catio

n of

Rev

enue

. •

Prov

ides

a te

chni

cal b

ridge

bet

wee

n th

e le

gisla

ture

, the

exe

cutiv

e an

d ot

her n

atio

nal a

nd in

tern

atio

nal

orga

nisa

tions

with

inte

rest

in b

udge

tary

and

soci

al e

cono

mic

mat

ters

.

PDM

O

Publ

ic D

ebt

Man

agem

ent O

ffic

e •

Advi

ses o

n m

anag

emen

t of n

atio

nal g

over

nmen

t deb

t (in

ord

er to

min

imize

risk

s).

•Ad

vise

s on

debt

sust

aina

bilit

y w

hich

impa

cts o

n gu

aran

tees

to c

ount

ies a

nd p

ublic

ent

ities

. •

Prep

ares

and

upd

ates

the

annu

al M

ediu

m T

erm

deb

t man

agem

ent s

trat

egy.

•

Carr

ies o

ut o

n a

regu

lar b

asis

a de

bt su

stai

nabi

lity

anal

ysis.

•

Proc

esse

s the

issu

ance

of l

oan

guar

ante

es in

clud

ing

asse

ssm

ent a

nd m

anag

emen

t of r

isks i

n th

e N

atio

nal G

over

nmen

t gua

rant

ee.

•M

aint

ains

and

upd

ates

nat

iona

l deb

t inc

ludi

ng g

uara

ntee

s and

any

der

ivat

ive

finan

cial

inst

rum

ent t

hat

gove

rnm

ent m

ay e

nter

into

. S-

F&BC

Se

nate

Fin

ance

and

Bu

dget

Com

mitt

ee

•Pr

opos

es to

the

sena

te th

e cr

iteria

for a

lloca

tion

of re

venu

es a

mon

g co

untie

s.

•Re

view

s the

Ann

ual D

ivisi

on o

f Rev

enue

Bill

whe

n su

bmitt

ed to

Sen

ate

by th

e N

atio

nal A

ssem

bly.

•

Revi

ews a

nd re

com

men

ds to

the

sena

te th

e An

nual

Cou

nty

Allo

catio

n of

Rev

enue

Bill

. •

Exam

ines

fina

ncia

l sta

tem

ent s

ubm

itted

to th

e se

nate

. •

Mon

itors

the

adhe

renc

e by

the

Coun

ty e

ntiti

es to

prin

cipl

es o

f pub

lic fi

nanc

e as

set o

ut in

the

cons

titut

ion.

Sour

ce: S

ome

cont

ent i

n th

is ta

ble

adap

ted

from

Pow

erPo

int p

rese

ntat

ions

dev

elop

ed b

y N

atio

nal T

reas

ury—

‘Con

stitu

tiona

l and

lega

l fra

mew

ork

for P

FM

and

impl

icat

ion

on C

ount

y PF

M’,

‘Ken

ya’s

new

bud

get p

roce

ss’ a

nd ‘I

mpl

emen

tatio

n of

the

Publ

ic F

inan

ce M

anag

emen

t Act

, 201

2’.

18

Budget Preparation Module – Participant Book, October 2014

Tab

le 4

: Qu

ick

Ref

eren

ce—

Key

doc

um

ents

in

the

cou

nty

bu

dg

et p

repa

rati

on p

roce

ss

Docu

men

t

Wha

t is i

t?

Why

is it

pro

duce

d?

Who

pro

duce

s it a

nd b

y w

hen?

Ho

w d

oes t

his d

ocum

ent

prog

ress

the

budg

et

prep

arat

ion

cycl

e?

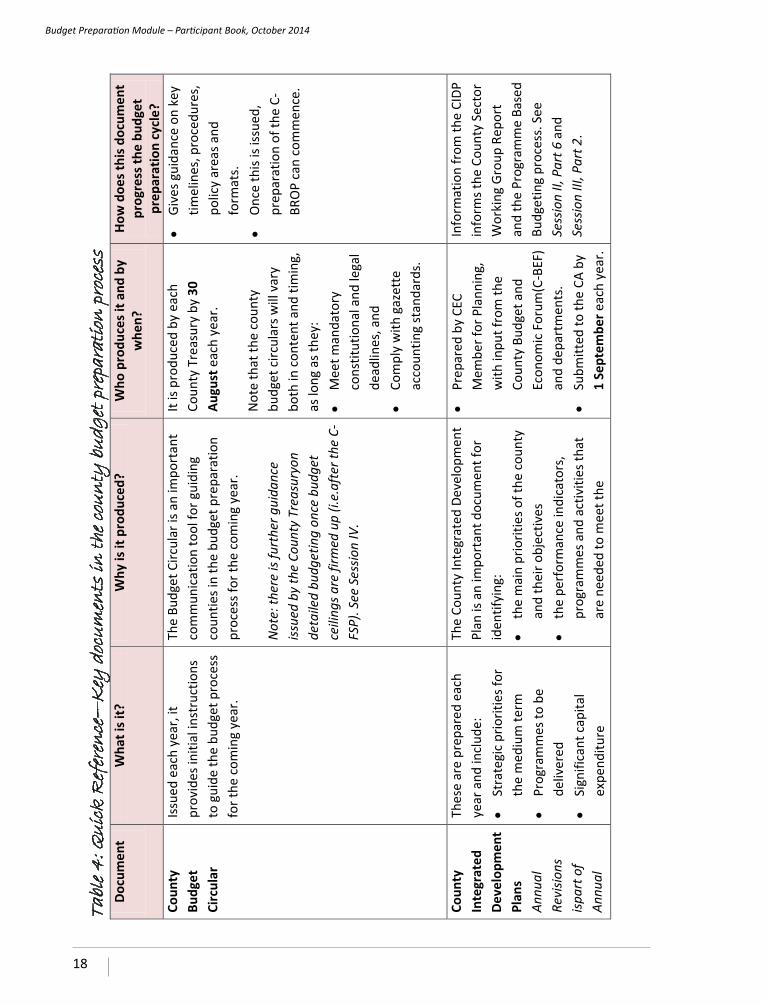

Coun

ty

Budg

et

Circ

ular

Issu

ed e

ach

year

, it

prov

ides

initi

al in

stru

ctio

ns

to g

uide

the

budg

et p

roce

ss

for t

he c

omin

g ye

ar.

The

Budg

et C

ircul

ar is

an

impo

rtan

t co

mm

unic

atio

n to

ol fo

r gui

ding

co

untie

s in

the

budg

et p

repa

ratio

n pr

oces

s for

the

com

ing

year

. N

ote:

ther

e is

furt

her g

uida

nce

issue

d by

the

Coun

ty T

reas

uryo

n de

taile

d bu

dget

ing

once

bud

get

ceili

ngs a

re fi

rmed

up

(i.e.

afte

r the

C-

FSP)

. See

Ses

sion

IV.

It is

prod

uced

by

each

Co

unty

Tre

asur

y by

30

Augu

st e

ach

year

. N

ote

that

the

coun

ty

budg

et c

ircul

ars w

ill v

ary

both

in c

onte

nt a

nd ti

min

g,

as lo

ng a

s the

y:

•M

eet m

anda

tory

co

nstit

utio

nal a

nd le

gal

dead

lines

, and

•

Com

ply

with

gaz

ette

ac

coun

ting

stan

dard

s.

•Gi

ves g

uida

nce

on k

ey

timel

ines

, pro

cedu

res,

po

licy

area

s and

fo

rmat

s.

•O

nce

this

is iss

ued,

pr

epar

atio

n of

the

C-BR

OP

can

com

men

ce.

Coun

ty

Inte

grat

ed

Deve

lopm

ent

Plan

s An

nual

Re

visio

ns

ispar

t of

Annu

al

Thes

e ar

e pr

epar

ed e

ach

year

and

incl

ude:

•

Stra

tegi

c pr

iorit

ies f

or

the

med

ium

term

•

Prog

ram

mes

to b

e de

liver

ed

•Si

gnifi

cant

cap

ital

expe

nditu

re

The

Coun

ty In

tegr

ated

Dev

elop

men

t Pl

an is

an

impo

rtan

t doc

umen

t for

id

entif

ying

: •

the

mai

n pr

iorit

ies o

f the

cou

nty

and

thei

r obj

ectiv

es

•th

e pe

rfor

man

ce in

dica

tors

, pr

ogra

mm

es a

nd a

ctiv

ities

that

ar

e ne

eded

to m

eet t

he

•Pr

epar

ed b

y CE

C M

embe

r for

Pla

nnin

g,

with

inpu

t fro

m th

e Co

unty

Bud

get a

nd

Econ

omic

For

um(C

-BEF

) an

d de

part

men

ts.

•Su

bmitt

ed to

the

CA b

y 1

Sept

embe

r eac

h ye

ar.

Info

rmat

ion

from

the

CIDP

in

form

s the

Cou

nty

Sect

or

Wor

king

Gro

up R

epor

t an

d th

e Pr

ogra

mm

e Ba

sed

Budg

etin

g pr

oces

s. S

ee

Sess

ion

II, P

art 6

and

Se

ssio

n III

, Par

t 2.

19

Budget Preparation Module – Participant Book, October 2014

Budg

et

•Gr

ants

, tra

nsfe

rs a

nd

subs

idie

s to

be m

ade

on

beha

lf of

CGs

.

obje

ctiv

es

•th

e co

stin

gs o

f the

prio

ritize

d ac

tiviti

es.

Coun

ty

Budg

et

Revi

ew a

nd

Out

look

Pa

per (

C-BR

OP)

The

C-BR

OP

com

pare

s pr

evio

us y

ear’s

reve

nue

and

spen

ding

aga

inst

wha

t was

pl

anne

d in

the

budg

et.

The

C-BR

OP

outli

nes:

•

Actu

al fi

scal

per

form

ance

in th

e pr

evio

us y

ear

•U

pdat

ed e

cono

mic

and

fina

ncia

l fo

reca

sts (

show

ing

any

chan

ges

from

the

fore

cast

s in

the

C-FS

P fr

om th

e pr

evio

us y

ear)

•

Iden

tific

atio

n of

bro

ad p

olic

y pr

iorit

ies

•In

dica

tive

avai

labl

e re

sour

ces t

o fu

nd C

G pr

iorit

ies.

•Pr

epar

ed b

y th

e Co

unty

Tr

easu

ry (

Coun

ty F

iscal

Pl

anni

ng G

roup

). •

Subm

itted

to C

A by

30

Sept

embe

r eac

h ye

ar.

•C-

BRO

P al

low

s for

the

CEC

to e

ngag

e on

ex

pend

iture

stra

tegi

es,

as w

ell a

s brie

f the

CA

on th

e bu

dget

pro

cess

an

d ec

onom

y of

the

coun

ty.

•O

nce

indi

cativ

e av

aila

ble

reso

urce

s are

id

entif

ied

in th

e C-

BRO

P, S

ecto

r Wor

king

Gr

oups

can

mee

t to

iden

tify

prio

ritie

s for

th

e co

min

g ye

ar.

Se

ctor

W

orki

ng

Gro

up R

epor

t

A re

port

whi

ch g

ives

sect

or

Visio

n an

d M

issio

n,

Stra

tegi

c Go

als o

f the

se

ctor

. A re

view

of t

he p

ast

perf

orm

ance

of t

he se

ctor

, in

clud

ing

a m

ediu

m te

rm

prio

ritie

s and

fina

ncia

l pla

n

The

purp

ose

of th

e Se

ctor

Rep

ort i

s to

out

linin

g th

e pr

iorit

izatio

n of

(c

oste

d) p

rogr

amm

es a

nd su

b-pr

ogra

mm

es, e

xpec

ted

outc

omes

, ou

tput

s and

key

per

form

ance

in

dica

tors

. The

Cou

nty

Inte

grat

ed

Deve

lopm

ent P

lan

is an

impo

rtan

t

•De

part

men

ts c

lust

ered

in

to se

ctor

s, le

d by

Ac

coun

ting

Offi

cers

. •

Grou

ps c

onve

ned

in

Oct

ober

, fol

low

ing

prep

arat

ion

of C

-BRO

P.

The

Sect

or R

epor

ts

prov

ide

a ba

sis fo

r the

de

part

men

ts to

go

thro

ugh

a pr

oces

s of

shar

ing

or a

lloca

ting

reso

urce

s am

ong

them

selv

es, o

n th

e ba

sis

20

Budget Preparation Module – Participant Book, October 2014

for t

he M

TEF

perio

d.

The

repo

rt g

ives

det

ails

of

cont

inui

ng p

roje

cts a

nd

prog

ram

s tha

t nee

d fu

ndin

g in

com

ing

fisca

l yea

r, w

hich

sh

ould

be

allo

cate

d fu

nds

befo

re n

ew o

nes.

docu

men

t to

info

rm th

e de

velo

pmen

t of t

his r

epor

t. A

form

at fo

r the

Sec

tor W

orki

ng

Grou

p re

port

is p

rovi

ded

in A

nnex

3.

of th

e se

ctor

al re

view

. Th

is w

ill th

en fe

ed in

to th

e pr

oces

s of p

repa

ring

depa

rtm

enta

l bud

get

estim

ates

, in

the

Ope

ratio

nal P

hase

of

budg

et p

repa

ratio

n.

Co

unty

Fis

cal

Stra

tegy

Pa

per (

C-FS

P)

The

C-FS

P co

ntai

ns:

•Su

mm

ary

of re

venu

e an

d ex

pend

iture

pe

rfor

man

ce fo

r the

FY

to d

ate.

•

Asse

ssm

ent f

or th

e re

mai

nder

of t

he

curr

ent F

Y.

•Br

oad

stra

tegi

c pr

iorit

ies a

nd p

olic

y go

als (

med

ium

and

lo

ng-t

erm

). •

Fina

ncia

l out

look

on

expe

nditu

res,

reve

nues

an

d bo

rrow

ing

for t

he

med

ium

term

.

The

CFSP

gui

des t

he fo

rmat

ion

of

the

budg

et fo

r the

com

ing

finan

cial

ye

ar. I

t loo

ks a

t pro

ject

ed re

venu

e an

d ex

pend

iture

and

impo

rtan

tly,

wha

t pro

port

ion

of th

e co

unty

’s

budg

et w

ill b

e al

loca

ted

to e

ach

sect

or. T

he S

ecto

r Wor

king

Gro

up

Repo

rts w

ill in

form

this

proc

ess.

•Pr

epar

ed b

y Co

untr

y Tr

easu

ry (

Coun

ty F

iscal

Pl

anni

ng G

roup

) •

Prep

ared

in ti

me

for

revi

ew a

nd a

ppro

val b

y th

e CE

C be

fore

su

bmiss

ion

to th

e CA

by

28 F

ebru

ary.

The

subm

issio

n of

the

C-FS

P sig

nals

the

end

of th

e ‘S

trat

egic

Pha

se’ o

f bud

get

prep

arat

ion

and

the

star

t of

the

‘Ope

ratio

nal P

hase

’. Fu

rthe

r ins

truc

tions

are

pr

ovid

ed to

cou

ntie

s on

how

to p

repa

re th

e de

taile

d bu

dget

est

imat

es.

!Not

e: T

he C

-FSP

mus

t be

alig

ned

with

the

natio

nal o

bjec

tives

in th

e Bu

dget

Pol

icy

Stat

emen

t (BP

S). T

he B

PS is

subm

itted

for a

ppro

val b

y on

15 F

ebru

ary,

whi

ch g

ives

co

untie

s tw

o w

eeks

to c

onsid

er th

e na

tiona

l obj

ectiv

es in

the

BPS

and

alig

n th

eir o

wn

C-FS

P ac

cord

ingl

y, b

efor

e su

bmitt

ing

by th

e en

d of

Feb

ruar

y.

21

Budget Preparation Module – Participant Book, October 2014

Coun

ty D

ebt

Man

agem

ent

Stra

tegy

This

med

ium

-ter

m st

rate

gy

stat

es a

ctua

l and

like

ly

liabi

lity

for t

he c

ount

y an

d ho

w to

dea

l with

it.

The

debt

man

agem

ent s

trat

egy

outli

nes:

•

The

tota

l sto

ck o

f deb

t as a

t the

da

te o

f the

stat

emen

t. •

The

sour

ces o

f loa

ns m

ade

to th

e co

unty

gov

ernm

ent a

nd ri

sks

asso

ciat

ed w

ith th

ose

loan

s.

•Th

e as

sum

ptio

ns u

nder

lyin

g th

e de

bt m

anag

emen

t str

ateg

y; a

nd

an a

naly

sis o

f the

sust

aina

bilit

y of

the

amou

nt o

f deb

t, bo

th

actu

al a

nd p

oten

tial.

The

Coun

ty D

ebt

Man

agem

ent S

trat

egy

is co

mpl

eted

and

su

bmitt

ed a

t the

sam

e tim

e as

the

C-FS

P, b

y 28

Fe

brua

ry.

The

Coun

ty D

ebt

Man

agem

ent S

trat

egy

com

plem

ents

the

C-FS

P in

th

at it

out

lines

how

co

untie

s pla

n to

dea

l with

an

y in

herit

ed d

ebt.

Sour

ce: S

ome

cont

ent i

n th

is ta

ble

adap

ted

from

pre

sent

atio

ns ‘C

onst

itutio

nal a

nd le

gal f

ram

ewor

k fo

r PFM

and

impl

icat

ion

on C

ount

y PF

M’,

by A

. Mw

enda

, N

atio

nal T

reas

ury

and

‘Ken

ya’s

new

bud

get p

roce

ss’.

22

Budget Preparation Module – Participant Book, October 2014

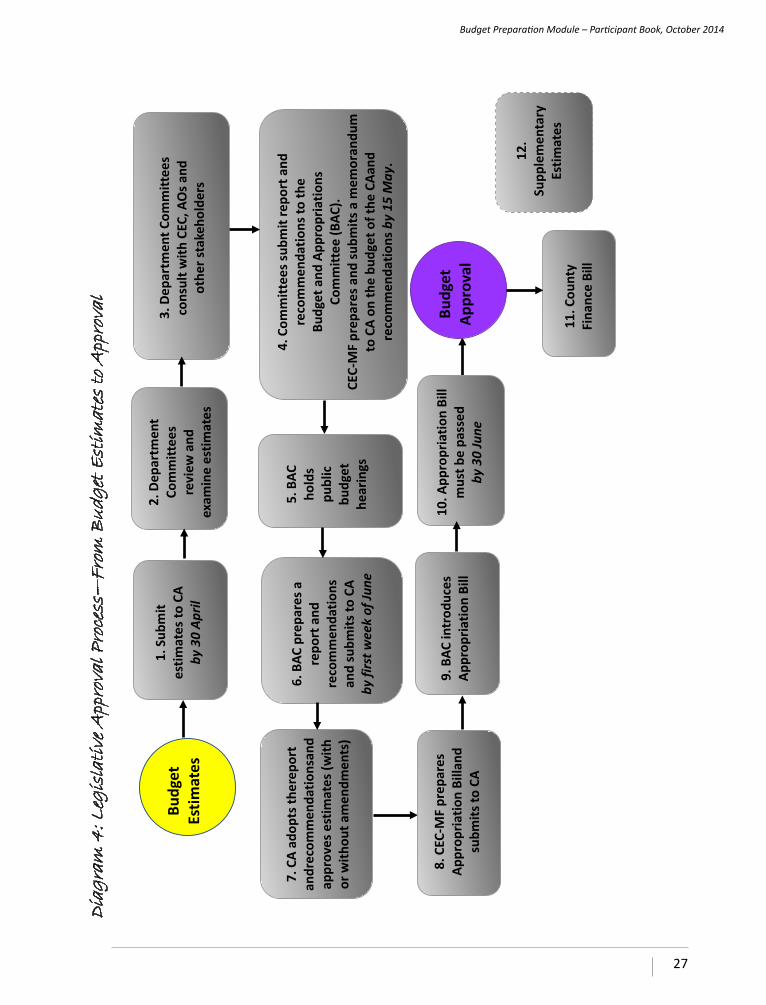

2. County Budget Cycle and Calendar Table 5: County Budget Calendar

Target Date (annually)

Activity Relevant Legislation

30 August

• Issued by CEC-MF from each county. • Budget Circular must also outline procedures for

inviting the public to participate in the process.

PFMA (2012) Section 128 (2)

1 September

• The CEC-MP submits the Development Plan to the County Assembly (CA) for approval.

• Copy of the plan to CRA and National Treasury (NT).

!Within 7 days of submission to the CA, the CEC-MP

must publish and publicize the plan.

PFMA (2012) Section 126 (3)

County Budget Circular Issued

County Integrated Development Plan Submitted

Concepts Box: County Budget Cycle and Calendar • The imperative for a county budgeting process is set down in key legislation –

including the Constitution of Kenya (2010) and the Public Finance Management Act (2012) (see Table 2).

• The budgeting process can be seen as a cycle (See Diagram 2), whereby the results of each year feed into the process for the following year.

• Linked to this budgeting cycle is a calendar (see Table 5; Diagram 3), which identifies target dates for the submission and approval of key budget documents. Many of these target dates for counties are aligned with key dates for the national budget.

• It is important to understand that the annual budgeting process ideally takes place using a Medium Term Expenditure Framework (MTEF)approach, which will be introduced later in this session.

• The Budget Calendar also identifies timeframes within which relevant documents must be published and publicized, in the interests of public participation. More details about public participation in the budgeting process will be provided later in this session.

23

Budget Preparation Module – Participant Book, October 2014

30 September

• The County Treasury (CT) prepares and submits the