budget integration to governmental accounting reports

TRANSCRIPT

Budget Integration to Governmental Budget Integration to Governmental Accounting ReportsAccounting Reports

Budgetary Basis of Accounting Budgetary Basis of Accounting Budgetary Control and Budgetary Accounting PoliciesBudgetary Control and Budgetary Accounting Policies

1.1. Each May, the City Manager submits to the City Council a proposed operating Each May, the City Manager submits to the City Council a proposed operating budget for the fiscal year commencing the following July 1. The operating budget for the fiscal year commencing the following July 1. The operating budget includes proposed expenditures and the means of financing them.budget includes proposed expenditures and the means of financing them.

2.2. Public hearings are conducted to obtain citizen’s comments.Public hearings are conducted to obtain citizen’s comments.3.3. The budget is legally enacted by City Council resolution. The budget is legally enacted by City Council resolution. 4.4. All budget adjustments over $5,000 and transfers between funds must be All budget adjustments over $5,000 and transfers between funds must be

approved by the City Council by resolution during the fiscal year. The City approved by the City Council by resolution during the fiscal year. The City Manager is authorized to transfer any unencumbered appropriations within a Manager is authorized to transfer any unencumbered appropriations within a fund or department, and may authorize encumbrances under $1,000. The fund or department, and may authorize encumbrances under $1,000. The legally adopted budget requires that expenditures not exceed total legally adopted budget requires that expenditures not exceed total appropriations within each fund. appropriations within each fund.

5.5. Budgets are adopted on a basis consistent with GAAP for governmental funds. Budgets are adopted on a basis consistent with GAAP for governmental funds. Budgets are adopted for the General Fund, all Special Revenue Funds except Budgets are adopted for the General Fund, all Special Revenue Funds except the Asset Forfeiture Fund, all Capital Projects Funds, and the Debt Service the Asset Forfeiture Fund, all Capital Projects Funds, and the Debt Service Fund. Fund.

6.6. Formal budgetary integration is employed as a management control device Formal budgetary integration is employed as a management control device during the year for all budgeted funds. during the year for all budgeted funds.

7.7. Budgeted amounts are as originally adopted, or as amended by the City Budgeted amounts are as originally adopted, or as amended by the City Council. Individual amendments were not material in relation to the original Council. Individual amendments were not material in relation to the original appropriations which were amended.appropriations which were amended.

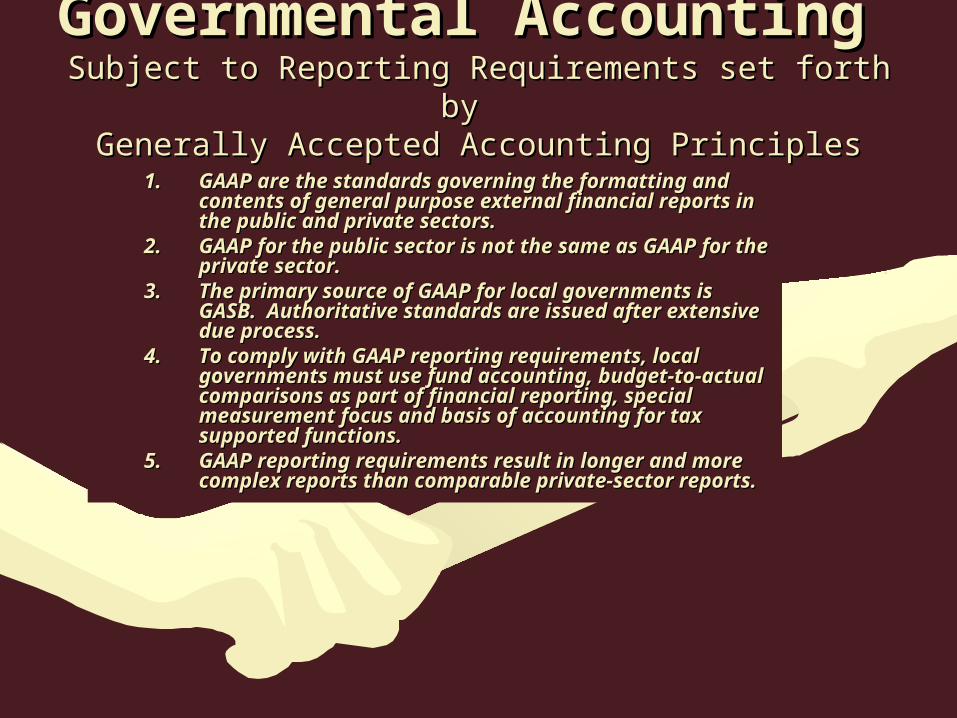

Governmental Accounting Governmental Accounting Subject to Reporting Requirements set forth by Subject to Reporting Requirements set forth by

Generally Accepted Accounting Principles (GAAP)Generally Accepted Accounting Principles (GAAP)1.1. GAAP are the standards governing the formatting and contents GAAP are the standards governing the formatting and contents

of general purpose external financial reports in the public and of general purpose external financial reports in the public and private sectors. private sectors.

2.2. GAAP for the public sector is not the same as GAAP for the GAAP for the public sector is not the same as GAAP for the private sector. private sector.

3.3. The primary source of GAAP for local governments is GASB. The primary source of GAAP for local governments is GASB. Authoritative standards are issued after extensive due process.Authoritative standards are issued after extensive due process.

4.4. To comply with GAAP reporting requirements, local To comply with GAAP reporting requirements, local governments must use fund accounting, budget-to-actual governments must use fund accounting, budget-to-actual comparisons as part of financial reporting, special measurement comparisons as part of financial reporting, special measurement focus and basis of accounting for tax supported functions.focus and basis of accounting for tax supported functions.

5.5. GAAP reporting requirements result in longer and more GAAP reporting requirements result in longer and more complex reports than comparable private-sector reports.complex reports than comparable private-sector reports.

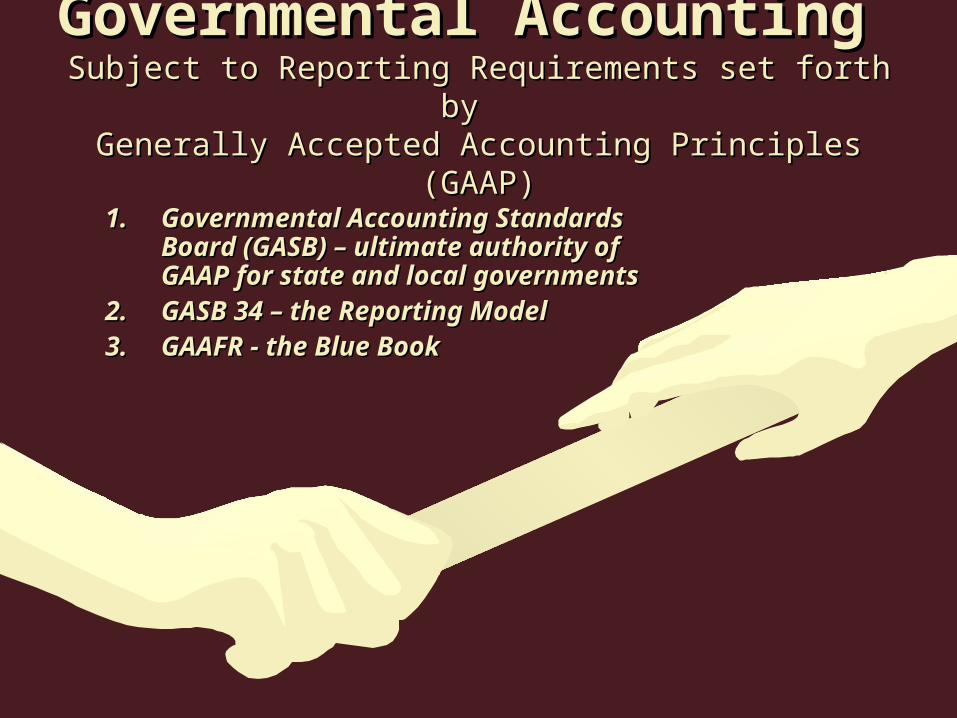

Governmental AccountingGovernmental Accounting Subject to Reporting Requirements set forth by Subject to Reporting Requirements set forth by

Generally Accepted Accounting Principles (GAAP)Generally Accepted Accounting Principles (GAAP)

1.1. Governmental Accounting Standards Board Governmental Accounting Standards Board (GASB) – ultimate authority of GAAP for state (GASB) – ultimate authority of GAAP for state and local governments and local governments

2.2. GASB 34 – the Reporting ModelGASB 34 – the Reporting Model3.3. GAAFR - the Blue BookGAAFR - the Blue Book

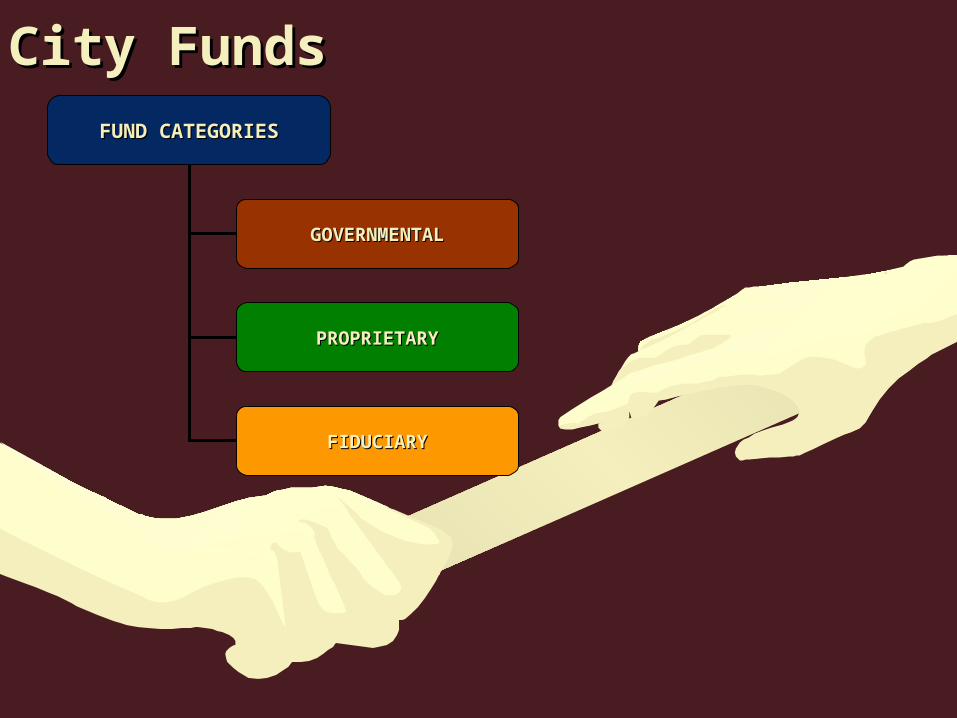

City FundsCity Funds

FUND CATEGORIESFUND CATEGORIES

GOVERNMENTALGOVERNMENTAL

PROPRIETARYPROPRIETARY

FIDUCIARYFIDUCIARY

Governmental FundsGovernmental Funds

General FundGeneral Fund

1.1. Accounts for essential services mainly supported by taxes, fees and Accounts for essential services mainly supported by taxes, fees and licenses, and other general revenueslicenses, and other general revenues

2.2. Revenues are not dedicated for specific useRevenues are not dedicated for specific use3.3. Expenditures for public safety are 65-70% of totalExpenditures for public safety are 65-70% of total4.4. Declining revenue stream Declining revenue stream

Governmental FundsGovernmental FundsSpecial Revenue FundsSpecial Revenue Funds

Account for revenues received for a specific purpose/projectAccount for revenues received for a specific purpose/project

1.1. Gas TaxGas Tax2.2. Fire & Police GrantsFire & Police Grants3.3. ATOD GrantATOD Grant4.4. RedevelopmentRedevelopment5.5. CDBGCDBG

Governmental FundsGovernmental FundsCapital Project Funds Capital Project Funds

Account for capital improvement projectsAccount for capital improvement projects

1.1. Storm DrainStorm Drain2.2. Municipal ImprovementsMunicipal Improvements3.3. Roadway ImpactRoadway Impact4.4. Street ProjectsStreet Projects

Governmental FundsGovernmental FundsDebt Service FundsDebt Service Funds

Pay for principal/interest for general purpose bond issuesPay for principal/interest for general purpose bond issues

1.1. Firehouse BondFirehouse Bond2.2. Redevelopment BondRedevelopment Bond

Enterprise FundsEnterprise FundsPrimarily supported by user fees and / or charges based on Primarily supported by user fees and / or charges based on

the cost of providing servicethe cost of providing service

1.1. WaterWater2.2. SewerSewer3.3. Airport Airport 4.4. Transit Transit 5.5. Business ParkBusiness Park

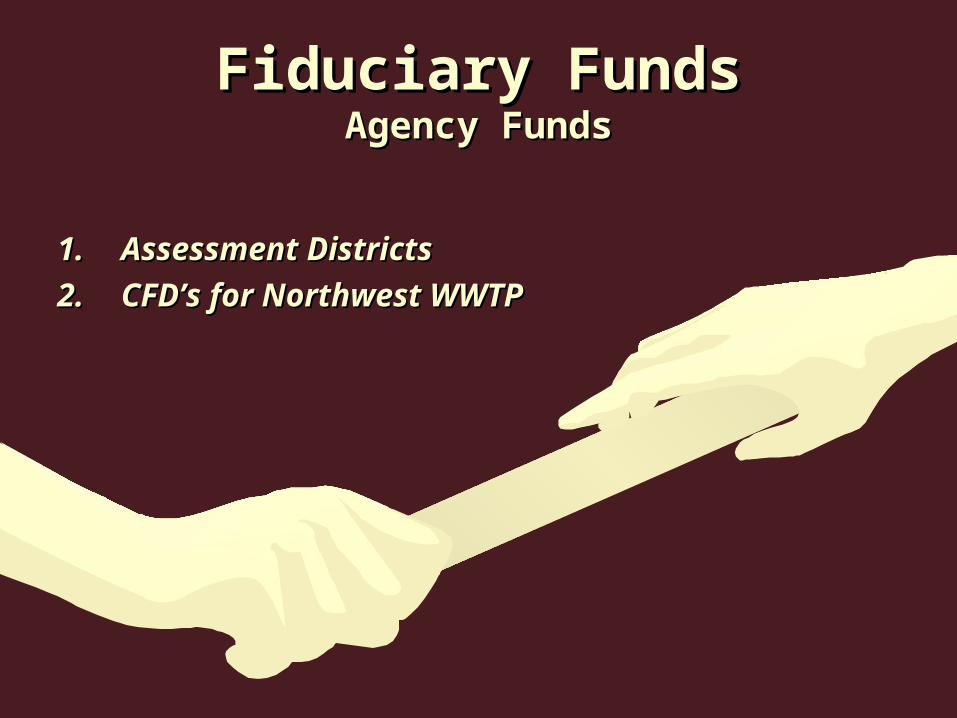

Fiduciary FundsFiduciary FundsAgency FundsAgency Funds

1.1. Assessment DistrictsAssessment Districts

2.2. CFD’s for Northwest WWTPCFD’s for Northwest WWTP

Budget MethodsBudget MethodsThere is no specific budget type required – the following are

types and methods that are incorporated into City’s budgets

1.1. Line ItemLine Item

2.2. ProgramProgram

3.3. Expenditure ControlExpenditure Control

4.4. Zero BudgetZero Budget

5.5. Multi-yearMulti-year

Line Item BudgetingLine Item Budgeting1.1. Integrated to Eden accounting systemIntegrated to Eden accounting system

2.2. Focuses on specific expendituresFocuses on specific expenditures

3.3. Budget policy segregates control into three Budget policy segregates control into three categories, personnel, operating & categories, personnel, operating & maintenance, and capital expenditures.maintenance, and capital expenditures.

4.4. Line items within the operating & Line items within the operating & maintenance categories are delegated to City maintenance categories are delegated to City staff. This is a form of Expenditure Control staff. This is a form of Expenditure Control method.method.

5.5. Control of Personnel and Capital Control of Personnel and Capital Expenditures is maintained by Council.Expenditures is maintained by Council.

Program BudgetingProgram BudgetingSSpecific program or project funded by an external sourcepecific program or project funded by an external source

1.1. Capital projectsCapital projects2.2. ATODATOD3.3. CDBGCDBG

Expenditure ControlExpenditure Control1.1. Pioneered by Fairfield City Manager Gale Pioneered by Fairfield City Manager Gale

WilsonWilson2.2. Lump sum budgets deemphasize financial detail Lump sum budgets deemphasize financial detail

by appropriating by departmentsby appropriating by departments3.3. Gives department heads more freedom to manageGives department heads more freedom to manage4.4. Elected bodies focuses more on goals and policiesElected bodies focuses more on goals and policies5.5. Incentive to save rather than “use it or lose it”Incentive to save rather than “use it or lose it”6.6. Unspent funds are carried forwardUnspent funds are carried forward

Zero Base BudgetingZero Base Budgeting1.1. All budget cost centers start with zeroAll budget cost centers start with zero2.2. Generally more burdensomeGenerally more burdensome3.3. Identifies relative priority of programsIdentifies relative priority of programs4.4. Can be modified to various funding Can be modified to various funding

levels of a base year or previous year levels of a base year or previous year budgetbudget

5.5. Works well as a process for Works well as a process for determining cutbacksdetermining cutbacks

Multi-year BudgetMulti-year BudgetMulti-yearMulti-year

1.1. The trend, 2 or 3 yr budgetsThe trend, 2 or 3 yr budgets2.2. Focus on next year; subsequent Focus on next year; subsequent

years more difficult to estimateyears more difficult to estimate3.3. Staff time savings can be achieved if Staff time savings can be achieved if

City does not go through a full City does not go through a full budget cycle by focusing on changes budget cycle by focusing on changes and exceptionsand exceptions

4.4. Alternate years can be refocused to Alternate years can be refocused to update capital budgetsupdate capital budgets

Budget PreparationBudget PreparationCalendarCalendar

1.1. Budget templates distributed to Budget templates distributed to each department for review and each department for review and completion in early Marchcompletion in early March

2.2. First draft of budget requests First draft of budget requests submitted for review in Aprilsubmitted for review in April

3.3. Budgets requests back to Budgets requests back to departments for further line item departments for further line item justifications and due in early Mayjustifications and due in early May

4.4. Complete Revenue projections in MayComplete Revenue projections in May5.5. Departments resubmitted line item Departments resubmitted line item

expenditure justification for zero based expenditure justification for zero based itemsitems

Budget PreparationBudget PreparationProcedure for operating and maintenance line itemsProcedure for operating and maintenance line items

1.1. Line Item budgeting integrated with Line Item budgeting integrated with accounting system accounting system

2.2. Program budgeting is used to Program budgeting is used to authorize funding for specific authorize funding for specific programs or projects programs or projects

3.3. Zero Based Budgeting is used Zero Based Budgeting is used where cost variable can be where cost variable can be eliminatedeliminated

Budget ApprovalBudget Approval1.1. Budget estimates provided to the City Budget estimates provided to the City

Council for discussion at public forumCouncil for discussion at public forum

2.2. Modifications made based on budget Modifications made based on budget discussiondiscussion

3.3. Final budget document brought back to Final budget document brought back to Council for final approval which establishes Council for final approval which establishes that years appropriationsthat years appropriations

Budget IssuesBudget Issues1.1. Continued decline in General Fund Continued decline in General Fund

revenuesrevenues

2.2. Governors proposal to eliminate Governors proposal to eliminate Redevelopment AgenciesRedevelopment Agencies

3.3. Local Initiative to reduce Water and Sewer Local Initiative to reduce Water and Sewer ratesrates