brookfield renewable partners (bep) - brookfield …/media/files/b/brookfield...brookfield renewable...

TRANSCRIPT

Brookfield Renewable A Leader in Renewable Power Generation

Brookfield Renewable Partners (BEP)

September 2016

Corporate Profile

2 2 CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This presentation contains forward-looking statements and information within the meaning of Canadian provincial securities laws and “forward-looking statements” within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, Section 21E of the U.S. Securities Exchange Act of 1934, as amended, “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 and in any applicable Canadian securities regulations. The words “will”, “should”, “could”, “potential”, “tend to”, “target” “future”, “growth”, “expect”, “believe”, “goal”, “plan”, derivatives thereof and other expressions which are predictions of or indicate future events, trends or prospects and which do not relate to historical matters identify the above mentioned and other forward-looking statements. Forward-looking statements in this presentation include statements regarding the quality of Brookfield Renewable’s business, the expectation for future cash flows and distribution growth, the availability of acquisition opportunities, liquidity, and the timing and completion of current acquisitions and development projects. Although Brookfield Renewable believes that these forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on them, or any other forward looking statements or information in this presentation. The future performance and prospects of Brookfield Renewable are subject to a number of known and unknown risks and uncertainties. Factors that could cause actual results of Brookfield Renewable to differ materially from those contemplated or implied by the statements in this presentation include economic conditions in the jurisdictions in which we operate; our ability to sell products and services under contract or into merchant energy markets; weather conditions and other factors which may impact generation levels at our facilities; changes to government regulations, including incentives for renewable energy; our ability to grow within our current markets or expand into new markets; our ability to complete development and capital projects on time and on budget; our inability to finance our operations or fund future acquisitions due to the status of the capital markets; the ability to effectively source, complete and integrate new acquisitions and to realize the benefits of such acquisitions; health, safety, security or environmental incidents; regulatory risks relating to the power markets in which we operate, including relating to the regulation of our assets, licensing and litigation; risks relating to our internal control environment; we do not have control over all of our operations; contract counterparties not fulfilling their obligations; and other risks associated with the construction, development and operation of power generating facilities.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. The forward-looking statements represent our views as of the date of this presentation and should not be relied upon as representing our views as of any date subsequent to the date of this presentation. While we anticipate that subsequent events and developments may cause our views to change, we disclaim any obligation to update the forward-looking statements, other than as required by applicable law. For further information on these known and unknown risks, please see “Risk Factors” included in our Form 20-F.

CAUTIONARY STATEMENT REGARDING USE OF NON-IFRS MEASURES

This presentation contains references to Adjusted EBITDA, Funds From Operations and Adjusted Funds From Operations, which are not generally accepted accounting measures under IFRS and therefore may differ from definitions of Adjusted EBITDA, Funds From Operations and Adjusted Funds From Operations used by other entities. We believe that Adjusted EBITDA, Funds From Operations and Adjusted Funds From Operations are useful supplemental measures that may assist investors in assessing the financial performance and the cash anticipated to be generated by our operating portfolio. Neither Adjusted EBITDA, Funds From Operations nor Adjusted Funds From Operations per LP Unit should be considered as the sole measure of our performance and should not be considered in isolation from, or as a substitute for, analysis of our financial statements prepared in accordance with IFRS.

References to Brookfield Renewable are to Brookfield Renewable Partners L.P. together with its subsidiary and operating entities unless the context reflects otherwise.

All amounts are in U.S. dollars and presented on a consolidated basis unless otherwise specified.

Calderwood, Tennessee, United States

Who We Are

4 Leader in Renewable Energy

One of the largest public pure-play renewable businesses globally

100 years of experience in power generation

Full operating, development and power marketing capabilities

Over 2,000 operating employees

10,700 MEGAWATTS OF

CAPACITY

88% HYDROELECTRIC

GENERATION

260 power generating facilities

15 markets in 7 countries

Situated on 82 river systems

$25B POWER ASSETS

5

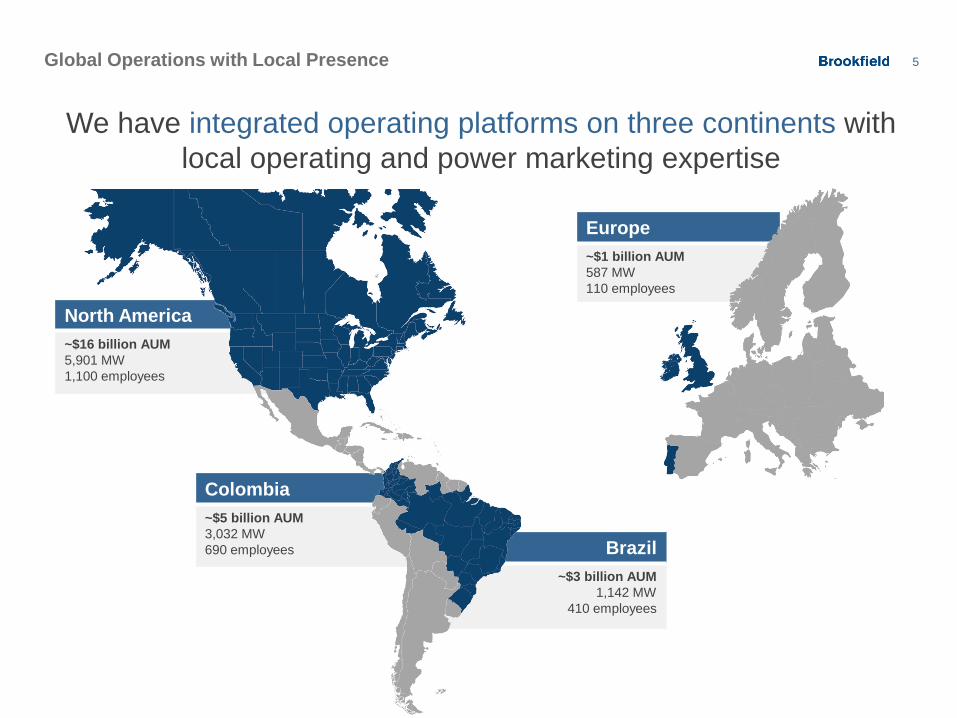

Colombia ~$5 billion AUM 3,032 MW 690 employees

Global Operations with Local Presence

We have integrated operating platforms on three continents with local operating and power marketing expertise

Europe ~$1 billion AUM 587 MW 110 employees

North America ~$16 billion AUM 5,901 MW 1,100 employees

Brazil ~$3 billion AUM

1,142 MW 410 employees

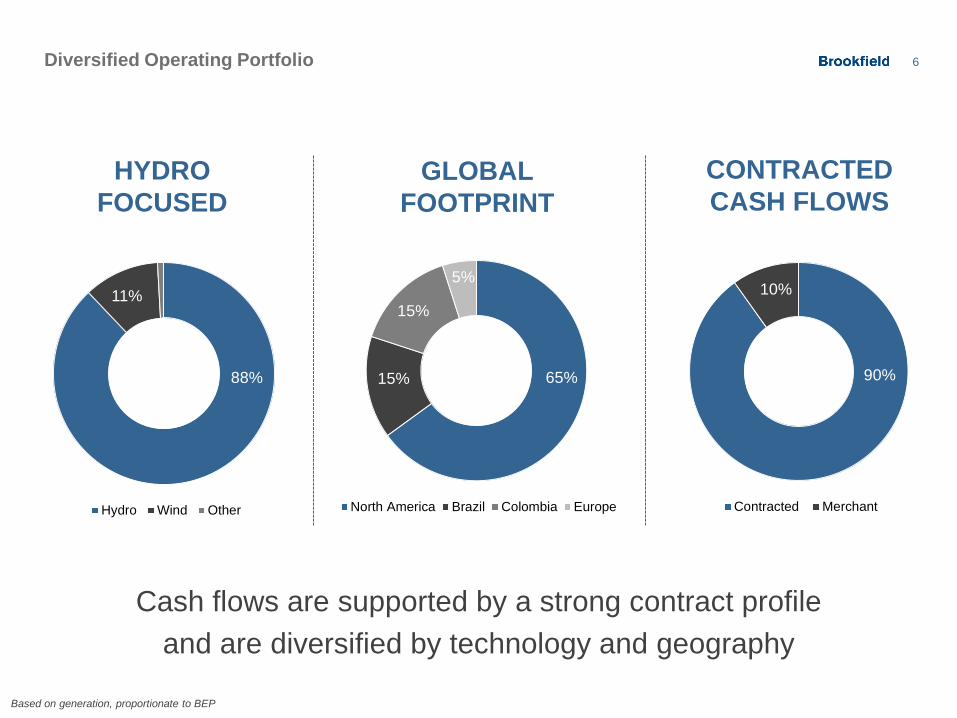

6 Diversified Operating Portfolio

Hydro Wind Other

11%

North America Brazil Colombia Europe

65%

5%

15%

15%

Contracted Merchant

90%

10%

88%

HYDRO FOCUSED

GLOBAL FOOTPRINT

CONTRACTED CASH FLOWS

Cash flows are supported by a strong contract profile and are diversified by technology and geography

Based on generation, proportionate to BEP

7

OPERATIONAL FOCUS

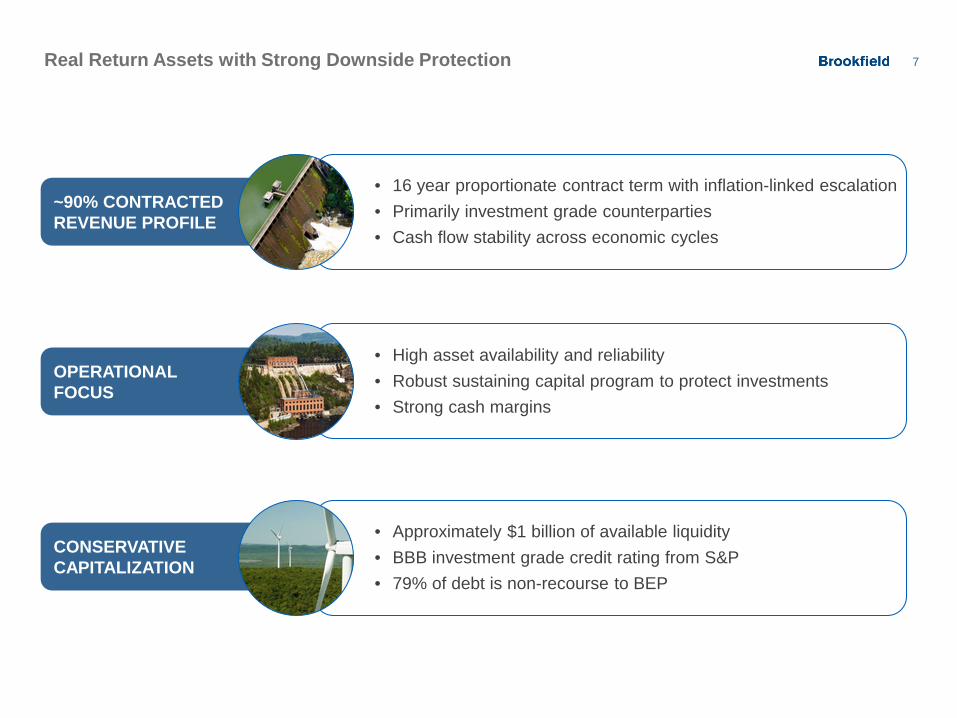

~90% CONTRACTED REVENUE PROFILE

Real Return Assets with Strong Downside Protection

CONSERVATIVE CAPITALIZATION

• High asset availability and reliability • Robust sustaining capital program to protect investments • Strong cash margins

• Approximately $1 billion of available liquidity • BBB investment grade credit rating from S&P • 79% of debt is non-recourse to BEP

• 16 year proportionate contract term with inflation-linked escalation • Primarily investment grade counterparties • Cash flow stability across economic cycles

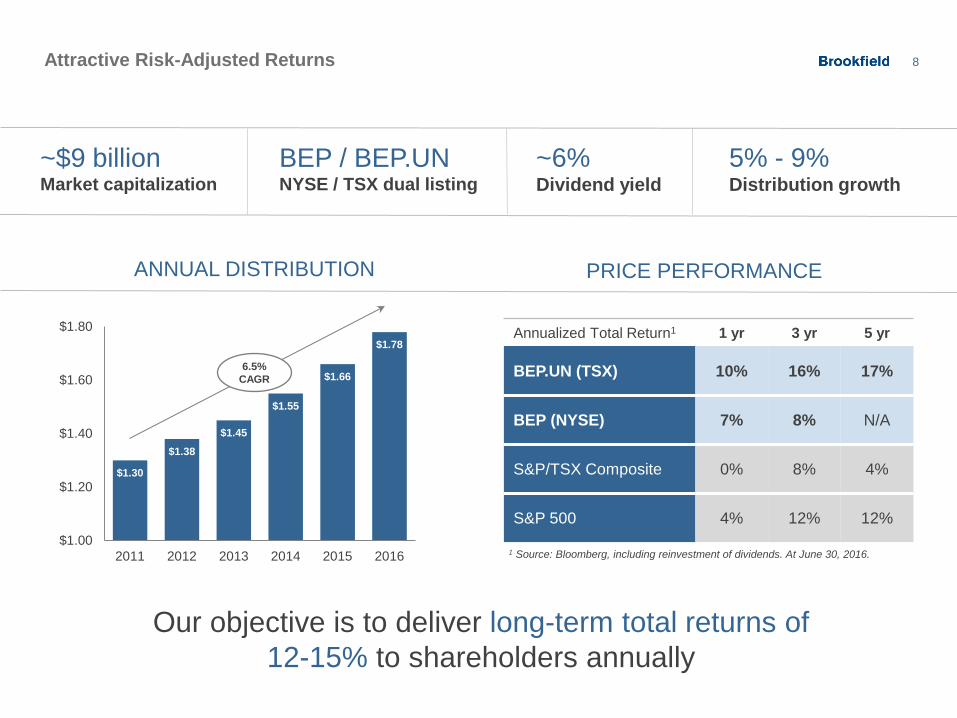

8 Attractive Risk-Adjusted Returns

BEP / BEP.UN NYSE / TSX dual listing

~6% Dividend yield

Annualized Total Return1 1 yr 3 yr 5 yr

BEP.UN (TSX) 10% 16% 17%

BEP (NYSE) 7% 8% N/A

S&P/TSX Composite 0% 8% 4%

S&P 500 4% 12% 12%

1 Source: Bloomberg, including reinvestment of dividends. At June 30, 2016.

5% - 9% Distribution growth

~$9 billion Market capitalization

$1.30

$1.38

$1.45

$1.55

$1.66

$1.78

$1.00

$1.20

$1.40

$1.60

$1.80

2011 2012 2013 2014 2015 2016

ANNUAL DISTRIBUTION PRICE PERFORMANCE

6.5% CAGR

Our objective is to deliver long-term total returns of 12-15% to shareholders annually

9 Multiple Levers to Drive Growth

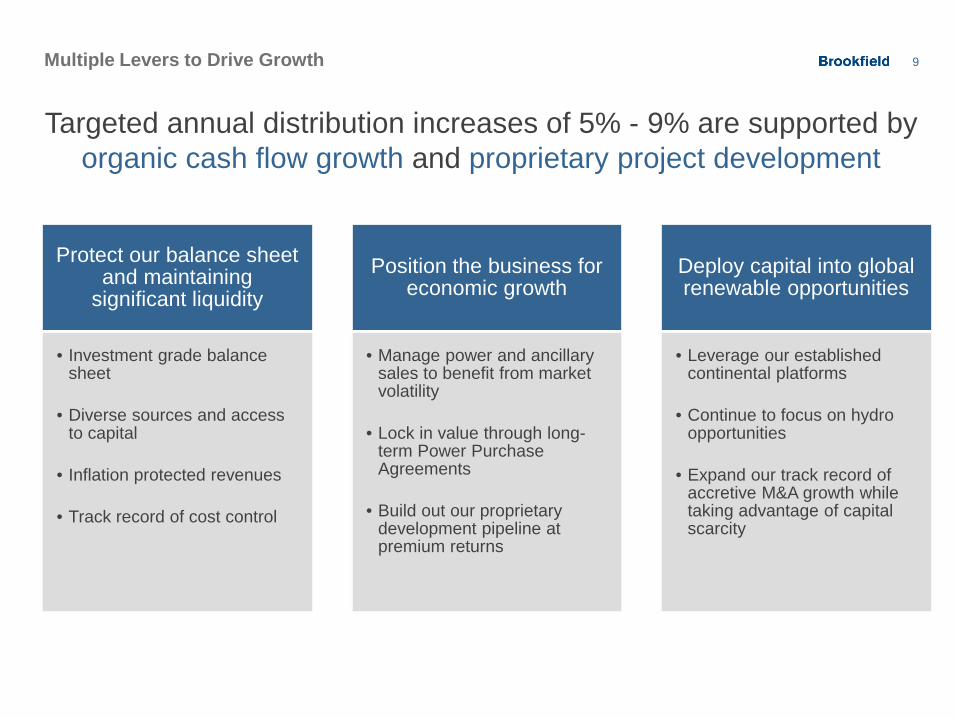

Targeted annual distribution increases of 5% - 9% are supported by organic cash flow growth and proprietary project development

Protect our balance sheet and maintaining

significant liquidity

• Investment grade balance sheet

• Diverse sources and access to capital

• Inflation protected revenues

• Track record of cost control

Position the business for economic growth

• Manage power and ancillary sales to benefit from market volatility

• Lock in value through long-term Power Purchase Agreements

• Build out our proprietary development pipeline at premium returns

Deploy capital into global renewable opportunities

• Leverage our established continental platforms

• Continue to focus on hydro opportunities

• Expand our track record of accretive M&A growth while taking advantage of capital scarcity

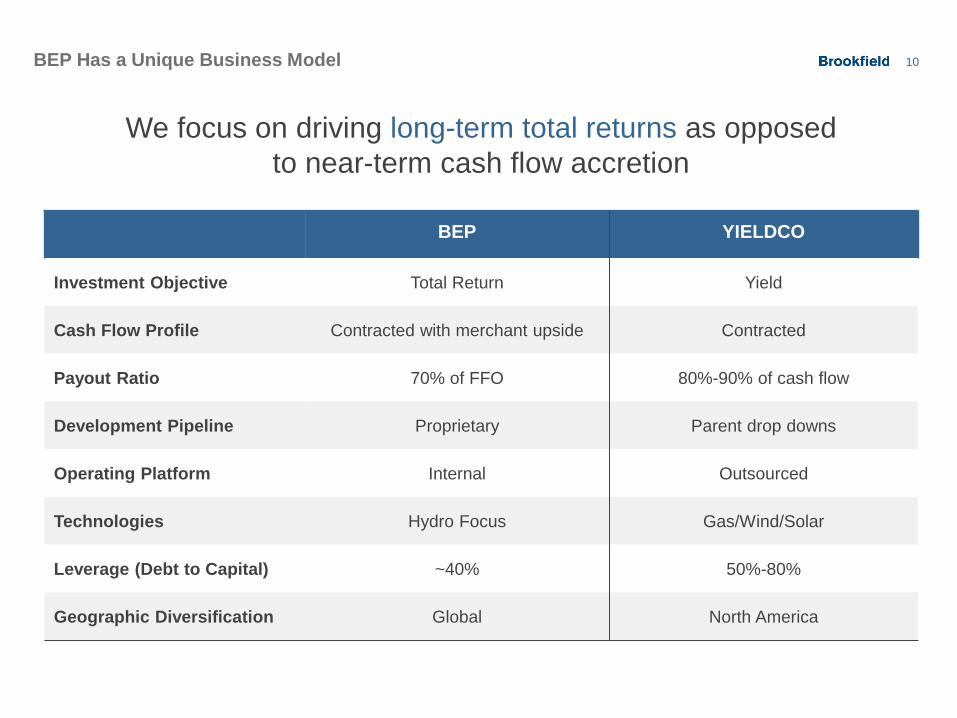

10

BEP YIELDCO

Investment Objective Total Return Yield

Cash Flow Profile Contracted with merchant upside Contracted

Payout Ratio 70% of FFO 80%-90% of cash flow

Development Pipeline Proprietary Parent drop downs

Operating Platform Internal Outsourced

Technologies Hydro Focus Gas/Wind/Solar

Leverage (Debt to Capital) ~40% 50%-80%

Geographic Diversification Global North America

BEP Has a Unique Business Model

We focus on driving long-term total returns as opposed to near-term cash flow accretion

High Falls Hydro Facility, Quebec, Canada

High Quality Assets

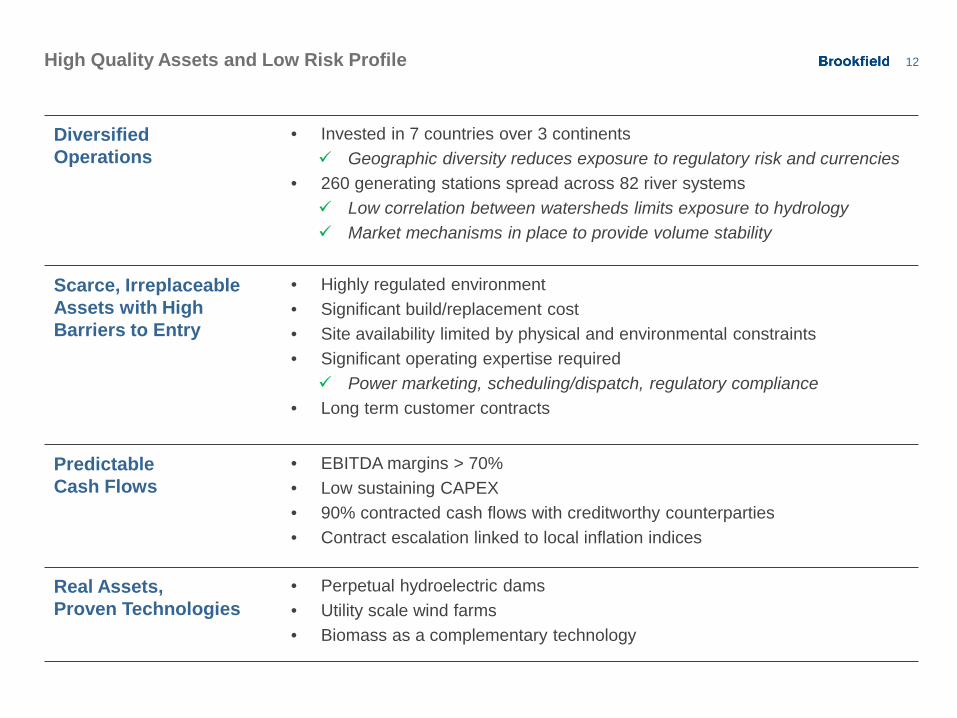

12 High Quality Assets and Low Risk Profile

Diversified Operations

• Invested in 7 countries over 3 continents Geographic diversity reduces exposure to regulatory risk and currencies

• 260 generating stations spread across 82 river systems Low correlation between watersheds limits exposure to hydrology Market mechanisms in place to provide volume stability

Scarce, Irreplaceable Assets with High Barriers to Entry

• Highly regulated environment • Significant build/replacement cost • Site availability limited by physical and environmental constraints • Significant operating expertise required Power marketing, scheduling/dispatch, regulatory compliance

• Long term customer contracts

Predictable Cash Flows

• EBITDA margins > 70% • Low sustaining CAPEX • 90% contracted cash flows with creditworthy counterparties • Contract escalation linked to local inflation indices

Real Assets, Proven Technologies

• Perpetual hydroelectric dams • Utility scale wind farms • Biomass as a complementary technology

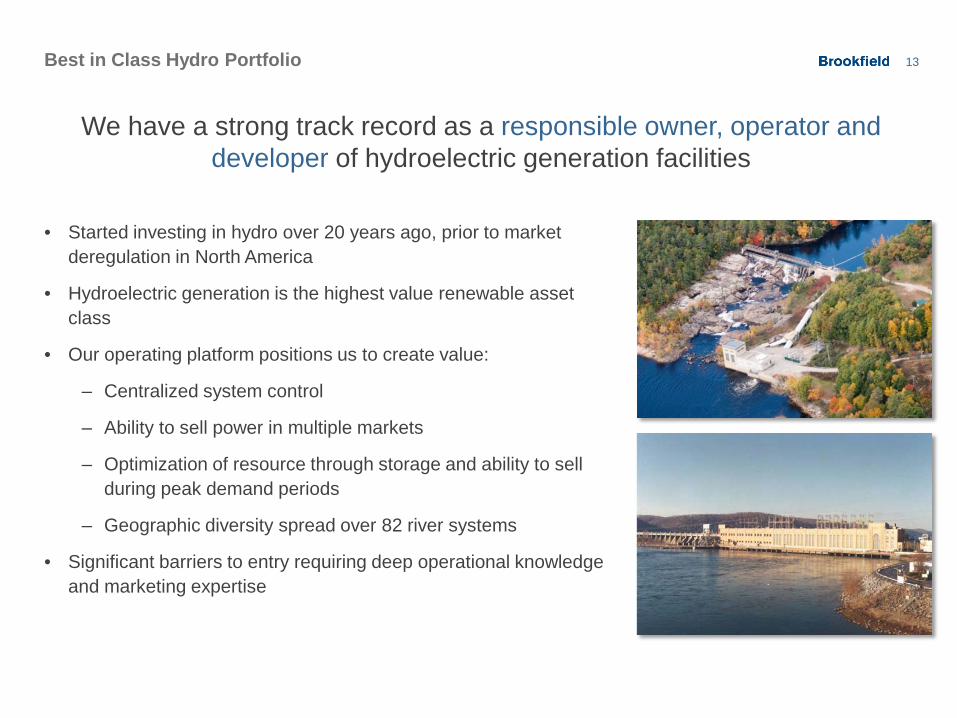

13 Best in Class Hydro Portfolio

• Started investing in hydro over 20 years ago, prior to market deregulation in North America

• Hydroelectric generation is the highest value renewable asset class

• Our operating platform positions us to create value:

‒ Centralized system control

‒ Ability to sell power in multiple markets

‒ Optimization of resource through storage and ability to sell during peak demand periods

‒ Geographic diversity spread over 82 river systems

• Significant barriers to entry requiring deep operational knowledge and marketing expertise

We have a strong track record as a responsible owner, operator and developer of hydroelectric generation facilities

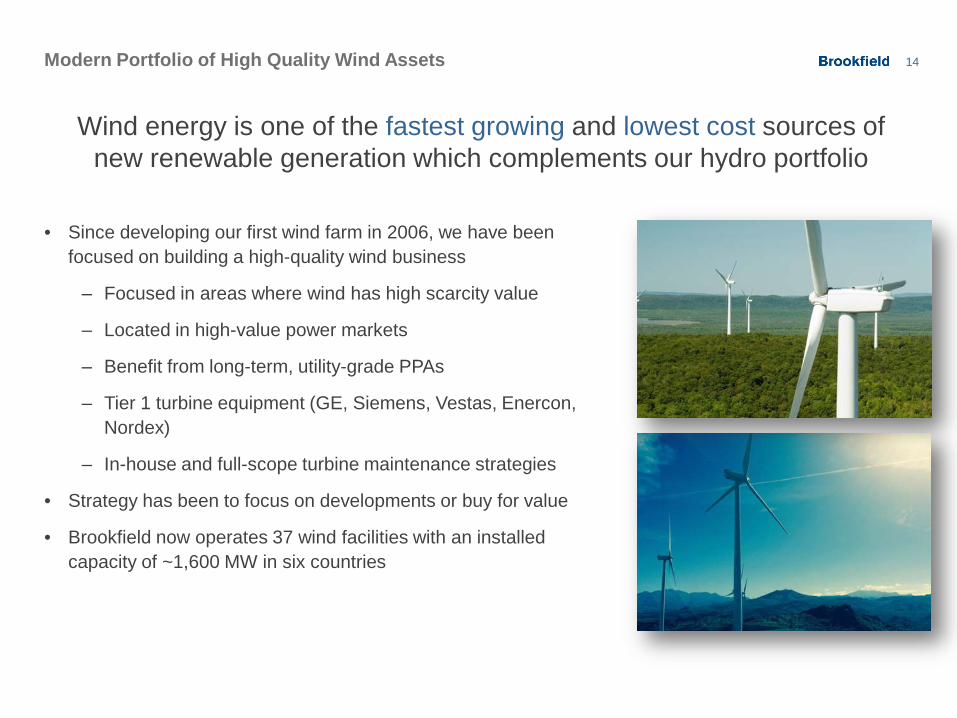

14 Modern Portfolio of High Quality Wind Assets

• Since developing our first wind farm in 2006, we have been focused on building a high-quality wind business

‒ Focused in areas where wind has high scarcity value

‒ Located in high-value power markets

‒ Benefit from long-term, utility-grade PPAs

‒ Tier 1 turbine equipment (GE, Siemens, Vestas, Enercon, Nordex)

‒ In-house and full-scope turbine maintenance strategies

• Strategy has been to focus on developments or buy for value

• Brookfield now operates 37 wind facilities with an installed capacity of ~1,600 MW in six countries

Wind energy is one of the fastest growing and lowest cost sources of new renewable generation which complements our hydro portfolio

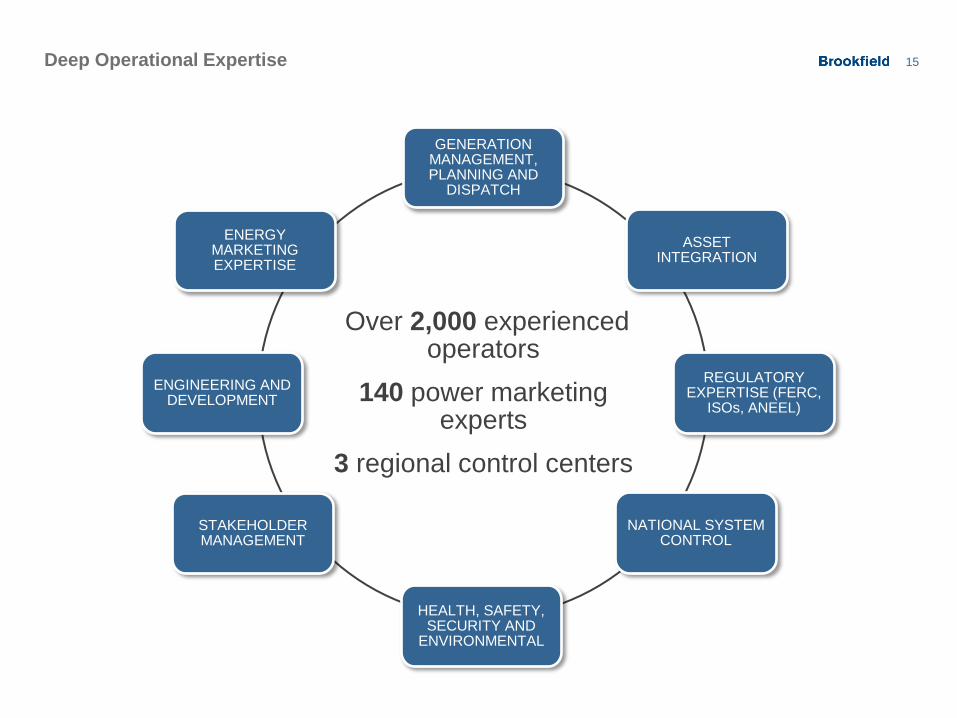

15 Deep Operational Expertise

Over 2,000 experienced operators

140 power marketing experts

3 regional control centers

GENERATION MANAGEMENT, PLANNING AND

DISPATCH

ASSET INTEGRATION

REGULATORY EXPERTISE (FERC,

ISOs, ANEEL)

NATIONAL SYSTEM CONTROL

HEALTH, SAFETY, SECURITY AND

ENVIRONMENTAL

STAKEHOLDER MANAGEMENT

ENGINEERING AND DEVELOPMENT

ENERGY MARKETING EXPERTISE

Prince Wind Farm, Ontario, Canada

Financial Profile

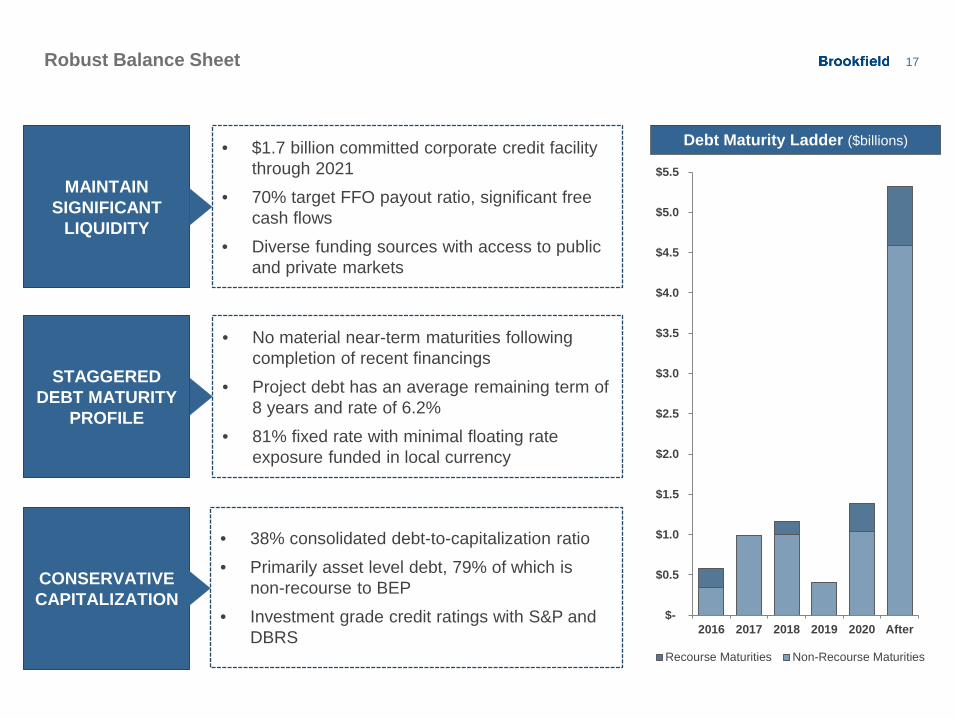

17 Robust Balance Sheet

MAINTAIN SIGNIFICANT

LIQUIDITY

• $1.7 billion committed corporate credit facility through 2021

• 70% target FFO payout ratio, significant free cash flows

• Diverse funding sources with access to public and private markets

STAGGERED DEBT MATURITY

PROFILE

• No material near-term maturities following completion of recent financings

• Project debt has an average remaining term of 8 years and rate of 6.2%

• 81% fixed rate with minimal floating rate exposure funded in local currency

CONSERVATIVE CAPITALIZATION

• 38% consolidated debt-to-capitalization ratio

• Primarily asset level debt, 79% of which is non-recourse to BEP

• Investment grade credit ratings with S&P and DBRS

Debt Maturity Ladder ($billions)

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

2016 2017 2018 2019 2020 After

Recourse Maturities Non-Recourse Maturities

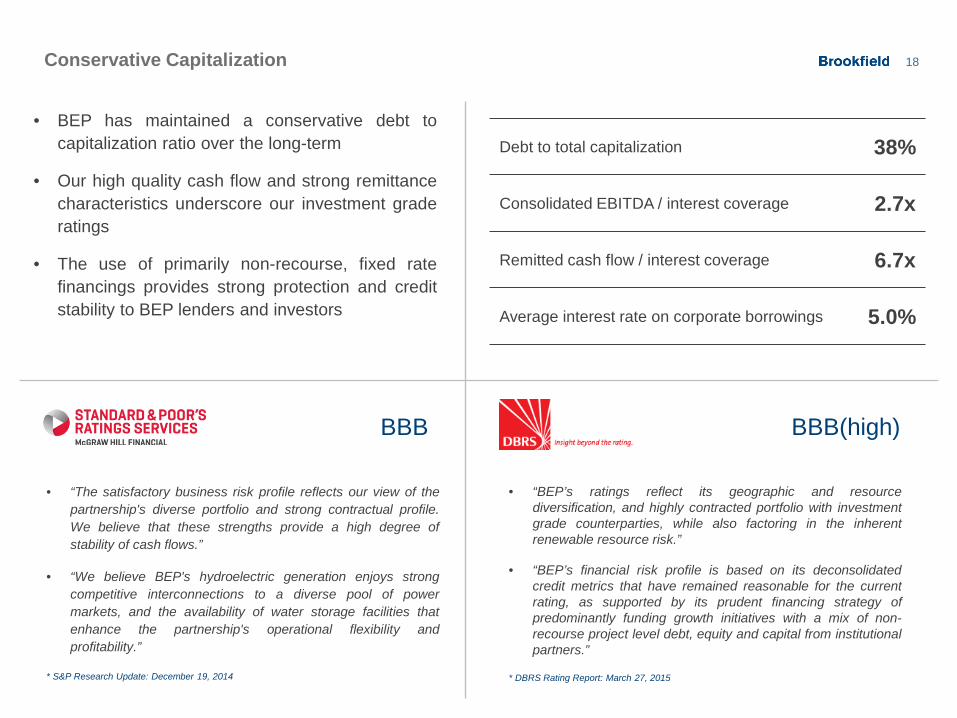

18 Conservative Capitalization

• BEP has maintained a conservative debt to capitalization ratio over the long-term

• Our high quality cash flow and strong remittance characteristics underscore our investment grade ratings

• The use of primarily non-recourse, fixed rate financings provides strong protection and credit stability to BEP lenders and investors

BBB BBB(high)

• “The satisfactory business risk profile reflects our view of the partnership's diverse portfolio and strong contractual profile. We believe that these strengths provide a high degree of stability of cash flows.”

• “We believe BEP's hydroelectric generation enjoys strong competitive interconnections to a diverse pool of power markets, and the availability of water storage facilities that enhance the partnership's operational flexibility and profitability.”

* S&P Research Update: December 19, 2014

• “BEP’s ratings reflect its geographic and resource diversification, and highly contracted portfolio with investment grade counterparties, while also factoring in the inherent renewable resource risk.”

• “BEP’s financial risk profile is based on its deconsolidated credit metrics that have remained reasonable for the current rating, as supported by its prudent financing strategy of predominantly funding growth initiatives with a mix of non-recourse project level debt, equity and capital from institutional partners.”

* DBRS Rating Report: March 27, 2015

Debt to total capitalization 38%

Consolidated EBITDA / interest coverage 2.7x

Remitted cash flow / interest coverage 6.7x

Average interest rate on corporate borrowings 5.0%

19

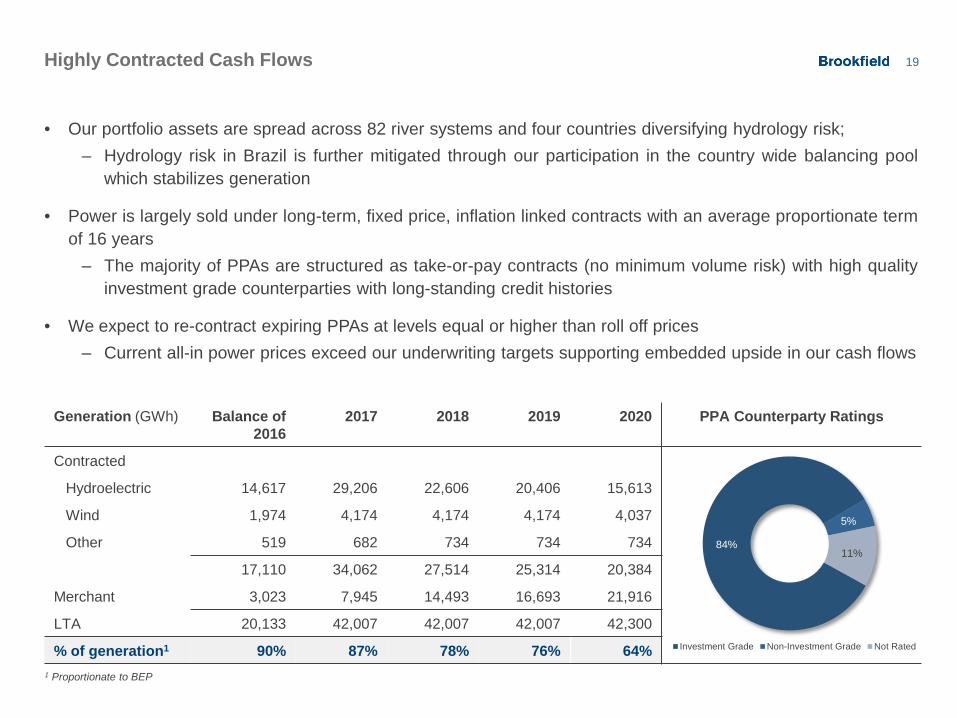

Generation (GWh) Balance of 2016

2017 2018 2019 2020 PPA Counterparty Ratings

Contracted

Hydroelectric 14,617 29,206 22,606 20,406 15,613

Wind 1,974 4,174 4,174 4,174 4,037

Other 519 682 734 734 734

17,110 34,062 27,514 25,314 20,384

Merchant 3,023 7,945 14,493 16,693 21,916

LTA 20,133 42,007 42,007 42,007 42,300

% of generation1 90% 87% 78% 76% 64%

Highly Contracted Cash Flows

• Our portfolio assets are spread across 82 river systems and four countries diversifying hydrology risk; ‒ Hydrology risk in Brazil is further mitigated through our participation in the country wide balancing pool

which stabilizes generation

• Power is largely sold under long-term, fixed price, inflation linked contracts with an average proportionate term of 16 years ‒ The majority of PPAs are structured as take-or-pay contracts (no minimum volume risk) with high quality

investment grade counterparties with long-standing credit histories

• We expect to re-contract expiring PPAs at levels equal or higher than roll off prices ‒ Current all-in power prices exceed our underwriting targets supporting embedded upside in our cash flows

84%

5%

11%

Investment Grade Non-Investment Grade Not Rated

1 Proportionate to BEP

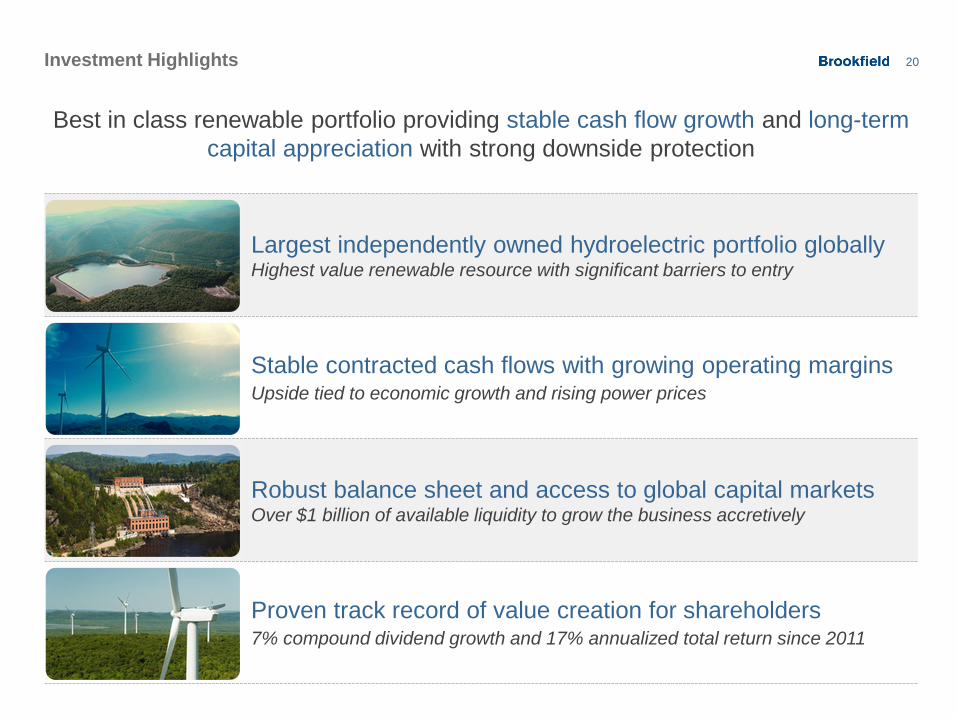

20 Investment Highlights

Best in class renewable portfolio providing stable cash flow growth and long-term capital appreciation with strong downside protection

Largest independently owned hydroelectric portfolio globally Highest value renewable resource with significant barriers to entry

Stable contracted cash flows with growing operating margins Upside tied to economic growth and rising power prices

Robust balance sheet and access to global capital markets Over $1 billion of available liquidity to grow the business accretively

Proven track record of value creation for shareholders 7% compound dividend growth and 17% annualized total return since 2011

21 Contacts

Sachin Shah Chief Executive Officer [email protected] 416.369.6008

Nick Goodman Chief Financial Officer [email protected] 416.369.2546

Zev Korman Senior Vice President, Investor and Media Relations [email protected] 416.359.1955

Rosie Mandla Manager, Investor Relations [email protected] 416.369.6010

Brookfield Tehachapi Wind Farm, California, United States

Appendix

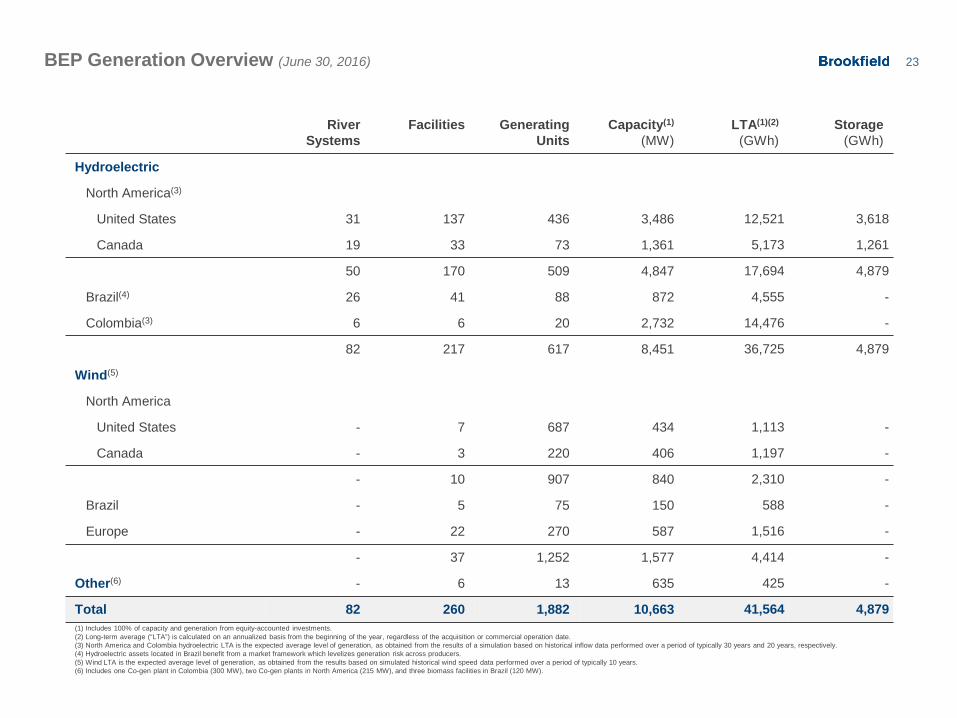

23 BEP Generation Overview (June 30, 2016)

River Systems

Facilities Generating Units

Capacity(1)

(MW) LTA(1)(2)

(GWh) Storage

(GWh)

Hydroelectric

North America(3)

United States 31 137 436 3,486 12,521 3,618

Canada 19 33 73 1,361 5,173 1,261

50 170 509 4,847 17,694 4,879

Brazil(4) 26 41 88 872 4,555 -

Colombia(3) 6 6 20 2,732 14,476 -

82 217 617 8,451 36,725 4,879

Wind(5)

North America

United States - 7 687 434 1,113 -

Canada - 3 220 406 1,197 -

- 10 907 840 2,310 -

Brazil - 5 75 150 588 -

Europe - 22 270 587 1,516 -

- 37 1,252 1,577 4,414 -

Other(6) - 6 13 635 425 -

Total 82 260 1,882 10,663 41,564 4,879 (1) Includes 100% of capacity and generation from equity-accounted investments. (2) Long-term average (“LTA”) is calculated on an annualized basis from the beginning of the year, regardless of the acquisition or commercial operation date. (3) North America and Colombia hydroelectric LTA is the expected average level of generation, as obtained from the results of a simulation based on historical inflow data performed over a period of typically 30 years and 20 years, respectively. (4) Hydroelectric assets located in Brazil benefit from a market framework which levelizes generation risk across producers. (5) Wind LTA is the expected average level of generation, as obtained from the results based on simulated historical wind speed data performed over a period of typically 10 years. (6) Includes one Co-gen plant in Colombia (300 MW), two Co-gen plants in North America (215 MW), and three biomass facilities in Brazil (120 MW).

24

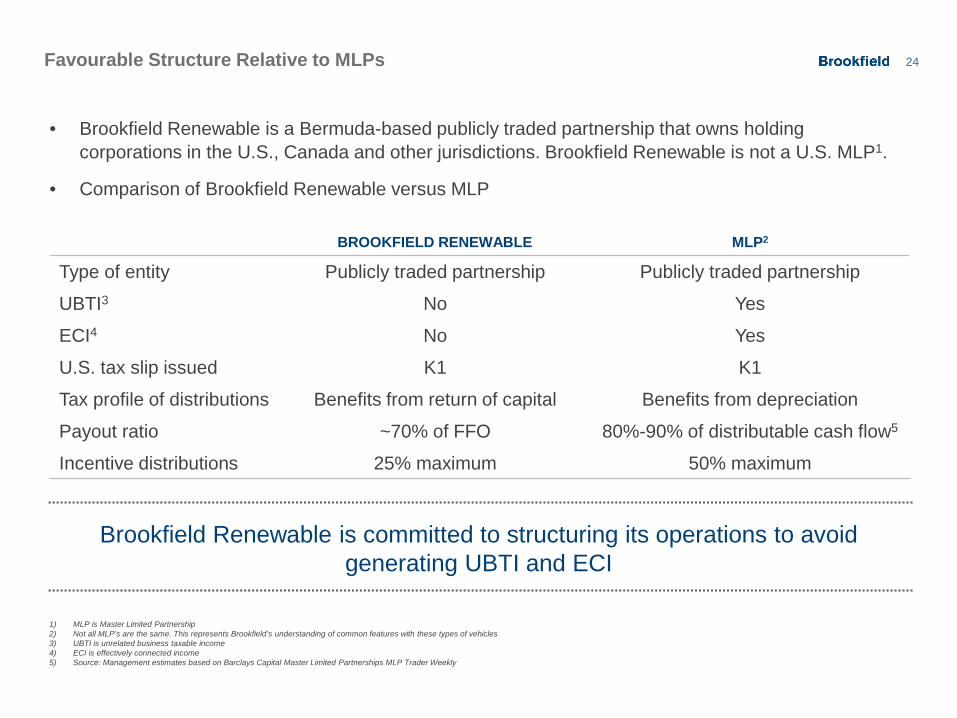

• Brookfield Renewable is a Bermuda-based publicly traded partnership that owns holding corporations in the U.S., Canada and other jurisdictions. Brookfield Renewable is not a U.S. MLP1.

• Comparison of Brookfield Renewable versus MLP

Brookfield Renewable is committed to structuring its operations to avoid generating UBTI and ECI

BROOKFIELD RENEWABLE MLP2

Type of entity Publicly traded partnership Publicly traded partnership

UBTI3 No Yes

ECI4 No Yes

U.S. tax slip issued K1 K1

Tax profile of distributions Benefits from return of capital Benefits from depreciation

Payout ratio ~70% of FFO 80%-90% of distributable cash flow5

Incentive distributions 25% maximum 50% maximum

1) MLP is Master Limited Partnership 2) Not all MLP’s are the same. This represents Brookfield’s understanding of common features with these types of vehicles 3) UBTI is unrelated business taxable income 4) ECI is effectively connected income 5) Source: Management estimates based on Barclays Capital Master Limited Partnerships MLP Trader Weekly

Favourable Structure Relative to MLPs

25 Leader in Green Energy & Sustainability

BEP is the largest member by market capitalization of the S&P/TSX Renewable Energy and Clean Technology Index.

BEP is committed to sustainable development principles that reduce the impact of our operations and help to manage the underlying water resources efficiently. Low Impact Hydropower Institute (LIHI) certification is a voluntary certification program designed to help identify and provide market incentives for hydropower operations that are minimizing their environmental impacts. BEP has received LIHI certification for 52 hydro facilities across the US, more than any other operator, making it the U.S. leader in low impact hydropower generation.

The Environmental Choice Program is a comprehensive national program sponsored by Environment Canada. It certifies manufacturers and suppliers that produce products and services that are less harmful to the environment. These bear the EcoLogo registered trademark. 22 of our hydroelectric facilities in Ontario, Quebec, and British Columbia meet the strict standards of the Environmental Choice Program.

The Brookfield Environmental Education Center was established in Guarani, Minas Gerais, Brazil, from a partnership between Brookfield Energia Renovável and the local community. The project aims to provide the entire population of the Pomba River Valley a place to develop environmental education projects. To make the project sustainable, the local community was trained to manage the Environmental Education Center and created a non-governmental organization to do it.