briefing to the portfolio committee on tourism sa tourism updated 5 year strategic plan and annual...

TRANSCRIPT

Briefing to the Portfolio Committee on Tourism

SA Tourism Updated 5 Year Strategic Plan and Annual Performance

Plan (Review 2014 /15)

04 July 2014

Slide no. 2

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Vision and Mission

Vision

For South Africa (SA) to be the preferred tourist destination in the world, in order to maximise the economic potential of tourism for our country and its people.

MissionTo develop and implement a world-class tourism marketing strategy for SA. In pursuance of this, SA Tourism will:•Implement domestic, regional and international marketing strategies informed by research•Implement a business events strategy•Implement and maintain a recognisable, credible and globally benchmarked system of quality assurance•Facilitate strategic alignment of Provinces and industry in support of global marketing of tourism.•Facilitate the removal of identified obstacles to tourism growth. •Ensure the efficient utilisation of resources to deliver the tourism strategy

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 3

Convince consumers that SA can be trusted to deliver memorable

experiences

Convince consumers that SA can be trusted to deliver memorable

experiences

Engage Stakeholders to deliver quality

visitor experience that re-affirm the

brand promise

Engage Stakeholders to deliver quality

visitor experience that re-affirm the

brand promise

Work the distribution channel to promote SA

Work the distribution channel to promote SA

Energise and empower the organisation to innovate and

achieve excellence

Energise and empower the organisation to innovate and

achieve excellence

Invest only in selected markets to deliver volume and

value

Invest only in selected markets to deliver volume and

value

SA Tourism recently refined its current objectives and strategies for the period until 2014/5 - in line with Government’s Performance Information Management Policy

Create a thriving tourism sector by making South Africa a tourism and business events destination of

choice

Create a thriving tourism sector by making South Africa a tourism and business events destination of

choice

Possible Tourism sector outcome which SA Tourism will need to deliver against

SA Tourism outcome

Strategies to deliver outcome

Make the SA brand a Global Player in portfolio markets, hubs and decision making centres which will grow tourism’s

trended revenue to the economy by 1.5% p.a. (excluding inflation)

Make the SA brand a Global Player in portfolio markets, hubs and decision making centres which will grow tourism’s

trended revenue to the economy by 1.5% p.a. (excluding inflation)

Strategic Plan & Annual Performance Plan – 04 July 2014Slide no. 4

Slide no. 5

SA Tourism’s Mandate set out in the Tourism Act makes it clear that it needs to make choices that will benefit all South Africans

Sustainable GDP Growth

Sustainable GDP Growth

Sustainable job creation

Sustainable job creation

Redistribution and

transformation

Redistribution and

transformation

The mandate to SA Tourism is ...

… through six key

objectives

…by acting in a focused way to

Increase in tourist volume

Increase in tourist volume

Increase in tourist spendIncrease in

tourist spendIncrease length

of stayIncrease length

of stay

Improve geographic

spread

Improve geographic

spread

Improve seasonality

patterns

Improve seasonality

patterns

Promote transformation

Promote transformation

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 6

SUPPORT

Business Focus

LEISURE TOURISM

“preferred tourism destination

BUSINESS EVENTS & MEETINGS

“preferred business events destination

GRADING/ QUALITY

ASSURANCE”improve quality

visitor experience”

Strategic Plan & Annual Performance Plan – 04 July 2014

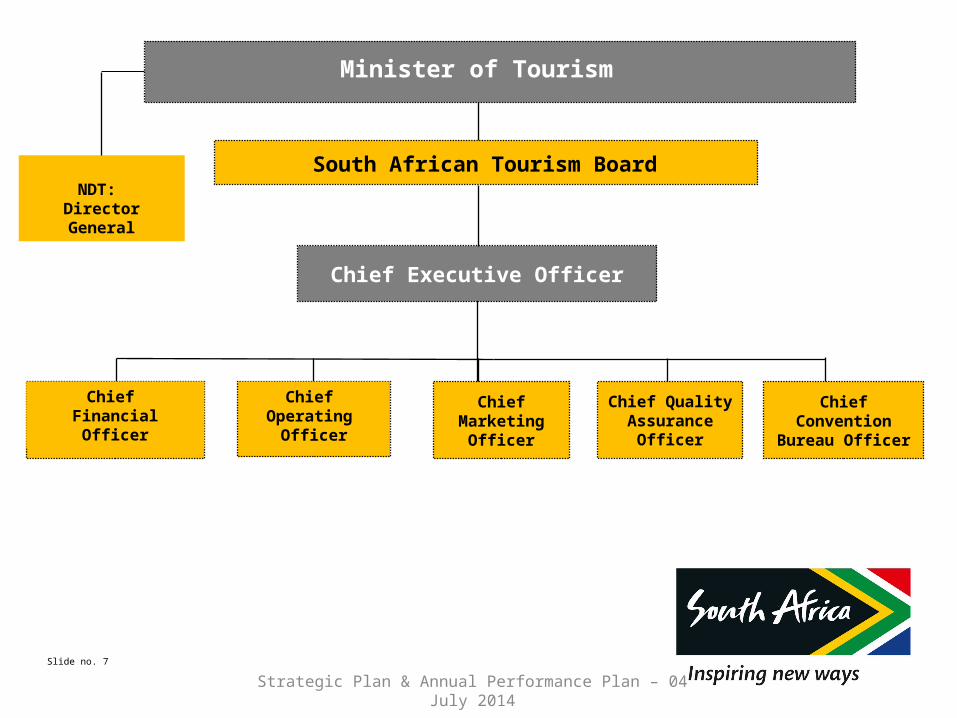

Minister of Tourism

Regional Director: Europe

Global Manager:Product

South African Tourism BoardNDT DG

Chief Executive Officer

Global Manager:Stakeholder/Global Trade

Chief FinancialOfficer

South African Tourism Board

Chief Marketing

Officer

Chief Quality Assurance

Officer

Chief Operating

Officer

QAO

Chief Convention

Bureau Officer

NDT: Director General

Slide no. 7

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 9

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 10

How attractive are these markets in the short term and the

long term?

CoreTactical

Investment and Watch-List

markets

2nd filter

Salient set

Steps of the Portfolio Review

Application of cost-benefit evaluation

1st filter

4th filter

*Africa land markets are markets where more than 60% of arrivals to SA arrive by land.

3rd filter

Final portfolio

Exclude Africa and subdivide it into 5

regions

Exclude SADC (Africa Land markets) from

the elimination process (proximity to

SA).

From the remaining countries. Excludes countries with less

than 150k outbound Travel and Population of less than 3 Million

Exclude markets population less than 3 million people OR GDP PPP of less than $11

000

Top markets in terms of outbound volume

and value

The remaining countries including SADC (Africa land

markets) qualify for Africa Salient set of

countries

199

countries

133

24

117

42

40

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 11

Key things that have changed in the 5th Portfolio Review

APPROACH:

1. We treat the African continent differently from the rest of the world Africa gets subdivided into 5 different regions / hubs Countries with outbound less than 150K per year and a population of 3 Million are

filtered out. The average outbound per annum for African countries is 500K , while population is 7 million. The aim is to include as many countries as we can hence the very low threshold.

SADC (Africa Land Markets) automatically qualify because of its proximity.

2. For the rest of the world, we no longer use the $2 000 Gross Domestic Product (GDP) filter. Instead we use GDP Purchasing Power Parity (PPP) of $11 000 per annum as a filter for affordability. This is similar to the Big Mac Index.

3. We plan to use the Hub Strategy approach around the world to increase market penetration. The Hub approach will also be applied when markets have been filtered through all the other criteria so that we can combine markets in the portfolio based on proximity, language, trade links – for instance, the US and Canada; Japan and Korea as well as Netherlands and Belgium – among others.

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 12

5th Portfolio Review Outcome to be Implemented - effective 01/04/2014 – 30/03/2017 AFRICA AMERICAS ASIA & AUSTRALASIA EUROPE & THE UK

CORE MARKETS AngolaMozambique

Nigeria

TanzaniaDomestic

BrazilUSA

AustraliaChina

India

FranceGermany

NetherlandsUK

INVESTMENT MARKETS

Botswana, DRC, Ghana, Lesotho, Uganda,

Zimbabwe

Canada Japan

South Korea

Italy

Russia

TACTICAL MARKETS

NamibiaUAE

Zambia

Singapore Switzerland

WATCH-LIST MARKETS

EthiopiaMalawi

Swaziland

Argentina New Zealand Austria Belgium

Denmark FinlandNorwaySpain

Sweden Turkey

STRATEGIC IMPORTANCE

Egypt, Israel, Morocco, Saudi Arabia, Tunisia,

Malaysia

USA

Brazil – 7/’14

China

Australia

India

France

Germany

Netherlands

UK

ItalyJapan

South Korea

Nigeria

Kenya: 05/’14

Angola: 6/’14

Existing Country Offices

Planned Country Offices

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 13

USA (Office) - Hub

Canada

India (Office) – Stand Alone

North AmericasNorth Americas

Asia & Australasia

Asia & Australasia EuropeEurope

Germany (Office): Hub

**Russia

* Brazil (Office): Hub

*** Argentina

*** Chile

Latin AmericasLatin Americas Central EuropeCentral Europe

IndiaIndia

AustralasiaAustralasia

Australia (Office) : Hub

New Zealand

AmericasAmericas

Norway

**Sweden

Denmark

Finland

United Kingdom (Office): Hub

Ireland

Scotland

Wales

United KingdomUnited

Kingdom

Benelux & ScandinaviaBenelux &

ScandinaviaNetherlands (Office) :Hub

Belgium

China - Office ** : Hub

Hong Kong

***Macau

Japan

** South Korea

Asia PacificAsia Pacific

Asia Air Link HubAsia Air Link Hub

The Hub Strategy for Global Markets to increase market penetration, footprint

and efficient resource utilisation.

Austria

France – Stand Alone

France (Office)France (Office)

Switzerland

Spain

Turkey

Malaysia

Singapore

* Kenya (Office) : Hub

**Tanzania & Uganda

*** Ethiopia

East AfricaEast Africa

AfricaAfrica

Nigeria (Office): Hub

Ghana*** ECOWAS countries

West AfricaWest Africa

* Angola (Office) – Stand Alone

DRC: Hub

Central AfricaCentral Africa

Italy – Stand Alone

Italy (Office)Italy (Office)

Botswana

Malawi

SADCSADC

Zimbabwe

Lesotho

Mozambique Zambia

Namibia

Notes: * Planned SA Tourism Offices (2013/2014 to 2014/2015)** 1 Trade Relations Manager will be appointed – approved by Board (2014/2015) (Shanghai, South Korea, Russia, Scandinavia as well as Tanzania and Uganda)*** Future Plans (2015/16 and Beyond)

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 14

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 15

MTEF Allocation to Aggressively Grow Africa

•Ring fenced budget to increase arrivals and spend from Africa to contribute to GDP and job creation.

•R50 million (2012/13) and R84 million for the MTEF period up to 2016/17

•Setting up five marketing offices in key African markets by 2020

•Implementation of regional tourism programmes

•In Africa Air markets, sizable opportunity exists to attract high value business and leisure travellers.

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 16

Regional Hub Strategy East Africa Hub Central Africa Hub West Africa Hub

Summary of

opportunity

Kenya is a relatively small market with only 36k arrivals in 2012.

Serving additional countries, such as Uganda and Tanzania from Kenya would increase arrivals to 95k – taking advantage of similar consumer profiles.

Good regional integration and growth is possible.

Angola, similarly to Kenya, will be a hub office – also servicing DRC and Congo-Brazzaville.

DRC will be serviced using a virtual office with only 1 Trade Relations Manager based in DRC but reporting to the hub office in Angola.

This approach is cost effective and most practical given the proximity and high connectivity.

The Nigerian market is large and fast growing.

Serving Ghana from Nigeria adds another 25k arrivals to the Nigerian market. Arrivals from Ghana are also growing fast.

Combined arrivals from both Ghana and Nigeria represent some 104k arrivals.

In 2013 a scoping exercise was performed to determine how to penetrate the market.

We will, continue to monitor Congo-Brazzaville and other surrounding Central African states to leverage opportunities as they arise.

Achieved milestone: The Nigerian office is fully operational.

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 17

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 18

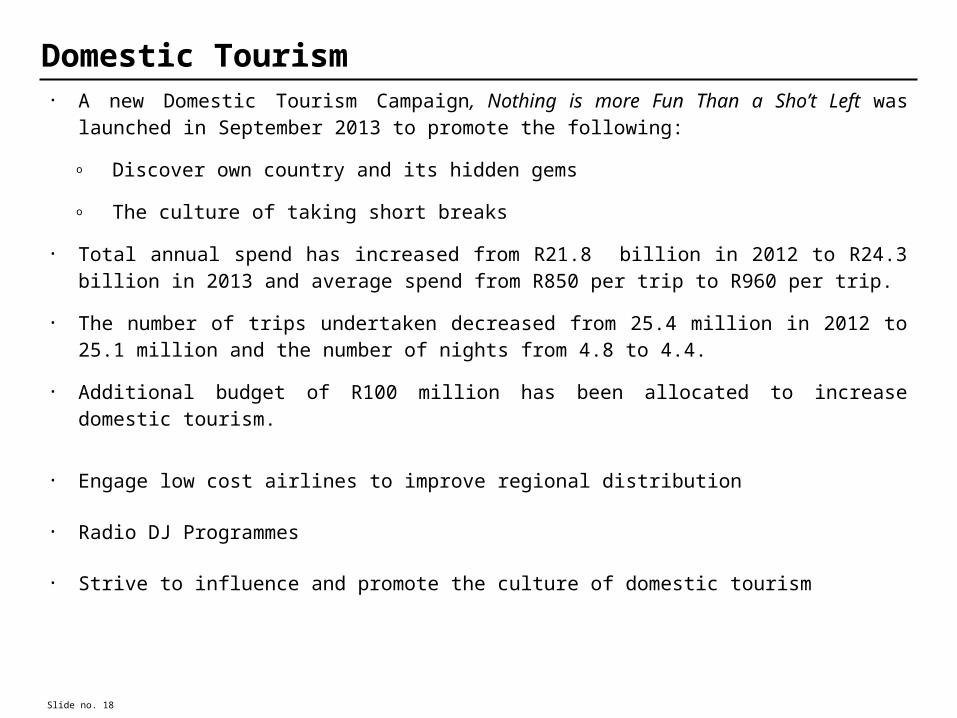

Domestic Tourism• A new Domestic Tourism Campaign, Nothing is more Fun Than a Sho’t Left was

launched in September 2013 to promote the following:

o Discover own country and its hidden gems

o The culture of taking short breaks

• Total annual spend has increased from R21.8 billion in 2012 to R24.3 billion in 2013 and average spend from R850 per trip to R960 per trip.

• The number of trips undertaken decreased from 25.4 million in 2012 to 25.1 million and the number of nights from 4.8 to 4.4.

• Additional budget of R100 million has been allocated to increase domestic tourism.

• Engage low cost airlines to improve regional distribution

• Radio DJ Programmes

• Strive to influence and promote the culture of domestic tourism

Slide no. 19

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Market Portfolio

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 20

Strategic Outcome Oriented Goals, Goal Statement and ObjectivesStrategic Objective Justification NTSS Alignment

1 Increase foreign visitor arrivals to SA

More foreign visitors will yield more tourism spend resulting to increased GDP contribution

Aligned

2 Increase domestic tourism in SA

Making SA more attractive to South Africans. This will increase tourism spend and GDP contribution

Aligned

3 Increase tourism trended revenue contribution to the economy (Total Foreign Direct Spend (TFDS) + Total Domestic Direct Spend (TDDS))

Attract tourists that will increase trended revenue contribution to GDP

Aligned

4 Increase SA brand awareness

Making SA more attractive to visitors and results in increased spend

Aligned

5 Provide quality assurance for tourism products

Marketing through word of mouth of the quality experience offered in SA

Aligned

6 Increase business events Selling SA as a “Meetings Destination” Aligned

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 21

Strategic Outcome Oriented Goals, Goal Statement and ObjectivesStrategi

c Objective

Key Perform -ance Indicator

Audited Outcome/ Actual Performance

Baseline – 2013/14 Performance

Medium Term Targets

2011 / 12

2012/13 2013/14 2014/15

Quarterly Targets

2015/16 2016/17

Increase foreign visitor arrivals to SA

# of foreign visitor arrivals(annually)

12 255 155

13 451 565

12 518 310

Tourist arrival estimate = 9 616 964

16 033 947

Tourist arrivals estimate: 10 000 228

Q1: 3 906 086 17 041 406

Tourist arrivals estimate: 10 446 753

18 049 947

Tourist arrivals estimate: 10 911 069

Q2: 3 687 842

Q3: 4 053 864

Q4: 4 386 156

# of buyers that SAT will host at Meetings Africa and Indaba during the financial year

N/A N/A Total: 376

Indaba: 207Meetings Africa: 169

Total: 427

(Indaba: 250 Meetings Africa: 177)

No quarterly targets

486 hosted buyers

(Indaba 309Meetings Africa: 177)

486 hosted buyers

(Indaba 309Meetings Africa: 177)

Increase domestic tourism in SA

# of domestic travellers

13.9m 12.5m 12.0m 12.9m Q1: 3.4m 13.5m 14.3m

Q2: 2.6m

Q3: 3.4m

Q4: 3.5m

Strategic Plan & Annual Performance Plan – 04 July 2014Slide no. 21

Slide no. 22

Strategic Outcome Oriented Goals, Goal Statement and Objectives

Strategic Objective

Key Performance Indicator

Audited Outcome/ Actual Performance

Baseline – 2013/14 Performance

Medium Term Targets

2011/12

2012/13

2013/14 2014/15 Quarterly Targets

2015/16 2016/17

Increase domestic tourism in SA

# of total domestic trips

26.3m 25.4m 25.1m 25.9m Q1: 6.9m 28.4m 31.2m

Q2: 5.0m

Q3: 6.9m

Q4: 7.1m

# of holiday trips

3.95m 2.9m 2.98m 3.07m Q1: 0.92 1m 3.3m 3.5.

Q2: 0.615m

Q3: 0.923m

Q4: 0.614m

Number of reports - seasonality

1 Report N/A 1 Report 1 Report

Increase tourism trended revenue contribution to the economy(TFDS+ TDDS)

Amount of Trended revenue

R8 600 R12 800 (NITS)R8 200 (TFDS)R105.4b (TFDS revenue)

R125.0b (Trended revenue)

R128.0b(Trended revenue)

Q1: R30.7b R129.7b(Trended revenue)

R133.6b (Trended revenue)

Q2: R29.4 b

Q3: R33.3b

Q4: R34.6b

Strategic Plan & Annual Performance Plan – 04 July 2014Slide no. 22

Slide no. 23

Strategic Outcome Oriented Goals, Goal Statement and Objectives

Increase SA brand awareness

Brand Awareness

77% 81% 79% 80% N/A 80% 81%

Provide quality assurance for tourism products

# of graded establishment

4 886 6 022 5 671 7 088(1 195 New 5 893 renewals)

Q1: 1 772 7 584 8 115

Q2: 1 772

Q3: 1 772

Q4: 1 772

Increase business events

# of delegates

N/A 52 587delegates

94 893 delegates

58 500 delegates

N/A 61 500 delegates at international conventions

65 000 delegates at international conventions

Strategic Objective

Key Performance Indicator

Audited Outcome/ Actual Performance

Baseline – 2013/14 Performance

Medium Term Targets

2011/12

2012/13

2013/14 2014/15 Quarterly Targets

2015/16 2016/17

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 24

Tourism’s GDP contribution increased from 2.8% (2011) to 3.0% (2012)

Tourism Contribution to GDP, 2008-2012*Tourism Contribution to GDP, 2008-2012*

Source: TSA, Statistics SA – Preliminary figures are used for 2011 and 2012

Tota

l D

irect

GD

P (

Billion

s)

67.1 69.376.6

83.593.3

3.0% 2.9% 2.9% 2.8% 3.0%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2008 2009 2010 2011 2012

Tourism direct GDP

Tourism share of SA GDP

To

urism

Sh

are of D

irect G

DP

CAGR (2008-2012)

Total Contribution to GDP 6.8%

Strategic Plan & Annual Performance Plan – 04 July 2014

Tourist arrivals to South Africa grew by almost 5% in 2013 in line with global growth

Note: UNWTO estimates incorporate provisional data for some regions

Source: Statssa Tourism & Migration release December 2013, SAT analysis; UNWTO World Tourism Barometer, Volume 12, April 2014 – Statistical Annex

4.7%5.4%

6.2%5.4%

-0.2%

3.2%

5.0%

-5%

0%

5%

10%

South Africa Africa Asia and thePacific

Europe Middle East Americas World

Year-on-Year Change in Tourist Arrivals to each region%

Change

2012 Tourist arrivals (Millions)

9.2 52.9 233.5 534.4 51.7 162.7 1,035

2013 Tourist arrivals (Millions)

9.6 55.8 248.1 563.4 51.6 167.9 1,087

Slide no. 25Strategic Plan & Annual Performance Plan – 04 July 2014

AFRICAAFRICAAFRICAAFRICA

11, 585,206 arrivals 12.4% up from 2012

11, 585,206 arrivals 12.4% up from 2012

Central & South AmericaCentral & South America

133, 959 arrivals 6.40% up from 2012

133, 959 arrivals 6.40% up from 2012

North AmericaNorth AmericaNorth AmericaNorth America

467, 956 arrivals 6.1% up from 2012

467, 956 arrivals 6.1% up from 2012

EuropeEuropeEuropeEurope

1,628,154 arrivals 6.7% up from 2012

1,628,154 arrivals 6.7% up from 2012

AsiaAsiaAsiaAsia

480, 064 arrivals 9.6% up from 2012

480, 064 arrivals 9.6% up from 2012

Australasia

162, 356 arrivals 2.3% up from 2012

162, 356 arrivals 2.3% up from 2012

Middle EastMiddle East

61, 994 arrivals 6.4% up from 2012

61, 994 arrivals 6.4% up from 2012

Indian Ocean IslandsIndian Ocean Islands

27, 486 arrivals 13.4% up from 2012

27, 486 arrivals 13.4% up from 2012Note : Tourist Arrivals figures shown above for Jan. - Dec 2013

Source: Statssa Tourism & Migration release December 2013, SAT analysis

14, 806, 216 arrivals 10.5% up from 2012

14, 806, 216 arrivals 10.5% up from 2012

GRAND TOTALGRAND TOTAL

Foreign arrivals to South Africa for January to December 2013 grew by 10.5% over 2012 to reach 14.8 million

Slide no. 26

Strategic Plan & Annual Performance Plan – 04 July 2014

AFRICAAFRICAAFRICAAFRICA

6,889,389 arrivals 3.8% up from 2012

6,889,389 arrivals 3.8% up from 2012

Central & South AmericaCentral & South America

129,463 arrivals 8.0% up from 2012

129,463 arrivals 8.0% up from 2012

North AmericaNorth AmericaNorth AmericaNorth America

417,582 arrivals 6.1% up from 2012

417,582 arrivals 6.1% up from 2012

EuropeEuropeEuropeEurope

1,494,978 arrivals 7.0% up from 2012

1,494,978 arrivals 7.0% up from 2012

AsiaAsiaAsiaAsia

435,076 arrivals 9.2% up from 2012

435,076 arrivals 9.2% up from 2012

Australasia

148,660 arrivals 4.0% up from 2012

148,660 arrivals 4.0% up from 2012

Middle EastMiddle East

57,382 arrivals 5.9% up from 2012

57,382 arrivals 5.9% up from 2012

Indian Ocean IslandsIndian Ocean Islands

24,394 arrivals 13.3% up from 2012

24,394 arrivals 13.3% up from 2012Note : Tourist Arrivals figures shown above for Jan. - Dec 2013

Source: Statssa Tourism & Migration release December 2013, SAT analysis

9,616,964 arrivals 4.7% up from 2012

9,616,964 arrivals 4.7% up from 2012

GRAND TOTALGRAND TOTAL

Tourist arrivals to South Africa in 2013 grew by 4.7% over 2012 to reach 9,616,964. All regions showed positive growth in tourist arrivals in this period

Slide no. 27Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 28

AFRICAAFRICAAFRICAAFRICA

1,736,166 arrivals 7.6% up from 2012

1,736,166 arrivals 7.6% up from 2012

Central & South AmericaCentral & South America

35,535 arrivals 15.2% up from 2012

35,535 arrivals 15.2% up from 2012

North AmericaNorth AmericaNorth AmericaNorth America

92,727 arrivals 5.2% up from 2012

92,727 arrivals 5.2% up from 2012

EuropeEuropeEuropeEurope

430,910 arrivals 9.2% up from 2012

430,910 arrivals 9.2% up from 2012

Asia & AustralasiaAsia & AustralasiaAsia & AustralasiaAsia & Australasia

108,272 arrivals 27.1% up from 2012

108,272 arrivals 27.1% up from 2012

Europe remains the main source of tourist arrivals to South Africa while Asia remains buoyant with the highest growth.

Asia

“GROW”

North America

“GROW”

Africa Air

“GROW”

Europe

“RETAIN & DEFEND”

Africa Land

“GROW”

Brazil

“GROW”

AustralasiaAustralasia

Australia

“RETAIN & DEFEND

Strategic Plan & Annual Performance Plan – 04 July 2014

Tourist Arrivals to South Africa and the World, 2011 to 2013Tourist Arrivals to South Africa and the World, 2011 to 2013Tourist Arrivals to South Africa and the World, 2011 to 2013Tourist Arrivals to South Africa and the World, 2011 to 2013

Long-haul Markets

Africa Air Markets

Africa Land Markets

All Markets Global Arrivals

All markets grew faster than global growth rate between 2011 and 2013

Note: Africa Air Markets are markets where at least 60% arrives to SA use air transport; Africa Land Markets are markets where at least 60% of arrivals to SA use road transport. Long-haul markets include all countries outside of AfricaSource: Statssa Tourism & Migration release December 2013, SAT analysis; UNWTO World Tourism Barometer, Volume 12, April 2014 – Statistical Annex

Tou

rist

Arr

ivals

(M

illio

ns)

5.7%

11%

7.4%

13.1%

1000 4.5%

12% 3.4% 6.8% 4.7% 5%14.2% 8.2% 15%

10.2% 4.0%% change y-o-y

CAGR 11 to 13

Slide no. 29

Number of Graded Establishments as at end March 2014

Non-Hotel Accommodation EC FS GP KZN LP MP NW NC WC

Grand Total

Backpacker & Hostelling 12 2 9 9 2 2 1 1 38 76

Bed & Breakfast 182 14 177 232 22 33 18 34 310 1 022

Caravan & Camping 16 7 1 11 14 10 10 4 24 97

Country House 32 7 29 15 9 10 4 2 69 177

Guest House 233 54 431 146 54 112 71 71 587 1 759

Lodge 49 9 43 58 83 55 13 34 32 376

Self Catering 112 33 80 181 79 63 27 28 735 1 338Non-Hotel Accommodation Total 636 126 770 652 263 285 144 174 1 795 4 845

Hotel Total 54 27 180 108 28 34 21 24 187 663

Accommodation Grand Total 690 153 950 760 291 319 165 198 1 982 5 508

MESE Total (Business Tourism) 7 11 72 4 15 18 5 13 18 163

Grand Total Graded Properties 697 164 1 022 764 306 337 170 211 2 000 5 671

Slide no. 30

Number of Graded Rooms as at end March 2014

Non-Hotel Accommodation EC FS GP KZN LP MP NW NC WC

Grand Total

Backpacker & Hostelling 556 132 798 723 87 49 200 32 1 278 3 855

Bed & Breakfast 1 575 105 1 117 1 516 258 270 119 340 1 624 6 924

Caravan & Camping 655 406 50 1 025 1 368 1 112 217 660 1 534 7 027

Country House 321 81 345 170 153 103 29 25 771 1 998

Guest House 2 536 619 4 395 1 540 785 1 327 667 907 4 481 17 257

Lodge 497 263 1 248 986 1 587 1 129 156 804 445 7 115

Self Catering 985 356 792 1 563 1 699 1 452 179 863 4 083 11 972

Non-Hotel Accommodation Total 7 125 1 962 8 745 7 523 5 937 5 442 1 567 3 631 14 216 56 148

Hotel Total 3 780 1 697 20 242 8 200 1 597 2 268 957 2 827 14 460 56 028Accommodation Grand Total 10 905 3 659 28 987 15 723 7 534 7 710 2 524 6 458 28 676 112 176

MESE Total (Business Tourism) 38 30 531 26 63 67 19 48 76 898

Grand Total Graded Properties 10 943 3 689 29 518 15 749 7 597 7 777 2 543 6 506 28 752 113 074

Slide no. 31

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 32

SA National Convention Bureau Update and Performance (2013-2014) 01 APRIL 2012: Establishment of SANCB

YEAR 1 OBJECTIVES: Fully operational business unit

SANCB FOCUS: Positioning and selling South Africa as a preferred business events destination and growing the industry’s capacity and skills.

STRATEGY: Approval of the SANCB’s 5 year strategy

COORDINATING FORUM: Guidelines for coordination of SANCB and all Provincial and City Convention Bureaus activities.

ICCA GLOBAL RANKING 2013: SA ranked 34th internationally, 1st in Africa, 11th long haul, 27th based on the number of participants

MEETINGS AFRICA: True Pan African Show celebrating 10 years in 2015 and boasting 13 African countries represented, 262 exhibitors, 170 Int, 37 association, 500 corporate buyers, 163 media

SUBVENTION: Incentive programme aimed at attracting international business events to South Africa. Subvention guidelines approved by SATB.

BIDS SUBMITTED 2013-2014 FINANCIAL YEAR

Note: R5.1 million was spent on 57 Bids = ROI: R948 million

TOTAL BIDS TOTAL NUMBER OF DAYS

ESTIMATED DELEGATE NUMBERS

ESTIMATED ECONOMIC IMPACT

57 180 76 843 R948 186 400

BIDS SECURED FOR SA: 2014 - 2018

TOTAL BIDS SECURED

TOTAL NUMBER OF DAYS

ESTIMATED DELEGATE NUMBERS

ESTIMATED ECONOMIC IMPACT

150 689 243 468 R3 222 870 000.00

Slide no. 32Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 33

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 34

Revenue and Expenditure Estimates Revenue

2010/11

2011/12

2012/13

2013/14 2013/14 2014/15

2015/16

2016/17

ENE Estimate

Adjustment

Approved

Rand Thousand

Audited Audited AuditedPre-Audited

Budget Budget Budget Budget Budget Estimate*

1Government grant

631 685

668 613

754 953

846 333

829 973 36 360 866 333876 309

974 0121 024 847

2TOMSA levies

104 973

98 169111 970

131 289

87 472 87 472 82 000 86 428 91 009

3Indaba & Meetings Africa

38 803 37 868 50 013 59 438 42 463 42 463 48 694 51 323 54 044

4Grading fees (note 1)

6 376 5 284 3 252 1 520 14 236 14 236 14 668 15 460 16 279

5Sundry revenue

52 567 19 045 50 318 57 610 18 168 18 168 20 567 36 531 38 466

Total834 404

828 979

970 506

1.096 m

992 312 36 360 1.028 m1.043 m

1.164 m 1.224 m

Note 1: Only the net grading revenue after the deduction of assessor fees were disclosed in the audited Annual Financial Statements for 2010/11, 2011/12 and 2012/13 respectively. Net grading fees for 2013/14 was R 1 520 250 after deducting assessor fees of R 10 393 618.

Strategic Plan & Annual Performance Plan – 04 July 2014Slide no. 34

Slide no. 35

Revenue and Expenditure Estimates per KPIName of the Objective

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

ENE Estimate

AdjustmentApproved

in Rand Audited Audited Audited Budget Budget Budget

Major Objectives

856 089 863 295 979 646 992 312 - 992 312 1 042 238 1 163 755 1 224 645

Administration 88 292 143 054 105 465 86 663 10 000 96 663 111 160 117 163 123 372

1

Increase annual foreign visitor arrivals to South Africa

227 535 223 734 268 375 291 519 - 291 519 290 462 291 509 310 334

2

Increase the number of Domestic Travellers

39 694 23 452 45 113 35 038 26 360 61 398 43 672 143 800 144 000

3

Increase tourism trended revenue contribution to the economy

227 535 223 734 268 375 291 519 291 519 290 462 291 509 310 334

4

Marketing South Africa to become the preferred Tourism Brand*

238 465 224 258 245 850 206 828 206 828 220 292 232 187 244 493

5

To provide quality assurance by having graded accommodation establishments

34 568 25 061 3 252 37 114 37 114 40 377 39 300 41 265

6

To increase the number of international Business Events delegates in South Africa

43 216 43 631 43 631 45 813 48 287 50 846

Total 856 089 863 293 979 646 992 312 36 3601 028 672

1 042 238 1 163 755 1 224 645

Slide no. 35 Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 36

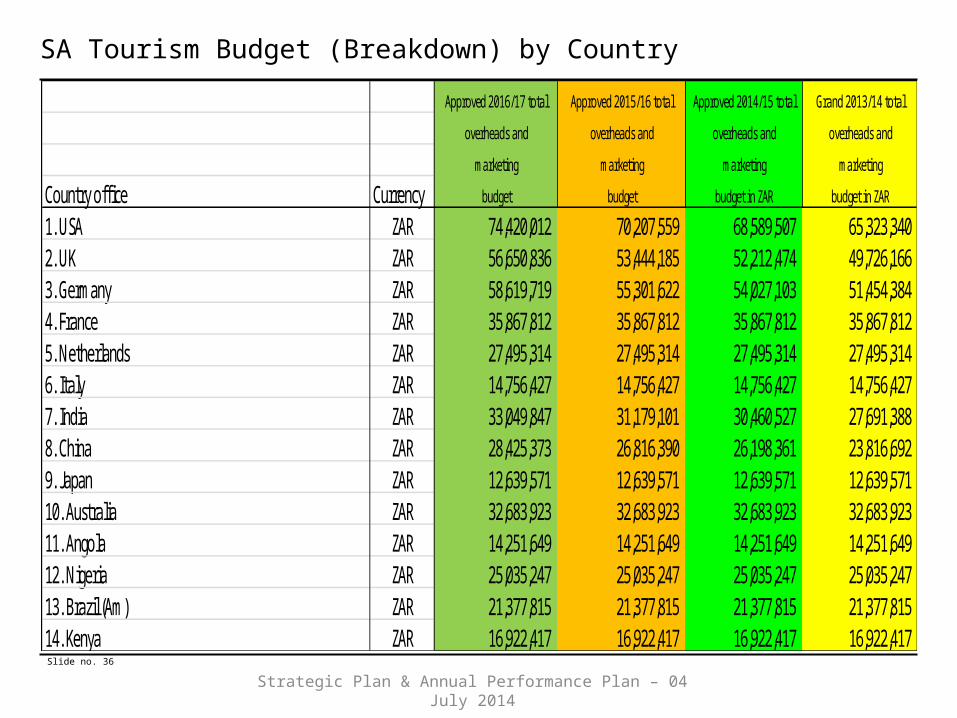

SA Tourism Budget (Breakdown) by Country

Strategic Plan & Annual Performance Plan – 04 July 2014

Approved 2016/17 total Approved 2015/16 total Approved 2014/15 total Grand 2013/14 total

overheads and overheads and overheads and overheads and

marketing marketing marketing marketing

Country office Currency budget budget budget in ZAR budget in ZAR

1. USA ZAR 74,420,012 70,207,559 68,589,507 65,323,340 2. UK ZAR 56,650,836 53,444,185 52,212,474 49,726,166 3. Germany ZAR 58,619,719 55,301,622 54,027,103 51,454,384 4. France ZAR 35,867,812 35,867,812 35,867,812 35,867,812 5. Netherlands ZAR 27,495,314 27,495,314 27,495,314 27,495,314 6. Italy ZAR 14,756,427 14,756,427 14,756,427 14,756,427 7. India ZAR 33,049,847 31,179,101 30,460,527 27,691,388 8. China ZAR 28,425,373 26,816,390 26,198,361 23,816,692 9. Japan ZAR 12,639,571 12,639,571 12,639,571 12,639,571 10. Australia ZAR 32,683,923 32,683,923 32,683,923 32,683,923 11. Angola ZAR 14,251,649 14,251,649 14,251,649 14,251,649 12. Nigeria ZAR 25,035,247 25,035,247 25,035,247 25,035,247 13. Brazil (Am) ZAR 21,377,815 21,377,815 21,377,815 21,377,815 14. Kenya ZAR 16,922,417 16,922,417 16,922,417 16,922,417

Slide no. 37

Other Resource Considerations

• Current staff complement of 206 is not expected to change in the 2014/15 financial year.

• Estimated Capital Expenditure (CAPEX) of R9.82m (2014/15) in respect of Head Quarters (HQ) office extension for Phase 1 and 2 respectively.

• Estimated R8.01m (2014/15) for software, hardware, vehicles and lease improvements.

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 38

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 39

Concluding Remarks

• Fragile economic recovery and expected economic recession

• Promising outbound tourism growth but short –haul travel

• Shrinking disposable income due to austerity measures

• Exchange currency weakness

• Growing middle class in Africa

• Unemployment dampening domestic tourism

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 40

Contents

• Vision, Mission and Mandate and Governance

• Strategic Approach and Performance

• Africa Growth Strategy

• Domestic Tourism Strategy

• Strategic Objective Annual Targets, Performance

• Breakdown of Tourism Budget

• Concluding Remarks

• Global Audio Visual – “Reconsider South Africa”

Strategic Plan & Annual Performance Plan – 04 July 2014

Slide no. 41

Reconsider South Africa (New South African Tourism brand video)

Strategic Plan & Annual Performance Plan – 04 July 2014

Thank You

Slide no. 42

Strategic Plan & Annual Performance Plan – 04 July 2014